f&i and showroom february 2011

DESCRIPTION

The industry’s leading source for F&I, sales and technologyTRANSCRIPT

WELCOME TO

THE

Learn How Bethany Johnson, Jon Hazelwood and the Rest of the RBM North Team Powered Through Early Challenges

to Become One of Their City’s Top High-Line Dealerships

Take an Exclusive Look Inside the Playbook of All-Star Special Finance Manager Greg Alore

New to Automotive Finance? Expert Breaks Down 10 Rules No F&I Manager Can Ignore

FEBRUARY 2011 $10.00

A BOBIT PUBLICATION FI-MAGAZINE.COM

WHAT A

EDITOR: THE EVIDENCE ‘GAP’ | MAD MARV: CHARGE-BACK CONTROL | LEGAL: BRAVE NEW WORLD

FI0211cover.indd 991FI0211cover.indd 991 2/2/11 2:06:37 PM2/2/11 2:06:37 PM

FI0211cna.indd 2-3 1/26/11 12:08:10 PMFI0211cover.indd 992FI0211cover.indd 992 1/31/11 4:07:02 PM1/31/11 4:07:02 PM

FI0211cna.indd 2-3 1/26/11 12:08:10 PMFI0211cover.indd 1FI0211cover.indd 1 1/31/11 4:07:02 PM1/31/11 4:07:02 PM

2 F&I and Showroom February 2011

February 2011 Volume 14, Issue 2

Dealer Profi le

12 Climb to the TopRBM North overcame an undeveloped market and stiff competition to become one of the top-rated high-line dealerships in the greater Atlanta area.

Finance and Insurance

18 F&I’s 10 CommandmentsStarting out in F&I is never easy, but the magazine’s resident expert lays out a game plan to get F&I “newbies” off on the right foot.

Q&A

24 Product PlacementShould the base payment be displayed on the menu? Offi cials with IAS offer their take on that hot-button issue and more.

Special Finance

26 Go Long!At Longmont Ford, Greg Alore relies on a roster of lenders, lead providers and satisfi ed customers to help his special fi nance team rack up hall-of-fame numbers.

Dealer Management

30 Pay Plan RebootThe Department of Labor is gearing up. The question is, will your pay plans be ready? Here’s a primer to help you get them up to speed.

4 Letters

6 Editorial Page

8 Developments

34 Sales Driver

36 Mad Marv

38 Legal

39 Bottomliners

40 Ad Index

44 Industry Trends

Departments

Features

F&I and Showroom (ISSN 2154-1728) (USPS 018-706) (CDN IPM# 40013413) is published monthly, by Bobit Business Media, 3520 Challenger Street, Torrance, California 905031-1640. Periodicals Postage Paid at Torrance, California 90503-9998 and additional mailing offi ces. POSTMASTER: Send address changes to F&I and Showroom, P.O. Box 1068 Skokie, IL 60076-8068. Please allow six to eight weeks for address changes to take effect. Subscription Prices: United States $20 per year; Canada $35 per year; Foreign: $35 per year. Single copy price: $10; Fact Book: $30. Please allow six to eight weeks to receive your fi rst issue. Bobit Business Media reserves the right to refuse nonqualifi ed subscriptions. Please address editorial and advertising correspondence to the executive offi ces at 3520 Challenger Street, Torrance, California 90503-1640. The contents of this publication may not be reproduced either in whole or in part without the consent of Bobit Business Media. All statements made, although based on information believed to be reliable and accurate, cannot be guaranteed and no fault or liability can be accepted for error or omission.

12

30

26

Contents Endorsed as the offi cial publication

of the Association of Finance & Insurance Professionals

18

FI0211toc.indd 2FI0211toc.indd 2 1/31/11 3:47:46 PM1/31/11 3:47:46 PM

�������*OOPWBUJWF�"GUFSNBSLFU�4ZTUFNT�-�1��"MM�3JHIUT�3FTFSWFE�

&RQWDFW�,$6�6DOHV�DW��������������[�����RU�YLVLW�ZZZ�LDVGLUHFW�FRP�IRU�PRUH�LQIRUPDWLRQ�

4HE�"ENEÚTS�OF�)!3�2EINSURANCE�ARE�#LEAR�

� r�������������RI�XQGHUZULWLQJ�SURILWV�DQG������RI�LQYHVWPHQW�LQFRPH�

� r��������&UHDWHV�DQ�DVVHW�WKDW�\RX�RZQ��1RW�D�UHWUR�RU�VHOI�LQVXUHG�

� r��������8QSDUDOOHOHG�SHUVRQDO�ZHDOWK�EXLOGLQJ�RSSRUWXQLW\�

� r��������&UHDWH�D�QHZ�FRPSDQ\�RU�UHLQVXUH�,$6�SURJUDPV�LQWR�DQ�H[LVWLQJ�FRPSDQ\�

� r��������,$6�SURJUDPV�DUH�IXOO\�LQVXUHG�E\�D�PXOWL�ELOORQ�GROODU�EHVW�UDWLQJ�RI�p$q��H[FHOOHQW��E\�$�0��%HVW�&RPSDQ\�

%LIGIBLE�0RODUCTS�)NCLUDE�

7KUO3^�,KXU3^�5OOZ3^�

� r� *$3�3URWHFWLRQ � r� :LQGVKLHOG�5HSDLU�RU�5HSODFHPHQW

� r� 7LUH��:KHHO�5RDG�+D]DUG � r� .H\�5HSODFHPHQW

� r� (WFK���7KHIW � r� 3DLQWOHVV�'HQW�5HSDLU�3URWHFWLRQ

� r� 3DLQW���)DEULF���/HDWKHU � r� 0XOWL�6KLHOG

FI0211toc.indd 3FI0211toc.indd 3 1/31/11 3:47:49 PM1/31/11 3:47:49 PM

The End of Sales vs. FinanceTO “MAD” MARV ELEAZER: Your De-

cember column (“Who Needs ’Em?”)

couldn’t be more spot on. I have been

a fi nance manager for 28 years and

have gone from being really diffi cult

with salespeople to having a very

good relationship with them. We’ve

realized that we have to work to-

gether in order to deliver a vehicle,

because, as you said, if the sales

force and F&I manager can’t work

together, it will surely spell doom for

the sales process.

Harvey CoopersmithBusiness Manager

Mercedes-Benz of Atlantic City (N.J.)

Thanks for the note, Harvey! I too have sown bad seeds that I’m still reaping. But I press onward, realiz-ing it’s not about me. I can’t tell you how much I appreciate when a sales-person gets excited over a deal I put together that he or she would never have been able to do. Sales staffers are real people who need manage-rial involvement — not managerial bullying. — Marv Eleazer

Compliance Survives When Deals DieTO MICHAEL BENOIT: At my dealership,

we scan completed and delivered

deal jackets and will soon be scan-

ning “dead” fi les. I have a couple of

questions about this process:

■ If we scan a deal jacket contain-

ing a customer’s personal informa-

tion, how long do I need to keep the

paper fi le before I can shred it?

■ Do I still have to keep the paper

fi le even if I have an electronic fi le

that follows state and federal record-

keeping guidelines?

I have visited the Federal Trade

Commission’s Website and other

resource sites, but I can’t get a clear

answer.

Vern SternCompliance Manager

Dave Smith Motors Kellogg, Idaho

Vern, the only issue is whether a state law requires the retention of “origi-nals.” This is true in the case of install-ment sale contracts in some states (i.e., the fi nance company that bought the contract might be required to re-turn the “original” marked “paid” to the buyer). That wouldn’t gener-ally apply in a deal jacket, except in a buy-here, pay-here or related fi nance company situation.

Your question requires answers as to what’s permitted in Idaho. Most states’ “rules of evidence” will per-mit you to use a scanned copy as the “best evidence” available when the originals have been destroyed. Your corporate counsel should know if this is the case in Idaho.

Counsel also should review the Idaho Credit Code for retention re-quirements relating to credit sale documents. Idaho’s dealer code also may indicate a restriction on scan-ning and destroying originals.

Federal law doesn’t restrict the practice of scanning and destroy-ing originals; however, you’ll want to verify with your counsel that the federal rules of evidence allow you to present scans as evidence in litigation. — Michael Benoit

New Rule, No ProblemTO THE EDITOR: Greg, you were right

on with your January editorial on the

Risk-Based Pricing Rule. It has been

a non-issue so far. I give customers

the exception, explain what it is, ask

them if they have any questions and

proceed with the delivery.

Recently, I had a customer trade

in a car she bought last August. Her

score had dropped and I couldn’t get

her the same rate. We reviewed her

sheet and old deal, and saw that she

had added $6,000 in credit card debt.

“Oh, I understand,” she said. It was

only a quarter point, but it defused an

argument over $7 per month and gave

me credibility.

Tom BrenholtsNationwide Car Sales

Wilkes-Barre, Pa.

Letters

4 F&I and Showroom February 2011

Vice President Group Publisher, Auto Group

Sherb Brown

Publisher, Dealer GroupNational Sales Manager

David Gesualdo727-947-4027

Executive EditorGregory Arroyo

Managing Editor / Art DirectorTariq Kamal

Senior EditorJustina Ly

Great Lakes Sales ManagerRobert Brown Jr.

Sales & Marketing CoordinatorTracey Tremblay

E-Media and Print Production Manager

Brian Peach310-533-2548

Web ManagerSam Kim

Audience Marketing ManagerTony Napoleone

Chairman Edward J. Bobit

President & CEOTy F. Bobit

Chief Financial Offi cerRichard E. Johnson

Business and Editorial Offi ceBobit Business Media3520 Challenger St.Torrance, CA 90503

Phone: 310-533-2400Fax: 310-533-2503

Change Service RequestedReturn Address:

Bobit Business MediaPO Box 2703

Torrance, CA 90509

Subscription Inquiries888-239-2455

Printed in U.S.A.

FI0211letters.indd 4FI0211letters.indd 4 2/2/11 9:35:36 AM2/2/11 9:35:36 AM

Lifetime Engine Warranty, Limited Warranty, Vehicle Service Contracts (VSCs) and GAP are backed by Lyndon Property Insurance Company in all states except NY. In NY, VSCs are backed by Old Republic Insurance Company. GAP, Lifetime Engine Warranty and Limited Warranty are not available in NY. Credit Insurance is backed by Protective Life Insurance Company in all states except NY, where it is backed by Protective Life and Annuity Insurance Company.

Vehicle Service Contracts I GAP Coverage I Credit Insurance

Lifetime Engine Warranty I Limited Warranty I Dealer Participation Programs

F&I Training I Advanced F&I Technology

888.276.0195www.protectiveassetprotection.com

We Listen • We Care • We Have Solutions

Call us today to get TSP installed in your dealership!

Looking to increase revenue with your service department?

Your solution is our TSP Vehicle Service Contract Program!TSP is sold exclusively in the service department.

To learn more about TSP go to www.youtube.com and type “Total Service Protection Video” (including quotation marks) in the search field.

We provide your service department with a

“turn-key” solution.

Call us today to schedule

your appointment for a Protective

representative to visit your dealership!

FI0211letters.indd 5FI0211letters.indd 5 2/2/11 9:35:38 AM2/2/11 9:35:38 AM

Au

6 F&I and Showroom February 2011

Imagine making a major business

decision based on how 18 people

responded to a survey. Pretty ir-

responsible, right? Well, the Federal

Reserve Board doesn’t think so. In

fact, that’s exactly what it’s doing

with its newly proposed disclosure

requirements under the Truth in

Lending Act’s Regulation Z, which,

if you hadn’t heard, will impact your

ability to sell credit insurance, GAP

and debt cancellation agreements.

The study in question was con-

ducted by Calverton, Md.-based ICF

Macro. The results, released last July,

helped Fed offi cials craft new dis-

closures for selling loan protection

products. The problem, as Michael

Benoit, the magazine’s Legal colum-

nist, puts it, is that they’re basically

“designed to convince your custom-

ers not to buy them.”

He’s right. In fact, one of the pro-

posed disclosures reads in big bold

letters: “You may not receive any ben-

efi ts even if you buy this product.” My

favorite is the one that reads: “Other

types of insurance can give you simi-

lar benefi ts and are often less expen-

sive.” Again, 18 people helped the Fed

come to its conclusions.

What’s even more amazing is the

study was focused mainly on credit

insurance for home mortgages. In

other words, respondents weren’t

shown GAP or debt cancellation

agreements. In fact, only one of the

18 respondents indicated that he was

familiar with credit life insurance “in

the context of car loans.” My ques-

tion is: When will regulators under-

stand that it wasn’t the auto business

that sent the economy and the credit

markets into a tailspin?

Look, I’m all about dumbing down

disclosures a bit so you don’t need a

law degree to understand them, but

come on. And why not allow the Fed-

eral Trade Commission and the new

Consumer Financial Protection Bu-

reau handle this? Well, truth is, the

Fed has been in the process of review-

ing Regulation Z since 2004. It’s goal

is to ensure that disclosures the rule

requires are structured and worded in

such a way that consumers can easily

understand them and use them in their

fi nancial decision making. Still, how

can you come to a conclusion based

on a survey that doesn’t mention all of

the products you aim to regulate?

To be fair, there were some eye-

opening fi ndings. In fact, I think most

of us would be willing to help fi x the

problems the study identifi ed.

For instance, only fi ve out of 10

interviewees questioned in Phoenix

last March understood that credit

insurance was not required on their

line of credit. Additionally, only half

understood that there was a cap on

their benefi ts. That’s fi xable, right?

Now, I think I fi gured out why the

Fed and its new disclosures took on

the tone they took. See, when eight

out of 10 respondents said they were

surprised to learn that they may not

realize the benefi ts of credit insur-

ance even after purchasing it and

making payments for a number of

years, many of them indicated that

knowing that made them less likely

to purchase the products.

So, when ICF Macro took its fi nd-

ings to Memphis for its second round

of interviews on April 16, it showed

interviewees its new “You may not

receive any benefi ts even if you buy”

disclosure. Well, guess how respon-

dents reacted? Yup, they weren’t in-

terested in the product. But is that full

disclosure? And was that the intent of

the study?

Again, I think I’m OK with review-

ing regs to make sure they’re working

as intended, but can we make sure all

parties are considered and that regu-

lator A is talking to regulator B?

Take what’s happening in Califor-

nia, where what seemed like a harm-

less Omnibus Bill (AB 2782) is now

threatening a key GAP benefi t — de-

ductible coverage. See, the bill was in-

tended to get the state in line with the

Producer Licensing Model Act. How-

ever, when the state’s dealer associa-

tion asked the California Department

of Insurance to clarify what was con-

sidered credit insurance, the agency, in

its response, said GAP waivers could

not cover a customer’s deductible.

San Diego-based OwnerGUARD

is on the case. The F&I product pro-

vider is working with the agency

and the state’s dealer association on

fi xer legislation, but there are several

hurdles standing in the way. The best

case scenario is to get something

through the legislature by June.

In the meantime, GAP provid-

ers are racing to get their forms up

to speed with the new law. Luckily,

the insurance agency has delayed

enforcement of the new requirement,

which went into effect on Jan. 1,

through March 31.

Remember when I wrote in De-

cember that we’re heading into a new

period of rulemaking? Well, welcome

to the party. But instead of complain-

ing, it’s time to get active, especially

those of you in California.

Fed Proposal Reveals Evidence GAP

Letter from the Editor

The Fed sure isn’t hiding its disdain for credit insurance with its proposed changes to Reg. Z. Then again, it might just be an information gap at work. By Gregory Arroyo

FI0211editor.indd 6FI0211editor.indd 6 1/28/11 4:12:32 PM1/28/11 4:12:32 PM

Automotive News – Full Page Ad Trim Size: 10.875 x 14.5 (Bleed Size: 11.125 x 14.75)

TM

.BLJOH�0VSTFMWFT�7BMVBCMF��UP�:06�&WFSZEBZ�SM

.BYJNJ[F�ZPVS�QSPGJUT�XJUI�/"$ �UIF�MFBEFS�JO�TBMFT�BOE�BENJOJTUSBUJPO�PG�NBSLFU�SFBEZ�WFIJDMF�TFSWJDF�DPOUSBDUT�BOE�NPSF�

4UBSU�ZPVS�XJOOJOH�TFBTPO�XJUI�/"$μT�JOOPWBUJWF�WFIJDMF�TFSWJDF�BHSFFNFOU�MJOFVQ �MJHIUFOJOH�GBTU�POMJOF�

DPOUSBDUJOH�BOE�SFTQPOTJWF�USBJOJOH �DPOTVMUJOH�BOE�TVQQPSU�

"U�/"$ �JUμT�BCPVU�XIBU�:06�OFFE�

UP�CF�TVDDFTTGVM�°�EJSFDU�BDDFTT�UP�

EFDJTJPO�NBLFST �SFTQPOTJWF�TUBGG �

RVJDL�DMBJNT�QBZNFOUT�°�BOE�UIF�BHJMJUZ �

GMFYJCJMJUZ�BOE�²DBO�EP³�BUUJUVEF�UIBU�XJMM�

ESJWF�OFX�BOE�QSPGJUBCMF�HSPXUI�GPS�

ZPV�BOE�ZPVS�DMJFOUT�

$BMM�/"$�OPX�BU��������������PS�WJTJU�OBDTPMVUJPO�DPN�BOE�QPTJUJPO�ZPVSTFMGUP�TVDDFFE�BOE�XJO�

+PJO�/"$μT�XJOOJOH�UFBN�BOEHFU�JO�QPTJUJPO�UP�TDPSF�#*(�QSPGJUT�

FI0211editor.indd 7FI0211editor.indd 7 1/28/11 4:12:33 PM1/28/11 4:12:33 PM

Prices Fall, Incentives Increase for DecemberTRUECAR.COM HAS ESTIMATED

that the average transaction price for light vehicles in the United States was $29,358 in December 2010, down $276 (0.9 percent) from December 2009 and down $95 (0.3 per-cent) from November 2010.

The estimated average transaction price for all vehicle types was $29,070 in 2010, up 4.7 percent from 2009’s aver-age transaction price of $27,757.

GAP providers in California

are racing to notify deal-

ers that one of the key sell-

ing features of GAP might be barred

since a new law took effect on Jan. 1.

In late September, Gov. Arnold

Schwarzenegger signed AB 2782

into law. The Omnibus bill included

a new licensing requirement for sell-

ers of accident and health insurance.

How GAP got thrown in is a case of

unintended consequences.

According to executives at San Di-

ego-based OwnerGUARD, the state

dealership association asked the Cal-

ifornia Department of Insurance to

clarify whether a GAP waiver would

fall under the new requirement. In its

response, the state agency said GAP

waivers could not cover a customer’s

deductible.

Fortunately for the industry, the

state’s department of insurance has

delayed enforcement of the new law

because many broker agents were un-

aware of the new requirement.

“GAP sales can continue, but the

law is what the law is,” said Michelle

Dicks, general counsel for Owner-

GUARD. “The Department of Insur-

ance has agreed to delay enforcement

through March 31, which means the

department, in looking at GAP waiv-

er forms, is not going to fi ne someone

or haul them into court for having a

form that indicates that the deduct-

ible will be covered. However, you

can’t cover the deductible.”

If left unchanged, California deal-

ers will be prohibited from selling de-

ductible coverage through GAP with-

out an agent license. In the meantime,

providers are adding language to their

agreements that informs consumers

that deductible coverage is void.

OwnerGUARD is working with the

state’s dealer association and the in-

surance agency on new legislation to

solve the deductible problem. “We’re

really close to having language that

will fi x this legislation,” Dicks said.

OwnerGUARD is also working

with John Norwood, a noted Cali-

fornia lobbyist who specializes in the

state’s insurance and fi nancial sector.

The company hopes he can clear the

way for the state legislature to vote and

pass its drafted legislation by June, but

company offi cials admit there are sev-

eral hurdles standing in the way.

“Our goal is to, hopefully, see

something in June, but nothing is ever

certain,” said Dicks. “If it doesn’t

work the way we’re anticipating, we

might be looking at a September vote.

But if our legislation is not labeled as

an emergency measure, we could be

looking at Jan. 1, 2012.”

APRs Hit All-Time Low in DecemberCAR BUYERS ENJOYED THE LOWEST-

ever average annual percentage rate (APR) on their auto loans in December 2010, according to Edmunds.com.

The average loan carried an APR of 4.16 percent that month, down 0.33 points from November and 0.55 points from December 2009. An estimated 15.4 percent of all loans carried zero interest, the third highest monthly pace in 2010.

Only 4 percent of all loans car-ried an APR higher than 10 percent in December 2010, the lowest pro-portion seen by Edmunds.com since

it started gather-ing data in this category in 2004.

A major contribu-

tor to the low December interest

rates was the luxury market, which is generally driven by an affl uent, fi scally stable set of consumers, Edmunds.com said. The average APR for fi nanced sales of the top seven luxury brands was 2.9 percent, the lowest monthly rate of 2010.

The top three makes with deals fi nanced at zero percent were Buick, Toyota and Cadillac.

California Law Threatens GAP Deductible Coverage

Sacramento, Calif.

2011 Buick Regal

Developments

8 F&I and Showroom February 2011 CALIFORNIA STATE CAPITOL PHOTO BY COOL CEASAR

FI0211develop.indd 8FI0211develop.indd 8 1/28/11 4:25:37 PM1/28/11 4:25:37 PM

5(;065(3

(<;646;0=,

,?7,9;:7,673,�796+<*;:�7,9-694(5*,�

;/,�>(@�0;�:/6<3+�),�

+PHTVU�-\ZPVU�

=LOPJSL� �4V[VYJ`JSL�:LY]PJL�*VU[YHJ[Z

3PTP[LK�>HYYHU[PLZ

>PUKZOPLSK�7YV[LJ[PVU

+LU[� �+PUN�7YV[LJ[PVU�

,U]PYVUTLU[HS�7YV[LJ[PVU�

9VHKZPKL�(ZZPZ[HUJL

*\Z[VTPaHISL�7YL�7HPK�4HPU[LUHUJL�7YVNYHTZ

;PYL� �>OLLS�7YV[LJ[PVU

2L`�9LWSHJLTLU[�

>HYYHU[`�-VYL]LY�

;OLM[�7YV[LJ[PVU

5V�<ZL�5V�3VZL�

.(7

����������� >>>�5(;065(3(<;646;0=,,?7,9;:�*64

@V\�+LZPNU�0[������������ ���>L�(KTPUPZ[LY�0[�

FI0211develop.indd 9FI0211develop.indd 9 1/28/11 4:25:41 PM1/28/11 4:25:41 PM

Ristken Obtains Reynolds Certifi cationRISTKEN SOFTWARE

Services has completed the Reynolds Certifi ed Interface (RCI) program. As a certifi ed vendor, Ristken’s retail automo-tive software now has the ability to exchange data within Reynolds’ dealer management system. Certifi cation also ensures the security, integrity and privacy of dealership data. Through the approved interface, Ristken will also be able to better service, sup-port and control dealers’ information with the Ristken application.

Impact Group Connects IAS Products to Fusion MenuTHE IMPACT GROUP’S

Fusion menu now offers e-rating and e-con-tracting capabilities for Innovative Aftermar-ket System (IAS)’s F&I product line. Users can now rate all available IAS

product plans through the Fusion menu, as well as automatically update the dealer manage-ment software, print the selected contracts, and remit deal information to IAS for processing.

GWC Warranty, Tidewater Announce PartnershipDUE TO A NEW

partnership, Tidewater Motor Credit is now offering GWC Warranty Corp.’s vehicle service contracts. The subprime

lender made GWC’s product available through its dealer network in January.

Fortegra Acquires Auto Knight Motor ClubFORTEGRA FINANCIAL

Corp. has acquired the Palm Springs, Calif.-based Auto Knight Motor Club Inc. The acquisition expands Fortegra’s geo-graphic reach to Canada, where Auto Knight offers vehicle service plans and tire-and-wheel programs

through a network of dealerships.

DataScan Field Services Adds Clubb Finance Corp.DATASCAN FIELD SERVICES

was selected by Clubb Finance Corp. to provide fl oorplan verifi cation services for its dealer networks in Canada. Clubb provides short-term fl oorplan fi nanc-ing to independent and franchised automobile dealers, brokers and wholesalers.

Reynolds to Continue as Website Provider for Asbury THE REYNOLDS AND

Reynolds Co. has ex-tended its relationship with Asbury Automotive Group Inc. Reynolds Web Solutions will continue to provide its Web technolo-gy platform and dedicat-ed Web support team to Asbury’s 84 dealerships in the United States.

Dealer.com, a provider of online marketing solutions for the auto-motive industry, has expanded its leadership team by naming fi ve new executives.

Kristin Halpin, who joined Dealer.com in 2009, will serve as vice president of human resources.

Dan Jackson, who spent the last fi ve years managing the company’s OEM and dealer relationships,

will now serve as vice president of account management.

Tom O’Leary, who fi rst joined the company in 2009, takes over as vice president of sales.

Bryan Landerman, who has been with the company for three years, assumes the title of vice president

of engineering.

Additionally, Chris Stephenson, who joined the company in 2007, will serve as vice president of

business solutions.

Developments

10 F&I and Showroom February 2011

Moves and Hires

CONSUMER BANKRUPT-

cies were up 9 percent nationwide in 2010 from the previous year, according to the Ameri-can Bankruptcy Institute. Overall consumer fi lings reached more than 1.5 million in 2010, up from the 1.4 million fi lings in 2009. Consumer fi lings reached 118,146

last December, a 4 per-cent increase from the 113,274 fi lings recorded in December 2009.

Consumer Bankruptcy FilingsIncrease 9 Percent in 2010

WALLET PHOTO ©ISTOCKPHOTO.COM / LUGO

FI0211develop.indd 10FI0211develop.indd 10 1/28/11 4:25:41 PM1/28/11 4:25:41 PM

CarMor® is the product marketing name used by Allstate Dealer Services. Allstate Dealer Services is a marketing name for Pablo Creek Services, Inc., E.R.J. Insurance Group, Inc. (d/b/a

American Heritage Insurance Services), the dealer services division of American Heritage Life Insurance Company (Home Office: Jacksonville, FL), Northbrook Indemnity Company,

(Home Office: Northbrook, IL) and First Colonial Insurance Company (Home Office: Jacksonville, FL); each of these entities is a part of the Allstate family of companies.

©2010 Allstate Insurance Company allstate.com

Dealer Services

It comes down to basics —when your customers recognize the benefit and the brand

behind your F&I products, you can profit. That’s why it pays to go with the name you know.

Allstate Dealer Services provides innovative products backed by the service and support

you’d expect from a real industry leader. Find out how our Good Hands® are good for your

F&I business.

Allstate Dealer Services. Experience the difference.

allstatedealerservices.com/ads008

or call 1-888-244-1935 today.

®

*Allstate Dealer Services does not guarantee dealer overall profitability

FI0211develop.indd 11FI0211develop.indd 11 1/28/11 4:25:47 PM1/28/11 4:25:47 PM

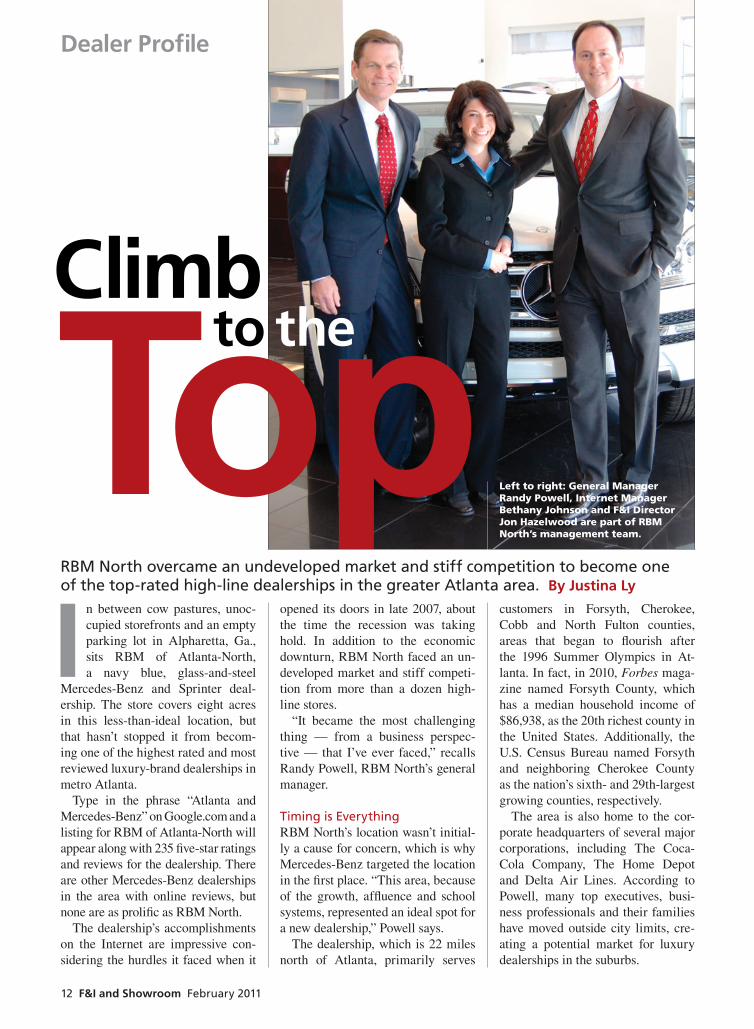

Topto theClimb

In between cow pastures, unoc-

cupied storefronts and an empty

parking lot in Alpharetta, Ga.,

sits RBM of Atlanta-North,

a navy blue, glass-and-steel

Mercedes-Benz and Sprinter deal-

ership. The store covers eight acres

in this less-than-ideal location, but

that hasn’t stopped it from becom-

ing one of the highest rated and most

reviewed luxury-brand dealerships in

metro Atlanta.

Type in the phrase “Atlanta and

Mercedes-Benz” on Google.com and a

listing for RBM of Atlanta-North will

appear along with 235 fi ve-star ratings

and reviews for the dealership. There

are other Mercedes-Benz dealerships

in the area with online reviews, but

none are as prolifi c as RBM North.

The dealership’s accomplishments

on the Internet are impressive con-

sidering the hurdles it faced when it

opened its doors in late 2007, about

the time the recession was taking

hold. In addition to the economic

downturn, RBM North faced an un-

developed market and stiff competi-

tion from more than a dozen high-

line stores.

“It became the most challenging

thing — from a business perspec-

tive — that I’ve ever faced,” recalls

Randy Powell, RBM North’s general

manager.

Timing is EverythingRBM North’s location wasn’t initial-

ly a cause for concern, which is why

Mercedes-Benz targeted the location

in the fi rst place. “This area, because

of the growth, affl uence and school

systems, represented an ideal spot for

a new dealership,” Powell says.

The dealership, which is 22 miles

north of Atlanta, primarily serves

customers in Forsyth, Cherokee,

Cobb and North Fulton counties,

areas that began to fl ourish after

the 1996 Summer Olympics in At-

lanta. In fact, in 2010, Forbes maga-

zine named Forsyth County, which

has a median household income of

$86,938, as the 20th richest county in

the United States. Additionally, the

U.S. Census Bureau named Forsyth

and neighboring Cherokee County

as the nation’s sixth- and 29th-largest

growing counties, respectively.

The area is also home to the cor-

porate headquarters of several major

corporations, including The Coca-

Cola Company, The Home Depot

and Delta Air Lines. According to

Powell, many top executives, busi-

ness professionals and their families

have moved outside city limits, cre-

ating a potential market for luxury

dealerships in the suburbs.

RBM North overcame an undeveloped market and stiff competition to become one of the top-rated high-line dealerships in the greater Atlanta area. By Justina Ly

Left to right: General Manager Randy Powell, Internet Manager Bethany Johnson and F&I Director Jon Hazelwood are part of RBM North’s management team.

12 F&I and Showroom February 2011

Dealer Profile

FI0211rbmatlanta.indd 12FI0211rbmatlanta.indd 12 2/2/11 1:58:14 PM2/2/11 1:58:14 PM

© 2008–2010 Associates Underwriting Limited L.L.C.

Get your profit motor running with AUL.Give us a call or visit us online and we’ll share our story of industry leadership, and more importantly, our passion for relentless customer service.

Service Contracts. It’s What We Do.®

800.826.3207www.aulcorp.com

Revvvenue

20OF SERVICEYEARS

SE

RV

ICE

CO

NTRACTS. IT’S W

H

AT W

E D

O.®

AU

L ADMINISTRATO

RS

FI0211rbmatlanta.indd 13FI0211rbmatlanta.indd 13 2/2/11 1:58:17 PM2/2/11 1:58:17 PM

In 2006, Mercedes-Benz ap-

proached RBM North’s dealer prin-

cipal, John Ellis, and offered him

the opportunity to open a brand-new

store in Alpharetta. Ellis, who also

owns RBM’s sister store, RBM of

Atlanta in Sandy Springs, agreed. He

then selected Powell to oversee the

dealership’s construction and hiring.

Powell staffed the dealership’s

sales, service and F&I departments

with more than 50 employees. In

March 2008, a mere six months after

the dealership opened, Powell began

to realize that the economy was tak-

ing a turn for the worse. Residential

and commercial construction came

to a screeching halt and unemploy-

ment started to rise, but Powell kept

his foot on the gas pedal.

“I was determined to get through

this without laying any employees

off,” said the 30-year industry vet-

eran. “So many of the dealerships

around here, and I’m not being judg-

mental in any way, had little choice

but to do that. But I was determined

to fi nd a way to continue growing the

operation to support the people we

had made these commitments to.”

Building an Online Reputation When RBM North fi rst opened, it

utilized mostly traditional market-

ing media, including newspaper and

billboard advertisements, direct mail

and local sports sponsorships. With

the onset of the recession and the

decline in new-vehicle sales, Pow-

ell looked to the Internet to drive in

more customers.

Today, more than 90 percent of

the dealership’s monthly advertis-

ing budget is directed toward digital

campaigns, according to Powell. “We

spend about $1.70 for every dollar

that a typical Mercedes dealer spends

to advertise,” he says. The dealer-

ship puts that money toward search

engine optimization, search engine

marketing, online reputation manage-

ment and online inventory listings on

Websites, such as eBayMotors.com

and AutoTrader.com.

Internet Manager Bethany Johnson,

who has spent 10 of her 12-year indus-

try career in Internet sales, oversees

RBM North’s “I-sales” department,

which she describes as a “mash-up

of an Internet department and a tradi-

tional business development center.”

Johnson and two other Internet

sales specialists employ a time-tested

leads process. As the process goes,

the I-salespeople will contact the

customer by phone three times and

by e-mail four times over a period of

10 to 12 days after a lead is received.

Once the customer expresses interest

in a vehicle, he or she is encouraged

to visit the dealership. If it’s an out-

of-state customer who is prepared to

buy, the Internet sales specialist will

nail down the price and other fi gures

over the phone.

Johnson estimates that 33 to 40

percent of total monthly sales are

now touched by the I-sales depart-

ment. In fact, 85 percent of total

14 F&I and Showroom February 2011

Dealer Profile

RBM North opened in late 2007, about the time the recession was

taking hold. The Mercedes-Benz and Sprinter dealership is housed

on an eight-acre lot.

“So many of the dealerships around here, and I’m not being judgmental in any way, had little choice but

to do that. But I was determined to fi nd a

way to continue growing the operation.” — Randy Powell

FI0211rbmatlanta.indd 14FI0211rbmatlanta.indd 14 2/2/11 1:58:17 PM2/2/11 1:58:17 PM

1Commercial banking products and services are offered through Wachovia Bank, a division of Wells Fargo Bank, N.A. and/or Wells Fargo Bank, N.A. Member FDIC and Equal Credit Opportunity Lender. 2Vehicle service contracts offered through Warranty Solutions® a member of the Wells Fargo family of companies. Wells Fargo Dealer Services, Inc. is a subsidiary of Wells Fargo Bank, N.A. © 2010 Wells Fargo Bank, N.A. All rights reserved. 2010680-001 10/10

Integrated solutions personalized for your dealership We offer integrated solutions to help dealers sell more cars, finance floorplans and real estate, and gain efficiencies in their business operation — while delivering a level of local, personalized customer service that’s unmatched in the industry.

ƌ�)�$- �/��0/*�Ũ)�)�$)"� ƌ��*(( -�$�'���)&$)"�. -1$� .1 ƌ��!/ -(�-& /�+-*�0�/.��1�$'��' �/#-*0"#���--�)/4��*'0/$*).Ʒ2

Please contact us for a customized solution. We’re here for you now and in the future.

��''�4*0-�'*��'�- +- . )/�/$1 �*-�888-937-9997, Monday through Friday, 5 a.m. to 5 p.m. PT.

Wells Fargo Dealer Services

FI0211rbmatlanta.indd 15FI0211rbmatlanta.indd 15 2/2/11 1:58:20 PM2/2/11 1:58:20 PM

monthly sales begin online, whether

through posted reviews or inventory

listings, she adds.

RBM North also maintains Face-

book and Twitter pages, but Johnson

prefers to use these social media sites

to connect with customers. “Being

high-line, I feel there should be a

softer, more personalized approach

rather than listing inventory and try-

ing to sell a car via Facebook,” she

says. “I just want it to humanize us.”

Even without the recession, John-

son admits that establishing a solid

online reputation for a new dealer-

ship like RBM North was a major

undertaking. That’s why the dealer-

ship turned to Riverside-Calif.-based

eXteresAuto three years ago for help.

Specializing in online reputation

management services, the company

helped RBM North rack up more than

235 fi ve-star customer ratings and re-

views from sites such as Google.com

and Edmunds.com.

“[Customers] see that there’re a lot

of good things about us,” Johnson

says. “We jump off the page with

200-plus fi ve-star ratings. It immedi-

ately makes you want to call us.”

Boosting CPO Sales Internet marketing also proved useful

when the dealership looked to boost

its certifi ed pre-owned (CPO) sales to

offset the recession-induced decline

in new-car sales. Powell even used the

medium to increase business in the

service drive. “We realized that, with

this decrease in business, people were

going to start reevaluating their car

needs,” Powell recalls.

Sensing this shift, he aggressively

marketed the dealership’s used-vehi-

cle inventory through third-party sites

such as eBay.com and AutoTrader.

com. Powell even offered free ship-

ping to customers. “We were ship-

ping cars to Montana and Seattle …

but mostly we sold in our area to help

grow our service business,” he says.

In addition, RBM North marketed

its inventory to leaseholders who were

near the end of their terms and wanted

vehicles that were “a little less expen-

sive and a little less ostentatious.”

By 2009, RBM North was one of

the Top 10 dealerships in the area in

terms of pre-owned vehicle volume.

“We had adjusted to that ahead of the

rest of the market,” says Powell. “So

we sold a lot of certifi ed pre-owned

cars in the fi rst year — more than we

sold new, which is pretty unusual for

a new-car dealer.”

Recession’s Impact on F&I The dealership’s average monthly

volume currently stands at 60 new

vehicles, 60 pre-owned units and 15

Sprinter vans, according to Powell.

Those fi gures have translated into a

solid performance for the F&I de-

partment. “Everything around us has

gone really bad, and we’ve done re-

ally well,” says Jon Hazelwood, the

dealership’s F&I director.

The store’s profi t per retail unit

averages around $1,000-$1,200 on

new vehicles and $500-$799 on CPO

vehicles. Hazelwood says most of his

customers have credit scores in the

700-800 range, with about 60 per-

cent of his customers opting for deal-

ership fi nancing. The rest of the deals

are cash. The dealership’s primary

lender is Mercedes-Benz Financial

Services (MBFS), but Hazelwood

also counts on Bank of America,

Wells Fargo and Chase to fi nance his

customers’ vehicles.

Most of RBM North’s F&I prod-

ucts carry the MBFS brand. Tire-

and-wheel protection leads the way

with a 40 percent acceptance rate.

Dent repair touts a 30 percent sell-

through, followed by GAP and CPO

extended warranties at 20 percent

each. Hazelwood says the dealership

also sells MBFS-branded interior/

exterior protection and a service con-

tract through Norcross, Ga.-based

EasyCare, which benefi ts trade-in

customers who want extra coverage.

Looking AheadDespite RBM North’s early strug-

gles, the store is now poised to make

greater strides this year. Powell says

he has no plan to change his Internet

marketing strategies, but he wants

to see a 10 to 12 percent increase in

new-vehicle sales. “I think the per-

centage of new versus pre-owned

will move back toward new, because

there is still pent-up demand in the

marketplace,” he says.

The economy’s slow recovery is

a cause for concern, but Powell is

hopeful that his dealership’s strong

Web presence and the continued sup-

port of his staff and dealer principal

will help RBM North achieve its

goals this year.

“Without that [economic] growth,

it’s going to continue to be a chal-

lenge for us, so we have to work hard-

er,” he says. “I look forward to the

day where we are surrounded by oth-

er businesses and this area becomes

more of a destination. In one way,

we’re a destination point now. That’s

because if you’re coming to us, you’re

looking for us.”

16 F&I and Showroom February 2011

Dealer Profile

RBM North sells Mercedes-Benz brand accessories, such as hats, T-shirts and teddy bears, at its boutique. Customers also can get complimentary drinks and snacks at the dealership’s café and lounge area (inset).

FI0211rbmatlanta.indd 16FI0211rbmatlanta.indd 16 2/2/11 1:58:20 PM2/2/11 1:58:20 PM

Insurance

Risk Management

Products and services are underwritten and provided by member companies of Zurich in North America, including Universal Underwriters Insurance Company and Universal Underwriters Service Corporation. Certain coverages and products and services are not available in all states. *Results based on 2010 data. ©2011 Zurich American Insurance Company

With our Streamlined Selling System® it‘s easier to increase dealership profits.

Zurich HelpPoint is here when you need more than just insurance.

It is our commitment to making it easier for dealerships to earn

the maximum per vehicle retail possible. Through Zurich’s exclusive

Streamlined Selling System® our Elite Performance dealership customers

earned an average F&I profit of $864 per vehicle sold—with our

top 20% earning an average of $1,208*. A local Zurich F&I specialist

can help you achieve this same success through our proven income

development program. Visit FandIResourceCenter.com for more tools

and information or contact a Zurich F&I specialist today at 877-368-7513.

Here to help your world.

Learn how the

economy will affect

auto dealer’s expectations

for F&I and sales – download

our FREE white paper at

www.zurichna.com/FIS

FI0211rbmatlanta.indd 17FI0211rbmatlanta.indd 17 2/2/11 1:58:26 PM2/2/11 1:58:26 PM

2

1

3

There’s nothing like those

fi rst few days of being an

F&I manager. You feel

like you can sell anything

to anybody. Unfortunate-

ly, that feeling wears off once you

realize that most customers aren’t

initially interested in your products

and it will take some ef-

fort to overcome those

walls of resistance.

Now that you

know working as an

F&I manager is harder than it looks,

let’s review the “10 Commandments

of F&I” that, if followed, will provide

a helpful roadmap to success in this

challenging position.

Diagnose Before You Prescribe Imagine the lawsuits and loss of pa-

tients a doctor would face if he or she

prescribed remedies before know-

ing the cause of his or her patients’

problems. The same goes for an F&I

manager, whose primary purpose is

to discover each customer’s unique

circumstances. That’s where open-

ended, needs-discovery questions

come in, allowing you to uncover

why your customers need your prod-

ucts. Remember, you can’t prescribe

without diagnosing the need your

products will fulfi ll.

Listen Twice as Much as You Speak A good listener can draw others in

like a magnet, while someone who

dominates a conversation will always

drive people away. Remember, people

don’t buy when they understand; they

buy when they feel understood. So,

when a customer says, “I bought a

service contract before and never

used it,” use the “Repeat-Re-

spond-Reap” method:

Repeat: “So, what I

hear you saying is

you feel like you

just wasted your

money the last time. Am I right?”

You build a high level of trust and

credibility with customers when they

feel like they’ve been heard and un-

derstood.

Respond: “You don’t have to buy

anything. These are just options.

However, if this vehicle breaks, we

can’t fi x it.”

Reap: “We don’t fi x anything any-

more. We just replace the failed com-

ponent. If your gas gauge fails, we

have to replace the entire instrument

cluster. That makes a minor repair a

major expense, which is why a ser-

vice contract is critical, especially on

a new vehicle.”

Be a Problem Solver The most successful salespeople are

those who are creative at fi xing prob-

lems. However, be careful of getting

caught up in pointing out problems.

Unless you uncover a need your

products can fi ll, you have no ba-

sis for discussing your solution. But

when you do, use creative techniques

18 F&I and Showroom February 2011

Finance and Insurance

PHOTO ©ISTOCKPHOTO.COM / DIANE39

F&I’s

Starting out in F&I is never easy, but the magazine’s resident expert lays out a game plan to get F&I ‘newbies’ off on the right foot.

By Rick McCormick

Commandments

FI0211mccormick.indd 18FI0211mccormick.indd 18 1/28/11 4:20:28 PM1/28/11 4:20:28 PM

3500 Piedmont Road NE, Suite 400, Atlanta, GA 30305 | [email protected] | www.safe-guardproducts.com

One Company. One Solution.

Depend on Safe-Guard to deliver the exceptionalservice and innovative products that are essentialin today’s changing F&I environment.• Competitive pricing.

• Comprehensive training.

• Complete reinsurance and retro.

• Unconditional commitment to service.

You demand it … we deliver.

| GAP | Tire & Wheel | Theft | Lease Wear & Tear | Paintless Dent Repair | Windshield | Roadside Assistance | Identity Theft || Key Replacement | Planned Maintenance | Interior & Exterior | Mechanical Protection | Emergency Notification |

| E-Business Solutions | Menu Software | Training & Development |

FI0211mccormick.indd 19FI0211mccormick.indd 19 1/28/11 4:20:32 PM1/28/11 4:20:32 PM

4

5

6

7

8

9

10

to illustrate how your products can

fulfi ll your customer’s need.

Practice PurposefullyIf you ever played Little League,

you’ll remember the phrase, “Prac-

tice like you play.” Well, skills that

are not practiced will never fi nd their

way into your customer interactions.

That’s why it’s important to attend

every training class you can, whether

in person or online. And once the

lesson is done, be sure to practice

what you learned so you can reach a

comfort level that will allow you to

put your newfound techniques to use

with real customers. Practice doesn’t

always make perfect, but profession-

als who practice purposefully pro-

duce more profi ts.

Go the Extra Mile for Your Dealer and Your Customer Anyone can do what is expected of

them. However, it takes commitment

to go the extra mile. Enterprise be-

came the nation’s No. 1 car rental

company by telling its employees,

“You can rise through the ranks and

make remarkable money, but only

after you demonstrate an ability to

knock the socks off every customer

that comes through the door.” So,

knock the socks off your internal

(i.e., your dealership colleagues) and

external customers and your value

will increase. Remember, great com-

panies and great F&I managers pro-

vide great customer service.

Stay Focused On What You Can Control Don’t waste time trying to fi x things

you can’t control. Yes, there always

will be issues of concern, but don’t

let them distract you from your main

purpose — which is to help custom-

ers make good decisions. Focus on

coming up with more effective ways

to sell your products. Yes, customers

are more reluctant to buy F&I prod-

ucts, but that’s easily overcome with

a selling process that draws interac-

tion from the customer. Remember,

an active customer is one who is more

willing to buy.

Choose Your Associates Wisely Who you spend time with during the

workday will have a huge impact on

your outlook. Every company has its

fair share of whiners and complain-

ers, so be sure to avoid that crowd.

They have a tendency to destroy their

coworkers’ motivation. Instead, seek

out those with a more positive out-

look, those who are always looking

to improve their skills. Better yet,

why not try to become that person at

your dealership?

Lose Productively How you react to setbacks and losses

will do more to shape your career

than almost anything else. Every

sales position — especially those

that sell intangibles — will experi-

ence a slump. It’s how you react to a

slump, not the cause, that will deter-

mine its length and depth. So, rather

than get down on yourself, use the

slump as an opportunity to review

your process. Role-play your presen-

tation, record it and review the video.

Remember, setbacks should make

you better, not bitter.

Never Stop Learning A recent survey revealed that 42 per-

cent of former college students never

pick up a book after they graduate. I

guess it’s because they learned it all

in college. Well, that can’t be the case

in the F&I offi ce. Being motivated to

learn all you can about your products

and why people buy isn’t a problem

when you’re new. It’s when you’ve

been around the block a few times

that learning tends to lose its luster.

So, make it your goal to read a book

about sales each quarter. Devour

F&I and Showroom magazine every

month and engage in the magazine’s

F&I Forum to exchange ideas with

other F&I managers.

Next, visit your dealership’s service

department and learn about at least

two parts on a vehicle. Make sure

you know what they do, what hap-

pens when they fail and what the cost

is to replace them. Remember, the

more you learn the more convincing

you’ll be when explaining why your

customer needs your products.

Seek Input From Others S. Truett Cathy, the 89-year-old

founder of Chick-fi l-A, recently gave

a presentation to high-level execu-

tives. After he was done, someone

from the audience came up to thank

him for his presentation. After thank-

ing him, Cathy said, “Please tell me

one thing I could have done better.”

You see, Mr. Cathy has been ask-

ing that question since the day he

launched his restaurant chain, and it

has been one of the keys to his suc-

cess. It takes a humble individual to

open up himself to the input of oth-

ers. But to be good at what you do,

you need to strive to be that person.

Regularly reviewing these 10 com-

mandments will defi nitely help an

F&I “newbie” get off to a great start.

But even a seasoned veteran can ben-

efi t from doing the same. Heck, it

might be exactly what you need to get

your career back on track.

Rick McCormick is the national ac-count development manager for Reahard & Associates Inc., which provides customized F&I training for dealerships throughout the United States and Canada. E-mail him at [email protected].

20 F&I and Showroom February 2011

Finance and Insurance

Customers are more reluctant to buy F&I products, but that’s

easily overcome with a selling process that draws

interaction from the customer. Remember, an

active customer is one who is more willing to buy.

FI0211mccormick.indd 20FI0211mccormick.indd 20 1/28/11 4:20:32 PM1/28/11 4:20:32 PM

©2011 The Reynolds and Reynolds Company. All rights reserved.

www.reyrey.com

www.coindata.com

s� !�12%�INCREASE�IN�SERVICE�CONTRACT�SALES�

s� 0ROlT�INCREASES�OF�$250�PER�DEAL�

s� 4IME�SAVINGS�OF�10 to 15�MINUTES�PER�DEAL�

®

FI0211mccormick.indd 21FI0211mccormick.indd 21 1/28/11 4:20:38 PM1/28/11 4:20:38 PM

Are these your stats?

Why not?

$1000 50%

How’s your blocking and tackling? Are you ready for the

big game? Because it’s already started. It’s called 2011. And making

it to the game and winning are two different stories. All it takes is the

right players and the right coach.

Since 1964 the team at Resource Automotive has been pushing dealers

to the top of their game. We virtually invented F&I, and since then

we’ve created additional profit centers for over 6000 dealers and

manufacturers. In fact, we call half of the top 100 dealers our clients.

With the industry’s widest menu of product options, we serve up what

you need, when you need it, including service contracts, GAP, CPO, CRM,

inventory management, training and a wide variety of business models.

This benefits you by taking the bias out of how we build your game plan,

and gives you the power of choice in determining how you want to reach

your profit objectives.

FI0211mccormick.indd 22FI0211mccormick.indd 22 1/28/11 4:20:39 PM1/28/11 4:20:39 PM

As we’ve done for over 46 years, Resource Automotive

makes an immediate impact in every department in your dealership —

fixed or variable, we do it all. As part of The Warranty Group, an 1800

employee and $5 billion asset global enterprise, we provide world-class

claims administration, plus, we have Virginia Surety Company,Inc.,

rated A- (Excellent) by AM Best, as a wholly-owned subsidiary.

In addition, we’re the leader in participation programs and facilitated

payouts of $100 million — just last year.

It’s critical to understand that you can’t realize your potential until

improvement opportunities are identified. That’s where we come in.

We help you assemble the people, processes and products to not just

compete, but win. Then we coach your team to victory, every time.

Now is the time to reach the next level of performance.

Contact Charlie Robinson today to arrange an in-depth, no-charge

business analysis.

[email protected] 312.560.9182

The game is on. What do your stats look like?

PVR VSC

thewarrantygroup.com

FI0211mccormick.indd 23FI0211mccormick.indd 23 1/28/11 4:20:40 PM1/28/11 4:20:40 PM

ProductPlacement

Should the base payment be displayed

on the menu? Offi cials with IAS offer their

take on that hot-button question and more.

By Gregory Arroyo

24 F&I and Showroom February 2011

Q&A

Meet the two guys

leading the charge

for Integrated Af-

termarket Systems

(IAS)’s software

and F&I product units: Bob Corbin,

president, and Matt Nowicki, direc-

tor of information technology. We

caught up with the execs to talk about

software integration, using the menu

as a compliance tool, and the new

No. 3 F&I product.

F&I: How has IAS faired in the e-contracting, e-rating and e-remittance arms race?

Nowicki: It’s really

ramped up over the last

six to eight months. Not

only are we connecting

to more providers, but

the way in which we’re doing it is

also changing.

F&I: Being that you’re also an F&I product provider, how do you work both sides?

Corbin: As you know, we

provide our software free

of charge to dealers who

sell our products. Now, if

one of our customers

chooses to use a non-IAS menu and

that menu offers e-rating and e-con-

tracting capabilities, then we want to

make sure our products are accessible

through that menu.

F&I: Has the industry considered a standardized link between product providers and menu makers?

Corbin: For a standard to be realized,

dealers need to embrace e-rating and

e-contracting a lot more than they

do today. If 50 percent of the dealers

were e-contracting today, then we’d

already have a standardized hub.

F&I: I would think not having a binder full of ratings would be reason enough.

Corbin: That’s how I see it. The real-

ity is, most F&I managers don’t need

to pull out the binder for every cus-

tomer because they sell a service con-

tract above dealer cost, which means

they’ve already built in enough mar-

gin. So, it’s about building interest in

the tools, not the tools themselves.

That’s really the battle.

F&I: How has your view of the menu changed?Corbin: Originally, it represented a

way to print something out that had

color and life to it, and that was spe-

cifi c to that consumer’s deal. We also

spent a lot of time doing tax calcula-

tions and a lot of credit life, accident

and health calculations. Today, it’s

about integration. Currently, we’re

certifi ed with the top three providers

of dealership management systems

— Reynolds, ADP and DealerTrack.

F&I: Integration is a big investment. Have you realized the benefi ts?

Corbin: Defi nitely. Most of all, we

have the ability to use them as ad-

vertising partners, which is a strong

marketing tool. But I’ll tell you, the

No. 1 reason for me is I never want to

be one of those companies that gets a

call from the dealer saying, “I’ve got

deals to deliver right now and your

software isn’t working.”

F&I: When did the menu become a compliance tool?Corbin: First of all, today’s menus of-

fer OFAC and identity verifi cations,

so that’s one aspect of compliance. I

also think the menu legitimizes the

sale of F&I products in the minds of

consumers. So, from the get-go, the

menu promised to make the operation

more compliant because it brought

consistency to the process. As it has

evolved, whether it was displaying

base payment or requiring initials or

signatures next to the base payment,

the idea that the menu was a compli-

ance tool began to grow.

F&I: Should the menu display the base payment?Nowicki: By default, our menu does.

We used to lock that feature so deal-

ers were kind of forced to show the

base payment. That’s not the case

anymore. We do suggest that they

show it, but we also suggest that they

talk to their legal counsel. And as

far as I know, there are no rules that

spell out anything that have to do

with the menu.

F&I: You offer a video recording feature. Isn’t there a danger that those recordings can be used against the dealer?

Corbin: If you’re doing F&I the right

way, the benefi ts outweigh the dis-

advantages. I would even say that

our SmartEye feature has actually

supported, rather than indicted, the

dealer. It eliminates those “he-said,

she-said” situations. Now, I’ve only

heard of fi ve instances in nine years

where the video was used in a law-

suit against a dealer. Every single

time the video actually supported

the dealer’s position.

F&I: What disclosure rules does a dealer need to consider before employing a recording system?

Nowicki: It varies by state. What

we recommend our customers do is

FI0211qa_ias.indd 24FI0211qa_ias.indd 24 1/28/11 4:33:31 PM1/28/11 4:33:31 PM

check www.rcfp.org/taping/states.

html. You can see what the rule is

for all 50 states and the District of

Columbia. The vast majority are

“one-party” states, which means that

as long as one party realizes they’re

being recorded, that’s all you need.

F&I: Do you see other product categories growing in popularity?

Corbin: Obviously, it’s about control-

ling the fi nancing, then selling the

service contract No. 1, then GAP No.

2. I would say that tire-and-wheel

protection is No. 3. It has really be-

come a staple product in F&I. After

that, it really comes down to what the

dealer wants to push. Is it windshield

protection or dent-and-ding?

Combo packages have really be-

come big for us. We offer what we

call Multi-Shield protection, which

offers tire-and-wheel, windshield

and dent-and-ding protection. It also

offers 24/7 emergency roadside as-

sistance. Another emerging product

is key replacement.

F&I: Considering how expensive keys are these days, I can see why.

Corbin: We have seen dealers offer

the product as a one-year compli-

mentary offering, then try to upsell it

to a three- or fi ve-year term in F&I.

F&I: So, has the industry found its stride?Corbin: I think we have. Our com-

pany has put together an aggressive

projection budget for 2011. We think

it’s going to be a 11.5 or 11.7 million-

unit sales year, maybe even 12 mil-

lion. Last year was a good comeback

year for us, so we expect that momen-

tum to continue.

February 2011 F&I and Showroom 25

IAS offers its software free of charge to dealers who sell its F&I products. Here’s a look at SmartMenu Complete’s e-rating and deal entry screens.

FI0211qa_ias.indd 25FI0211qa_ias.indd 25 1/28/11 4:33:32 PM1/28/11 4:33:32 PM

26 F&I and Showroom February 2011

Last fall, after several years

of success running the spe-

cial fi nance department for

Longmont Ford in Long-

mont, Colo., Greg Alore set

a new goal for himself: He wanted to

be a Diamond Dealer. He knew that

Capital One Auto Finance’s preferred

dealer program offered fl exible rates

for subprime buyers and that his par-

ent company’s Denver store, Freeway

Ford, was already signed up. Alore

wanted in.

When the general sales manager at

the Denver store called to tell him he

was on his way to a Capital One event

at Invesco Field, home of the Nation-

al Football League’s Broncos, Alore

sprang into action. Knowing that the

executives were fl ying in from the

Dallas area, the longtime Cowboys

fan pulled his Marion Barber jersey

off the hanger and headed for Mile

High to make his pitch.

“Three weeks later, I was a Dia-

mond Dealer,” Alore says with a laugh.

“Our fi rst month out of the shoot was

November. We booked 14 special fi -

nance deals with Capital One, and

that wasn’t even a whole month.”

With Capital One now on board,

along with GM Financial (formerly

AmeriCredit Corp.) and several other

fi nance sources, Alore expects his

department to move at least 10 new

and 35 used units each month in

2011. It’s an ambitious goal, but he’s

confi dent he and his staff are well on

their way.

A New Game PlanAlore’s devotion to the Cowboys is

a byproduct of the 25 years he spent

working as a dealer and consultant

in the Dallas/Fort Worth market. In

1980, the Detroit native steered his

Pontiac Firebird south to take an en-

try-level sales job at a Ford dealership

in Abilene. Many years and several

dealerships later, he took a consulting

gig at F&I Holding Service Life.

“My specialty was training sales-

people for the proper turn to F&I,”

Alore says. “They sent me to Colo-

rado once a month, and one of those

stores was Freeway Ford.”

Impressed by his work, Freeway

Owner Mike Peebles offered Alore a

chance to jump back in the trenches

as the new-car manager at the Long-

After fi rst serving as Longmont Ford’s new-car sales manager, Greg

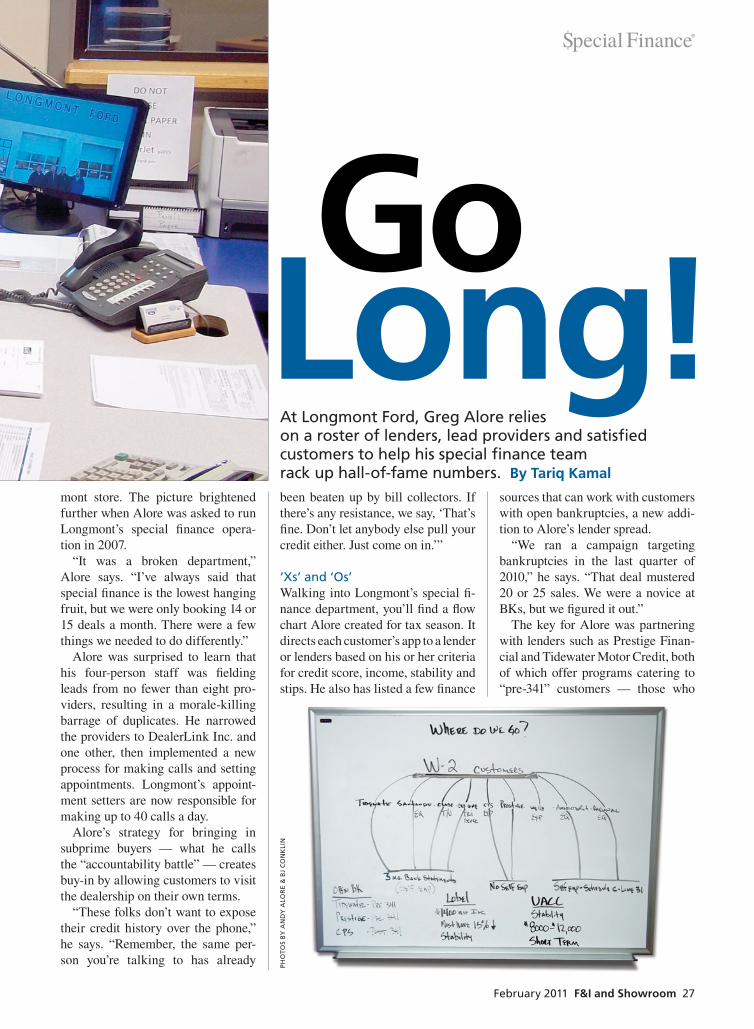

Alore took the reins of the store’s special fi nance department.

The result? Fewer duplicate leads, more sales and more referrals.

FI0211longmont.indd 26FI0211longmont.indd 26 1/28/11 4:16:01 PM1/28/11 4:16:01 PM

mont store. The picture brightened

further when Alore was asked to run

Longmont’s special fi nance opera-

tion in 2007.

“It was a broken department,”

Alore says. “I’ve always said that

special fi nance is the lowest hanging

fruit, but we were only booking 14 or

15 deals a month. There were a few

things we needed to do differently.”

Alore was surprised to learn that

his four-person staff was fi elding

leads from no fewer than eight pro-

viders, resulting in a morale-killing

barrage of duplicates. He narrowed

the providers to DealerLink Inc. and

one other, then implemented a new

process for making calls and setting

appointments. Longmont’s appoint-

ment setters are now responsible for

making up to 40 calls a day.

Alore’s strategy for bringing in

subprime buyers — what he calls

the “accountability battle” — creates

buy-in by allowing customers to visit

the dealership on their own terms.

“These folks don’t want to expose

their credit history over the phone,”

he says. “Remember, the same per-

son you’re talking to has already

been beaten up by bill collectors. If

there’s any resistance, we say, ‘That’s

fi ne. Don’t let anybody else pull your

credit either. Just come on in.’”

‘Xs’ and ‘Os’Walking into Longmont’s special fi -

nance department, you’ll fi nd a fl ow

chart Alore created for tax season. It

directs each customer’s app to a lender

or lenders based on his or her criteria

for credit score, income, stability and

stips. He also has listed a few fi nance

sources that can work with customers

with open bankruptcies, a new addi-

tion to Alore’s lender spread.

“We ran a campaign targeting

bankruptcies in the last quarter of

2010,” he says. “That deal mustered

20 or 25 sales. We were a novice at

BKs, but we fi gured it out.”

The key for Alore was partnering

with lenders such as Prestige Finan-

cial and Tidewater Motor Credit, both

of which offer programs catering to

“pre-341” customers — those who

February 2011 F&I and Showroom 27

Go Long!

At Longmont Ford, Greg Alore relies on a roster of lenders, lead providers and satisfi ed customers to help his special fi nance team rack up hall-of-fame numbers. By Tariq Kamal

PHO

TOS

BY

AN

DY

ALO

RE

& B

J C

ON

KLI

N

FI0211longmont.indd 27FI0211longmont.indd 27 1/28/11 4:16:03 PM1/28/11 4:16:03 PM

FI1010friendly.indd 1 9/21/10 1:43:39 PM

28 F&I and Showroom February 2011

have fi led for Chapter 7 or 13 but have

yet to offi cially declare their assets. It

is, as Alore puts it, “a low point” for

those customers.

“But after their debt is cleared, and

they’re in a great car, they’re elated,”

he says.

Alore wears his passion for helping

subprime customers on his sleeve. He

says he never hesitates to spend a few

extra minutes with a customer to of-

fer counseling or review stips — even

if they’re not likely to buy that day.

He credits that personal touch with

driving referrals.

“We tell our customers, ‘Text your

friends, let them know,’” Alore says.

“We just had a referral who walked

in and said, ‘I heard you’re awesome.’

He drove away in a 2010 Impala.”

Like he does for every referral that

results in a sale, Alore rewarded the

texter with $200 — and not in the

form of coupons for oil changes. “We

just give them a check,” he says.

A Team EffortAlore’s time on the consulting side

taught him that rebuilding his de-

partment would require buy-in from

management. His team handles ev-

ery lead that is paid for by the spe-

cial fi nance budget, as well as every

customer with a TransUnion score of

620 or below.

“It’s an automatic turn to SF,” Alore

says. “There’s no resentment. We

worked through that as a team. And

that extends to inventory, our business

model, our plan, our execution.”

Longmont’s business model calls

for 180 used units in stock on a three-

month turn. His focus is on quality,

late-model vehicles — another factor

that separates Alore from his com-

petitors. One recent customer drove

a spot-delivered, high-mileage mini-

van onto the Longmont lot with three

kids in tow.

“She pulled up in a 2000 Windstar

with 150,000 miles on it that some

other dealer ranched her on,” Alore

says. “I put her in an ’07 Sienna at

12.9 percent. We’ll make maybe two

points, and she’s in a nice, nice car.”

The vehicles are sourced mostly

from auctions, and Alore has buy-

ers on the lookout for special fi nance

units from as far away as California

and Michigan.

“There has been a better supply

over the last few months, and I’m

hearing [the auctions] want to get rid

of everything after 30 days,” Alore

says. “I don’t know if there’s an ideal

special fi nance vehicle, but our Cali-

fornia guy just brought in a bunch of

Ford Escapes. Even when it comes to

Corvettes, Mercedes and Hummers,

he thinks of special fi nance.”

Looking Downfi eldAlore believes that, as the economy

continues to recover, the lessons

he and his staff learned during the

downturn will result in further gains.

He points out that many dealers, in-

cluding a few of his competitors,

turned their back on the subprime

market prematurely.

“I went into a 20 Group meeting

in Colorado Springs with my dealer,

and Greg Goebel spoke to the group,”

he says. “Part of what he was talking

about was risk. It’s true. Dealers are

afraid of getting in too deep.”

The Longmont team persisted, and

their reward was a Top 10 ranking

in used-car sales for all of Colorado.

Alore says he won’t relinquish that

distinction willingly.

“It blows me away that there are

still dealers out there who won’t do it

right,” he says. “Yes, there is risk.

There always will be. But if you’re

thinking big for 2011, it’s here in

special fi nance.”

The Longmont Ford special fi nance team (L-R): Erich Halverson, Sean

Queen, Alore, Gary Lapuma, Travis Holtzman and Chas Cuzzoni.

“It blows me away that there are still dealers out

there who won’t do it right. Yes, there is risk. There

always will be. But if you’re thinking big for 2011, it’s here in special fi nance.”

— Greg Alore

FI0211longmont.indd 28FI0211longmont.indd 28 1/28/11 4:16:04 PM1/28/11 4:16:04 PM

FRIENDLYFINANCECORPORATION Turning Problems into Solutions® Since 1949

Licensed in DE, GA, IL, IN, KY, MD, MI, OH, TN and VAAnd Now Licensed in: KS & NE

For more information callFriendly Finance Corporation at

800.872.2877, ext. 231 or ext. 241,or visit our website @

www.friendlyfinancecorp.com

DealerTrack Lender No Dealer Agreements Always 100% Non-Recourse

For 1 in 125 U.S. Households,BANKRUPTCY Has Become the Only Option.

Don’t Pass By this Rapidly Growing Demographic!

We Fund OPEN Chapter 13 Bankruptcies We Fund OPEN Chapter 7 Bankruptcies BEFORE 341 Meeting

FI1010friendly.indd 1 9/21/10 1:43:39 PMFI0211longmont.indd 29FI0211longmont.indd 29 1/28/11 4:16:07 PM1/28/11 4:16:07 PM

Given the attention auto

retailing has received

over the years, it might

be diffi cult to fathom

that one area has es-

caped the watchful eye of federal

regulators: pay plans. Recent actions

by the Department of Labor and

heightened awareness for wage and

hour laws among employees could

change that.

The subject of pay plans was cov-

ered in a recent Webinar co-hosted

by my company, Compli, and John

Donovan, a partner at noted labor law

fi rm Fisher & Phillips LLP. The goal

of the presentation was to highlight

common misconceptions and best

practices to help dealers in an area

that’s often challenging, especially

when dealing with poorly written,

out-of-date and, sometimes, undocu-

mented pay plans.

But there’s good reason to plug this

noncompliance hole. The Department

of Labor recently hired 250 new inves-

tigators to more aggressively investi-

gate employee complaints. Employees

also are more aware of employment

laws these days, and wronged staffers

no longer have to discuss employment

matters with their bosses; they can go

straight to their lawyer.

Also remember that if a dealership

employee sues for wage and hour vi-

olations because his or her pay plan

didn’t comply with the law, the dealer

can be on the hook for three years’

worth of wages. Even if your new

guy or gal has been with you only six

months, you can bet his or her attor-

ney will track down his or her pre-

decessors until they can build three

years’ worth of claims. Remember, a

prevailing lawyer automatically gets

all of his or her fees paid.

Let’s review some common mis-

conceptions about pay plans:

Misconception No. 1: “We’ve used this pay plan for fi ve, 10, maybe 15 years, and we’ve never had a problem, so I’m sure it’s okay.”

Reality: Most payroll managers will

tell you they learned their job from

their predecessor, which means their

bad practices get carried on from

year to year.

Misconception No. 2: “Well, he signed the pay plan and he signed his timecard, so he agreed to this amount.”

Reality: If an employer pays an em-

ployee at variance with what he has

previously agreed to, it is a potential

contract claim.

30 F&I and Showroom February 2011

FI0211reaheard.indd 1 1/26/11 8:40:44 AM

Pay PlanReboot

The Department of Labor is gearing up. The question is, will your pay plans be ready? Here’s a primer to help you get them up to speed. By Lon Leneve

Dealer Management

PHOTO ©ISTOCKPHOTO.COM / JGROUP

FI0211payplan.indd 30FI0211payplan.indd 30 1/28/11 4:32:14 PM1/28/11 4:32:14 PM

FI0211reaheard.indd 1 1/26/11 8:40:44 AMFI0211payplan.indd 31FI0211payplan.indd 31 1/28/11 4:32:15 PM1/28/11 4:32:15 PM

Misconception No. 3: “Oh, everyone in my 20 Group does this.”

Reality: The “everyone else does it”

excuse doesn’t provide you with any

protection, because regulations vary

from state to state.

Misconception No. 4: “This is an ‘at will’ state.” Reality: Yes, a manager can change

his pay plan tomorrow, but he can’t

go back, change the pay plan and

make it retroactive to the fi rst of the

month. A change to a pay plan can

only apply to future earnings.

Misconception No. 5: “He’s paid a salary, so he’s exempt from overtime.”

Reality: That’s the furthest from the

truth. Before we get into some best

practices, there are two things you

need to remember about pay plans:

First, pay plans are wage and hour

documents that have to comply with

both state and federal wage and hour

laws. Second, pay plans are con-

tracts. When you write up a pay plan

and hand it to your employee, you are

effectively telling him or her, “If you

do these things, I will pay you this

much money.” Not only is that docu-

ment legally binding, it’s enforceable

in court. Even if it’s not in writing,

it’s at least a verbal contract which is

enforceable in court.

One thing people don’t realize is

a contract is construed against the

party that drafted it. That being said,

let’s review some best practices:

■ EVERY employee should have

a written pay plan that’s signed and

dated by the employee.

■ The pay plan should be drafted

so that even a layperson who is unfa-

miliar with the car business can un-

derstand what it means.

■ The pay plan should spell out in

detail how the employee will be paid

— salary, draw or commission — and

how the money will be calculated.

■ The pay plan should include all

aspects of the compensation: hourly,

salary, commissions, bonuses and

spiffs. If it’s not clearly delineated in

the pay plan contract, there could be

a problem.

■ If there are special contests that

aren’t in the pay plan, they should be

documented with the same amount of

seriousness and accuracy as a regular

pay plan.

■ If a guarantee is included, make

sure the plan states that it is a guar-

antee of compensation, not employ-

ment.

■ Decide if the employee is exempt

from overtime or not, and be sure he

or she is aware as well.