fiaas forum - finity consulting · 3/24/2015 · eq risk a real challenge (and not the only one!)...

TRANSCRIPT

© 2015 Finity Consulting Pty Limited

FIAAS Forum

24 March 2015

Finity Consulting Pty Limited 2015 Supplied subject to the FIAAS terms of agreement and http://www.finity.com.au terms of use of the Finity client website available at: http://www.finity.com.au/Website_Terms_of_Use.pdf Queries can be directed to [email protected]

Agenda

Use of catastrophe model results by actuaries – GIPC

guidance note

Royal Commission into Child Sexual Abuse

Risk Margins – APRA industry review

Reminder of Chatham House rule:

“Participants are free to use the information received, but neither

the identity nor the affiliation of the speaker(s), nor that of any

other participant, may be revealed.”

2

© 2014 Finity Consulting Pty Limited

Use of Catastrophe Models

by Actuaries

GIPC Guidance Note

Some introductory comments

4

Context of the note

“It does not represent a professional standard or

Practice Guideline” … (2)

“some tools …to assist…in gaining comfort in” relying on

work of others … (6)

“It is not suggesting that an actuary either asks all these

questions or carries out all the investigations” … (22)

Provides good assistance in how to tackle technical aspects

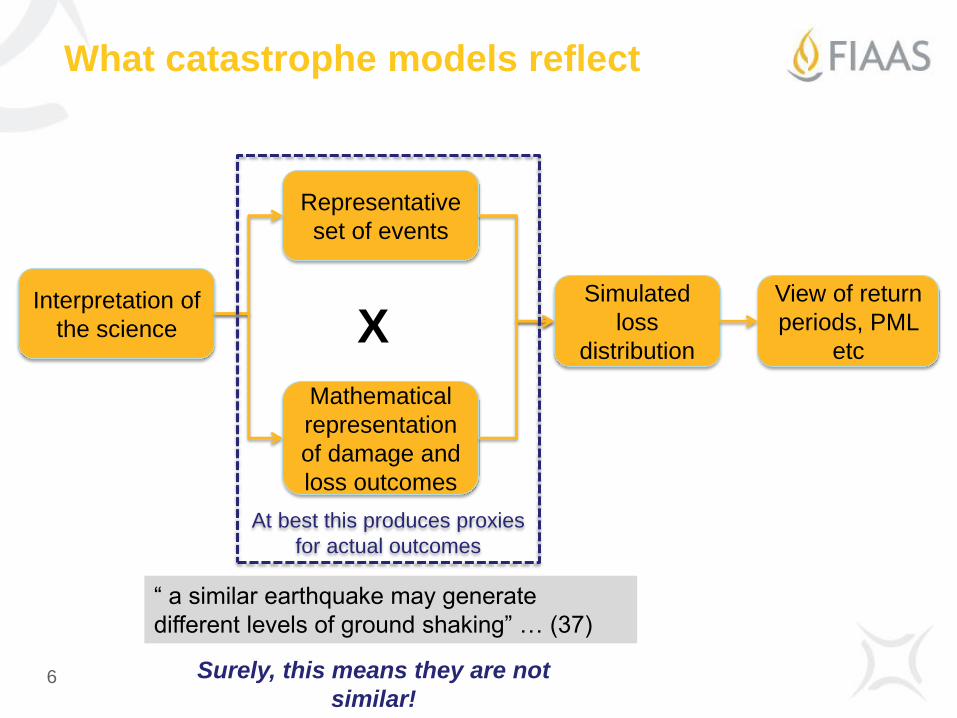

The catastrophe modelling process

5

Interpretation of

the science

Representative

set of events

Mathematical

representation

of damage and

loss outcomes

Simulated

loss

distribution

View of return

periods, PML

etc X

What catastrophe models reflect

Interpretation of

the science

Representative

set of events

Mathematical

representation

of damage and

loss outcomes

Simulated

loss

distribution

View of return

periods, PML

etc X

“ a similar earthquake may generate

different levels of ground shaking” … (37)

Surely, this means they are not

similar!

At best this produces proxies

for actual outcomes

6

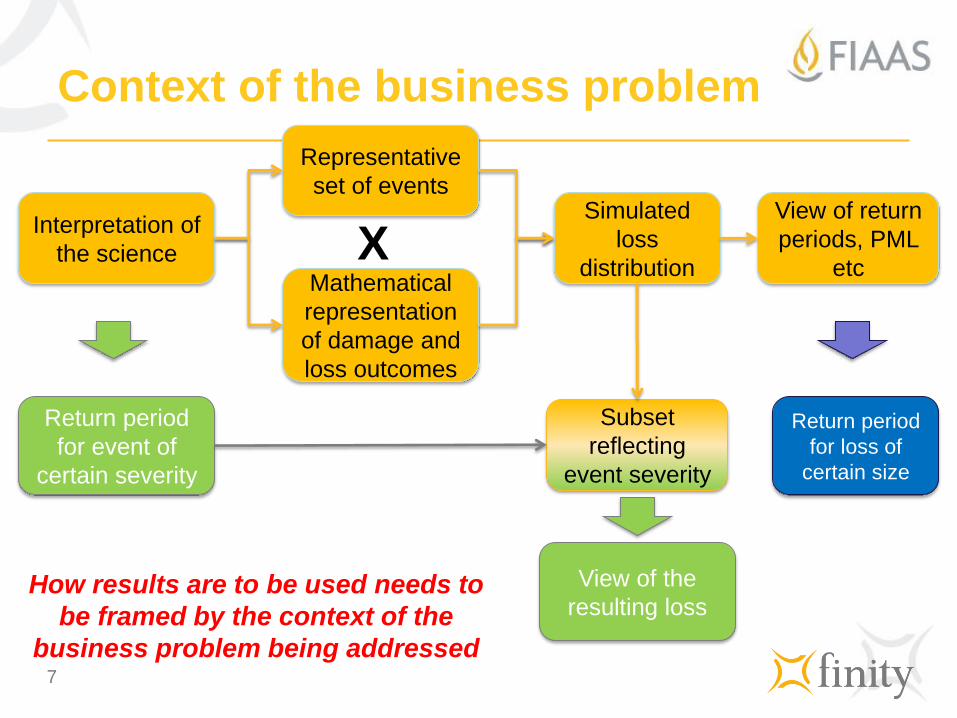

Context of the business problem

Interpretation of

the science

Representative

set of events

Mathematical

representation

of damage and

loss outcomes

Simulated

loss

distribution

View of return

periods, PML

etc X

How results are to be used needs to

be framed by the context of the

business problem being addressed

Return period

for loss of

certain size

Return period

for event of

certain severity

View of the

resulting loss

Subset

reflecting

event severity

7

EQ risk a real challenge

(and not the only one!)

For many Australian portfolios, PML is driven by EQ peril

Very few historical data points to test calibration

Scientific views continue to develop

Models lag in reflecting changes in scientists’ views

How to resolve differences between models giving very

different results

Protection of the IP in the vendor software inhibits deep

exploration and may be well beyond our area of expertise

© 2015 Finity Consulting Pty Limited

Royal Commission into Child

Sexual Abuse

National Redress & Implications for Civil

Liability

Outline

Child Sexual Abuse in Australia

National Redress Estimates

Possible Implications for Civil Liability

Reasonable Responses of Insurers

10

Institutional Child Sexual

Abuse in Australia

Sources of Information

Royal Commission Private Sessions

Close to 2,000 interviews with survivors of institutional child

sexual abuse

Claims Project Information

More than 2,700 claims resolved between 1995 and 2014

including civil claims from insurers and government bodies as

well as faith based redress schemes (Catholic & Salvation Army)

12

Sources of Information

State based Redress Schemes

Redress WA

Queensland ex gratia

Tasmanian Abuse in Care ex gratia

13

Where the Abuse Occurred

14

Estimated Child Sexual Abuse by Institution Type

Residential Care

Foster Care

Education

Other Religious Institutions

Recreation / Sport

Health and Allied

Other/unknown

Where the Abuse Occurred

NSW and VIC are most highly represented

15

0%

5%

10%

15%

20%

25%

30%

35%

40%

NSW WA QLD VIC SA TAS ACT NT

Proportion of Abuse by State - Private Session Data

National Redress

Estimates

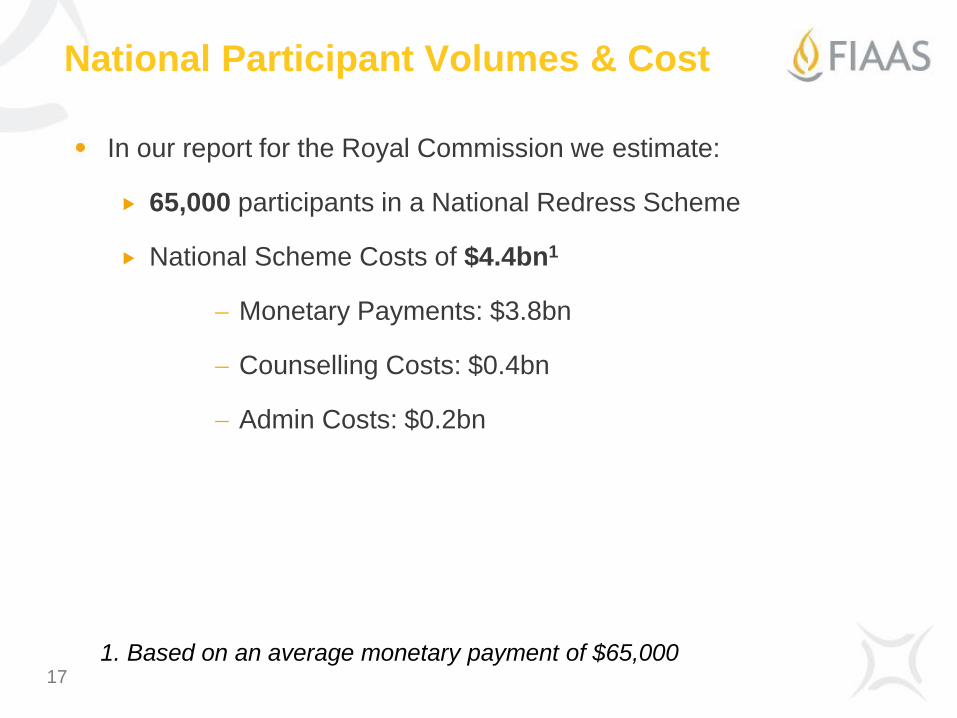

National Participant Volumes & Cost

In our report for the Royal Commission we estimate:

65,000 participants in a National Redress Scheme

National Scheme Costs of $4.4bn1

Monetary Payments: $3.8bn

Counselling Costs: $0.4bn

Admin Costs: $0.2bn

17

1. Based on an average monetary payment of $65,000

Participant Volumes

National estimates based on extrapolation of State based Redress

Schemes

18

Redress WA Extrapolation Example

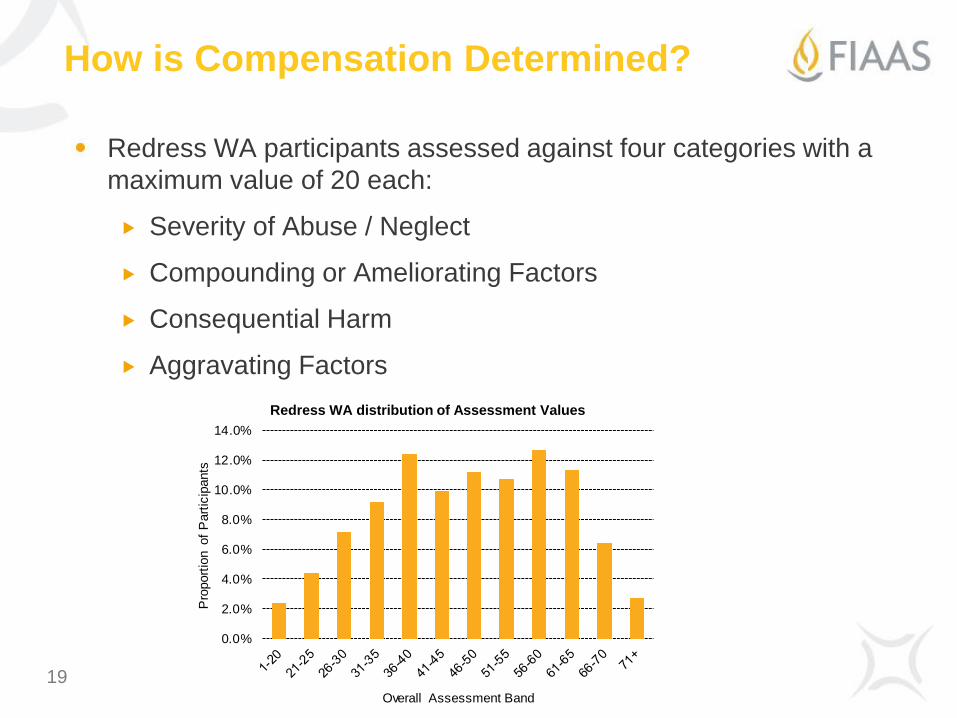

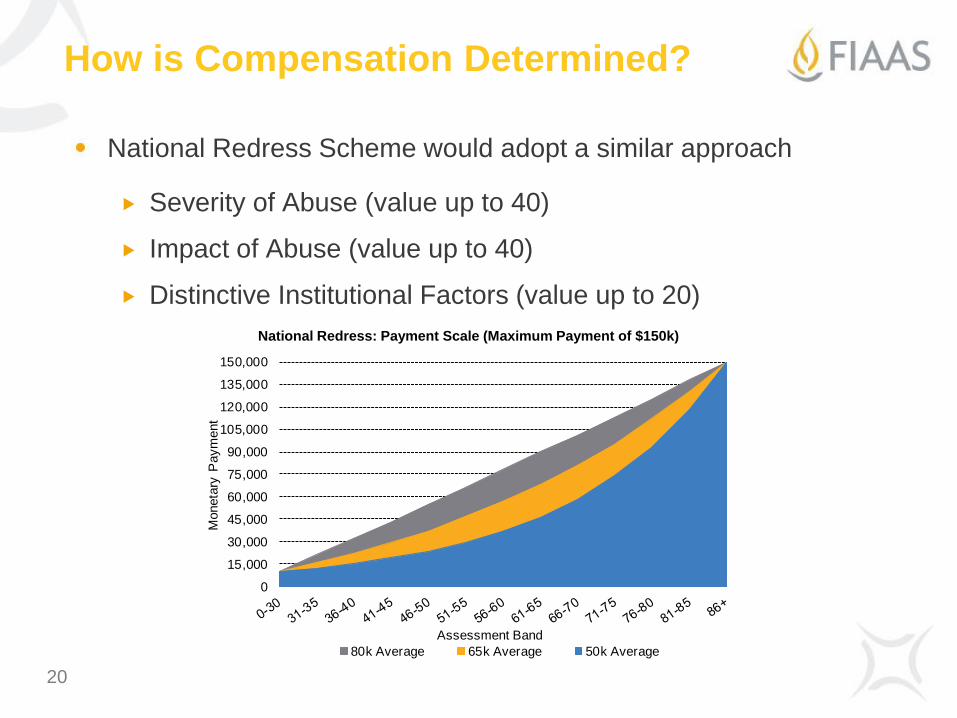

How is Compensation Determined?

Redress WA participants assessed against four categories with a

maximum value of 20 each:

Severity of Abuse / Neglect

Compounding or Ameliorating Factors

Consequential Harm

Aggravating Factors

19

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Pro

port

ion o

f P

art

icip

ants

Overall Assessment Band

Redress WA distribution of Assessment Values

How is Compensation Determined?

National Redress Scheme would adopt a similar approach

Severity of Abuse (value up to 40)

Impact of Abuse (value up to 40)

Distinctive Institutional Factors (value up to 20)

20

National Redress: Payment Scale (Maximum Payment of $150k)

0

15,000

30,000

45,000

60,000

75,000

90,000

105,000

120,000

135,000

150,000

Moneta

ry P

aym

ent

Assessment Band

80k Average 65k Average 50k Average

Possible Implications for

Civil Liability

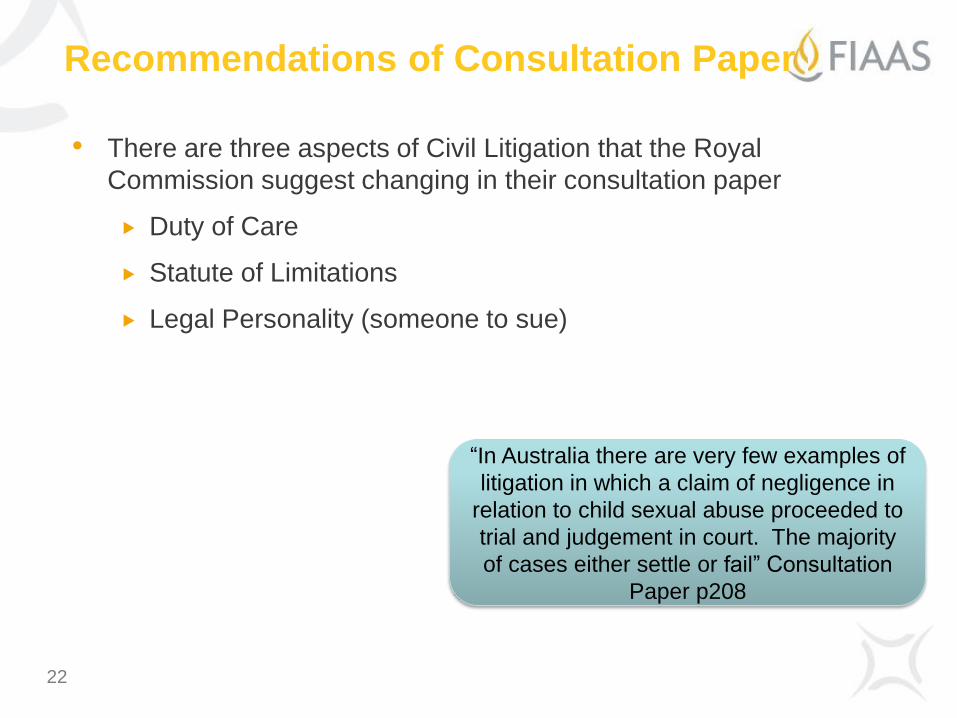

Recommendations of Consultation Paper

• There are three aspects of Civil Litigation that the Royal

Commission suggest changing in their consultation paper

Duty of Care

Statute of Limitations

Legal Personality (someone to sue)

22

“In Australia there are very few examples of

litigation in which a claim of negligence in

relation to child sexual abuse proceeded to

trial and judgement in court. The majority

of cases either settle or fail” Consultation

Paper p208

Duty of Care

• Institutions have a non-delegable duty of care to children in their

custody

• BUT this does not extend to the deliberate criminal acts of

employees or volunteers

• Vicarious liability does not apply as courts have determined abuse is

not in the normal ‘course of employment’

• Options Proposed in Consultation Paper:

• Imposing an absolute liability on institutions for acts committed by

employees, contractors or volunteers

• Imposing liability on the institutions, with the onus of proof reversed

such that the institution would have to prove that it took reasonable

precautions to prevent the abuse

• Either of these may result in major changes in civil litigation

23

Statute of Limitations / Legal Personality

24

• Limitation periods vary across states but most common is 3 years,

commencing from age 18 for minors

• The Consultation paper discusses a range of options from including

extending limitation periods to removing them altogether

• Victoria has already released a draft bill that would remove the

limitation period for criminal child abuse

• An entity can only be sued if it has a distinct ‘legal personality’ (issue

made famous in Ellis / Pell case)

• There are a number of options presented but the Royal Commission

is clear in its recommendation that this issue should be addressed

Reasonable Responses

of Insurers

Considerations for Insurers

Unlikely to be any legal liability for Redress: Insurance Contracts are

not likely to be triggered

BUT, the existence of a national redress scheme is likely to have a

strong impact on the behaviours of survivors and their legal

representatives

These behavioural changes will depend heavily on the structure and

design of the redress scheme i.e. level of payments offered, whether

or not a deed of release is required of redress participants etc.

If Statute of Limitations and Duty of Care rules are changed there

could be a large impacts for civil litigation and hence insurers

Where to from here?

There are a large number of uncertainties and contingencies that will

make it difficult for actuaries respond in their liability valuations as

yet.

However, the appointed actuary must make adequate inquiries

about the potential exposures and should not just rely on what has

been identified to date

Further, where an insurer identifies potential exposures, these risks

should be adequately addressed in the insurer’s Financial

Condition Report

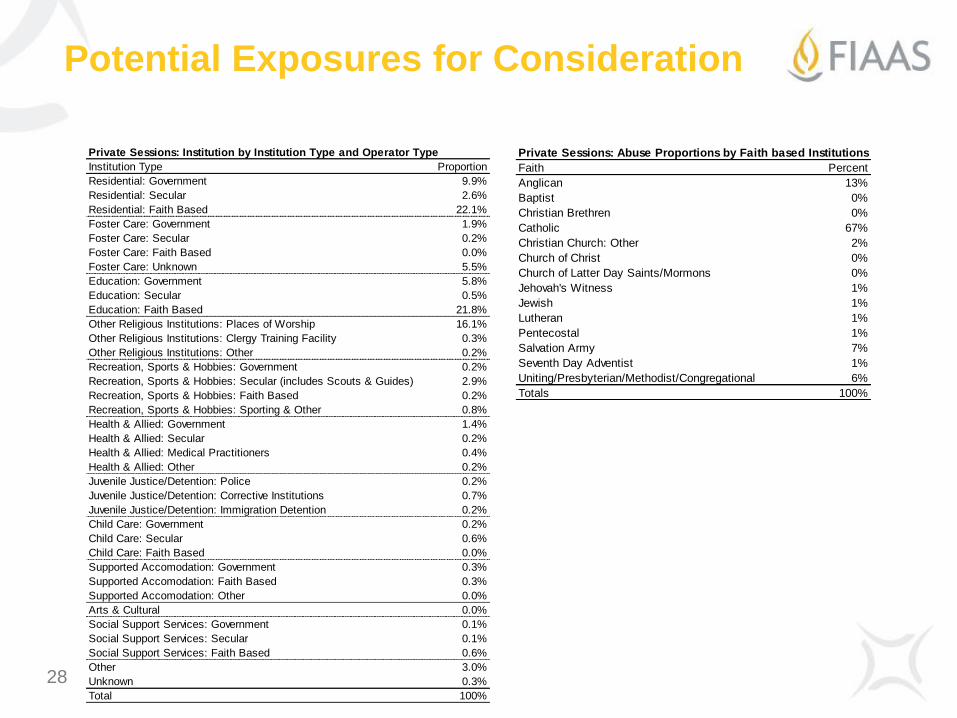

Potential Exposures for Consideration

28

Private Sessions: Institution by Institution Type and Operator Type

Institution Type Proportion

Residential: Government 9.9%

Residential: Secular 2.6%

Residential: Faith Based 22.1%

Foster Care: Government 1.9%

Foster Care: Secular 0.2%

Foster Care: Faith Based 0.0%

Foster Care: Unknown 5.5%

Education: Government 5.8%

Education: Secular 0.5%

Education: Faith Based 21.8%

Other Religious Institutions: Places of Worship 16.1%

Other Religious Institutions: Clergy Training Facility 0.3%

Other Religious Institutions: Other 0.2%

Recreation, Sports & Hobbies: Government 0.2%

Recreation, Sports & Hobbies: Secular (includes Scouts & Guides) 2.9%

Recreation, Sports & Hobbies: Faith Based 0.2%

Recreation, Sports & Hobbies: Sporting & Other 0.8%

Health & Allied: Government 1.4%

Health & Allied: Secular 0.2%

Health & Allied: Medical Practitioners 0.4%

Health & Allied: Other 0.2%

Juvenile Justice/Detention: Police 0.2%

Juvenile Justice/Detention: Corrective Institutions 0.7%

Juvenile Justice/Detention: Immigration Detention 0.2%

Child Care: Government 0.2%

Child Care: Secular 0.6%

Child Care: Faith Based 0.0%

Supported Accomodation: Government 0.3%

Supported Accomodation: Faith Based 0.3%

Supported Accomodation: Other 0.0%

Arts & Cultural 0.0%

Social Support Services: Government 0.1%

Social Support Services: Secular 0.1%

Social Support Services: Faith Based 0.6%

Other 3.0%

Unknown 0.3%

Total 100%

Private Sessions: Abuse Proportions by Faith based Institutions

Faith Percent

Anglican 13%

Baptist 0%

Christian Brethren 0%

Catholic 67%

Christian Church: Other 2%

Church of Christ 0%

Church of Latter Day Saints/Mormons 0%

Jehovah's Witness 1%

Jewish 1%

Lutheran 1%

Pentecostal 1%

Salvation Army 7%

Seventh Day Adventist 1%

Uniting/Presbyterian/Methodist/Congregational 6%

Totals 100%

© 2014 Finity Consulting Pty Limited

2013 Industry Risk Margins

29

Stand-alone Margins (OSC, Direct)

30

CTP has an

unusually

narrow range of

results

Source: Figure 1 – APRA 2013 Industry Review

Report

Other L-Tail

classes are

broadly similar Long-Tail

Commercial

Lines

Personal

Lines S-Tail P-lines

property has

lowest result

Stand-alone Margins (PL, Direct)

31

Long-

Tail

Commercial

Lines

Personal

Lines

Source: Figure 2 – APRA 2013 Industry Review

Report

Long-tail margins

are closer to

Commercial

classes

Employers

Liability is

lower than

OSC

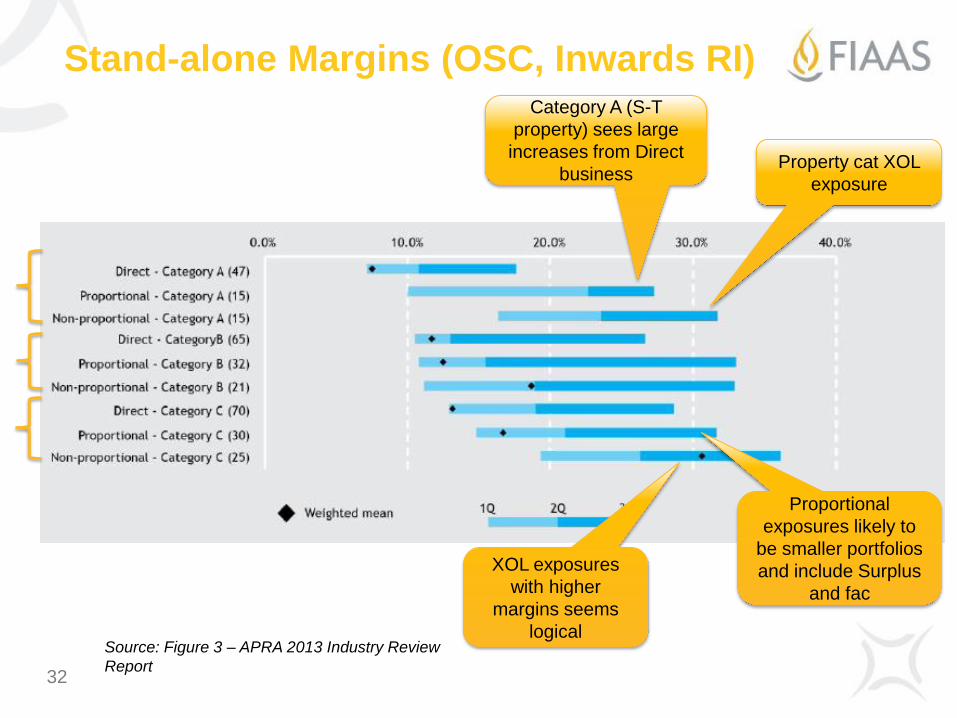

Stand-alone Margins (OSC, Inwards RI)

32

Source: Figure 3 – APRA 2013 Industry Review

Report

Category A (S-T

property) sees large

increases from Direct

business Property cat XOL

exposure

XOL exposures

with higher

margins seems

logical

Proportional

exposures likely to

be smaller portfolios

and include Surplus

and fac

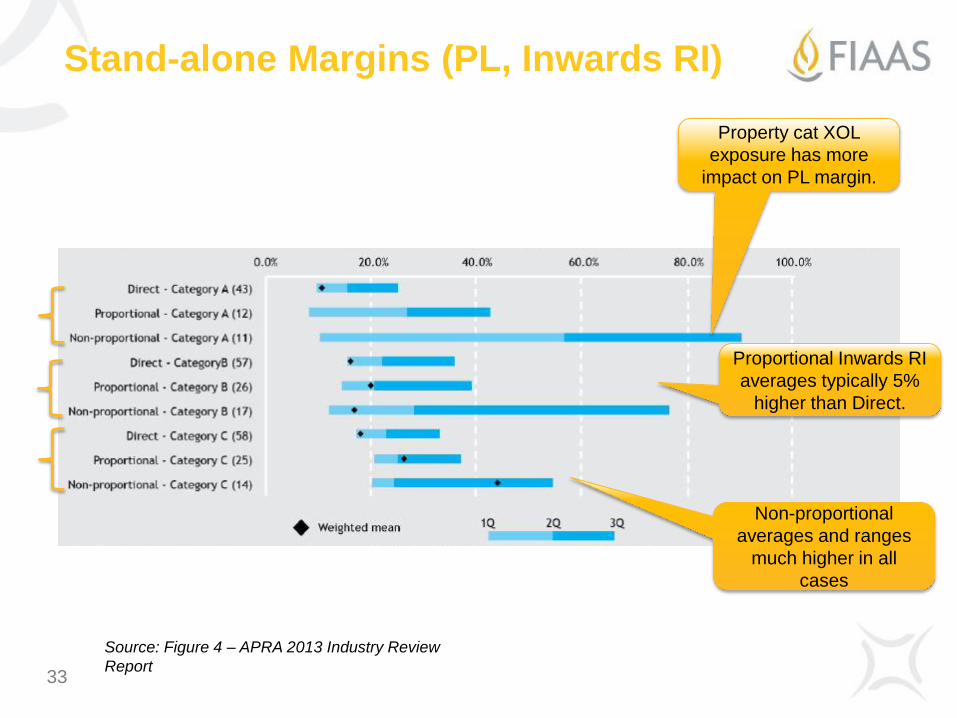

Stand-alone Margins (PL, Inwards RI)

33

Property cat XOL

exposure has more

impact on PL margin.

Source: Figure 4 – APRA 2013 Industry Review

Report

Proportional Inwards RI

averages typically 5%

higher than Direct.

Non-proportional

averages and ranges

much higher in all

cases

Approach – Stand-alone Risk Margins

Many insurers using the Institute Risk Margin Framework

More reliance on Industry Papers for PL Risk Margins (PL/OSC

scaling factors)

34

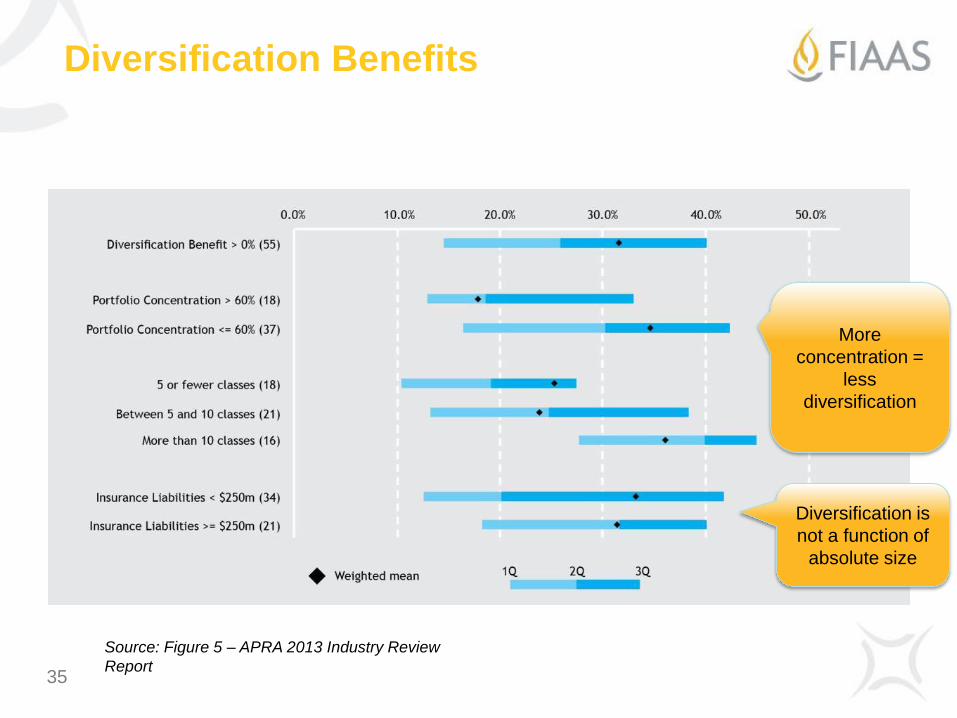

Diversification Benefits

35

Source: Figure 5 – APRA 2013 Industry Review

Report

More

concentration =

less

diversification

Diversification is

not a function of

absolute size

Changes in Industry Risk

Margins since 2007

36

Diversified Risk Margins – Direct

Risk margins have generally decreased by 1-2% (LMI is the main

exception, with sizeable increases)

OSC PL

APRA Class 2013 2007 Change 2013 2007 Change

Household 4.3% 5.6% -1.3% 7.8% 8.8% -1.0%

Domestic Motor 4.7% 5.6% -0.9% 6.5% 7.0% -0.5%

Commercial Motor 5.2% 7.1% -1.9% 7.8% 9.1% -1.3%

Travel 7.0% 7.7% -0.7% 10.1% 6.8% 3.3%

Fire and ISR 7.2% 8.5% -1.3% 11.0% 13.0% -2.0%

Marine 7.7% 9.5% -1.8% 10.2% 12.3% -2.1%

Aviation 8.9% 6.7% 2.2%

Consumer Credit 6.7% 8.2% -1.5% 13.8% 14.5% -0.7%

Other Accident 6.5% 8.2% -1.7% 10.8% 12.3% -1.5%

Mortgage 15.7% 9.4% 6.3% 26.5% 18.4% 8.1%

CTP 8.2% 9.3% -1.1% 11.0% 12.3% -1.3%

Public and Product Liability 9.6% 11.2% -1.6% 11.7% 12.6% -0.9%

Professional Indemnity 12.4% 13.8% -1.4% 15.3% 17.0% -1.7%

Employers' Liability 10.0% 12.5% -2.5% 9.8% 11.7% -1.9%

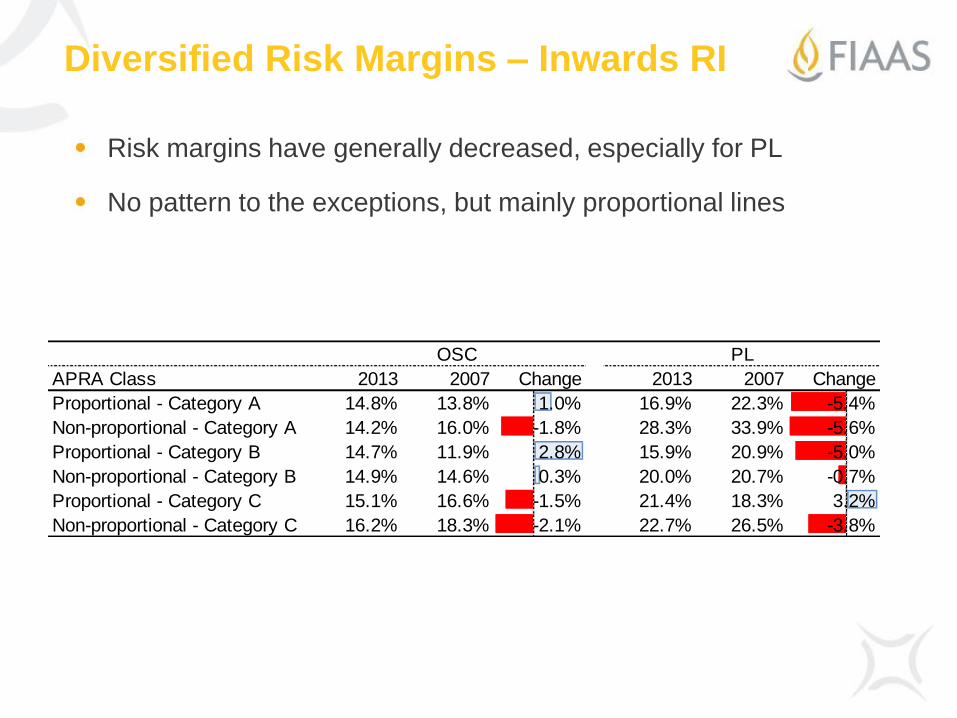

Diversified Risk Margins – Inwards RI

Risk margins have generally decreased, especially for PL

No pattern to the exceptions, but mainly proportional lines

OSC PL

APRA Class 2013 2007 Change 2013 2007 Change

Proportional - Category A 14.8% 13.8% 1.0% 16.9% 22.3% -5.4%

Non-proportional - Category A 14.2% 16.0% -1.8% 28.3% 33.9% -5.6%

Proportional - Category B 14.7% 11.9% 2.8% 15.9% 20.9% -5.0%

Non-proportional - Category B 14.9% 14.6% 0.3% 20.0% 20.7% -0.7%

Proportional - Category C 15.1% 16.6% -1.5% 21.4% 18.3% 3.2%

Non-proportional - Category C 16.2% 18.3% -2.1% 22.7% 26.5% -3.8%

© 2014 Finity Consulting Pty Limited

Benchmarking tool

Finity has created a small spreadsheet to

quickly benchmark your portfolio against the

2013 industry risk margins.

39

FIAAS 2015

40

FIAAS 2015 Agenda

Suggested dates for 2015 forums –

26 May

25 August

24 November