fiduciary responsibilities: the long & winding road

TRANSCRIPT

Fiduciary Responsibilities:

The Long & Winding Road Presented by:

Tara Mashack-Behney

Bridget Q. Casher

About us

Bridget Casher, AIF®

Investment Consultant

This presentation is provided for informational and educational purposes only and is intended to be used as a general guide in planning. It should not be viewed as personalized

investment, tax, legal, or financial advice. Please review our detailed disclosure, which will appear at the end of our presentation.

Tara Mashack-Behney,

CFP®, ChFC®

Partner & President of

Investment Advisory Services

2

Fiduciary Responsibility

3

Fiduciary responsibility

Who is a Fiduciary?

Not who, but WHAT

4

Discretionary control

Who is a Fiduciary?

Typically include:

5

Plan’s trustee(s)

Note: Accountants, TPAs, and attorneys, are not commonly in a fiduciary role

Investment Advisor

Plan’s Administrative & Investment

Committee

Named Fiduciary

Fiduciary responsibilities

Best interest of participants

6

Prudent manner Follow documents

Diversify investments Reasonable expenses

Did you know?

Personally liable

7

DOL penalty taxes Civil action

We can work it out (No text insert song)

Fiduciary Responsibility

8

Process, best practices & IPS

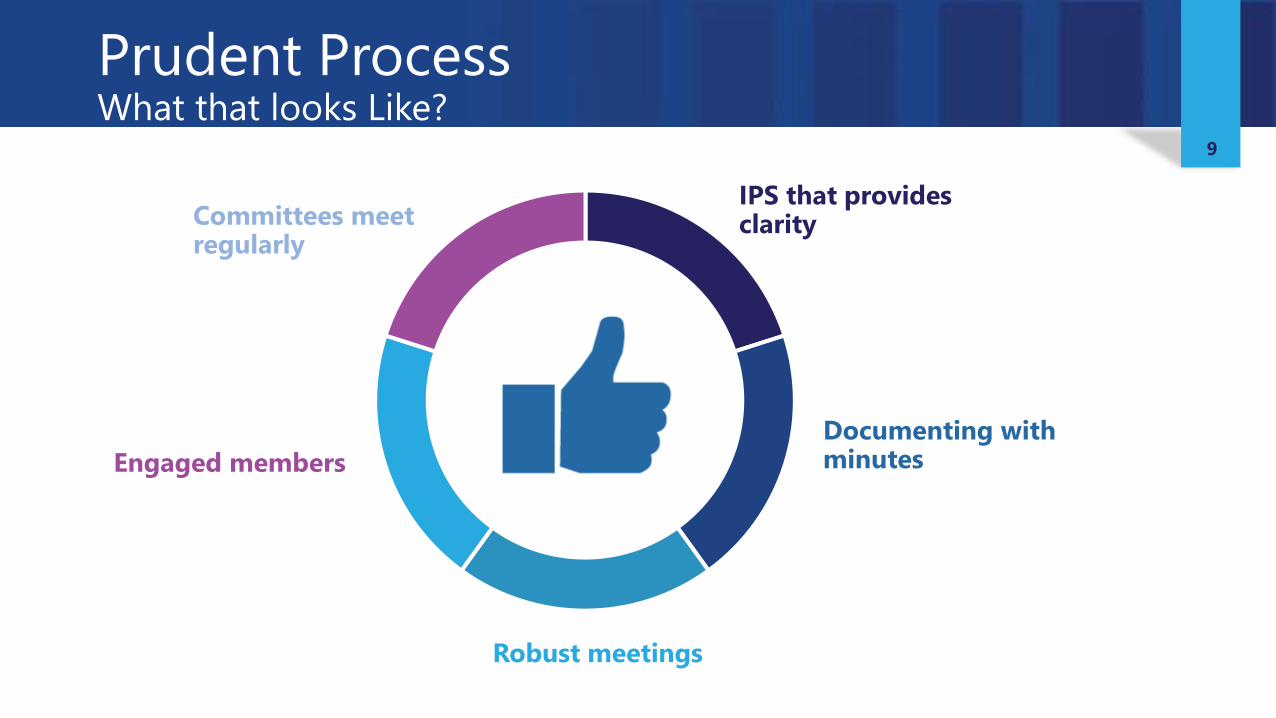

Prudent ProcessWhat that looks Like?

Committees meet regularly

9

IPS that provides clarity

Engaged members

Robust meetings

Documenting with minutes

Investment Committee Best Practices

Structure•Reasonable Size

•Diversity

•Terms

•Charter

10

Meetings•At least annually

•Agenda

•Minutes

•Plan ahead

Chair•Stay on track

•Clarity on decisions

•Establish next steps

Members•Show up

•Review materials

•Be prepared

•Ask questions

•Enthusiastic

•Seek understanding

Investment Policy Statement

Investment and Plan Objectives• Be realistic

• Within the committee’s control

11

If not meeting criteria• Replace, don’t just add

• Don’t ignore

Responsible Parties• Reminders• Training

Investment criteria

• Be specific, but not too specific

Monitoring procedures• Clarity

• Long term performance

We can work it out (No text insert song)

Fiduciary Responsibility

12

Fund menu

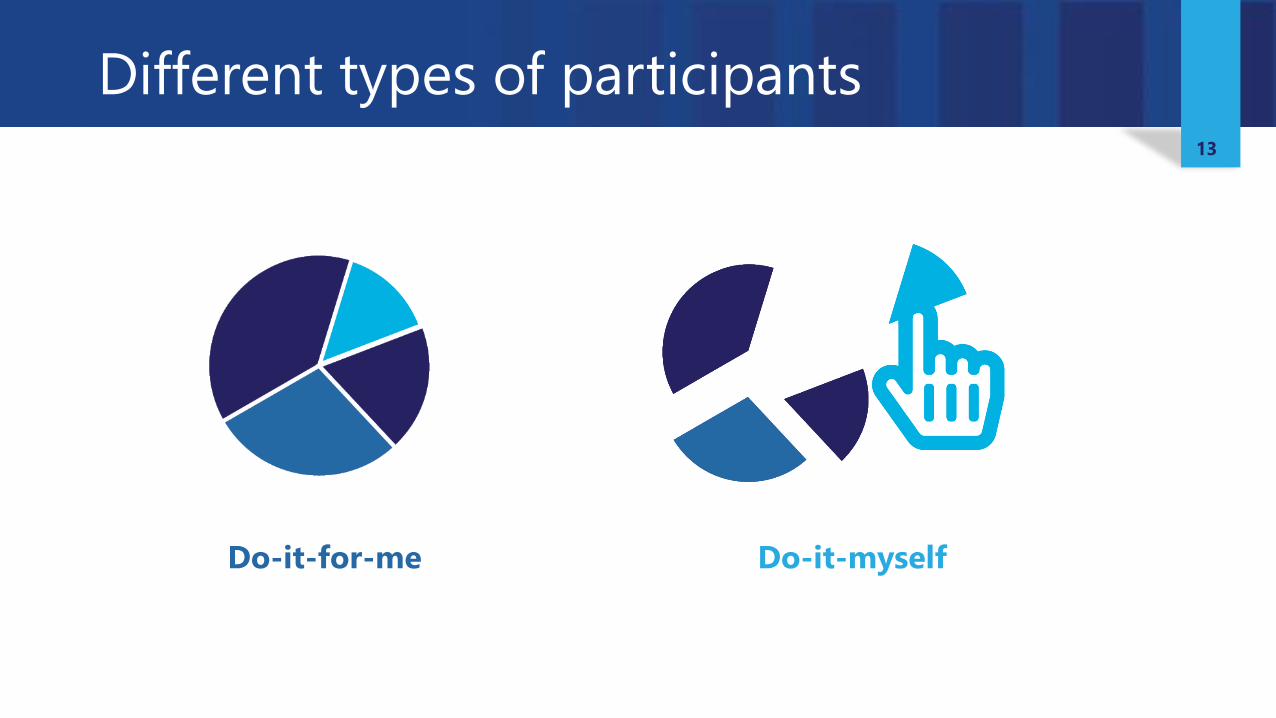

Different types of participants

Do-it-for-me Do-it-myself

13

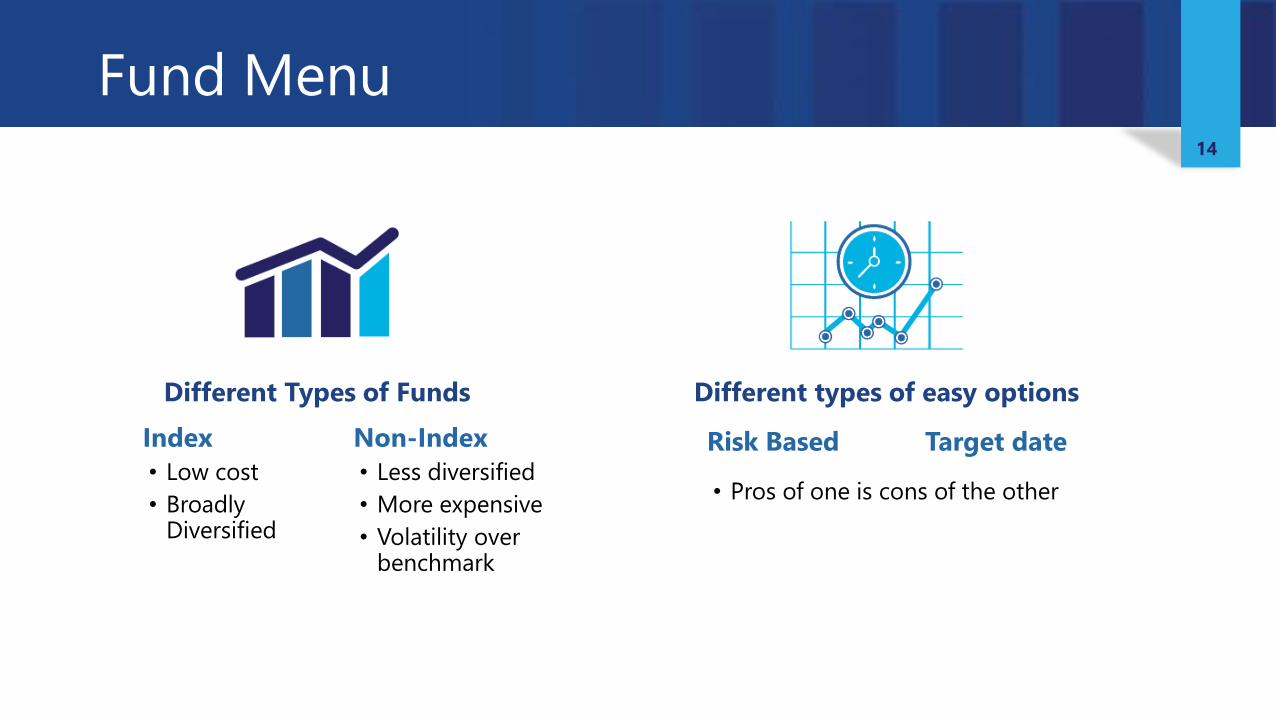

Fund Menu

Different Types of Funds Different types of easy options

14

Non-Index

• Less diversified

• More expensive

• Volatility over benchmark

Index

• Low cost

• Broadly Diversified

Risk Based Target date

• Pros of one is cons of the other

Beyond fees and performance

Glide path

15

Domestic/international splitType of fixed income

We can work it out (No text insert song)

Fiduciary Responsibility

16

Know the TRUE cost of your plan

Fees

Annual review

• Total fee

• Benchmarking

• RFP/RFI

• Document including trend

17

Revenue Sharing• Return of excess revenue

• Share class my present higher costs

• Inequitable to participants (if used to pay plan fees)

• Return to participants (best practice)

Assessment• Per Participant

• Basis Point

Questions

18

Download presentationToday’s presentations will be available for download

conradsiegel.com/elevate

Disclosures

All investment advisory services and fiduciary services are provided through Conrad Siegel Investment Advisors, Inc. (“CSIA”), a fee-for-service investment adviser registered with the U.S. Securities and Exchange Commission with its principal place of business in the Commonwealth of Pennsylvania. Registration of an Investment Advisor does not imply any level of skill or training. CSIA operates in a fiduciary capacity for its clients. Investing in securities involves the potential for gains and the risk of loss and past performance may not be indicative of future results. Any testimonials do not refer, directly or indirectly, to CSIA or its investment advice, analysis or other advisory services. CSIA and its representatives are in compliance with the current notice filing registration requirements imposed upon registered investment advisors by those states in which CSIA maintains clients. CSIA may only transact business in those states in which it is noticed filed, or qualifies for an exemption or exclusion from notice filing requirements. Any subsequent, direct communication by CSIA with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of CSIA, please contact CSIA or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov) For additional information about CSIA, please refer to the Firm’s disclosure documents, the current versions of which are available on the SEC’s Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov) and may also be made available upon request.

20