fin ©2006 m. p. narayanan valuation methods an overview for details, see “finance for strategic...

Post on 21-Dec-2015

214 views

TRANSCRIPT

©2006 M. P. Narayanan

FIN Valuation methodsValuation methods

An overviewFor details, see “Finance for Strategic Decision Making,”

by M. P. Narayanan & Vikram Nanda,

Published by Jossey-Bass

©2006 M. P. Narayanan

2

FIN MethodologiesMethodologies

Comparable multiples P/E multiple Market to Book multiple Price to Revenue multiple Enterprise value to EBITDA multiple

Discounted Cash Flow (DCF) NPV, IRR, or EVA based methods

WACC method CF to Equity method

©2006 M. P. Narayanan

3

FIN Understanding ValueUnderstanding Value

In the context of valuing companies, it is important to understand what we mean by value.

From an economic perspective, value is the present value of future free cash flows (FCF) expected to be produced by the company, discounted at the weighted average cost of capital (WACC) that reflects the risk of the cash flows. For a definition of free cash flow, see cash flow template later For an understanding of the WACC, see conceptual diagram

later

©2006 M. P. Narayanan

4

FIN Understanding ValueUnderstanding Value

This value, is often called the “Economic Value” or “Market Value” of the company.

Let us first clearly understand the differences between Economic value of the company Accounting or book value of the company

©2006 M. P. Narayanan

5

FIN Understanding Value: Book ValueUnderstanding Value: Book Value

Consider a company whose balance sheet is shown on the next page.

The important points to note are: Fixed assets represent the investment in property, plant and

equipment, minus the depreciation Cash is cash on hand Accounts receivable is the amount due from customers. It is

an interest free loan to customers. Accounts payable is the amount owed to suppliers. It is an

interest free loan from suppliers. Accrued expenses are amounts owed to employees,

government, etc. It is also an interest free loan. Financial investments include holdings in other companies.

©2006 M. P. Narayanan

6

FIN Understanding Value: Book ValueUnderstanding Value: Book Value

Accounting Balance Sheet

Fixed assets $1500 Current liabilities

Current assets Short-term debt $150

Cash $200 Payable $320

Marketable securities

& financial investments $150 Accrued expenses $80

Inventory $350 Noncurrent liabilities

Receivable $400 Long-term debt $1000

Equity $1050

$2600 $2600

©2006 M. P. Narayanan

7

FIN Understanding Value: Book ValueUnderstanding Value: Book Value

Finally the Shareholder funds in an accounting balance sheet (called the book value of equity) is the amount of equity capital invested in the company. This includes The original equity capital invested when the company was

started. Additional equity invested in the company through

subsequent external equity financings minus any equity repurchases.

Profits reinvested in the company. It is important to understand that the value of equity in

the accounting balance sheet is NOT what the shareholders can obtain if they sold the company and paid off all the debt.

©2006 M. P. Narayanan

8

FIN Understanding Value: Book ValueUnderstanding Value: Book Value

Before we relate the accounting balance sheet to economic values, we slightly reconfigure the accounting balance sheet.

The cash on hand is decomposed into “operating cash” and “excess cash”. Operating cash is the cash required for working capital

purposes. It is determined by the company’s cash budgeting process. “Excess cash” is cash that is not required for working capital

purposes. It is presumably kept for strategic reasons

In this example, we assume that $25 cash is required for operating purposes.

Remaining cash ($175) is “Excess cash.”

©2006 M. P. Narayanan

9

FIN Understanding Value: Book ValueUnderstanding Value: Book Value

Marketable securities and financial investments are taken out of current assets which is now re-labeled as “current operating assets.”

If there are any interest-bearing current liabilities, they are left on the sources side of the balance sheet.

Remaining items are re-labeled as “current operating liabilities.”

©2006 M. P. Narayanan

10

FIN Understanding Value: Book ValueUnderstanding Value: Book Value

Accounting Balance Sheet: Reconfigured

Uses Sources Fixed assets $1500

Excess Cash $175

Marketable securities &

financial investments $150

Current operating assets

Operating cash 25

Inventory $350

Receivable $400

Current operating liabilities Short-term debt $150

Payable ($320) Long-term debt $1000

Accrued expenses ($80) Equity $1050

$2200 $2200

Wor

king

cap

ital

©2006 M. P. Narayanan

11

FIN Understanding Value: Book ValueUnderstanding Value: Book Value

The total capital (on which a return must be provided) raised by the company is $2200: Short-term debt = $150 Long-term debt = $1000 Equity = $1050

Note that accounts payable and accrued expenses are not included as they are not interest-bearing liabilities.

©2006 M. P. Narayanan

12

FIN Understanding Value: Book ValueUnderstanding Value: Book Value

This capital is used to Acquire fixed assets = $1500 Invest in working capital = $375 Acquire financial holdings in other companies and invest in

excess cash and marketable securities (possibly for future investment needs) = $325

Note that working capital is the difference between current operating assets and current operating liabilities.

©2006 M. P. Narayanan

13

FIN Understanding Value: Economic ValueUnderstanding Value: Economic Value

Using the reconfigured accounting balance sheet as a model, we can now create an economic balance sheet.

The main difference is that Values in the accounting balance sheet represent what has

been invested. Values in the economic balance sheet represent the current

value of what has been invested.

The goal of companies is to ensure that the economic value exceeds the accounting value!!

©2006 M. P. Narayanan

14

FIN Understanding Value: Economic ValueUnderstanding Value: Economic Value

Economic Balance Sheet

Free CF @ WACC $2500 Short-term debt 150

Excess Cash $175 Long-term debt $1000

Marketable securities & financial investments

$150 Equity $1675

$2825 $2825

Enterprise value

©2006 M. P. Narayanan

15

FIN Understanding Value: Economic ValueUnderstanding Value: Economic Value

Fixed assets and working capital in the accounting balance sheet have been replaced by the present value of the free cash flow they are expected to generate in the future ($2500). This figure is just an assumed number.

This is the economic value of the operations of the company and is often called Enterprise Value.

Excess cash and marketable securities are usually valued the same as in the accounting balance sheet as their values are unlikely to be different.

Financial investments should be valued at market It is assumed in this example that the market and book values

are the same.

©2006 M. P. Narayanan

16

FIN Understanding Value: Economic ValueUnderstanding Value: Economic Value

The total value of the company is: Enterprise Value + Excess cash + Marketable securities +

Financial investments

In this example it is assumed the economic value of the debt is the same as in the accounting balance sheet. This is more likely to be true for short-term debt. The value of the long-term debt is more sensitive to changes

in interest rates. If the interest rates had increases since their issue, their value

would decrease from the face value.

©2006 M. P. Narayanan

17

FIN Understanding Value: Economic ValueUnderstanding Value: Economic Value

In general, liabilities also include, in addition to debt, obligations to other parties such as Legal and environmental liabilities Liabilities to employees such as pension

The value of equity is the difference between the total value of the company and all its liabilities. It is also called the market capitalization and is equal to the

share price times the number of shares outstanding.

This is the current value of the equity, i.e., what the shareholder will receive if they were to sell the company off at its current value and payoff all the liabilities.

©2006 M. P. Narayanan

18

FIN Constructing Economic Value Constructing Economic Value Balance SheetBalance Sheet

If a company is publicly traded, it is easy to construct the right side of the balance sheet: Debt values can be obtained from the accounting balance

sheet Equity value can be calculated by multiplying the share price

by the number of outstanding shares.

Value of items such as excess cash, marketable securities, and financial investments can be obtained from the accounting balance sheet and market prices of these items.

The enterprise value can then be calculated as the residual.

©2006 M. P. Narayanan

19

FIN Multiples: P/EMultiples: P/E

If valuation is being done for an IPO or a takeover, Value of firm = Average Transaction P/E multiple EPS of

firm Average Transaction multiple is the average multiple of recent

transactions (IPO or takeover as the case may be) If valuation is being done to estimate firm value

Value of firm = Average P/E multiple in industry EPS of firm

This method can be used when firms in the industry are profitable (have positive earnings) firms in the industry have similar growth (more likely for

“mature” industries) firms in the industry have similar capital structure

See next page

©2006 M. P. Narayanan

20

FIN P/E and leverageP/E and leverage

Gordon growth model: P0 = D1/(re − g) P0 = Stock price today

D1 = Expected next-year dividend per share

re = Cost of equity g = Expected dividend growth rate

Assume constant payout ratio K = Payout ratio = D1/ EPS1

P0 = K × EPS1/(re − g)

Simple algebra yields P0/EPS1 = K /(re − g)

As leverage increases, re increases, decreasing P/E multiple

©2006 M. P. Narayanan

21

FIN Multiples: Price to bookMultiples: Price to book

The application of this method is similar to that of the P/E multiple method.

Since the book value of equity is essentially the amount of equity capital invested in the firm, this method measures the market value of each dollar of equity invested.

This method can be used for companies in the manufacturing sector which have significant

capital requirements. companies which are not in technical default (negative book

value of equity)

©2006 M. P. Narayanan

22

FIN Multiples: Enterprise Value to Multiples: Enterprise Value to EBITDAEBITDA

This multiple measures the enterprise value, that is the value of the business operations (as opposed to the value of the equity).

In calculating enterprise value, only the operational value of the business is included.

Value from investment activities, such as investment in treasury bills or bonds, or investment in stocks of other companies, is excluded.

©2006 M. P. Narayanan

23

FIN Value to EBITDA multiple: Value to EBITDA multiple: ExampleExample

Suppose you wish to value a target company using the following data: Revenue = $800 million COGS = $500 million SG&A = $150 million

All from continuing operations only Excludes any non-operating income such as interest and dividend

income Excludes interest expenses

Depreciation (from CF statement) = $50 million Cash in hand = $25 million Marketable securities = $45 million Sum of long-term and short-term debt held by target = $750

million

©2006 M. P. Narayanan

24

FIN Value to EBITDA multiple: Value to EBITDA multiple: ExampleExample

You collect the following data about a recent takeover in the same industry Selling price = $40 a share (40 shares) Cash on hand = $50 million (all assumed “Excess Cash”) Marketable securities = $200 million Market value of financial investments = $120 million Short-term debt = $200 million Long-term debt = $1100 million From continuing operations

Revenue = $1000 million COGS = $650 million SG&A = $120 million Depreciation = $70 million

©2006 M. P. Narayanan

25

FIN Value to EBITDA multiple: Value to EBITDA multiple: ExampleExample

First compute enterprise value at which this comparable company sold.

Equity value = 40 × 40 = $1600 million Enterprise value = 1600 + 1100 + 200 − 250 − 120 = $2530 million

Economic Balance Sheet

Enterprise value $2530 Short-term debt 200

Excess Cash & marketable securities

$250 Long-term debt $1100

Market value of financial investments

$120 Equity $1600

$2900 $2900

©2006 M. P. Narayanan

26

FIN Value to EBITDA multiple: Value to EBITDA multiple: ExampleExample

Next compute the EBITDA of the comparable company from continuing operations EBITDA = Revenue − COGS − SG&A + Depreciation EBITDA = 1000 − 650 − 120 + 70 = $300 million

Compute the Enterprise value/EBITDA multiple at which the comparable firm sold Enterprise value/EBITDA = 2530/300 = 8.43

Compute EBITDA of your target company EBITDA of target = 800 − 500 − 150 + 50 = $200 million

Compute enterprise value of the target Enterprise value of target = 200 × 8.43 = $1686 million

©2006 M. P. Narayanan

27

FIN Value to EBITDA multiple: Value to EBITDA multiple: ExampleExample

Compute equity value of target company Equity value = 1686 + 70 − 750 = $1006 million Finally, if there are acquisition costs (Investment banking, legal)

and financing costs (bank fees, transaction costs) subtract from equity value (not done in this example).

Economic Balance Sheet

Enterprise value $1686 Total debt $750

Excess Cash & marketable securities

$70 Equity $1006

$1756 $1756

©2006 M. P. Narayanan

28

FIN Valuation: Value to EBITDA Valuation: Value to EBITDA multiplemultiple

Since this method measures enterprise value it accounts for different capital structures cash and security holdings

By evaluating cash flows prior to discretionary capital investments, this method provides a better estimate of value.

Appropriate for valuing companies with large debt burden: while earnings might be negative, EBIT is likely to be positive.

Gives a measure of cash flows that can be used to support debt payments in leveraged companies.

©2006 M. P. Narayanan

29

FIN Mutiples methods: drawbacksMutiples methods: drawbacks

While Multiples methods are simple, all of them share several common disadvantages: They do not accurately reflect the synergies that may be

generated in a takeover. They assume that the market valuations are accurate. For

example, in an overvalued market, we might overvalue the firm under consideration.

They assume that the firm being valued is similar to the median or average firm in the industry.

They require that firms use uniform accounting practices.

©2006 M. P. Narayanan

30

FIN Valuation: DCF methodValuation: DCF method

This is similar to the technique we used in capital budgeting: Estimate expected free cash flows of the target including any

synergies resulting from the takeover Discount it at the appropriate cost of capital This yields enterprise value

After calculating enterprise value, equity value of target is calculated using the same process as before.

©2006 M. P. Narayanan

31

FIN Valuation: DCF methodValuation: DCF method

DCF methods impose stricter discipline on the acquiring company They need to specify the value drivers of the takeover They need to provide estimates of the value created and their

sources Allows for post-audit of the takeover based on these

benchmarks

©2006 M. P. Narayanan

32

FIN DCF methods: Starting dataDCF methods: Starting data

Free Cash Flow (FCF) of the firm WACC

©2006 M. P. Narayanan

33

FIN Template for Free Cash FlowTemplate for Free Cash Flow

Ope

ratin

g In

com

e S

tate

men

tRevenue

Less Costs

Less Depreciation

Profits from asset sale

Taxable income

Less Tax

NOPAT

Add back Depreciation

Less Profits from asset sale

Operating cash flow

Less increase in working capital

Less capital expenditure

Cash from asset sale

Free cash flow (or unlevered CF)

©2006 M. P. Narayanan

34

FIN Template for Free Cash FlowTemplate for Free Cash Flow

The goal of the template is to estimate cash flows, not profits.

Template is made up of three parts. An Operating Income Statement Adjustments for non-cash items included in the Operating

Income Statement to calculate taxes Capital items, such as capital expenditures, working capital,

cash from asset sales, etc. The Operating Income Statement portion differs from the usual

income statement because it ignores interest. This is because, interest, the cost of debt, is included in the cost of capital and including it in the cash flow would be double counting.

©2006 M. P. Narayanan

35

FIN Template for Free Cash FlowTemplate for Free Cash Flow

There are four categories of items in our Operating Income Statement. While the first three items occur most of the time, the last one is likely to be less frequent. Revenue items Cost items Depreciation items Profit from asset sales

Cash from asset sale − Book value of asset Book value of asset = Initial investment − Accumulated depreciation

Adjustments for non-cash items is to simply add all non-cash items subtracted earlier (e.g. depreciation) and subtract all non-cash items added earlier (e.g. Profit from asset sale).

©2006 M. P. Narayanan

36

FIN Template for Free Cash FlowTemplate for Free Cash Flow

There are two type of capital items Fixed capital (also called Capital Expenditure (Cap-Ex), or

Property, Plant, and Equipment (PP&E)) Working capital

We need to include only additions to capital (both fixed and working) since the capital originally invested is still employed in the project.

It is important to recover both types of capital at the end of a finite-lived project. Recover the market value property plant and equipment

Cash from asset sale Recover the working capital left in the project (assume full

recovery)

©2006 M. P. Narayanan

37

FIN Template for Free Cash FlowTemplate for Free Cash Flow

What is the FCF template actually doing?

See table on the right The template is longer

because of tax calculations Items on the right are the

value drivers You may view this as a

conceptual template

Revenue

Less Costs

Less Tax

Less increase in working capital

Less capital expenditure

Cash from asset sale

Free cash flow (or unlevered CF)

©2006 M. P. Narayanan

38

FIN Estimating HorizonEstimating Horizon

For a finite stream, it is usually either the life of the product or the life of the equipment used to manufacture it.

Since a company is assumed to have infinite life: Estimate FCF on a yearly basis for about 5 years. After that, calculate a “Terminal Value”, which is the ongoing

value of the firm.

©2006 M. P. Narayanan

39

FIN Terminal ValueTerminal Value

Terminal value can be calculated several ways: Use the constant growth perpetuity model with a long-term

growth closer to economy growth rates. Works for mature industries

Estimate a two- or three-stage model, Higher growth rate(s) in the initial stage(s) (for about 10 years) A lower long-term growth for the final stage

Use a Enterprise value to EBITDA multiple based on industry averages to estimate terminal value

©2006 M. P. Narayanan

40

FIN WACCWACC

One of the issues in the valuation of companies for acquisition is what WACC to use. Should we use the target company’s WACC or the acquirer’s

WACC? Or something else? As always, the answer is “it depends.” If a conglomerate is buying a target company, it is

appropriate to use the target company’s WACC. There is likely to be very little interaction between the target

company’s operations and that of the acquirer. If it is a horizontal merger, the WACC of acquirer and

target are likely to be close. A weighted average WACC may be appropriate (weights

based on the enterprise values of the two parties)

©2006 M. P. Narayanan

41

FIN WACCWACC

The idea is that if the integration of the target with the acquirer is minimal, the target’s WACC is appropriate.

If there is substantial integration, but companies are not in the same industry, it becomes more difficult to figure out a precise WACC to value the target. The issue has to be dealt on a case by case basis.

©2006 M. P. Narayanan

42

FIN Valuation of private companiesValuation of private companies

Private company stocks are very illiquid Similar to small firms with less liquid stocks, private company

stocks also will sell at a discount. The liquidity issue much more severe with private companies.

Private company owners are likely to be less diversified. Therefore, they bear both the market risk and the company-specific risk, increasing their cost of capital and decreasing the value of the firm to them. If you own only GM stock you are bearing the risk of the auto

industry as well risk that is GM-specific (a strike at GM). If you own all the auto company stocks (GM, Ford, Toyota,

Nissan, Volkswagen, Diamler-Chrysler), you bear only the auto industry risk.

©2006 M. P. Narayanan

43

FIN Valuation of private companiesValuation of private companies

The typical method of valuing a private company is to value it as if it is a public company and then apply a discount for the reasons stated earlier. Find a pure-play and use its WACC to discount the cash flows

of the private company Pure-play is a public company that has the same business risk as

the private company Or, use the multiples of a public company

The trick is to compute this discount. There are ways to get some handle on this discount. The discounts are in the 20-40% range

©2006 M. P. Narayanan

44

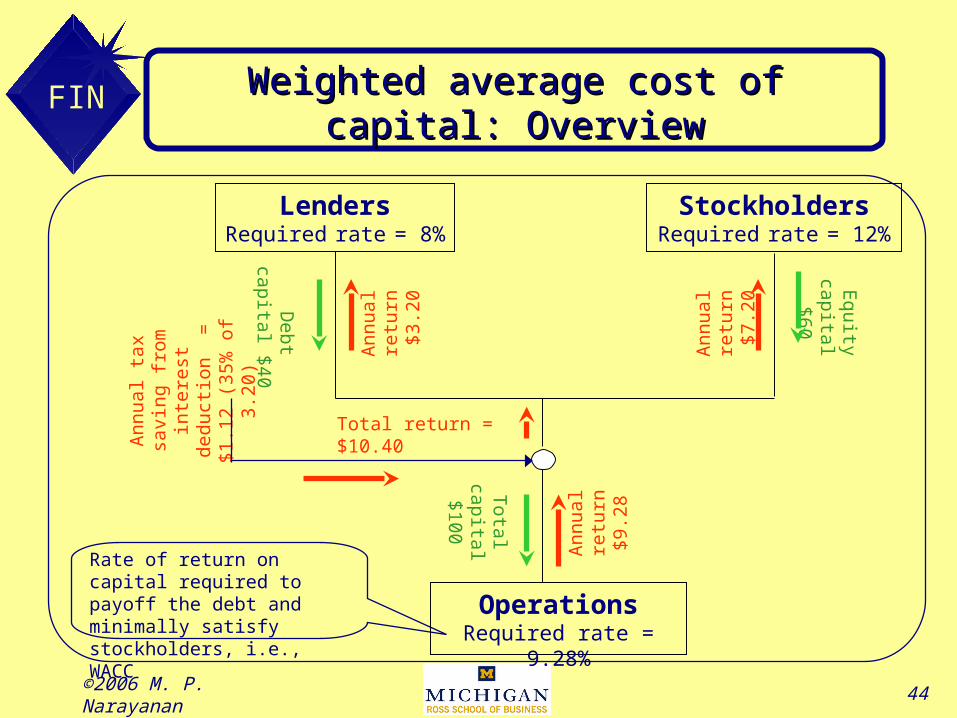

FIN Weighted average cost of capital: Weighted average cost of capital: OverviewOverview

LendersRequired rate = 8%

Debt capital

$40

Ann

ual r

etur

n $

3.20

StockholdersRequired rate = 12%

Equ

ity capital $60

Ann

ual r

etur

n $

7.20

Tota

l capital $10

0

Ann

ual r

etur

n$9

.28

Ann

ual t

ax

savi

ng

from

inte

rest

de

duc

tion

=

$1.

12

(35%

of

3.20

)

Total return = $10.40

Rate of return on capital required to payoff the debt and minimally satisfy stockholders, i.e., WACC

OperationsRequired rate = 9.28%

©2006 M. P. Narayanan

45

FIN Costs of debt and equityCosts of debt and equity

Cost of debt can be approximated by the yield to maturity of the debt.

If the yield is not directly available, check the bond rating of the company and find the YTM of similar rated bonds.

Cost of equity CAPM

Find e and calculate required re. Use Gordon-growth model and find expected re. Under the

assumption that market is efficient, this is the required re. You need an estimate of future dividend growth rate to do this. Therefore, works better for firms with a history of dividend

payments

©2006 M. P. Narayanan

46

FIN Valuation: CF to Equity methodValuation: CF to Equity method

In the WACC method, we compute Enterprise value by discounting the free cash flows at WACC Add value of any financial investments Subtract value of debt to obtain equity value

In CF to Equity method, we Compute CF that are available to equity-holders

This is Free Cash Flow less principal and after-tax interest payments

Discount this at cost of equity and directly compute equity value

©2006 M. P. Narayanan

47

FIN Equity value: WACC methodEquity value: WACC method

Value from Operations

Value of DebtEquity value

Value generated

Value from investments

Enterprise value

All are values: CF discounted at appropriate cost of capital

©2006 M. P. Narayanan

48

FIN Equity value: CF to Equity Equity value: CF to Equity methodmethod

FCF from Operations

CF to Debt(Principal, after-tax

interest) CF to Equity

Total CF generated

CF from investments

All are CF

Equity value = CF to Equity @ re