final level paper 4: corporate and economic laws

TRANSCRIPT

VIRTUAL COACHING CLASSESORGANISED BY BOS (ACADEMIC), ICAI

FINAL LEVELPAPER 4: CORPORATE AND ECONOMIC LAWS

Faculty: CA Navin Khandelwal, DISA, Regd Valuer, Insolvency Professional

© The Institute of Chartered Accountants of India

Date: 10th Feb 2021

11 February 2021 1

Inspection &Enquiry by ROC

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 2

POWER TO CALL FOR INFORMATION, INSPECT BOOKS AND CONDUCT INQUIRIES (SECTION 206 )

On a scrutiny of any document filed by a company

On any information received by him

to furnish in writing such information or explanation; or

to produce such documents,

Registrar is of opinion that any information or explanation is necessary.

Written notice

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 3

Company and its officers

furnish information

Produce any document

Past officers may be called upon (through separate notice)

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 4

Additional written notice by the Registrar

No information

supplied

Supplied information

is inadequate

On submission

ROC satisfied affairs are unsatisfied

2nd notice to call for inspection

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 5

on the basis of information available with or furnished to him; or

The Registrar may call on the company to furnish in writing any information or explanation and carry out such inquiry as he deems fit after providing the company a reasonable opportunity of being heard, if the Registrar is satisfied:

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 6

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 7

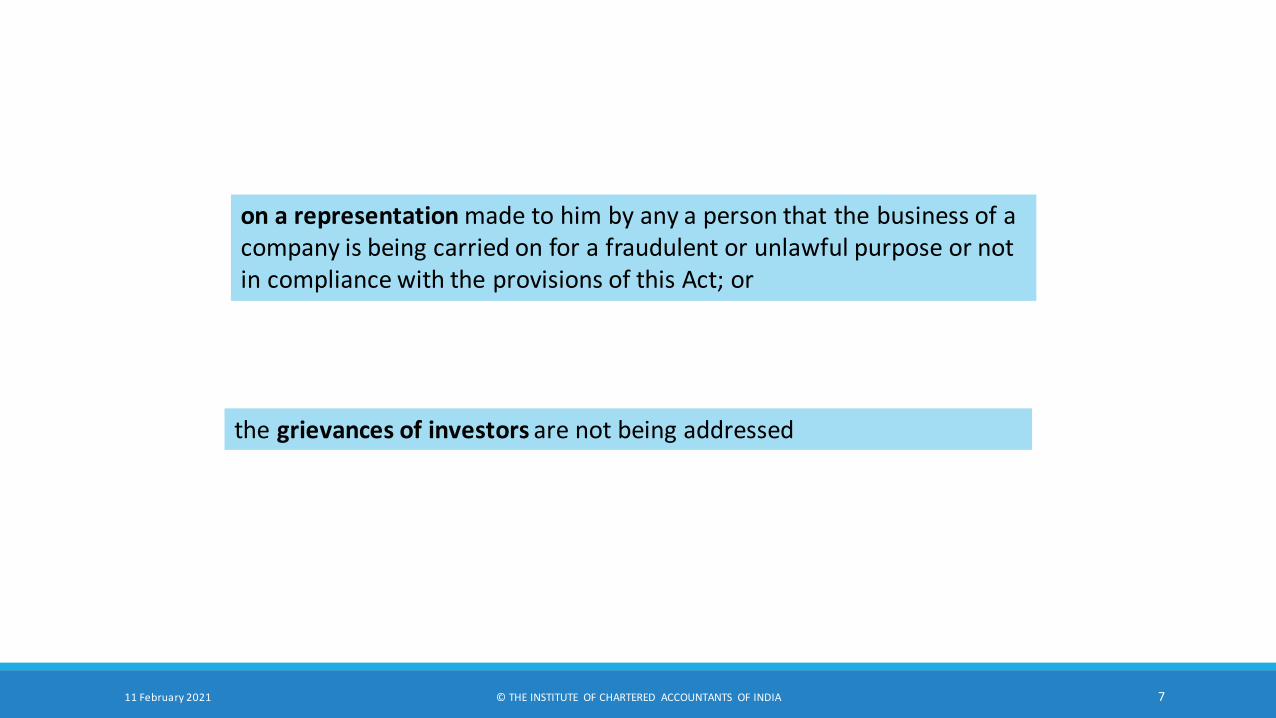

the grievances of investors are not being addressed

on a representation made to him by any a person that the business of a company is being carried on for a fraudulent or unlawful purpose or not in compliance with the provisions of this Act; or

Before calling the company

• to furnish in writing any information or explanations and carrying out the inquiry, the Registrar has to inform the company of the allegations made against it by a written order.

The Central Government

may

• if it is satisfied that the circumstances so warrant, direct to carry out inquiry.

fraudulent or unlawful

purpose

• every officer of the company who is in default shall be punishable for fraud in the manner as per section 447

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 8

Inspection by Central

Government

inspection of books by an inspector appointed by it

authorize any statutory authority

to carry out the inspection of books

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 9

Failure to furnish information

Company Every officer

Punishable fine which may extend to 1 lakh rupees and in case of a continuing failure, with an additional fine which may extend to 500 rupees for every

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 10

Powers during Inspection & Enquiry

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 11

Duties of Director

Powers of Registrar

Penalty

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 12

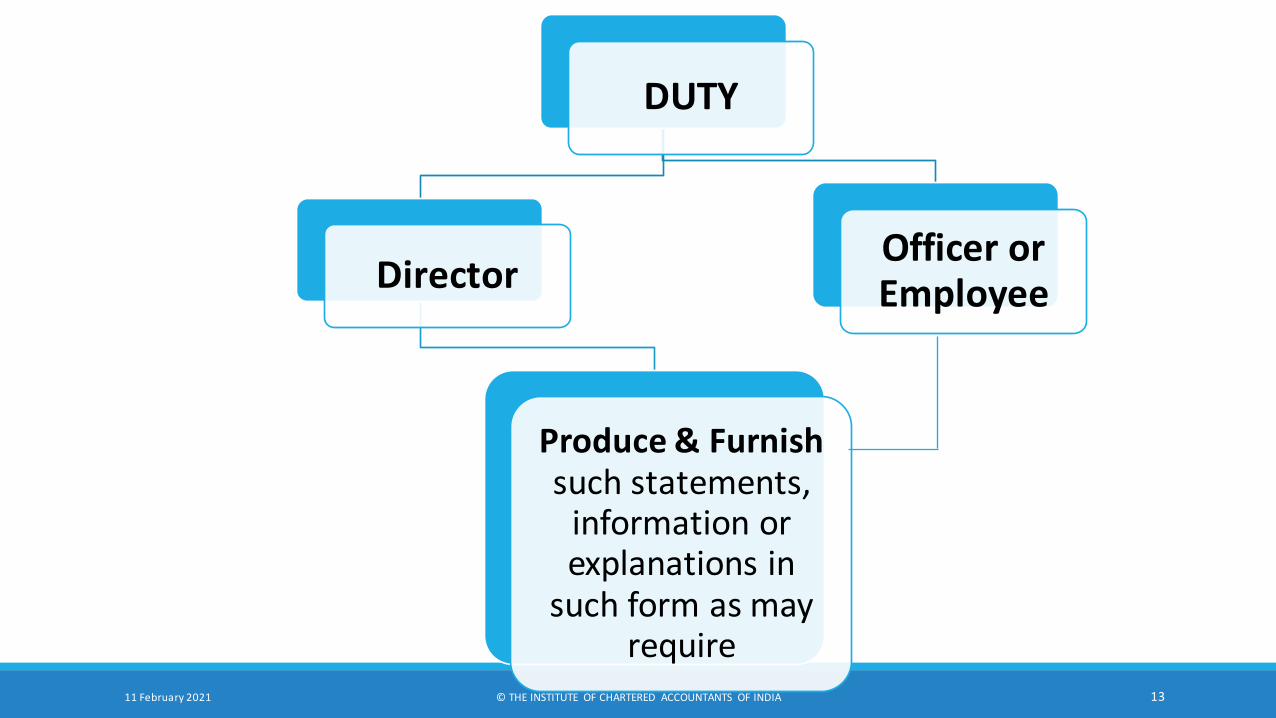

DUTY

Director

Produce & Furnish such statements,

information or explanations in

such form as may require

Officer or Employee

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 13

Powers of the Registrar or inspector

make or cause to be made copies of books of

account and other books and papers

place or cause to be placed any marks of identification in such books in token of the

inspection having been made

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 14

CIVIL POWER OF REGISTRAR & INSPECTOR

The Discovery and

Production of books of

account and other

documents

Summoningand enforcing

the attendance of persons and examining

them on oath

Inspection of any books,

registers and other

documents of the company at any place

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 15

Penalty for Contravention

DIRECTOR OTHER OFFICER

with fine which shall not be less than 25,000 rupees to 1

lakh rupees & shall be punishable with imprisonment

upto 1 year

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 16

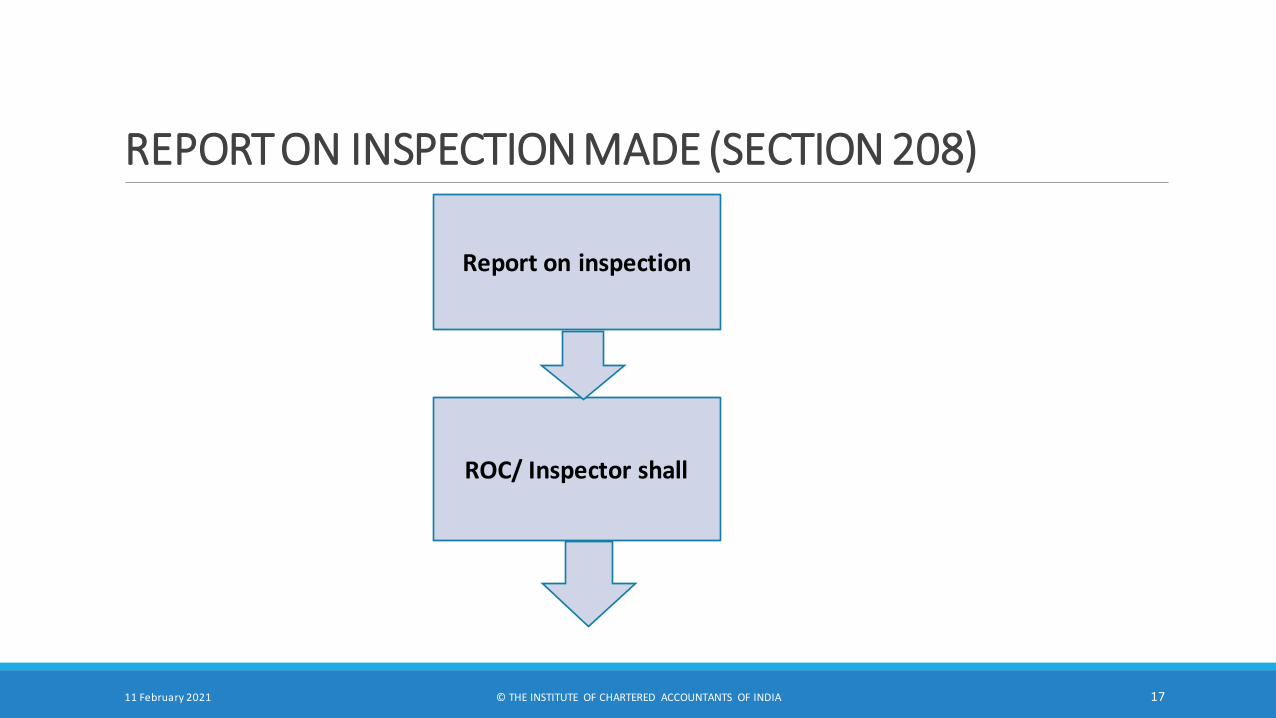

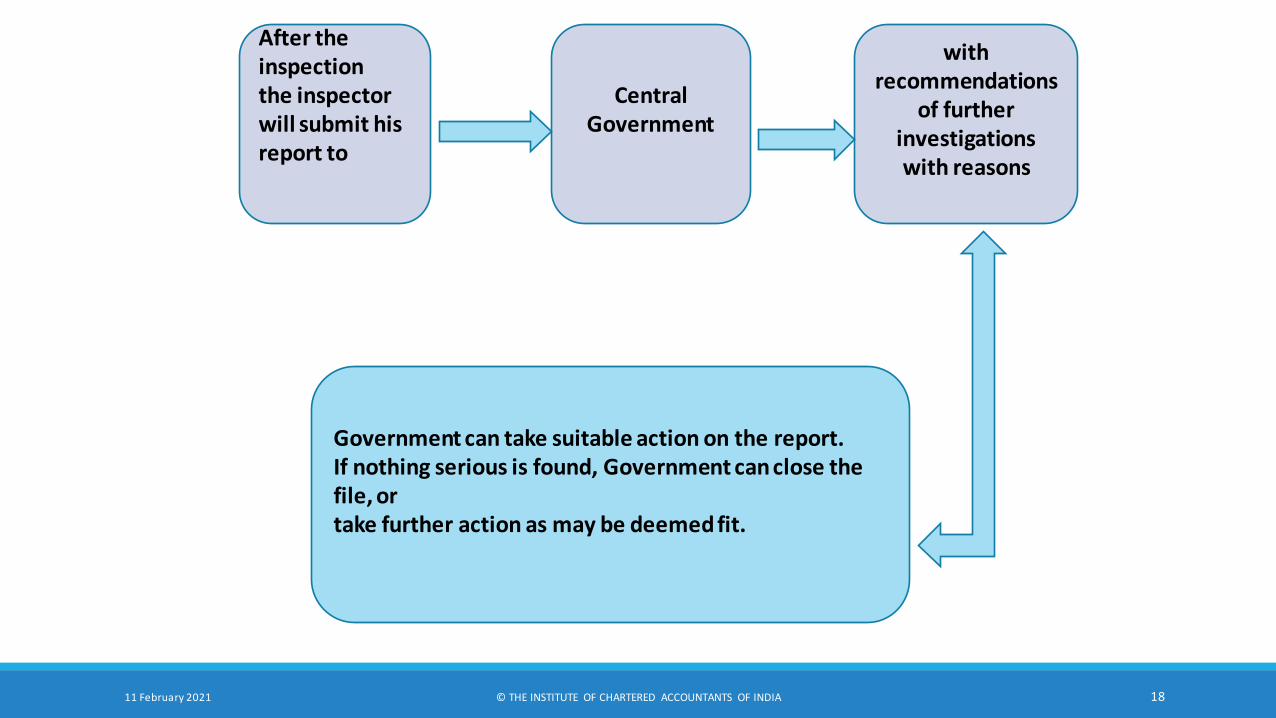

REPORT ON INSPECTION MADE (SECTION 208)

Report on inspection

ROC/ Inspector shall

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 17

After the inspectionthe inspector will submit his report to

Central Government

with recommendations

of further investigations with reasons

Government can take suitable action on the report.If nothing serious is found, Government can close the file, ortake further action as may be deemed fit.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 18

SEARCH AND SEIZURE (SECTION 209)

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 19

Registrar or inspector on reasonable grounds to believe that books relating to the affairs of the company may be

MutilatedDestroyed Altered Falsified or Secreted

After order of special court

Enter & Search Place

Search and seize books

MAX 180 DAYS + ADD. 180 DAYS11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 20

Example 1: A group of creditors of Mac Trading Limited makes a complaint to the Registrar of Companies, Hyderabad alleging that the management of the company is indulging in destruction and falsification of the accounting records of the company. The complainants request the Registrar to take immediate steps to seize the records of the company so that the management may not be allowed to tamper with the records. The complaint was received at 10 A.M. on 1stJuly 2018 and the ROC entered the premises at 10.30 A.M. for the search. Examine the powers of the Registrar to seize the books of the company

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 21

Answer: According to the provisions, Registrar may enter and search the place where such books or papers are kept and seize them only after obtaining an order from the Special Court.

Since in the given question, Registrar entered the premises for the search and seizure of books of the company without obtaining an order from the Special Court, he is not authorized to seize the books of the Mac Trading Limited.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 22

6. INVESTIGATION INTO AFFAIRS OF COMPANY (SECTION 210)

CG is of opinion on basis of

Report u/s 208

SR by Co.Public

Interest

May order investigation into affairs

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 23

Court/tribunal, if Order to CG

CG shall order investigation

Person submitting

Complaint Upto 25000 to be submitted

To be refunded

If investigation resulted into prosecution

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 24

Turnover as per previous year balance sheet Amount of security

Turnover up to 50 crores 10,000

Turnover more than 50 crore and up to 200 crore

15,000

Turnover more than 200 crore 25,000

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 25

Example 2: Shareholders of Hide and Seek Ltd. are not satisfied about performance of the company. It is suspected that some activities being run in the name of the company are not in the interest of the company or its members. 101 out of total 500 share holders of the company have made an application to the Central Government to appoint an inspector to carry out investigation and find out the true picture. Whether the shareholders’ application will be accepted? .

Answer: The shareholders’ application will not be accepted as under 210 of the Companies Act, 2013, Central Government may order an investigation into affairs of the company on the intimation of a special resolution passed by a company that the affairs of the company ought to be investigated and then may appoint the inspectors.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 26

Here, 101 out of total 500 shareholders of the company have made an application to the Central Government to appoint an inspector to carry out investigation but it is not sufficient as the company has not passed the special resolution.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 27

7. ESTABLISHMENT OF SERIOUS FRAUD INVESTIGATION OFFICE (SECTION 211)

Setting up of Serious Fraud Investigation Office (SFIO) [(1)]: The Central Government shall, by notification, establish an office to be called the Serious Fraud Investigation Office to investigate frauds relating to a company.

Composition of SFIO [Section 211 (2)]: The SFIO shall be:◦ Headed by a Director, and

Consist of such number of experts from the following fields to be appointed by the Central Government from amongst persons of ability

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 28

SFIO

BANKING

CORPORATE A/CING

FORENSIC

CAPITAL

INFORMATION

LAWINVESTIGATION

CYBER FORENSIC

MANAGEMENT

OTHER FIELDS

COST

FINANCIAL

TAXATION

DIRECT

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 29

Appointment of Experts Officers & Employees [(4)]: The Central Government may appoint such experts and other officers and employees in the SFIO as it considers necessary for the efficient discharge of its functions under this Act.

According to Rule 3 of the Companies (Inspection, Investigation and Inquiry) Rules, 2014, the Central Government may appoint

persons having expertise in the fields of investigations, cyber forensics, financial accounting, management accounting, cost accounting and any other fields as may be necessary for the

efficient discharge of Serious Fraud Investigation Office (SFIO) functions under the Act

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 30

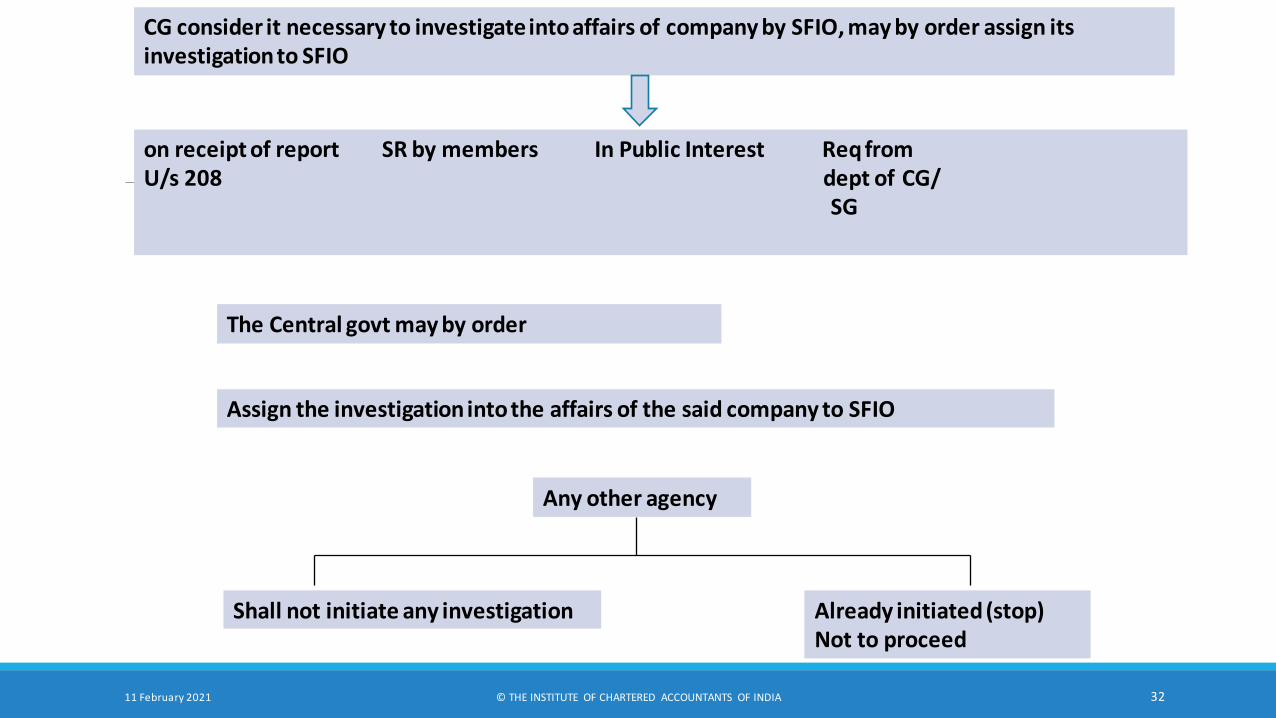

8. INVESTIGATION INTO AFFAIRS OF COMPANY BY SERIOUS FRAUD INVESTIGATION OFFICE (SECTION 212)

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 31

CG consider it necessary to investigate into affairs of company by SFIO, may by order assign its investigation to SFIO

on receipt of report SR by members In Public Interest Req from U/s 208 dept of CG/

SG

The Central govt may by order

Assign the investigation into the affairs of the said company to SFIO

Any other agency

Shall not initiate any investigation Already initiated (stop)Not to proceed

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 32

SFIO Report to CG

CO/Officers /Employees, to provide info/document as required by SFIO

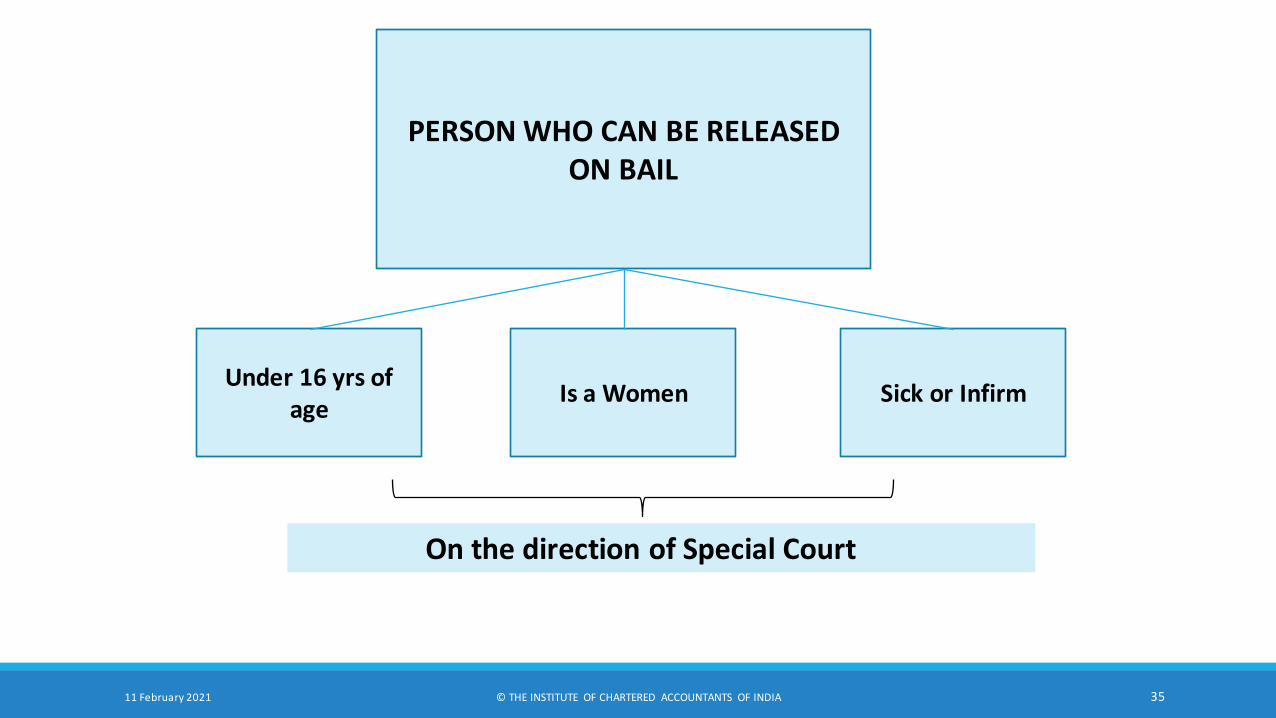

Offence covered u/s 447 of this act shall be cognizable and no person accused of any offence under those section shall be released on bail or on his own bond unless

Opportunity to public prosecutor to oppose Court is satisfied

The reasonable ground exist to prove

That person is not guilty

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 33

Special court shall not take cognizance except on complaint by

Director , SFIO Any other authorized by CG

Director/ Additional Director/Associate Director of SFIO

May arrest any person guilty of offence u/s 447

Every such person to be taken to judicial magistrate within 24 hours

SFIO Report of investigation C.Govt

On such report CG may direct To initiate prosecution against all guilty

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 34

PERSON WHO CAN BE RELEASED ON BAIL

Under 16 yrs of age

Is a Women Sick or Infirm

On the direction of Special Court

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 35

is of the opinion that it is necessary to investigate into the affairs of a company by the SFIO, the Central Government may, by order, assign the investigation into the affairs of the said company to the SFIO.

On receipt of such order, the Director, SFIO may designate such number of inspectors, as he may consider necessary for the purpose of such investigation.

Where any case has been assigned by the Central Government to the SFIO for investigation under this Act, no other investigating agency of Central Government or any State Government shall proceed with investigation in such case in respect of any offence under this Act.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 36

9. INVESTIGATION INTO COMPANY’S AFFAIRS IN OTHER CASES (SECTION 213 OF THE COMPANIES ACT, 2013)

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 37

Tribunal may

1.On application by

At least 100 members or 1/5 of members

Having 1/10 of total voting power Company having no share capital

In case of company having share capital

Along with necessary evidence

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 38

2. On application by other person(creditors) suggesting that

Buss. Of co. conducted Person concerned in formation or mgmt.

Inadequate Information to members

Incl. calculation of Managerial Remun.

• Issue direction to CG to investigate

• CG shall appoint 1 or more person

• Where upon investigation it is proved that

• Buss of co. conducted to Defraud creditors/member

• Person concerned in formation or mgmt is guilty of fraud, misfeasance

• All concerned shall be punishable with fraud u/s 447

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 39

PUNISHMENT IF PROVED

The business is conducted with intent to defraud its creditors, members

fraudulent or unlawful purpose

every officer of the company who is in default, and

the person or persons concerned in the formation of the company or the management of its affairs shall be punishable for fraud in the manner as provided in section 447.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 40

10. SECURITY FOR PAYMENT OF COSTS AND EXPENSES OF INVESTIGATION (SECTION 214)

• Where an investigation is ordered by the CG u/s 210 or 213

• The central govt may, before appointing an inspector

• Under section 210 or section 213,

• Require the applicant to give such security not exceeding 25000 rs.

• For payment of cost and expenses of the investigation and

• Such security shall be refunded to the applicant if the investigation results in prosecution

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 41

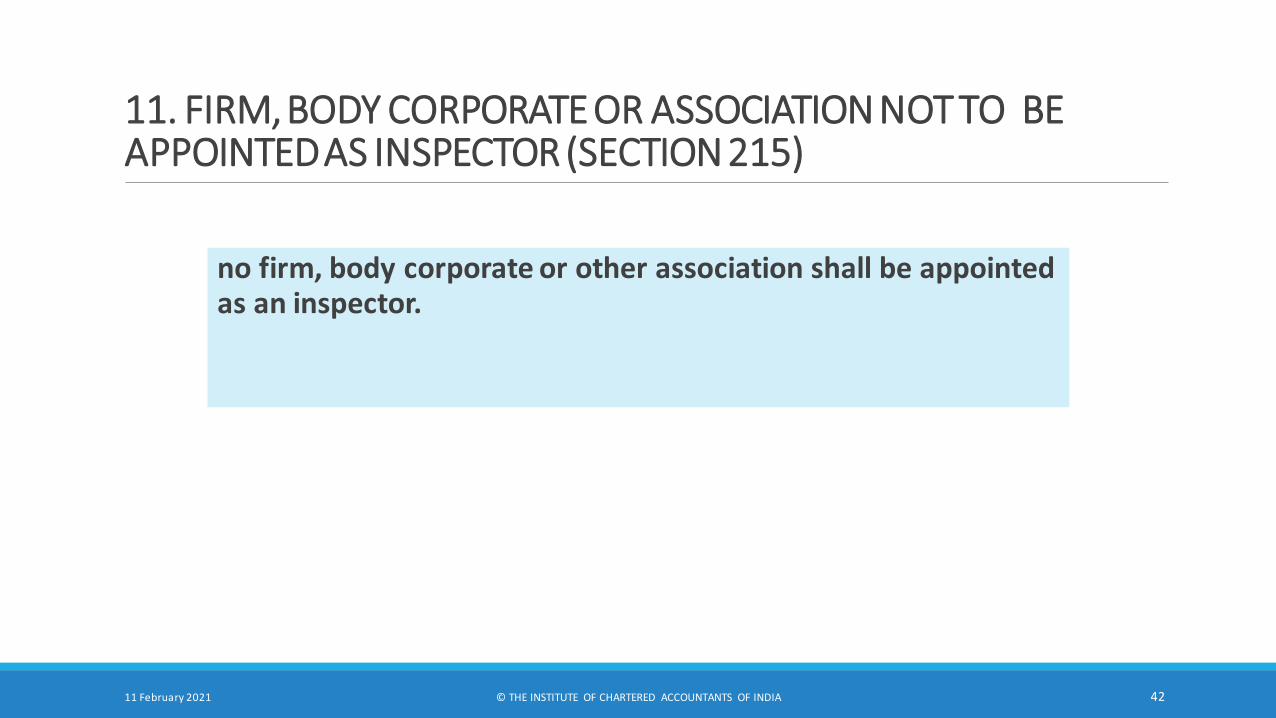

11. FIRM, BODY CORPORATE OR ASSOCIATION NOT TO BE APPOINTED AS INSPECTOR (SECTION 215)

no firm, body corporate or other association shall be appointed as an inspector.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 42

12. INVESTIGATION OF OWNERSHIP OF COMPANY (SECTION 216)

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 43

CG may appoint inspector To find true person

Who have financial interest in success/failure

Have been able to control policy of co.

or

CG shall appoint inspector If direction by Tribunal u/s 213

Regarding investigation with regard to membership of co.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 44

CG may define scope of investigation

Tenure Matter to be covered Any other matter

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 45

Imposition on restrictions during investigation on securities issued or to be issued by company

NCLT can impose certain restrictions upon securities upto three years

Prohibition of which company as well as every officer who is in default is liable for punishment of fine and imprisonment

Applicability of provisions to foreign company - The provisions of investigation of ownership apply to foreign company also

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 46

14. PROTECTION OF EMPLOYEES DURING INVESTIGATION (SECTION 218)

• During investigation of affairs of co./ other body corporate or any person u/s 210/212/213 or sec 219 or any member u/s 216

Any such co./Body corporate/person, proposed

To discharge or suspend any employee

Punish him by way of dismissal/removal

Change terms of his employee to his disadvantage

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 47

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 48

Any such co./B.C/Person to obtain prior approval of tribunal before proposed action

Tribunal to raise its objection if any by post

If no objection from trib. Within 30 days, Co./B.C/Person may proceed to take proposed action

Co./B.C/person is dissatisfied with objection of tribunal

Further appeal within 30 days to appellate tribunal

15. POWERS OF INSPECTOR

To conduct investigation into affairs of related companies, etc. (Section 219)

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 49

any other body corporate

Which is/ has been

Subs.+ subs of its holding co

Any other body corporate

Accustomed to act as per instruction of director of

such co. under investigation

Any person

which is/has been

MD/Manager or Employee of such co.

Any other Body corporate

Which is managed by

MD/Manager of co. under investigation

If during investigation u/s 210/212/213 inspector appointed consider it necessary to investigate affairs of

He shall investigate U/S 219 subject to prior approval of CG .11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 50

Seizure of documents by inspector (Section 220)

If during course of investigation

Inspector has reasonable ground to believe that

Book/paper relating to Co./MD/Manager or other Body Corporate

Likely to be destroyed/altered/mutilated

He may enter any such where these books are kept

Seize them after allowing copy to company Till completion of investigation

While returning such books, he may keep copies as well

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 51

Freezing of Assets of Company on Inquiry and Investigation (Section 221)

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 52

Tribunal may upon

On Reference by central govt

In connection with inquiry/investigation into affairs of company

Complaint by no. Of member as prescribed u/s 244

Complaint by creditors having o/s of 1 lakh or more

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 53

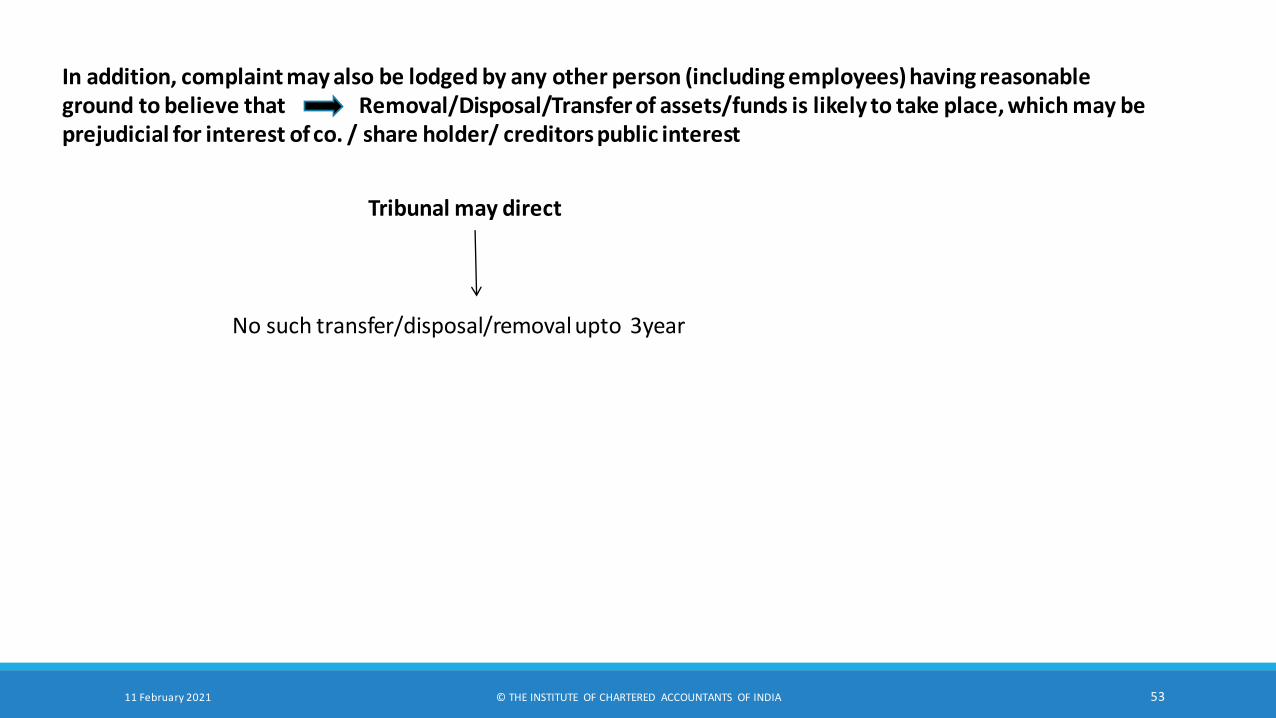

In addition, complaint may also be lodged by any other person (including employees) having reasonable ground to believe that Removal/Disposal/Transfer of assets/funds is likely to take place, which may be prejudicial for interest of co. / share holder/ creditors public interest

Tribunal may direct

No such transfer/disposal/removal upto 3year

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 54

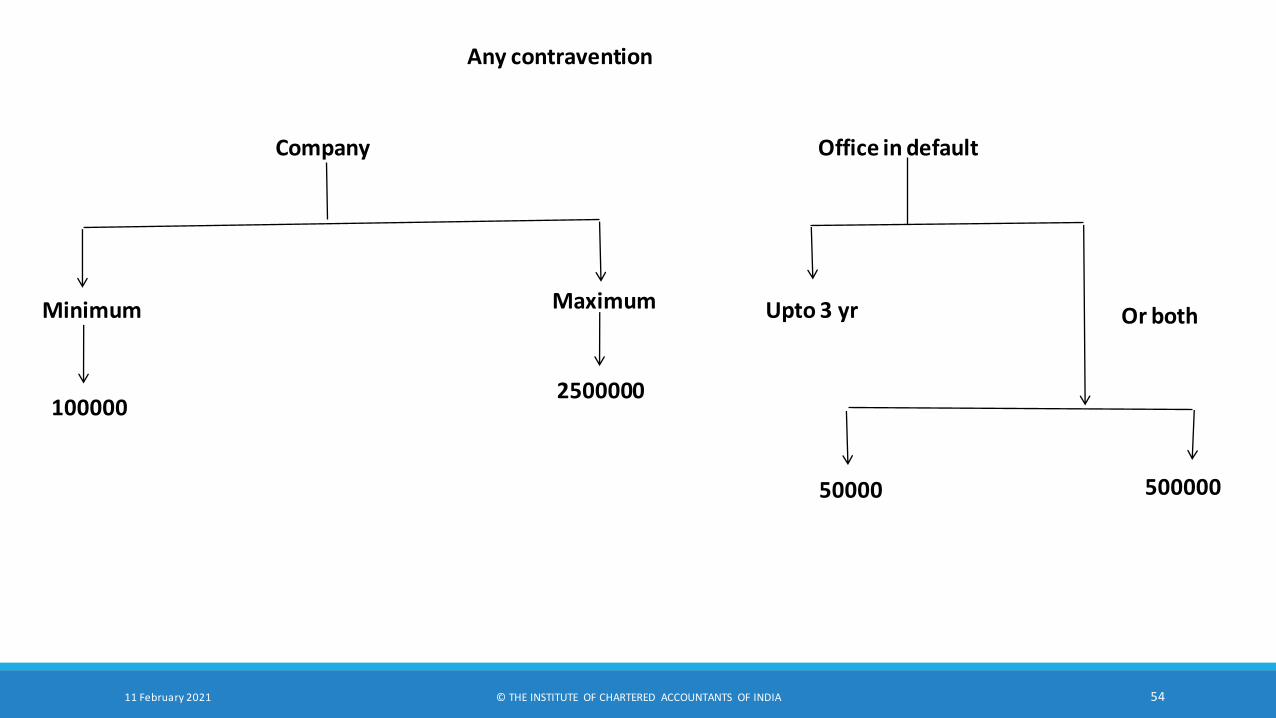

Any contravention

Company Office in default

Minimum Maximum

1000002500000

Upto 3 yr

50000 500000

Or both

Imposition of Restrictions upon Securities (Section 222 of the Companies Act, 2013)

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 55

Where it appears to the tribunal,• In connection with any investigation u/s 216 or• on a complaint made by any person in this behalf,

That there is good reason to find out the relevant facts about any securities issued or to be issued by a company and

• In opinion of Tribunal

•Any such facts cannot be found out unless certain restrictions are imposed,

•The tribunal may, by order, direct that

•The securities shall be subject to such as it may deem fit

•For such period not exceeding 3 yrs as may be specified in the order.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 56

Any contravention

Company Office in default

Minimum Maximum

1000002500000

Upto 6 months

25000 500000

Or both

16. INSPECTOR’S REPORT (SECTION 223 )

Inspector’s report

Interim Only if directed by CG Final

Copy may be obtained By application to CG

Report admissible in any legal proceeding as evidence if authenticated either

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 57

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 58

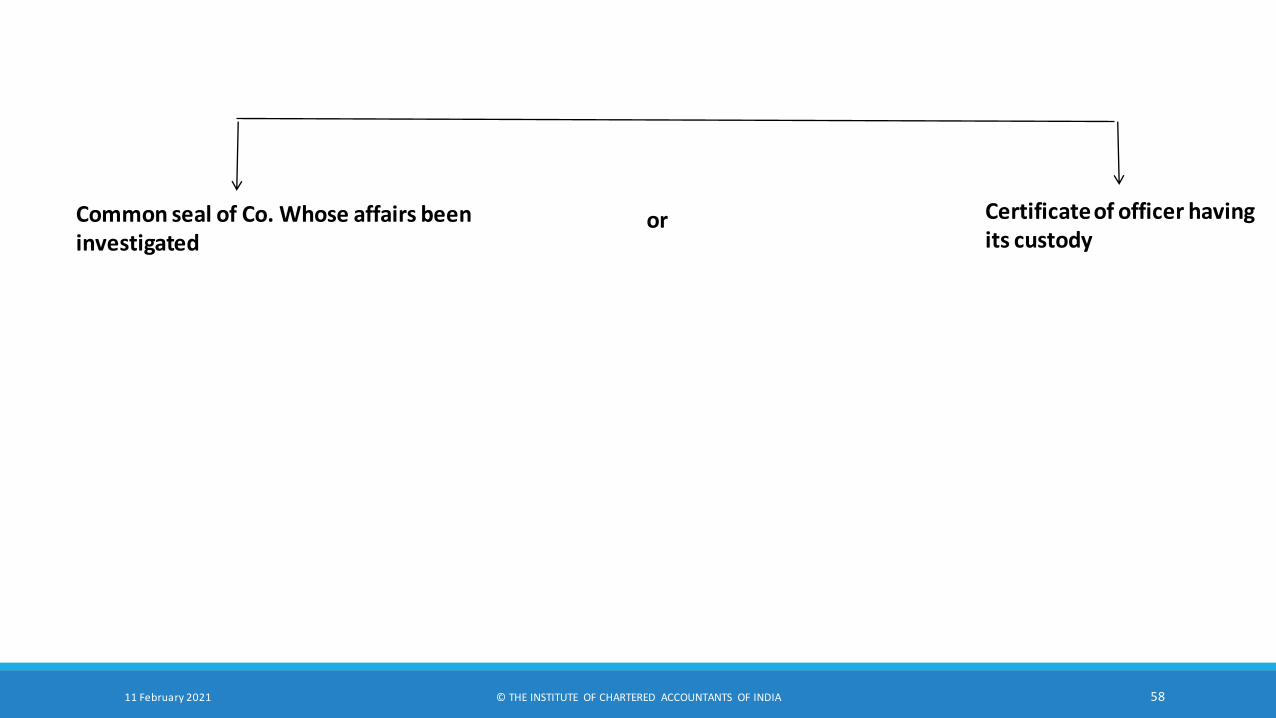

Common seal of Co. Whose affairs been investigated

Certificate of officer having its custody

or

17. ACTIONS TO BE TAKEN IN PURSUANCE OF INSPECTOR’S REPORT (SECTION 224)

Section 224 of the Companies Act, 2013 provides the following provisions in respect of the actions

to be taken in pursuance of inspector’s report:

On basis of report , if person appears to be guilty of offence: If, from an inspector’s report, made under section 223, it appears to the Central Government that any person has, in relation to the company or in relation to any other body corporate or other person whose affairs have been investigated under this Chapter been guilty of any offence for which he is criminally liable, the Central Government may prosecute such person for the offence and it shall be the duty of all officers and other employees of the company or body corporate to give the Central Government the necessary assistance in connection with the prosecution [Sub section (1)].

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 59

Filing of petition by person authorized by the Central Government: As per sub-section (2), if any company or other body corporate is liable to be wound up under this Act or under the Insolvency and Bankruptcy Code, 2016 and it appears to the Central Government from any such report made under section 223 that it is expedient so to do by reason of any such circumstances as are referred to in section 213, the Central Government may, unless the

company or body corporate is already being wound up by the Tribunal, cause to be presented to the Tribunal by any person authorized by the Central Government in this behalf—

◦ a petition for the winding up of the company or body corporate on the ground that it is just and equitable that it should be wound up;

◦ an application under section 241 or

◦ both.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 60

Initiation of winding up proceeding suo moto by the Central Government: As per sub-section (3), if from any such report as aforesaid, it appears to the Central Government that proceedings ought, in the public interest, to be brought by the company or any body corporate whose affairs have been investigated under this Chapter—

◦ for the recovery of damages in respect of any fraud, misfeasance or other misconduct in connection with the promotion or formation, or the management of the affairs, of such company or body corporate; or

◦ for the recovery of any property of such company or body corporate which has been misapplied or wrongfully retained,

the Central Government may itself bring proceedings for winding up in the name of such company or body corporate.

Indemnification to the Central Government: The Central Government, shall be indemnified by such company or body corporate against any costs or expenses incurred by it in, or in connection with, any proceedings brought by virtue of sub-section (3) [Sub section (4)].

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 61

Where fraud has been committed: Where the report made by an inspector states that fraud has taken place in a company and due to such fraud any director, key managerial personnel, other officer of the company or any other person or entity, has taken undue advantage or benefit, whether in the form of any asset, property or cash or in any other manner, the Central Government may file an application before the Tribunal for appropriate orders with regard to disgorgement of such asset, property, or cash, as the case may be, and also for holding such director, key managerial personnel, officer or other person liable personally without any limitation of liability. (Refer example given in section 212)

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 62

18. EXPENSES OF INVESTIGATION (SECTION 225)

Reimbursement of expenses: The expenses of, and incidental to, an investigation by an inspector appointed by the Central Government under this Chapter (Chapter XIV- Inspection, Inquiry and Investigation) other than expenses of inspection under section 214 (Security for

any person who is convicted on a prosecution instituted, or who is ordered to pay damages , or

restore any property in proceedings brought

payment of costs and expenses of investigation) shall be defrayed in the fi rst instance by the Central Government, but shall be reimbursed by the following persons to the extent mentioned below, namely:—

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 63

any person who is convicted on a prosecution

instituted, or who is ordered to pay damages

Reimbursement to the extent that he may in the same proceedings be ordered to pay the said expenses as may be specified by the court convicting such person, or ordering him to pay such damages or restore such property, as the case may be;

Any company or body corporate in whose name proceedings are brought, to the extent of the amount or value of any sums or property recovered by it as a result of such proceedings;

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 64

Where a prosecution is instituted: unless, as a result of the investigation, a prosecution is instituted under section 224,—◦ any company, body corporate, managing director or manager dealt with by the report of

the inspector; and

◦ the applicants for the investigation, where the inspector was appointed under section 213,

to such extent as the Central Government may direct.

Extent of liability: Any amount for which a company or body corporate is liable, shall be a first charge on the sums or property mentioned in that clause.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 65

19. VOLUNTARY WINDING UP OF COMPANY, ETC., NOT TO STOP INVESTIGATION PROCEEDINGS (SECTION 226)

Section 226 of the Companies Act, 2013 provides that an investigation under this Chapter may be initiated notwithstanding, and no such investigation shall be stopped or suspended by reason only of, the fact that—

an application has been made under section 241 (Application to Tribunal for relief in cases of oppression, etc.);

the company has passed a special resolution for voluntary winding up; or

any other proceeding for the winding up of the company is pending before the Tribunal.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 66

Where a winding up order is passed by the Tribunal in a proceeding referred to in clause (c), the inspector shall inform the Tribunal about the pendency of the investigation proceedings before him and the Tribunal shall pass such order as it may deem fit.

Nothing in the winding up order shall absolve any director or other employee of the company from participating in the proceedings before the inspector or any liability as a result of the finding by the inspector.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 67

20. LEGAL ADVISERS AND BANKERS NOT TO DISCLOSE CERTAIN INFORMATION (SECTION 227)

Section 227 of the Companies Act, 2013 provides for non-disclosure of certain information by certain persons.

Nothing in this Chapter shall require the disclosure to the Tribunal or to the Central Government or to the Registrar or to an inspector appointed by the Central Government—

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 68

by a legal adviser, of any privileged communication made to him in that capacity, except as respects the name and address of his client; or

by the bankers of any company, body corporate, or other person, of any information as to the affairs of any of their customers, other than such company, body corporate, or person

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 69

21. INVESTIGATION ETC. OF FOREIGN COMPANIES (SECTION 228)

Section 228 of the Companies Act, 2013 provides for Investigation etc. of foreign companies. According to this section:

The provisions of this Chapter (Chapter XIV- Inspection, Inquiry and Investigation) shall apply

mutatis mutandis to inspection, inquiry or investigation in relation to foreign companies.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 70

22. PENALTY FOR FURNISHING FALSE STATEMENT, MUTILATION, DESTRUCTION OF DOCUMENTS (SECTION 229)

Section 229 of the Companies Act, 2013 lays down the following penalty for furnishing false statement, mutilation, destruction of documents:

Where a person who is required to provide an explanation or make a statement during the course of inspection, inquiry or investigation, or an officer or other employee of a company or other body

corporate which is also under investigation, shall be punishable for fraud in the manner as provided in section 447, if he—

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 71

destroys, mutilates or falsifies, or conceals or tampers or unauthorizedly removes, or is a party to the destruction, mutilation or falsification or concealment or tampering or unauthorized removal of, documents relating to the property, assets or affairs of the company or the body corporate

makes, or is a party to the making of, a false entry in any document concerning the company or body corporate; or

provides an explanation which is false or which he knows to be false,

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 72

TEST YOUR KNOWLEDGE

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 73

As per section 212 of the Companies Act, 2013, the Central Government may assign the investigation into affairs of a company to the Serious Frauds Investigation Office on the basis of an opinion formed from the following:

◦ After the inspection of books of account or papers or inquiry the Registrar shall submit a written report to the Central Government. The report may recommend the need for further investigation along with reasons in support. The Central Government on receipt of such report can order an investigation under Serious Frauds Investigation Office.

◦ The company may pass a special resolution and can request Central Government to investigate into the affairs of the company.

◦ The Central Government can order investigation under Serious Frauds Investigation Office, in public interest.

◦ The departments Central Government and State Governments can request for investigation under Serious Frauds Investigation Office.

Provide various grounds on which the investigation is assigned to Serious Fraud Investigation Office?

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 74

Section 219 states that, if the inspector appointed under Sections 210, 212 or 213 to investigate into the affairs company considers it necessary for the purposes of the investigation to investigate, he can do the investigation of the affairs of otherrelated companies or body corporate with the prior approval of the Central Government.

Holding or Subsidiary Company: which is or has been at the relevant time been the

company’s subsidiary or holding or subsidiary of its holding company;

Related Party: which is or has been at the relevant time been managed by any person as a managing director or manager who is or was at the relevant time the managing director or the manager of the company;

Deemed Control: whose Board of Directors’ comprises nominees of the company or is accustomed to act in accordance with the directions of the company or any of its directors; or

In Employment of Company: in case any person is or has at any relevant time been

the company’s managing director or manager or employee.

The results of the investigation are relevant to the investigation of the affairs of the company for which he is appointed.

Discuss the powers of Inspectors regarding investigation into affairs of related companies

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 75

Section 209, of the Companies Act, 2013 states that, if the Registrar has reasonable ground to believe that the books and papers of

A company or

relating to the key managerial personnel or

any director or

auditor or

company secretary in practice if the company has not appointed a company secretary are likely to be destroyed, mutilated, altered, falsified or secreted he may, after obtaining an order from the special court for the seizure of such books and papers

A group of creditors of XYZ Limited makes a complaint to the Registrar of Companies, Gujarat alleging that the management of the company is indulging in destruction and falsification of the accounting records of the company. The complainants request the Registrar to take immediate steps to seize the records of the company so that the management may not be allowed to tamper with the records. The complaint was received at 11 A.M. on 06th June, 2018 and the registrar has attempted to enter the premise of company but has been denied by the company, due to not having order from special court.Is the contention of company being valid in terms of Companies Act, 2013?

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 76

◦ enter with such assistance as may be required and search the place where such books or papers are kept; and

◦ seize such books and papers as he considers necessary after al lowing the company to take copies or extracts there from.

According the above provisions the registrar may enter, search and seize the books only after obtaining an order from the Special Court.

In the given scenario, the registrar has failed to obtain permission from the special court so, he is not authorized to enter the premises of the company and seize the books of accounts of XYZ Limited. Hence, the contention of the XYZ Limited is valid in law

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 77

The provision of Section 218 states that, the company shall require to take approval of the tribunal before taking action against the employee if there is any pendency of any proceedings against any person concerned in the conduct and management of the affairs of the company.

The company shall require approval in the following circumstances:

discharge or suspension of an employee; or

punishment to an employee by dismissal, removal, reduction in rank or otherwise; or

Mr. Atul is an employee of the company ABC Limited and investigation is going on him under the provisions of Companies Act, 2013. The company wants to terminate the employee on the ground of investigation is going against him. They have filed the application to tribunal for approval of termination. Company has not received any reply from the tribunal within 30 days of filling an application. The company consider it as a deemed approval and terminated Mr. Atul.Is the contention of company being valid in law?What is remedy available to Mr. Atul?What is remedy available to Mr. Atul, if reply of Tribunal has been received within 30 days of application?

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 78

change in the terms of employment to the disadvantage of employee(s); The Tribunal shall notify its objection to the action proposed in writing.

In case, the company, other body corporate or person concerned does not receive the approval of the Tribunal within 30 days of making the application, it may proceed to take the action proposed against the employee. That means it can be consider as a deemed approval by the tribunal.

Appeal to the Appellate Tribunal

If the company, other body corporate or person concerned is dissatisfied with the objection raised by the Tribunal, it may, within a period of 30 days of the receipt of the notice of the objection, refer an appeal to the Appellate Tribunal in such manner and on payment of fees of INR 1,000 as per the schedule of Fees.

The decision of the Appellate Tribunal on such appeal shall be final and binding on the Tribunal and on the company, other body corporate or person concerned.

◦ Yes, the termination of Mr. Atul made by the company is totally valid in law and company can do so by considering deemed approval of tribunal.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 79

◦ In this scenario, Mr. Atul has not any remedy available. As per the provision of the law appeal to the appellate tribunal can be made only if the person is dissatisfied with the objection raised by the tribunal. Hence, in this case the tribunal has not replied Mr. Atul cannot refer an appeal to Appellate Tribunal.

◦ In this case, Mr. Atul can refer and appeal to appellate tribunal within 30 days o f the receiving letter of objection raised bythe tribunal and with payment of Fees on 1,000 as per schedule of Fees

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 80

A group of shareholders of M/s. FMG Limited made a complaint to the concerned Registrar of Companies (RoC) that the business of the Company is being carried on for unlawful and fraudulentpurposes and filed an application to enquire into the affairs of the Company. Referring to and analyzing the provisions of the Companies Act, 2013, decide:

Whether the RoC has the power to order for an inquiry into the affairs of the Company?

If yes, state the procedure to be followed by the RoC.

Whether the inquiry should be pursued by the RoC in case the complaint is withdrawn by the same group of shareholders subsequent to the Order for enquiry?

Whether the Central Government has the power to direct the RoC to carry out the inquiry?

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 81

Yes, the RoC has the power to order for an inquiry as he deems fit after providing the company a reasonable opportunity of being heard, into the affairs of the company if he is satisfied on a representation made to him by any person that the business of a company is being carried on for a fraudulent or unlawful purpose or not in compliance with the provisions of this Act. [Section 206(4) of the Companies Act, 2013]

Procedure followed by RoC: The Registrar may, after informing the company of the allegations made against it by a written order, call on the company to furnish in writing any information or explanation on matters specified in the order within such time as he may specify therein and carry out such inquiry as he deems fit after providing the company a reasonable opportunity of being heard.

The inquiry can be pursued by the ROC in case the complaint is withdrawn by same group of shareholders subsequent to the order for inquiry in terms of section 206(4).

Yes, the Central Government may, if it is satisfied that the circumstances so warrant, direct the Registrar for the purpose to carry out the inquiry under section 206(4).

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 82

Chapter 4: Inspection, Inquiry & Investigation (Sec 206-229)

Sec 209: Search and Seizure

A group of creditors of Mac Trading Limited makes a complaint to the Registrar of Companies, Hyderabad alleging that the management of the company is indulging in destruction and falsification of the accounting records of the company. The complainants request the Registrar to take immediate steps to seize the records of the company so that the management may not be allowed to tamper with the records. The complaint was received at 10 A.M. on 1st July 2015 and the ROC entered the premises at 10.30 A.M. for the search. Examine the powers of the Registrar to seize the books of the company.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 83

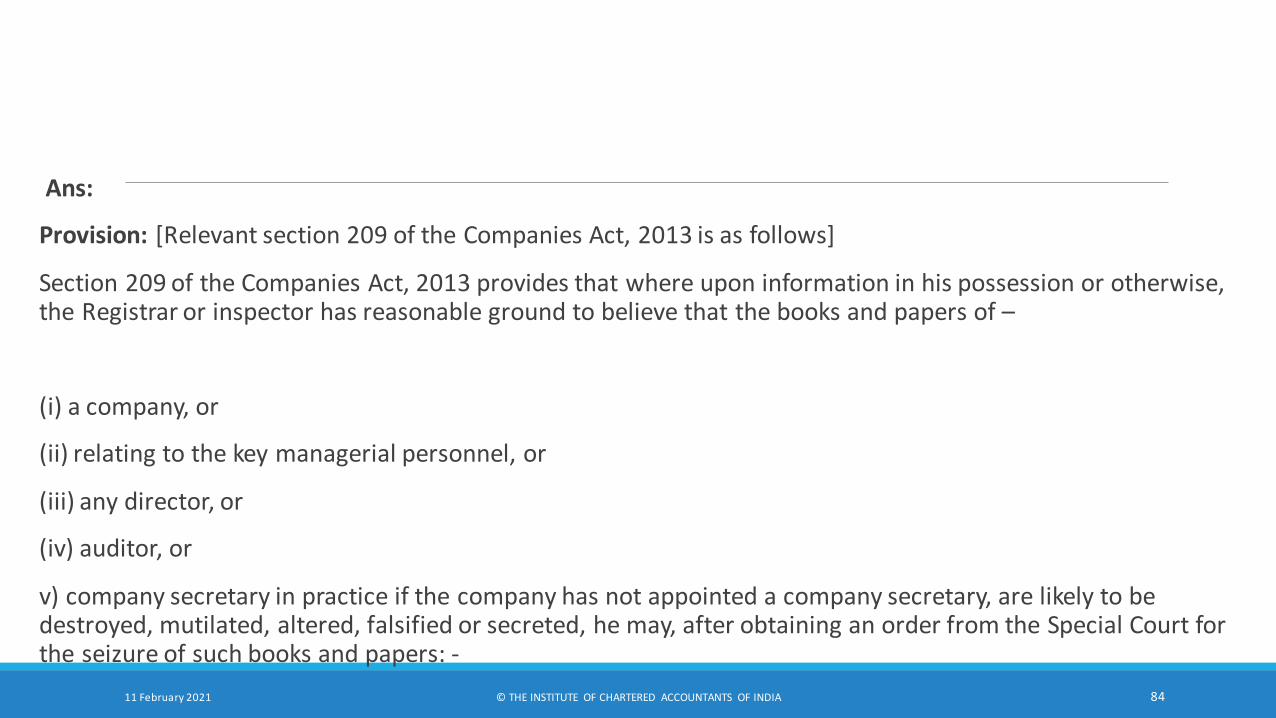

Ans:

Provision: [Relevant section 209 of the Companies Act, 2013 is as follows]

Section 209 of the Companies Act, 2013 provides that where upon information in his possession or otherwise, the Registrar or inspector has reasonable ground to believe that the books and papers of –

(i) a company, or

(ii) relating to the key managerial personnel, or

(iii) any director, or

(iv) auditor, or

v) company secretary in practice if the company has not appointed a company secretary, are likely to be destroyed, mutilated, altered, falsified or secreted, he may, after obtaining an order from the Special Court for the seizure of such books and papers: -

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 84

a. enter, with such assistance as may be required, and search, the place or places where such books or papers are kept; and

b. seize such books and papers as he considers necessary after allowing the company to take copies of, or ex-tracts from, such books or papers at its cost.

Explanation and Answer:

According to the above provisions, Registrar may enter and search the place where such books or papers are kept and seize them only after obtaining an order from the Special Court.

Since in the given question, Registrar entered the premises for the search and seizure of books of the company with-out obtaining an order from the Special Court, he is not authorised to seize the books of the Mac Trading Limited.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 85

The Registrar of Companies, West Bengal has received a complaint from a group of creditors of a Company, in order to prevent the unearthing of their embezzlement of company’s funds, are engaged in falsification and destruction of original accounting books and records. The complaints urged the Registrar seize the accounting books and records of the company so that the Directors may not be able to tamper the same. You are required to state the powers, if any, of the Registrar in this respect.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 86

Ans:

Provision: [Relevant section 209 of Companies Act, 2013]

If the ROC is of the following opinion it can seize the books of the company or any officer of the company:

a. The book will be destroyed.

b. The book will be mutilated.

c. The book will be altered.

d. The book will be falsified.

e. The book will be secreted.

On the basis of the above facts the ROC can seize the books as per following process:

1. ROC shall take prior approval of the special court for seizure of books.

2. Enter the premises or places where the books are kept.

3. Allow the company to take the copies, extracts of the books first. The cost of the same shall be borne by company

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 87

Seize the books of the company after company finished to take the copies of the same.

Explanation &Answer:

In the given case, The Registrar of Companies, West Bengal has received a complaint from a group of creditors of a Company regarding embezzlement of company’s funds, falsification and destruction of original accounting books and records; if the complaint is found true the ROC has power to seize the books by following the above mentioned process.

Suggestion: The ROC shall return the books to the company within 180 days of seizure. If the ROC further requires the books it can call the books for further 180 days by making an order in writing.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 88

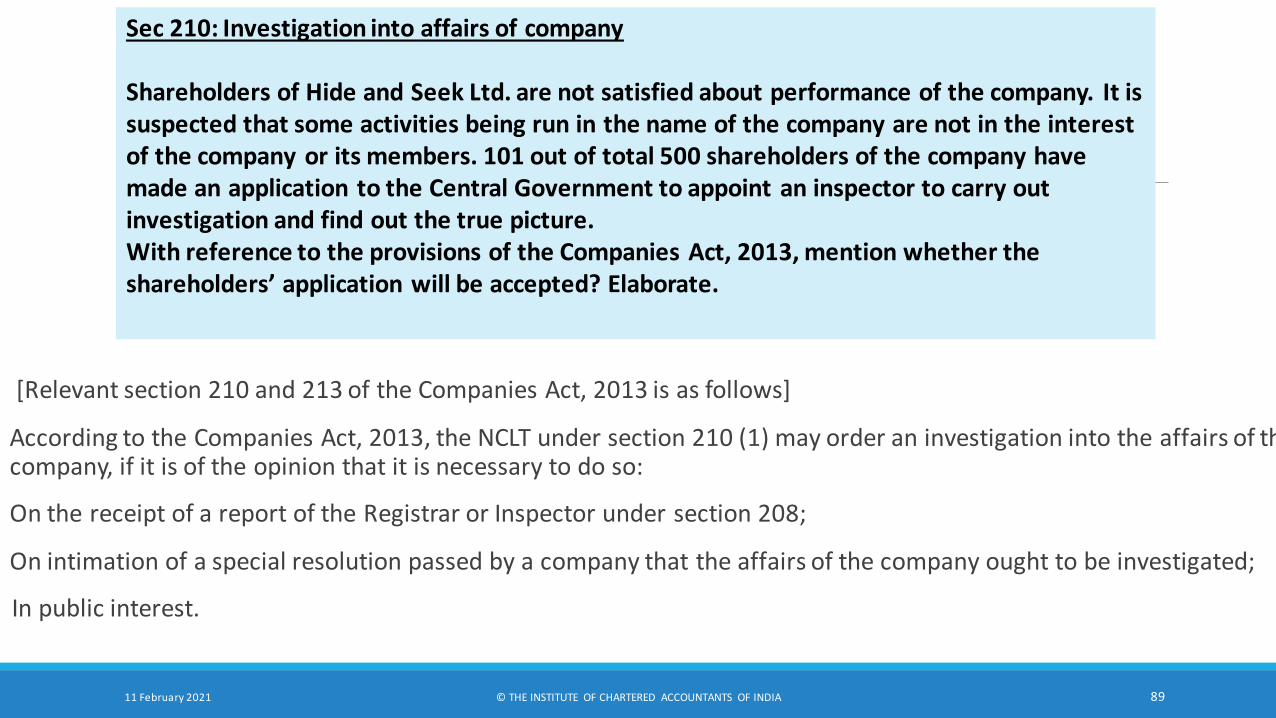

[Relevant section 210 and 213 of the Companies Act, 2013 is as follows]

According to the Companies Act, 2013, the NCLT under section 210 (1) may order an investigation into the affairs of the company, if it is of the opinion that it is necessary to do so:

On the receipt of a report of the Registrar or Inspector under section 208;

On intimation of a special resolution passed by a company that the affairs of the company ought to be investigated;

In public interest.

Sec 210: Investigation into affairs of company

Shareholders of Hide and Seek Ltd. are not satisfied about performance of the company. It is suspected that some activities being run in the name of the company are not in the interest of the company or its members. 101 out of total 500 shareholders of the company have made an application to the Central Government to appoint an inspector to carry out investigation and find out the true picture.With reference to the provisions of the Companies Act, 2013, mention whether the shareholders’ application will be accepted? Elaborate.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 89

According to section 210 (3) of the Companies Act, 2013, the NCLT may appoint one or more persons as inspectors to investigate into the affairs of the company and to report thereon in such manner as the NCLT may direct.

The shareholders’ application will not be accepted as under 210 of the Companies Act, 2013, NCLT may order an investigation into affairs of the company on the intimation of a special resolution passed by a company that the affairs of the company ought to be investigated and then may appoint the inspectors.

As per section 213 of the Companies Act, 2013, The Tribunal may:

On an application made by-◦ Not less than One Hundred members or members holding not less than one tenth of the voting power, in the case of

a company having a share capital; or

◦ Not less than one fifth of the persons on the company’s register of members, in the case of a company having no share capital,

and supported by such evidence as may be necessary for the purpose of showing that the applicants have good reasons for seeking an order for conducting an investigation into the affairs of the company; or

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 90

On an application made to it by any other person or otherwise, if it is satisfied that there are circumstances suggesting that-

◦ The business of the company is being conducted with intent to defraud its creditors, members or any other person or otherwise for a fraudulent or unlawful purpose or in a manner oppressive to any of its members or that the company was formed for any fraudulent or unlawful purpose;

◦ Persons concerned in the formation of the company or the management of its affairs have in connection therewith been guilty of fraud, misfeasance or other misconduct towards the company or towards any of its members, or

◦ The members are not provide with the sufficient information regarding payment of the remuneration or commission to managerial personnel

Order, after reasonable opportunity of being heard to the parties concerned. The investigation will be conducted by one or more inspector appointed by the CG for investigation. The CG will also state the manner under which the investigation shall be conducted.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 91

Explanation and Answer

In the present case, 101 out of total 500 shareholders of the company have made an application to the NCLT to appoint an inspector to carry out investigation but it is not sufficient as the company has not passed the special resolution.

Note: in Old Act, applications were made to CG, but in the new Act, applications are made to NCLT under 2013 and to CG with special resolution in 210. So now the question will ask on NCLT rather than CG.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 92

Ans:

Provision: [Relevant section 210 and 213 of the Companies Act, 2013 as follows]

The NCLT may order the investigation of the company based on the following points.

On the report made by inspector or ROC u/s 208. The ROC or inspector can also make the recommendation for investigation under the inspection report made u/s 208.

If the members passes the GM-SR for conduct of the investigation in their own company

A majority of the Board of directors of M/s High Value Infotech Ltd. have realised that some of the business activities carried out in the name of the company are not in the interest of either the company or its members. They want that the company should make an application to the NCLT to appoint an Inspector to carry out investigation and find out the whole truth. Explain the steps that should be taken to achieve the purpose and draft the application under the Companies Act, 2013

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 93

NCLT may suo motu start investigation in the company in public interest

Where an order is passed by a court or the Tribunal in any proceedings before it that the affairs of a company ought to be investigated, the Central Government shall order an investigation into the affairs of that company.

As per section 213 of the Companies Act, 2013, The Tribunal may:

c. On an application made by-◦ Not less than One Hundred members or members holding not less than one tenth of the voting power, in the case

of a company having a share capital; or◦ Not less than one fifth of the persons on the company’s register of members, in the case of a company having no

share capital,

and supported by such evidence as may be necessary for the purpose of showing that the applicants have good reasons for seeking an order for conducting an investigation into the affairs of the company; or

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 94

On an application made to it by any other person or otherwise, if it is satisfied that there are circumstances suggesting tha t-

The business of the company is being conducted with intent to defraud its creditors, members or any other person or otherwise for a fraudulent or unlawful purpose or in a manner oppressive to any of its members or that the company was formed for any fraudul ent or unlawful purpose;

Persons concerned in the formation of the company or the management of its affairs have in connection therewith been guilty o f fraud, misfeasance or other misconduct towards the company or towards any of its members, or

The members are not provide with the sufficient information regarding payment of the remuneration or commission to managerialpersonnel

Order, after reasonable opportunity of being heard to the parties concerned. The investigation will be conducted by one or mo re inspector appointed by the CG for investigation. The CG will also state the manner under which the investigation shall be conducted.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 95

Explanation:

In the given case, the majority of directors are already of the view that the affairs of the company are not conducted in a manner beneficial either to the company or to the members and want to make an application to the NCLT to appoint an inspector.

Therefore, the steps to be carried out for the purpose will be as under:

Convene an Extraordinary General Meeting of members for passing the required special resolution. The provisions for convening the meeting should be complied with and the explanatory statement with the notice of the meeting must provide full details of the proposed special resolution.

Once the special resolution is passed, a copy of it along with the copy of the notice should be filed with the Registrar;

An application should be made under section 210 (1) to the NCLT requesting it to appoint an inspector to investigate the affairs of the company.

The NCLT on receipt of such notice will ask for information, documents and other supporting evidence and may order an investigation only if it is of the opinion that an investigation is warranted. It may appoint one or more inspectors to investigate into the affairs of the company and to report thereon in such manner as it may direct.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 96

Draft of application:

High Value InfoTech Ltd. (Address) Date:

The Secretary,

Ministry of Corporate Affairs, New Delhi

Sir,

At a meeting of the shareholders of the company held on at , The members have passed the following resolution as a Special Resolution:

“Resolved that the NCLT be approached to appoint one or more Inspector to carry out an investigation into the affairs of the company to determine whether the activities in

The name of the Company is being carried on in a manner which is against the interest of either the company or its members.

Resolved further that the Board of Directors be and is hereby authorized to make necessary application to the Central Government for this purpose and submit the necessary documents and information as may be required by the Central Government in this regard.”

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 97

The above referred special resolution was passed at an extraordinary general meeting of the company held on………….

It is, therefore, prayed that the Central Government be pleased to appoint as per section 210 of the Companies Act, 2013, an inspector to investigate the affairs of the company regarding the matters mentioned in the above resolution and communicate its decision to the company.

Yours faithfully,

For and on behalf of High Value InfoTech Ltd. Secretary

Note: in Old Act, applications were made to CG, but in the new Act, applications are made to NCLT under 2013 and to CG with special resolution in 210. So now the question will ask on NCLT rather than CG.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 98

Ans:

Provision: [Relevant section 212 of the Companies Act, 2013 is as follows]

According to Section 212(6) of the Companies Act, 2013, notwithstanding anything contained in the Code of Criminal Procedure, 1973 (2 of 1974), offence covered under section 447 shall be cognizable and no person accused of any offence under those sections shall be released on bail or on his own bond unless—

Sec 212: Investigation into affairs of company by Serious Fraud Investigation Office

Mrs. Preeti, a lady aged about 32 years and Managing Director of M/s Grow more plantations Ltd., has been arrested for an offence covered under section 447 of the Companies Act, 2013 on a complaint made by the Director, Serious Fraud Investigation Officer. Mrs. Preeti seeks your legal advice as to the conditions under which she can be released on bail and the role of Special Court in this regard.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 99

the Public Prosecutor has been given an opportunity to oppose the application for such release; and

where the Public Prosecutor opposes the application, the court is satisfied that there are reasonable grounds for believing that he is not guilty of such offence and that he is not likely to commit any offence while on bail.

A person, who, is under the age of sixteen years or is a woman or is sick or infirm, may be released on bail, if the Special Court so directs.

The Special Court shall not take cognizance of any offence referred to this sub-section except upon a complaint in writing made by—

◦ the Director, Serious Fraud Investigation Office; or

◦ any officer of the Central Government authorised, by a general or special order in writing in this behalf by that Government.

◦ -

Explanation and Answer:

In the instant case, Mrs. Preeti has been arrested for an offence covered under section 447 of the Act on a complaint made bythe Director, SFIO.

As Mrs.Preeti is a woman, she may be released on bail if the Special Court so directs

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 100

Ans:

Provision: [Relevant section 222 of the Companies Act, 2013 is as follows]

Where it appears to the NCLT, in connection with any investigation under Section 216 of the Companies Act, 2013 or on a complaint made by any person in this behalf, that there is good reason to find out the relevant facts any securities issued or to be issued by the company and the Tribunal is of the opinion that such facts cannot be found out unless certain restrictions as it may deem fit are imposed, the Tribunal may, by order, direct that the securities shall be subject to such restrictions as it may deem fit for such period not exceeding 3 years as be specified in the order.

Sec 216: Investigation of ownership of company

Remedial Pharma Limited, over the years, enjoys a high reputation in the market and its general reserves are ten times more than the paid up capital of the company. There is a serious apprehension of cornering the share of the company by a group of unscrupulous persons likely to result in change in the Board of directors which may be prejudicial to the public interest. The company seeks your advice as to how it can block the transfer of shares of the company under the provisions of the Companies Act, 2013.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 101

Where securities in any company are issued or transferred or acted upon in contravention of an order of the Tribunal under sub section (1), the company shall be punishable with fine which shall not less than one lakh rupees but which may extend to 25 lakh rupees and every officer of the company who is in default shall be punishable with imprisonment for a term which may extend to 6 months or with fine which shall not be less than twenty five thousand rupees but which may extend to 5 lakh rupees or with both. [Section 222(2)]

Explanation and Answer:

The facts given in the question squarely fall within the provision of Section 222 of the Companies Act, 2013. The management of Remedial Pharma Limited may make a complaint to the NCLT and convince that the transfer of shares in favour of the group of unscrupulous persons would change the composition of the Board of directors of the company which shall be prejudicial to the public interest and if the NCLT is convinced with the pleas of the company, it may pass an order as stated above which would block the transfer of shares as stated in the question.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 102

Ans:

Provision: [Relevant section 218 of the Companies Act, 2013 is as follows]

Section 218 of the Act deals with the Protection of Employees during Investigation and relevant provisions are as under:

Approval of tribunal to take action against the employee: Notwithstanding anything contained in any other law for the time being in force, if –

Sec 218: Protection of employees during investigation

Damage Ltd, the Company wanted to suspend Mr. Z, the CFO of the Company during the pendency of an investigation being conducted under the provisions of the Companies Act, 2013 on the order of Tribunal. The Company approached the Tribunal on 3rd January, 2017 for the proposed action. The Company on 15th February, 2017 passed an order of suspension without waiting for the orders from Tribunal. Comment upon the action taken by the Company with reference to the relevant provisions of the Act.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 103

during the course of any investigation of the affairs and other matters of or relating to a company, other body corporate or person under section 210,section 212, section 213 or section 219 or of the membership and other matters of or relating to a company, or the ownership of shares in or debentures of a company or body corporate, or the affairs and other matters of or relating to a company, other body corporate or person, under section 216; or

during the pendency of any proceeding against any person concerned in the conduct and management of the affairs of a company under Chapter XVI, such company, other body corporate or person proposes –

to discharge or suspend any employee; or

to punish him whether by dismissal, removal, reduction in rank or otherwise; or

to change the terms of employment to his disadvantage the Company, other body corporate or person, as the case may be shall obtain approval of the Tribunal of the action proposed against the employee and if the Tribunal has any objection to the action proposed, it shall send by post notice thereof in writing to the Company, other body corporate or person concerned.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 104

Action against employee: if the company, other body corporate or person concerned does not receive within thirty days of making of application under sub-section (1), the approval of the Tribunal, then the only then, the company, Other body corporate or person concerned may proceed to take against the employee, the action proposed.

Explanation and Answer:

In the instant case, the action taken by Damage Ltd. to suspend Mr. Z, the CFO of the company is valid as the company approached the Tribunal on 3rd January, 2017 for the proposed action and on 15th February, 2017 passed an order of suspension without waiting the orders from Tribunal (after 30 days of marking the application)

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 105

Ans:

Provision: [Relevant section 218 of Companies Act, 2013] It may happen that:

◦ during the course of any investigation of the affairs and other matters of or relating to a company, other body corporate or person under section 210 or section 212 or section 213 or of section 219 or of the membership and other matters of or relating to a company, or the ownership of shares in or debentures of a company or body corporate, or the affairs and other matters of or relating to a company, body or person, under section 216; or

◦ during the pendency of any proceeding against any person concerned in the con-duct and management of the affairs of a company under Chapter XVI, such company, body or person may propose—

An inspector was appointed under Section 210 of the Companies Act, 2013 to investigate the affairs of a public company. Mr. WM, the works manager of the company, who is aware of certain misdeeds of the management, desires to know whether he is entitled to any protection against dismissal by the company, if he discloses the misdeeds during the course of examination by the inspector. Advise him explaining the relevant provisions of the Companies Act, 2013.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 106

◦ to discharge or suspend any employee; or

◦ to punish, whether by dismissal, removal, reduction in rank or otherwise, any employee, or

◦ to change the terms of employment to employee’s disadvantage.

In any of the above cases, the approval of the Tribunal will be required and if the Tribunal has any objection to the action proposed, it shall send by post notice thereof in writing to the company, other body corporate or person concerned.

If the company, other body corporate or person concerned does not receive within thirty days of the making of the application, any notice of the objection from the Tribunal, then and only then, the company other body corporate or person concerned may proceed to take against the employee, the action proposed.

Answer:

In the given case, Mr. WM, the works manager of the company shall have above mentioned protection against dis- missal by the company.

Suggestion:

If the company, other body corporate or person concerned is dissatisfied with the objection raised by the Tribunal, it may, within a period of thirty days of the receipt of the notice of the objection, prefer an appeal to the Appellate Tribunal.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 107

Ans:

Provision: [Relevant section 219 of the Companies Act, 2013 as follows]

According to section 219 of the Companies Act, 2013, if an inspector appointed under section 210 or section 212 or section 213 to investigate into the affairs of a company considers it necessary for the purposes of the investigation,

can also investigate the affairs of—

any other body corporate which is, or has at any relevant time been the company’s subsidiary company or holding company, or a subsidiary company of its holding company

219: Investigation in related companies

What are the circumstances in which an inspector appointed under section 210 of the Companies Act, 2013, can investigate into affairs of related companies also?

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 108

• any other body corporate which is, or has at any relevant time been managed by any person as managing di- rector or as manager, who is, or was, at the relevant time, the managing director or the manager of the company;

• any other body corporate whose Board of Directors comprises nominees of the company or is accustomed to act in accordance with the directions or instructions of the company or any of its directors; or

any person who is or has at any relevant time been the company’s managing director or manager of employee, he shall, subject to the prior approval of the Central Government, investigate into and report on the affairs of the other body corporate or of the managing director or manager, in so far as he considers that the results of his investigation are relevant to the investigation of the affairs of the company for which he is appointed

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 109

Ans:

Provision: [Relevant section 219 of the Companies Act, 2013 is as follows]

Section 219 of the companies Act, 2013, provides for power of Inspector to conduct investigation into the affairs of related companies etc., if an inspector appointed under section 210 or section 212 or section 213 to investigate into the affairs of a company considers it necessary for the purposes of the investigation, to investigate also the affairs of:

any other body corporate which is, or has at any relevant time been the company’s subsidiary company or holding company, or a subsidiary company of its holding company;

any other body corporate which is, or has at any relevant time been managed by any person as managing director or as manager, who is, or was, at the relevant time, the managing director or the manager of the company;

During investigations conducted on the affairs of a company in the public interest, the inspector observed that the Directors of the company had been acting on the instructions of the holding company and he proceeded to investigate the holding company. Is Inspector permitted to do under the provisions of the Companies Act, 2013?

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 110

any other body corporate whose Board of Directors comprises nominees of the Company or is accustomed to act in accordance with the directions or instructions of the company or any of its directors; or

any person who is or has at any relevant time been the company’s managing director or manager of employee, he shall, subject to the prior approval of the Central Government, investigate into and report on the affairs of the other body corporate or of the managing director or manager, in so far as he considers that the results of his investigation are relevant to the investigation of the affairs of the company for which he is appointed.

Therefore, the inspector shall subject to the prior approval of the Central Government, investigate into and report on the affairs of the other body corporate or of the Managing Director or Manager, in so for as he considers that the results of his investigation is relevant to the investigation of the affairs of the Company for which he is appointed.

Explanation and Answer:

By applying the above provision of the Act, the Inspector is permitted to investigate the holding company

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 111

Ans:

Provision: [Relevant section 223 of the Companies Act, 2013 as follows]

Section 223 of the Companies Act, 2013 deals with Inspector’s report. The following provisions are applicable in respect of the Inspector’s report on investigation:

Submission of interim report and final report [Sub section (1)]: An inspector appointed under this Chapter (Chapter XIV- Inspection, Inquiry and Investigation) may, and if so directed by the Central Government shall, submit interim reports to that Government, and on the conclusion of the investigation, shall submit a final report to the Central Government.

Report to be writing or printed [Sub section (2)]: Every report made under sub section (1) above, shall be in writing or printed as the Central Government may direct.

223: Inspector’s report / Investigation Report

What are the duties of the inspector as enumerated in section 223 of the Companies Act, 2013, in relation to his report.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 112

Obtaining copy or report [Sub section (3)]: A copy of the above report may be obtained by making an application in this regard to the Central Government.

Authentication of report [Sub section (4)]: The report of any inspector appointed under this Chapter shall be authenticated either—

◦ by the seal of the company whose affairs have been investigated; or

◦ by a certificate of a public officer having the custody of the report, as provided under section 76 of the Indian Evidence Act, 1872, and such report shall be admissible in any legal proceeding as evidence in relation to any matter contained in the report.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 113

Ans:

Provision: [Relevant section 224 of Companies Act, 2013]

If, from an inspector’s report made under section 223, it appears to the Central Government that any person has been guilty of any offence for which he is criminally liable, in relation to the company or in relation to any other body corporate or other person whose affairs have been investigated, the Central Government may prosecute such person for the offence.

224: Actions to be taken in pursuance of inspector’s report / Order against investigation by CG. The report submitted by the inspector appointed under Section 210/213 of the Companies Act, 2013

to investigate the affairs of a Company revealed that substantial funds of the Company have been misappropriated by the Managing Director of the Company. The Central Government is of the opinion that effective action may not be taken the company for recovery of the funds misappropriated by the Managing Director. Examine with reference to the provisions of the Companies Act, 2013 the action that can be taken by the Central Government for recovery of damages or funds misappropriated by the Managing Director.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 114

It shall be the duty of all officers and other employees of the company or body corporate to give the Central Government the necessary assistance in connection with the prosecution.

If CG is of the opinion that the company shall be wound up as per report of sec 223 of the inspector, the CG may present to tribunal:

◦ a petition for the winding up of the company or body corporate on the ground that it is just and equitable that it should be wound up, or

◦ an application for relief from oppression etc. [See section 241]; or◦ Both. [Section 224(2)]

If such company is already under winding up as per tribunal then the question of above application by CG will not arise.

The CG may order winding up in the following situations:

for the recovery of damages in respect of any fraud, misfeasance or other misconduct in connection with the promotion or formation, or the management of the affairs, of such company or body corporate; or

for the recovery of any property of such company or body corporate which has been misapplied or wrongfully retained

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 115

The Central Government shall be indemnified by such company or body corporate against any costs or expenses incurred by it in, or in connection with, any proceedings brought by virtue of sub-section (3).

If a report made by an inspector states that:

fraud has taken place in a company; and

due to such fraud any director, KMP, other officer of the company or any other person or entity has taken undue advantage or benefit whether in the form of any asset, property or cash or in any other manner, the Central Govt. may file an application before the Tribunal for:

Appropriate orders with regard to disgorgement of such asset, property or cash; and

Holding such director, KMP, other officer of the company or any other person or entity liable personally without any limitation of liability.

Explanation &Answer:

In the given case, above actions can be taken by the Central Government for recovery of damages or funds misappropriated by the Managing Director.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 116

© THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

MCQ’S

11 February 2021 117

Q-1 Offences covered u/s 447 of this Act shall be cognizable and no person accused of any such offence shall be released on bail. However, on the direction of Special court, following person may be released on bail.

A) under the age of 16 years

B) a women

C) sick or infirm person

D) any of the above

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 118

Q-2 What is the circumstance in which notice can be served for inspection of books etc. u/s 206(3) of Companies Act, 2013

A) If no information or explanation is furnished to the Registrar which in the time specified u/s 206(1)

B) If the Registrar on an examination of the documents furnished is of the opinion that the information or explanation furnished is inadequate

C) If the Registrar is satisfied on a scrutiny of the documents furnished that an unsatisfactory state of affairs exists in the company and the company and the information or documents do not disclose a full and fair statement of the information required.

D) Al of the above.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 119

Q-3 Which of the following persons can be appointed as inspector u/s 215 of Companies Act, 2013?

A) Individual

B) Firm

C) Body Corporate

D) Any of the above

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 120

Q-4 A notice was sent to Mr. Left by the registrar to furnish the information related to a business transacted during his tenure in the X company. Mr. Left ignored the notice considering that he is no more an employee of X company. Choose the right option in the light of the Companies Act, 2013

A) Mr. Left is liable to provided such information.

B) Officer in place of Mr. Left is liable to provide such information.

C) Company is liable to provide such information.

D) None of the above.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 121

Q-5 Who has the power to call for information, insect books and conduct inquires u/s 206 of the Companies Act, 2013

A) Ministry of Corporate Affairs

B) Registrar of companies

C) National Company Law Tribunal

D) Central Government

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 122

Q_6 Mrs. Preeti, a lady aged about 32 years and Managing Director of M/s Growmore plantations Ltd., has been arrested for an offence covered under section 447 of the Companies Act, 2013 on a complaint made by the Director, Serious Fraud Investigation Officer. Mrs. Preeti seeks your legal advise as to the conditions under which she can be released on bail.

A) She can be released on bail on the direction of Supreme Court.

B) She can be released on bail on the direction of Special Court.

C) She can be released on bail on the direction of High Court.

D) She can't be released on bail.

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 123

Q-7 Central Government may order an investigation into the affairs of the company in certain circumstances except:

A) On the receipt of a report of the Registrar or Inspector u/s 208

B) on intimation of a special resolution passed by a company that the affairs of the company ought to be investigated

C) on intimation of a board resolution passed by a Board of a company that the affairs of the company ought to be investigated

D) in public interest

11 February 2021 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 124