ff-road diesel w need k - ctema.com · page 2 of 7 pages icpa advisory on everything you need to...

TRANSCRIPT

Page 1 of 7 Pages ICPA Advisory on Everything You Need to Know on Off-Road Diesel

July 2, 2007

OFF-ROAD DIESEL – WHAT YOU NEED TO KNOW

Retail fuel dealers need to know about several key issues that will dictate how they will sell off-road diesel to their customers. Below you will learn what you need to do and when you need to do it so that you and your customers are in compliance with the new U.S. Environmental Protection Agency (EPA) low sulfur off-road diesel requirements. Delivery Ticket Language

A. Effective June 1, 2007 all heating oil delivery tickets must have the following statement printed on them:

“Dyed Unmarked Heating Oil: Not for use in highway, locomotive or marine engines.” Note that the old IRS language “Dyed Diesel Fuel, Non Taxable Use Penalty for Taxable Use” is no longer required. If you are still using this language, it should be removed and replaced with the language stated above.

B. Effective June 1, 2007 through October 1, 2007 all off-road diesel delivery tickets using heating oil must have the following statement printed on them:

“HS Dyed NRLM-may exceed 500-ppm sulfur. Not for use in nonroad engines requiring ULSD or highway engines.”

C. Effective June 1, 2007 all dyed off-road LS diesel (containing a maximum of 500ppm sulfur) delivery tickets must have the following statement printed on them:

“500-ppm sulfur dyed LSD. Non-road or tax exempt use only. Not for use in 2007 and later vehicles.”

D. Effective June 1, 2007 all dyed off-road LS diesel (containing a maximum of 15ppm sulfur) delivery tickets must have the following statement printed on them:

“15-ppm sulfur dyed ULSD. Non-road or tax exempt use only.”

E. Effective June 1, 2007 in the event that dyed off-road diesel is not available you may use clear ULSD 15ppm diesel - in that case delivery tickets must have the following statement printed on them:

Page 2 of 7 Pages ICPA Advisory on Everything You Need to Know on Off-Road Diesel

“15-ppm sulfur ULSD.” Note: End users, using clear taxable diesel fuel for non-taxable off-road purposes is eligible for federal and state excise tax refunds. See attached tax guidance for refund information. If you have preprinted delivery tickets you should purchase a stamp to mark your tickets with this new language. Off Road Diesel Sulfur Content

• Until October 1, 2007 you may continue to sell heating oil for off-road purposes. Use the delivery ticket language as stated in B above.

• After October 1, 2007 you are required to sell off-road diesel that has a sulfur content of not more than 500 parts per million (ppm), and will no longer be permitted to sell heating oil for that purpose. Use the delivery ticket language as stated in C or D above.

• An exemption to the low sulfur off-road diesel rule exists for stationary generators manufactured prior to April 1, 2006. Any stationary generator manufactured before April 1. 2006 can continue to use heating oil beyond the October 1, 2007 low sulfur off-road deadline.

Note that heating oil sold in Connecticut contains not more than 3000ppm sulfur and does not meet the EPA off-road diesel standard of 500ppm sulfur as of October 1, 2007. Dispenser Labeling

• As of June 1, 2007 off-road diesel, heating oil and dyed kerosene dispensers are required to be labeled with specific information prescribed by EPA.

Attached you will find an order form for EPA compliant off-road diesel, on-road diesel and kerosene labels that are being offered by the New England Fuel Institute (NEFI). Record Keeping

• Off-road diesel delivery tickets, invoices, bills of lading, shipping papers, etc. are required to be maintain for five years.

Frequently Asked Questions and Answers – Off Road Diesel [PMAA]

The compliance deadline for U.S. EPA’s low sulfur non-road diesel fuel regulations starts June 1. On this date refiners must begin the phase-out of high sulfur non-road, locomotive and marine (NRLM) engine diesel fuel for distillates except heating oil and jet fuel. The length of the phase-out and the compliance requirements differ depending on which part of the country the fuel is marketed. The two compliance areas are: (1) the Northeast/Mid-Atlantic (NEMA) region and (2) the rest of the country (non-NEMA area). The following is a Q & A of the most frequently asked questions on compliance with the new NRLM regulations:

Q. How do I know which of the two NRLM compliance areas I am in?

A. There are two NRLM compliance areas with different requirements The following states and counties are located in the Northeast/Mid-Atlantic (NEMA) area: Massachusetts Vermont, New Hampshire, Maine,

Page 3 of 7 Pages ICPA Advisory on Everything You Need to Know on Off-Road Diesel

Connecticut, Rhode Island, New York (except for the counties of Chautauqua, Cattaraugus, and Allegany), New Jersey, Delaware, North Carolina, Virginia, Maryland, Washington D.C., , Pennsylvania (except for the counties of Erie, Warren, Mc Kean, Potter, Cameron, Elk, Jefferson, Clarion, Forest, Venango, Mercer, Crawford, Lawrence, Beaver, Washington, and Greene), and the eight eastern-most counties of West Virginia (Jefferson, Berkeley, Morgan, Hampshire, Mineral, Hardy, Grant, and Pendleton). Every other state and county not listed above is located in the non-NEMA area.

Q. Can I still sell heating oil for off-road use in the NEMA area?

A. No. Product designated as heating oil may not be sold for non-road locomotive or marine engines after June 1, 2007. However, heating oil may be re-designated on product transfer documents as high sulfur NRLM in the NEMA area and sold as NRLM until October 1, 2007. On this date, any diesel fuel over 500-ppm sulfur cannot be used as NRLM fuel (see stationary engine exception below).

Q. Can I still sell high sulfur NRLM for off-road use in the non-NEMA area after June 1, 2007?

A. Yes, if you can find it. High sulfur NRLM fuel is allowed for off-road use in the non-NEMA area until October 1, 2010 for downstream petroleum marketers.

Q. Can I sell marked heating oil in a NEMA area?

A. Yes, marked heating oil from the non-NEMA area may be sold within the NEMA area. However, unmarked heating oil from the NEMA area may not be sold in the non-NEMA area. All product designated as "heating oil" in the non-NEMA area must be marked.

Q. What language do I need to include on kerosene product transfer documents?

A. Kerosene is also subject to the EPA’s sulfur reduction requirements. Kerosene PTD language is identical to the above language for diesel fuel, except that the word "kerosene" must be substituted for the word "diesel fuel" and the designation "ULSK", and "LSK" and must be substituted for "ULSD", and "LSD" respectively. These PTD language notices are required for all transfers of NRLM kerosene, including sales to end users at retail and to wholesale purchaser consumers.

Q. Can I shorten the PTD language to fit on my shipping papers and delivery tickets?

A. No. You must use the exact language authorized by the EPA. If you do not have room, use an ink stamp or print or stamp the information on the back of the document as long as there is a phrase on the front directing you to the back.

Q. What are the diesel fuel dispenser decal requirements?

A. There is an array of dispenser decals that are required by June 1, 2007. NRLM ULSD, LSD and HS all require specific decals for retail and wholesale purchaser/consumer dispensers. There are also decals for marked and unmarked heating oil and kerosene. These decals may be obtained from the New England Fuel Institute at www.nefi.com or by calling (617) 924-1000.

Q. Are stationary generators subject to the NRLM regulations?

A. It depends on the date of manufacture of the equipment. Beginning October 1, 2007, all stationary engines (emergency generators, etc.) manufactured, remanufactured or modified on or after April 1, 2006 may only use NRLM diesel fuel with a sulfur content of 500-ppm or less. Stationary engines manufactured, remanufactured or modified before April 1, 2006 may continue to use heating oil with sulfur content greater than 500-ppm.

Page 4 of 7 Pages ICPA Advisory on Everything You Need to Know on Off-Road Diesel

Q. Are there any downgrading limits for NRLM?

A. No. In the non-NEMA area, you may mix NRLM 15-ppm, 500-ppm and HS product without limitation. You may even mix these products with marked heating oil. However, once evidence or a marker is in product, it can only be used as heating oil and not for NRLM use. In the NEMA area, you may mix 15-ppm dyed fuel with 500-ppm dyed fuel without limitation. However, you may not mix these products with heating oil in the NEMA area.

Q. I am in the non-NEMA area and my supplier tells me I cannot sell high sulfur NRLM after June 1, 2007. Is this true?

A. No. Petroleum marketers in the non-NEMA areas may continue selling high sulfur NRLM until October 1, 2010. The supply of HS NRLM will be limited due to EPA trading credits and small refiner exemptions in the non-NEMA area. However, if you can find HS NRLM, you can sell it.

Q. I can’t find marked heating oil in the non-NEMA area. Can I use 500-ppm NRLM for heating oil instead?

A. Yes, but you can’t call it "heating oil". You must use the PTD language for dyed 500-ppm NRLM. Only marked fuel can be called heating oil in the non-NEMA area.

Q. Why do the NRLM rules keep changing?

A. There have been a number of downstream issues that the EPA did not foresee when writing the NRLM regulations. As these issues come to light, the agency has moved quickly to make corrections. For example, when PTD language was too long for onboard ticket printers, the EPA shortened the required language. It is expected that additional issues will come up that require the EPA to additional NRLM changes.

OFF-ROAD DIESEL FEDERAL & STATE

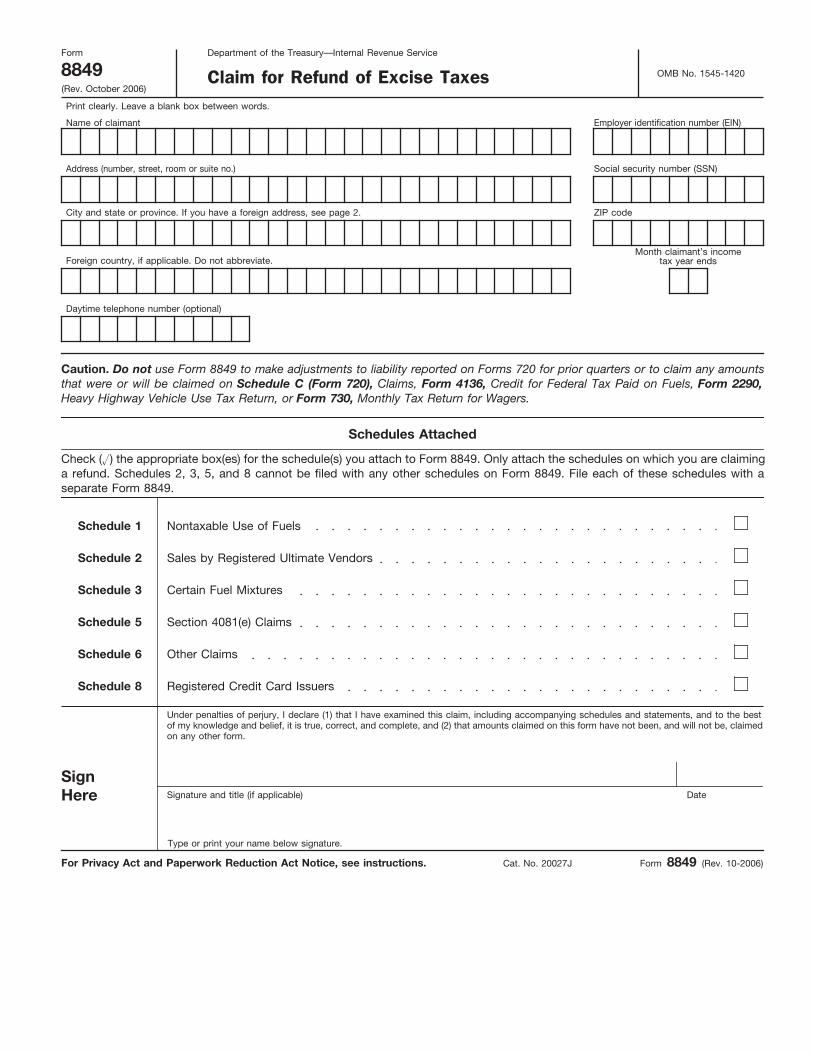

TAX REFUND INFORMATION As of October 1, 2007 diesel fuel being sold for off road purposes must contain not more than 500ppm sulfur. Note that #2 heating oil will no longer be able to be used for off road purposes as of October 1, 2007. Retailers who are unable to obtain dyed off-road diesel will need to provide information on how their customers can obtain a refund of the taxes paid on clear on-road diesel being used for non-taxable off-road purposes. Please contact your supplier to determine what product will be available. Below is information on how to obtain a Federal and State tax refund from the Internal Revenue Service (IRS) and the Connecticut Department of Revenue Services (DRS). Federal Refund Information The end user of clear diesel fuel being used for a non-taxable off-road purpose may apply for a refund of the Federal Diesel Excise Tax of 24.4 cents per gallon by using an IRS Form 8849 (attached) http://www.icpa.org/protect/TBs/fed_forms/f8849.pdf. The end user should must also fill out Schedule 1 (Form 8849) http://www.icpa.org/protect/TBs/fed_forms/f8849s1.pdf.

Page 5 of 7 Pages ICPA Advisory on Everything You Need to Know on Off-Road Diesel

State Refund Information The end user of clear diesel fuel being used for a non-taxable off-road purpose may apply for a refund of the State Excise Tax of 26 cents per gallon by using an DRS Form AU-724 (attached) http://www.ct.gov/drs/lib/drs/forms/2007forms/excise/motorvehiclefuels/au-724.pdf. Note that there is NO exemption for Gross Earnings Tax. This bulletin does not take the place of professional accounting advice. You are strongly urged to consult a tax professional for guidance in addition to reading this material. For more information contact IRS at 203-781-3081 and DRS at 860-541-3243.

Commonly Asked Off-Road Diesel Tax Questions

Q: If I sell clear diesel for a non-taxable off road purpose can my customer get a refund of the state and federal tax? A: Yes – the end user may apply for a refund of the federal diesel excise tax of 24.4 cents by filling out an IRS Form 8849 and the 26 of the 37 cent state diesel excise tax can be claimed by filling out a DRS Form AU-724. Q: Can I get a refund of the state and federal diesel excise tax so that my customer does not have to apply for a refund? A: No – the only way to recapture the state and federal excise tax is if the end user applies for it. Q: What tax do I charge if I sell dyed #2 oil for off-road purposes? A: Retailers selling heating oil before October 1, 2007 must charge the 37 cent excise tax and the 7.53% gross receipts tax. 26 of the 37 cent excise tax can be refunded to the end user by using a state form AU-724. Q: What tax should be charged when diesel fuel is being used in a generator that is being used to provide electricity?

Page 6 of 7 Pages ICPA Advisory on Everything You Need to Know on Off-Road Diesel

A: Diesel fuel sold exclusively for use in portable power system generators that are larger than 150 kilowatts is exempt from the motor fuel tax of 37¢ per gallon, pursuant to Conn. Gen. Stat. Sec. 12-458(M) .

Diesel fuel used in portable power system generators larger than 150 kilowatts is also exempt from sales and use taxes, pursuant to Conn. Gen. Stat. §12-412(107).

Therefore the Connecticut distributor would not charge either sales and use taxes or Motor Fuels Tax on diesel sold exclusively for use in portable power system generators that are larger than 150 kilowatts.

If the generator is smaller then 150 kilowatts you would charge the 37¢ Motor Fuels Tax on the Diesel Fuel. Your customer in this case would use Form AU-724 to file a motor vehicle fuels tax refund claim for diesel fuel used for off road purposes at the end of the calendar year.

Q: If clear diesel fuel is sold to a farmer, which refund form they should use if they wish to continue purchasing clear diesel tax free? A: If the farmer holds an farmers tax exemption permit, they may buy motor vehicle fuels exempt from tax as long as the diesel fuel will be used either in a vehicle not licensed to be operated on state highways, or in a vehicle registered with the Department of Motor Vehicles exclusively for use for farming purposes. The fuel may not be delivered to a tank in which the farmer stores fuel used for both farm and non-farm purposes. The farmer must furnish the fuel distributor with Form AU-302, Farmer Declaration Motor Vehicle Fuels Tax Exemption, at the time of purchase.

Farmers holding an exemption permit who did not claim the exemption may file a claim for refund on or before the last day of May, as long as the refund claim involves the purchase of at least 200 gallons of fuel during the preceding calendar year. The farmer must file a refund claim using Form AU-725, Motor Vehicle Fuels Tax Refund Claim - Farm Use. Submit copies or originals of each numbered slip or invoice issued to you at the time of each purchase with the claim for refund. Farmers should also attach Form OR-248 Farmers Tax Exemption Permit in order not to be assessed use tax on the diesel fuel.

Q:

If I am selling kerosene for off-road purposes what tax do I charge?

A:

Kerosene being sold for off-road purposes should be charged the 37 cent excise tax and the 7.53% gross earnings tax. The end user may apply for a partial 26 cent refund of the excise tax.

If you have any state tax questions please contact the DRS Excise Audit Unit at 860-541-3224. Federal tax questions should be directed to the IRS at 203-781-3081.

Page 7 of 7 Pages ICPA Advisory on Everything You Need to Know on Off-Road Diesel

ICPA Tax Chart – July 1, 2007

Product Tax Charged

Dyed red #2 Oil sold as off-road diesel

37 cent CT excise tax (26 cents is refundable)

7.53% gross earnings tax (the GET does not apply if the fuel is labeled as “high sulfur diesel”)

Clear diesel sold for off road purposes

37 cent CT excise tax (26 cents is refundable)

24.4 cent Federal excise tax

Clear diesel for on-road purposes 37 cent CT excise tax 24.4 cent Federal excise tax

Clear Kerosene sold for off-road purposes

37 cent CT excise tax (26 cents is refundable)

7.53% gross earnings tax 24.4 cent Federal excise tax

Clear Kerosene sold for on-road purposes

37 cent CT excise tax 7.53% gross earnings tax 24.4 cent Federal excise tax

Gasoline

25 cent CT excise tax 18.4 cent Federal excise tax 7.53% gross earnings tax

CAUTION

Your downstream sales and what you label product sales is critical. If you sell kerosene that has to include the GRT at the 7.53% rate and the 37c excise tax. If you sell #1 diesel then that has no GRT after July 1st and only includes the 37c excise tax. If you sell heating oil as offroad diesel until October 1st that sale has to include the 7.53% GRT and the 37c excise tax. If you sell high sulfur off road diesel fuel then that has no GRT and only includes the 37c excise tax. Exempt users may only apply for a refund of 26c against the 37c they paid. Be careful with these sales.

OMB No. 1545-1420

Claim for Refund of Excise Taxes

(Rev. October 2006)

Department of the Treasury—Internal Revenue Service

Name of claimant

Address (number, street, room or suite no.)

Form 8849

City and state or province. If you have a foreign address, see page 2.

Foreign country, if applicable. Do not abbreviate.

Month claimant’s incometax year ends

ZIP code

Social security number (SSN)

Employer identification number (EIN)

For Privacy Act and Paperwork Reduction Act Notice, see instructions.

Schedules Attached

Schedule 1 Schedule 2 Schedule 3 Schedule 5 Schedule 6

Caution. Do not use Form 8849 to make adjustments to liability reported on Forms 720 for prior quarters or to claim any amounts that were or will be claimed on Schedule C (Form 720), Claims, Form 4136, Credit for Federal Tax Paid on Fuels, Form 2290,Heavy Highway Vehicle Use Tax Return, or Form 730, Monthly Tax Return for Wagers.

Nontaxable Use of Fuels

Sales by Registered Ultimate Vendors

Certain Fuel Mixtures

Section 4081(e) Claims

Other Claims

SignHere

Under penalties of perjury, I declare (1) that I have examined this claim, including accompanying schedules and statements, and to the bestof my knowledge and belief, it is true, correct, and complete, and (2) that amounts claimed on this form have not been, and will not be, claimedon any other form.

Signature and title (if applicable)

Date

Type or print your name below signature.

Cat. No. 20027J

Form 8849 (Rev. 10-2006)

Print clearly. Leave a blank box between words.

Daytime telephone number (optional)

Check (u) the appropriate box(es) for the schedule(s) you attach to Form 8849. Only attach the schedules on which you are claiming a refund. Schedules 2, 3, 5, and 8 cannot be filed with any other schedules on Form 8849. File each of these schedules with aseparate Form 8849.

Schedule 8

Registered Credit Card Issuers

Page 2 Form 8849 (Rev. 10-2006)

General Instructions Section references are to the Internal Revenue Code.

Additional Information ● Pub. 510, Excise Taxes for 2006, has moreinformation on nontaxable uses, and the definitions ofterms such as ultimate vendor and blocked pump.Pub. 510 also contains information on fuel tax creditsand refunds previously in Pub. 378.

Use Schedule 6 for claims not reportable onSchedules 1, 2, 3, 5, and 8, including refunds of excisetaxes reported on: ● Form 720, Quarterly Federal Excise Tax Return;

How To Fill In Form 8849 Name and Address Print the information in the spaces provided. Beginprinting in the first box on the left. Leave a blank boxbetween each name and word. If there are not enoughboxes, print as many letters as there are boxes. Usehyphens for compound names; use one box for eachhyphen. P.O. box. If your post office does not deliver mail toyour street address and you have a P.O. box, showyour box number instead of your street address. Foreign address. Enter the information in the followingorder: city, state or province, and the name of thecountry. Follow the country’s practice for entering thepostal code. Do not abbreviate the country’s name. Taxpayer Identification Number (TIN) Enter your employer identification number (EIN) in theboxes provided. If you are not required to have an EIN,enter your social security number (SSN). An incorrector missing number will delay processing your claim. Month Income Tax Year Ends Enter the month your income tax year ends. Forexample, if your income tax year ends in December,enter “12” in the boxes. If your year ends in March,enter “03”.

● Form 11-C, Occupational Tax and RegistrationReturn for Wagering; or ● Form 2290, Heavy Highway Vehicle Use Tax Return.

● Form 730, Monthly Tax Return for Wagers;

Filers only need to complete and attach to Form 8849the applicable schedules. Do not use Form 8849:

● To make adjustments to liability reported on Forms720 filed for prior quarters. Instead, use Form 720X. ● To claim amounts that you took or will take as acredit on Schedule C (Form 720), Form 730, Form2290, or Form 4136.

What’s New

● Schedules 1, 2, 3, and 6 have all been revised basedon the Safe, Accountable, Flexible, & EfficientTransportation Equity Act of 2005 (SAFETEA); theEnergy Policy Act of 2005; and the Pension ProtectionAct of 2006.

● New Schedule 8, Registered Credit Card Issuers, isused by registered credit card issuers to make a claimfor a refund or payment of the tax paid on certain salesof taxable fuel to states and local governments andcertain sales of gasoline to nonprofit educationalorganizations after December 31, 2005.

You may also call the business and specialty tax lineat 1-800-829-4933 with your excise tax questions.

Purpose of Form Use Schedules 1, 2, 3, 5, and 8 to claim certain fuelrelated refunds such as nontaxable uses (or sales) offuels. Form 8849 lists the schedules by number andtitle.

● Schedule 1 has been revised to include claims for thenontaxable use of a diesel-water fuel emulsion andalternative fuel.

● Schedule 3 is re-titled Certain Fuel Mixtures to reflectthe new claims for refund related to renewable dieselmixtures and alternative fuel mixtures. ● Schedule 6 has been revised to remove claims for thenontaxable use of a diesel-water fuel emulsion. Theseclaims are now made on Schedule 1.

● Pub. 225, Farmer’s Tax Guide, also includesinformation on credits and refunds for the federalexcise tax on fuels applicable to farmers.

Caution. A refund claim for the communications excisetax on nontaxable service billed after February 28,2003, and before August 1, 2006, cannot be made onForm 8849. See your income tax return for theprocedures to make this claim.

● Schedule 2 has been revised to include type of use11, Exclusive use by a qualified blood collectororganization, as an allowable sale of kerosene for use inaviation claimed on lines 3d and 3e.

● Schedule 6 has been revised to include claims for thealternative fuel credit under Form 720 for certain exemptentities.

● After December 31, 2006, qualified blood collectororganizations are exempt users of fuel taxed undersection 4081. Type of use 11, Exclusive use by aqualified blood collector organization, has been addedto the Type of Use Table on page 3. Two conditionsmust be met to apply for the credit. 1. The fuel is used for the organization’s exclusive

use in the collection, storage, or transportation ofblood. 2. The organization is registered by the IRS. Toapply for registration, see Form 637, Application forRegistration (For Certain Excise Tax Activities).

Page 3 Form 8849 (Rev. 10-2006)

Additional Information for Schedules 1, 2,and 3 Annual Claims If a claim was not made for any gallons during theincome tax year on Form 8849, an annual claim maybe made. Generally, an annual claim is made on Form4136 for the income tax year during which the fuelwas: ● Used by the ultimate purchaser;

● Sold by the registered ultimate vendor;

Type of Use 1

On a farm for farming purposes 2

Off-highway business use (for business use otherthan in a highway vehicle registered or requiredto be registered for highway use) (other than usein mobile machinery) 3

Export 4

In a boat engaged in commercial fishing 5

6

In certain intercity and local buses

7

In a qualified local bus

8

In a bus transporting students and employees ofschools (school buses)

9

For diesel fuel and kerosene (other thankerosene used in aviation) used other than as afuel in the propulsion engine of a train ordiesel-powered highway vehicle (but notoff-highway business use)

10

In foreign trade

11 12

Certain helicopter and fixed-wing aircraft uses Exclusive use by a qualified blood collectororganization (beginning after December 31, 2006)

17

In a highway vehicle owned by the UnitedStates that is not used on a highway Exclusive use by a nonprofit educationalorganization

In an aircraft or vehicle owned by an aircraftmuseum

Exclusive use by a state, political subdivision ofa state, or the District of Columbia

16

15

14

13

For use in the production of alternative fuel

Enter the period of the claim for each type of claimusing the MMDDYYYY format. For example, the firstquarter of 2007 for a calendar-year taxpayer would be01012007 to 03312007.

The following table lists the nontaxable uses of fuels.You must enter the number from the table in the Typeof Use column as required on Schedules 1 and 2.

Period of Claim

Type of Use Table

In military aircraft

No.

Type of Use 13 and 14. Generally, claims for sales ofdiesel fuel, kerosene, kerosene for use in aviation,gasoline, or aviation gasoline for the exclusive use of astate or local government (and nonprofit educationalorganization for gasoline or aviation gasoline) must bemade following the order below. 1. By the registered credit card issuer if the state orlocal government (or nonprofit educational organizationif applicable) used a credit card and the credit cardissuer meets the requirements discussed in theSchedule 8 (Form 8849) instructions. 2. By the registered ultimate vendor if the ultimatepurchaser did not use a credit card and the ultimatevendor meets the requirements discussed in theSchedule 2 (Form 8849) instructions. 3. By the ultimate purchaser if the ultimate purchaserused a credit card and neither the registered creditcard issuer nor the registered ultimate vendor iseligible to make the claim.

If you need more space for any line on a schedule (forexample, you have more than one type of use) preparea separate sheet with the same information. Includeyour name and TIN on each sheet you attach.

For additional requirements, see Pub. 510.

● Amount of refund.

Information for Completing Schedules Note. Your refund will be delayed or Form 8849 will bereturned to you if you do not follow the requiredprocedures or do not provide all the requiredinformation. See the instructions for each schedule. Complete each schedule and attach all informationrequested for each claim you make. Be sure to enteryour name and TIN on each schedule you attach.Generally, for each claim, you must enter the: ● Period of the claim.

● Rate (as needed). See the separate scheduleinstructions. ● Number of gallons.

● Item number (when requested) from the Type of UseTable below.

Signature Form 8849 must be signed by a person with authorityto sign this form for the claimant. Where To File ● For Schedules 1 and 6, mail Form 8849 to:

Internal Revenue ServiceCincinnati, OH 45999-0002 ● For Schedules 2, 3, 5, and 8, mail Form 8849 to: Internal Revenue ServiceP.O. Box 312Covington, KY 41012-0312 Caution. Private delivery services designated by the

IRS cannot deliver items to P.O. boxes. You must usethe U.S. Postal Service to mail any item to an IRS P.O.box address. For details on designated private deliveryservices, see Pub. 509, Tax Calendars for 2006. Including the Refund in Income Include any refund of excise taxes in your gross incomeif you claimed the amount of the tax as an expensededuction that reduced your income tax liability. Cash method. If you use the cash method and file aclaim for refund, include the refund amount in your grossincome for the tax year in which you receive the refund. Accrual method. If you use an accrual method, includethe amount of refund in gross income for the tax year inwhich you used the fuels (or sold the fuels if you are aregistered ultimate vendor or registered credit card issuer).

Page 4 Form 8849 (Rev. 10-2006)

If you have comments concerning the accuracy ofthese time estimates or suggestions for making theform and schedules simpler, we would be happy tohear from you. You can write to the Internal RevenueService, Tax Products Coordinating Committee,SE:W:CAR:MP:T:T:SP, 1111 Constitution Ave. NW,IR-6406, Washington, DC 20224. Do not send Form8849 to this address. Instead, see Where To File onpage 3.

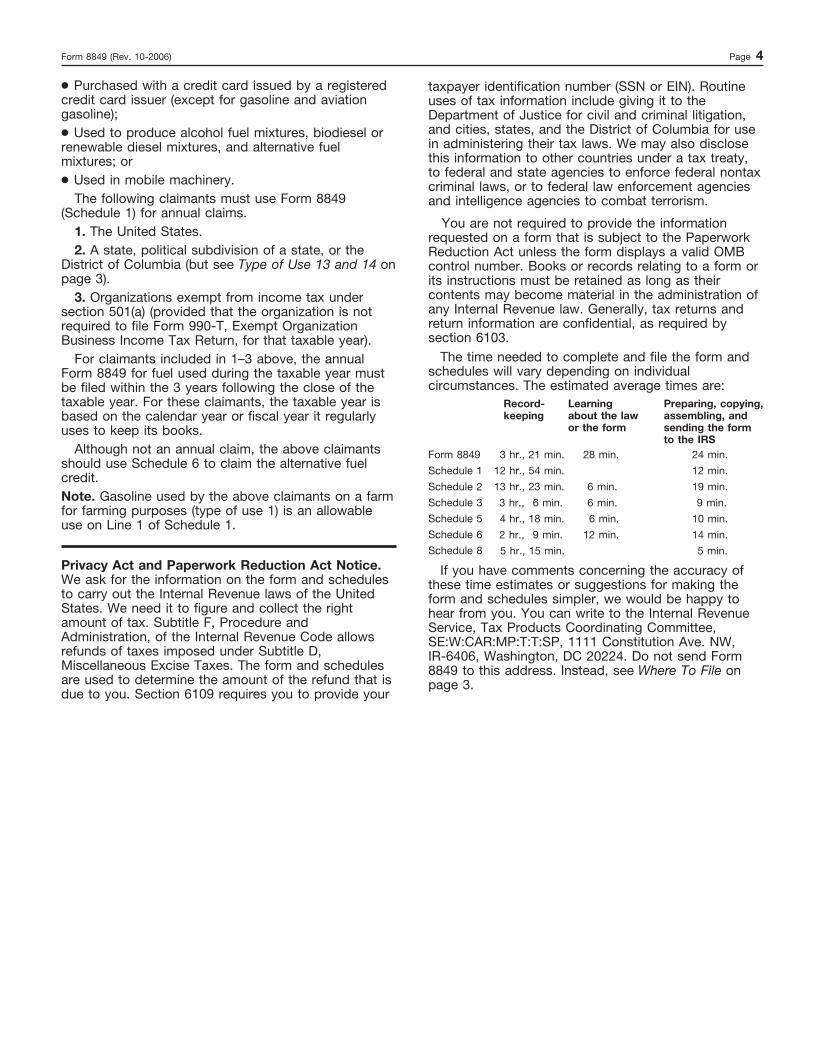

Record-keeping

Preparing, copying,assembling, andsending the form to the IRS

Learningabout the lawor the form

Schedule 1

Form 8849

Schedule 2 Schedule 3 Schedule 5 Schedule 6

12 hr., 54 min.

3 hr., 21 min.

13 hr., 23 min. 3 hr., 6 min. 4 hr., 18 min. 2 hr., 9 min.

28 min.

6 min.

6 min. 12 min.

12 min.

24 min.

19 min. 9 min. 10 min. 14 min.

6 min.

Schedule 8

5 hr., 15 min.

5 min. Privacy Act and Paperwork Reduction Act Notice.

We ask for the information on the form and schedulesto carry out the Internal Revenue laws of the UnitedStates. We need it to figure and collect the rightamount of tax. Subtitle F, Procedure andAdministration, of the Internal Revenue Code allowsrefunds of taxes imposed under Subtitle D,Miscellaneous Excise Taxes. The form and schedulesare used to determine the amount of the refund that isdue to you. Section 6109 requires you to provide your

You are not required to provide the informationrequested on a form that is subject to the PaperworkReduction Act unless the form displays a valid OMBcontrol number. Books or records relating to a form orits instructions must be retained as long as theircontents may become material in the administration ofany Internal Revenue law. Generally, tax returns andreturn information are confidential, as required bysection 6103. The time needed to complete and file the form andschedules will vary depending on individualcircumstances. The estimated average times are:

The following claimants must use Form 8849(Schedule 1) for annual claims. 1. The United States.

For claimants included in 1–3 above, the annualForm 8849 for fuel used during the taxable year mustbe filed within the 3 years following the close of thetaxable year. For these claimants, the taxable year isbased on the calendar year or fiscal year it regularlyuses to keep its books.

● Used to produce alcohol fuel mixtures, biodiesel orrenewable diesel mixtures, and alternative fuelmixtures; or

3. Organizations exempt from income tax undersection 501(a) (provided that the organization is notrequired to file Form 990-T, Exempt OrganizationBusiness Income Tax Return, for that taxable year).

2. A state, political subdivision of a state, or theDistrict of Columbia (but see Type of Use 13 and 14 onpage 3).

Note. Gasoline used by the above claimants on a farmfor farming purposes (type of use 1) is an allowableuse on Line 1 of Schedule 1.

● Used in mobile machinery.

● Purchased with a credit card issued by a registeredcredit card issuer (except for gasoline and aviationgasoline);

Although not an annual claim, the above claimantsshould use Schedule 6 to claim the alternative fuelcredit.

taxpayer identification number (SSN or EIN). Routineuses of tax information include giving it to theDepartment of Justice for civil and criminal litigation,and cities, states, and the District of Columbia for usein administering their tax laws. We may also disclosethis information to other countries under a tax treaty,to federal and state agencies to enforce federal nontaxcriminal laws, or to federal law enforcement agenciesand intelligence agencies to combat terrorism.

OMB No. 1545-1420

Nontaxable Use of Fuels (Rev. October 2006)

Schedule 1

Name as shown on Form 8849

Period of claim: Enter month, day, and yearin MMDDYYYY format.

(Form 8849) © Attach to Form 8849.

Total refund (see instructions)

Nontaxable Use of Aviation Gasoline Use in commercial aviation(other than foreign trade)

Nontaxable Use of Undyed Diesel Fuel

Nontaxable use

Use in trains (after December 31, 2006)

Kerosene Used in Commercial Aviation (Other Than Foreign Trade)

From ©

To ©

362

324

360 353

350

1

Nontaxable Use of Gasoline Gasoline (see Caution above line 1)

2

3

5

a

a

b

b c

Other nontaxable use (see Caution above line 1)

Claimant certifies that the diesel fuel did not contain visible evidence of dye. Exception. If any of the diesel fuel included in this claim did contain visible evidence of dye, attach a detailed explanationand check here ©

(c) Gallons

.183 .184

.15 .193

.243 .243 .22

.17

.200

$

$

Multiply col. (b) by col. (c)

$

EIN or SSN

$

$

$

$

354

417

Nontaxable Use of Undyed Kerosene (Other Than Kerosene Used in Aviation)

Nontaxable use

4 Claimant certifies that the kerosene did not contain visible evidence of dye.

Exception. If any of the kerosene included in this claim did contain visible evidence of dye, attach a detailed explanation and check here ©

Caution. Claims cannot be made on line 4 for kerosene sales from a blocked pump. Only registered ultimate vendors maymake those claims using Schedule 2.

.243

$

$

Use in trains (before January 1, 2007)

Caution. Claimant has the name and address of the person who sold the fuel to the claimant and the dates of purchase. Forclaims on lines 1a and 2b (type of use 13 and 14), 3e, 4c, and 5, claimant has not waived the right to make the claim. For claims on lines 1a and 2b (types of use 13 and 14), claimant certifies that a certificate has not been provided to the credit card issuer.

Department of the TreasuryInternal Revenue Service

a

.17

347

b

353

d

.243

c

© See instructions.

a b

Kerosene taxed at $.244 (see Caution above line 1) .175

$ Kerosene taxed at $.219 (see Caution above line 1)

$

a b

Exported

411

Exported

c

412

.194

Use on a farm for farming purposes

Use in certain intercity and local buses(see Caution above line 1)

e

Exported

f

.244

413

Use on a farm for farming purposes

.243

346

Use in certain intercity and local buses(see Caution above line 1)

d

.244

414

Exported

For Privacy Act and Paperwork Reduction Act Notice, see Form 8849 instructions.

Cat. No. 27449T

Schedule 1 (Form 8849) (Rev. 10-2006)

(a) Typeof use

(e)CRN

(d) Amount of refund (b) Rate

(c) Gallons

Multiply col. (b) by col. (c)

(a) Typeof use

(e)CRN

(d) Amount of refund (b) Rate

(c) Gallons

Multiply col. (b) by col. (c)

(a) Typeof use

(e)CRN

(d) Amount of refund (b) Rate

(c) Gallons

Multiply col. (b) by col. (c)

(e)CRN

(d) Amount of refund (b) Rate

%

355

%

Nontaxable Use of Liquefied Petroleum Gas (LPG) (before October 1, 2006)

6

a b

Use in certain intercity and local buses Use in qualified local buses and in school buses

361

.062 .136

$

$

352

.136

395

Other nontaxable use

c

Schedule 1 (Form 8849) (Rev. 10-2006)

Nontaxable Use of Alternative Fuel (after September 30, 2006)

7

419

Liquefied petroleum gas (LPG)

.183

$

$

a 420

“P Series” fuels

.183

b 421

Compressed natural gas (CNG) (GGE=126.67 cu. ft.)

.183

c 422

Liquefied hydrogen

.183

d

423

Any liquid fuel derived from coal (including peat)through the Fischer-Tropsch process

.243

e

424

Liquid hydrocarbons derived from biomass

.243

f 425

Liquefied natural gas (LNG)

.243

g

309

Nontaxable use

.197

$

$

a 306

Exported

.198

b

Nontaxable Use of a Diesel-Water Fuel Emulsion

8

415

Exported dyed diesel fuel

.001

$

$

a 416

Exported dyed kerosene

.001

b

Exported Dyed Fuel

9

(a) Typeof use

(e)CRN

(d) Amount of refundMultiply col. (b) by col. (c)

(b) Rate

(c) Gallons or gasolinegallon equivalents (GGE)

(a) Typeof use

(e)CRN

(d) Amount of refundMultiply col. (b) by col. (c)

(b) Rate

(c) Gallons

(a) Typeof use

(e)CRN

(d) Amount of refundMultiply col. (b) by col. (c)

(b) Rate

(c) Gallons

Page 2 Schedule 1 (Form 8849) (Rev. 10-2006)

(a) Typeof use

(e)CRN

(d) Amount of refundMultiply col. (b) by col. (c)

(b) Rate

(c) Gallons

Caution. There is a reduced credit rate for use in certain intercity and local buses (type of use 5). See page 4 for the credit rate.

Caution. There is a reduced credit rate for use in certain intercity and local buses (type of use 5). See page 4 for the credit rate.

Page 3 Schedule 1 (Form 8849) (Rev. 10-2006)

Instructions

The following requirements must be met.

a. Making a claim for fuel used during any quarter of aclaimant’s income tax year or b. Aggregating amounts from any quarters of theclaimant’s income tax year for which no other claim has beenmade. 2. The claim must be filed during the first quarter followingthe last quarter included in the claim. For example, a claimfor the quarters consisting of July through September andOctober through December must be filed between January 1and March 31.

Note. If requirements 1–3 above are not met, see AnnualClaims in the Form 8849 instructions.

Line 1. Nontaxable Use of Gasoline Allowable uses. For line 1a, the gasoline must have beenused during the period of claim for type of use 2, 4, 5, 7, 11,12, 13, 14, or 15. Type of use 2 does not include any personaluse or use in a motorboat. See Type of use 13 and 14 in theForm 8849 instructions.

Allowable uses. For line 2b, the aviation gasoline must havebeen used during the period of claim for type of use 9, 10,11, 13, 14, 15, or 16. See Type of use 13 and 14 in the Form8849 instructions.

Line 3. Nontaxable Use of Undyed Diesel Fuel Allowable uses. For line 3a, the diesel fuel must have been

used during the period of claim for type of use 2, 5, 6, 7, 8, 11,12, 13, 14, or 15. Type of use 8 includes use as heating oil anduse in a boat. Type of use 2 does not include any personal useor use in a motorboat. See Type of use 13 and 14 in the Form8849 instructions.

1. The amount claimed on Schedule 1 must be at least$750. This amount may be met by:

An ultimate purchaser of certain fuels uses Schedule 1 tomake a claim for refund. The fuels for which a claim can bemade are listed on the form. The fuel must have been usedin a nontaxable use. See Type of Use below and theinstructions for lines 1 through 9 for more information.

The fuel must have been used for one or more of the typesof use listed in the instructions for lines 1 through 4 and 6through 8. The nontaxable uses are listed in the Type of UseTable in the Form 8849 instructions.

Add all amounts in column (d) and enter the result in thetotal refund box at the top of the schedule.

Line 2. Nontaxable Use of Aviation Gasoline

3. Only one claim may be filed for a quarter.

Attach Schedule 1 to Form 8849. Mail to the IRS at theaddress under Where To File in the Form 8849 instructions.

Purpose of Schedule

Claim Requirements

Total Refund

Type of Use

How To File

Line 4. Nontaxable Use of Undyed Kerosene (OtherThan Kerosene Used in Aviation) Allowable uses. For line 4a, the kerosene must have beenused during the period of claim for type of use 2, 6, 7, 8, 11,12, 13, 14, 15, or 16. Type of use 8 includes use as heating oiland use in a boat. Type of use 2 does not include anypersonal use or use in a motorboat. See Type of use 13 and14 in the Form 8849 instructions.

What’s New ● Claims for the nontaxable use of alternative fuel afterSeptember 30, 2006, are made on line 7. ● After September 30, 2006, liquefied petroleum gas (LPG) isconsidered an alternative fuel. Claims for nontaxable use ofLPG before October 1, 2006, are made on line 6. If thenontaxable use occurs after September 30, 2006, the claimmust be made on line 7a. ● Claims for the nontaxable use of a diesel-water fuelemulsion are made on line 8. These claims were previouslymade on Schedule 6. However, the person claiming thecredit for production of the diesel-water fuel emulsion shouldcontinue to use Schedule 6. ● Claims for exported taxable fuel are made on lines 1b, 2c,3f, 4d, 9a, and 9b.

Exported taxable fuel. The claim rates for exported taxablefuel are listed on lines 1b, 2c, 3f, 4d, 9a, and 9b. Taxpayersmaking a claim for exported taxable fuel must include withtheir records proof of exportation. Proof of exportationincludes: ● A copy of the export bill of lading issued by the deliveringcarrier, ● A certificate by the agent or representative of the exportcarrier showing actual exportation of the fuel, ● A certificate of lading signed by a customs officer of theforeign country to which the fuel is exported, or ● A statement of the foreign consignee showing receipt ofthe fuel.

For line 1b, the gasoline must have been exported duringthe period of claim (Type of use 3). See Exported taxable fuelearlier.

For line 3f, the diesel fuel must have been exported duringthe period of claim (Type of use 3). See Exported taxable fuelearlier.

For line 2c, the aviation gasoline must have been exportedduring the period of claim (Type of use 3). See Exportedtaxable fuel earlier.

For line 4d, the kerosene must have been exported duringthe period of claim (Type of use 3). See Exported taxable fuelearlier.

● Claims by the ultimate purchaser, if eligible, for certainfuels used for type of use 13 and 14 are made on Schedule1. These claims were previously made on Schedule 6. Todetermine if the ultimate purchaser is eligible to make theseclaims, see Type of use 13 and 14 in the Form 8849instructions. ● After December 31, 2006, qualified blood collectororganizations are exempt users of fuel taxed under section4081. Type of use 11, Exclusive use by a qualified bloodcollector organization, has been added to the Type of UseTable in the Form 8849 instructions. Two conditons must bemet to apply for the credit. 1. The fuel is used for the organization’s exclusive use inthe collection, storage, or transportation of blood. 2. The organization is registered by the IRS. To apply forregistration, see Form 637, Application for Registration (ForCertain Excise Tax Activities).

Page 4 Schedule 1 (Form 8849) (Rev. 10-2006)

Line 8. Nontaxable Use of a Diesel-Water FuelEmulsion

Allowable uses. The taxed alternative fuel must have beenused after September 30, 2006, for type of use 1, 2, 4, 5, 6,7, 11, 13, 14, or 15.

Allowable uses. For line 8a, the diesel-water fuel emulsionmust have been used during the period of claim for type ofuse 1, 2, 5, 6, 7, 8, 11, 12, 13, 14, or 15. For line 8b, thediesel-water fuel emulsion must have been exported duringthe period of claim (Type of use 3). See Exported taxable fuelon page 3.

Line 9. Exported Dyed Fuel

Line 7. Nontaxable Use of Alternative Fuel (afterSeptember 30, 2006)

A claim may be made for dyed diesel fuel or dyed kerosene exportedin a trade or business during the period of claim. See Exportedtaxable fuel on page 3.

Type of use 5. Write “Bus” in the space to the left of column(a). Enter the correct credit rate in column (b). The credit ratesfor type of use 5 are listed below.

Type of use 5. Write “Bus” in the space to the left of column (a).Enter the correct credit rate in column (b). The credit rate for type ofuse 5 is $.124 per gallon.

14b

Credit rate

14c 14d

14f

14e

14g

Line number 14a

*This is the credit rate per gasoline gallon equivalent (126.67 cubic feet of CNG).

$.109 .110

.109* .110 .17 .17 .169

Line 6. Nontaxable Use of Liquefied Petroleum Gas(LPG) (before October 1, 2006) Allowable uses. For line 6c, the taxed LPG (such as propaneor butane) must have been used during the period of claimfor type of use 1, 2, 4, 13, 14, or 15.

Line 5. Kerosene Used in Commercial Aviation (Other Than Foreign Trade) Allowable uses. For lines 5a and 5b, claimant certifies thatthe right to make the claim has not been waived. If theclaimant buys kerosene partly for use in commercial aviationand partly for use in noncommercial aviation, see the rules inNotice 2005-80, section 3(e)(3). Only one claim may be filedwith respect to any gallon of kerosene used in commercialaviation.

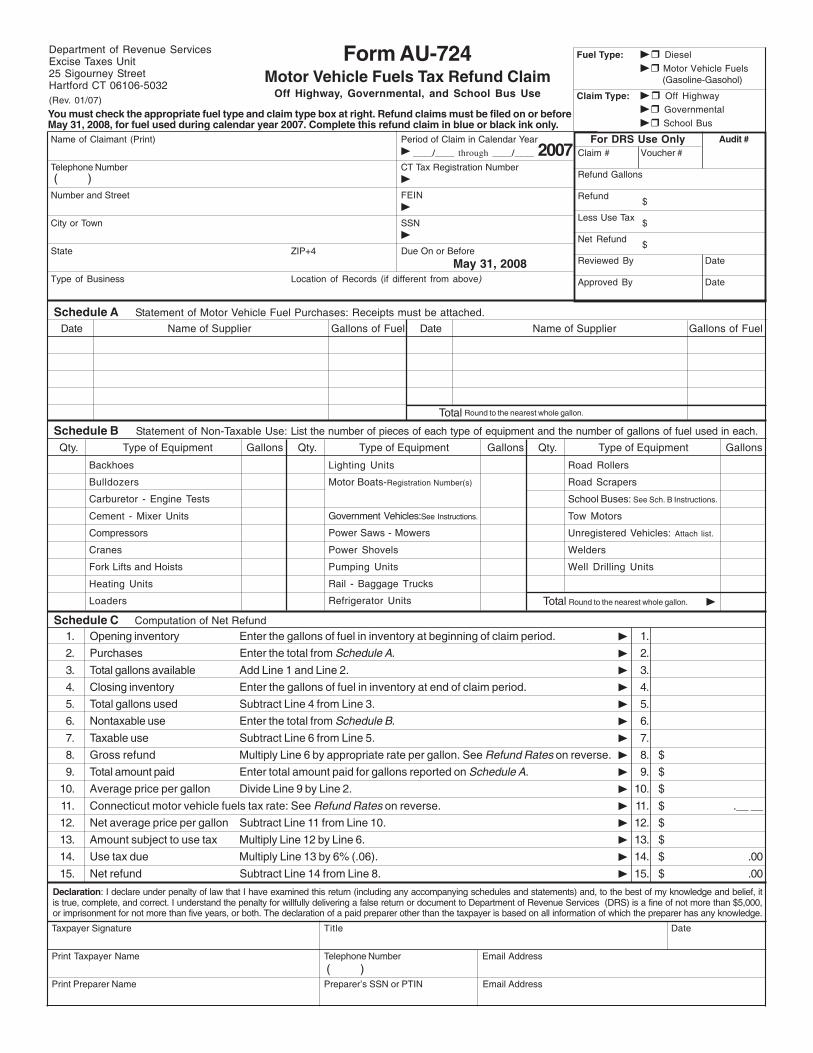

Schedule B Statement of Non-Taxable Use: List the number of pieces of each type of equipment and the number of gallons of fuel used in each.

Lighting Units

Motor Boats-Registration Number(s)

Government Vehicles:See Instructions.

Power Saws - Mowers

Power Shovels

Pumping Units

Rail - Baggage Trucks

Refrigerator Units

Road Rollers

Road Scrapers

School Buses: See Sch. B Instructions.

Tow Motors

Unregistered Vehicles: Attach list.

Welders

Well Drilling Units

Qty. Type of Equipment Gallons Qty. Type of Equipment Gallons Qty. Type of Equipment Gallons

Backhoes

Bulldozers

Carburetor - Engine Tests

Cement - Mixer Units

Compressors

Cranes

Fork Lifts and Hoists

Heating Units

Loaders �

Declaration: I declare under penalty of law that I have examined this return (including any accompanying schedules and statements) and, to the best of my knowledge and belief, itis true, complete, and correct. I understand the penalty for willfully delivering a false return or document to Department of Revenue Services (DRS) is a fine of not more than $5,000,or imprisonment for not more than five years, or both. The declaration of a paid preparer other than the taxpayer is based on all information of which the preparer has any knowledge.

Taxpayer Signature Title Date

Print Taxpayer Name Telephone Number Email Address

Print Preparer Name Preparer’s SSN or PTIN Email Address

Total Round to the nearest whole gallon.

( )

Name of Claimant (Print) Period of Claim in Calendar Year

Telephone Number CT Tax Registration Number

Number and Street FEIN

City or Town SSN

State ZIP+4 Due On or Before

Type of Business Location of Records (if different from above)

Department of Revenue ServicesExcise Taxes Unit25 Sigourney StreetHartford CT 06106-5032(Rev. 01/07)

( )

�

�

�

�

May 31, 2008

Form AU-724Motor Vehicle Fuels Tax Refund Claim

Off Highway, Governmental, and School Bus Use

Audit #For DRS Use OnlyClaim # Voucher #

Refund Gallons

Refund

Less Use Tax

Net Refund

Reviewed By Date

Approved By Date

You must check the appropriate fuel type and claim type box at right. Refund claims must be filed on or beforeMay 31, 2008, for fuel used during calendar year 2007. Complete this refund claim in blue or black ink only.

Fuel Type: �� Diesel

�� Motor Vehicle Fuels (Gasoline-Gasohol)

Claim Type: �� Off Highway

�� Governmental

�� School Bus

2007

$

$

$

____/____ through ____/____

Date Name of Supplier Gallons of Fuel Date Name of Supplier Gallons of Fuel

Schedule A Statement of Motor Vehicle Fuel Purchases: Receipts must be attached.

Total Round to the nearest whole gallon.

1. Opening inventory Enter the gallons of fuel in inventory at beginning of claim period. 1.

2. Purchases Enter the total from Schedule A. 2.

3. Total gallons available Add Line 1 and Line 2. 3.

4. Closing inventory Enter the gallons of fuel in inventory at end of claim period. 4.

5. Total gallons used Subtract Line 4 from Line 3. 5.

6. Nontaxable use Enter the total from Schedule B. 6.

7. Taxable use Subtract Line 6 from Line 5. 7.

8. Gross refund Multiply Line 6 by appropriate rate per gallon. See Refund Rates on reverse. 8. $

9. Total amount paid Enter total amount paid for gallons reported on Schedule A. 9. $

10. Average price per gallon Divide Line 9 by Line 2. 10. $

11. Connecticut motor vehicle fuels tax rate: See Refund Rates on reverse. 11. $ .__ __

12. Net average price per gallon Subtract Line 11 from Line 10. 12. $

13. Amount subject to use tax Multiply Line 12 by Line 6. 13. $

14. Use tax due Multiply Line 13 by 6% (.06). 14. $ .00

15. Net refund Subtract Line 14 from Line 8. 15. $ .00

Schedule C Computation of Net Refund

�

�

�

�

�

�

�

�

�

�

�

�

�

�

�

You must use black or blue ink to complete your return.

Use Form AU-724, Motor Vehicle Fuels Tax Refund Claim, tofile a motor vehicle fuels tax refund claim for diesel or motorvehicle fuels, gasoline - gasohol:

a. Used by the United States, the State of Connecticut, or amunicipality of the State of Connecticut;

b. Used in any school bus, as defined in Conn. Gen. Stat.§14-275; or

c. Used for off highway use.

The appropriate fuel type and claim type box must be markedon the front of this form in order to process this claim. Youmust file a separate Form AU-724 for each motor vehicle fueltype and claim type.

Your motor vehicle fuels tax refund claim for fuel used duringcalendar year 2007 must:

1. Be filed with DRS on or before May 31, 2008; and

2. Involve at least 200 gallons of fuel eligible for tax refund.

Be sure to provide a telephone number where you can becontacted.

You must indicate your Connecticut Tax Registration Number,Federal Identification Number (FEIN), or Social SecurityNumber (SSN) in the space provided.

For all purchases reported on Line 2, you must attach a copyof each numbered slip or invoice issued at the time of thepurchase. The slip or invoice may be the original or a photocopyand must show the:

• Date of purchase;

• Name and address of the seller which must be printed orrubber stamped on the slip or invoice;

• Name and address of the purchaser which must be thename and address of the person or entity filing the claimfor refund;

• Number of gallons of fuel purchased;

• Price per gallon;

• Total amount paid; and

• If payment is made within a discounted period, provideproof of amount paid.

You must retain records to substantiate your refund claim forat least three years following the filing of the claim and makethem available to DRS upon request.

Mail the completed refund application to:

Department of Revenue ServicesExcise Taxes Unit25 Sigourney StreetHartford CT 06106-5032

Schedule A InstructionsIndicate the date of purchase, name of the supplier, and numbergallons of fuel purchased. Round the total line to the nearestwhole gallon.

Instructions

Form AU-724 Back (Rev. 01/07)

Schedule B Instructions1. Enter the quantity of each type of equipment and total

number of gallons used in each.

2. Enter a registration number for all motor boats you list.

3. The school bus refund is for any school bus, as defined inConn. Gen. Stat. §14-275.

4. Total gallons, rounding to the nearest whole gallon. Enterzero if less than 200 gallons.

Schedule C InstructionsPurchases of fuel on which a motor vehicle fuels tax refundclaim is allowed are subject to Connecticut use tax at the taxrate in effect at the time of the purchase. Use tax is calculatedon the price paid per gallon less the Connecticut motor vehiclefuels tax rate. You must determine your Connecticut use taxliability on such purchases by completing Schedule C.

Specific Line InstructionsLine 14 and Line 15 only - Rounding Off to Whole Dollars:You must round off cents to the nearest whole dollar on yourmotor vehicle fuels tax refund claim. Round down to the nextlowest dollar all amounts that include 1 through 49 cents. Roundup to the next highest dollar all amounts that include 50 through99 cents. However, if you need to add two or more amounts tocompute the total to enter on a line, include cents and roundoff only the total. If you do not round, DRS will disregard thecents.

Example: Add two amounts ($1.29 + $3.21) to compute thetotal ($4.50) to enter on a line. $4.50 is rounded to $5.00 andentered on the line.

If you claim exemption from the Connecticut use tax becausethe fuel was used and consumed directly in manufacturing orcommercial fishing, you must send the appropriate exemptioncertificate with each refund claim filed.

Additional InformationIf you need additional information or assistance, call theExcise Taxes Unit at 860-541-3224, Monday through Friday,8:30 a.m. to 4:30 p.m. Visit the DRS website atwww.ct.gov/DRS to download and print Connecticut taxforms.

Your refund will be applied against any outstandingDRS tax liability.

2007 Motor Vehicle Fuels Tax Refund Rates

January 1, 2007 through December 31, 2007

Diesel ...................................26¢ per Gallon

Motor Vehicle Fuels ...........25¢ per Gallon

Note: You must file a separate Form AU-724 for each motorvehicle fuel type and each claim type.