fema’s elevation certificate€™s new elevation certificate updated fall 2016 ... “flood...

TRANSCRIPT

FEMA’s New Elevation CertificateUpdated Fall 2016

Expires Nov 30, 2018

VFMA Fall Workshop

David GunnHenrico County DPW

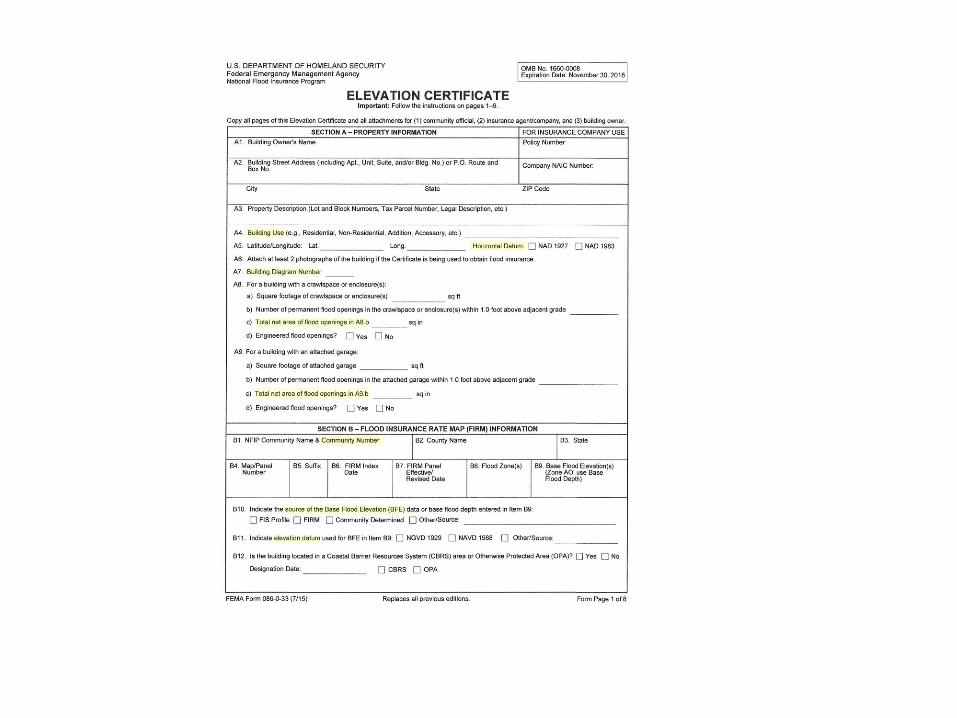

What????

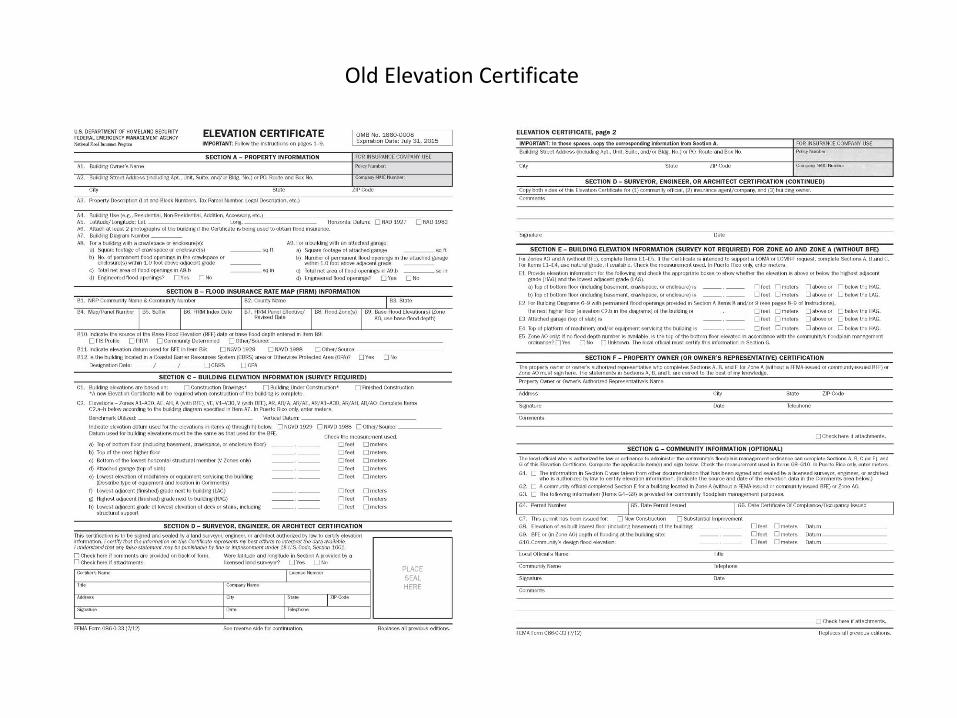

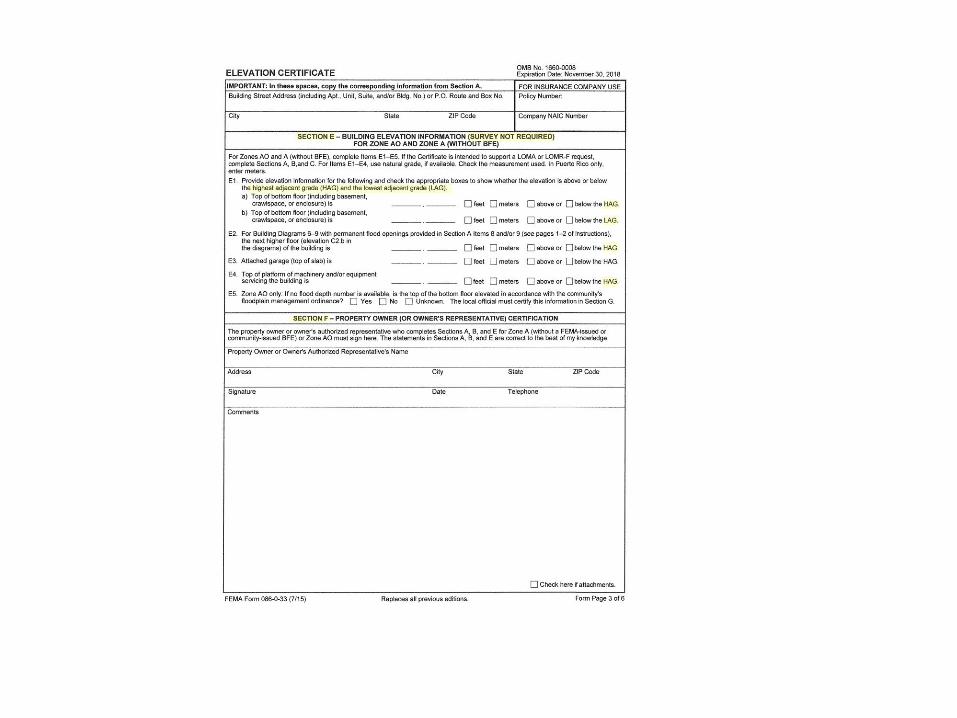

Old Elevation Certificate

VFMA Workshop

October, 2016

David M. Gunn, P.E., CFM

Henrico County DPW

NFIP Started in 1968 and expanded ever since - many reforms

over 50 years. Reduce/Avoid Disaster Relief for Foreseeable Events. Policies underwritten by Federal Flood Insurance

Administration – policy published in CFR Not traditional insurance – uniform policies –no reserve,

no profits.

“Flood Damages are not the result of a Natural Disaster,They are the result of poor decisions.”

Three Supports

Flood Insurance – initially subsidized to encourage participation – Added Mortgage Company Mandate & Periodic Portfolio Reviews.

Flood Insurance Rate Maps – Coastal Updates, GIS conversions – still major issues.

Floodplain Management by locality – follow minimum Federal rules in development decisions – can & should enforce higher standards .

Reason for Reform

$24 Billion in Debt – Katrina & Sandy

Premiums don’t meet Payments

No Reserves in original NFIP

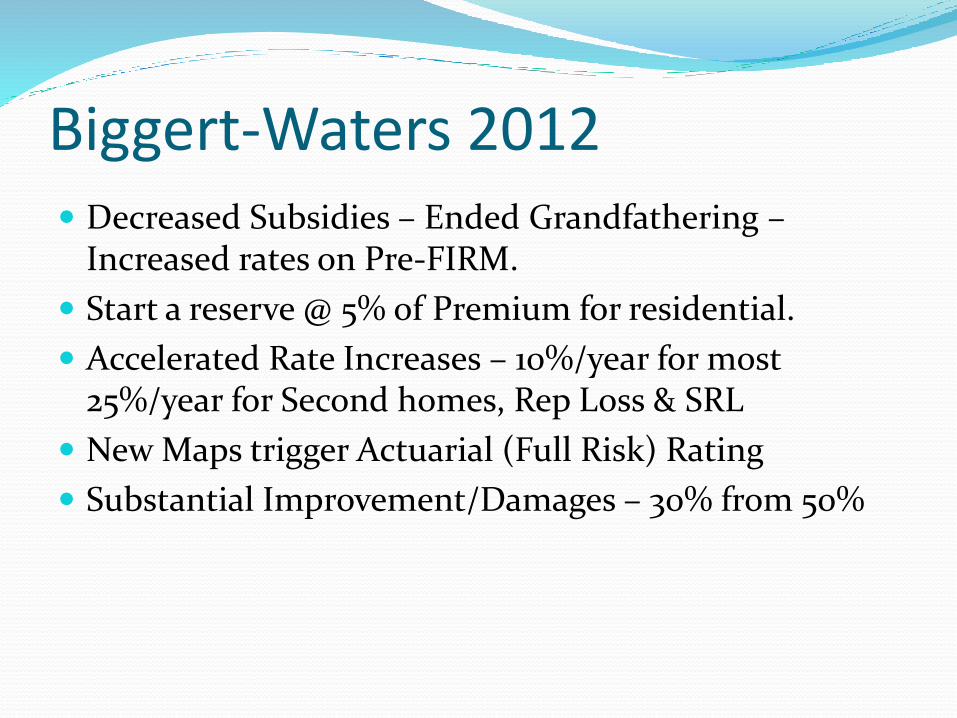

Biggert-Waters 2012 – Good Ideas – affordability issues & politics.

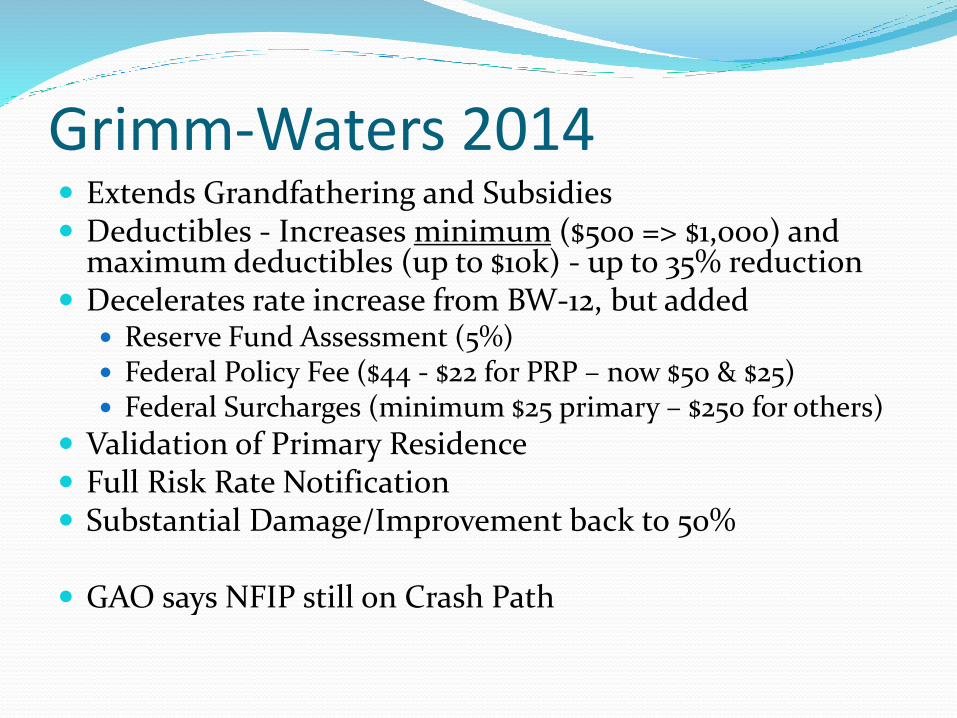

Grimm-Waters 2014 – slows down some reforms, but keeps most.

Biggert-Waters 2012 Decreased Subsidies – Ended Grandfathering –

Increased rates on Pre-FIRM.

Start a reserve @ 5% of Premium for residential.

Accelerated Rate Increases – 10%/year for most 25%/year for Second homes, Rep Loss & SRL

New Maps trigger Actuarial (Full Risk) Rating

Substantial Improvement/Damages – 30% from 50%

Grimm-Waters 2014 Extends Grandfathering and Subsidies Deductibles - Increases minimum ($500 => $1,000) and

maximum deductibles (up to $10k) - up to 35% reduction Decelerates rate increase from BW-12, but added

Reserve Fund Assessment (5%) Federal Policy Fee ($44 - $22 for PRP – now $50 & $25) Federal Surcharges (minimum $25 primary – $250 for others)

Validation of Primary Residence Full Risk Rate Notification Substantial Damage/Improvement back to 50%

GAO says NFIP still on Crash Path

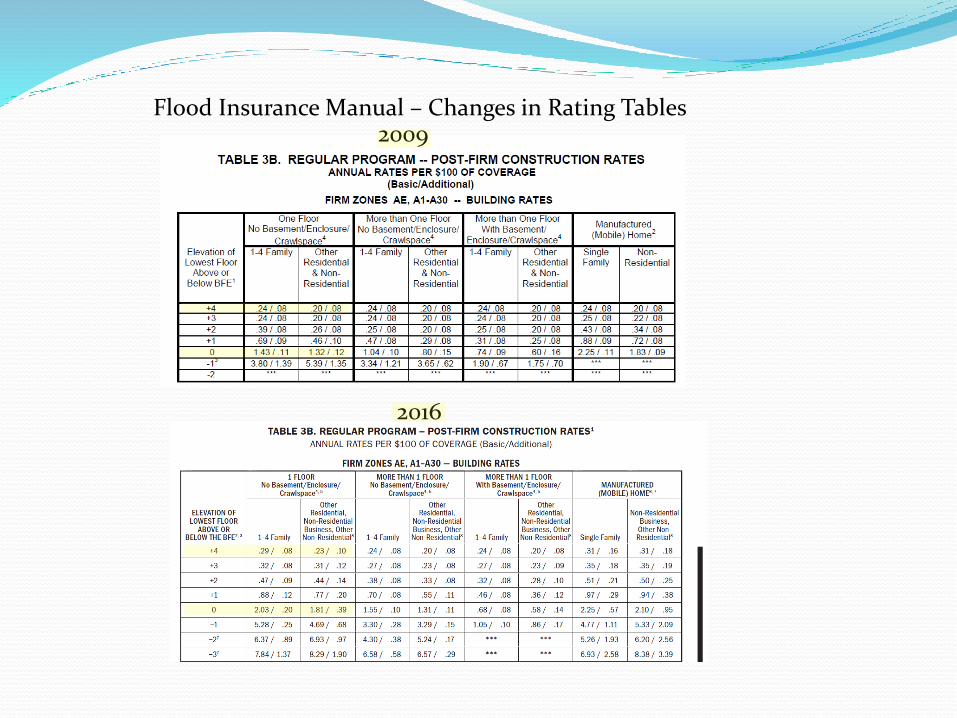

Flood Insurance Manual - Rating Tables

Multiply Rate X $100 of Coverage

Building Basic Limit $.88 x $60,000 = $528

Bldg Addl Limit $.08 x $140,000 = $112

Contents Basic Limit $.69 x $25,000 = $95

Content Addl Limit $.12 x $75,000 = $90

Bldg/Content Subtotal Bldg $640 / Contents $185 $825

ICC Premium $34 – typical

CRS Discount $0 for this example

Reserve Fund Assessment $43 (5%)

Probation Surcharge $0 for this example

Federal Policy Fee $44 for this example

Total $946

Premium Calculation

$200,000 building coverage - $100,000 contents coverage

Flood Insurance Manual – Changes in Rating Tables2009

2016

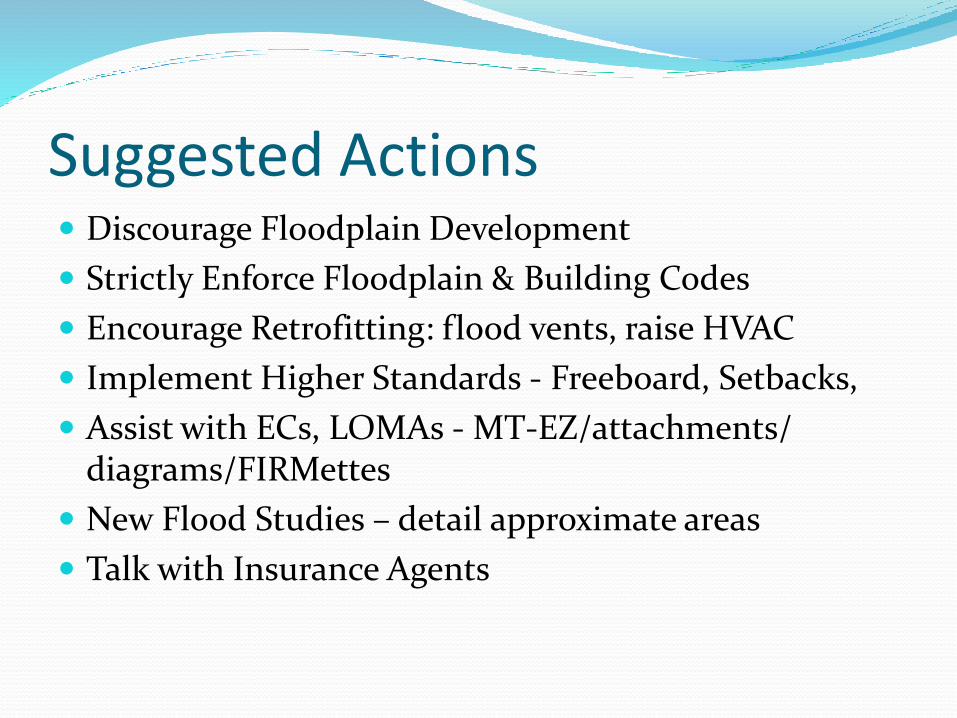

Suggested Actions Discourage Floodplain Development

Strictly Enforce Floodplain & Building Codes

Encourage Retrofitting: flood vents, raise HVAC

Implement Higher Standards - Freeboard, Setbacks,

Assist with ECs, LOMAs - MT-EZ/attachments/ diagrams/FIRMettes

New Flood Studies – detail approximate areas

Talk with Insurance Agents