fiem industries limited - myirisbreport.myiris.com/firstcall/fieindus_20130912.pdf · cmp 185.00...

TRANSCRIPT

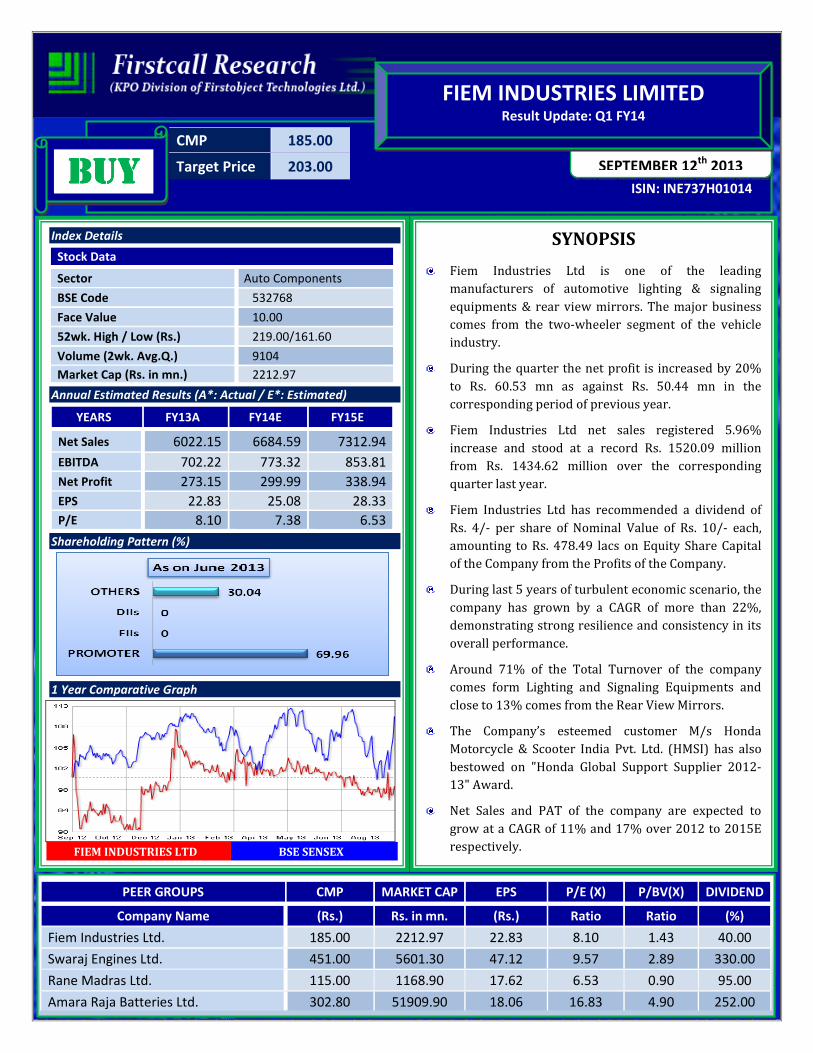

CMP 185.00

Target Price 203.00

ISIN: INE737H01014

SEPTEMBER 12th

2013

FIEM INDUSTRIES LIMITED

Result Update: Q1 FY14

BUYBUYBUYBUY

Index Details

Stock Data

Sector Auto Components

BSE Code 532768

Face Value 10.00

52wk. High / Low (Rs.) 219.00/161.60

Volume (2wk. Avg.Q.) 9104

Market Cap (Rs. in mn.) 2212.97

Annual Estimated Results (A*: Actual / E*: Estimated)

YEARS FY13A FY14E FY15E

Net Sales 6022.15 6684.59 7312.94

EBITDA 702.22 773.32 853.81

Net Profit 273.15 299.99 338.94

EPS 22.83 25.08 28.33

P/E 8.10 7.38 6.53

Shareholding Pattern (%)

1 Year Comparative Graph

FIEM INDUSTRIES LTD BSE SENSEX

SYNOPSIS

Fiem Industries Ltd is one of the leading

manufacturers of automotive lighting & signaling

equipments & rear view mirrors. The major business

comes from the two-wheeler segment of the vehicle

industry.

During the quarter the net profit is increased by 20%

to Rs. 60.53 mn as against Rs. 50.44 mn in the

corresponding period of previous year.

Fiem Industries Ltd net sales registered 5.96%

increase and stood at a record Rs. 1520.09 million

from Rs. 1434.62 million over the corresponding

quarter last year.

Fiem Industries Ltd has recommended a dividend of

Rs. 4/- per share of Nominal Value of Rs. 10/- each,

amounting to Rs. 478.49 lacs on Equity Share Capital

of the Company from the Profits of the Company.

During last 5 years of turbulent economic scenario, the

company has grown by a CAGR of more than 22%,

demonstrating strong resilience and consistency in its

overall performance.

Around 71% of the Total Turnover of the company

comes form Lighting and Signaling Equipments and

close to 13% comes from the Rear View Mirrors.

The Company’s esteemed customer M/s Honda

Motorcycle & Scooter India Pvt. Ltd. (HMSI) has also

bestowed on "Honda Global Support Supplier 2012-

13" Award.

Net Sales and PAT of the company are expected to

grow at a CAGR of 11% and 17% over 2012 to 2015E

respectively.

PEER GROUPS CMP MARKET CAP EPS P/E (X) P/BV(X) DIVIDEND

Company Name (Rs.) Rs. in mn. (Rs.) Ratio Ratio (%)

Fiem Industries Ltd. 185.00 2212.97 22.83 8.10 1.43 40.00

Swaraj Engines Ltd. 451.00 5601.30 47.12 9.57 2.89 330.00

Rane Madras Ltd. 115.00 1168.90 17.62 6.53 0.90 95.00

Amara Raja Batteries Ltd. 302.80 51909.90 18.06 16.83 4.90 252.00

QUARTERLY HIGHLIGHTS (STANDALONE)

Results updates- Q1 FY14,

Fiem Industries Ltd is a formidable name in

automotive lighting industries with 8 state of the art

manufacturing units. The Company is engaged into

manufacturing of auto components and main

product line are Automotive Lighting & Signaling

Equipments, Rear View Mirrors, Sheet Metal Parts,

Plastic Moulded Parts and some other components.

Company supplies these parts to all leading OEMs in

India and also exports to other countries and has

reported its financial results for the quarter ended

30 JUNE, 2013.

Months JUNE-13 JUNE-12 % Change

Net Sales 1520.09 1434.62 5.96%

PAT 60.53 50.44 20.00%

EPS 5.06 4.22 20.00%

EBITDA 178.17 165.74 7.50%

The company achieved a turnover of Rs. 1520.09 million for the 1st quarter of the current year 2013-14 as

against Rs. 1434.62 millions in the corresponding quarter of the previous year. The company has reported an

EBITDA of Rs. 178.17 millions and a net profit of Rs. 60.53 million against Rs. 50.44 million reported respectively

in the corresponding quarter of the previous year. The company has reported an EPS of Rs. 5.06 for the 1st

quarter as against an EPS of Rs. 4.22 in the corresponding quarter of the previous year.

Break up of Expenditure:

During the quarter Total Expenditure rose by 6 per cent and increase in Cost of Material consumed with

consideration of other Expenses and Employee benefit expenses. Total expenditure in Q1 FY14 stood to Rs.

1394.44 million as against Rs. 1314.10 million in Q1 FY13.

Employees’ benefits expenses incurred Rs.197.46 against Rs.176.32 millions in the corresponding period of the

previous year. Purchase of stock in trade is at Rs 34.39 mn in Q1 FY14 against Rs. 23.62 mn in Q1 FY13. In the

same quarter of Q1 FY14 Other Expenditure faced at Rs. 242.77 million where as costs of material consumed at

Rs. 907million in Q1 FY14 against Rs. 844.95 million are the primarily attributable to growth of expenditure.

Latest Updates

� The Company recently has selected by its esteemed customer Honda as their Global Supplier for selected

high end Motorcycle of 670 cc. Esteemed customer M/s Honda Motorcycle & Scooter India Pvt. Ltd.(HMSI)

has also bestowed on us "Honda Global Support Supplier 2012-13" Award.

COMPANY PROFILE

Fiem Industries Ltd. is one of the leading manufacturers of automotive lighting & signaling equipments and rear

view mirrors. The major business comes from the two-wheeler segment of the vehicle industry. It has a wide

range of lighting systems and rear view mirrors, sheet metals parts and plastic components for two and four

wheeler and its diversified products portfolio ranging form rear view mirrors, head lamps, tail lamps, roof lamps,

wheel covers, warning triangle, complete rear fender assembly, frame assembly, mudguards and various sheet

metal & plastic parts etc. is capable of catering to the needs of almost all segments of automobile industry viz.,

four-wheelers, LCVs, HTVs and tractors. The company has one foreign subsidiary i.e. 'Fiem Industries Japan Co.

Ltd.' incorporated in Japan.

FIEM has acquired certifications such as ISO 9002, QS 9002, QS 9000, ISO/ TS 16949:2002, & ISO 9001. It has

also acquired certification for conformity of production form RDW Netherlands. FIEM has also been accredited

with ISO14001-2004 Certification for Environment Management Systems. FIEM employees are constantly being

trained to meet the customer's specific requirements as per TQM. FIEM has become a Tier I Supplier not only in

India but also in Europe and USA.

FIEM is a known brand in Automotive Lighting and Rear View Mirrors in international OEMs and is considered as

synonymous of High Quality & Low Cost manufacturing Company.

Company has diversified into LED indoor and outdoor lighting business and manufacturing a large range of LED

products like LED Home Lighting, LED Bulbs and tubes, LED Solar Street Lighting, Multi-Functional Torches cum

Flasher Lights, LED Solar Lanterns, LED Display panels for buses and trucks and LED display signal systems for

Railways etc. which also forms part of above turnover.

Products

Fiem Industries Ltd is one of the leading manufacturers of automotive lighting & signaling equipments and rear

view mirrors for automobiles.

• Two Wheelers

� Kinetic

� Bajaj

� Hero Honda

� LML

� Yamaha

� TVS

� Honda

� Suzuki

� Piaggio

� Royal Enfield

• Four wheelers

� Maruti Suzuki

� Tata

� Daewoo

� Reva car

� Pre, Automobiles H.

Motors

� DCM Toyota

� Force Motors

� Ashok Leyland

� Peugeot

� Hyundai/ General

Motors

� Trailer & Truck

� Trailer & Car

� Swaraj mazda

� International Tractor

� Ford

� HMT

� Tafe

� Indo Form/ Preet

Tractor

� JCB Terex Vectr

� M7M VST Tractor

Trailers

• Auxillary Lamps

� Halogen Lamps

� Work lamps

• Warning Tringles

• Reflex Reflector

• Led Lamps

• Led Luminaires

Clients

• Two - Wheeler Segment (Domestic OEM Customers)

• Two - Wheeler Segment (Global OEM Customers)

• Four - Wheeler Segment (Domestic OEM Customers)

• Four - Wheeler Segment (Global OEM Customers)

FINANCIAL HIGHLIGHT (STANDALONE) (A*- Actual, E* -Estimations & Rs. In Millions)

Balance Sheet as at March31, 2012 -2015E

Value(Rs.in.mn) FY12A FY13A FY14E FY15E

EQUITY AND LIABILITIES:

Shareholders’ Funds:

Share Capital 119.62 119.62 119.62 119.62

Reserves and Surplus 1323.71 1562.33 1723.08 2062.01

a) Net worth (a) 1443.33 1681.95 1842.70 2181.63

Non-Current Liabilities:

Long-term borrowings 949.90 761.84 876.12 981.25

Deferred Tax Liabilities [Net] 193.04 242.14 305.10 378.32

Other Long Term Liabilities 25.92 17.37 28.82 42.65

Long Term Provisions 6.24 7.94 9.93 11.91

b) Long term liabilities 1175.10 1029.29 1219.95 1414.13

Current Liabilities:

Short-term borrowings 441.65 303.54 346.04 387.56

Trade Payables 644.09 745.61 864.91 979.08

Other Current Liabilities 429.26 494.05 592.86 687.72

Short Term Provisions 53.02 73.71 89.19 107.03

c) Current Liabilities 1568.02 1616.91 1892.99 2161.38

Total (a+b+c) 4186.45 4328.15 4955.65 5757.14

ASSETS:

Non-Current Assets:

Tangible Assets 2805.42 2915.54 3318.71 3837.59

Intangible Assets 9.64 10.87 17.94 27.80

Capital work-in-progress 13.73 14.79 16.27 17.90

Other non-current assets 0.99 1.08 1.56 2.02

Non Current Investments 0.46 0.46 0.46 0.46

Long Term Loans and Advances 72.15 80.87 63.89 50.47

d) Non-Current Assets 2902.39 3023.61 3418.82 3936.24

Current Assets:

Inventories 457.37 486.66 525.59 565.01

Trade Receivables 670.70 688.17 894.62 1145.11

Cash and Bank Balances 52.66 15.32 18.38 21.69

Short Term Loans and Advances 101.57 108.93 92.59 83.33

Other Current Assets 1.76 5.46 5.64 5.75

e) Current Assets 1284.06 1304.54 1536.83 1820.90

Total (d+e) 4186.45 4328.15 4955.65 5757.14

Annual Profit & Loss Statement for the period of 2012 to 2015E

Value(Rs.in.mn) FY12 FY13 FY14E FY15E

Description 12m 12m 12m 12m

Net Sales 5335.42 6022.15 6684.59 7312.94

Other Income 3.01 3.53 4.59 5.51

Total Income 5338.43 6025.68 6689.18 7318.44

Expenditure -4658.86 -5323.46 -5915.86 -6464.64

Operating Profit 679.57 702.22 773.32 853.81

Interest -207.56 -129.30 -142.23 -156.45

Gross profit 472.01 572.92 631.09 697.35

Depreciation -168.84 -183.48 -196.32 -206.14

Profit Before Tax 303.17 389.44 434.76 491.21

Tax -91.73 -116.29 -134.78 -152.28

Net Profit 211.44 273.15 299.99 338.94

Equity capital 119.62 119.62 119.62 119.62

Reserves 1183.48 1423.09 1723.08 2062.01

Face value 10.00 10.00 10.00 10.00

EPS 17.68 22.83 25.08 28.33

Quarterly Profit & Loss Statement for the period of 31 DEC, 2012 to 30 SEP, 2013E

Value(Rs.in.mn) 31-Dec-12 31-Mar-13 30-June-13 30-Sep-13E

Description 3m 3m 3m 3m

Net sales 1501.07 1653.56 1520.09 1541.37

Other income 0.42 0.91 0.49 0.51

Total Income 1501.49 1654.47 1520.58 1541.89

Expenditure -1323.93 -1457.51 -1342.41 -1364.11

Operating profit 177.56 196.96 178.17 177.77

Interest -39.12 -8.88 -36.99 -39.21

Gross profit 138.44 188.08 141.18 138.56

Depreciation -44.90 -50.08 -52.03 -53.59

Profit Before Tax 93.54 138.00 89.15 84.97

Tax -27.38 -43.90 -28.62 -26.77

Net Profit 66.16 94.10 60.53 58.21

Equity capital 119.62 119.62 119.62 119.62

Face value 10.00 10.00 10.00 10.00

EPS 5.53 7.87 5.06 4.87

Ratio Analysis

Particulars FY12 FY13 FY14E FY15E

EPS (Rs.) 17.68 22.83 25.08 28.33

EBITDA Margin (%) 12.74 11.66 11.57 11.68

PBT Margin (%) 5.68 6.47 6.50 6.72

PAT Margin (%) 3.96 4.54 4.49 4.63

P/E Ratio (x) 10.47 8.10 7.38 6.53

ROE (%) 16.23 17.71 16.28 15.54

ROCE (%) 31.48 29.76 28.96 28.18

EV/EBITDA (x) 1.07 0.93 0.82 0.72

Book Value (Rs.) 5.23 5.11 4.72 4.36

P/BV 108.94 128.97 154.05 182.38

Charts

OUTLOOK AND CONCLUSION

� At the current market price of Rs. 185.00, the stock P/E ratio is at 7.38 x FY14E and 6.53 x FY15E

respectively.

� Earning per share (EPS) of the company for the earnings for FY14E and FY15E is seen at Rs.25.08 and

Rs.28.33 respectively.

� Net Sales and PAT of the company are expected to grow at a CAGR of 11% and 17% over 2012 to 2015E

respectively.

� On the basis of EV/EBITDA, the stock trades at 4.72 x for FY14E and 4.36 x for FY15E.

� Price to Book Value of the stock is expected to be at 1.20 x and 1.01 x respectively for FY14E and FY15E.

� We expect that the company surplus scenario is likely to continue for the next three years, will keep its

growth story in the coming quarters also. We recommend ‘BUY’ in this particular scrip with a target price of

Rs.203.00 for Medium to Long term investment.

INDUSTRY OVERVIEW

The Indian market conditions are acting as a catalyst for luxury and premium carmakers, which receive a boost

from new launches and numerous offers from carmakers, thereby giving impetus to the auto components

industry. The industry is expected to invest around Rs 70 billion (US$ 1.17 billion) over the next three years on

new projects, as per rating agency ICRA’s estimates. The investments are foreseen on back of auto

manufacturers, such as Maruti Suzuki, Hero MotoCorp and Ford, planning to establish green field facilities in

Gujarat, prompting component makers to invest around these facilities.

In addition, the automotive aftermarket is poised for robust growth, as per a McKinsey & Co report titled, ‘Scaling

the Indian Automotive Aftermarket: Path to Profitable Growth’. The report highlighted that the growth outlook

continues to be positive, driven by sustained increase in vehicle population and a shift towards higher-end

vehicles.

Market Structure

The Indian auto component industry’s turnover is reported to be US$ 40.6 billion in 2012-13 and is projected to

touch US$ 115 billion by 2020-21, according to data provided by Automotive Component Manufactures

Association (ACMA). The industry is estimated to grow at a compound annual growth rate (CAGR) of 14 per cent

during 2013-21. Moreover, the industry’s exports were recorded at US$ 9.3 billion in 2012-13 and are projected

to touch US$ 30 billion by 2020-21, as per ACMA.

More so, the tyre production in India is anticipated to reach 191 million units by the end of FY 2016, highlighted

an RNCOS research report titled, 'Indian Tyre Industry Forecast to 2015'. The manufacturers are expected to

invest huge amount into the industry over the next few years, with a major proportion of this investment

directed towards the radial tyre capacity expansion.

India: The Global Auto Hub

Indicative of growing relevance of Indian technological expertise; Pratt & Whitney, the US-based aerospace

engine manufacturer, is exploring opportunities to source components for its global operations from India.

• Wheels India entered into a 10 year technical agreement with Turkish manufacturing and engineering

company EGE Endustri, one of the major suppliers to original equipment market (OEM) in Europe. As per

the agreement, Wheels India would get technology access in the Lift axle market

• Honda Cars India Ltd (HCIL) plans to export diesel engine components to Asian and European markets

from India

• Apollo Tyres has opened a sales office in Bangkok, Thailand, making it the hub for Association of

Southeast Asian Nations (ASEAN) operations. This is the second hub outside the company's operations in

India

Furthermore, the amount of cumulative FDI inflow into the Indian automobile industry during April 2000 to

April 2013 was worth US$ 8.32 million, amounting to 4 per cent of the total FDI inflows (in terms of US$), as per

data published by Department of Industrial Policy and Promotion (DIPP), Ministry of Commerce, Government of

India.

Key Developments & Investments

� Valvoline Cummins will begin production of automotive lubricants at its new manufacturing and

packaging plant at Ambernath, near Thane district. Western India is a manufacturing hub that has the

largest consumption of industrial lubricants among all regions,” according to Mr Sam Mitchell, President

of Ashland Consumer Markets, a unit of Ashland Inc

� Italian auto component maker Streparava Holding SPA announced that it has bought out its Indian

partner Sansera Engineering from the joint venture (JV) that makes engine parts

� Hyundai Motor India Foundation has opened an automobile servicing training centre at the Government

Industrial Training Institute (ITI), Ulundurpet, Tamil Nadu (TN). The firm plans to set up 10 more such

centres at various ITI's in the state this year.

� Robert Bosch GmbH is to set up a joint venture (JV) with two Japanese companies to develop lithium-ion

batteries to double the range of electric vehicles, the companies. The plan is to boost the capacity of

lithium-ion batteries to enable electric vehicles to travel about 400 km per charge from the current range

of 180 to 240 km, while reducing weight and volume

� JSW Steel will complete its new plant in Bellary, Karnataka by December 2013. The 2.3 million tonne

(MT) capacity plant, being set up at an investment of US$ 1 billion, is specially designed to make products

for the Indian automotive industry

� The Mangalore-based Arvind Motors Pvt Ltd (dealers of Tata Motors) will launch its new 3S (sales,

service, spares) facility in Mangalore

Government Initiatives

The Union Budget 2013-14 presented by Mr P Chidambaram, the Union Finance Minister, Government of India,

in the Parliament on February 28, 2013, had a few add-ons for the industry. The analysis by Deloitte on the Union

Budget highlighted the following:

� The period of concession available for specified part of electric and hybrid vehicles till April 2013 has

been extended upto March 31, 2015

� The basic customs duty (BCD) on imported luxury goods such as high-end motor vehicles, motor cycles,

yachts and similar vessels was increased. The duty was raised from 75 percent to 100 percent on cars/

motor vehicles (irrespective of engine capacity) with CIF value more than US$ 40,000; from 60 percent to

75 percent on motorcycles with engine capacity of 800 cc or more and on yachts and similar vessels from

10 percent to 25 percent

� An increase in excise duty from 27 to 30 per cent has been allowed for SUVs with engine capacity

exceeding 1,500 cc, while excise duty was decreased from 80 to 72 per cent, in case of SUVs registered

solely for taxi purposes

� An exemption from BCD on lithium ion automotive battery for manufacture of lithium ion battery packs

for supply to manufacturers of hybrid and electric vehicles

� The excise duty on chassis of diesel motor vehicles for transport of goods reduced from 14 per cent to 13

per cent

Additionally, the Automotive Mission Plan (AMP) 2006-2016, highlighted that the contribution of automotive

sector in the gross domestic product (GDP) is expected to double, reaching to touch a turnover worth US$ 145

billion in 2016, with special focus on export of small cars, multi-utility vehicles (MUV), two & three wheelers and

auto components.

Road Ahead

Global and Indian manufacturers are focussing their efforts to develop innovative products, technologies and

supply chains in the industry. With an ever-increasing influx of car makers, Mr Srivats Ram, MD, Wheels India,

observed that this is an opportunity for us to build our internal strength.

Over the medium term, factors such as growing thrust on localisation and expanding businesses in new

geographies should allow the components industry to grow at a relatively faster pace than the auto OEM

segment, according to a study by ICRA. Overall, the market foresees better demand for times to come.

Disclaimer:

This document prepared by our research analysts does not constitute an offer or solicitation for the purchase or sale

of any financial instrument or as an official confirmation of any transaction. The information contained herein is

from publicly available data or other sources believed to be reliable but do not represent that it is accurate or

complete and it should not be relied on as such. Firstcall India Equity Advisors Pvt. Ltd. or any of it’s affiliates shall

not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the

information contained in this report. This document is provide for assistance only and is not intended to be and must

not alone be taken as the basis for an investment decision.

Firstcall India Equity Research: Email – [email protected]

C.V.S.L.Kameswari Pharma

U. Janaki Rao Capital Goods

Ashish.Kushwaha IT, Consumer Durable & Banking

Anil Kumar Diversified

Suhani Adilabadkar Diversified

M. Vinayak Rao Diversified

Firstcall India also provides

Firstcall India Equity Advisors Pvt.Ltd focuses on, IPO’s, QIP’s, F.P.O’s,Takeover

Offers, Offer for Sale and Buy Back Offerings.

Corporate Finance Offerings include Foreign Currency Loan Syndications,

Placement of Equity / Debt with multilateral organizations, Short Term Funds

Management Debt & Equity, Working Capital Limits, Equity & Debt

Syndications and Structured Deals.

Corporate Advisory Offerings include Mergers & Acquisitions(domestic and

cross-border), divestitures, spin-offs, valuation of business, corporate

restructuring-Capital and Debt, Turnkey Corporate Revival – Planning &

Execution, Project Financing, Venture capital, Private Equity and Financial

Joint Ventures

Firstcall India also provides Financial Advisory services with respect to raising

of capital through FCCBs, GDRs, ADRs and listing of the same on International

Stock Exchanges namely AIMs, Luxembourg, Singapore Stock Exchanges and

other international stock exchanges.

For Further Details Contact:

3rd Floor,Sankalp,The Bureau,Dr.R.C.Marg,Chembur,Mumbai 400 071

Tel. : 022-2527 2510/2527 6077/25276089 Telefax : 022-25276089

E-mail: [email protected]

www.firstcallindiaequity.com