feeding the fish of the future 9th november 2010

TRANSCRIPT

Marine Conservation Society

Feeding the fish of the future

9th November 2010

Paddy Campbell

BioMar Ltd.

Introduction

• Raw material used in last 10 years

– Fishmeal and protein sources

– Fish oil and vegetable oils

• Current raw material use and comparison of Scotland to Norway, Chile and Canada

• Comparisons to other non Salmonid species reference: Tilapia

(Note: Based mainly on BioMar’s view and industry figures)

Raw materials

• Key area for all feed

manufacturers why?

• Feed cost and flexibility

• Feed performance

• Processing / factory

performance

• Traceability and feed

safety

• Sustainability

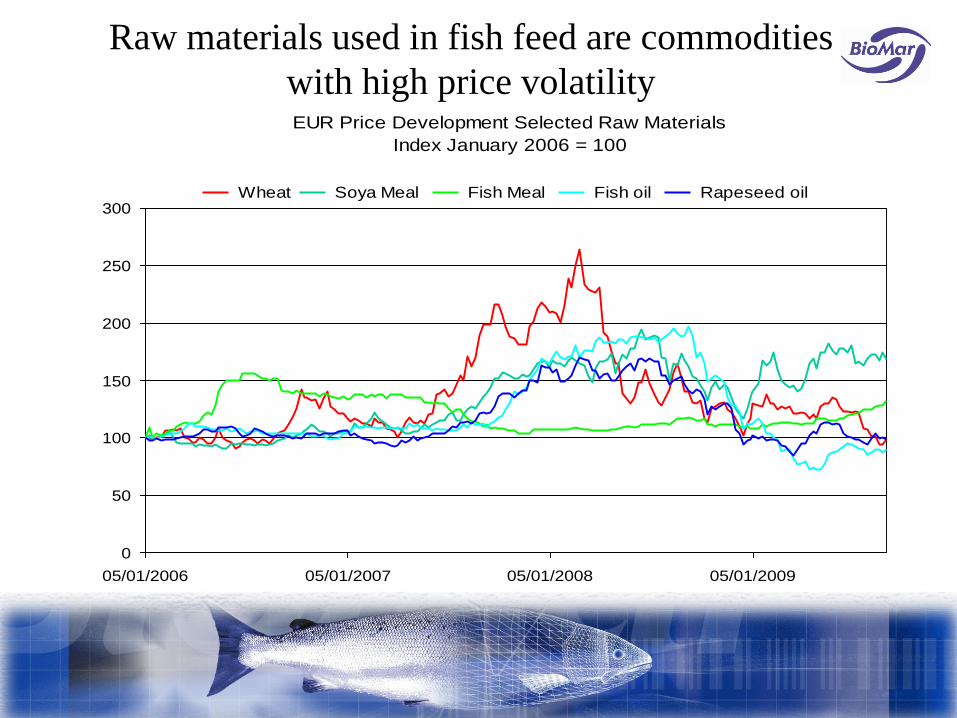

Raw materials used in fish feed are commodities

with high price volatilityEUR Price Development Selected Raw Materials

Index January 2006 = 100

0

50

100

150

200

250

300

05/01/2006 05/01/2007 05/01/2008 05/01/2009

Wheat Soya Meal Fish Meal Fish oil Rapeseed oil

Fishmeal and alternative protein

sources

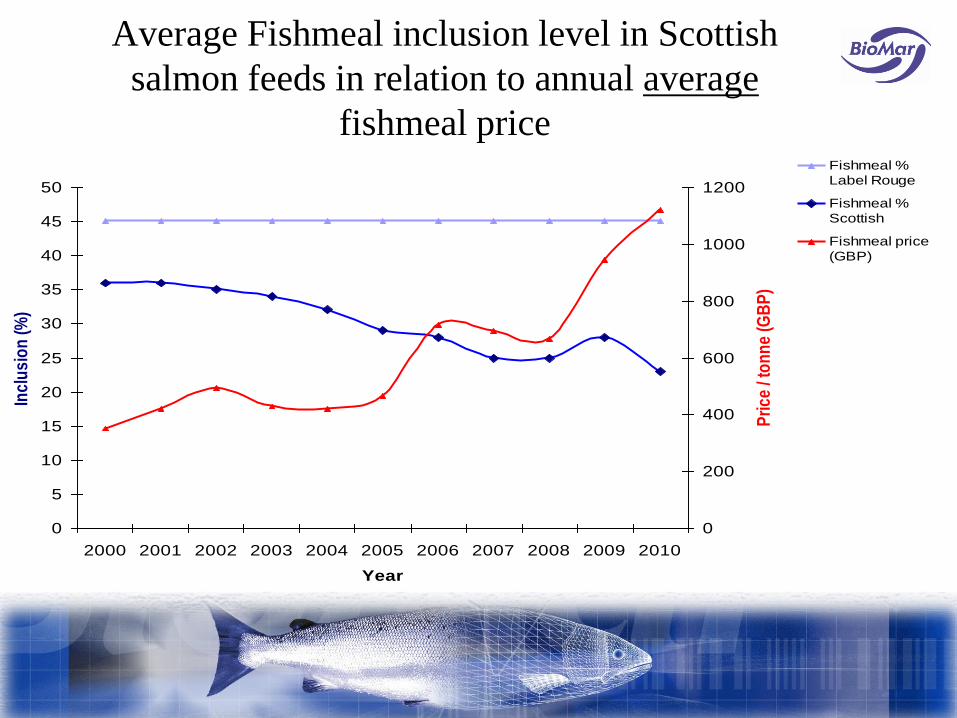

Average Fishmeal inclusion level in Scottish

salmon feeds in relation to annual average

fishmeal price

0

5

10

15

20

25

30

35

40

45

50

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Year

Incl

usi

on

(%

)

0

200

400

600

800

1000

1200

Pri

ce /

ton

ne

(GB

P)

Fishmeal %

Label Rouge

Fishmeal %

Scottish

Fishmeal price

(GBP)

Use of fishmeal and it’s vegetable protein

replacers over time in Scottish salmon feeds

0

5

10

15

20

25

30

35

40

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Year

% in

clus

ion

Fishmeal

Oilseed meals

Refined vegetableproteins

fishmeal Sunflower cakeHi Pro Soya Soy protein conc. Corn gluten

Fishmeal and alternative proteins

• Apart from Label Rouge feeds, fishmeal levels in Scottish Salmon

feeds has reduced from approx 36% to 23% over the last 10 years

• Replacement generally associated with:

– Increasing fishmeal price

– Change in price ratio of fishmeal to vegetable proteins (soya)

– Knowledge base of feed manufacturers

– Market acceptance

• With decreasing fishmeals the level of refined vegetable proteins has

increased (SPC) and oils seed meals like Hi Pro soya and sunflower

meal have decreased

• Fishmeal levels can come down further if need be (nutritional ‘task’

not needed for other reasons (human health benefits)

Fish oil, vegetable oils and EPA and

DHA|

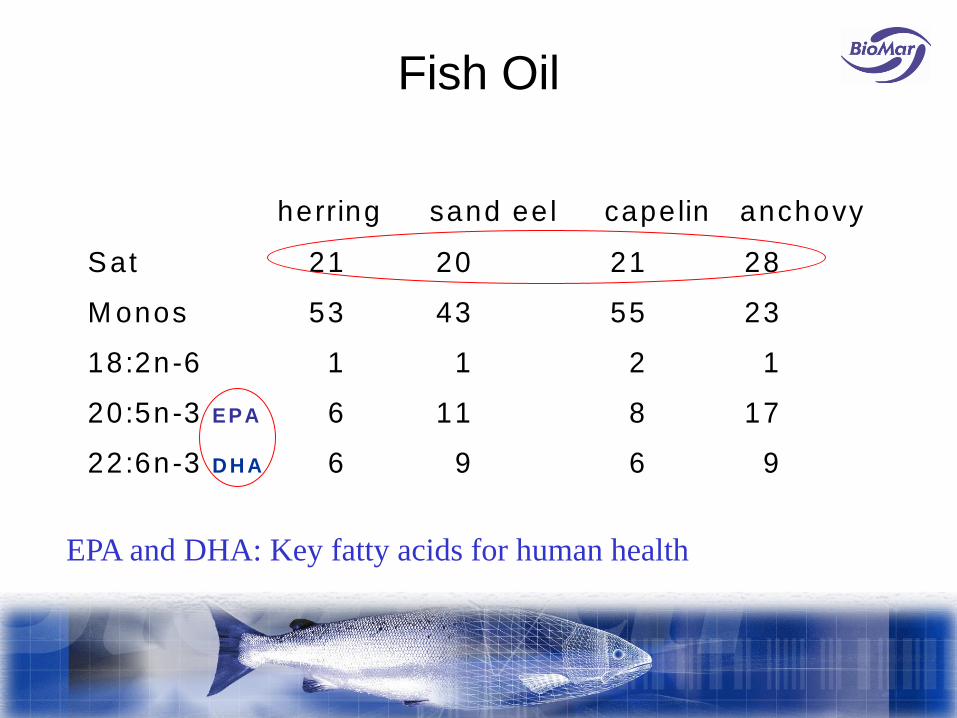

Fish Oil

herring sand ee l capelin anchovy

Sat 21 20 21 28

M onos 53 43 55 23

18:2n-6 1 1 2 1

20:5n-3 EPA 6 11 8 17

22:6n-3 D H A 6 9 6 9

EPA and DHA: Key fatty acids for human health

Vegetable Oil choice

soya rape palm olive linseed

16:0 11 4 44 10 7

18:1 22 56 39 78 15

18:2n-6 53 26 11 7 18

18:3n-3 8 10 1 1 56

20:5n-3 EPA 0 0 0 0 0

22:6n-3 D H A 0 0 0 0 0

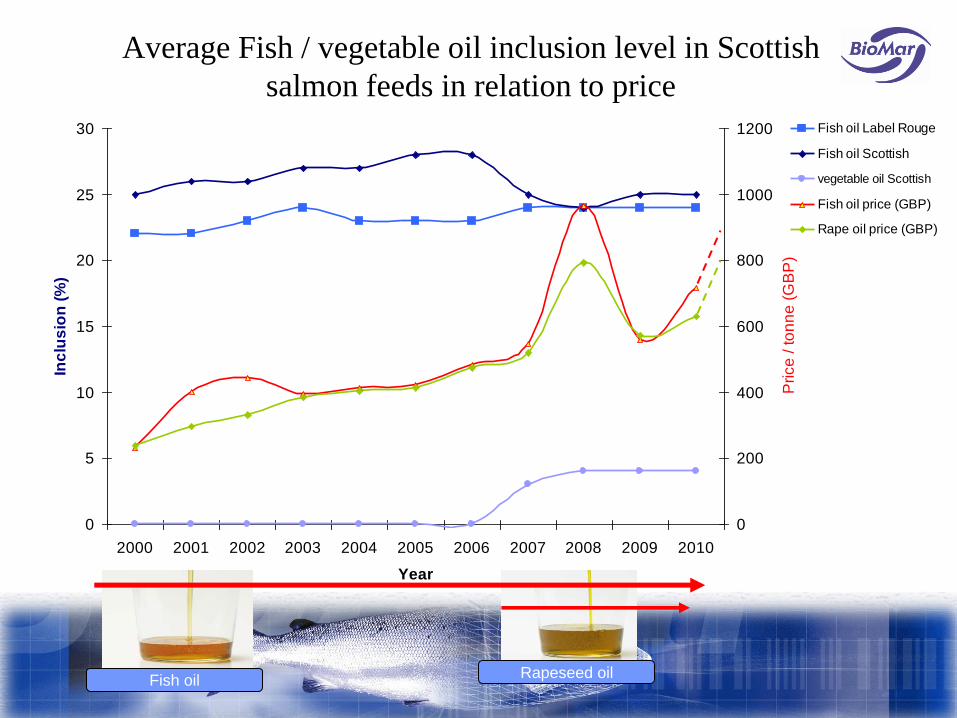

Average Fish / vegetable oil inclusion level in Scottish

salmon feeds in relation to price

0

5

10

15

20

25

30

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Year

Inc

lus

ion

(%

)

0

200

400

600

800

1000

1200

Price

/ to

nn

e (

GB

P)

Fish oil Label Rouge

Fish oil Scottish

vegetable oil Scottish

Fish oil price (GBP)

Rape oil price (GBP)

Fish oilRapeseed oil

What does our use of fish oil and vegetable oil mean

in regard to EPA and DHA levels in flesh?

• Assume a use of both NH and SA fish oils with the

majority being NH fish oils

• Assume 26% EPA and DHA for SA fish oil

• Assume 14% EPA and DHA for NH fish oil

• Vegetable oil use as of today (average 4% inclusion in

feeds)

• Scottish salmon will have an average of approximately

16% EPA and DHA (% of flesh oil)

• 2.25% of fillet (14% fat in fillet)

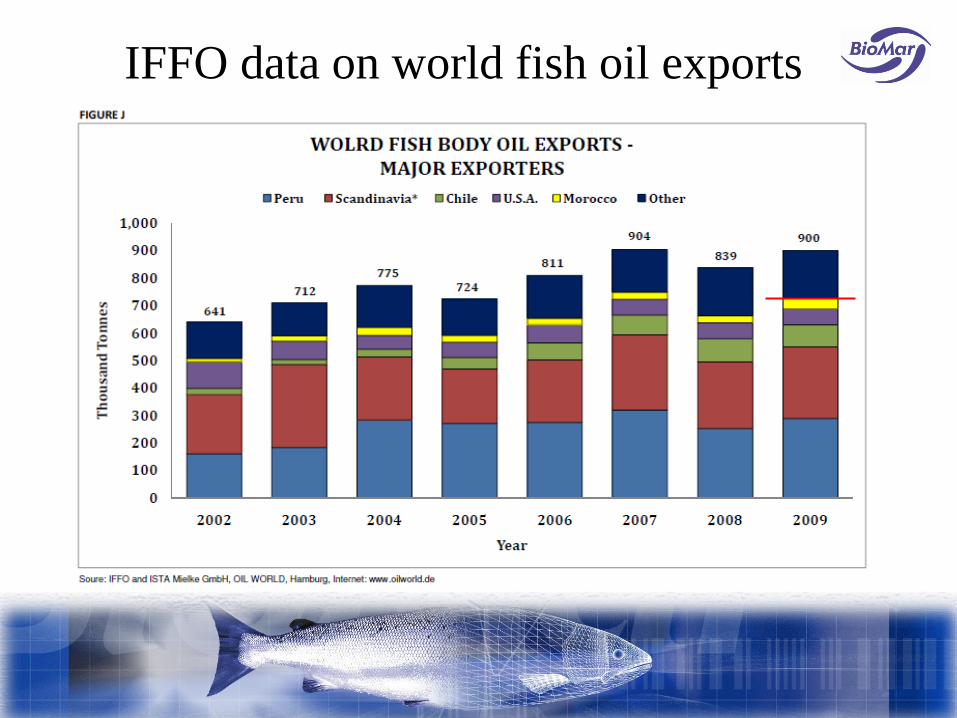

IFFO data on world fish oil exports

Growth in Omega 3 refining industry / year and

volume of fish oil used / year (GOED, 2010)G

row

th /

yea

r (%

)

Ton

nes

/ y

ea

r

Focus on EPA / DHA and fish oil supply

Supply

Farming

Farming + human consumption

Farming + human consumption

Farming +

human consumption

Farming

FarmingSupply

Supply

10% EPA and DHA

in fillet fat

7.5% EPA and

DHA

5.0% EPA and

DHA

Figure showing 3 scenarios for fish oil supply and use based on 10%, 7.5% and 5% EPA and DHA

targets for farmed salmonids production (FHL, Norway)

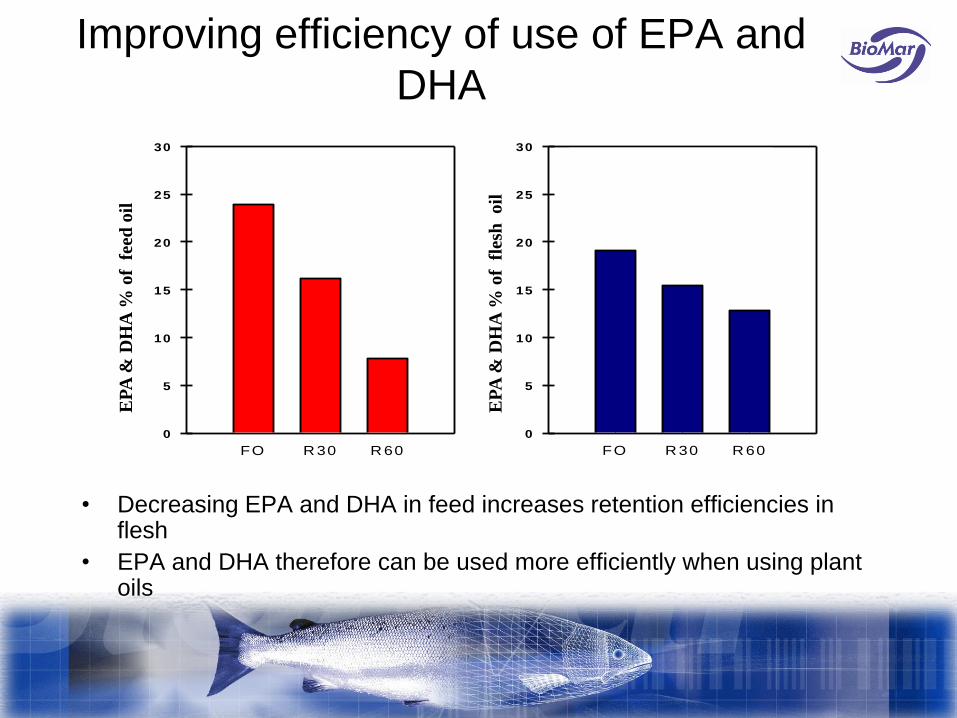

Improving efficiency of use of EPA and

DHA

• Decreasing EPA and DHA in feed increases retention efficiencies in flesh

• EPA and DHA therefore can be used more efficiently when using plant oils

FO R 30 R 60

EP

A+

DH

A,

% a

v f

ett

sy

rer

0

5

10

15

20

25

30

EPA+D H A i fôr

FO R 30 R 60

EP

A+

DH

A,

% a

v f

ett

sy

rer

0

5

10

15

20

25

30

EPA+D H A i fisk

EP

A &

DH

A %

of

fee

d o

il

EP

A &

DH

A %

of

fle

sh o

il

Fish oil, vegetable oils and EPA and

DHA|

• Only very modest replacement of fish oil with vegetable

oil has taken place in Scotland

• Scottish salmon therefore contains high levels of EPA and

DHA (approx 16% of fillet fat)

• Global supply of fish oil / EPA and DHA becoming critical

• We use far more than other salmon producing countries /

tonne of fish produced

• Unlike fishmeal this is not a nutritional challenge but a

market driven development

Current raw material use and comparison

of Scotland to Norway, Chile and

Canada

Current estimated raw material inclusion (weighted average

of all products) in different salmon farming regions

23

24

36

4

13

45

25

17

13

23

15

34

15

13

19

12

21

21

11

3

13

17

12

24

22

48

13

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% in

clu

sio

n

Scotland

standard

Scotland LR Norway Chile Canada

Country / feed type

Starch sources

Poultry oil

Vegetable oils

Land animal proteins

Vegetable proteins

Fish oil

Fishmeal

Total Marine

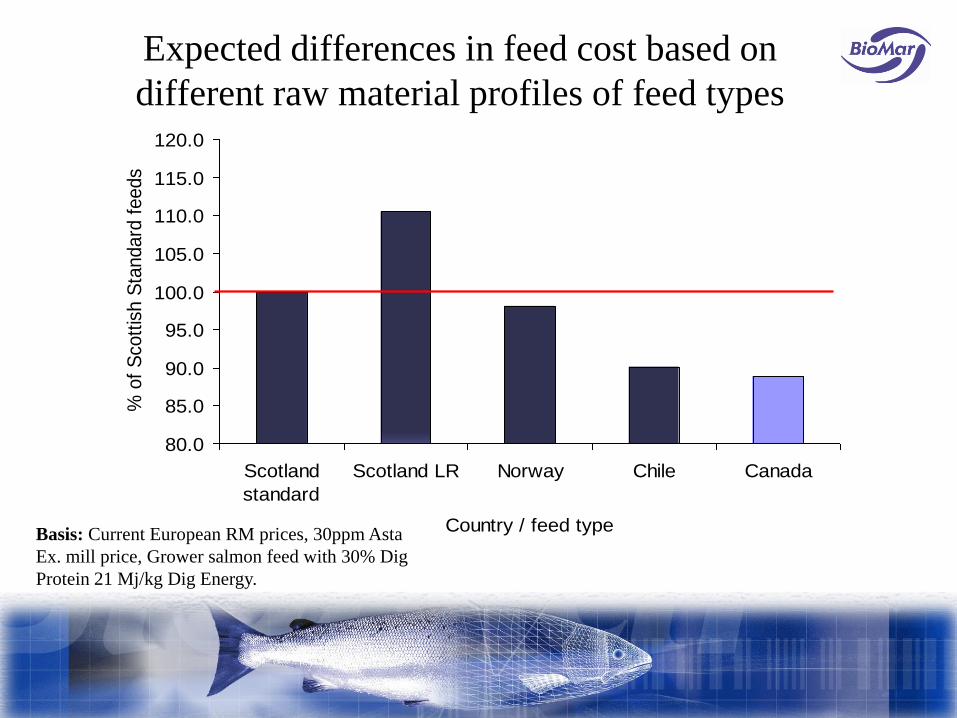

Expected differences in feed cost based on

different raw material profiles of feed types

80.0

85.0

90.0

95.0

100.0

105.0

110.0

115.0

120.0

Scotland

standard

Scotland LR Norway Chile Canada

Country / feed type

% o

f S

cott

ish S

tandard

feeds

Basis: Current European RM prices, 30ppm Asta

Ex. mill price, Grower salmon feed with 30% Dig

Protein 21 Mj/kg Dig Energy.

Current raw material use and comparison of

Scotland to Norway, Chile and Canada

• Main difference between Scottish feeds (non Label Rouge)

and Norwegian feeds is the higher use of fish oil in

Scotland

• Main difference between Chilean and Canadian salmon

feeds and European feeds is the use of land animal proteins

and oil, principally poultry meal, feather meal, bloodmeal

and poultry oil

• Considering above currently feed price will be ± 10% from

typical Scottish feed price

Comparison to other species e.g.

Tilapia

Tilapia Grower feed in relation to Scottish

salmon feed

23

24

36

4

13

2.52

41.5

10

9

35

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% in

clu

sio

n

Scotland standard Tilapia Grower

Feed type

Starch sources

Poultry oil

Vegetable oils

Land animal proteins

Vegetable proteins

Fish oil

Fishmeal

Comparison to other species e.g. Tilapia

• Tilapia only have a small requirement for marine raw

materials (approximately 6% total fishmeal and fish oil)

• Tilapia feeds lower in protein (32%) and energy

(15.5MJ/kg)

• Tilapia utilize carbohydrate as energy source also hence

higher level of starch sources (wheat, corn, sorghum)

• Feed cost approximately 50% of salmon feed

• Commercial FCRs 1.9 (Tilapia) vs. 1.2 (salmon)

• No requirement to achieve a flesh EPA and DHA level

Summary

• Fishmeal levels have decreased overtime, further decreases are possible depending upon knowledge and price

• A far bigger challenge is the use of Fish oil. We use far more fish oil / tonne of salmon in Scotland compared to all other salmon rearing countries, this is market driven not a nutritional requirement

• Use of LAPs of course gives Chile and Canada a major benefit in feed and hence production costs

• Scottish Salmon feeds are much higher in marine raw materials compared to feeds for other species such as Tilapia

• Differentiation in both feeds and salmon products has been far quicker in the UK than elsewhere, an important part of this has been healthy eating (EPA and DHA) and sustainability (choice of raw materials in particular marine raw materials)

• How do we continue to differentiate but deal with important issues like our fish oil use?