fiduciary services in a continuously changing global tax environment. pitfalls and recommendations...

TRANSCRIPT

Fiduciary Services in a continuously changing global tax environment. Pitfalls and recommendations for best practices

Pieris MarkouHead of Tax ServicesDeloitte, Cyprus

Recent Global Developments

• Cadbury Schweppes

Recent Global Developments

• Vodafone

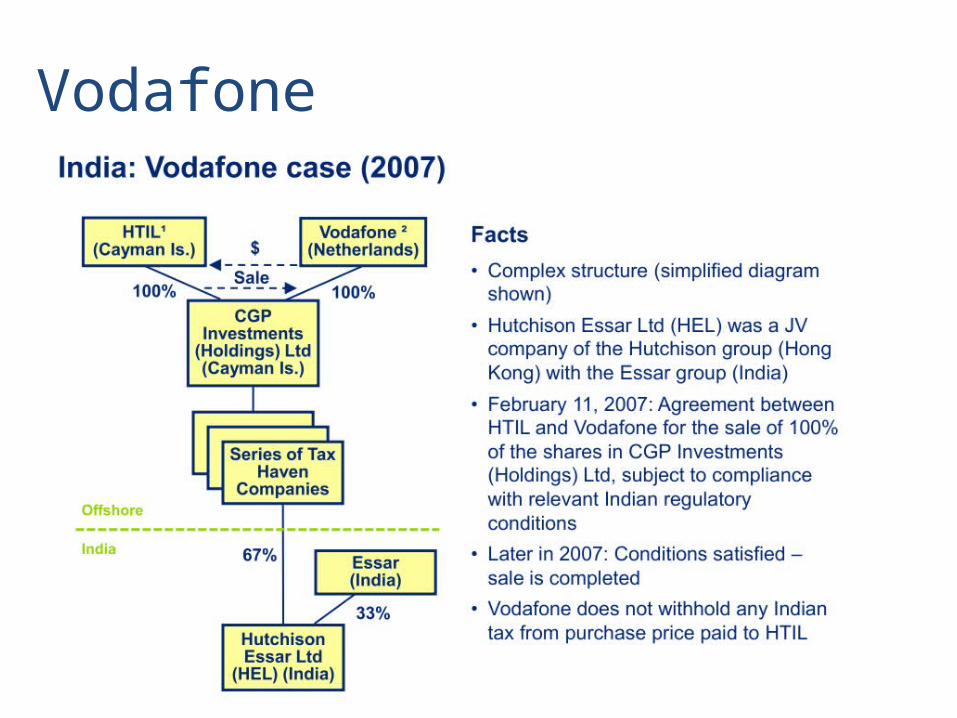

Vodafone

Recent Global Developments

• German Anti-abuse rules (1-1-2012)

Recent Global Developments

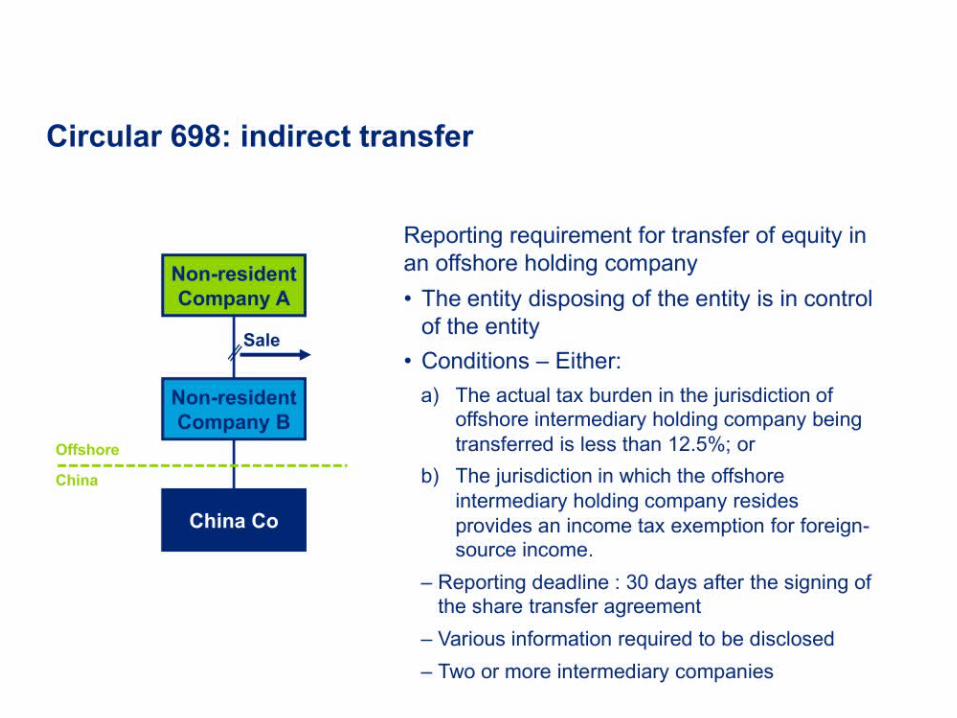

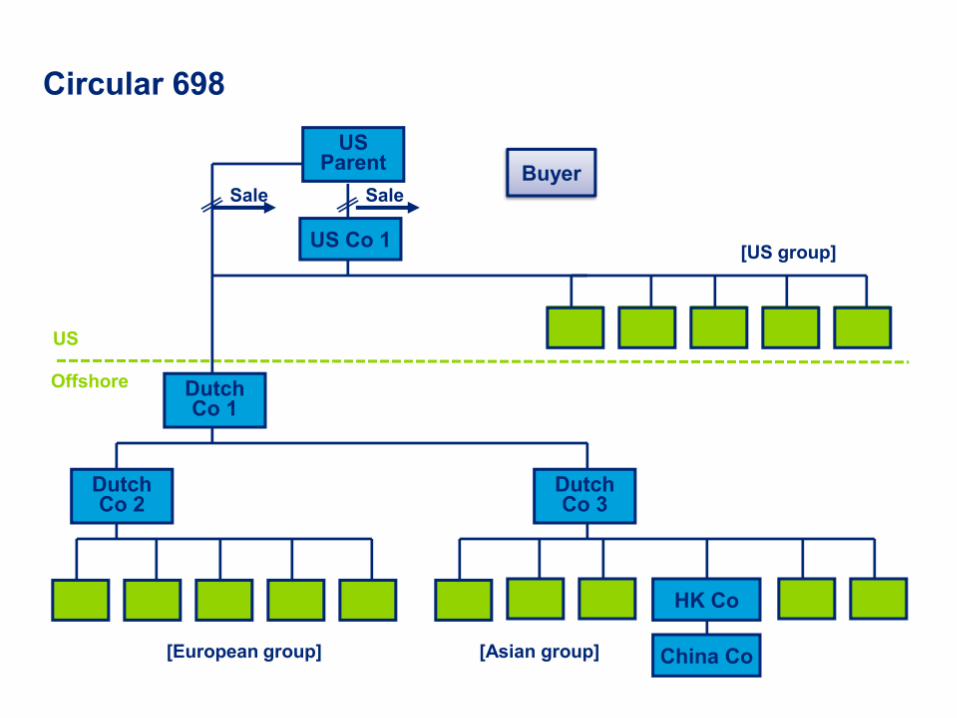

• Chinese Circulars, 698 and 601

Recent Global Developments

• Indian GAAR

Recent Global Developments

• Monetka Case

11

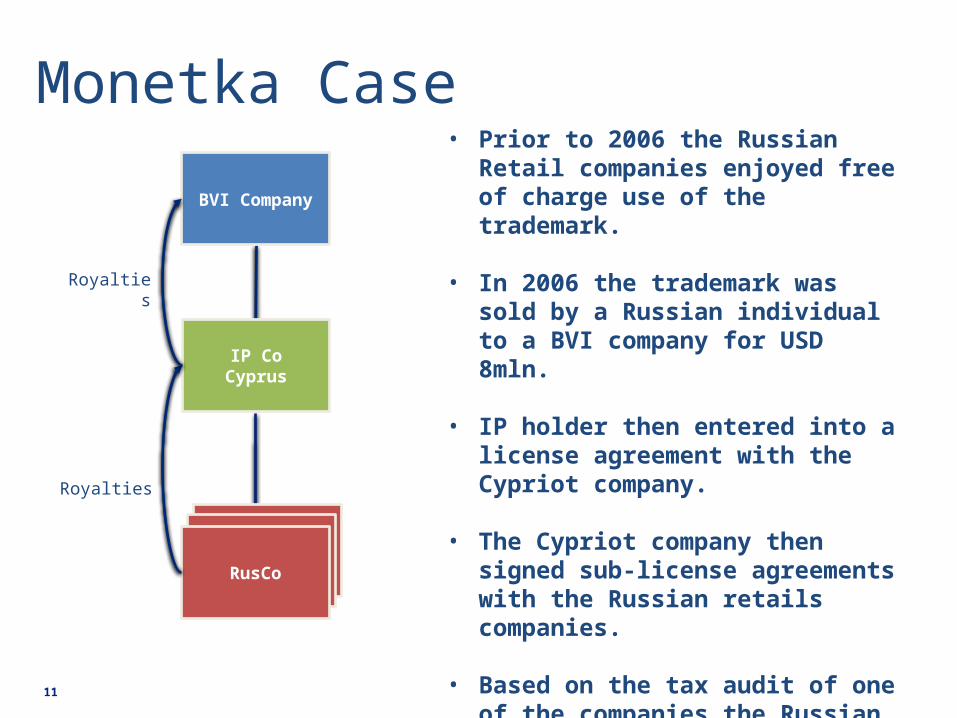

• Prior to 2006 the Russian Retail companies enjoyed free of charge use of the trademark.

• In 2006 the trademark was sold by a Russian individual to a BVI company for USD 8mln.

• IP holder then entered into a license agreement with the Cypriot company.

• The Cypriot company then signed sub-license agreements with the Russian retails companies.

• Based on the tax audit of one of the companies the Russian tax authorities challenged the deduction of USD 15mln of royalties related to 2006 – 2008.

IP CoCyprus

Foreign HoldCoForeign HoldCoRusCo

BVI Company

Royalties

Royalties

Monetka Case

Recent Global Developments

• Cadbury Schweppes• Vodafone• German Anti-abuse rules (1-1-2012)• Chinese Circulars, 601 and 698• Indian GAAR• Monetka Case

Threats

• Russia - Proposals target treaty shopping and payments to blacklisted jurisdictions

• India - Gains on sale of compulsory convertible debentures treated as interest

• Liaison offices in India under the taxman's scanner – mandatory reporting

Threats

• China - Guidance issued on determination of beneficial owner

• French court decision could trigger imposition of tax on all cross-border restructurings

Competitors

• Malta - Parliament expands royalty and participation exemption

• Singapore tax authorities clarify non-taxation of companies' gains on disposal of equity investment

• Singapore: Home for billionaires and superstars• Luxembourg rolls out the red carpet for alternative

investment funds

Light at the end of the tunnel

• Denmark - Authorities rule EU parent is beneficial owner of deemed dividends

• Italy - Tax authorities loose beneficial ownership case

Opportunities

China

IndiaRussiaBrazil

South Africa

Opportunities

ChinaIndia

RussiaBrazil

South Africa

Opportunities

ChinaIndia

RussiaBrazil

South Africa

Opportunities

CI

RB

S

Structuring your tax affairs in the BRICS

• Strong focus on anti-avoidance• Close collaboration to crack down on tax evasion• Use of beneficial ownership concept and extended

Black Lists• Strict transfer pricing legislation• Non-OECD members

Structuring your tax affairs in the BRICS

• Aggressive in tax enforcement and collection• Taxation of indirect equity transfers (Vodafone &

China’s circular 698)• Non-OECD members – possible double taxation• Shift from traditional holding company jurisdictions

to jurisdictions with legitimate substance• No one-size-fits-all

The way forward• Greater emphasis on Beneficial Ownership

• Increased economic and commercial substance

• Real decision making by directors

The way forward• Continuous and proper compliance with local

regulations

• Increased reporting obligation in operating locations

• Full transparency and exchange of information

Opportunities

CI

VE

T

s

Opportunities

ColombiaIndonesia

VietnamEgypt

Turkey