feeding the future: how to meet the challenge - march...

TRANSCRIPT

Feeding the future:

How to meet the challenge

CMAA International Cocoa Conference

13th March 2015 │ Miami, Florida

2

Six key global developmental challenges confronts us this century

I believe that there are six key developmental challenges that confront all of us this century:

Food security

Water security

Energy security

Impact of climate change

Sustainable growth

Inclusive growth

3

Agri-sector comprises a huge global market: US$5.9 trillion inproduction value with attractive growth prospects. Olam currently participates in 26% of this addressable market

Eth

anol

Bio

die

sel

DAP

Oilseeds

Biofuels

Fertiliser

Ure

aN

PK

CAGR(07-11)* 8.0% 11.4% 10.3% 13.8% 4.5% 15.5% 8.4%

Olam’s current participation

4

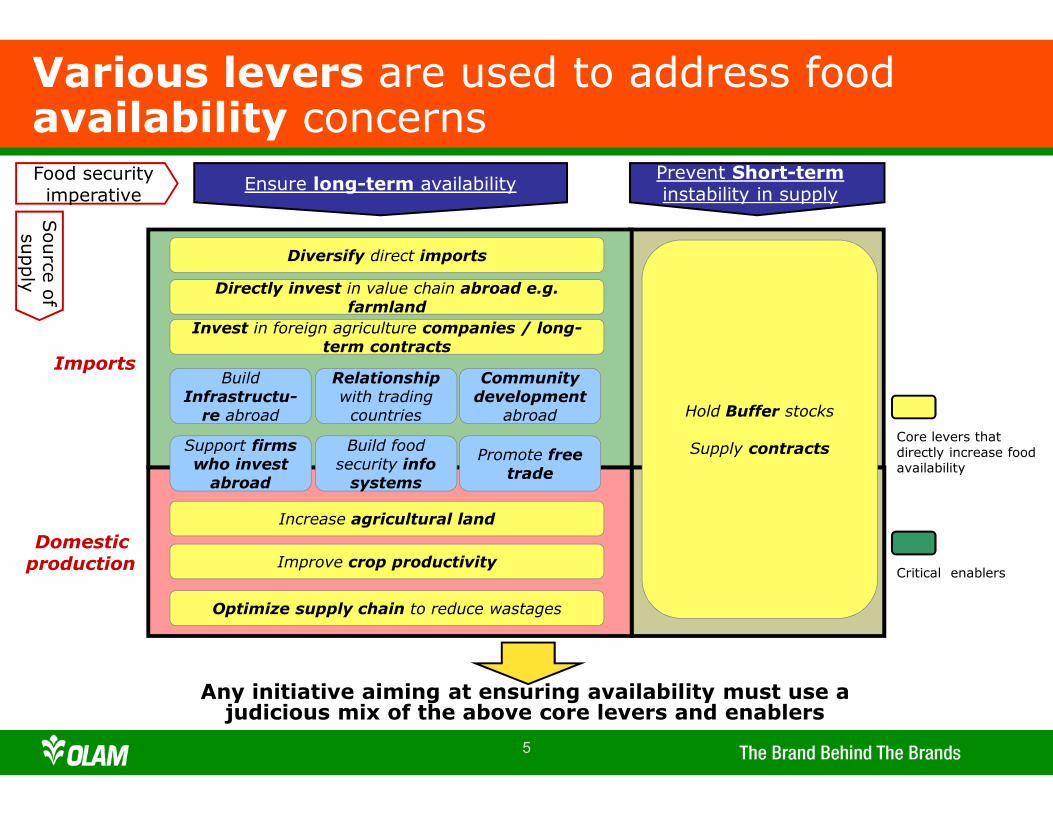

Food security defined

Food SecurityAvailability Accessibility

Adequacy

Affordability

• Logistics (storage, transport and distribution) to ensure access to food for all people –both during normal times and emergencies

• Pricing of food and purchasing power of households

• Quantity (sufficient amount of various nutrition components –energy, protein etc) and quality of food (safe, nutritious…)

• Addresses the ‘supply side’ of food security at the national-level

- Domestic production- Net trade- Food Aid

1

2

3

4

5

availabilityterm -longEnsure

Imports

Domestic production

Prevent Short-term instability in supply

Food security imperative

Source o

f su

pply

Directly invest in value chain abroad e.g. farmland

Invest in foreign agriculture companies / long-term contracts

BuildInfrastructu-re abroad

Relationship with trading countries Hold Buffer stocks

Supply contracts

Increase agricultural land

Improve crop productivity

Optimize supply chain to reduce wastages

Diversify direct imports

Community development abroad

Support firms who invest abroad

Build food security info systems

Promote free trade

Core levers that directly increase food availability

Critical enablers

Any initiative aiming at ensuring availability must use a judicious mix of the above core levers and enablers

Various levers are used to address food availability concerns

6

Oct 2011FAO Food Price Index

(Oct 2011)Food Commodity Price Indices

(Oct 2011)

2008 & 2011 Food Price Inflation:Cyclical or secular / structural trend?

7

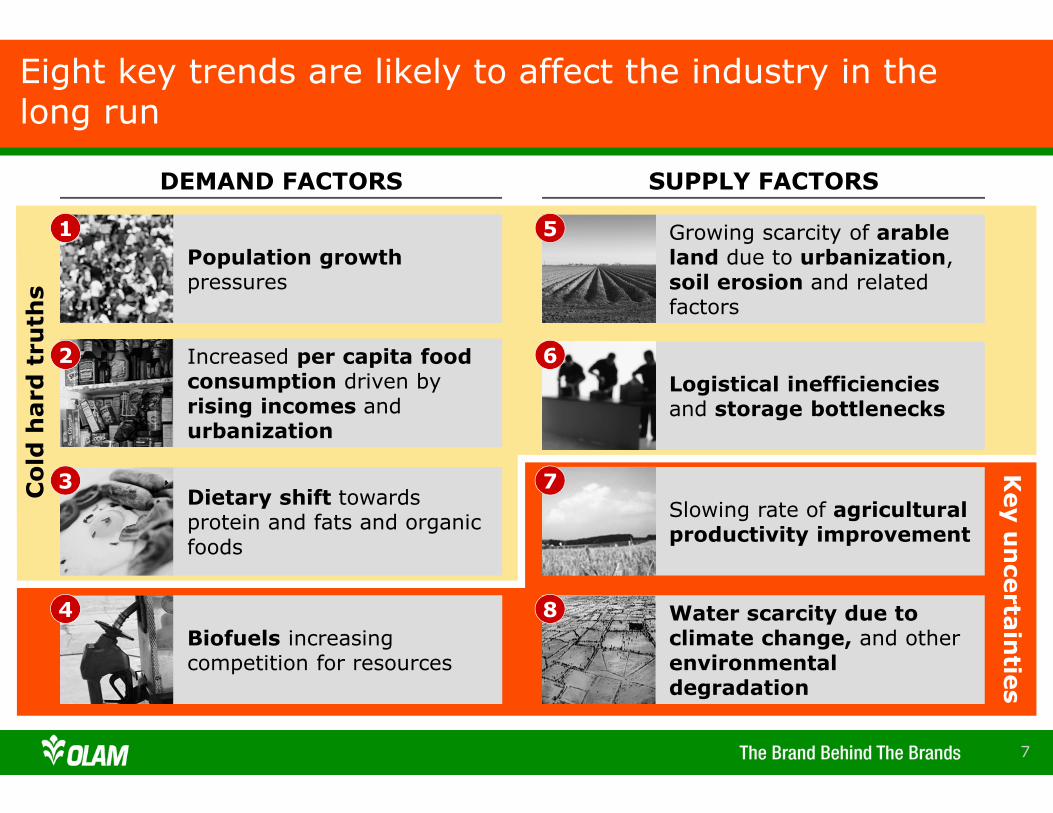

Eight key trends are likely to affect the industry in the long run

DEMAND FACTORS SUPPLY FACTORS

Population growth pressures

1

Increased per capita food consumption driven by rising incomes and urbanization

2

Dietary shift towards protein and fats and organic foods

3

Biofuels increasing competition for resources

4

Growing scarcity of arable land due to urbanization, soil erosion and related factors

5

Slowing rate of agriculturalproductivity improvement

7

Water scarcity due to climate change, and other environmental degradation

8

Logistical inefficienciesand storage bottlenecks

6

Cold hard truths

Key uncertainties

8 8

2.3x

1.2x

Asia & Africa will be the key regions to supply

Demand: Growing global population to increase overall consumption, particularly in developing markets

99

0.6%1.1%

0.4%

1979-81 1997-99

2015E 2030Ex 1997-

2030 CAGR

Demand: Rising income levels will result in increased food consumption and shift in dietary habits

HIGHER GDP/CAPITA CORRELATED WITH INCREASED CONSUMPTION

GROWTH IN MEAT CONSUMPTION MAINLY FROM DEVELOPING COUNTRIES

0

50

100

150

World

29

36 40 44

Developingcountries

12

25

32 36

Industrialcountries

80

88

96 100

Meat consumption (kg/capita)

2,000

3,000

4,000

0 20 40 60

Austria

Ireland

USA

Italy

UK

HK

Portugal

Korea

Taiwan

Turkey

2013 Per Capita GDP (USD K)

2013 Per capita daily calorie intake

FranceGermany

Canada

Spain

Greece

NZ

S. Arabia

Russia

Brazil

Mexico

Argentina

China

Malaysia

S. Africa

Peru

Thailand

Morocco

Indonesia

Philippines

Vietnam

Côte d'Ivoire

IndiaCambodia

Bangladesh

1010

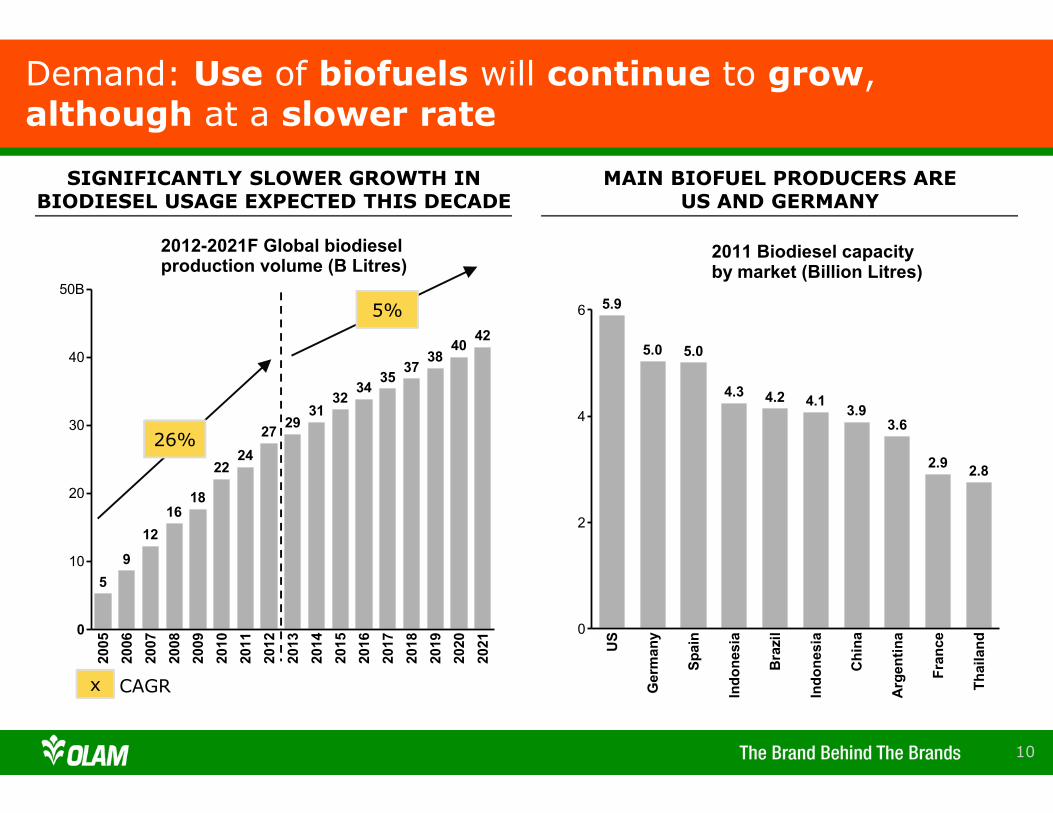

26%

5%

x CAGR

Demand: Use of biofuels will continue to grow, although at a slower rate

SIGNIFICANTLY SLOWER GROWTH IN BIODIESEL USAGE EXPECTED THIS DECADE

MAIN BIOFUEL PRODUCERS AREUS AND GERMANY

0

10

20

30

40

50B

2005

5

2006

9

2007

12

2008

16

2009

18

2010

22

2011

24

2012

27

2013

29

2014

31

2015

32

2016

342017

35

2018

37

2019

38

2020

40

2021

42

2012-2021F Global biodieselproduction volume (B Litres)

0

2

4

6

US

5.9

Germany

5.0

Spain

5.0

Indonesia

4.3

Brazil

4.2

Indonesia

4.1

China

3.9

Argentina

3.6

France

2.9

Thailand

2.8

2011 Biodiesel capacityby market (Billion Litres)

11

Biofuels: Feedstock used for biofuel production and quantity produced will affect demand for commodities

ADVANCEMENTS IN TRANSPORTATION INDUSTRY WOULD AFFECT DEMAND FOR BIOFUELS

HOW BIOFUEL IS PRODUCED IN FUTURE AFFECTS DEMAND FOR DIFFERENT TYPES OF COMMODITIES

Use of biofuels in aviation

Electrification of ground vehicles

Gen 1 Gen 1.5 Gen 2 Gen 3

Corn Sugarcane Crop Waste Algae

Accounts for 40% of biofuel production today

Full potential hindered by US Agri Policy & Europe climate

Technology is complex and costly

Technology still in infancy

Source of

biofuel

• Biofuels will continue to grow with increasing global mobility

• Electric vehicle uptake unlikely to displace biofuel demand

• Non-food feedstock unlikely to be commercialized at large scale in next 10 years, corn still most relevant in near term

What do we think will happen?

1212

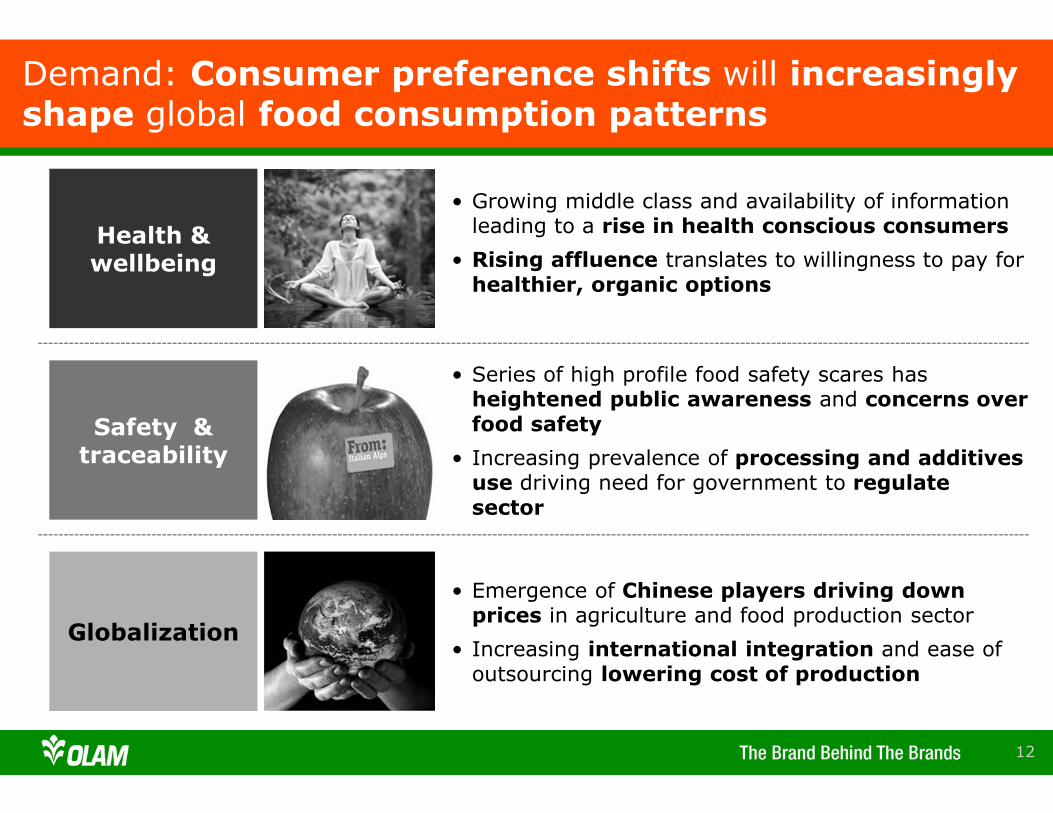

Globalization

Health & wellbeing

Safety & traceability

• Emergence of Chinese players driving down prices in agriculture and food production sector

• Increasing international integration and ease of outsourcing lowering cost of production

• Growing middle class and availability of information leading to a rise in health conscious consumers

• Rising affluence translates to willingness to pay for healthier, organic options

• Series of high profile food safety scares has heightened public awareness and concerns over food safety

• Increasing prevalence of processing and additives use driving need for government to regulate sector

Demand: Consumer preference shifts will increasingly shape global food consumption patterns

13

SustainableFood

Global agribusiness takes off

Sustainable Food: Today, market for organic commodities & fair trade is small but growing strongly

US LEADS ORGANIC FOOD MARKET BUT SHARE OF ORGANIC FOOD SMALL

HIGH GROWTH IN ORGANIC DEMAND EXPECTED TO

CONTINUE

RETAIL SALES OF FAIR TRADE PRODUCTS HAVE BEEN GROWING STEADILY

3x

Source: Organic Trade Association; Fair Trade International

Emergence of geneticengineering

Food Crisis

Green Revolution

1970 1980 1990 2000 2010 20141960

Organic Food Fair Trade

15%CAGR

14

Wealthier people, healthier diets: As incomes rise, dietary preferences become more sophisticated

What does this mean for us?

• How can we adapt our business to suit changing consumer food patterns?

• What do we need to be considered a responsible, fair and transparent partner?

Image

Healthier diets to combat “rich man” diseases

More of greens, whole grains, natural ingredients; Less of sugars, fats & processed

food

Image

Eating with social responsibilities in mind

Traceability of food products and responsible food production (e.g. fair trade) an increasing

concern

Image

Nutrition levels rising in emerging markets

Rice substituting inferior sources of nutrition (e.g. tubers and roots) in emerging markets

like Africa

1515

“Indian, Chinese, and US companies are among many inking land investment deals in Africa, including Ethiopia, Tanzania, South Sudan, Mali and Mozambique. [...] foreign investors bought or leased a land area in sub-Saharan Africa about the size of France in 2009 alone.”

Press article

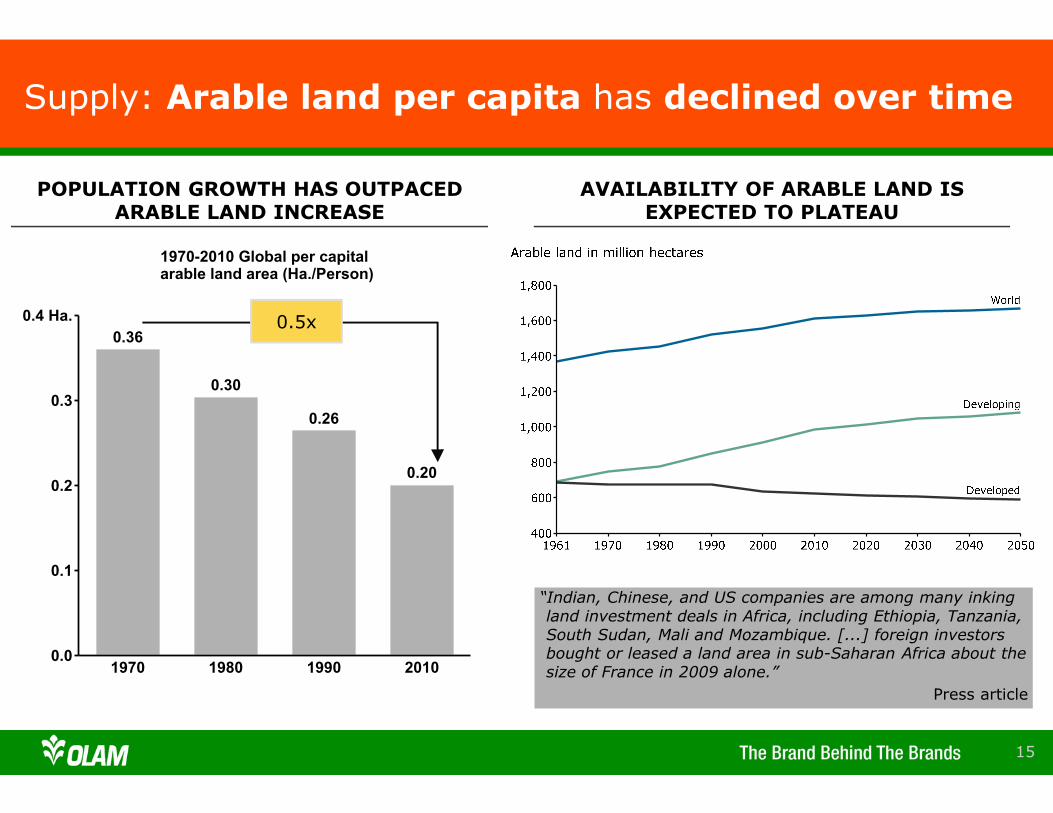

Supply: Arable land per capita has declined over time

POPULATION GROWTH HAS OUTPACED ARABLE LAND INCREASE

AVAILABILITY OF ARABLE LAND IS EXPECTED TO PLATEAU

0.5x

0.0

0.1

0.2

0.3

0.4 Ha.

1970

0.36

1980

0.30

1990

0.26

2010

0.20

1970-2010 Global per capitalarable land area (Ha./Person)

1616

Supply: Agricultural productivity improvement has slowed

0

5,000

10,000

15,000

1965

6,235

1985

7,120

2005

10,550

2010

12,304

Global cereals yield (hg/ha)

0.7%

2.0%1.5%

x CAGR

17

Agricultural productivity: Slowdown in productivity improvement could be abated by tech advancements

AGRI PRODUCTIVITY IMPROVEMENT HAS STARTED TO SLOW DOWN…

…BUT TECH ADVANCEMENTS COULD UNLOCK NEW POTENTIAL IN PRODUCTIVITY

0.7%

CAGR

Big Data in the Fields

Image

Big Data to increasingly drive production decisions

as pioneered by Climate Corp

Farming with Robots

Image

Farmbots and drones to surpass manual labor, boosting

field efficiency

3D Printing of Food

Image

“Food cartridges” and “bioink” changes landscape of food processing and preparation

GM – the New Norm

Image

Breakthrough in commercialization of more GM

varieties

2.0%1.5%

• Emerging players that digitalize their supply chain earlier on will catch up quickly

• Both private and public sectors will see investments in technology as a means to resolving scarcity

• High level of uncertainty dependent on technological breakthrough

What do we think will happen?

18

Poor weather conditions and world

energy crisis

2

Global agribusinesses see sharp growth

4

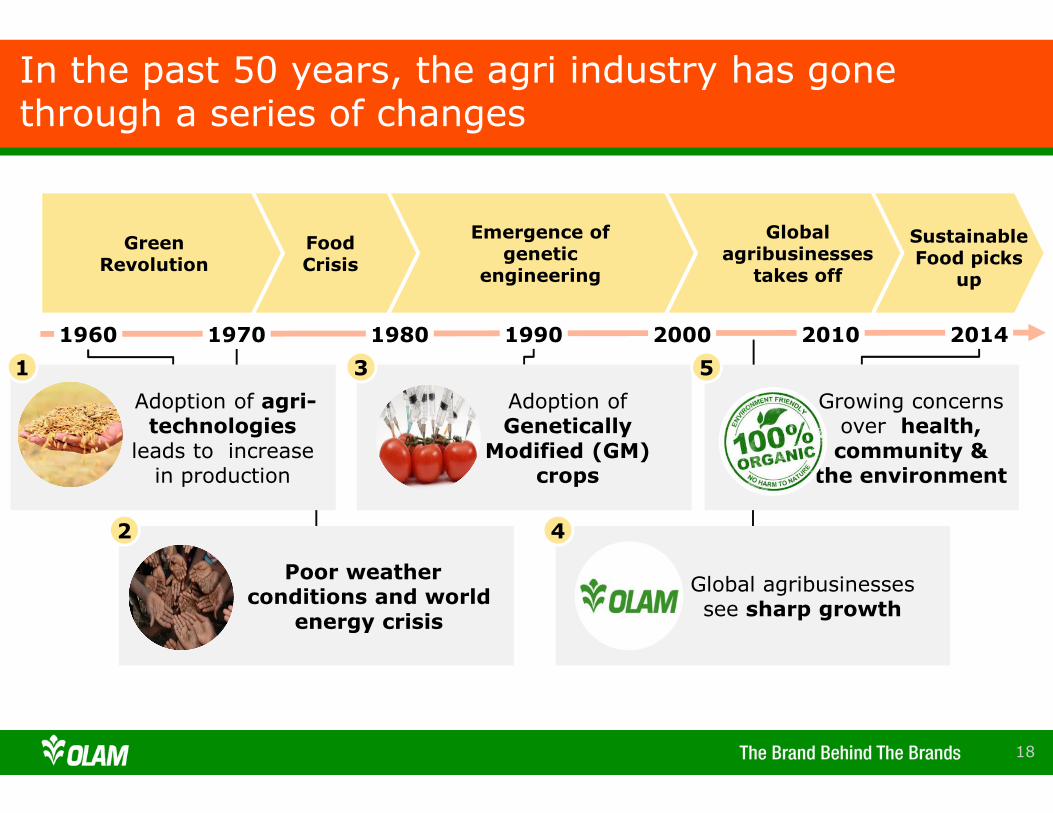

In the past 50 years, the agri industry has gone through a series of changes

Global agribusinesses

takes off

Emergence of genetic

engineering

Food Crisis

Green Revolution

1970 1980 1990 2000 2010 2014

Sustainable Food picks

up

1960

Adoption of agri-technologies

leads to increase in production

1

Adoption of Genetically

Modified (GM) crops

3

Growing concerns over health, community &

the environment

5

19

Green Revolution: Production boomed in the 60s due to improved yields and agri technology

Source: Land Commodities Research

Green Revolution led to spike in growth

Green Revolution led to spike in growth

Sustainable Food

Global agribusiness takes off

Emergence of geneticengineering

Food Crisis

Green Revolution

1970 1980 1990 2000 2010 20141960

HYV seeds Fertilizers Irrigation

+ +

20

Sustainable Food

Global agribusiness takes off

Food Crisis: Production shortfalls in 1970s caused record food prices

0

100

200

300

400

FAO Food Price Index (1990 = 100)

1961 1971 1981 1991 2001 2010Source: FAO

EARLY ’70S MARKED BY PRODUCTION SHORTFALLS

• Unfavorable weather conditions in major food producing countries

- E.g. Prolonged droughts in Sahel countries in Africa

• Energy crisis resulting in spike in cost of petroleum-based inputs

- Fertilizer prices tripled in 1973

LEADING TO SOARING FOOD PRICES

Emergence of geneticengineering

Food Crisis

Green Revolution

1970 1980 1990 2000 2010 20141960

21

Sustainable Food

Global agribusiness takes off

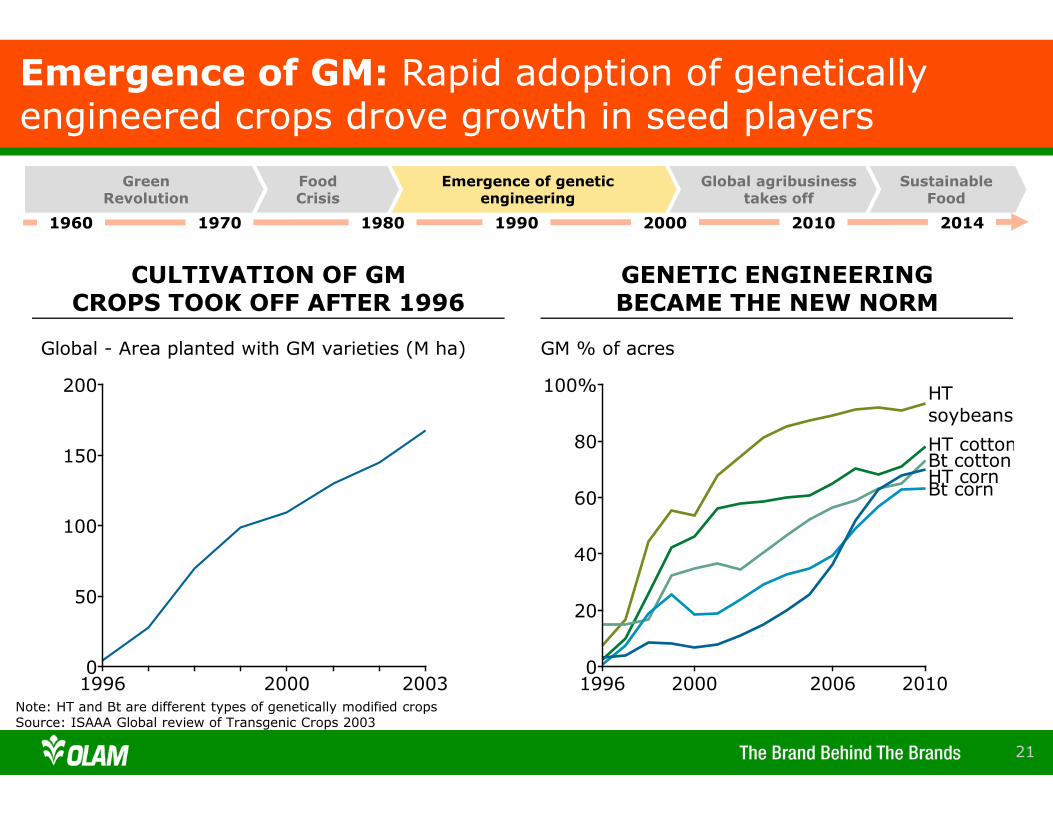

Emergence of GM: Rapid adoption of genetically engineered crops drove growth in seed players

0

20

40

60

80

100%

GM % of acres

HTsoybeans

Bt corn

1996 2000 2006 2010

HT cottonBt cottonHT corn

Note: HT and Bt are different types of genetically modified cropsSource: ISAAA Global review of Transgenic Crops 2003

CULTIVATION OF GM CROPS TOOK OFF AFTER 1996

GENETIC ENGINEERING BECAME THE NEW NORM

0

50

100

150

200

Global - Area planted with GM varieties (M ha)

1996 2000 2003

Emergence of geneticengineering

Food Crisis

Green Revolution

1970 1980 1990 2000 2010 20141960

2222

Supply: Adverse weather conditions and climate change have resulted, and may result, in supply shocks

23

Climate change & Water scarcity: Natural environment will be increasingly challenging

Source: US Dept of Energy; IPCC

Worst case

High emission levels

Best case

Low emission levels

“If carbon emissions not curbed, half the world will be living under extreme water scarcity”

“If carbon emissions not curbed, half the world will be living under extreme water scarcity”

(KM3)

Degree of climate change will affect global

temperatures & water scarcity

Water for irrigation also challenged by water

demand for urbanization

• Environmental degradation and water scarcity will persist; agri production will become more challenging

• Greater global emphasis on reducing carbon footprints; however coordinated efforts across countries expected to remain difficult

What do we think will happen?

24

By 2025, 36 countries, home to 1.4B peoplewill be affected by water scarcity

Source: National Intelligence Council, Global Trends 2025: A Transformed World International, 2008

Physical water scarcity: More than 75% of river flows are allocated to agriculture, industries, or domestic purposes. This definition of scarcity – relating water availability to water demand – implies that dry area are not necessarily water-scare.

Approaching physical water scarcity: More than 60% of river flows are allocated. These basins will experience physical water scarcity the near future.

Economic water scarcity: Water resources are abundant relative to water use, with less than 25% of water from rivers withdrawn for human purposes, but malnutrition exists.

Little or no water scarcity: Abundant water resources relative to use. Less than 25% of water from rivers is withdrawn for human purposes.

Not estimated

25

Many of the largest rivers in the Himalayas Hindu Kush region are strongly dependent upon snow and glacial melt for waterflow.Indeed, some scenarios suggest a 20–90% increase in annual flow due to glacial reduction, followed by a 10–40% decline, as glaciers and snow fall below critical thresholds for functions as water towers in 2050–2100. Combined with possible extreme precipitation events, this may result in greater seasonal droughts, and damage from floods. (Source: Rees and Collins, 2004; UNEP, 2007).

Impact of Climate Change

2626

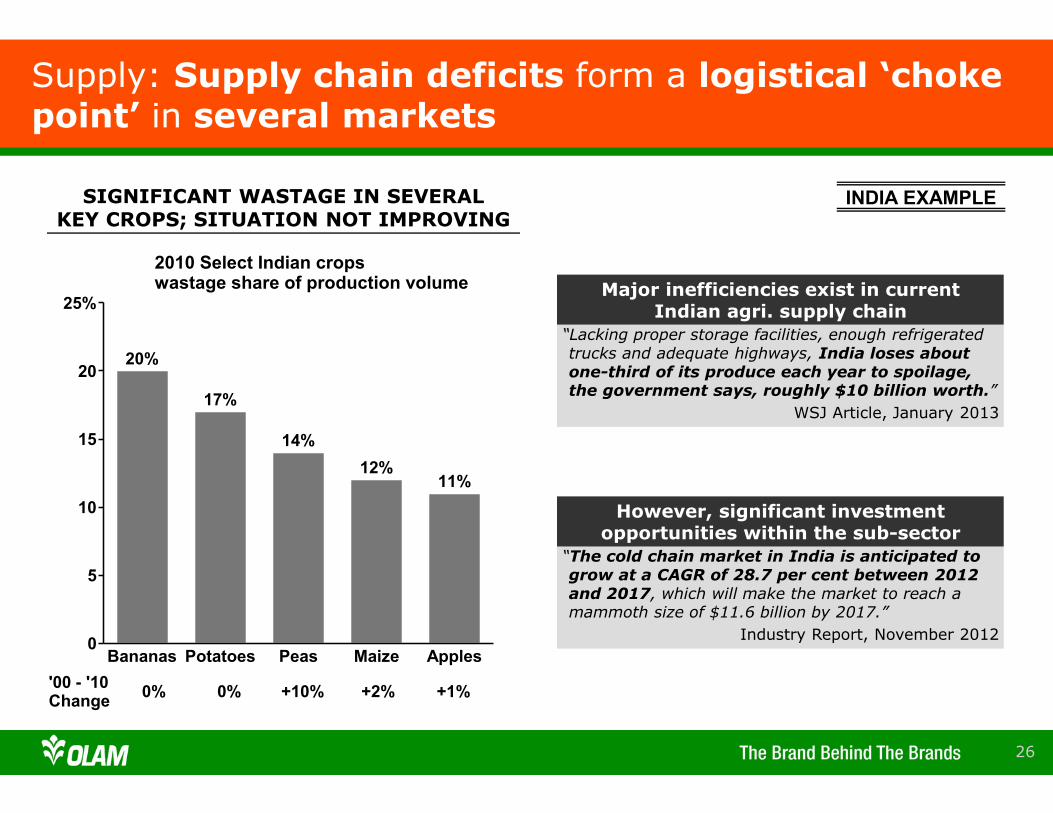

“Lacking proper storage facilities, enough refrigerated trucks and adequate highways, India loses about one-third of its produce each year to spoilage, the government says, roughly $10 billion worth.”

WSJ Article, January 2013

INDIA EXAMPLE

Major inefficiencies exist in currentIndian agri. supply chain

“The cold chain market in India is anticipated to grow at a CAGR of 28.7 per cent between 2012 and 2017, which will make the market to reach a mammoth size of $11.6 billion by 2017.”

Industry Report, November 2012

However, significant investment opportunities within the sub-sector

SIGNIFICANT WASTAGE IN SEVERALKEY CROPS; SITUATION NOT IMPROVING

Supply: Supply chain deficits form a logistical ‘choke point’ in several markets

0

5

10

15

20

25%

Bananas

20%

Potatoes

17%

Peas

14%

Maize

12%

Apples

11%

2010 Select Indian cropswastage share of production volume

0%0% +10% +2% +1%'00 - '10Change

27

Agri-sector will require significant investment

over the long-term

Agri-sector will require significant new investment estimated at US$200B every year over the next ~ 40 years to meet growing demand

2828

Supply: A 40% increase in global supply required to meet future demand for key staple grains

Total =

29 29

% change

Yieldlevers

Areaharvestedlevers

Supply: With limited supply of new land, all available levers will have to be used to increase production

30

Four possible scenarios for 2040Supply structure

Demand/Supply BalanceScarcity Over supply

Supply sources today

Commodities Revolution

Tech Disruption

World in Imbalance

Today is Tomorrow

New supply sources

31

Q&A

32

Thank You