file copy memorandum on the current economic position...

TRANSCRIPT

Report No. 1315-AL FILE COPYMemorandum on the Current EconomicPosition and Prospects of Algeria(In Two Volumes)

Vol. 1: Main ReportJanuary 25, 1977

EMENA RegionCountry Programs Department II

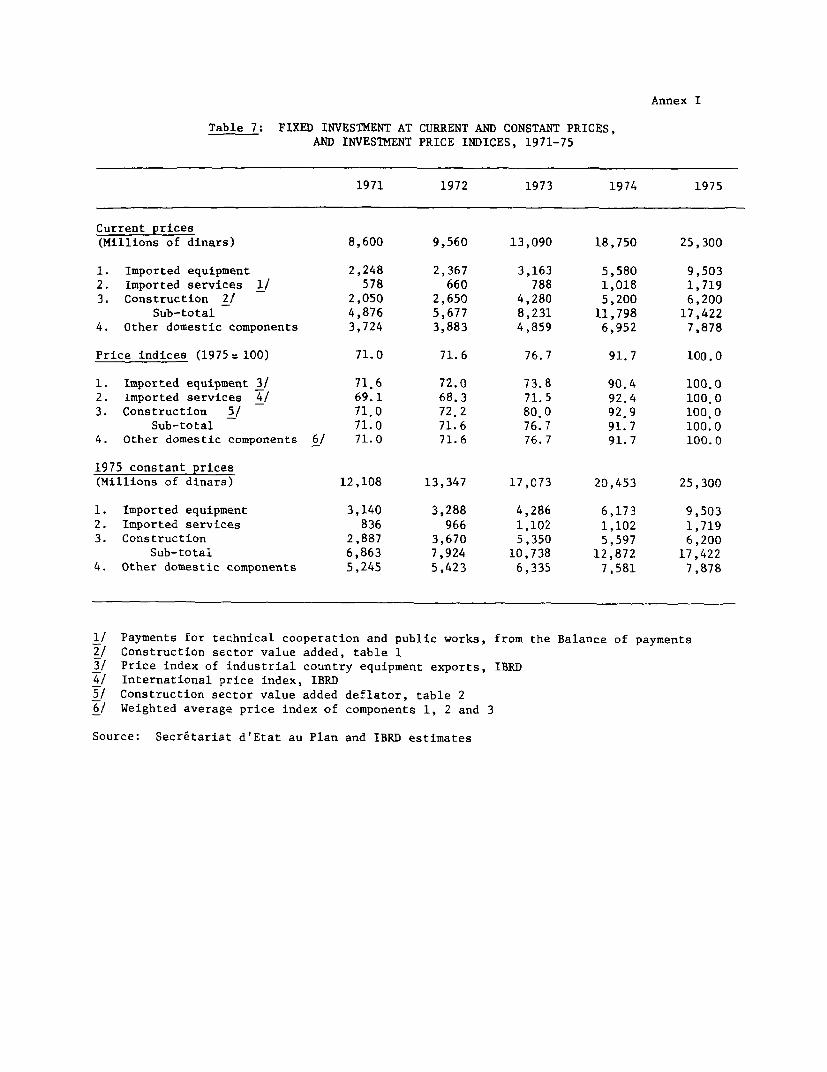

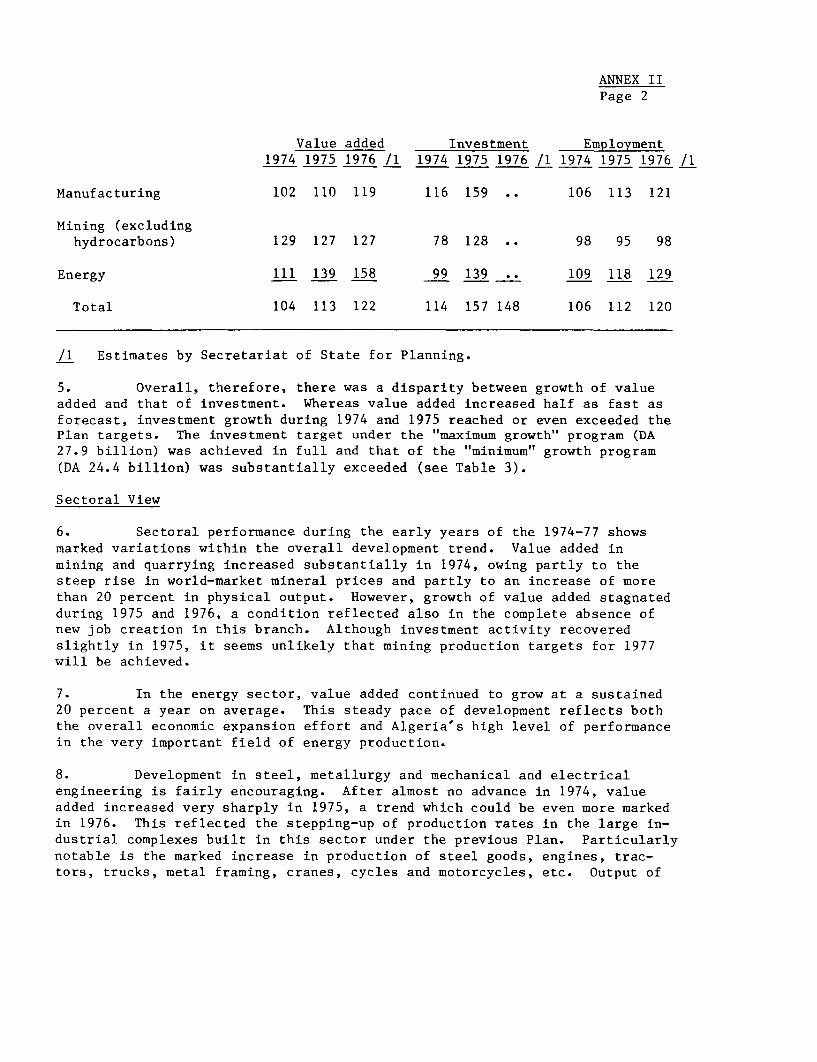

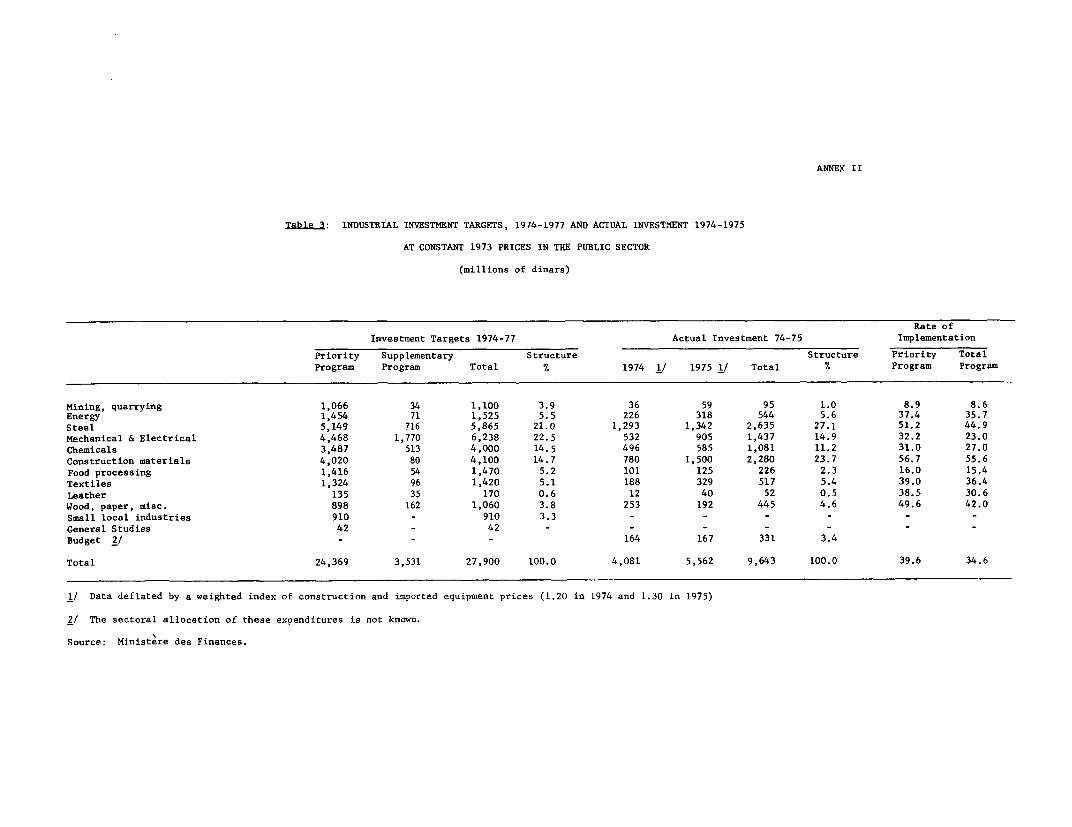

FOR OFFICIAL USE ONLY

Document of the World Bank

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may nototherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

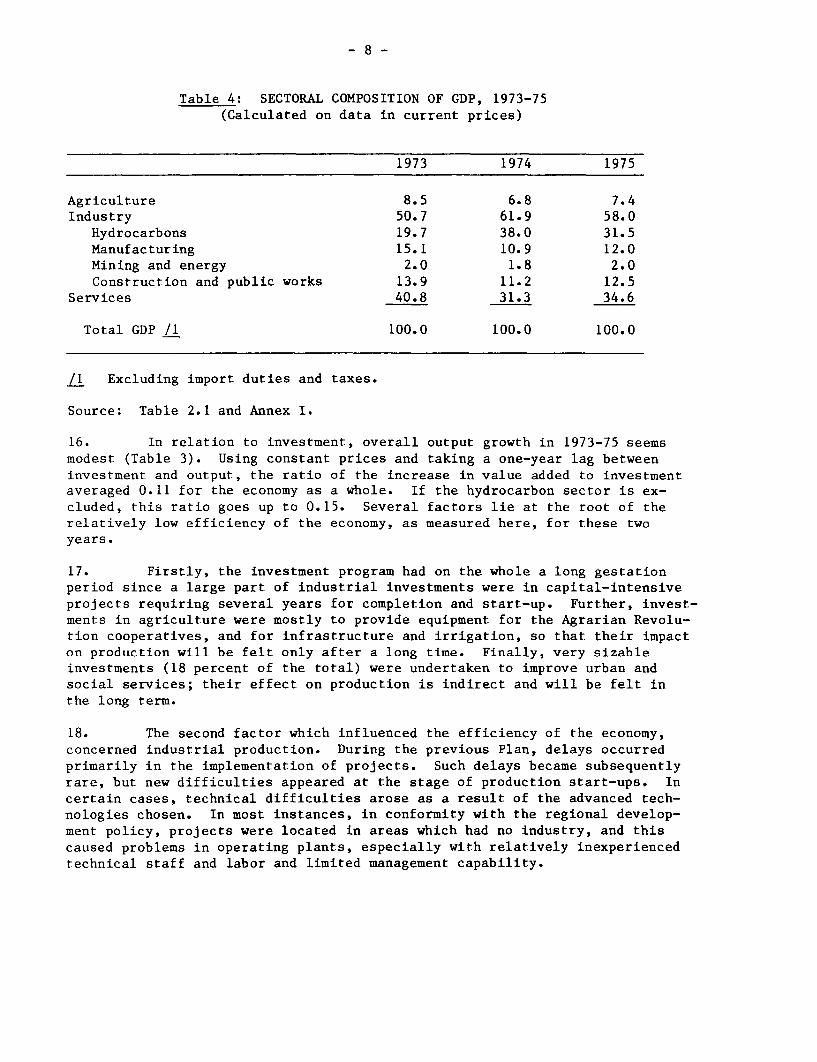

Pub

lic D

iscl

osur

e A

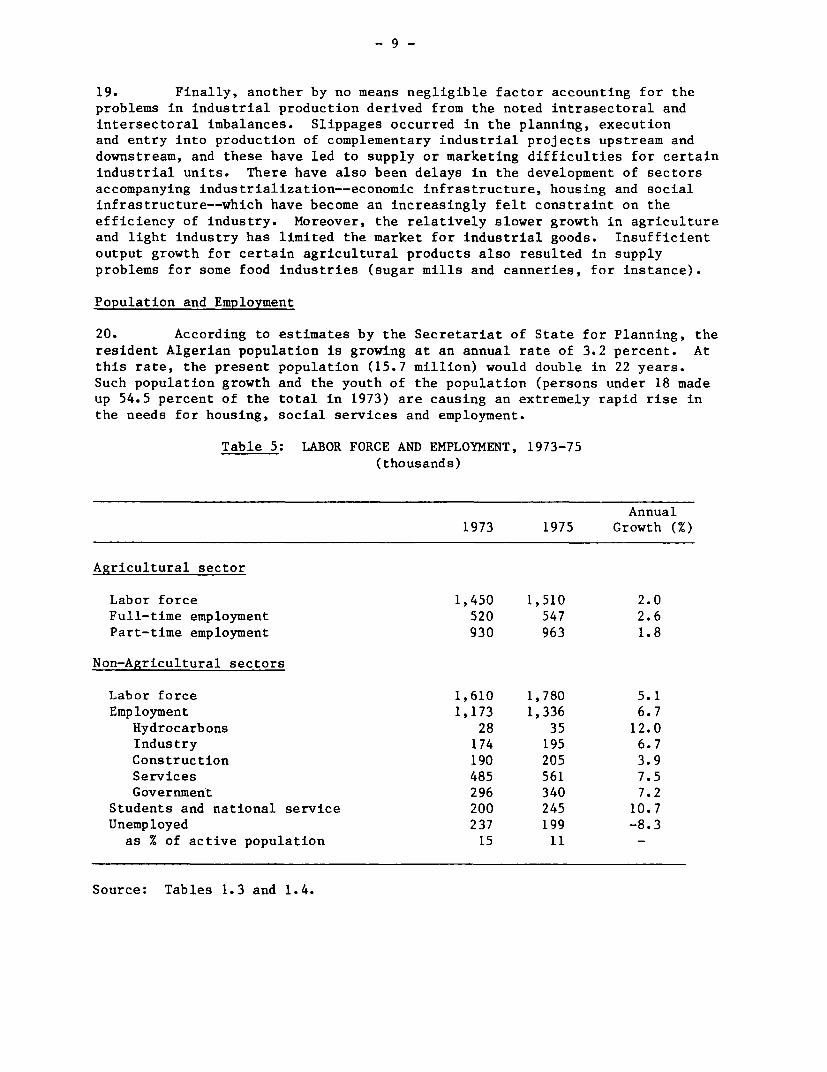

utho

rized

Pub

lic D

iscl

osur

e A

utho

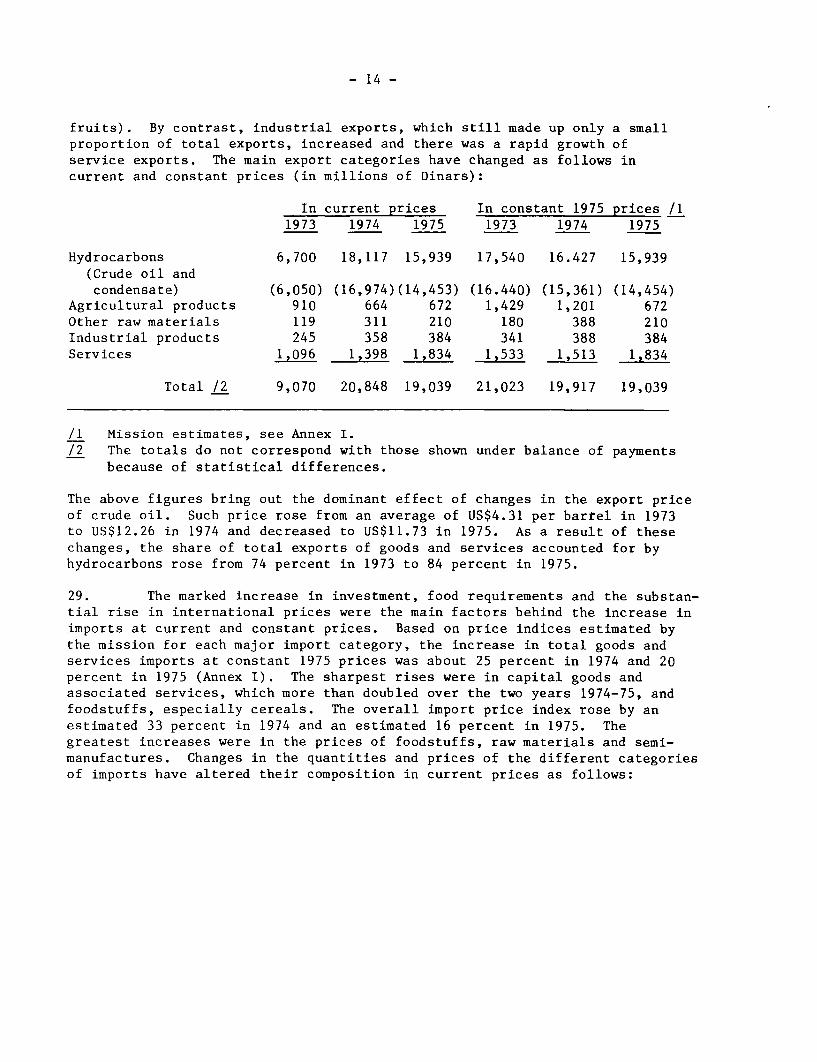

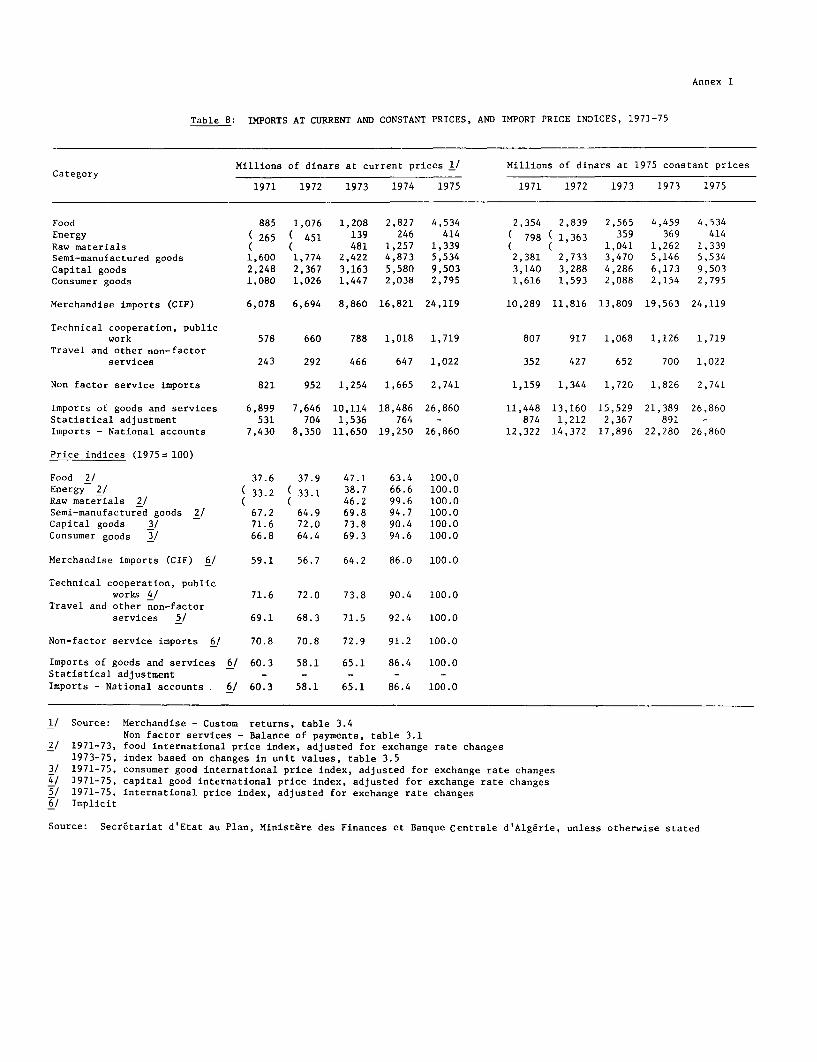

rized

Pub

lic D

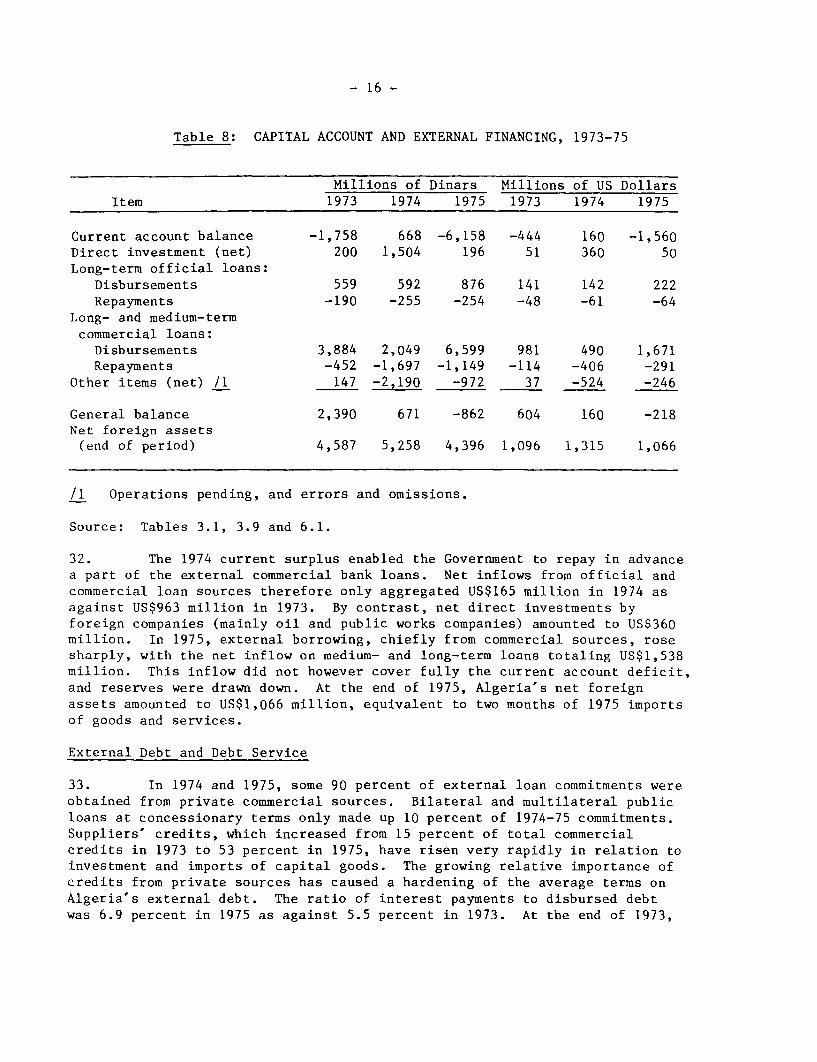

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

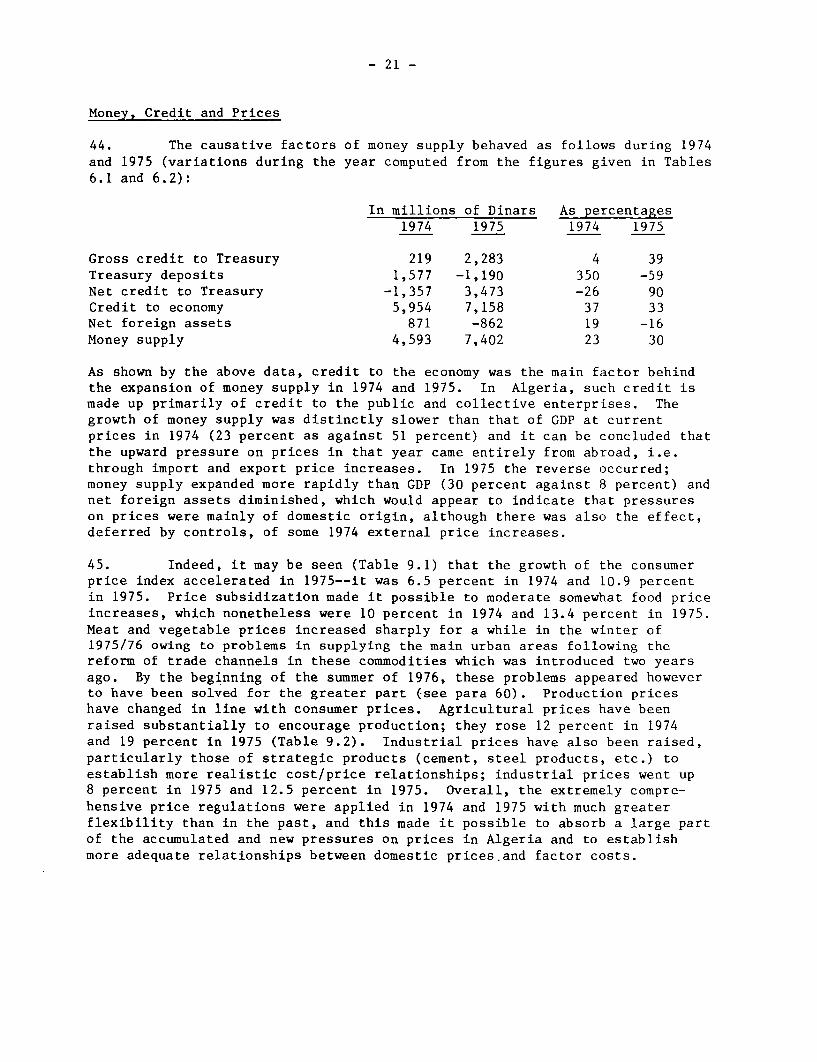

lic D

iscl

osur

e A

utho

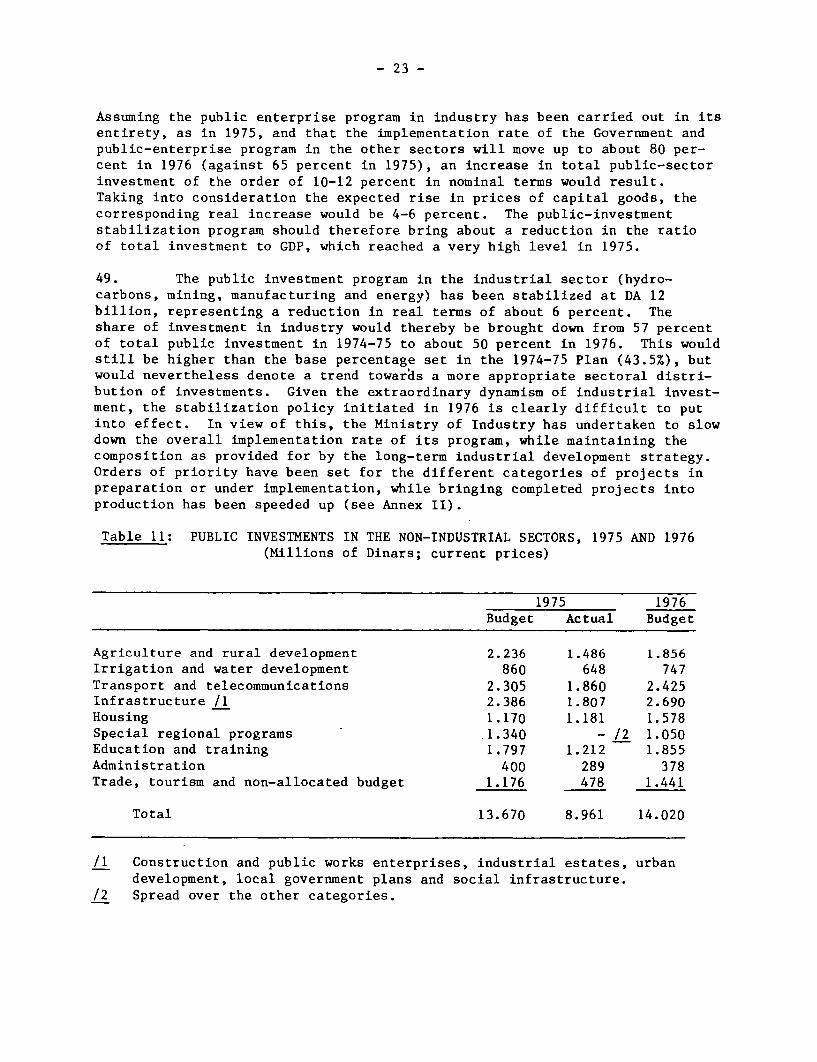

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

(Algerian Dinars per US dollar)

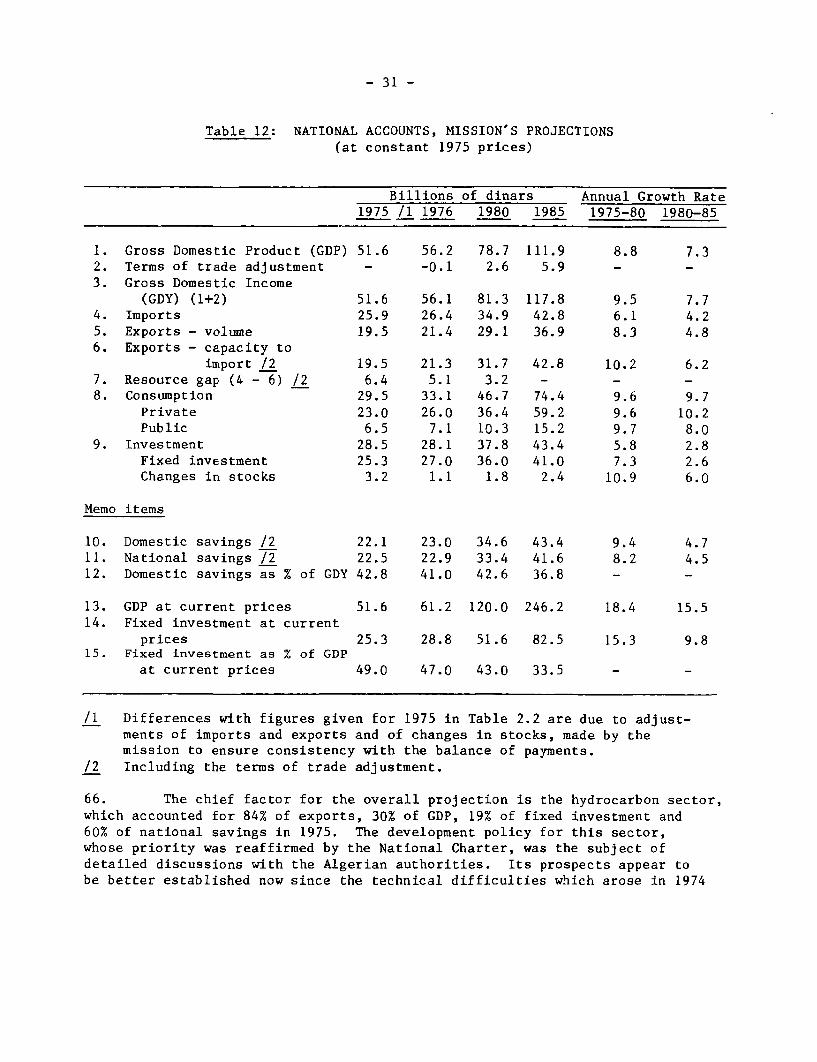

Official TradeExchange conversion

Period Rate 1/ Factor 2/

1970 4.937 4.937

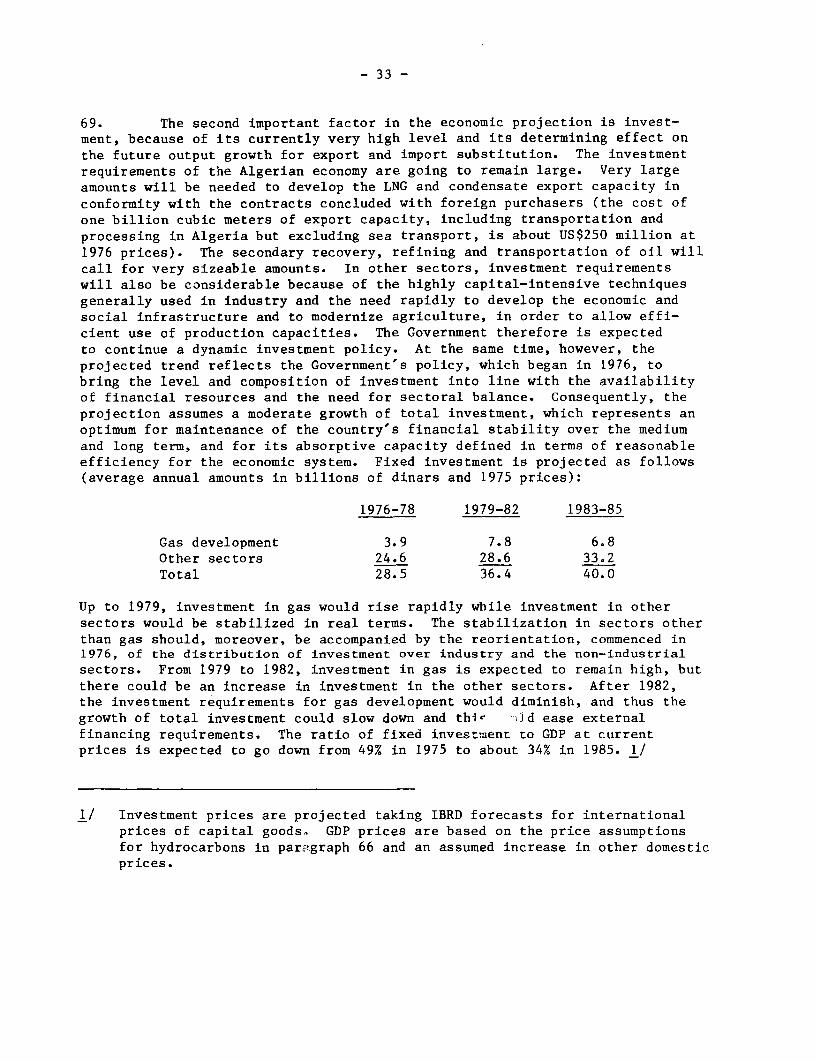

1971 4.644 4.913

1972 4.556 4.484

1973 4.185 3.959

1974 3.997 4.181

1975 4.125 3.949

October. 1976 4.183 4.162

1/ End of period

2/ Average of period

Source: IMF, International Financial Statistics, December 1976.

FOR OFFICIAL USE ONLY

MEMORANDUM ON THE

CURRENT ECONOMIC SITUATION AND PROSPECTS OF ALGERIA

Table of Contents

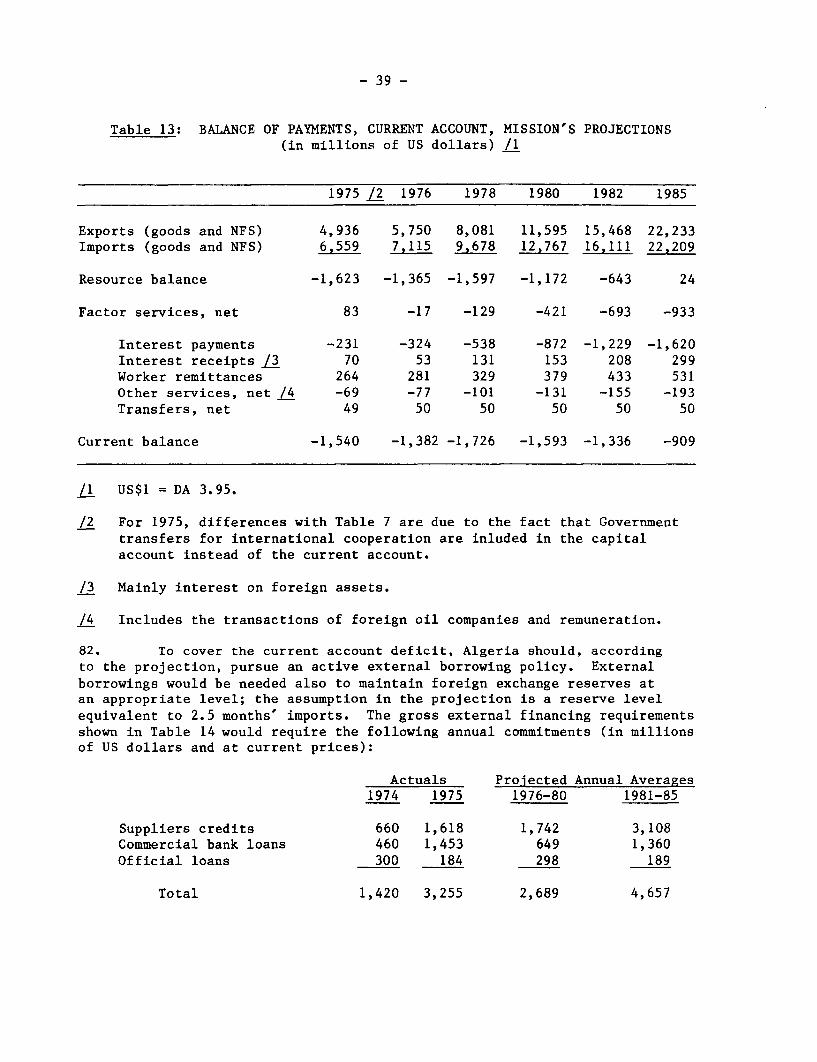

Page No.

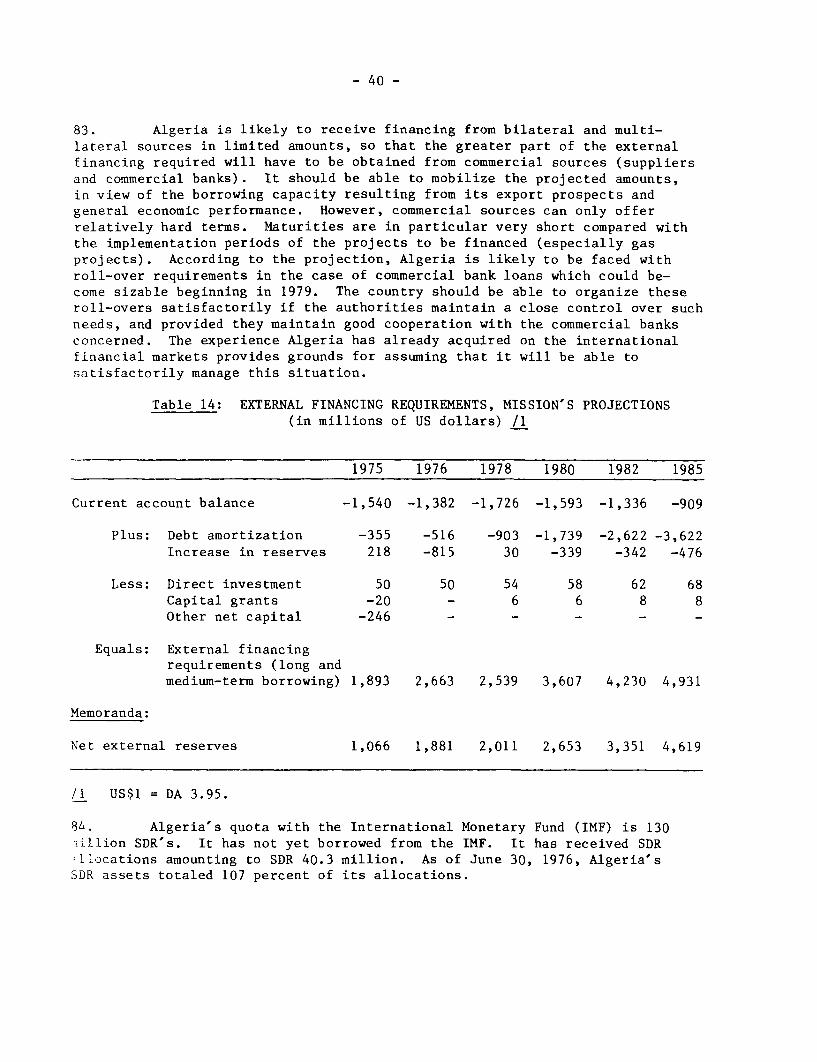

MAP

BASIC DATA

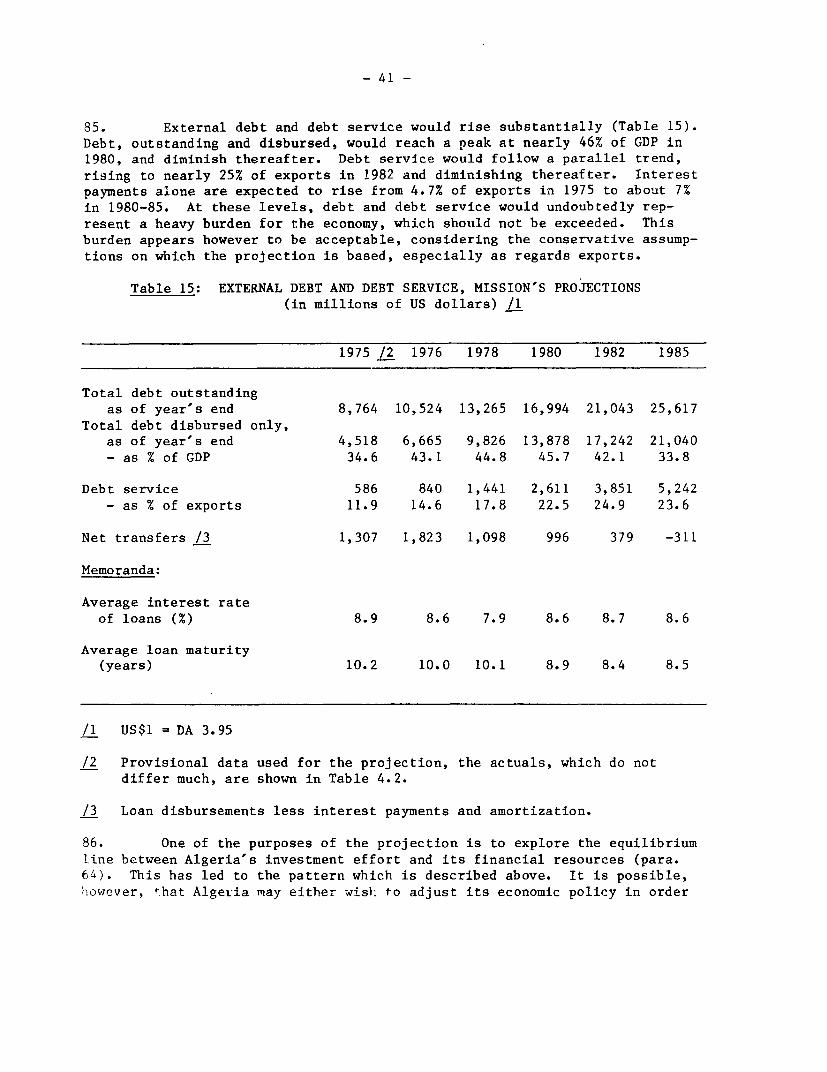

SUMMARY AND CONCLUSIONS

I. INTRODUCTION ............................................. 1

II. ECONOMIC PERFORMANCE IN 1974-75 AND THE SITUATION IN 1976. 2

Investment and Production. . . 2Population and Employment. . . 9Savings and External Deficit .. .11

Balance of Payments . . .12External Debt and Debt Service . . .16Public Finances . . .17Money, Credit and Prices . . .21

The Situation in 1976 . . .22

III. DEVELOPMENT OBJECTIVES AND PROSPECTS. ... .. 27

Development Objectives .. 27Economic Prospects ......... 30Financial Prospects .. 38

ANNEX I Estimate of National Accounts at Constant Prices

ANNEX II Recent Progress and Prospects of Industrialization

STATISTICAL ANNEX

This report is based on the findings of an economic mission which visitedAlgeria in April 1976. The mission was composed of Messrs. Christian Merat(chief), Francois Laporte (general economist), and Marc Ollivier (industrialeconomist).

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disckeed without Wofid Bank authorization.

EBRD 12604R

PORTUGAL Me ite rian so o Seo

f. N. X z 9 t - > i ' TU 51Ad-d

MAIN NATT bNA

ROADS

v f o/~~~~~~MAN SHARA TRACKS7

INTRRNATIONAL ARPORTS~ ~ ~ ~ ~ ~ ~~~~~~~~~L BY MAURRIV T AN INTER STM a

ALGERIA RR i; A R

1Z MA N PORTS \8; ', O rasrv* MAIN NATONAL ROARS [ | ,

-- -MAIN SAHARA TRACKS ' w / _ /\

b | E STANDARD GAUGE RAlLWAYI \. OTT..NARROW GAU)GE RAILWAYS \ / ~ }R\ \

* INTERNATIONAt AIRPORTS N. G F R\ \ + SECONDARY AIRPORTS ~

_- OIL PPELINES i * .

-- GAS PIPELINES t' t> | ] \ ,

- RIVERS AND INTERMITTENT STREAMS -F>. / ,

MoUNTANouS AREAS AA AI) K;--- INTERNATIONAL EOUNDARIES /V|f g>lh .srd

-METIR~~ <1.15 1 ... <,,

Page I of 2 pages

COUNTRY DATA ALGERIA

AREA (1,000 Km2): 2,381.7 POPULATION: 15.7 million DENSITY: 6.6 per Km2

POPULATION CHARACTERISTICS (1975) EDUCATION (1972)Crude Birth Rate (per 1,000) 48.7 Adjusted primary school enrollment ratio 85.0Crude Death Rate (per 1,000) 15.4 Adjusted secondary school enrollment ratio i/ 15.0Gross Reproduction Rate 3.5 Vocational enrollment (% of secondary) 19.0

Adult Literacy rate (%) (1970) 26.0Population growth rate, total (1970-75) 3.2

urban (1970-75) 6.7Urban Popuilation (% of total) 50.4 HOUSING AND CONSUMPTION (1973)

Persons per room (average)Age structure (%) 0 to 14 years 48.0 Occupied dwellings without piped water (%)

15 to 64 years 48.8 Access to electricity (% of all dwellings)65 years and over 3.2 Electricity (Kwh/yr per capita) (1974) 200.0

Radio receivers (per 1,000 pop.) 46.0Passenger cars (per 1,000 pop.) 12.0

HEALTH AND NUTRITION (1972)Population per physician 7,809.0Population per hospital bedPer capita calorie supply as % of

requirements 72.0Per capita protein supply (grams per day) 46.0

GNP PER CAPITA IN 1975 : US$ 780

US dollar millions - 1975 prices andNATIONAL ACCOUNTS exchange rates Annual Growth Rates

19197 73~ 1975 AGDP-1975 1971-73 1974 1975Gross domestic product 9,387 12,039 13,067 100.0 13.2 4.0 4-3Gains from terms of trade -1,734 - 1,572Gross domestic income 7,653 10,467 13,067 100.0 17.0 29.5 -3.6

Imports 3,120 4,532 6,802 52.0 20.5 24.5 20.6Exports (import capacity) 2,091 3,081 4,938 37.8 21.6 91.8 -16.4Resource gap 1,029 1,451 1,864 14.2

Consumption expenditures 5,324 6,460 7,587 58.o 10.2 5.9 10.9Investment (mncl. stocks) 3,115 4,802 7,344 56.2 24.3 31.0 16.8

Domestic savings 2,086 3,351 5,480 41.9 26.8 95.6 -16.4National savings 2,387 3,786 5,569 42.6 25.8 70.3 -13.6

OUTPUT. LABOR FORCE ANDPRODUCTIVITY IN 1975

Value Added Labor Force V.A. per worker(USS Mln.) % Thousand us$

Agriculture i/ 937 7.5 1,510 49.6 620 A9Industry 7,318 58.0 435 14.3 16,822 406.2- Hydrocarbons 3,975 31.5 35 1.2 113,571 2,742.6- Others 3,343 26.5 400 13.1 8,357 201.8Services 4 356 34.5 901 29.6 4,834 116.7Unemployed / . . 199 6.5

Total 12,611 100.0 3,045 100.0 4,141 100.0

GOVERNMENT FINANCECentral Government

(Dinar Mln.) of GOP

1974 1975 19274 1975 1971-73

Current revenue 23,417 25,372 49.0 49.2 33.7- Petroleum (13,402) (13,462) (28.1) (26.1) (11.1)- Other (10,015) (11,910) (20.9) (23.1) (22.7)Current expenditure 8.501 13,231 17.8 25.6 19.9Current surplus 14,916 12,141 3T12 23.5 13Capital expenditure 13,016 18,578 27.2 36.0 22.3- Central government investment (4,130) (5,505) (8.6) (10-7) (10.9)- Capital transfer to public (8,886) (13,073) (18.6) (25.3) (11.4)

Enterprises j/

External borrowing (net) - 159 18 -0.3 - -0.4

1/ 12-18 years of age

! The per capita GNP estimate is that of the World Bank Atlas:/ Data at 1975 prices and exchange rates are Bank estimates| Includes part-time workers5/ Includes only non-agricultural unemployed./ Includes investment loan disbursement allocations for the working capital of enterprise, and enterprises'debt rescheduling.

Page 2 of 2 Pages

COUNTRY DATA ALGERIA

MONEY, CREDIT AND PRICES 1971 1972 1973 1974 1975(Millions Dinar, end of period)

Money and Quasi Money 13,925 18,139 20,362 24,955 32,357

Claims on Government (net) 5,974 5,236 5,198 3,941 7,314

Claims on the Economy 8,068 13,611 15,897 21,851 29,009

(percentage or index numbers)

Money and Quasi Money as % of GDP 62.2 67.9 64.6 52.2 62.7

General Price Index 1/ 100.0 98.0 109.8 159.9 165.6

Retail Price Index 100.0 103.7 110.0 117.2 130.0

Annual percentage change in:

General Price Index .. -2.0 12.0 45.6 3.6

Retail Price Index 9.6 3.7 6.1 6.5 10.9

Claims on Government (net) - -12.4 -0.7 -26.1 90.4

Claims on the Economy 25.0 68.7 16.8 37.5 32.8

BALANCE OF PAYMENTS 1971 1972 1973 1974 1975(US$ Millions)

Exports of Goods, NFS 973 1,361 2,108 4,935 4,936

Imports of Goods, NFS 1,274 1.672 2.713 4,477 6560

Resource Gap (deficit = -) -301 -311 -605 458 -1,624

Interest Payments (net) -16 -30 -63 -70 -161

Workers' Remittances (net) 157 184 176 156 201

Other Factor Payments (net) -40 -3 -2 -383 -

Net Transfers 139 38 50 -1 24

Balance on Current Account -61 -122 -444 160 -1,560

Direct Foreign Investment -46 18 51 360 50

Net MLT Borrowing 153 182 960 165 1,538

Disbursements 225 293 1,122 632 1,893

Amortization -72 -111 -162 -467 -355

Other Capital (net) -42 71 37 -524 -246

Increase in Reserves (+) 4 149 604 160 -128

Net Reserves (end of year) 329 482 1,096 1,315 1,066

MERCHANDISE EXPORTS Average 1971-73 1974 1975

US$ Mln. % US$ Mln. % US$ Mln. %

Crtude Oil 1,021 75.4 3,645 85.6 3,495 83.7

Refined Oil Products 36 2.7 237 5.6 277 6.6

Gas 38 2.8 57 1.3 82 2.0

Wine 101 7.5 113 2.7 56 1.3

Fruits, citrus fruits & vegetables 21 1.6 31 0.7 43 1.0

Iron, ore, phosphate and other

minerals 32 2.3 50 1.2 53 1.3

Metal and Metal Products 17 1.3 33 0.7 54 1.3

Others 87 6.4 92 2.2 115 2.8

Total Merchandise Exports 1,353 100.0 4,258 100.0 4,175 100.0

IBRD Lending, Sept. 30, 1976 (Mln. US$) EXTERNAL DEBT, December 31, 1975 (Mln. US$)

Outstanding and Disbursed 73.1 Public Debt, Incl. Guaranteed 9,003

Undisbursed 307.4 Total Outstanding and disbursed 4,527

Outstanding incl. Undisbursed 380.5 DEBT SERVICE RATIO 1973 1974 1975

In % of Exports of Goods, NFS 14.4 14.5 11.9

In % of Exports of Goods, NFS 13.3 14.0 11.4

and workers remittances

In % of Government Revenues 10.9 12.7 9.1

1/ GDP deflator, Bank estimate. December, 1976~~~~~~~~ ~~~~~~~- nil or negligible

not availablenot applicable

SUMMARY AND CONCLUSIONS

i. In 1974 and 1975, Algeria continued to execute the second four-yearPlan, 1974-77, which aims at a sharp acceleration in the implementation ofthe country's long-term development strategy. Based on the increased receiptsderiving from the new relative prices for oil and gas, the Plan calls for aconsiderable acceleration in investment growth to broaden the productive baseof the economy, a marked shift in investment composition in favor of sectorsother than industry, and a substantial improvement in the employment ofunskilled workers and in the living standards and consumption of the dis-advantaged social groups, especially the agricultural population. Moreover,the Plan provides for the vigorous and systematic implementation of thepolicies that have been introduced since 1971 to decentralize and improveeconomic management at all levels.

ii. Mid-way through the Plan period at the end of 1975, the country hadscored solid successes for investment and employment by comparison with thePlan objectives. Investment doubled from US$3.3 billion in 1973 to US$6.4billion in 1975 at current prices, reflecting the dynamism of the Governmentand public enterprises. Employment creation has also been substantial. Inthe nonagricultural sectors, it exceeded the increase in the labor force,and the unemployment rate dropped 4 points (11 percent in 1975 and 9 percentexpected in 1976, as compared with 15 percent in 1973). In the agriculturalsector, the Agrarian Revolution cooperatives now provide permanent new jobs tosome 100,000 beneficiaries. Although precise data are lacking, it seems thatthe increase in permanent employment, coupled with the tax and budget measurestaken by the Government in 1974 and 1975 (especially the tax relief measures,the higher producer prices for agricultural products, the price subsidisationof basic commodities, and the expenditures on rural public services) havegreatly helped to raise, as planned, the living standards and consumptionlevels of the least privileged population groups.

iii. Of perhaps even greater importance for the country's long-termdevelopment prospects, initial measures to decentralize and improve economicmanagement have been implemented with vigour, as envisaged in the Plan.Although much remains to be done, there is clear evidence of this policy inthe productive sectors and at local government level. The National Charterapproved by referendum in June 1976 gives this policy quasi-constitutionalstatus. With the rapid growth of the number of technicians and middle levelmanagers graduating from educational and training institutions, the improve-ments already made in the institutional framework of the economy seem toindicate that Algeria may gradually gain a satisfactory command of its invest-ments, which should enable it to attain a rate of rapid economic growth.

iv. Some less favorable economic developments should also be noted.For technical and commercial reasons, receipts from oil and gas exports didnot reach the level expected in the Plan. The rate of investment in sectorsother than industry proved insufficient. Consequently, some of the imbalancesthat have affected Algeria's development, persisted. Investment became very

- ii -

high in relation to GDP (49 percent in 1975) and, especially, to the availabil-ity of skilled labor. In conjunction with the shortfall in oil and gas re-ceipts and the expansion of private consumption, pressure on the country'sfinancial resources increased sharply. After a surplus in 1974, the balanceof payments current account showed a deficit of US$1.6 billion in 1975, morethan 12 percent of GDP. Despite increased external borrowing, the country'snet reserves fell by US$250 million in 1975. Government transactions alsoshowed a deficit in 1975. Industrial development continued at a very rapidpace, compared with that of most other sectors, and bottlenecks persisted,especially in infrastructure, housing and urban public services. Finally, out-put growth was rather slow in relation to investment and employment creation.

v. Aware of the consequences of these imbalances, the Governmentdecided to stabilize investment in 1976 and begin redressing its compositionin favor of the lagging sectors. Industrial investment was to be held at thesame level as in 1975, while investment in other sectors would be stepped upmore rapidly. In addition, the Government has undertaken to reduce theoverall budget deficit. These decisions, combined with the marked accelera-tion of output growth and exports since the last quarter of 1975 (particularlyin the oil and gas sector), are enabling Algeria to keep the domestic andexternal financial situation under control. Import requirements have beenslowing down in 1976, and external borrowing needs have been diminishingsomewhat.

vi. After 1976, this report foresees a relatively rapid grQwth of theeconomy (by about 8.5 percent yearly on average during the 1976-80 period),which would be accompanied by relatively large needs for external financing.This forecast is based on a conservative appraisal of the prospects open tothe oil and gas sector and the results that can be expected from the develop-ment policies pursued by Algeria.

vii. The prospects for the oil and gas sector, which accounted for 84 per-cent of exports and 30 percent of GDP in 1975, seem assured in both quantitiesand prices. The sector's export receipts may reach the following amounts (inbillions of US dollars):

Actuals Projections1973 1975 1976 1980 1985

Constant 1975 prices 4.4 4.0 4.4 5.9 7.0

Current prices 2.7 4.0 4.7 9.5 17.6

Price index (1975 - 1.0) 0.6 1.0 1.1 1.6 2.5

The share of liquefied natural gas in total export receipts at current priceswould rise due to projected increases in export quantities and prices for thisproduct, based on the sales contracts recently signed by Algeria.

- iii -

viii. Investment requirements of the Algerian economy are expected toremain large. Considerable amounts will be needed to develop hydrocarbonexports, particularly gas. In other economic sectors, investments would alsoneed to be substantial, partly because of the Algerian planners' choice ofcapital intensive production processes, and especially because of investments(in physical infrastructure, water development, housing and urban publicservices, for example) which must be made to ease the constraints on the useof existing or planned production capacities. In view of these investmentneeds, the Government is expected to pursue a dynamic investment policy. Atthe same time, however, the policy of overall and sectoral balance developedin 1976 would be maintained. Projected investments would rise moderately inthe years ahead, while representing an optimum in relation to expected devel-opments in the country's financial resources and absorptive capacity (in termsof acceptable economic efficiency). They would grow yearly by 7% in 1976-80,with most of the increase allocated for development of gas exports. From 1980to 1985, investment requirements for gas development would diminish so thattotal investment would grow only slowly (about 3 percent p.a.), while therewould be room for satisfactory increases in other sectors. Fixed investmentwould gradually decline from 49 percent of GDP in 1975 to 34 percent in1985.

ix. The policies aimed at improving economic efficiency refer inparticular to the following areas:

- training of technicians and middle level management staff,where very substantial efforts are being made but willprobably leave unsatisfied needs throughout the periodunder review;

- preparation, implementation and initial operation of projects,where recent efforts indicate that a generally improvingsituation should emerge in the years to come;

- intersectoral and intrasectoral coordination of projects,where balancing investment needs may be considerable, buthave not yet been systematically identified;

- price policy and its impact on the financial situation ofenterprises;

- detailed preparation of the procedures for decentralization,which involves shifting the focus of central supervisionfrom day-to-day management to programming and follow-up ofthe operations of decentralized-enterprises and institutions;

- the role to be played by financial institutions in the de-centralized management structures.

On the basis of a qualitative appraisal of these factors, a relatively highincremental capital-output ratio (5.3 in 1976-80 and 5.7 in 1981-85) isprojected.

- iv -

x. Financially, the projection implies a required sustained effort tomobilize domestic and external savings. Budgetary savings, which do notoriginate in the hydrocarbon sector, would be increased, and the mechanismsfor mobilizing individuals' financial savings would be strengthened. Externalloans would be sought to cover the projected external deficit and keep reservesat an adequate level. External borrowings would be considerable in absoluteterms--of the order of US$2.7 billion per year on average in 1976-80 and US$4.6billion in 1981-85--but reasonable in relative terms, in view of the borrowingcapacity which Algeria derives from its prospective oil and gas receipts andits well-controlled economic development, overall. Most borrowings wouldprobably come from private commercial sources offering rather short repaymentperiods in relation to the gestation periods of the investments financed(especially in gas). Roll-over of these borrowings would become substantialfrom 1979 onwards, and this will entail an intensification of relationsbetween the commercial sources concerned and Algeria.

xi. Algeria's external debt and debt service would increase. Debtoutstanding and disbursed would rise from an estimated 35 percent of GDPin 1975 to about 46 percent in 1980, but decline thereafter. Debt service,which would rise from an estimated 12 percent of exports in 1975 to nearly 25percent in 1982, and like the outstanding debt, would tend to decline there-after. As projected, the debt burden would therefore be important during thereview period, but this should not be cause for undue concern, in view of theconservative assessment of the country's prospects adopted here, especiallythe hydrocarbon projections. It is possible, however, that Algeria may eitherwish to adjust its economic policy in order to reduce its external borrowingrequirements, or find some financing on more favorable terms than thoseassumed in this report.

I. INTRODUCTION

1. The framework for the recent development and prospects of theAlgerian economy is set by the country's long-term development objectives andstrategy (1967-80) and by the second four-year Plan (1974-77). A descriptionand a detailed assessment of the long-term strategy and of the 1974-77 Plan aregiven in the last IBRD economic report (No. 900-AL, dated October 20, 1975),which also analyzes the country's economic performance during the 1967-73period and attempts to quantify its economic and financial prospects up to theearly 1980's. The National Charter, approved by referendum of June 27, 1976,provides further details as to the institutional context in which the country'seconomy will henceforth develop. The most important aspects of the Charter,from an economic and financial point of view, are described and taken intoconsideration in the analysis of future prospects in Section III.

2. The decision taken by the Government at the beginning of 1974 tospeed up implementation of the long-term development strategy to the maximumis reflected in the proposed policies and investments of the 1974-77 Plan,introduced in 1974. This decision was based on the results of the 1967-73planning period. It also took into account the improved financial prospectsresulting from the new oil and gas prices. In brief, the objectives of the1974-77 Plan are as follows:

(a) To increase sharply investments (at least 2.3 times the1970-73 totals) with a view to speeding up constructionof the country's productive base and economic infrastruc-tures, and expansion of the urban and social services;

(b) To shift the balance of resources allocated to investmentin favor of sectors other than industry, and of regionsother than the coastal plains and Northern valleys, and

(c) To improve substantially the employment of unskilled labor,individual consumption levels and the distribution of growthbenefits.

The Plan also calls for vigorous implementation of the measures which theGovernment has introduced since 1971 with the aim of both decentralizing andimproving the management of the economy at all levels.

3. The rest of the report consists of two sections. Section II analyzeseconomic performance during the first two years of the 1974-77 Plan and thesituation in 1976. It points out the successes which the speeding up of thedevelopment strategy has made possible in investment and employment. It alsodraws attention to imbalances which became apparent in 1975 and which the Gov-ernment tried to correct in 1976. These imbalances mainly derived from theexcessive acceleration of investment, particularly in industry, as comparedwith the development of the country's financial and human resources. SectionIII examines the overall prospects of the economy in the years immediatelyahead, on the basis of the data available at the time the report was finalized(December 1976). This review confirms the need for Algeria to pursue the policy,

- 2 -

implemented in 1976, of adjusting further the total amount and the sectoralbreakdown of investment to resources. This policy should facilitate themanagement improvements expected from economic decentralization. It shouldalso enable the country to ensure satisfactorily the servicing of externalborrowings which will still be required to develop its productive base overthe years ahead in conformity with its objectives.

II. ECONOMIC PERFORMANCE IN 1974-75 AND THE SITUATION IN 1976

Investment and Production

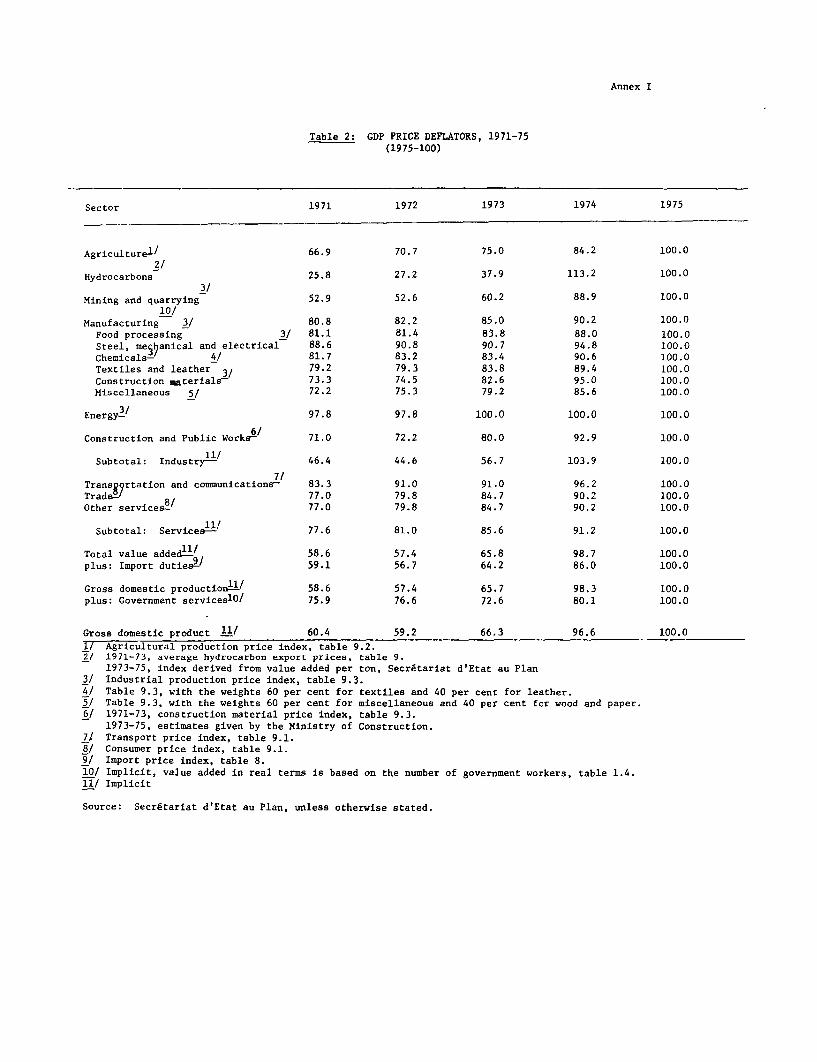

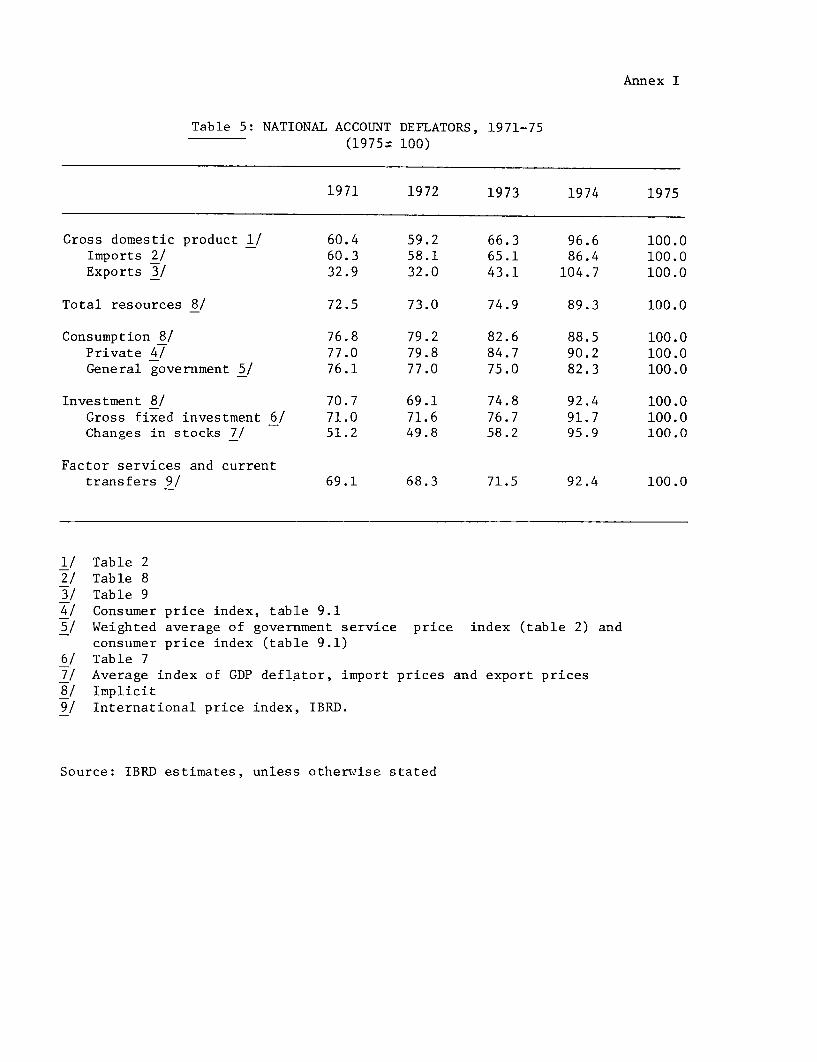

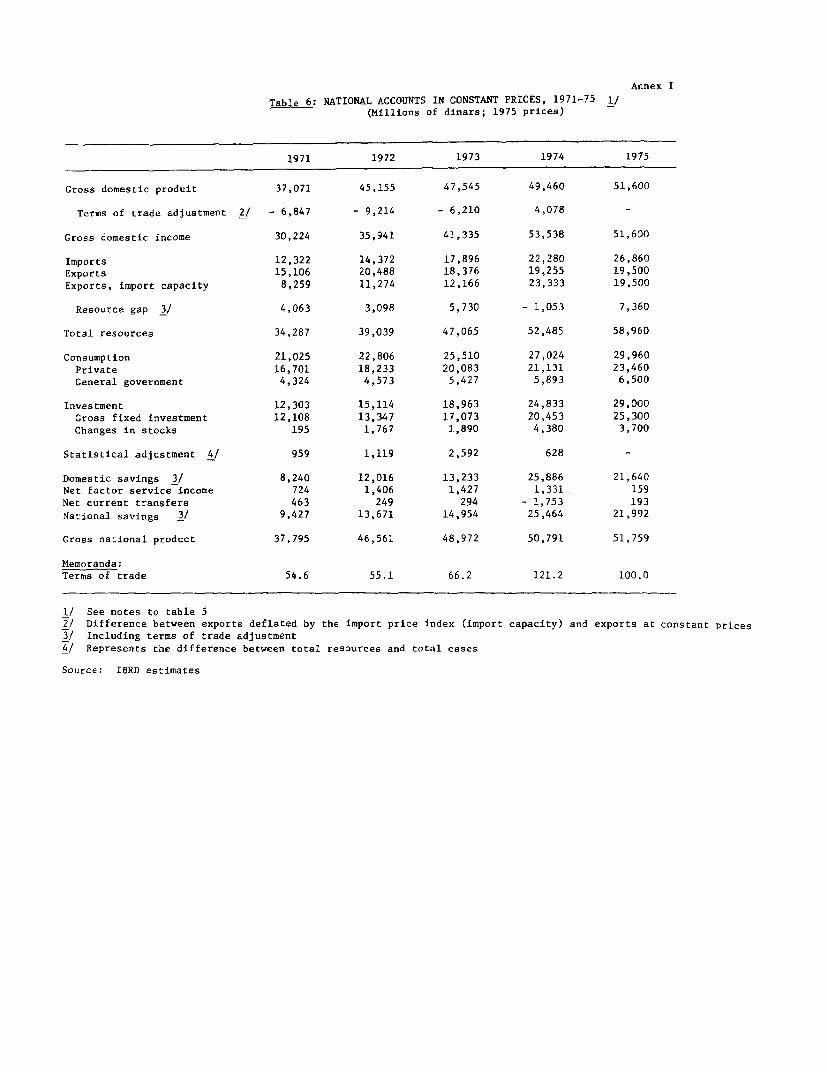

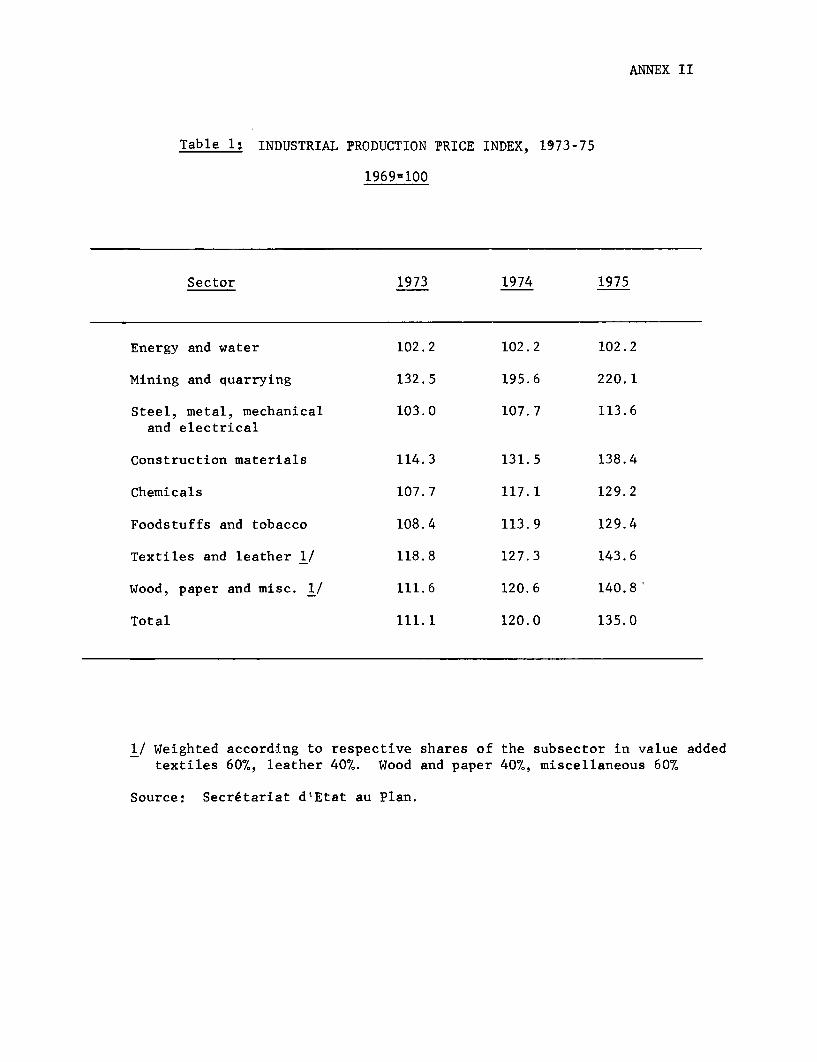

4. Since the end of 1973, two factors have dominated Algeria's economicperformance which were the major changes in hydrocarbon export prices and themarked increase in investment. These two factors acted in the same directionin 1974, but in conflicting directions in 1975, thus bringing about spectacularvariations in the main economic magnitudes (Table 1). In 1974, GDP at currentprices increased by 52 percent while domestic demand rose by 33 percent andthe economy produced a substantial resource surplus. In 1975, domestic demandincreased by a further 25 percent, mainly because of investment growth, butGDP growth was only 8 percent in current terms; this led to a considerableresource gap (13.4 percent of GDP) which was covered by external borrowing.As a result primarily of changed oil and gas prices, the terms of trade indexalmost doubled in 1974, but declined by about 20 percent in 1975.- The effectsof changes in the terms of trade on the real flow of resources, the importcapacity of exports 1/, and savings are analyzed in Annex I, which givesestimates of the national accounts at constant prices.

1/ The import capacity of exports is measured by dividing exports atcurrent prices by the import price index; an equivalent expressionwould be the international purchasing power of exports.

- 3 -

Table 1: CHANGES IN, AND STRUCTURE OF, RESOURCES AND USES

(calculated on data in dinars and in current prices)

Annual Growth (%) Percent of GDpItem 1973 1974 1975 1973 1974 1975

Gross Domestic product 18.1 51.5 8.0 100.0 100.0 100.0

Imports 39.5 65.2 33.0 36.9 40.3 49.6Exports 20.9 154.5 -7.2 25.1 42.2 36.2

Resource gap - - - 11.8 -1.9 13.4

Fixed investment 36.9 43.2 34.9 41.5 39.2 49.0

Changes in stocks 25.0 281.8 -12.0 3.5 8.8 7.2Private consumption 16.9 12.1 20.7 53.9 39.9 44.6Government consumption 15.6 19.2 34.0 12.9 10.2 12.6

Total uses 23.7 32.9 24.8 111.8 98.1 113.4

Memoranda

Import prices /1 12.0 32.7 15.7Export prices /1 34.7 142.9 -4.7Terms of trade /1 20.2 83.1 -21.2

/1 Indices calculated by the mission on the basis of Customs data and inter-

national prices.

Source: Table 2.2 and Tables 8 and 9, Annex I.

5. As called for by the 1974-77 Plan, fixed investment rose by 43percent in current terms in 1974 and by 35 percent in 1975. Deducting invest-ment cost increases, real investment growth averaged about 20 percent per year(Annex I, Table 7). Fixed investment therefore reached the extremely highlevel of 49 percent of GDP in 1975. Since there was also a considerable build-up of stocks, mainly of capital goods, intermediate goods and foodstuffs,total investment absorbed the same proportion of' resources as did consump-tion. Overall, investment increased at the rate set in the Plan for 1974-77,since midway through that period it had reached 32 percent of the maximumtarget and 42 percent of the minimum target (Table 2.5).

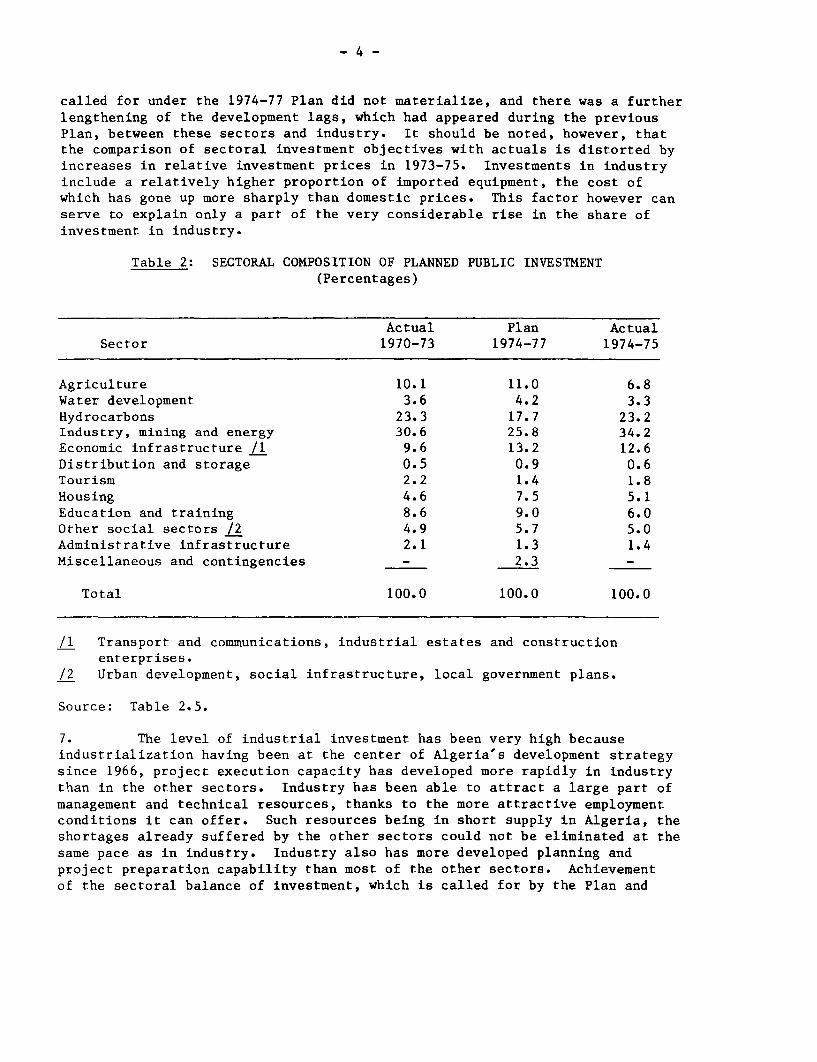

6. The sectoral distribution of investments was not however entirely inline with the Plan. In 1974 and 1975, the industrial sector received a shareof planned investment which was substantially larger than that envisaged inthe Plan and well above that of the preceding Plan (Table 2). On the otherhand, the proportion of investment in other sectors, particularly agriculture,economic infrastructure, housing, and education and training, was below thatplanned. The increased emphasis on non-industrial sectors and infrastructure

- 4 -

called for under the 1974-77 Plan did not materialize, and there was a furtherlengthening of the development lags, which had appeared during the previousPlan, between these sectors and industry. It should be noted, however, thatthe comparison of sectoral investment objectives with actuals is distorted byincreases in relative investment prices in 1973-75. Investments in industryinclude a relatively higher proportion of imported equipment, the cost ofwhich has gone up more sharply than domestic prices. This factor however canserve to explain only a part of the very considerable rise in the share ofinvestment in industry.

Table 2: SECTORAL COMPOSITION OF PLANNED PUBLIC INVESTMENT(Percentages)

Actual Plan ActualSector 1970-73 1974-77 1974-75

Agriculture 10.1 11.0 6.8Water development 3.6 4.2 3.3Hydrocarbons 23.3 17.7 23.2Industry, mining and energy 30.6 25.8 34.2Economic infrastructure /1 9.6 13.2 12.6Distribution and storage 0.5 0.9 0.6Tourism 2.2 1.4 1.8Housing 4.6 7.5 5.1Education and training 8.6 9.0 6.0Other social sectors /2 4.9 5.7 5.0Administrative infrastructure 2.1 1.3 1.4Miscellaneous and contingencies - 2.3 -

Total 100.0 100.0 100.0

/1 Transport and communications, industrial estates and constructionenterprises.

/2 Urban development, social infrastructure, local government plans.

Source: Table 2.5.

7. The level of industrial investment has been very high becauseindustrialization having been at the center of Algeria's development strategysince 1966, project execution capacity has developed more rapidly in industrythan in the other sectors. Industry has been able to attract a large part ofmanagement and technical resources, thanks to the more attractive employmentconditions it can offer. Such resources being in short supply in Algeria, theshortages already suffered by the other sectors could not be eliminated at thesame pace as in industry. Industry also has more developed planning andproject preparation capability than most of the other sectors. Achievementof the sectoral balance of investment, which is called for by the Plan and

- 5 -

essential to ensure the efficiency of industrial investment, will therefore

depend not simply on reallocating financial resources. It will also depend

on strengthening the absorptive capacity of non-industrial sectors, includingplanning, implementation and management.

8. Within the industrial sector, the growth of investment variedgreatly from branch to branch. In steel and construction materials, which

received 51 percent of all investment in industry, excluding hydrocarbons, it

was exceptional moving ahead of schedule. Investment growth has also beenstrong in hydrocarbons, energy and in heavy industry in general. In light

and small industries, however, it remained below planned levels. As regardslocal industries of small and medium sizes, the program instituted by thewilawate (provinces) is still at the design or study stage in most cases.

Its implementation should however gain momentum in 1976 and 1977.

9. In the non-industrial sectors, investment has generally remained

below Plan targets, although there are differences among sectors. In relative

terms, targets were nearly reached in economic infrastructure, which includes

transport and communications, industrial estates and construction enterprises.Investment in the latter was particularly significant at the national andregional levels, but the sector's capacity remained insufficient in relation

to demand. The delays in implementing the Plan in the social sectors are a

cause for concern, especially as regards urban services. In these sectors,

investment expenditures halfway through the Plan period represented only 30

percent of the minimum objectives in current terms, and an even lower percent-

age in real terms. The greatest delays were experienced in agriculture, where

investments after two years stand at only 25 percent of the target for the

four years, in current terms. Key agricultural investments have been for the

establishment of the Agrarian Revolution cooperatives and for agriculturaland rural infrastructure. In view of the rapid progress in the implementationof the Agrarian Revolution, the Plan might have over-estimated the sector's

initial absorptive capacity since its investment was very low up to 1974.Specific data are not available for private investment. It appears to have

increased in 1974 and 1975, especially in construction enterprises, certainbranches of industry such as textiles and leather, and especially in housing.

10. GDP at current prices grew by an average of 27 percent per year

in the first two years of the Plan, but if hydrocarbons are excluded valueadded by the other sectors grew annually by 17 percent. This marked differ-

ence should be seen in the light of marked changes in relative prices over

the period. Reflecting the changes in average export prices, hydrocarbonstripled their value added in 1974 and registered a 10 percent decline in 1975.

As regards the other sectors, the various price indices prepared by the

Secretariat of State for Planning show an average annual increase in produc-

tion prices of 11 percent since 1973 (Annex 1). Real GDP growth, excluding

hydrocarbons, was about 6.7 percent p.a. in 1974-75--a rate higher than the

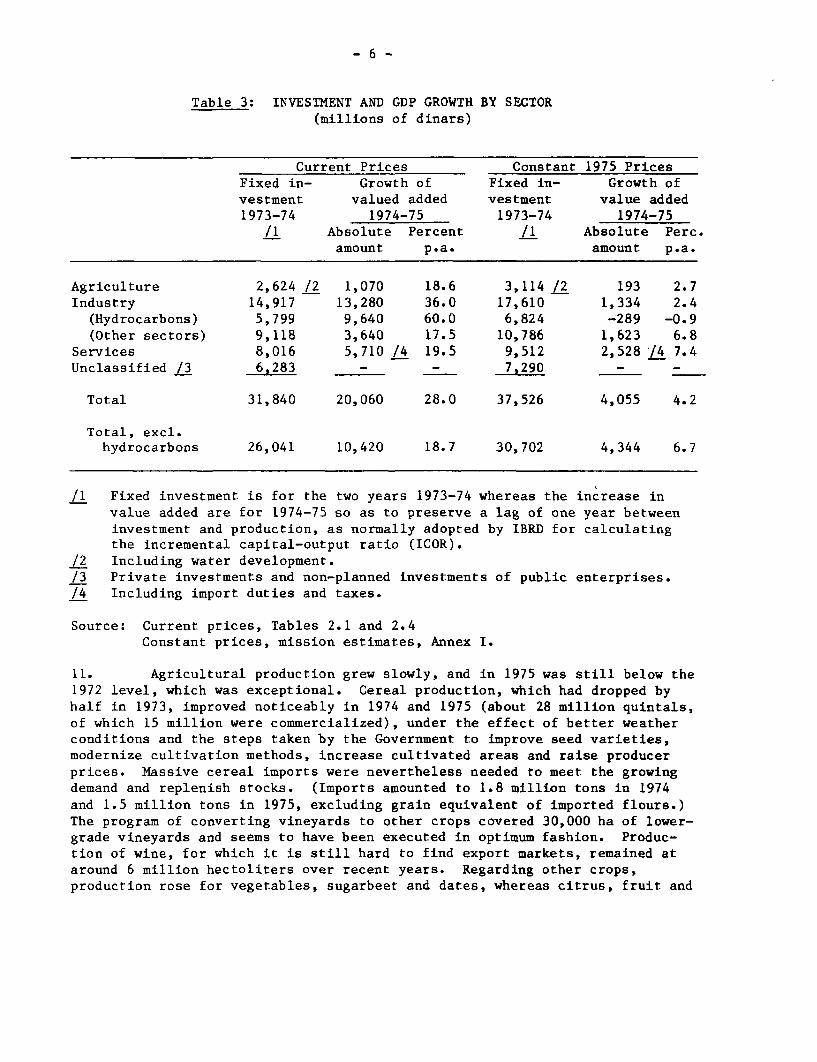

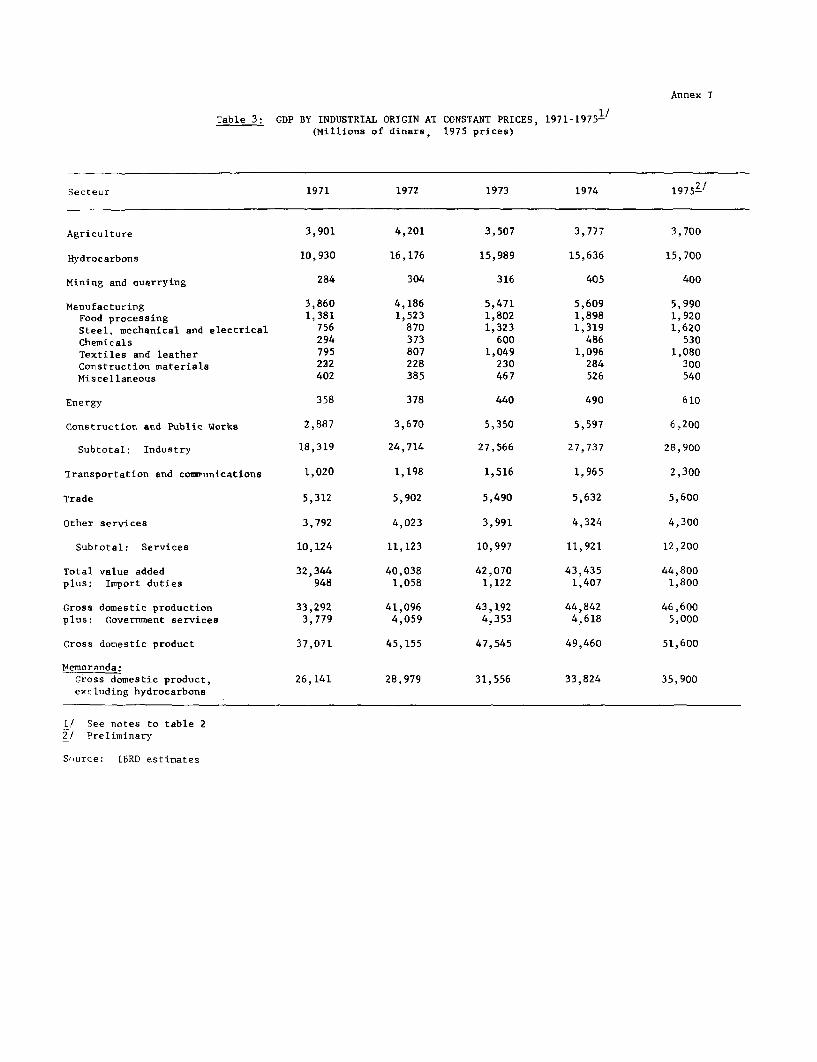

5.3 percent achieved in the 1970-73 period. Table 3 compares investment and

GDP growth in the main economic sectors..

-6-

Table 3: INVESTMENT AND GDP GROWTH BY SECTOR(millions of dinars)

Current Prices Constant 1975 PricesFixed in- Growth of Fixed in- Growth ofvestment valued added vestment value added1973-74 1974-75 1973-74 1974-75

/1 Absolute Percent /1 Absolute Perc.amount p.a. amount p.a.

Agriculture 2,624 /2 1,070 18.6 3,114 /2 193 2.7Industry 14,917 13,280 36.0 17,610 1,334 2.4

(Hydrocarbons) 5,799 9,640 60.0 6,824 -289 -0.9(Other sectors) 9,118 3,640 17.5 10,786 1,623 6.8

Services 8,016 5,710 /4 19.5 9,512 2,528 -4 7.4Unclassified /3 6,283 - - 7,290 - -

Total 31,840 20,060 28.0 37,526 4,055 4.2

Total, excl.hydrocarbons 26,041 10,420 18.7 30,702 4,344 6.7

/1 Fixed investment is for the two years 1973-74 whereas the increase invalue added are for 1974-75 so as to preserve a lag of one year betweeninvestment and production, as normally adopted by IBRD for calculatingthe incremental capital-output ratio (ICOR).

/2 Including water development./3 Private investments and non-planned investments of public enterprises.14 Including import duties and taxes.

Source: Current prices, Tables 2.1 and 2.4Constant prices, mission estimates, Annex I.

11. Agricultural production grew slowly, and in 1975 was still below the1972 level, which was exceptional. Cereal production, which had dropped byhalf in 1973, improved noticeably in 1974 and 1975 (about 28 million quintals,of which 15 million were commercialized), under the effect of better weatherconditions and the steps taken by the Government to improve seed varieties,modernize cultivation methods, increase cultivated areas and raise producerprices. Massive cereal imports were nevertheless needed to meet the growingdemand and replenish stocks. (Imports amounted to 1.8 million tons in 1974and 1.5 million tons in 1975, excluding grain equivalent of imported flours.)The program of converting vineyards to other crops covered 30,000 ha of lower-grade vineyards and seems to have been executed in optimum fashion. Produc-tion of wine, for which it is still hard to find export markets, remained ataround 6 million hectoliters over recent years. Regarding other crops,production rose for vegetables, sugarbeet and dates, whereas citrus, fruit and

-7 -

tree crops (mainly olive oil) tended to stagnate owing to aging of thevarieties. Livestock production has increased but is still below domesticdemand, with the result that in spite of growing imports there have beenstrong upward pressures on meat prices. The implementation of the AgrarianRevolution and agricultural policies are examined in Section III.

12. In the hydrocarbon sector, price increases were accompanied by areduction in crude oil production since 1973 and a drop in value added in realterms. For technical and commercial reasons, production of crude oil andcondensate went down from 50.8 million tons in 1973 to 47.1 million tons in1974 and 45.4 million tons in 1975. Natural gas production has howeverrisen rapidly, reaching 7.4 billion m3 in 1975 compared to 5.6 billion m3in 1973. Half of the gas output has gone to the two liquefaction plants forexport. Data on the hydrocarbon sector are given in Tables 10.1 to 10.7.

13. Developments in industry apart from hydrocarbons are analyzed inAnnex II. The real increase in manufacturing value added is estimated at anaverage of 5 percent p.a. in the first two years of the Plan, but with markedvariations within the sector. Value added rose sharply in heavy industriesproducing capital and intermediate goods, steel, mechanical and electricalengineering, and construction materials industries, as several large plantscame into operation. Value added showed by contrast little increase in lightindustry, textiles and leather, agricultural and food industries and themiscellaneous industries category. The energy sector's value added continuedto grow at a sustained rate of 20 percent p.a. .on average, in response tooverall economic development and thanks to the good operating capability ithas acquired. The real increase in value added in the construction sectorwas also high, in response to demand for industrial investment.

14. For the services sector, real value added increased by over 7 per-cent p.a. on average. Growth was particularly rapid in transportation andpublic services, the latter specifically reflecting the effort made todevelop education and training.

15. The composition of GDP at current prices was substantially changedbetween 1973 and 1975 (Table 4). The share of the hydrocarbon sector rosefrom one-fifth in 1973 to nearly one-third in 1975 solely as a result ofprice changes. Of the other sectors, manufacturing industry and servicessaw their shares of GDP decline mostly because of smaller price increases.It should be noted however, that the full impact of increases in oil and gasprices and other external prices on the economy has not yet been fully feltand that the composition of GDP will probably undergo further changes on thisaccount in 1976 and subsequent years.

- 8 -

Table 4: SECTORAL COMPOSITION OF GDP, 1973-75(Calculated on data in current prices)

1973 1974 1975

Agriculture 8.5 6.8 7.4Industry 50.7 61.9 58.0

Hydrocarbons 19.7 38.0 31.5Manufacturing 15.1 10.9 12.0Mining and energy 2.0 1.8 2.0Construction and public works 13.9 11.2 12.5

Services 40.8 31.3 34.6

Total GDP /1 100.0 100.0 100.0

/1 Excluding import duties and taxes.

Source: Table 2.1 and Annex I.

16. In relation to investment, overall output growth in 1973-75 seemsmodest (Table 3). Using constant prices and taking a one-year lag betweeninvestment and output, the ratio of the increase in value added to investmentaveraged 0.11 for the economy as a whole. If the hydrocarbon sector is ex-cluded, this ratio goes up to 0.15. Several factors lie at the root of therelatively low efficiency of the economy, as measured here, for these twoyears.

17. Firstly, the investment program had on the whole a long gestationperiod since a large part of industrial investments were in capital-intensiveprojects requiring several years for completion and start-up. Further, invest-ments in agriculture were mostly to provide equipment for the Agrarian Revolu-tion cooperatives, and for infrastructure and irrigation, so that their impacton production will be felt only after a long time. Finally, very sizableinvestments (18 percent of the total) were undertaken to improve urban andsocial services; their effect on production is indirect and will be felt inthe long term.

18. The second factor which influenced the efficiency of the economy,concerned industrial production. During the previous Plan, delays occurredprimarily in the implementation of projects. Such delays became subsequentlyrare, but new difficulties appeared at the stage of production start-ups. Incertain cases, technical difficulties arose as a result of the advanced tech-nologies chosen. In most instances, in conformity with the regional develop-ment policy, projects were located in areas which had no industry, and thiscaused problems in operating plants, especially with relatively inexperiencedtechnical staff and labor and limited management capability.

- 9 -

19. Finally, another by no means negligible factor accounting for the

problems in industrial production derived from the noted intrasectoral and

intersectoral imbalances. Slippages occurred in the planning, executionand entry into production of complementary industrial projects upstream and

downstream, and these have led to supply or marketing difficulties for certain

industrial units. There have also been delays in the development of sectors

accompanying industrialization--economic infrastructure, housing and social

infrastructure--which have become an increasingly felt constraint on the

efficiency of industry. Moreover, the relatively slower growth in agriculture

and light industry has limited the market for industrial goods. Insufficient

output growth for certain agricultural products also resulted in supply

problems for some food industries (sugar mills and canneries, for instance).

Population and Employment

20. According to estimates by the Secretariat of State for Planning, the

resident Algerian population is growing at an annual rate of 3.2 percent. At

this rate, the present population (15.7 million) would double in 22 years.

Such population growth and the youth of the population (persons under 18 made

up 54.5 percent of the total in 1973) are causing an extremely rapid rise in

the needs for housing, social services and employment.

Table 5: LABOR FORCE AND EMPLOYMENT, 1973-75

(thousands)

Annual1973 1975 Growth (%)

Agricultural sector

Labor force 1,450 1,510 2.0Full-time employment 520 547 2.6Part-time employment 930 963 1.8

Non-Agricultural sectors

Labor force 1,610 1,780 5.1

Employment 1,173 1,336 6.7

Hydrocarbons 28 35 12.0Industry 174 195 6.7

Construction 190 205 3.9Services 485 561 7.5Government 296 340 7.2

Students and national service 200 245 10.7Unemployed 237 199 -8.3

as % of active population 15 11 -

Source: Tables 1.3 and 1.4.

- 10 -

21. The high employment creation targets set in the 1974-77 Plan havebeen achieved in the first two years of its implementation thanks above allto the considerable investment made. For analyzing employment, Algeria'slabor force is divided into two categories: agricultural and non-agricultural.The employment statistics are relatively reliable for the non-agriculturalsectors, but are less so for agriculture where underemployment is difficult tomeasure. Changes in employment from 1973 to 1975 are summarized in Table 5.According to preliminary estimates, some 163,000 jobs were created in thenon-agricultural sectors, but the final and yet non-published results of theannual survey of non-agricultural employment indicate that the actual figurecould be higher. Despite the rapid increase (5.1 percent p.a.) in the non-agricultural labor force, unemployment has lessened appreciably in bothabsolute and relative terms. Full-time employment in agriculture has alsocontinued to increase, thanks particularly to the expansion of the AgrarianRevolution sector, where nearly 100,000 jobs had been created by the end of1975. Moreover, a large number of the non-agricultural jobs were created inthe interior of the country as a result of the considerable regional develop-ment efforts made by the Government, and this made it possible to absorb apart of the surplus agricultural labor force. The number of workers employedpart-time in agriculture nevertheless remained very high.

22. Algeria stopped the emigration of its workers in 1973. A net returnof about 10,000 emigrant workers per year has since been registered. Of theworker returns, about 4,000 were initiated by enterprises and local govern-ments looking for skilled workers. According to provisional estimates bythe Secretariat of State for Planning, it is likely that in 1976 the numberof workers in industry will, for the first time, exceed that of emigrantworkers.

23. Some major imbalances nevertheless subsist with respect to employ-ment by sector and level of qualification. In the non-agricultural sectors,the new jobs have gone for the greater part to skilled workers, in linewith the considerable training effort made by Algeria. However, many skilledpositions are still open, especially in the middle technical and managerialcategories and in the training system. Unemployment affects almost solelythe unskilled. These imbalances have been accompanied by marked stresses inthe sectoral distribution of skilled workers, owing to variations acrosssectors in wages, salaries and fringe benefits. There has been competitionon employee compensation between the private and public sectors, between thecivil service and the national enterprises in the public sector, and evenamong the public enterprises. Housing availability has also played a veryimportant role in the distribution of the labor force. In a situation char-acterized by shortages, employers have tended to train and retain skilledworkers ahead of the completion of the projects for which they were recruited.This behavior explains partly the approximately 5 percent drop in real valueadded per worker in the industrial sector between 1973 and 1975. It alsoexplains the better investment capability noted in industry as compared withthe other sectors.

Savings and External Deficit

24. Whereas in 1974 national savings exceeded investment, a sizabledeficit appeared in 1975. The investment for 1975 was programmed in thecontext of the 1974-77 Plan and based on levels of oil revenues and savingssimilar to those of 1974. The 1975 decline in hydrocarbon prices and produc-tion brought about a gap of over 20 percent between national savings and in-vestment, which was covered by higher external borrowing.

Table 6: SAVINGS AND EXTERNAL DEFICIT, 1973-75(Based on data in dinars and in current prices)

Item 1973 1974 1975

As percentage of GDP

Gross domestic savings 33.2 50.0 42.0Gross national savings 37.1 49.1 43.4Government current surplus 14.6 31.2 23.5Government oil revenue 13.1 28.1 26.1Emigrant workers' remittances 2.8 1.8 2.0Interest on external debt 1.0 1.9 1.8

As percentage of investment

Gross national savings 82.4 102.3 77.2External deficit 12.4 -3.0 21.2

Source: Tables 2.2, 3.1, 5.1 and 5.2.

25. The savings effort in 1975 did not match the exceptional levelachieved in 1974 but, viewed over the two years it was nonetheless high.Gross domestic savings moved from 33 percent of GDP in 1973 to 50 percent in1974, and to 42 percent in 1975. The marginal domestic saving rate reached56 percent, which means that the greater part of the increase in resourcesresulting from higher domestic production and increased oil and gas priceswas saved. The increase in national savings was less than that in domesticsavings, however, owing to the rapid rise in interest payments on externalloans and the slower growth in emigrant workers' remittances. The Governmentcurrent surplus (budgetary savings) almost tripled in current prices between1973 and 1975 and became the country's main source of savings. This was duefirstly to the rise in the Government's oil revenues, which went from 13percent to 26 percent of GDP, and also to the relatively moderate increasein current public expenditures (see paragraph 40).

26. The Government continued the austerity policy towards private in-comes and consumption. While it keeps closely in check the overall increasein private incomes and consumption, this policy is designed in such a way as

- 12 -

to improve relatively the real incomes of the least privileged social groups.Private consumption rose by about 17 percent a year at current prices since1973, which corresponded to a real annual increase of 7 percent, taking intoaccount the consumer price rises. Public consumption increased by about 9percent a year in real terms over the same period, due mainly to the growth ofpriority expenditures on education and other social sectors such as health.The increase in private consumption was substantially higher than during theprevious Plan period and was attributable chiefly to the rise in employmentand to the steps taken to improve the situation of low-income groups. Wageincreases were kept strictly in line with prior price rises, and the controlson non-essential consumer goods were maintained. The measures to assist low-income groups consisted primarily of the government price subsidies for basicconsumer goods (to offset the higher import prices), the abolition of agricul-tural taxes and the exemption of lower incomes from taxation. In addition,the Government's social expenditures were sharply stepped up.

Balance of Payments

27. During 1974-75, the balance of payments was greatly influenced byhydrocarbon exports and by the national investment program, and it experiencedsharp changes. In 1974, the tripling of oil and gas export receipts produceda sizeable current balance of payments surplus, despite a relatively largeincrease in imports. In 1975, the lower oil and gas export volumes coupledwith the deterioration in the terms of trade and the continuing increase inimports, especially of capital goods, resulted in a considerable currentdeficit. The overall deficit on the balance of payments was, however, rela-tively small because of high inflows of external capital.

- 13 -

Table 7: BALANCE OF PAYMENTS, CURRENT ACCOUNT, 1973-75

Millions of Dinars Millions of US Dollars

1973 1974 1975 1973 1974 1975

Exports of goods andNFS /1 8,345 20,634 19,494 2,108 4,935 4,936

(Hydrocarbons) (6,700) (18,117) (15,938) (1,692) (4,333) (4,036)

Imports of goods andNFS /1 -10,741 -18,718 -25,901 -2,713 -4,477 -6,559

(Capital goods) (-3,163) (-5,580) (-9,503) (-799)(-1,335) (-2,406)

(Foodstuffs) (-1,208) (-2,827) (-4,534) (-305) (-676) (-1,148)

Resource balance -2,396 1,916 -6,407 -605 458 -1,623

Interest payments -330 -910 -930 -83 -218 -231

Interest receipts 80 617 276 20 148 70

Workers' remittances (net) 698 654 795 176 156 201

Other services andtransfers (net) 190 -1,609 108 48 -384 23

Net factor servicesand transfers 638 -1,248 249 161 -298 63

Current accountbalance -1,758 668 -6,158 -444 160 -1,560

Memo items

Terms of trade index(1973=100) 100 183 151

Exchange Rate(Dinars per US dollar) 3.96 4.18 3.95

/1 The import statistics are taken from financial settlement data prepared

by the Central Bank; it should be noted that imports of capital goods

against supplier credit have been included only since 1974. The export

statistics are based on Customs data.

Source: Tables 3.1, 3.4, 3.5 and 3.9 and Annex I.

28. From 1973 to 1975, the rise in export receipts was accompanied by

a reduction in total export quantities. In quantity, crude oil exports de-

clined by 12 percent during the two years, but exports of refined products

and liquefied gas went up. Export of agricultural products declined by more

than half in quantity, mainly because of the lower wine exports and the grow-

ing domestic demand for the other products that are exported (particularly

- 14 -

fruits). By contrast, industrial exports, which still made up only a smallproportion of total exports, increased and there was a rapid growth ofservice exports. The main export categories have changed as follows incurrent and constant prices (in millions of Dinars):

In current prices In constant 1975 prices /11973 1974 1975 1973 1974 1975

Hydrocarbons 6,700 18,117 15,939 17,540 16.427 15,939(Crude oil andcondensate) (6,050) (16,974)(14,453) (16.440) (15,361) (14,454)

Agricultural products 910 664 672 1,429 1,201 672Other raw materials 119 311 210 180 388 210Industrial products 245 358 384 341 388 384Services 1,096 1,398 1,834 1,533 1,513 1,834

Total /2 9,070 20,848 19,039 21,023 19,917 19,039

/1 Mission estimates, see Annex I./2 The totals do not correspond with those shown under balance of payments

because of statistical differences.

The above figures bring out the dominant effect of changes in the export priceof crude oil. Such price rose from an average of US$4.31 per barrel in 1973to US$12.26 in 1974 and decreased to US$11.73 in 1975. As a result of thesechanges, the share of total exports of goods and services accounted for byhydrocarbons rose from 74 percent in 1973 to 84 percent in 1975.

29. The marked increase in investment, food requirements and the substan-tial rise in international prices were the main factors behind the increase inimports at current and constant prices. Based on price indices estimated bythe mission for each major import category, the increase in total goods andservices imports at constant 1975 prices was about 25 percent in 1974 and 20percent in 1975 (Annex I). The sharpest rises were in capital goods andassociated services, which more than doubled over the two years 1974-75, andfoodstuffs, especially cereals. The overall import price index rose by anestimated 33 percent in 1974 and an estimated 16 percent in 1975. Thegreatest increases were in the prices of foodstuffs, raw materials and semi-manufactures. Changes in the quantities and prices of the different categoriesof imports have altered their composition in current prices as follows:

- 15 -

Percentages1973 1974 1975

Capital goods and associated services /2 34.5 34.1 41.8Food products 16.5 20.8 16.9Raw materials and semi-manufactures 31.4 31.7 27.1Consumer goods 13.4 10.1 10.4Services 4.2 3.3 3.8

100.0 100.0 100.0

/1 Based on Customs data./2 These services comprise technical assistance and major civil works

by foreign enterprises.

As a result of the considerable investment effort, the share of capital goodsand associated services in total imports rose to more than 40 percent in 1975.After an exceptional peak of 21 percent of the total in 1974, the share offoodstuffs dropped back to 17 percent in 1975, which was still a considerableburden for the country. The relative importance of the other categories,especially consumer goods, declined appreciably.

30. Despite the reversal in external price trends in 1975, the termsof trade in that year were still some 50 percent above their 1973 level.Algeria used this gain however largely to step up imports. Over the two years1974-75, the increase in export receipts represented US$189 per capita whilethe rise in import expenditures amounted to US$256 per capita.

31. The balance of factor services and transfers, which had been posi-tive since 1970, showed a large deficit in 1974 and returned to a slightsurplus in 1975. The 1974 deficit was due mainly to Government transfers forcontributions to international cooperation (DA 1,785 million or US$427 mil-lion). At the same time, interest payments increased rapidly as a result ofincreased borrowing from private external sources, while net workers' remit-tances tended to level out following the interruption of worker emigrationto Europe and the increase in transfers of foreign workers in Algeria.

- 16 -

Table 8: CAPITAL ACCOUNT AND EXTERNAL FINANCING, 1973-75

Millions of Dinars Millions of US DollarsItem 1973 1974 1975 1973 1974 1975

Current account balance -1,758 668 -6,158 -444 160 -1,560Direct investment (net) 200 1,504 196 51 360 50Long-term official loans:

Disbursements 559 592 876 141 142 222Repayments -190 -255 -254 -48 -61 -64

Long- and medium-termcommercial loans:Disbursements 3,884 2,049 6,599 981 490 1,671Repayments -452 -1,697 -1,149 -114 -406 -291

Other items (net) /1 147 -2,190 -972 37 -524 -246

General balance 2,390 671 -862 604 160 -218Net foreign assets(end of period) 4,587 5,258 4,396 1,096 1,315 1,066

/1 Operations pending, and errors and omissions.

Source: Tables 3.1, 3.9 and 6.1.

32. The 1974 current surplus enabled the Government to repay in advancea part of the external commercial bank loans. Net inflows from official andcommercial loan sources therefore only aggregated US$165 million in 1974 asagainst US$963 million in 1973. By contrast, net direct investments byforeign companies (mainly oil and public works companies) amounted to US$360million. In 1975, external borrowing, chiefly from commercial sources, rosesharply, with the net inflow on medium- and long-term loans totaling US$1,538million. This inflow did not however cover fully the current account deficit,and reserves were drawn down. At the end of 1975, Algeria's net foreignassets amounted to US$1,066 million, equivalent to two months of 1975 importsof goods and services.

External Debt and Debt Service

33. In 1974 and 1975, some 90 percent of external loan commitments wereobtained from private commercial sources. Bilateral and multilateral publicloans at concessionary terms only made up 10 percent of 1974-75 commitments.Suppliers' credits, which increased from 15 percent of total commercialcredits in 1973 to 53 percent in 1975, have risen very rapidly in relation toinvestment and imports of capital goods. The growing relative importance ofcredits from private sources has caused a hardening of the average terms onAlgeria's external debt. The ratio of interest payments to disbursed debtwas 6.9 percent in 1975 as against 5.5 percent in 1973. At the end of 1973,

- 17 -

maturities on Algeria's external debts ranged up to 5 years for 43 percentof the total, between 5 and 10 years for 40 percent, between 10 and 15 yearsfor 14 percent, and 15 years and longer for 3 percent. The shortening ofthe average maturity of external loans implies a rapid rise in roll-overneeds in the years ahead.

Table 9: EXTERNAL DEBT AND DEBT SERVICE, 1973-75

Millions of US Dollars1973 1974 1975

Commitments 2,304 1,458 3,255

Official sources 399 327 184Private commercial sources 1,905 1,131 3,071

(Commercial banks) 1,613 466 1,453(Suppliers' credits) 292 665 1,618

Total debt outstanding (year's end) 4,942 6,031 8,764

Total debt disbursed only (year's end) 2,955 3,330 4,518- as percentage of GDP 37.1 29.1 34.6

Debt service 304 714 586- as percentage of exports 14.4 14.5 11.9- as percentage of Government

revenues 10.9 12.7 9.1

Source: External debt report; provisional estimates for 1975.

34. Provisional Government and IBRD estimates indicate that as of theend of 1975, external debt outstanding and disbursed reached US$4.5 billion,to which should be added an almost equal amount of undisbursed debts. Theratio of disbursed debt to GDP diminished substantially in 1974, due to therapid rise in GDP at current prices and the advance repayments made by theGovernment. This ratio however moved back up to nearly 35 percent in 1975following the sharp increase in external borrowing. Debt service remained at14.5 percent of exports of goods and services in 1974 as a result of advanceloan repayments made in that year, and then dropped to less than 12 percentin 1975, a level which left Algeria with a sizable capacity to incur furtherindebtedness.

Public Finances

35. The reforms introduced in the financial system in 1971 and 1972assign the Government a preponderant role in the mobilization and allocationof the country's financial resources. The Government taps the greater partof national savings through taxation and Treasury operations designed to

- 18 -

mobilize liquid funds. In 1973-75, the amounts mobilized by the Treasury--inthe form of budgetary savings, deposits by correspondents and bond issues--represented three-quarters of national savings. Regarding the allocation ofthese resources to investment, the Government exercises particularly closecontrol through the central planning system. Some 81 percent of fixed invest-ment made in 1973-75 was authorized through individual approvals 1/ given bythe Government for each development project or program included in the annualand multi-year plans. The Government further strongly influenced the alloca-tion of the remaining 19 percent (unplanned and private investments) throughthe various regulations in force, particularly those governing bank credit.

36. The financing of projects and programs is effected through thefinancing plans laid down in individual approvals and revised subsequently ifneed be. Government capital expenditures are financed from the budget and theTreasury assumes responsibility for any foreign loans that are allocated tothe financing of such expenditures. The capital expenditures of public enter-prises are financed with loans from the Treasury, the banking system andforeign sources. All funds pass through the banking system, which controlstheir use as directed by individual approvals. The banks involved are eitherthe Banque Algerienne de Development (BAD), the Caisse Nationale d'Epargneet de Prevoyance (CNEP) or one of the three primary banks (BNA, BEA or CPA).Some changes were made in the financial system in 1976 with a view to intro-duce some decentralization. These changes are described in Section III.

37. The accounts of local governments, certain public institutionsand public enterprises are not yet consolidated in Algeria. An overall viewof public sector finances, particularly with respect to current operations,cannot therefore be taken. The Treasury's accounts are however available(Tables 10 and 5.1), and they closely follow developments in the economy dueto the importance, just described, of the role played by the Government.

38. Treasury accounts showed sharp changes during the first twoyears of the 1973-77 Plan. In 1974, budgetary savings more than tripled,primarily as a result of higher oil revenues. Despite a very marked expan-sion in the Government's funding of investment and debt rescheduling ofpublic enterprises 2/, there was an overall budget surplus. In 1975, bycontrast, budgetary savings declined somewhat, whereas investment growthaccelerated and debt rescheduling of enterprises remained at a high level.As a result, a relatively sizable overall budget deficit was experienced.

1/ These individual approvals are officially known as "decisionsd'individualisation et de financement" in Algeria.

2/ Debt rescheduling of public enterprises is officially called inAlgeria "assainissement financier" or "re-structuration financiere".

- 19 -

Table 10: SUMMARIZED TREASURY ACCOUNTS, 1973-75

Millions of Dinars Percentage of GDPItem 1973 1974 1975 1973 1974 1975

Oil revenue 4,116 13,402 13,462 13.1 28.1 26.1Ordinary tax revenue 5,701 7,976 9,891 18.1 16.7 19.2

Other current revenue 1,195 2,036 2,019 3.8 4.3 3.9Current expenditures -6,415 -8,501 -13,231 -20.3 -17.8 -25.6

Budgetary savings 4,597 14,916 12,141 14.6 31.2 23.5

Investment -7,353 -9,363 -14,724 -23.3 -19.6 -28.5(Investment expenditures) (3,719) (4,130) (5,505) (11.8) (8.6) (10.7)(Investment loan dis-bursements) (3,634) (5,263) (9,219) (11,5) (11.0) (17.8)

Enterprises' debt re-scheduling -784 -3,623 -3,854 -2.5 -7.6 -7.5

Miscellaneous capital,net 142 28 968 0.5 0.1 1.9

General balance -3,398 1,958 -5,469 -10.8 4.1 -10.6

/1 Details may not add up to totals due to rounding.

Source: Tables 5.1, 5.2 and 2.1.

39. Already high in 1973 and preceding years, tax revenue increased in1974 (44.8 percent of GDP) and in 1975 (45.3 percent of GDP). Oil revenueaccounted for the bulk of this increase, the Government having capturedvirtually the full amount of additional receipts from higher hydrocarbonprices. Oil tax revenue was equivalent to 61 percent of the current valueof hydrocarbon exports in 1973, to 74 percent in 1974 and to 84 percent in1975, thanks partly to improvements in collection procedures. It should bestressed, however, that in 1975 revenue from ordinary taxation exceeded therelative level reached in 1973, after a slight drop in 1974. This increasewas accounted for by receipts from indirect ordinary taxation on importedgoods and services (see Table 5.2). Receipts from direct ordinary taxationalso increased but did not keep pace with GDP. The absolute value of thecontributions of the public enterprises to the Government's budget declinedin 1975.

40. The ratio of Government current expenditure to GDP showed a sharpincrease in 1975 after dropping in 1974. The normal current expenditures(personnel, materials, maintenance and miscellaneous; Table 5.3) remained ina constant proportion to GDP (13 percent) in 1974 and 1975, notwithstandingwage and salary increases in 1975 of 30 percent for teachers and 20 percent

- 20 -

for other government personnel. On the other hand, current transfers, par-ticularly those benefiting the less privileged social groups, showed a verymarked increase. Transfers to individuals (family allowances, student grants,etc.) rose from DA 0.9 billion in 1973 to more than DA 2 billion in 1975.More importantly, price subsidies to staple foodstuffs (cereals, sugar andedible oil) amounted to DA 3.4 billion in 1975, or 6.6 percent of GDP, com-pared to nil in 1973 and only a very small amount in 1974. These subsidiesmade it possible to maintain the consumers' purchasing power while ensuringavailability of supplies through imports that had to be made at 1975's highprices. They were nonetheless one of the causes of the budget deficit in thatyear. Algeria pursued a policy of modest defense spending (2.3 percent of GDPin 1974 and 2.5 percent in 1975). It also continued giving priority toeducation and training. For reasons connected with their absorptive capacity,the two education ministries' expenditures declined somewhat in relation toGDP (6.9 percent in 1975 as against 8.3 percent in 1973), but it should benoted that these expenditures do not cover the training effort made by thetechnical ministries (Industry, Agriculture and Public Works) and the enter-prises reporting to these. Systematic records have not been kept of thiseffort, but it is known to have been stepped up very rapidly.

41. Government investment expenditure (Table 5.5) favored the sectorsthat lagged behind industry in 1974 and 1975, especially rural development,water development, communications and social infrastructure. However, theauthorities responsible for these sectors had difficulty raising theirimplementation capacities to the levels set in the Plan for 1974-77. In 1975,the Government's investment expenditure increased by 38 percent from the 1974level, but was one third below budget allocations.

42. Government loans for investment and debt rescheduling of publicenterprises increased spectacularly. Loans for investment were in 1975some 2.5 times larger than in 1973, most of the increase having gone toindustry (see paras 6 to 8). Loans for debt rescheduling nearly quintupled,reaching about US$870 million in 1974 and US$970 million in 1975. The re-scheduling operations made it possible to clear cumulative deficits and torestructure the debts of public enterprises that had been in growing financialdifficulties for several years for a variety of reasons (inappropriate initialfinancing of investments, unfavorable cost/price relationships, managementshortcomings, etc.). They were an essential step for implementation of thedecentralization policy (see paras 59 to 63).

43. The overall budget surplus in 1974 enabled the Treasury to reduceits net indebtedness to the banking system (see Table 6.1). By the endof 1974, it had built up a healthy credit balance with the Central Bank whilereducing its indebtedness to the primary banks by over DA 1 billion over theyear (see Tables 6.2 and 6.3). The overall deficit in 1975 was covered for alarge part (61 percent) by the increase in deposits by Treasury correspondents(including the Postal Checking Accounts) and drawing down the Treasury accountwith the Central Bank, as well as, to a lesser extent, by net proceeds fromequipment bonds issues. The net position vis-a-vis the Central Bank neverthe-less moved slightly into debit as of the year's end.

- 21 -

Money, Credit and Prices

44. The causative factors of money supply behaved as follows during 1974and 1975 (variations during the year computed from the figures given in Tables6.1 and 6.2):

In millions of Dinars As percentages1974 1975 1974 1975

Gross credit to Treasury 219 2,283 4 39Treasury deposits 1,577 -1,190 350 -59Net credit to Treasury -1,357 3,473 -26 90Credit to economy 5,954 7,158 37 33Net foreign assets 871 -862 19 -16Money supply 4,593 7,402 23 30

As shown by the above data, credit to the economy was the main factor behindthe expansion of money supply in 1974 and 1975. In Algeria, such credit ismade up primarily of credit to the public and collective enterprises. Thegrowth of money supply was distinctly slower than that of GDP at currentprices in 1974 (23 percent as against 51 percent) and it can be concluded thatthe upward pressure on prices in that year came entirely from abroad, i.e.through import and export price increases. In 1975 the reverse occurred;money supply expanded more rapidly than GDP (30 percent against 8 percent) andnet foreign assets diminished, which would appear to indicate that pressureson prices were mainly of domestic origin, although there was also the effect,deferred by controls, of some 1974 external price increases.

45. Indeed, it may be seen (Table 9.1) that the growth of the consumerprice index accelerated in 1975--it was 6.5 percent in 1974 and 10.9 percentin 1975. Price subsidization made it possible to moderate somewhat food priceincreases, which nonetheless were 10 percent in 1974 and 13.4 percent in 1975.Meat and vegetable prices increased sharply for a while in the winter of1975/76 owing to problems in supplying the main urban areas following thereform of trade channels in these commodities which was introduced two yearsago. By the beginning of the summer of 1976, these problems appeared howeverto have been solved for the greater part (see para 60). Production priceshave changed in line with consumer prices. Agricultural prices have beenraised substantially to encourage production; they rose 12 percent in 1974and 19 percent in 1975 (Table 9.2). Industrial prices have also been raised,particularly those of strategic products (cement, steel products, etc.) toestablish more realistic cost/price relationships; industrial prices went up8 percent in 1975 and 12.5 percent in 1975. Overall, the extremely compre-hensive price regulations were applied in 1974 and 1975 with much greaterflexibility than in the past, and this made it possible to absorb a large partof the accumulated and new pressures on prices in Algeria and to establishmore adequate relationships between domestic prices.and factor costs.

- 22 -

46. To preserve the real purchasing power of the wage-earning population,the Government authorized sizable wage increases, especially for the lower-paid groups. Minimum wage increases were as follows:

Agriculture Other sectorsAs of: Dinars/day Dinars/hour

May 1, 1972 9.80 1.73January 4, 1974 12.25 2.08January 1, 1976 15.30 2.40

Family allowances and other social transfers were also increased. Steps weretaken to ease the tax burden on farmers and the lower-income groups. Publicsalaries were increased as of the end of 1974 (see para 40). The ceiling onthe taxable income of individuals was raised in 1975 from DA 2,000 to DA2,500/month. A national commission set up in 1974 continued the studiesneeded for reform of the regulations governing individual wages and otherincomes called for under the 1974-77 Plan.

The Situation in 1976

47. The economic situation appears to have been consolidated in 1976.Based on the data available as of this writing and on indications regardingdevelopments during the year, there have been an appreciable acceleration ofGDP growth and an increase in hydrocarbon exports in both quantity and price.There has been also a stabilization of investment. In combination, these twofactors have reduced the resource gap and enabled the Government to keep thedomestic and external financial situation under control. Further, investmentsmoved towards a more balanced sectoral distribution.

48. An investment stabilization program was put into effect in 1976to bring the economy back into real and financial balance. The Governmentdecided, when drawing up the budget and annual plan for 1976, to maintain theinvestment of public enterprises in industry at the same level as in 1975,in nominal terms. In addition, the budget allocations for Government andpublic-enterprise investment in other sectors were kept at practically thesame nominal level as in the 1975 budget. The figures below illustrate thesedecisions (Millions of Dinars):

Fixed Investment1975 1976

Budget Actual Budget

Public enterprises, industry 12,000 11,970 12,000

Government and public enter-prises, other sectors 13,670 8,960 14,020

- 23 -

Assuming the public enterprise program in industry has been carried out in itsentirety, as in 1975, and that the implementation rate of the Government andpublic-enterprise program in the other sectors will move up to about 80 per-cent in 1976 (against 65 percent in 1975), an increase in total public-sectorinvestment of the order of 10-12 percent in nominal terms would result.Taking into consideration the expected rise in prices of capital goods, thecorresponding real increase would be 4-6 percent. The public-investmentstabilization program should therefore bring about a reduction in the ratioof total investment to GDP, which reached a very high level in 1975.

49. The public investment program in the industrial sector (hydro-carbons, mining, manufacturing and energy) has been stabilized at DA 12billion, representing a reduction in real terms of about 6 percent. Theshare of investment in industry would thereby be brought down from 57 percentof total public investment in 1974-75 to about 50 percent in 1976. This wouldstill be higher than the base percentage set in the 1974-75 Plan (43.5%), butwould nevertheless denote a trend towards a more appropriate sectoral distri-bution of investments. Given the extraordinary dynamism of industrial invest-ment, the stabilization policy initiated in 1976 is clearly difficult to putinto effect. In view of this, the Ministry of Industry has undertaken to slowdown the overall implementation rate of its program, while maintaining thecomposition as provided for by the long-term industrial development strategy.Orders of priority have been set for the different categories of projects inpreparation or under implementation, while bringing completed projects intoproduction has been speeded up (see Annex II).

Table 11: PUBLIC INVESTMENTS IN THE NON-INDUSTRIAL SECTORS, 1975 AND 1976(Millions of Dinars; current prices)

1975 1976Budget Actual Budget

Agriculture and rural development 2.236 1.486 1.856Irrigation and water development 860 648 747Transport and telecommunications 2.305 1.860 2.425Infrastructure /1 2.386 1.807 2.690Housing 1.170 1.181 1.578Special regional programs 1.340 - /2 1.050Education and training 1.797 1.212 1.855Administration 400 289 378Trade, tourism and non-allocated budget 1.176 478 1.441

Total 13.670 8.961 14.020

/1 Construction and public works enterprises, industrial estates, urbandevelopment, local government plans and social infrastructure.

/2 Spread over the other categories.

- 24 -

50. As regards the non-industrial sectors (Table 11), the 1976 budgetallocations show pronounced increases for housing (11.3 percent of the non-industrial investment budget compared with 8.6 percent in 1975) and infra-structure, including construction enterprises (19.2 percent in 1976 comparedwith 17.5 percent in 1975). The investment budget for trade is also higher(3.2 percent in 1976 as against 2 percent in 1975). These increases are inresponse to the need to reduce the considerable lags which the development ofthese sectors experienced as compared with the development of the industrialsector. The budget allocations for transportation, telecommunications,education and training have been maintained at about the same levels as in1975. The investment budget for agriculture, rural development and waterdevelopment was scaled down in 1976, to take account of the absorptivecapacity of these sectors, which had been overestimated when setting up the1974 and 1975 budgets with low implementation rates as a result. The budgetfor special regional development programs, which benefit selected wilayate(provinces), has also been reduced because most of these programs are nearingcompletion and are being replaced by the rapidly expanding village and citydevelopment plans.

51. Production in 1976 should benefit from the expected upturn in thehydrocarbon sector. The technical problems posed by the secondary recoveryof crude oil deposits which had caused lower production since 1973 appearto have been solved. The international demand for petroleum products has,moreover, improved. According to estimates by the Secretariat of State forPlanning, production of crude oil and condensate should reach 50 million tonsin 1976 compared with 45.4 million tons in 1975. Gas production should go upfrom 7.4 billion m3 to 10 billion m3 and there should also be an appreciableincrease in the output of refined petroleum products. Altogether, the valueadded of the hydrocarbon sector is expected to be 10 percent up in real termsand hydrocarbon exports should total US$4.7 billion in current prices, asagainst US$4 billion in 1975.

52. Substantial growth is also expected in other sectors. In agricul-ture, the 1975/76 cereal crop benefited from abundant and well distributedrain. Agricultural crops are benefiting now from production prices which,apart from some exceptions such as sugarbeet, appear to be remunerative. Theincreasing management autonomy granted to collective farms in the course ofthe past two years is beginning to have a positive effect on their results.In manufacturing, the production of certain branches (heavy industry, steel,mechanical industry and construction materials) is expected to rise sharply asnew units come into production. Output in light industries should benefitfrom the general rise in purchasing power, especially on the part of farmers,and from the measures taken in 1975 to improve trade channels. For industryas a whole, an increase in capacity utilization can be expected, especially inthe 144 units that came into operations in 1974 and 1975. Finally, consider-able production increases are expected in energy, construction (especiallyhousing construction) and transport, in view of the strong demand and thehigh investments made in preceding years.

- 25 -

53. Altogether, GDP should grow by over 10 percent in real terms in

1976, which would be an appreciable acceleration from the growth rates of the

previous two years. Growth of total consumption should speed up under the

effect of higher domestic income (GDY) and an improved domestic supply of

agricultural and industrial products. This increase in consumption would be

in line with the Government's social policy since it would originate for a

large part from the least privileged social groups who now have access for the

first time to employment and income. Savings would, nonetheless, increase

sufficiently to cover a larger part of total investment than they did in 1975.

54. The resource gap is therefore likely to be significantly smaller