final goldman sachs gold day 300513 - newcrest … sachs australia gold day 30 may 2013, sydney...

TRANSCRIPT

Goldman SachsAustralia Gold Day30 May 2013, Sydney

Spencer ColeManager Investor Relations

2

Disclaimer

Forward Looking Statements

These materials include forward looking statements. Often, but not always, forward looking statements can generally be identified by the use of forward looking words such as “may”, “will”, “expect”, “intend”, “plan”, “estimate”, “anticipate”, “continue”, and “guidance”, or other similar words and may include, without limitation, statements regarding plans, strategies and objectives of management, anticipated production or construction commencement dates and expected costs or production outputs.

Forward looking statements inherently involve known and unknown risks, uncertainties and other factors that may cause the company’s actual results, performance and achievements to differ materially from any future results, performance or achievements. Relevant factors may include, but are not limited to, changes in commodity prices, foreign exchange fluctuations and general economic conditions, increased costs and demand for production inputs, the speculative nature of exploration and project development, including the risks of obtaining necessary licenses and permits and diminishing quantities or grades of reserves, political and social risks, changes to the regulatory framework within which the company operates or may in the future operate, environmental conditions including extreme weather conditions, recruitment and retention of personnel, industrial relations issues and litigation.

Forward looking statements are based on the company and its management’s good faith assumptions relating to the financial, market, regulatory and other relevant environments that will exist and affect the company’s business and operations in the future. The company does not give any assurance that the assumptions on which forward looking statements are based will prove to be correct, or that the company’s business or operations will not be affected in any material manner by these or other factors not foreseen or foreseeable by the company or management or beyond the company’s control.

Although the company attempts and has attempted to identify factors that would cause actual actions, events or results to differ materially from those disclosed in forward looking statements, there may be other factors that could cause actual results, performance, achievements or events not to be as anticipated, estimated or intended, and many events are beyond the reasonable control of the company. Accordingly, readers are cautioned not to place undue reliance on forward looking statements. Forward looking statements in these materials speak only at the date of issue. Subject to any continuing obligations under applicable law or any relevant stock exchange listing rules, in providing this information the company does not undertake any obligation to publicly update or revise any of the forward looking statements or to advise of any change in events, conditions or circumstances on which any such statement is based.

Ore Reserves and Mineral Resources Reporting Requirements

As an Australian company with securities listed on the Australian Securities Exchange (“ASX”), Newcrest is subject to Australian disclosure requirements and standards, including the requirements of the Corporations Act and the ASX. Investors should note that it is a requirement of the ASX listing rules that the reporting of ore reserves and mineral resources in Australia comply with the 2004 Edition of the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves (the “JORC Code”) and that Newcrest’s ore reserve and mineral resource estimates comply with the JORC Code. As a company listed on the Toronto Stock Exchange (“TSX”), Newcrest is subject to certain Canadian disclosure requirements and standards, including the requirements of National Instrument 43-101 - Standards of Disclosure for Mineral Projects of the Canadian Securities Administrators (“NI 43-101”). In accordance with NI 43-101, Newcrest reports its ore reserves and mineral resources estimates in compliance with the JORC Code, along with a reconciliation to the material differences between the JORC Code and the applicable definitions adopted by the Canadian Institute of Mining, Metallurgy and Petroleum (CIM Definition Standards). In relation to the December 2012 Resources and Reserves Statement, the reconciliation is set out in Newcrest’s Canadian News Release dated 8 February 2013, and is available at www.sedar.com and at Newcrest’s website www.newcrest.com.au. Except as otherwise noted in that document, there are no material differences between the definitions of Measured, Indicated and Inferred Mineral Resources, and Proven and Probable Reserves, under the CIM Definition Standards and the equivalent or corresponding definitions in the JORC Code.

Competent Person’s Statement

The information in this presentation that relates to Exploration Results and other scientific and technical information is based on information compiled by C. Moorhead, EGM Minerals for Newcrest who is a Fellow of The Australasian Institute of Mining and Metallurgy, and a full-time employee of Newcrest. Mr Moorhead has sufficient experience which is relevant to the styles of mineralisation and types of deposits under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the JORC Code and is a Qualified Person within the meaning of NI 43-101. Mr Moorhead consents to and has approved the inclusion in this presentation of the matters based on this information in the form and context in which it appears including sampling, analytical and test data underlying the results. For details of exploration reports refer to the Newcrest website at www.newcrest.com.au.

Non-IFRS Financial Information

This presentation uses Non-IFRS financial information including Underlying Profit, EBITDA and EBIT. Underlying Profit is presented to assist in the assessment of the relative performance of the Group. EBITDA and EBIT are used to measure segment performance and have been extracted from the Segment Information disclosed in the ASX Appendix 4D. Non-IFRS information has not been subject to review by Newcrest’s external auditor.

3

Newcrest Mining

Telfer

Gosowong

Lihir Is

Cadia Valley

Wafi-GolpuTandai

Manus Is

Gold Equivalent Resource

Bonikro

Namosi JV

Hidden Valley

• 4th largest global gold producer1

• Primarily Australia and Asia Pacific

• 6 production assets in 4 countries

• FY13 Gold production 2.00 – 2.15Moz2

• FY13 Copper production 75 – 85kt2

• Reserve life >30 years

• Gearing 17%3

+50Moz20-50Moz0-20Moz

1 By market capitalisation2 March 2013 production guidance.3 Per December 2012 half year financial results. Gearing = Net Debt / (Net Debt + Equity)

• Gold

• Long life, low cost, moderate growth

• Australia, SE Asia focus

• Unhedged, low gearing, dividend growth

• Focus on early stage resources

• People & technical capability focus

• Management incentives =ROCE, reserve growth, and cost position

Newcrest in a snapshot

Newcrest strategy

4

Why Newcrest

• Find– Company built on exploration success– Low cost resource capture– Long Reserve life (>30 years)

• Develop– Successful delivery of major projects– Near term growth from capital already

invested

• Operate– High quality, low cost assets drive growth– Focus on consistent, predictable delivery– Strong balance sheet– Positioning for higher free cash flow

5

Near term growth from past investment

• 30 year + mine life, second quartile cash cost• Production capability of ~1 million ounces p.a.• Old plant refurbishment key to improving

reliability (> 50% complete)

• Highly automated, large tonnage bulk underground mine – expected mining cost $6/t

• Production growth to ~750,000 ounces gold p.a. over next 5 years

• Lowest cost quartile, 30 year mine life

Cadia – commercial production from Jan 2013

Lihir – plant expansion completed Feb 2013

• High grade, low cost, 20+ year mine life• Resource 29moz Au1, 9mt Cu1

• Production objective 600koz Au1 and 300kt Cu1

• Technical prefeasibility done, initial capex $4.8B1

Wafi Golpu – the next major growth engine

1 Figures shown on 100% basis – Newcrest share is 50%

6

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

0% 25% 50% 75% 100%

USD$/oz

Percentile

Industry Reported Total Cash Cost($/oz post by product credit)

GosowongCadia Valley

Lihir

Telfer

Bonikro

Hidden Valley

1st Quartile

2nd Quartile

3rd Quartile

4th Quartile

Source: Thompson-Reuters GFMS; CY2012 (Q1 to Q3)

Production growth at low end of the cost curveGold industry cash costs (post by product credits)

Major growth projects in 1st and 2nd quartile

Future Wafi-Golpu cost position

All-in sustaining cash cost around $1,250 in FY13, expected to be lower in future years

7

Declining capital expenditure profile

• Cadia East panel cave 1 established and Lihir plant expansion complete

• FY14 capital remains focused on Cadia and Lihir

• Studies paused on some longer dated projects

• Wafi-Golpu capex estimate review, minimal expenditure in FY14

Capital expenditure trend

0

500

1,000

1,500

2,000

2,500

3,000

FY12 FY13 FY14 FY15 FY16 FY17

A$mWafi Golpu

Major Projects

Minor Projects

Development

Sustaining

Higher free cashflow anticipated from increased production and declining capital expenditure

8

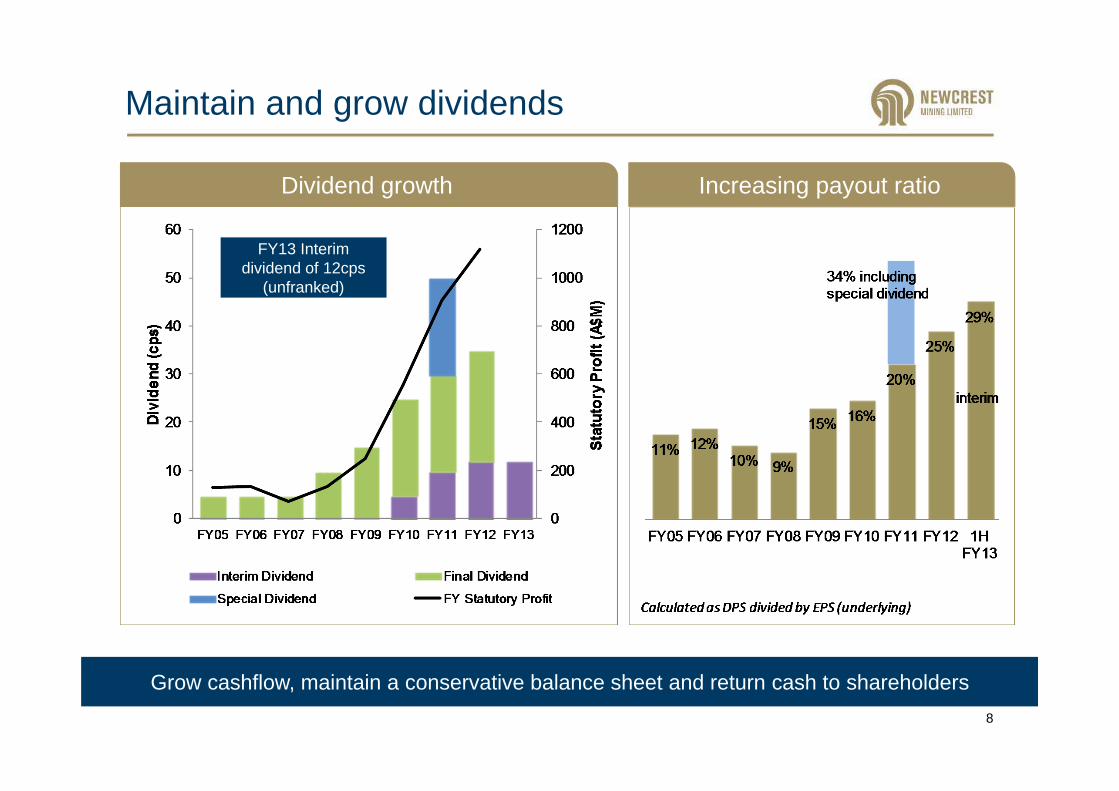

Maintain and grow dividends

Dividend growth

FY13 Interim dividend of 12cps

(unfranked)

Increasing payout ratio

Grow cashflow, maintain a conservative balance sheet and return cash to shareholders

9

Strong balance sheet

• Conservative balance sheet to absorb gold price volatility

• Long dated debt repayment profile

• Credit ratings BBB & Baa2, stable outlook

• Gearing 17%1

Maintain conservative balance sheet

1 Per December 2012 half year financial results. Gearing = Net Debt / (Net Debt + Equity)

Long dated debt repayment profile1

10

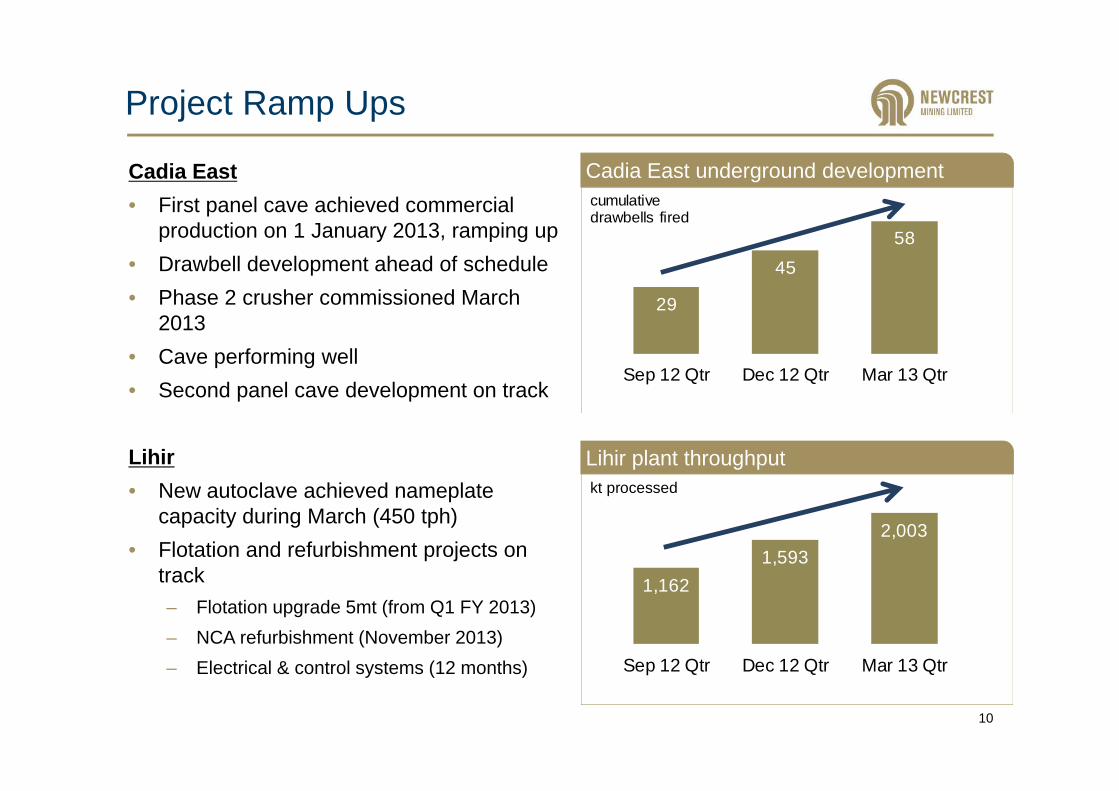

Project Ramp Ups

Cadia East• First panel cave achieved commercial

production on 1 January 2013, ramping up• Drawbell development ahead of schedule• Phase 2 crusher commissioned March

2013• Cave performing well• Second panel cave development on track

Lihir• New autoclave achieved nameplate

capacity during March (450 tph) • Flotation and refurbishment projects on

track– Flotation upgrade 5mt (from Q1 FY 2013)– NCA refurbishment (November 2013)– Electrical & control systems (12 months)

29

4558

Sep 12 Qtr Dec 12 Qtr Mar 13 Qtr

cumulative drawbells fired

Cadia East underground development

Lihir plant throughput

1,1621,593

2,003

Sep 12 Qtr Dec 12 Qtr Mar 13 Qtr

kt processed

11

Telfer

• High cost mine, produce only cash profitable ounces

• Producing to plan of ~ 500koz

• No new capital in current price and cost environment

Gosowong

• High margin mine, focus on extending reserve life

• Re-established access to higher grade ore

• Expected 2013 production around 300 - 325koz

Hidden Valley

• Actions to improve production and cost structure

• Primary crusher installation May 2013

• Targeting 20-30% cost reduction over next 12 months

Bonikro

• 3rd quartile cash cost, steady production

• Possible expansion delayed for 2 years

• Stripping investments continue, providing margins hold

Focus on operating cashflow at other assets

12

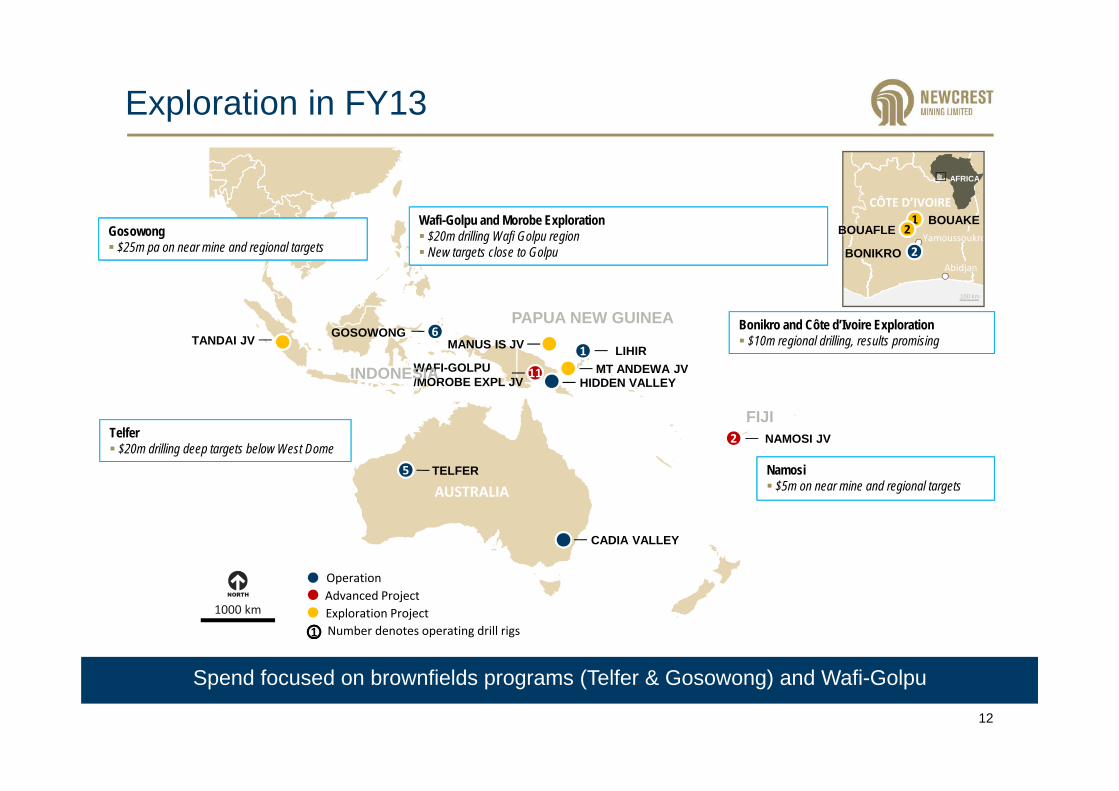

Exploration in FY13

WAFI-GOLPU/MOROBE EXPL JV

PAPUA NEW GUINEA

INDONESIA

AUSTRALIA

FIJI

55

22

6611

100 km

AFRICA

Yamoussoukro

AbidjanBONIKRO

11 BOUAKEBOUAFLE

CÔTE D’IVOIRE

22

22

1000 km

1111

CADIA VALLEY

NAMOSI JV

HIDDEN VALLEY

TANDAI JV

MT ANDEWA JV

MANUS IS JVGOSOWONG

TELFER

LIHIR

OperationAdvanced ProjectExploration Project

Bonikro and Côte d’Ivoire Exploration $10m regional drilling, results promising

Telfer $20m drilling deep targets below West Dome

Wafi-Golpu and Morobe Exploration $20m drilling Wafi Golpu region New targets close to Golpu

Namosi $5m on near mine and regional targets

Gosowong $25m pa on near mine and regional targets

11 Number denotes operating drill rigs

Spend focused on brownfields programs (Telfer & Gosowong) and Wafi-Golpu

13

Price & cost pressure= delay capital, attack costs

• Costs have followed higher commodity prices (labour, energy, commodity inputs)• Industry trend - declining grades and labour productivity• Exchange rates drive regional differences• Await firmer direction for larger capital decisions

Relative cost impacted by exchange rates

Source: Thomson Reuters GFMS, Bloomberg

Stop high cost ounces, lower business activity, productivity remains key

-250

0

250

500

750

1,000

1,250

1,500

1,750

2,000

0 10 20 30 40 50 60 70 80 90 100

Cash

Cos

t US$

/oz

(net

of b

y-pr

oduc

t cre

dit)

Cumulative Production (Percent)

H1 2012

2006

Industry cash costs

Source: Thomson Reuters GFMS Gold Mine Economics Service

Average Cash Cost• 2006 US$317/oz• 2012 US$738/ozAustralia• 2012 US$857/oz

14

Gold price and money supply

• Western economies have loosened monetary policy

• Fundamentals still support a strong gold price– Currency devaluation– Negative real interest rates– Inflation, political and economic

uncertainty

• Physical gold buyers strong

Fundamentals remain for a strong medium term gold price

Global money supply and gold price

15

Insulating against gold price volatility

• Long dated debt maturity profile• Low gearing to absorb gold price volatility• Credit ratings BBB & Baa2, stable outlook

• Production growth from low cost operations• Simplified off-site activity and reduced headcount• Re-negotiating costs and activity with key suppliers• Heavy emphasis on productivity & technology

• Postponed or slowed some long dated studies• Reviewed exploration program• Retain sight of “cheap resource capture”

• Focus on delivering return on past investments• Stopping all capital investment in higher cost

ounces• Reviewing open pit material movements

Strong Balance Sheet

Free Cashflow

Focus

Protect Margins

Prioritise Growth Options

16

Summary

• Deliver Lihir and Cadia ramp up• Reduce business activities and costs• Focus capital expenditure on low cost ounces• Reduce Wafi‐Golpu start up capital • Maximize free cash flow• Increase dividends, subject to profitability• Maintain strong balance sheet