kuwait files/arabic...feasibility study offered by the proposer that has an economic and social...

TRANSCRIPT

KUWAIT PUBLIC-PRIVATE PARTNERSHIP PROJECTSPROJECT GUIDEBOOK 2018

2 K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

© 2018 Kuwait Authority for Partnership Projects Touristic Enterprises Company BuildingSecond FloorAl-Shuwaikh Administrative ZoneAl-Jahra Street Telephone: 00 965 – 2496 5900 Internet: http://www.kapp.gov.kw/en/Home

This work is a product of the staff of the Kuwait Authority for Partnership Projects with external contributions. The findings, interpretations, and conclusions expressed in this work do not necessarily reflect the views of the Kuwait Authority for Partnership Projects, its Board of Executive Directors, or the governments they represent.

The Kuwait Authority for Partnership Projects does not guarantee the accuracy of the data included in this work. The boundaries, colors, denominations, and other information shown on any map in this work do not imply any judgment on the part of the Kuwait Authority for Partnership Projects concerning the legal status of any territory or the endorsement or acceptance of such boundaries.

Rights and Permissions

Any queries on rights and licenses, including subsidiary rights, should be addressed to the Kuwait Authority for Partnership Projects, Touristic Enterprises Company Building, Second Floor, Al-Shuwaikh Administrative Zone, Al-Jahra Street or email [email protected].

Page 271 photo © ArloMagicman/istockphoto.com/ Original Report and Cover design: Victoria Adams-Kotsch.

i

KUWAIT PUBLIC-PRIVATE PARTNERSHIP PROJECTSPROJECT GUIDEBOOK 2018

i i K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

i i iC O N T E N T S

CONTENTS

MESSAGE FROM HIS EXCELLENCY, THE MINISTER OF FINANCE viii

MESSAGE FROM THE DIRECTOR GENERAL OF KUWAIT AUTHORITY FOR PARTNERSHIP PROJECTS ix

ACKNOWLEDGMENTS x

ABBREVIATIONS AND ACRONYMS xii

CHAPTER 1: PUBLIC-PRIVATE PARTNERSHIPS—AN INTRODUCTION 1

1.1 What are PPPs? 1

1.2 What are the Benefits of PPPs? 2

1.3 Value for Money 2

1.4 Types of PPP 4

1.5 PPP Process 6

1.5.1 Project Initiation 7

1.5.2 Project Feasibility and Structuring 7

1.5.3 Project Procurement 8

1.5.4 Project Implementation and Monitoring 8

1.6 Further Readings 9

CHAPTER 2: PPP LEGAL AND INSTITUTIONAL STRUCTURES IN KUWAIT 11

2.1 Introduction 11

2.2 Key Features of Law No. 116 of 2014 Regarding Public-Private Partnerships 11

2.2.1 Transition Arrangements 13

2.2.2 Key Aspects of Executive Regulations 13

2.3 Key Differences between the 2008 and 2014 Legislation 13

2.3.1 Establishing the Project Company and Shareholding Structure 14

2.3.2 Changes in Project Documentation 14

2.3.3 Ownership and Security over Assets 15

2.3.4 Procurement Processes 15

2.3.5 Term 16

2.3.6 Land 16

2.4 Interface with Other Legislation 16

2.5 Institutional Structure for PPPs 17

i v K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

2.5.1 The Higher Committee (HC) 17

2.5.2 The Kuwait Authority for Partnership Projects (KAPP) 18

2.5.3 Public Entities 19

2.5.4 The Department of Legal Advice and Legislation 20

2.5.5 The State Audit Bureau 20

2.6 Kuwait PPP Flow Process 21

CHAPTER 3: PROJECT INITIATION 23

3.1 The Legal Framework for Project Initiation 23

3.2 Solicited Project Proposals 24

3.2.1 The Role of the Public Entity at Initiation 24

3.2.2 The Role of KAPP at Initiation 25

3.2.3. Establishing the Competition Committee 25

3.2.4 The Role of the Transaction Advisor 25

3.2.5 The Process for Recruiting the Transaction Advisor 26

3.3 Unsolicited Project Proposals 36

3.3.1 Introduction to Unsolicited Proposals 36

3.3.2 Procedures for Initiating Unsolicited Project Proposals 38

CHAPTER 4: PROJECT FEASIBILITY AND STRUCTURING 39

4.1 The Legal Framework for Feasibility Studies 39

4.2 Feasibility Studies for Solicited Projects 43

4.2.1 Pre-Feasibility Studies 43

4.2.2 Comprehensive Feasibility Studies 45

4.2.4 Indicative List of Requirements for the Comprehensive Feasibility Study Report 62

4.2.5 Feasibility Study Approval 63

4.2.6 Indicative Timelines for Tendering a Project 64

4.2.7 Financing Sources, including Viability Gap Funding 66

4.2.8 Other Forms of Government Support 67

4.3 Feasibility Studies for Unsolicited Projects 67

4.3.1 Legislative Arrangements for USP Feasibility Studies 67

4.3.2 Feasibility Study Arrangements for USP Initiatives 69

CHAPTER 5: PROJECT PROCUREMENT 71

5.1 Important Considerations in the Pre-Procurement Stage 71

5.1.1 The Legal Framework for Procurement Process 71

5.2 Initiation of the Procurement Process: Calls for Expressions of Interest 78

5.3 Pre-Qualification 78

vC O N T E N T S

5.3.1 Introduction to Pre-Qualification 78

5.3.2 Important Considerations in the Pre-Qualification Stage 79

5.4 Preparation, Approval, and Distribution of the RFQ Documents 81

5.4.1 Preparation of RFQ Documents 81

5.4.2 Approval of RFQ Document 85

5.4.3 Advertisement and Distribution of RFQ Document 85

5.5 Pre-Qualification Documents and Approval of Pre-Qualified Parties 87

5.5.1 Receipt of Pre-Qualification Documents 87

5.5.2 Evaluation of the Pre-Qualification Documents 87

5.5.3 Approval of Pre-Qualified Investors 88

5.6 Preparation and Approval of the Request for Proposals (RFP) 89

5.6.1 Preparation of the Request for Proposal 89

5.6.2 Approval of the Request for Proposal 106

5.6.3 Important Considerations for Managing the Bid Process 106

5.7 Bidding 109

5.7.1 Role of the Competition Committee 114

5.7.2 Bidding Process with Post-Qualification 114

5.8 Competitive Dialogue Process (pursuant to Article 34 of the Regulations) 115

5.9 Contract Finalization 116

5.10 Sale of Shares of Public Joint Stock Company 122

5.10.1 Incorporation of Public Joint-Stock Company 126

5.10.2 Process of Transfer of Shares 126

5.10.3 Role of KAPP as Temporary Shareholder 127

5.10.4 Tender Process for Investor Shares 127

5.10.5 Equity Rate of Return for Citizen Shareholders 127

CHAPTER 6: PROJECT FINANCING ISSUES 129

6.1 Equity Bridge/Shareholder Loans 129

6.2 Security 129

6.3 Refinancing 130

6.4 Timetable to Financial Close 130

6.5 Termination Payments 130

CHAPTER 7: OTHER CONTRACTING ISSUES 131

7.1 Kuwaitization Requirements 131

7.2 Handover Bonds 131

7.3 Bidding Restrictions 131

v i K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

CHAPTER 8: PROJECT IMPLEMENTATION AND MONITORING 133

8.1 Contract Management Process 135

8.2 Performance Monitoring 136

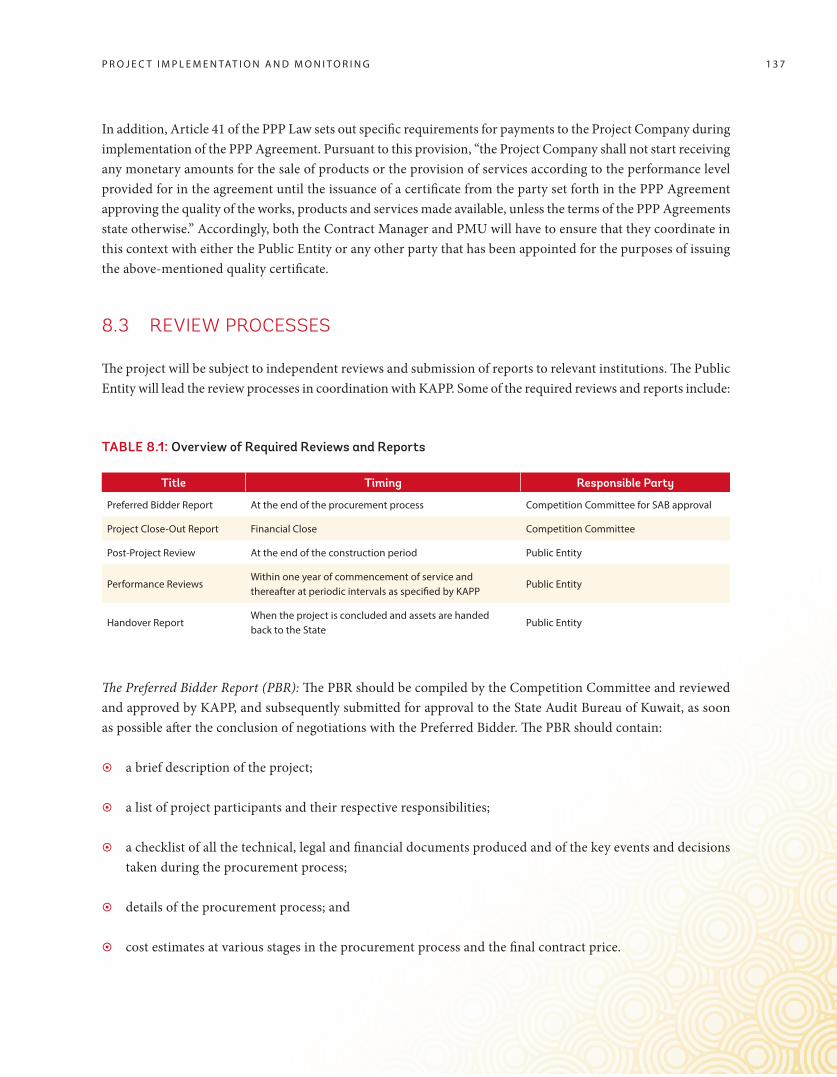

8.3 Review Processes 137

8.4 Dispute Resolution 139

8.5 Renegotiation Requests 140

8.6 Termination 140

8.7 Concession Extension 141

8.8 Handback Procedures 141

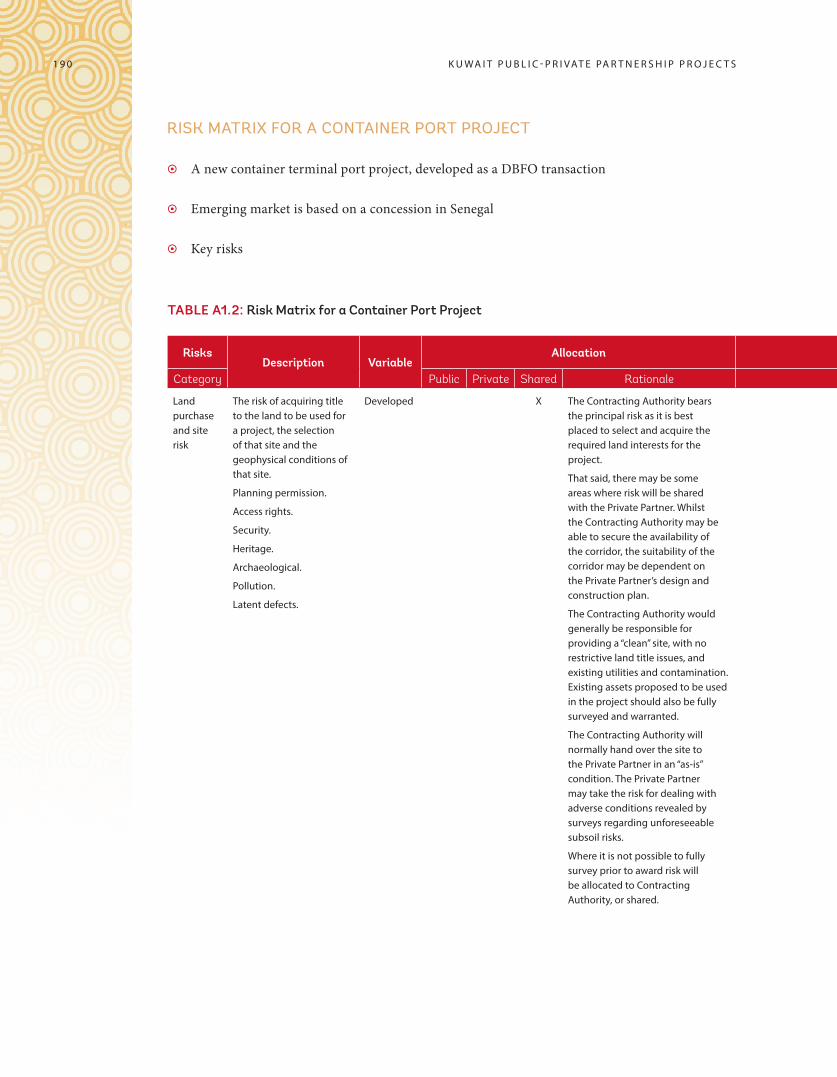

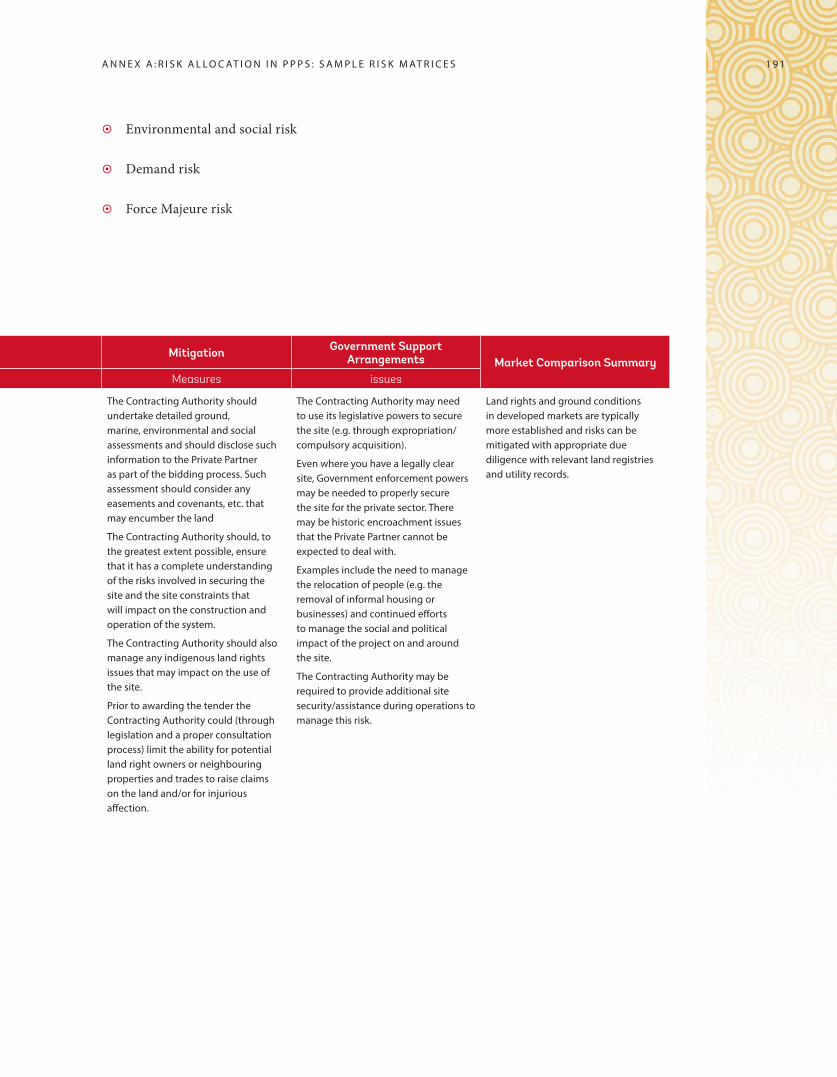

ANNEX A: RISK ALLOCATION IN PPPs: SAMPLE RISK MATRICES 142

Risk Matrix for a Water Desalination Project 143

Risk Matrix for a Container Port Project 190

ANNEX B: RECOMMENDED PPP CONTRACTUAL PROVISIONS, WITH GUIDANCE NOTES 224

B.1 Force Majeure 224

B.2 Material Adverse Government Action 231

B.3 Change in Law 235

B.4 Termination Payments 242

B.5 Refinancing 248

B.6 Lenders’ Step-in Rights 251

B.7 Confidentiality and Transparency 254

B.8 Governing Law and Dispute Resolution 259

v i iC O N T E N T S

FIGURES

Figure 1.1: Spectrum of PPP Agreements 4

Figure 1.2: The PPP Process 6

Figure 2.1: PPP Project Cycle, Kuwait 21

Figure 4.1: Process to Calculate Risk Adjusted PSC 57

Figure 4.2: Competitive Neutrality Adjustment 58

TABLES

Table 2.1: Comparison of Joint Stock Company Share Allocation Arrangements under the PPP Law and the Old Law 14

Table 4.1: Indicative Timelines for Tendering a Project 64

Table 8.1: Overview of Required Reviews and Reports 137

Table 8.2: PPP Concession Extension 141

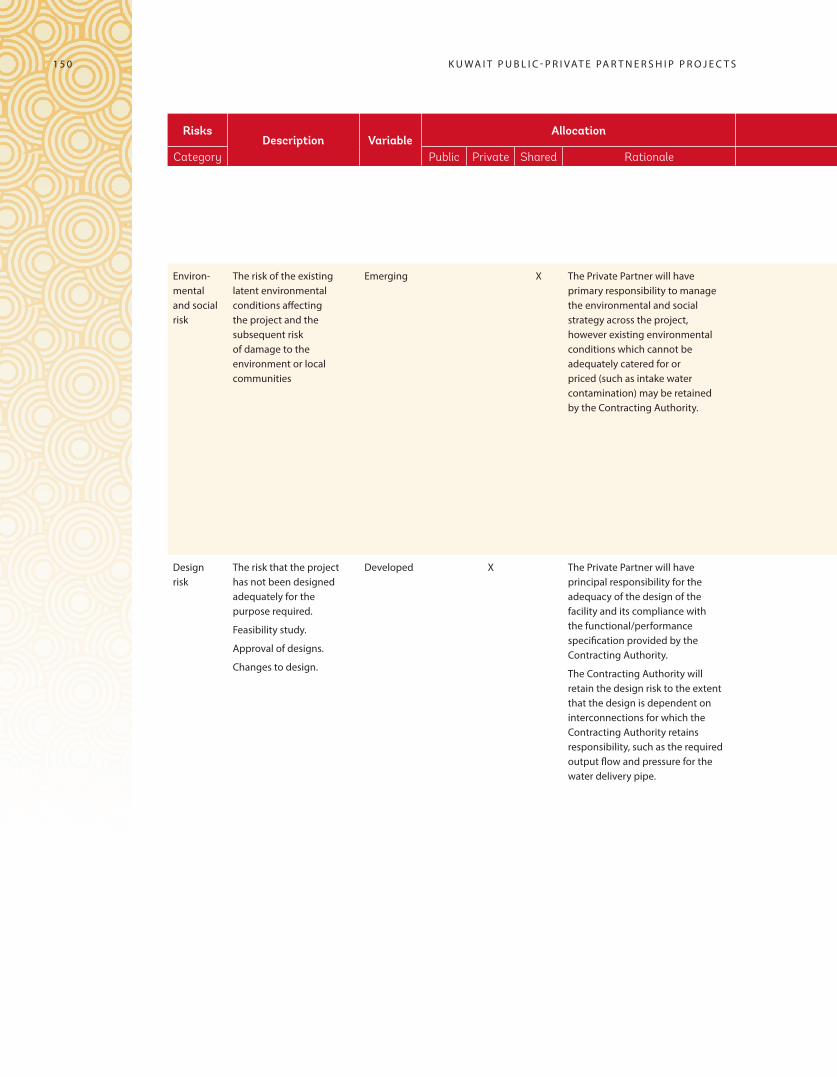

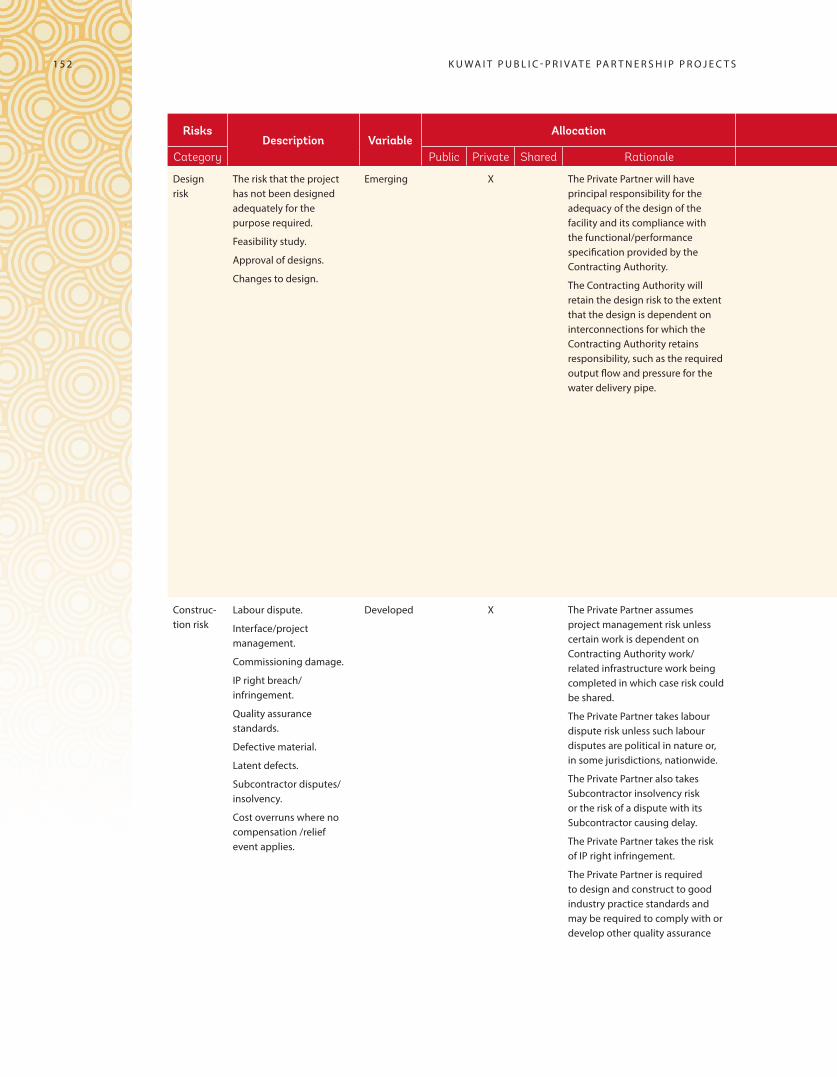

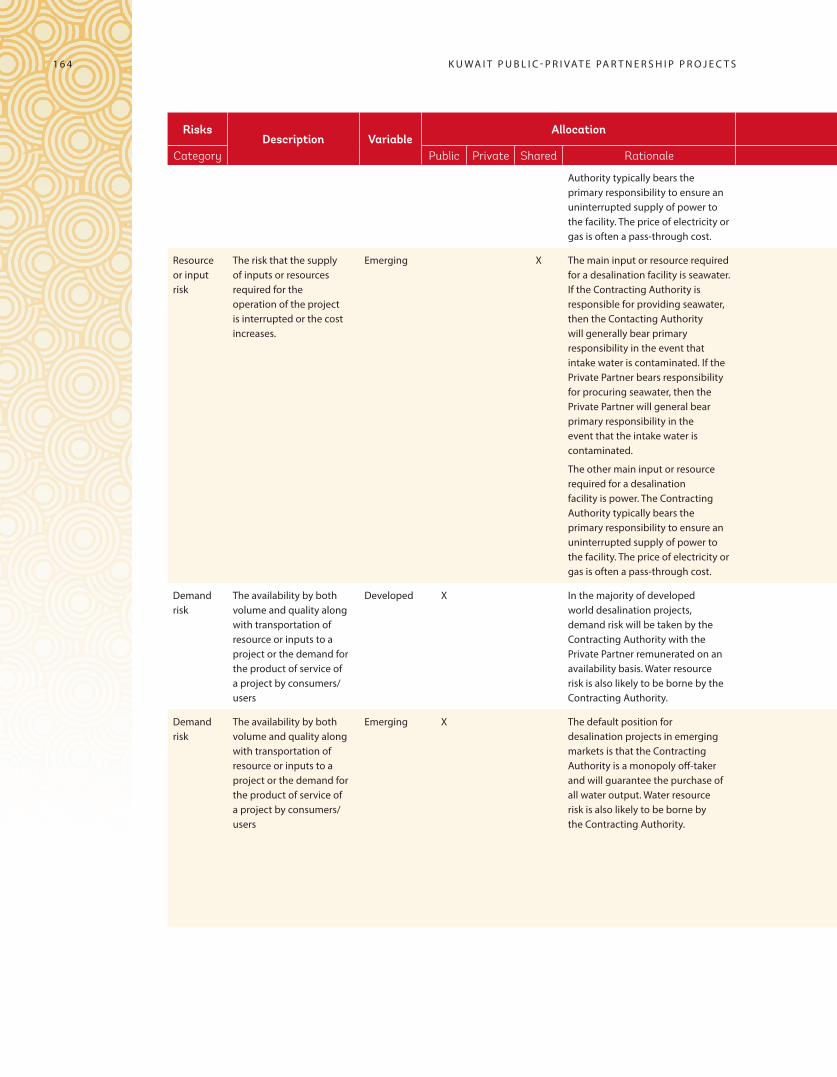

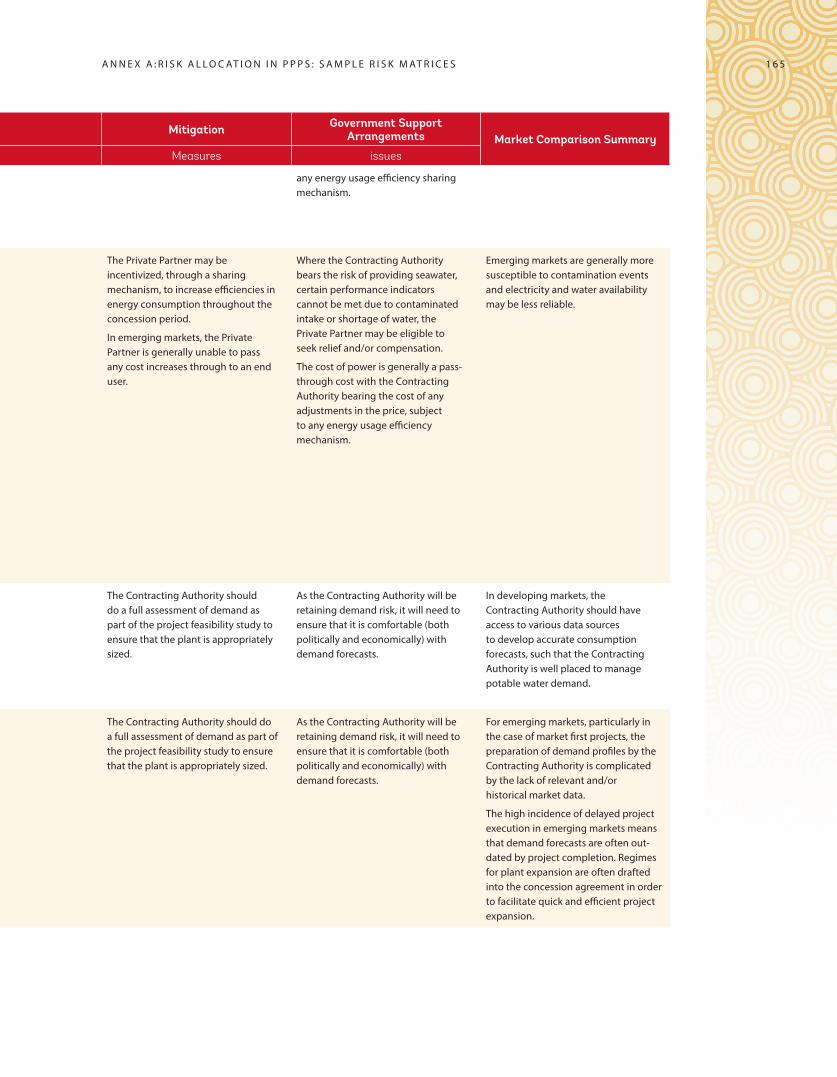

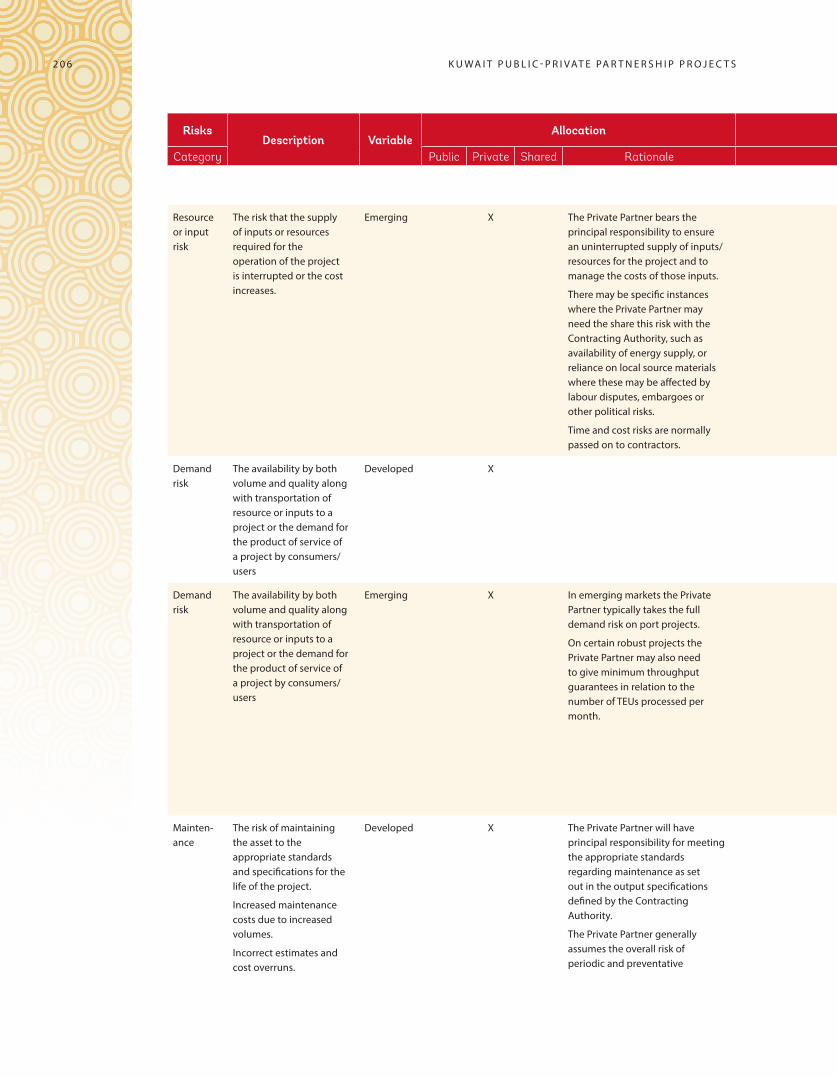

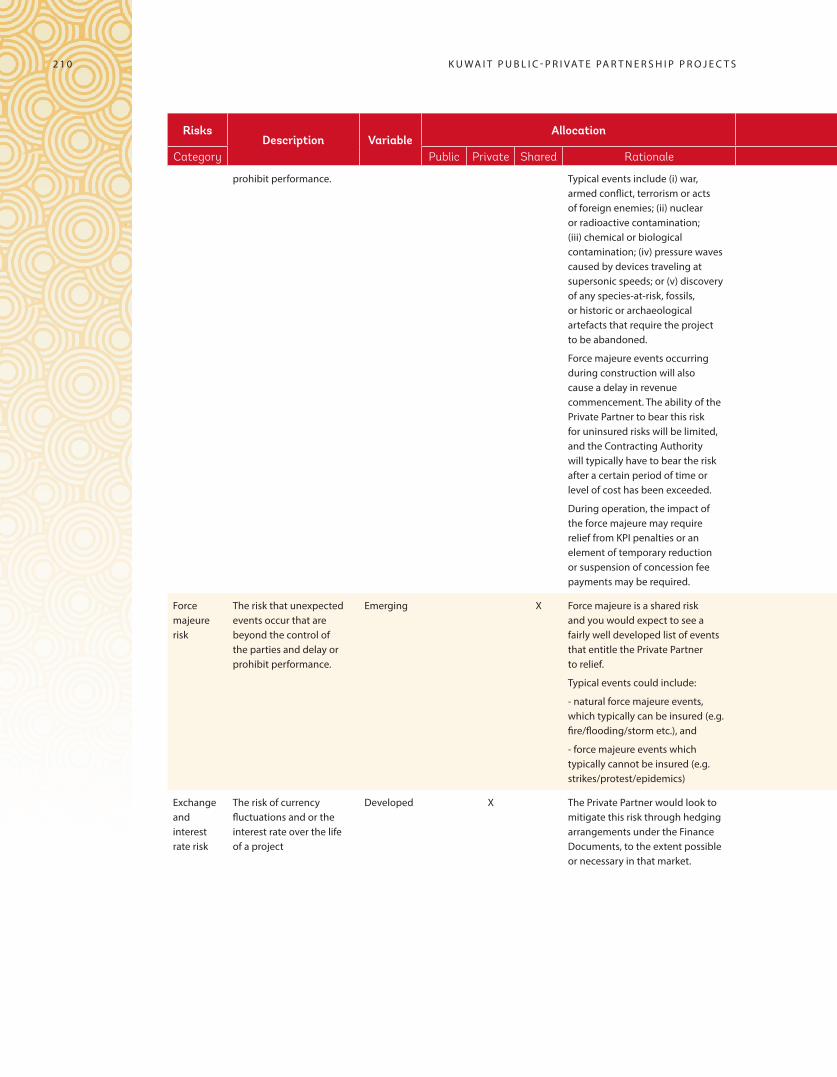

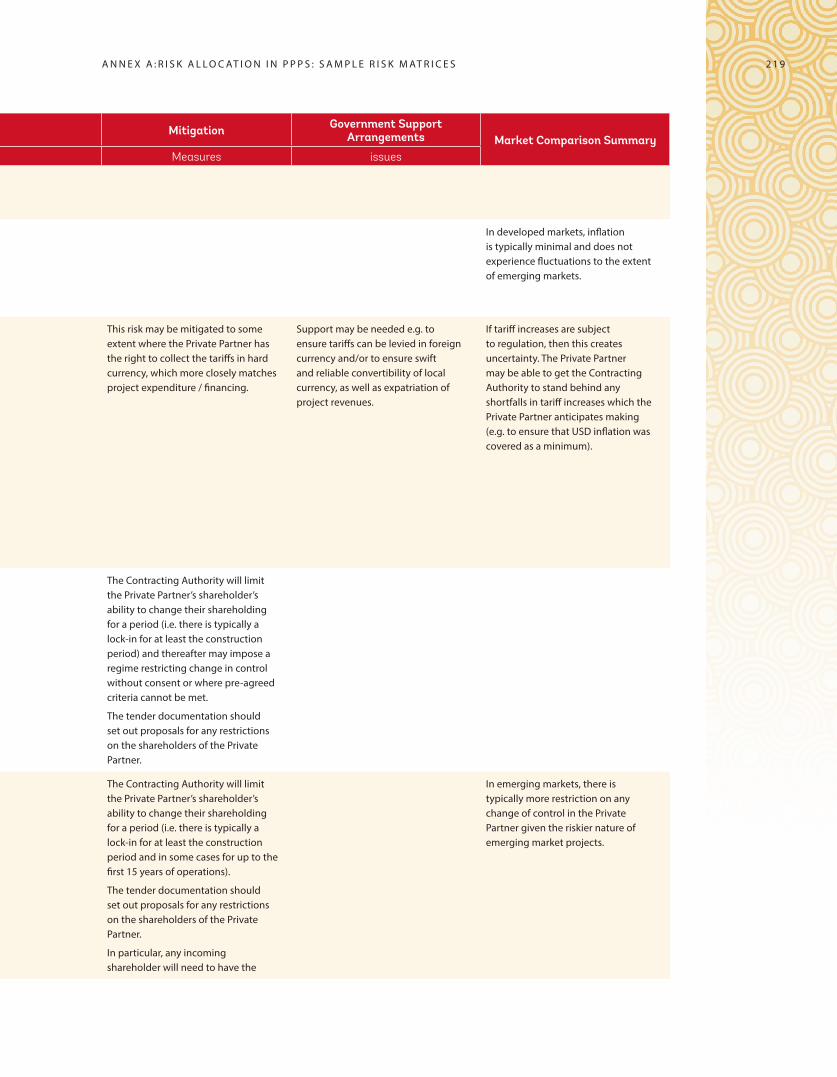

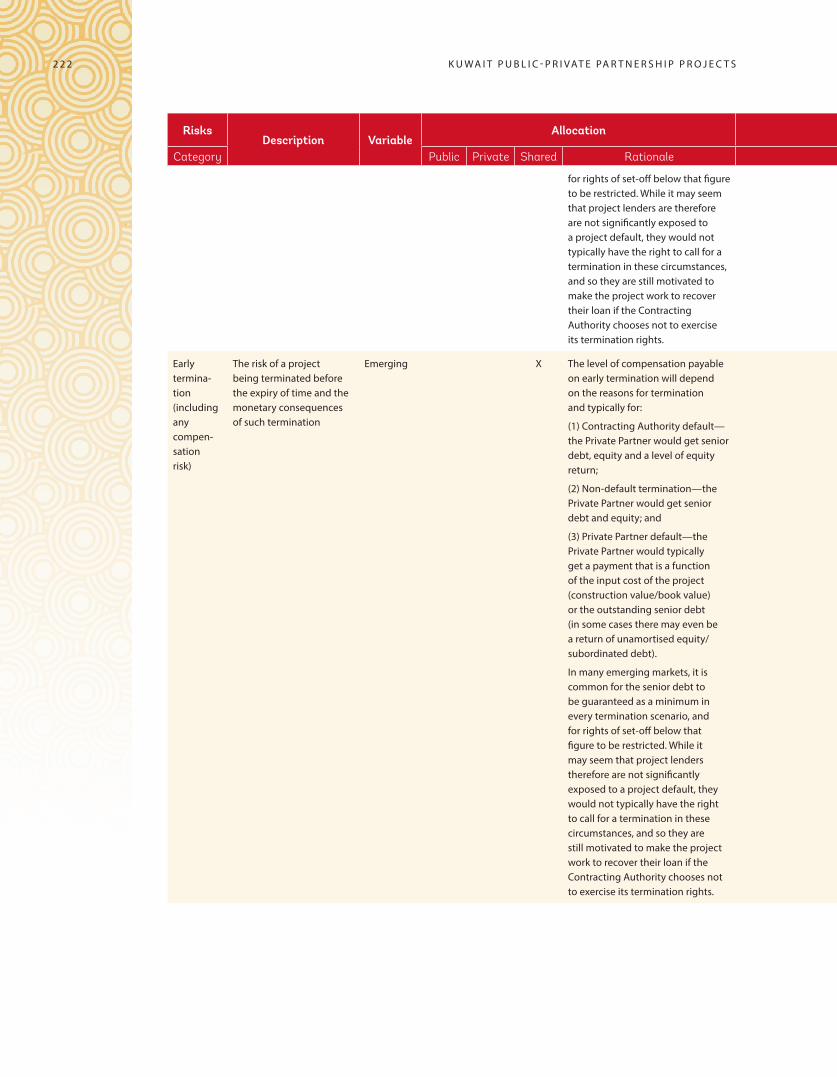

Table A1.1: Risk Matrix for a Water Desalination Project 144

Table A1.2: Risk Matrix for a Container Port Project 190

BOXES

Box B.1: Enforcement of Arbitral Awards 266

v i i i K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

MESSAGE FROM HIS EXCELLENCY THE MINISTER OF FINANCE

Aspiring for creating a comprehensive legislative system and a procedural framework to regulate the process of partnerships between private and public sectors in strategic projects, the State of Kuwait has enacted Law No. 116 of 2014 on Public Private Partnerships, followed by Decree No. 78 of 2015 issuing its Executive Regulations, which called for the preparation of this Guidebook, to define the mechanisms for tendering Public Private Partnership (PPP) projects.

This Guidebook was prepared with the assistance of the World Bank, and benefits from the Institution’s international experience and expertise. It includes general instructions on project tendering in accordance with Law No. 116 of 2014 on Public Private Partnerships and its Executive Regulations, taking into consideration Kuwait’s own legal and economic stance.

The State of Kuwait aims at keeping pace with the international and regional developments in executing strategic projects in a manner consistent with the latest international standards and best practices. This goes in line with developing a safe and attractive investment climate to accomplish the Government’s goals of securing citizens’ needs for sustainable infrastructure and establishing a prosperous society.

H.E. Dr. Nayef Al-Hajraf,Minister of Finance of Kuwait

i xM E S S A G E F R O M T H E D I R E C T O R G E N E R A L O F K U WA I T A U T H O R I T Y F O R PA R T N E R S H I P P R O J E C T S

MESSAGE FROM THE DIRECTOR GENERAL OF KUWAIT

AUTHORITY FOR PARTNERSHIP PROJECTS

Striving to improve the business environment in Kuwait, develop the investment climate and increase direct investments by engaging the private sector and Kuwaiti citizens through owning shares in major infrastructure projects, Law No. 116 of 2014 on Public Private Partnerships created the Kuwait Authority for Partnership Projects (“KAPP”) as a national institution specializing in Public Private Partnership (“PPP”) Projects.

Law No. 116 of 2014 on Public Private Partnerships regulates and defines the mechanism and procedures of tendering PPP projects. The tender process is regulated to achieve the highest levels of transparency, provide equal opportunities to investors, and to ensure that PPP projects are developed under a well-integrated legal and institutional system. This represents a significant development in Kuwait’s legal system and investment framework.

This Guidebook is issued pursuant to Law No. 116 of 2014 on Public Private Partnerships and its Executive Regulations to provide detailed guidance on PPP project tendering, so as to facilitate PPP processes in Kuwait.

His Excellency Mutlaq Al-Sanea,Director General of the Kuwait Authority for Partnership Projects

x K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

ACKNOWLEDGMENTS

This Guidebook was prepared by Kuwait Authority for Partnership Projects (KAPP) in close collaboration with the World Bank. The World Bank team was led by Mark M Moseley, Lead Lawyer in the Infrastructure, PPPs and Guarantees (IPG) Group under the Global Themes Vice Presidency. Mark Giblett (Senior Infrastructure Finance Specialist), Christina Paul (Lawyer) and Deblina Saha (Infrastructure Analyst) were the other members of the IPG Group from the Singapore Urban and Infrastructure Hub who drafted the Guidebook. The team would like to express its sincere appreciation for the guidance and support of Firas Raad (Country Manager, Kuwait Country Office), Maher F. Abu-Taleb (Senior Operations Officer), Maryam Abdullah (Operations Analyst) and Ayah Elhashash (Team Assistant) throughout the preparation of the Guidebook.

The Guidebook benefited from the valuable contributions of the staff of KAPP led by Engineer Nayaf AlHaddad (Manager, Research Strategic Planning, Risk). The team gratefully acknowledges the guidance provided by the KAPP working group as well as Messrs. Ahmad AlShorbagy (Legal Consultant, Al-Hamad) and is thankful for the feedback received from other KAPP officials during the seminar for the dissemination of the Guidebook, which was held in Kuwait in November 2017.

x iA C K N O W L E D G M E N T S

x i i K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

ABBREVIATIONS AND ACRONYMS

Authority Kuwait Authority for Partnership Projects

BOO Build-Operate-Own

BOT Build-Operate-Transfer

Contracting Authority (in annexes)

Public Agency contracting a partnership project. See “Public Entity”

DBO Design-Build-Operate

Distinguished Project Project approved by the Higher Committee and based on an integral feasibility study offered by the proposer that has an economic and social return conform to the State’s strategy and developing plan (also called Privileged Project)

GCC Gulf Cooperation Council

EPC Engineering, Procurement and Construction

ECOD Early Commercial Operation Date

ECWPA Energy Conversion and Water Purchase Agreement

Executive Regulations Kuwait PPP Law Executive Regulations (Decree No. 78 of 2015)

Guidebook Kuwait Public-Private Partnership (PPP) Projects Guidebook

HC The Higher Committee for PPP Projects

HoldCo A corporate entity, formed by the members of the investor consortium, for owning shares in the Project Company

Initiative An innovative Partnership Project for a creative unprecedented idea, in Kuwait, approved by the Higher Committee, per an integral feasibility study offered by the proposer to the Authority, with an economic and social return conform with the State’s strategy and developing plan.

IPP Independent Power Producer

IRR Internal Rate of Return

IWP Independent Water Project

IWPP Independent Water and Power Project

IWPP Law Law 39 of 2010 and its amendments

IWPP Regulations Executive Regulations associated to IWPP Law and its modifications (Decree No. 1 of 2015)

KAPP Kuwait Authority for Partnership Projects

x i i iA B B R E V I AT I O N S A N D A C R O N Y M S

KDIPA Kuwait Direct Investment Promotion Authority

KM Kuwait Municipality

KMRT Kuwait Metropolitan Rapid Transit System

KNRR Kuwait National Rail Road

KWD Kuwaiti Dinar

MIGD Million Imperial Gallons per Day

MEW Kuwait Ministry of Electricity and Water

MPW Kuwait Ministry of Public Works

MW Megawatt

O&M Operations and Maintenance

Old Law Law No. 7 of 2008 regarding the Regulation of Build, Operate and Transfer (BOT) Operations

PCOD Project Commercial Operation Date

PPP Public-Private Partnership

PPP Law Kuwait Public-Private Partnerships Law (Law No. 116 of 2014)

Private Partners (in annexes)

Private investors

Project Company The corporate entity created to implement a PPP project. See “SPV”

Public Entity Public Agency contracting a partnership project. See “Contracting Authority”

PTB Kuwait Partnerships Technical Bureau (the predecessor to KAPP)

SAB State Audit Bureau

SLA Service Level Agreement

Solicited Proposal Proposal for a PPP submitted at the behest of the government

SPV The corporate entity (Special Purpose Vehicle) created to implement a PPP project. See “Project Company”

State (the) State of Kuwait

TA Transaction Advisor(s)

Unsolicited Proposal Proposal made by a private party to undertake a PPP project, submitted at the initiative of the private firm, rather than in response to a request from the government.

WBG World Bank Group

x i v K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

1

CHAPTER

1

PUBLIC-PRIVATE PARTNERSHIPS: AN INTRODUCTION

1.1 WHAT ARE PPPs?

There is no single widely-accepted definition of public-private partnerships (PPPs). The PPP Knowledge Lab1 defines a PPP as “a long-term contract between a private party and a government entity, for providing a public asset or service, in which the private party bears significant risk and management responsibility, and remuneration is linked to performance.”

Kuwait’s PPP Law (Law No 116 of 2014) defines a PPP as being “a project to implement an activity through which the State targets to provide a public service of economic, social or service importance, or to improve an existing public service or to develop, reduce the costs or increase the efficiency of any such service, procured by the Kuwait Authority for Partnership Projects (KAPP) in cooperation with the Public Entity and in accordance with the PPP Model after the approval of the Higher Committee, provided it does not contradict with the provisions of Article 152 and 153 of the Constitution.”

PPPs typically do not include turnkey construction contracts, which are usually categorized as public procurement projects, or a full privatization, where there is typically only a limited ongoing regulatory role for the public sector.

PPPs are very flexible and can be used for both economic infrastructure as well as social infrastructure. Economic infrastructure includes energy projects (e.g. IPPs, IWPPs), transportation projects (e.g. roads, rail, ports, airports, bus rapid transport, etc.), water projects (e.g. desalination plants, bulk water and waste water treatment plants) and waste management projects. Social infrastructure includes schools, universities, hospitals, social housing, sports facilities and government office buildings.

1 The PPP Knowledge Lab is a curated and comprehensive knowledge resource on public-private partnerships: https://pppknowledgelab.org/

2 K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

1.2 WHAT ARE THE BENEFITS OF PPPs?

Facing constraints on public resources and fiscal space, while at the same time recognizing the importance of investment in infrastructure to help their economies grow, many governments are increasingly turning to the private sector as an alternative additional source of financing to help meet the funding gap.

However, aside from the potential fiscal benefits of entering into a PPP (e.g. reducing the upfront costs to the government of providing a service and/or building an asset), governments often look to collaborate with the private sector for other reasons, including:

~ economic diversification and, in the case of Kuwait, reduction in the relative GDP share of the oil sector;

~ exploring PPPs as a way of introducing private sector technology and innovation in providing better public services through improved operational and maintenance efficiency;

~ incentivizing the private sector to deliver projects on time and within budget;

~ imposing budgetary certainty by setting present and the future costs of infrastructure projects over time;

~ utilizing PPPs as a way of developing local private sector capabilities through joint ventures with large international firms, as well as sub-contracting opportunities for local firms in areas such as civil works, electrical works, facilities management, security services, cleaning services, maintenance services thereby creating new job opportunities for citizens;

~ using PPPs as a way of gradually exposing state owned enterprises and government to increasing levels of private sector;

~ supplementing limited public sector capacities to meet the growing demand for infrastructure development; and

~ extracting long-term value-for-money through appropriate risk transfer to the private sector over the life of the project – from design/ construction to operations/ maintenance.

1.3 VALUE FOR MONEY

A PPP project yields value for money (VfM) if it results in a net positive gain to society which is greater than that which could be achieved through an alternative procurement route. It is often considered essential to carry out a VfM analysis during the feasibility stage as part of the initial preparation of any PPP project. However, VfM analysis can be very subjective and heavily driven by underlying assumptions, which themselves can be unreliable, especially at a pre-transaction stage where little or no upfront analysis has been done.

Based on a long and successful track record across various countries and sectors, it has frequently been demonstrated that the PPP procurement option can be more efficient in terms of investment and operating and maintenance

3P U B L I C - P R I VAT E PA R T N E R S H I P S : A N I N T R O D U C T I O N

costs than the public procurement option. Therefore, the key question in assessing value for money is usually whether the greater efficiency of the PPP project is likely to outweigh factors that might make the PPP costlier, the main ones being transaction and contract oversight costs (i.e. additional bidding, contracting and monitoring costs in a PPP setting) and financing and legal costs (i.e. possible added costs due to private sector financing). The value for money assessment should also take into account the potential non-financial benefits of PPPs, such as the accelerated and enhanced delivery of projects, improved quality of service, greater transparency in the procurement process, better focus on due diligence, etc. Experience suggests that the likelihood that a PPP project or a PPP program will provide value for money is higher when all or most of the following conditions are met:

~ there is major investment involved, whether it is local or foreign, which would benefit from the effective management of risks associated with construction and delivery (this may be a single major project or a series of replicable smaller projects in a given sector);

~ the private sector has the expertise to design, implement and operate complex projects;

~ the public sector is able to define its service needs as outputs that can be written into the PPP contract ensuring effective and accountable delivery of services over the long run;

~ risk allocation between the public and private sectors can be clearly identified and implemented;

~ it is possible to estimate, over the whole life of the project, the long-term costs of providing the assets and services involved;

~ the value of the project is sufficiently large to ensure that procurement costs are not disproportionate; and

~ the technological aspects of the project are reasonably tested and proven and not susceptible to obsolescence.

There are numerous analyses and reports developed by (or for) governments and national audit offices as to whether PPPs are, in fact, delivering VfM. The majority of these reports conclude that PPPs do generate VfM. United Kingdom studies indicate that government departments which implemented PPPs, registered cost savings of between 10 and 20 percent. According to the 2002 census of the United Kingdom National Audit Office (NAO), only 22 percent of PFI deals experienced cost overruns and 24 percent experienced delays, compared to 73 percent and 70 percent of projects undertaken by the public sector as reviewed in an NAO survey in 1999. The UK Treasury reported in 2006 that, according to a study for the Scottish Executive by Cambridge Economic Policy Associates (CEPA), 50 percent of authorities administering PPPs reported that they received good value for money, with 28 percent reporting satisfactory value for money. Australia’s National PPP Forum (representing Australia’s Commonwealth, State and Territory governments) commissioned the University of Melbourne in 2008 to compare 25 Australian PPP projects with 42 traditionally-procured projects. The study found that traditionally-procured projects had a median cost overrun of 10.1 percent, whereas PPP projects had a median cost overrun of 0.7 percent. Traditionally-procured projects had a median time overrun of 10.9 percent, whereas PPP projects had a median time overrun of 5.6 percent.

4 K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

1.4 TYPES OF PPP

Public-private partnerships can take a wide range of forms, varying in the extent of involvement of and risk taken by the private party. The terms of a PPP are typically set out in a contract or agreement that outlines the responsibilities of each party and clearly allocates risk. The diagram below depicts the spectrum of PPP agreements:

FIGURE 1.1: Spectrum of PPP Agreements

Utility Restructuring Corporatization Decentralization

Civil Works

Service Contracts

Management andOperatingContracts

Leases/Affermage

Concessions

BOT Projects

DBOs

JointVenture/PartialDivestitureof PublicAssets

FullDivestiture

HighLowExtent of Private Sector Participation

Public-Private Partnership

Public Ownsand

Operates Assets

Private Sector Owns and

Operates Assets

PPPs can range from the public sector entering into a relatively straightforward management and/or operating contract with the private sector, through to a joint venture or partial divestiture of ownership in a public asset.

Examples of the different forms that a PPP may take include:

Management and Operating Contracts

The term “management contract” can apply to a range of contracts from technical assistance contracts through to full-blown operation and maintenance agreements and, as such, it is difficult to generalize about them. However, the main common feature is that the awarding authority engages the contractor to manage a range of activities for a relatively short time period (two to five years). Management contracts tend to be task specific, and more focused on inputs rather than outputs. Operation and maintenance agreements may have more outputs or performance requirements.

The simplest management contracts involve the private operator being paid a fixed fee by the awarding authority for performing specific tasks—the remuneration does not depend on collection of tariffs and the private operator does not typically take on the risk of asset condition. Where the management contracts become more performance-based, they may involve the operator taking on more risk, potentially including the risk of asset condition and replacement of more minor components and equipment.

5P U B L I C - P R I VAT E PA R T N E R S H I P S : A N I N T R O D U C T I O N

Leases/Affermage Contracts

Leases and affermage contracts are generally public-private sector arrangements under which the private operator is responsible for operating and maintaining the existing utility but is not responsible for building and financing any new investments.

Leases and affermages differ from management and operating contracts in that:

~ the operator does not receive a fixed fee for its services from the awarding authority but charges an operator fee to consumers, with

� in the case of a lease: a portion of the receipts going to the awarding authority as owner of the assets as a lease fee and the remainder being retained by the operator

� in the case of an affermage: the operator retaining the operator fee out of the receipts (prix du fermier) and paying an additional surcharge that is charged to customers to the awarding authority to go towards investments that the awarding authority makes/ has made in the infrastructure;

~ the operator tends to bear greater operating risk; and

~ the operator tends to employ the staff directly.

In the case of a lease, the rental payment to the authority tends to be fixed irrespective of the level of tariff collection that is achieved, so the operator takes a risk on bill collection and on the level of receipts being sufficient to cover its operating costs. In the case of an affermage transaction, the operator is assured of its fee (assuming that the receipts are sufficient to cover it) and it is the authority that takes the risk of the rest of the receipts collected from customers covering its investment commitments.

The awarding authority in each case remains responsible for financing and managing investment in the assets – which is supposed to come, at least in part, from the rental payment/surcharge.

Concessions, BOT Projects and DBO

Concessions, Build-Operate-Transfer (BOT) Projects, and Design-Build-Operate (DBO) Projects are types of PPP transactions that are output-focused. BOT and DBO projects typically involve significant design and construction as well as long-term operations, for new build (greenfield) or projects involving significant refurbishment, rehabilitation or extension (brownfield).

A Concession gives a concessionaire the long-term right to use all assets conferred on the concessionaire, including responsibility for operations and some investment. Asset ownership remains with the authority, and the authority is typically responsible for replacement of larger assets. Assets revert to the authority at the end of the concession period, including assets purchased by the concessionaire. In a concession, the concessionaire typically obtains most

P U B L I C - P R I VAT E PA R T N E R S H I P S : A N I N T R O D U C T I O N

6 K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

of its revenues directly from the consumer and so it has a direct relationship with the consumer. A concession covers an entire infrastructure system (so may include the concessionaire taking over existing assets as well as building and operating new assets). The concessionaire will pay a concession fee to the authority which will usually be ringfenced by the authority and put towards asset replacement and expansion.

A Build Operate Transfer (BOT) Project is typically used to develop a discrete asset rather than a whole network and is generally entirely new or greenfield in nature (although refurbishment may be involved). In a BOT Project the project company must build the asset and generally obtains its revenues through a fee charged to the utility/ government rather than tariffs charged to consumers. At the end of an agreed period of time, the asset will be transferred to the government.

In a Design-Build-Operate (DBO) Project, the public sector owns and finances the construction of new assets. The private sector designs, builds and operates the assets to meet certain agreed outputs. The documentation for a DBO is typically simpler than a BOT or Concession, as there are no financing documents. Typically, there will be a turnkey construction contract plus an operating contract, or a section added to the turnkey contract covering operations. The private sector party takes no or minimal financing risk on the capital and will typically be paid a sum for the design-build of the plant, payable in installments on completion of construction milestones, and then an operating fee for the operating period. The private sector party is responsible for the design and the construction as well as operations, and so if parts need to be replaced during the operations period prior to the end of its assumed life span, the private sector party is likely to be responsible for replacement.

1.5 PPP PROCESS

FIGURE 1.2: The PPP Process

Project Initiation

ProjectFeasibility and

Structuring

ProjectProcurement

Project Implementationand Monitoring

7

1.5.1 PROJECT INITIATION

Governments are often faced with competing priorities in terms of infrastructure investments and this fact, combined with fiscal constraints, frequently requires governments to be selective in initiating infrastructure projects. Projects can be initiated by the central government (through the various line ministries) or by local governments2. However, irrespective of which entity has initiated the project, it is important to note that not all projects are suitable for procurement through a PPP. Indeed, before a decision is made to procure a project through a PPP route, it is important to carry out a feasibility study.

Under the Kuwait PPP Law, a concept for a PPP project can be initiated by either a Public Entity, the Higher Committee or as an unsolicited proposal from a private Kuwaiti or non-Kuwaiti person/entity.

1.5.2 PROJECT FEASIBILITY AND STRUCTURING

It only makes sense to procure a project through a PPP framework if it is economically viable. Therefore, most governments subject proposed PPP projects to the same technical, social and economic appraisal as any other public investment decision. There are typically two broad elements to this assessment. The first is assessing the feasibility of the project concept itself (including technical feasibility, legal feasibility and environmental and social sustainability) and the second is appraising whether the project is a good public investment decision based on some form of economic viability analysis, i.e. an assessment as to whether the economic benefits of the project exceed its economic costs and that there is appetite/interest for the project in the market - which will be heavily influenced by whether the project generates sufficient returns for the private sector investors.

In accordance with the PPP Law, a Public Entity that proposes a PPP project must carry out a feasibility study and submit it to KAPP for its review (Article 2 of the Executive Regulations). However, KAPP may, in certain cases, choose to commission a feasibility study in cooperation and coordination with the Public Entity (Article 10 of the Executive Regulations). For an unsolicited proposal, any Kuwaiti or foreign natural or legal person must prepare an initial feasibility study for submission to KAPP. In both cases, the feasibility study must demonstrate, amongst other matters, that the project provides an economic return or social benefit in line with the State’s strategy and development plan.

Structuring a PPP project means allocating responsibilities, rights and risks to each party to the PPP contract. Information from the feasibility and economic viability analysis is a key input to the structuring of a PPP, e.g. identifying the key technical risks and providing estimates of the demand for the proposed infrastructure. It is important that PPP projects are structured in a way that is not only commercially viable from a private sector perspective but is also economically and socially viable and beneficial from the public sector’s perspective, i.e. the project provides value for money to the public sector. Market sounding is often carried out during the feasibility study/structuring phase to find out the views of the various stakeholders and this feedback is used to help strengthen the viability of the project.

2 When the public sector invites the private sector to tender for a PPP project, this is often called a ‘solicited bid.’ However, sometimes, the private sector can propose a PPP project to the government in which case it is called an ‘unsolicited bid.’

P U B L I C - P R I VAT E PA R T N E R S H I P S : A N I N T R O D U C T I O N

8 K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

1.5.3 PROJECT PROCUREMENT

Once the project structure has been finalized (with the support of the Transaction Advisors, i.e. professional advisors such as financial advisors, legal advisors and technical advisors) and approved by the relevant authorities—the project is ready to be procured. The objective of the procurement phase is to select a firm or consortium that provides the most effective and efficient solution to the proposed project’s objectives from both a technical and financial perspective. The best way to achieve these objectives is to carry out a competitive, efficient and transparent procurement process, as this will likely maximize value for money from the government’s perspective.

1.5.4 PROJECT IMPLEMENTATION AND MONITORING

It is important for the Public Entity to establish a project management team as soon as possible in the procurement process to manage the project after financial close. Managing PPP contracts involves monitoring and enforcing the PPP contract requirements as well as managing the relationship between the public and private partners. Contract management spans the whole lifetime of the agreement, from the date of contract effectiveness through to the end of the contract period. Managing PPP contracts differs from managing traditional government contracts. PPPs are long-term and complex and, as such, contracts are necessarily incomplete i.e. the requirements and rules covering all possible scenarios cannot be comprehensively specified upfront in the contracts. Therefore, the aims of contract management for PPPs are to ensure:

~ services are delivered continuously and to a high standard in accordance with the contract, and payments (or penalties) are made accordingly;

~ contractual responsibilities and risk allocations are maintained and the government’s responsibilities and risks managed efficiently; and

~ changes in the external environment (both risks and opportunities) are identified and acted on in an effective and timely manner.

Under Article 33 of the PPP Law, the Minister of Finance is required to submit an annual report to the Council of Ministers (with a copy to the National Assembly) that provides a status update on all PPP projects that have been executed or implemented. This report will cover, amongst other matters, land issues and the degree to which the private sector counterparties are complying with the terms of the PPP agreements together with a summary of any breaches of these agreements. This information will be provided by the relevant ministries that are undertaking the PPP project.

9P U B L I C - P R I VAT E PA R T N E R S H I P S : A N I N T R O D U C T I O N

1.6 FURTHER READINGS

Additional information on the above and PPPs in general can be found from the following sources:

~ PPP Knowledge Lab (https://pppknowledgelab.org/)

~ PPP Infrastructure Resource Centre (http://ppp.worldbank.org/public-private-partnership/)

~ PPP Reference Guide Version 3 (https://ppp.worldbank.org/public-private-partnership/library/ppp-reference-guide-3-0 )

~ The Private Participation in Infrastructure Database (https://ppi.worldbank.org/)

~ The Public Private Infrastructure Advisory Facility (https://ppiaf.org/ )

~ The Global Infrastructure Hub (https://www.gihub.org/ )

~ The APMG Public-Private Partnerships Certification Program (https://ppp-certification.com/ )

~ PPIAF paper on Mobilizing Islamic Finance for Infrastructure Public-Private Partnerships (https://ppiaf.org/documents/5369?ref_site=kl)

~ A Framework for Disclosure in PPPs (http://pubdocs.worldbank.org/en/773541448296707678/Disclosure-in-PPPs-Framework.pdf)

~ World Bank Group paper on Financial Viability Support (https://library.pppknowledgelab.org/documents/2847?ref_site=kl)

1 0 K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

1 1

CHAPTER

2

PPP LEGAL AND INSTITUTIONAL STRUCTURES IN KUWAIT

2.1 INTRODUCTION

The Kuwait PPP Law (Law No. 116 of 2014 regarding Public Private Partnerships) establishes a legislative framework to promote and facilitate PPPs in public infrastructure and services in the State of Kuwait, based on the principles of transparency and competitiveness. A PPP is defined in the PPP Law as “a project to implement an activity through which the State targets to provide a public service of economic, social or service importance, or to improve an existing public service or to develop, reduce the costs or increase the efficiency of any such service, procured by the Authority in cooperation with the Public Entity and in accordance with the PPP Model after the approval of the Higher Committee, provided it does not contradict with the provisions of Articles 152 and 153 of the Constitution.”

2.2 KEY FEATURES OF LAW NO. 116 OF 2014 REGARDING PUBLIC- PRIVATE PARTNERSHIPS

PPPs must follow the “PPP Model” which, in Article (1) of the PPP Law, is defined as “a model whereby a private Investor invests in State-owned real property – if required – in one of the projects procured by the Authority in collaboration with one of the Public Entities after signing an agreement with the Investor to implement or build or develop or operate or rehabilitate a service or an infrastructure project, and to provide financing thereto and operate or manage and develop the project, for a specified term, after which the project shall be transferred to the State; the foregoing shall be carried out in one of two forms: 1) the implementation of the project in consideration for fees – for services or works performed - to be paid to the Investor by the beneficiaries or by the Public Entities who have entered into an agreement with the Investor, and whose objectives are in compliance with the project or by both the beneficiaries and the Public Entities; and 2) the purpose of the project is for the Investor

1 2 K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

to implement a project with strategic importance to the national economy and to exploit it for a specified term. In both cases, the Investor shall pay a fee for the use of any State-owned real property allocated for the project.”

In accordance with this definition, the PPP Model in Kuwait therefore requires the following criteria to be met:

~ a private investor to invest in a project on state-owned property (if required);

~ procurement of the project by KAPP, in collaboration with a Public Entity;

~ the signing of an agreement with the Investor to implement or build or develop or operate or rehabilitate a service or an infrastructure project, to provide financing to this end and to operate or manage and develop the project, for a specific period of time; and

~ following the end of the agreement, the transfer of the infrastructure facilities to the State.

This process may be conducted in one of two forms:

~ the implementation of the project in consideration for fees (for services or works performed) to be paid to the Investor by the beneficiaries or by the Public Entities who have entered into an agreement with the Investor, or

~ the implementation by an Investor of a project of strategic importance to the national economy, whereby the project can be exploited by the Investor for a specified term.

The salient features of the PPP Law include:

~ in general, no public body may enter into a PPP Contract without first obtaining the approval of the Higher Committee for PPPs3;

~ KAPP provides advisory support to the Higher Committee in its decision making;

~ a time limit for PPP Projects of 50 years4 (if a project's bid documents do not contain a certain term, its lifespan will be deemed to be 25 years);

~ restrictions on the sale or mortgage of State Land/public property in PPP Projects, although security over the “private assets” are permitted, which includes revenues of the project and shares in the project company;

~ provisions allowing the State to collect a fee from the project for use of State land;

~ projects exceeding KWD 60 million in value must be carried out by a PPP Project Company which will be a special purpose vehicle formed as a Kuwaiti joint stock company, in which no less than 26% and up to

3 There are a few exceptions to this general rule, such as is the case with the Public Authority for Housing Welfare established under Law No. (47) of 1993, which may tender PPPs within its scope of work.

4 Under the IWPPP Law and the IWPP Regulations the time limit for PPP Projects is capped at 40 years.

1 3P P P L E G A L A N D I N S T I T U T I O N A L S T R U C T U R E S I N K U WA I T

44% shares would be offered to an Investor, with the majority of the remainder of the shares being offered to the Kuwaiti citizens and Public Entities allowed to invest in the project (subject to these shares being held temporarily by KAPP until full operation of the project);

~ provisions allowing for unsolicited proposals of two types: (i) Initiative Projects and (ii) Distinguished Projects;

~ possibility of settlement of disputes through arbitration; and

~ grievance mechanism for violations of the PPP Law and the Executive Regulations.

2.2.1 TRANSITION ARRANGEMENTS

Under Article 7 of the PPP Law, projects existing before the entry into force of the PPP Law shall continue until the expiry of the term in the agreement or until termination. Upon the entry of the PPP Law into force, no amendments, renewals or extensions may be given on such projects, and such projects shall be handed back to the State for re-tendering or for operating and managing the project itself (in accordance with Article 30 of the PPP Law). Further transitional arrangements are in place for projects whose term has expired at the time the PPP Law came into force. These may be granted a one-time extension for a maximum period of one year pursuant to their respective contractual provisions and subject to the approval of the Higher Committee.

2.2.2 KEY ASPECTS OF EXECUTIVE REGULATIONS

The PPP Executive Regulations (Decree No. 78 of 2015) were issued to set out further details on the project flow process, procurement, and implementation of PPPs in Kuwait. These aspects are dealt with in detail in Sections 3 to 6 of this Guidebook.

2.3 KEY DIFFERENCES BETWEEN THE 2008 AND 2014 LEGISLATION

The PPP Law replaces previous Law No. 7 of 2008 regarding the Regulation of Build, Operate and Transfer (BOT) Operations (the Old Law), and the new PPP Law was designed to support the Government of Kuwait’s program to promote collaboration between the public and private sectors to develop infrastructure and to provide services to Kuwaiti citizens and local residents. More specifically, the legal framework under the new PPP Law is aimed at enhancing the procurement process for PPP projects in Kuwait (while incorporating lessons learned from recently closed transactions), clarifying the provisions for their implementation, and bringing it better into line with international standards to attract more private sector investment into Kuwait. The following sections set out the key differences between the two laws.

1 4 K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

2.3.1 ESTABLISHING THE PROJECT COMPANY AND SHAREHOLDING STRUCTURE

The PPP Law clarifies that, for projects that are estimated to be worth less than KWD 60 million in total cost, the successful Investor shall establish a Project Company. For projects with total costs deemed to be above KWD 60 million, KAPP will establish a Joint Stock Company (with an exception for “projects of a special nature” as detailed in Article (16) of the Law). The method of calculating the value of the project is changed in the PPP Law, such that only capital expenditure is considered in the calculation5, which, in theory, should reduce the cost for most projects, allowing more to fall under the KWD 60 million threshold. If a Joint Stock Company must be established, specific share allocations are specified under both laws, though the percentages and entities are different (see Table 2.1, below).

TABLE 2.1: Comparison of Joint Stock Company Share Allocation Arrangements under the PPP Law and the Old Law

Share Allocation under the Old Law (%)

Share Allocation under the PPP Law (%)

Project Sponsors (i.e. the successful bidders)

10% [Art. 5(b)] 26%–44% [Art. 13(2)]

Kuwaiti Citizens, acquiring shares through a transfer offered to them

50% [Art. 5(c)] 50% [Art. 13(3)]

Joint stock companies listed on the Kuwait Stock Market

40% [Art. 5(a)] —

Kuwaiti Public Entities (i.e. Government entities)

May be allocated up to 20%, equally deducted from Kuwaitis and joint stock companies listed on the Kuwait Stock

Market

[Art. 5]

6%–24% [Art. 13(1)]

Also, any shares that are not subscribed after the transfer of shares can then be offered to the Public Entities or to the private consortium, rather than being auctioned, as was the case previously, which introduced uncertainty into the shareholding structure (Article 15 of the PPP Law).

2.3.2 CHANGES IN PROJECT DOCUMENTATION

The Old Law prohibited changes to contracts or authorizations, even in the event of a ‘material adverse government action,’ such as change in law. The PPP Law now permits negotiations of contracts as far as the project’s technical and financial aspects are concerned during the tendering and bid evaluation stage (except for those aspects that are deemed non-negotiable) (Article 17 of the PPP Law), as well as amendments to the contracts after signature (Article 36 of the PPP Law).

5 Compare the definition of a project’s “Total Cost” in Article 1 No. 20 of the PPP Law and Article 11 of the Executive Regulations. For commentary on how this is calculated, please see Section 4.2.2.4.

1 5P P P L E G A L A N D I N S T I T U T I O N A L S T R U C T U R E S I N K U WA I T

2.3.3 OWNERSHIP AND SECURITY OVER ASSETS

Under the Old Law, security over project assets and land was not permitted. Under the PPP Law, permitted security now includes:

~ security over project assets owned by the private party;

~ a pledge over accounts (revenues in the project); and

~ shares in both the Project Company and the consortium company, even during the initial lock-in period.

The PPP Law states that the split of public/private ownership of assets will be set out in the PPP Agreement (Article 18). Under the Old Law, all project assets were to be considered as “state property,” that is, they could not be secured, and had to be transferred back to the state at the end of the term without compensation. Under the new PPP Law, certain project assets are now categorized as “private assets,” that is, they are allowed to be mortgaged and, to the extent any of these assets are transferred to the Government of Kuwait, compensation is payable. Also, the new PPP Law does not stipulate any additional criteria for foreign companies to observe other than those applicable to all proponents participating in a tender process.

2.3.4 PROCUREMENT PROCESSES

The PPP Law articulates some basic principles on the procurement process for PPPs, including the principle that the selection of investors should be transparent, open, competitive, and equal, in conformity with international best practice (Article 8 of the PPP Law).

Unsolicited proposals, or proposals originating from the private sector, require special consideration. The Executive Regulations provide that all projects that are initiated by unsolicited proposals must be competitively tendered, but different rules apply for the two different types of unsolicited proposals:

~ “Initiatives,” which are defined as “an innovative Partnership Project for a creative unprecedented idea, in Kuwait, approved by the Higher Committee, according to an initial feasibility study offered by the proposer to the Authority, with an economic and social return conform[ing] with the State’s strategy and develop[ment] plan;” and

~ “Distinguished Projects” which are defined as “a Partnership Project approved by the Higher Committee based on an initial feasibility study offered by the proposer to the Authority, with an economic and social return conform[ing] with the State’s strategy and develop[ment] plan.”

For Initiatives, the proposer will still receive the same benefits that were provided under the Old Law:

~ reimbursement of the costs of the feasibility study, plus a bonus of 20% of those costs (to a maximum of KWD 200,000) and;

1 6 K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

~ during the tender, an advantage of 5% of the best bid value or a share of the stocks in the Joint Stock Company, if applicable, not to exceed 10% of the shares’ nominal value.

On the other hand, for Distinguished Projects, the proposer simply gets reimbursed for the costs of the feasibility study, plus a bonus of 10% of those costs (to a maximum of KWD 100,000). In this regard, KAPP may develop procedural guidelines for dealing with these reimbursements.

In all cases, these fees should be indicated in the Request for Proposals (RFP) that is prepared for the competitive tendering process, on the basis that these fees will paid by the successful bidder via the project company upon financial close. (Article 58 of the Executive Regulations).

2.3.5 TERM

The term of PPP Agreements has been extended to a maximum of 50 years, from 30 years under the Old Law (40 years with Cabinet approval), with a default of 25 years if no term is specified in the bid documents, allowing more flexibility for structuring PPPs (Article 18 of the PPP Law).

2.3.6 LAND

Leases on state-owned land under the PPP Law will be back-to back with the PPP Agreement, that is, the term of the lease will be set forth in the tendering documents and will be the same length as the term of the PPP (Article 18 of the PPP Law). The PPP Law specifically annuls a provision in the State Property Law that limited the length of leases on State-owned land. Aside from that, in case of termination of a PPP Agreement, the land lease is automatically terminated.

2.4 INTERFACE WITH OTHER LEGISLATION

The PPP Law must be considered alongside the entire legal framework in Kuwait. These laws include, but are not limited to, land laws, companies law, investment laws, environmental and social regulations.. Before embarking on any PPP project in Kuwait, local legal counsel should be sought to understand how these laws might impact the project.

One law has a particularly important role to play in PPPs: Law No. 39 of 2010 on the Incorporation of Kuwaiti Joint Stock Companies to Undertake the Building and Execution of Electricity Power and Water Desalination Stations in Kuwait (the IWPP Law), and the associated IWPP Executive Regulations.

Essentially, the IWPP Law outlines specific requirements concerning the construction and implementation of electric power and water desalination plant projects in Kuwait as part of a PPP arrangement.

1 7P P P L E G A L A N D I N S T I T U T I O N A L S T R U C T U R E S I N K U WA I T

The IWPP Law governs those projects which fall under its mandate, including projects which are purely power projects without any water desalination component. In case of conflicts between the IWPP Law and the PPP Law, the former will prevail. However, where the IWPP Law is silent on matters that, in turn, are covered in the PPP Law, the provisions of the latter apply to such projects.

2.5 INSTITUTIONAL STRUCTURE FOR PPPs

The institutional structure for the implementation of PPP Projects, as presented in the PPP Law and the Executive Regulations, consists of the following institutions:

2.5.1 THE HIGHER COMMITTEE (HC)

The Higher Committee has the powers and authorities of acting as KAPP’s board of directors. It is chaired by the Minister of Finance and consists of:

~ the Minister of Municipalities;

~ the Minister of Public Works;

~ the Minister of Trade and Industry;

~ the Minister of Electricity and Water;

~ the Director General of the Kuwait Environment Public Authority;

~ the Director General of KAPP;

~ three experienced specialists to be named by the Council of Ministers from civil servants; and

~ a representative of the Public Entity responsible for the project under consideration, who shall be invited to the concerned meeting but will not have a right to vote.

The responsibilities of the Higher Committee include:

~ setting the general policies for projects and initiatives of strategic importance to the national economy, identifying priorities and approving detailed documentation related thereto;

1 8 K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

~ approving the requests of the Public Entities for the procurement of PPP Projects;

~ proposing PPP projects to Public Entities;

~ approving KAPP’s proposed budget and final accounts;

~ approving the financial and administrative statutes as well as KAPP’s employees’ regulations and its organization structure;

~ identifying the relevant Public Entity which will participate in the procurement of a project with KAPP and which will countersign the PPP Agreement and be responsible for its implementation and monitoring;

~ approving requests for allocation of land necessary for the implementation of PPP Projects, in coordination with the competent authorities;

~ approving the studies and concepts of PPP Projects and approving the procurement thereof;

~ approving the successful investor for a project, on the recommendation of KAPP;

~ approving PPP Agreements to be executed by Public Entities;

~ deciding upon the requests of Public Entities for contract cancellation/termination (including for public interest); and

~ examining the semi-annual report of PPP Projects.

Article 2 of the PPP Law states that the decisions of the Higher Committee will only have effect after they have been approved by the Minister of Finance.

2.5.2 THE KUWAIT AUTHORITY FOR PARTNERSHIP PROJECTS (KAPP)

The PPP Law creates a new PPP governing authority, the Kuwait Authority for Partnership Projects (KAPP), which replaced its predecessor, the Partnerships Technical Bureau (PTB). KAPP is overseen by a governing board (i.e. the Higher Committee) and will be staffed by a Director General appointed by the Council of Ministers (upon nomination from the Minister of Finance).

KAPP has a budget provided directly from the State Budget rather than from the Ministry of Finance.6 It is primarily responsible for preparing PPPs, as well as advising the Higher Committee. It also ensures standardization and consistency in PPP projects in Kuwait through its responsibilities of setting out procedures and creating templates.

6 Though KAPP’s budget is supplemented by the budget of the Ministry of Finance, KAPP’s resources are generated from funds allocated to it from the State Budget as well as from fees offered for the services it renders.

1 9P P P L E G A L A N D I N S T I T U T I O N A L S T R U C T U R E S I N K U WA I T

Specifically, KAPP is responsible for (Article 6 of the PPP Law):

~ conducting surveys and preliminary studies to identify projects and referring them to the Higher Committee;

~ reviewing and studying projects and Initiatives prepared by the Public Entities or a concept proposer and submitting appropriate recommendations regarding the same to the Higher Committee;

~ assessing feasibility studies, preparing and completing the studies as needed, and submitting recommendations on projects to the Higher Committee;

~ preparing a Guidebook for PPP projects;

~ setting a mechanism for submission of Initiatives, as well as their methods of evaluation and procurement;

~ setting out approaches to evaluating the performance of approved PPP projects over the entire contract period;

~ developing contract templates;

~ preparing drafts of PPP Agreements and Terms of Reference;

~ submitting recommendations to the Higher Committee for approval of the selection of a successful investor;

~ incorporating public joint stock companies for PPP implementation, and determining the capital of such companies;

~ developing PPP Project programs and following-up on their completion, and issuing necessary decisions in relation thereto;

~ compiling and submitting a semi-annual report on PPP Projects to the Higher Committee for approval, prior to the Ministry of Finance presenting the same to the Council of Ministers;

~ following-up on PPP project implementation and addressing any associated obstacles in collaboration with the contracting Public Entity; and

~ proposing the exemption of projects from taxes and custom duties, and raising such recommendations with the Higher Committee.

2.5.3 PUBLIC ENTITIES

Public Entities include any government, Ministry or Department, or any public entity with an independent budget that enters into a PPP Agreement to implement a PPP Project. Their responsibilities include:

2 0 K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

~ proposing projects to KAPP (with feasibility studies) for their review and recommendation to the Higher Committee;

~ participating in project procurement with KAPP;

~ executing, implementing and monitoring PPP Agreements after approval by the Higher Committee;

~ recommending, where appropriate, contract cancellation/termination for the public interest;

~ collaborating with KAPP on project and contract management issues; and

~ providing all necessary means and support towards the project, including but not limited to land allocation, required budget for payments under PPP arrangements, required infrastructure, data and information, preparation of terms and conditions as well as technical advice.

Given that Public Entities have critical responsibilities in the procurement and management of PPP projects, it is important for the relevant Public Entity to be actively engaged from the beginning of the project initiation, through tendering and contract negotiation.

Under Article 3 of the Executive Regulations, for every project which is approved after the initial screening, KAPP is to set up a Competition Committee to represent the Public Entity and other relevant entities where needed, which will be responsible for reviewing or developing the project’s studies, documents, tender and approval documents. The Competition Committee will also participate in the procurement, review the technical and financial proposals, and supervise the public session scheduled for opening the financial tenders.

2.5.4 THE DEPARTMENT OF LEGAL ADVICE AND LEGISLATION

The Department of Legal Advice and Legislation (Fatwa and Tashrea) is crucial to the preparation of PPP contracts in Kuwait. While Fatwa and Tashrea does not have a formal role under the PPP Law, it must provide legal advice on all government contracts and it is responsible for interpreting the laws and defending the State’s interest and safeguarding it. Therefore, Fatwa and Tashrea will be consulted during the process of developing the documentation related to PPP projects, i.e. the RFP and PPP contracts, and negotiation of the same with the preferred bidder.

2.5.5 THE STATE AUDIT BUREAU

The State Audit Bureau plays an essential role in completing the procurement process for a PPP Project. In accordance with Article 44 of the Executive Regulations, its approval is required before a project can ultimately be awarded to the preferred bidder. Accordingly, all relevant documentation (i.e. the RFP, the preferred bidder’s proposal, minutes of the negotiations as well as the PPP contract that has been agreed between the parties) needs to

2 1P P P L E G A L A N D I N S T I T U T I O N A L S T R U C T U R E S I N K U WA I T

be submitted to it for its review. In addition, Article 31 of the PPP Law stipulates that all PPP contracts (including related consultancy agreements) are subject to the ex-ante and ex-post auditing by the State Audit Bureau.

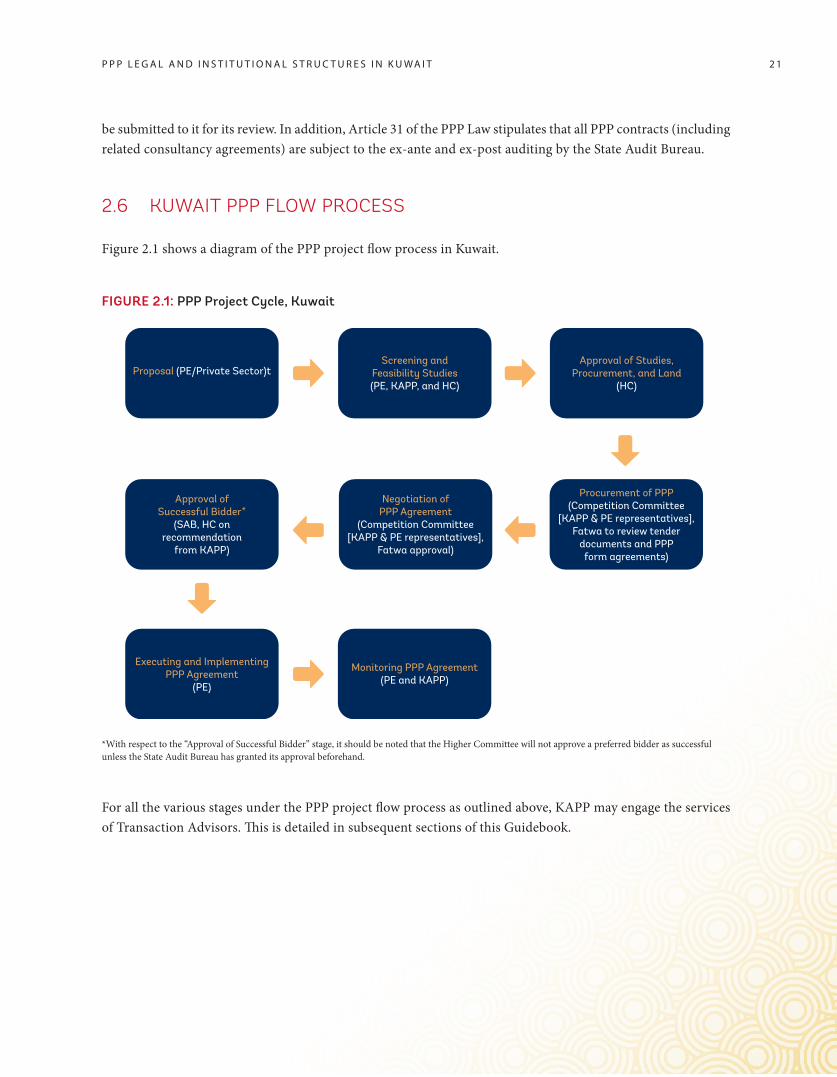

2.6 KUWAIT PPP FLOW PROCESS

Figure 2.1 shows a diagram of the PPP project flow process in Kuwait.

For all the various stages under the PPP project flow process as outlined above, KAPP may engage the services of Transaction Advisors. This is detailed in subsequent sections of this Guidebook.

FIGURE 2.1: PPP Project Cycle, Kuwait

Proposal (PE/Private Sector)tScreening and

Feasibility Studies (PE, KAPP, and HC)

Approval of Studies,Procurement, and Land

(HC)

Procurement of PPP(Competition Committee

[KAPP & PE representatives], Fatwa to review tender

documents and PPP form agreements)

Negotiation of PPP Agreement

(Competition Committee [KAPP & PE representatives],

Fatwa approval)

Approval of Successful Bidder*

(SAB, HC on recommendation

from KAPP)

Executing and Implementing PPP Agreement

(PE)

Monitoring PPP Agreement(PE and KAPP)

*With respect to the “Approval of Successful Bidder” stage, it should be noted that the Higher Committee will not approve a preferred bidder as successful unless the State Audit Bureau has granted its approval beforehand.

2 2 K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

2 3

CHAPTER

3

PROJECT INITIATION

3.1 THE LEGAL FRAMEWORK FOR PROJECT INITIATION

The relevant article of the PPP Law related to the initiation phase of PPP Projects is as follows:

Article 6—THE AUTHORITY AND ITS COMPETENCES

The Authority (KAPP) shall collaborate and cooperate with the Public Entities …. and shall carry out the following: 1. Conduct surveys and preliminary studies to identify projects that may be procured under this Law and submit reports regarding the same to the Higher Committee. 2. Review and study projects and Initiatives prepared by the Public Entities or Concept proposer and submit appropriate recommendations regarding the same to the Higher Committee. 3. Assess the comprehensive feasibility studies of PPP Projects and proposed Concepts, prepare and complete these studies as needed, submit appropriate recommendations in relation to the same to the Higher Committee in preparation for the procurement of the project….

The relevant article of the Executive Regulation in regard to project initiation is:

Article 2—PROPOSING A PPP PROJECT

The proposal for the procurement and implementation of a PPP Project may be submitted by the following entities:

1 | Public Entities: a Public Entity wishing to propose a project that falls within its competences in accordance with the PPP Law shall submit a request to the Authority along with the comprehensive feasibility studies of the project in accordance with the Law, its Executive Regulations and the Guidebook.

2 | The Higher Committee: the Higher Committee approves the request of the relevant Public Entity for the procurement of a PPP Project in accordance with a PPP Model, and it may propose PPP Projects to Public Entities.

2 4 K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

3 | The private sector: the private sector may submit before the Authority draft Concepts along with preliminary feasibility studies, as per the Authority’s requirements, for the implementation of a project and the approval of the procurement thereof in accordance with the provisions of the Law.

The Authority shall in coordination with the Public Entity review the feasibility studies presented by the aforementioned entities and finalize the same, as needed, in order to submit an appropriate recommendation thereon to the Higher Committee.

The Authority may prepare the project’s comprehensive feasibility studies and procurement documents, and it may in all cases seek support from advisory firms and specialized offices whether local or foreign as it deems suitable for this purpose in accordance with the provisions of the laws and regulations.

This part of the Guidebook provides guidance on project initiation issues for the implementation of the above-mentioned provisions.

3.2 SOLICITED PROJECT PROPOSALS

3.2.1 THE ROLE OF THE PUBLIC ENTITY AT INITIATION

A Public Entity that is interested in proposing a project within its area of jurisdictional competence shall submit a request to KAPP, along with a comprehensive Feasibility Study for the Project (Article 2 of the Executive Regulations). The process of submission, and the required set of documents, are set out on KAPP’s website.

However, notwithstanding the foregoing, KAPP may choose to develop a Feasibility Study in cooperation and coordination with the Public Entity. KAPP may also refer to anyone it deems convenient for this purpose, whether from local or foreign consultant offices or other Public Entities, depending on the Project’s nature and needs (Article 10 of the Executive Regulations).

At the time of submitting a proposed project to KAPP, the Public Entity should nominate a Project Manager, to act as the Public Entity’s focal point for interaction with KAPP. The Project Manager is the Public Entity’s anchor and champion for the proposed PPP Project, and should be given suitable delegations by the Public Entity for this central, driving role. It is recommended that the Project Manager also be appointed as the Head of the Competition Committee. The Project Manager should, therefore, be a member of the Public Entity’s senior management throughout the assignment, to ensure the Public Entity’s buy-in for key project decisions. The Project Manager should be appropriately resourced with administrative authority, support and a suitable operating budget. The Project Manager should have the delegated authority within the Public Entity to coordinate the implementation of the project and, specifically, to manage, along with KAPP, the Transaction Advisor. The Project Manager/Head of the Competition Committee shall appear before and answer to the Higher Committee for all matters related to the project.

2 5P R O J E C T I N I T I AT I O N

3.2.2 THE ROLE OF KAPP AT INITIATION

KAPP shall collaborate and cooperate with the Public Entities for the implementation of PPP projects in compliance with the provisions of the PPP Law, and shall carry out the following activities:

~ conduct surveys and preliminary studies to identify projects that may be procured under the PPP Law and submit reports regarding the same to the Higher Committee;

~ review and study projects and Initiatives prepared by the Public Entities or concept proposer and submit appropriate recommendations regarding the same to the Higher Committee; and

~ assess the comprehensive feasibility studies of PPP Projects and proposed concepts or pre-feasibility studies submitted by the Public Entity, prepare and complete these studies whenever KAPP deems it necessary, and submit appropriate recommendations in relation to the same to the Higher Committee in preparation for the procurement of the project.

3.2.3. ESTABLISHING THE COMPETITION COMMITTEE

After the approval of the Higher Committee and as required, the KAPP shall constitute for each project a committee known as the Competition Committee, to represent the Public Party(ies) associated with the project, having at least one member with a level of seniority exceeding that of an auxiliary agent, and with the required technical, financial, and legal expertise. The Competition Committee shall be responsible for examining, integrating, or developing the project studies and its tender and contractual documents. The Competition Committee shall also be responsible for evaluating the technical and financial offers, and supervising the public session scheduled for opening the financial tenders of the technically approved bids for the project.

In addition to dealing with the procurement of the investor for a project, the Competition Committee also has a key role to play in the selection of the Transaction Advisor, except in those situations where KAPP appoints a Transaction Advisor directly, pursuant to the exemption process permitted under the Law on Public Tenders (Law 49 of 2016).

3.2.4 THE ROLE OF THE TRANSACTION ADVISOR

The Transaction Advisor is typically a team of professional consultants, from one or more firms, who work collectively under a single contract with the Public Entity through a lead advisory firm or a consortium of advisory firms. The Transaction Advisor shall be appointed by the Public Entity or KAPP in accordance with Law on Public Tenders (Law No. 49 of 2016), through a competitive bidding process, and should be managed on a day-today basis by the Project Manager who is the contact point between the Transaction Advisor and all relevant parties to the Project. The Transaction Advisor will conduct all the detailed financial, technical, environmental and legal due diligence associated with the project, starting from the feasibility studies and leading to the successful signing of the PPP Contract and Financial Closure by the Project Company. The professional skills and experience of the

2 6 K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

team are typically in: a) project finance transactions, financial assessment for similar projects and financial closing for PPP Projects, b) developing contractual frameworks/security packages for similar projects and PPP projects, c) administrative and local laws, insurance policies, d) PPP procurement management, project management, and e) all technical disciplines relevant to the particular project sector. An effective Transaction Advisor brings clear advantages to the project procurement process through:

~ experience from similar transactions (national and international);

~ demonstrated track record in closing PPP projects on time;

~ avoidance of mistakes which could have significant costs associated with them;

~ access to national and international best practice;

~ enhancement of local and foreign Investor interest and confidence;

~ an opportunity for skills development and capacity building among relevant parties; and

~ assuming the role of being a single point of accountability for delivering high quality results on time.

The agreement between the Public Entity/KAPP and the Transaction Advisor may include two distinct phases:

Phase I: The task in Phase I is to conduct/complete/review and/or amend a Feasibility Study as per the PPP Law and the Executive Regulations to a standard that will enable the Competition Committee to seek Higher Committee approval (or to review and comment on an Unsolicited Proposal’s Feasibility Study for Higher Committee consideration). If the Higher Committee approves a PPP project, the relevant Competition Committee may assign the Transaction Advisor to continue with Phase II.

Phase II: The task in Phase II is to prepare for and implement the PPP procurement process, including preparing all necessary documentation to enable the Competition Committee to obtain Higher Committee approvals in terms of the PPP Law and the Executive Regulations, and proceed with the project procurement.

3.2.5 THE PROCESS FOR RECRUITING THE TRANSACTION ADVISOR

The process for recruitment of the Transaction Advisor will be governed by the provisions of Law on Public Tenders (Law No. 49 of 2016), which is applicable for regulating the procurement of items, contracting and services operations, by public authorities.

2 7P R O J E C T I N I T I AT I O N

The Central Agency for Public Tenders

The Central Agency for Public Tenders is a public authority attached to the Council of Ministers, and is responsible for performing the following tasks in coordination with the Public Entity:

~ offer public tenders (and similar methods of contract);

~ receive and evaluate bids;

~ award and cancel contracts; and

~ extend or renew administrative contracts, as well as variation orders.

Procurement Committee in the Public Entity

The head of the relevant Public Entity forms the Procurement Committee, consisting of at least five members, to be selected from among the staff of the Public Entity, with appropriate qualifications and experience in accordance with what is determined by the procurement systems department of Ministry of Finance. This Procurement Committee is responsible for all procurements undertaken by the relevant Public Entity and as described in the Law on Public Tenders (Law No. 49 of 2016), including the procurement for Transaction Advisors.

The process for hiring a Transaction Advisor starts with the preparation of a Transaction Advisor Bid Package by the Competition Committee in conjunction with the Procurement Committee of the Public Entity. Different components of the bid package are discussed below, in the order in which they should be prepared. Once prepared, the entire Bid Package must be endorsed by KAPP and the Central Agency for Public Tenders in accordance with its internal procurement system, prior to issue, as elaborated below.

3.2.5.1 Drafting the Terms of Reference for Transaction Advisors

The purpose of the Terms of Reference is to give the bidding Transaction Advisor clear direction on what the Procurement Committee and the Competition Committee seek and expect. It is important to consider that the quality of the technical solutions, pricing and other terms of the bid package will depend on the quality of inputs or information made available to the prospective transaction advisors by KAPP and the Public Entity. The Terms of Reference need to be customized, based on the needs of the particular project. However, some of the key sections which Terms of Reference should contain are listed below, along with their descriptions.

2 8 K U WA I T P U B L I C - P R I VAT E PA R T N E R S H I P P R O J E C T S

Background: This section should introduce the project as comprehensively as possible and outline:

~ the State’s needs (such as power generation, treated water, and so on) that has led to the project;

~ the legal and policy framework within which the project is being proposed; and

~ all non-confidential preliminary work done to date by the Public Entity and/or KAPP.

Scope of Work: This is one of the most important sections in the Terms of Reference, as this lays out the extent and type of work for which the Transaction Advisor is being hired. It is important that clear, unambiguous details on each type of action by the Transaction Advisor as envisaged by the Public Entity and/or KAPP be included in this section.

Time-Bound Deliverables: In this section, KAPP, in conjunction with the Public Entity, must specify precisely the timelines for delivery, i.e. what the Transaction Advisor must deliver at each stage of the PPP project timeline.