final report - infoterreinfoterre.brgm.fr/rapports/rp-55008-fr.pdf · 2007-10-31 · sapm and gig)....

TRANSCRIPT

,706 13 O

/v. H O L I W A S T - Deliverable D O - 4 aFirst m a n a g e m e n t report

\ Final Report

BRGM/RP-55008-FR- April, 2007

GtoícifBCtfwi sustsíiublí Earth

brgm

Holiwast First Management Report

European Commission

PRIORITY [policy-oriented research priority SSP/8.1]

SPECIFIC TARGETED R E S E A R C H O R INNOVATION PROJECT

HOLIWAST

Holistic assessment of waste management technologies.

Contract number: 006509

April 16th, 2007

First Management Report

and

Report on the distribution of the Community'scontribution

Period covered by the report: 1sl August 2005 to 31st July 2006

Sections included: 1 to 3

N a m e of the co-ordinator: Jacques Villeneuve

Project h o m e page: http://holiwast.bram.fr

1/36

Holiwast First Management Report

2/36

Holiwast First Management Report

2/36

Holiwast First Management Report

CONTENTS

MANAGEMENT REPORT 5

1. SECTION 1: JUSTIFICATION OF MAJOR COST ITEMS AND RESOURCES 5

1 .1 . Description of the work performed by each contractor 51.1.1. BRGM 51.1.2. Ecologie 61.1.3. SAPl^ 61.1.4. TU Vienna 81.1.5. ULund 101.1.6. 2.-0 LCA 101.1.7. GIG 11

1.2. Explanatory note ON MAJOR COST ITEMS 121.3. Overview OF COSTS 131.4. Overview OF PERSON-MONTHS 141.5. Impact OF MAJOR DEVIATIONS 14

2. SECTION 2: FORM C FINANCIAL STATEMENT 17

2.1. BRGM 172.2. ECOLOGIC 192.3. SAPM 212.4. TU Vienna 232.5. ULUND 252.6. 2.-0 LCA 272.7. GIG 29

3. SECTION 3: SUMMARY FINANCIAL REPORT 31

REPORT ON THE DISTRIBUTION OF THE COMMUNITY'S CONTRIBUTION 34

3/36

Holiwast First Management Report

CONTENTS

MANAGEMENT REPORT 5

1. SECTION 1: JUSTIFICATION OF MAJOR COST ITEMS AND RESOURCES 5

1 .1 . Description of the work performed by each contractor 51.1.1. BRGM 51.1.2. Ecologie 61.1.3. SAPl^ 61.1.4. TU Vienna 81.1.5. ULund 101.1.6. 2.-0 LCA 101.1.7. GIG 11

1.2. Explanatory note ON MAJOR COST ITEMS 121.3. Overview OF COSTS 131.4. Overview OF PERSON-MONTHS 141.5. Impact OF MAJOR DEVIATIONS 14

2. SECTION 2: FORM C FINANCIAL STATEMENT 17

2.1. BRGM 172.2. ECOLOGIC 192.3. SAPM 212.4. TU Vienna 232.5. ULUND 252.6. 2.-0 LCA 272.7. GIG 29

3. SECTION 3: SUMMARY FINANCIAL REPORT 31

REPORT ON THE DISTRIBUTION OF THE COMMUNITY'S CONTRIBUTION 34

3/36

Holiwast First Management Report

4/36

Holiwast First Management Report

4/36

Holiwast First Management Report

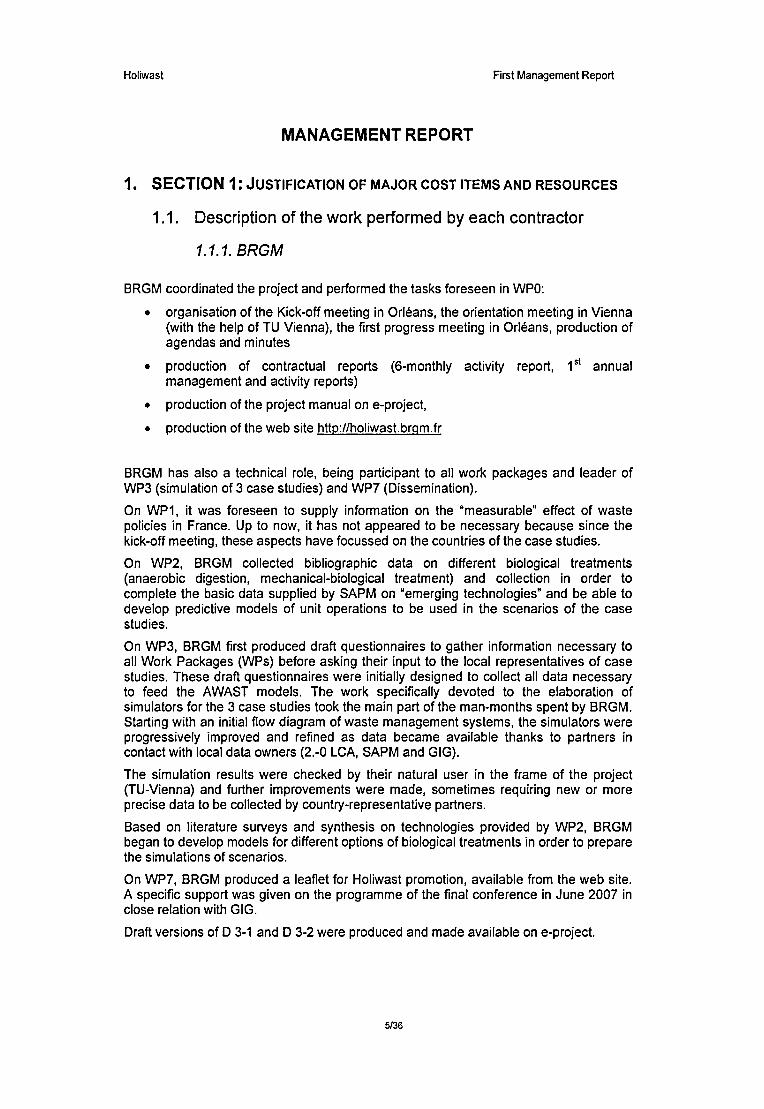

MANAGEMENT REPORT

1 . SECTION 1 : Justification of major cost items and resources

1.1. Description of the work performed by each contractor

1.1.1. BRGM

BRGM coordinated the project and performed the tasks foreseen in WPO:

organisation of the Kick-off meeting in Orléans, the orientation meeting in Vienna(with the help of TU Vienna), the first progress meeting in Oriéans, production ofagendas and minutes

production of contractual reports (6-monthly activity report, 1^' annualmanagement and activity reports)

production of the project manual on e-project,

production of the web site http://holiwast.brqm.fr

BRGM has also a technical role, being participant to ail work packages and leader ofWP3 (simulation of 3 case studies) and WP7 (Dissemination).

On WP1, it was foreseen to supply information on the "measurable" effect of wastepolicies in France. Up to now, it has not appeared to be necessary because since thekick-off meeting, these aspects have focussed on the countries of the case studies.

On WP2, BRGM collected bibliographic data on different biological treatments(anaerobic digestion, mechanical-biological treatment) and collection in order tocomplete the basic data supplied by SAPM on "emerging technologies" and be able todevelop predictive models of unit operations to be used in the scenarios of the casestudies.

On WP3, BRGM first produced draft questionnaires to gather information necessary toall Work Packages (WPs) before asking their input to the local representatives of casestudies. These draft questionnaires were initially designed to collect ail data necessaryto feed the AWAST models. The work specifically devoted to the elaboration ofsimulators for the 3 case studies took the main part of the man-months spent by BRGM.Starting with an initial flow diagram of waste management systems, the simulators wereprogressively improved and refined as data became available thanks to partners incontact with local data owners (2.-0 LCA, SAPM and GIG).

The simulation results were checked by their natural user in the frame of the project(TU-Vienna) and further improvements were made, sometimes requiring new or moreprecise data to be collected by country-representative partners.

Based on literature surveys and synthesis on technologies provided by WP2, BRGMbegan to develop models for different options of biological treatments in order to preparethe simulations of scenarios.

On WP7, BRGM produced a leaflet for Holiwast promotion, available from the web site.A specific support was given on the programme of the final conference in June 2007 inclose relation with GIG.

Draft versions of D 3-1 and D 3-2 were produced and made available on e-project.

5/36

Holiwast First Management Report

MANAGEMENT REPORT

1 . SECTION 1 : Justification of major cost items and resources

1.1. Description of the work performed by each contractor

1.1.1. BRGM

BRGM coordinated the project and performed the tasks foreseen in WPO:

organisation of the Kick-off meeting in Orléans, the orientation meeting in Vienna(with the help of TU Vienna), the first progress meeting in Oriéans, production ofagendas and minutes

production of contractual reports (6-monthly activity report, 1^' annualmanagement and activity reports)

production of the project manual on e-project,

production of the web site http://holiwast.brqm.fr

BRGM has also a technical role, being participant to ail work packages and leader ofWP3 (simulation of 3 case studies) and WP7 (Dissemination).

On WP1, it was foreseen to supply information on the "measurable" effect of wastepolicies in France. Up to now, it has not appeared to be necessary because since thekick-off meeting, these aspects have focussed on the countries of the case studies.

On WP2, BRGM collected bibliographic data on different biological treatments(anaerobic digestion, mechanical-biological treatment) and collection in order tocomplete the basic data supplied by SAPM on "emerging technologies" and be able todevelop predictive models of unit operations to be used in the scenarios of the casestudies.

On WP3, BRGM first produced draft questionnaires to gather information necessary toall Work Packages (WPs) before asking their input to the local representatives of casestudies. These draft questionnaires were initially designed to collect ail data necessaryto feed the AWAST models. The work specifically devoted to the elaboration ofsimulators for the 3 case studies took the main part of the man-months spent by BRGM.Starting with an initial flow diagram of waste management systems, the simulators wereprogressively improved and refined as data became available thanks to partners incontact with local data owners (2.-0 LCA, SAPM and GIG).

The simulation results were checked by their natural user in the frame of the project(TU-Vienna) and further improvements were made, sometimes requiring new or moreprecise data to be collected by country-representative partners.

Based on literature surveys and synthesis on technologies provided by WP2, BRGMbegan to develop models for different options of biological treatments in order to preparethe simulations of scenarios.

On WP7, BRGM produced a leaflet for Holiwast promotion, available from the web site.A specific support was given on the programme of the final conference in June 2007 inclose relation with GIG.

Draft versions of D 3-1 and D 3-2 were produced and made available on e-project.

5/36

Holiwast First Management Report

1.1.2. Ecologie

Ecologie was mainly involved in the work packages WP1 and WPS.

In WP 1 for the deliverable D1-1 "Review of policy instruments". Ecologie provided theoverview over economic instruments for waste management. The review discusses theiradvantages and disadvantages, drawn from existing case studies. For this task a set ofeconomic instruments that act at different stages of the waste management processwere described and evaluated according to a set of criteria. The elaboration of thesecriteria was done in close co-operation with the University of Lund.

For WP 4 a common strategy between WP 4 and WP 5 was developed.

The main task in Ecologic's work was the development of a framework to assess thesocio-economic consequences of waste management concepts in WP 5 (seedeliverable D5-1). In close co-operation with the University of Vienna and the tasksperformed in WP4, an approach was elaborated that complements the impactassessment done in WP 4 to guarantee a holistic impact assessment.

The proposed actor-based impact assessment concentrates on conflicts associated withthe implementation and running of waste management concepts.

The following conflicts were identified as most relevant and will be investigated in detail:

Conflict between local political decision makers and local industry;Conflict between local political decision makers and local waste managementservices (local traditions of waste management);Conflict between local political decision makers and local citizens/companiesproducing municipal waste (waste producers);Conflict between local political decision makers of different communities forming aunion with regard to waste management;Conflict between local political decision makers and academics.

Based on this concept a questionnaire will be developed to measure the impact of theproposed waste management concepts on the different stakeholders involved. Theresults of this actor-based impact assessment will allow local wasteauthorities/politicians to fine-tune the recommendations of the technical impactassessment to minimise the socio-economic impacts. Furthermore the findings will helpto develop a public awareness strategy to ensure a successful, and as unproblematic aspossible implementation of the new waste-management concept.

Ecologie additionally participated in ail project meetings of the first year.

1.1.3. SAPM

Concerning WP2, the work was started through investigations in literature to seekdescriptions of treatment technologies and collection systems.

Efforts have been focused on evaluation of cross-consistency of systems for collection,related changes in waste to be treated and disposed of, and technologies for treatmentand disposal.

This establishes a "mobile target" of investigations, since data-mining about collectionsystems provided for a wide data set according to which deep changes in nature,composition, calorific value and percentage of biodégradables in residual waste is to beexpected as a consequence of collection systems that are factually implemented.

6/36

Holiwast First Management Report

1.1.2. Ecologie

Ecologie was mainly involved in the work packages WP1 and WPS.

In WP 1 for the deliverable D1-1 "Review of policy instruments". Ecologie provided theoverview over economic instruments for waste management. The review discusses theiradvantages and disadvantages, drawn from existing case studies. For this task a set ofeconomic instruments that act at different stages of the waste management processwere described and evaluated according to a set of criteria. The elaboration of thesecriteria was done in close co-operation with the University of Lund.

For WP 4 a common strategy between WP 4 and WP 5 was developed.

The main task in Ecologic's work was the development of a framework to assess thesocio-economic consequences of waste management concepts in WP 5 (seedeliverable D5-1). In close co-operation with the University of Vienna and the tasksperformed in WP4, an approach was elaborated that complements the impactassessment done in WP 4 to guarantee a holistic impact assessment.

The proposed actor-based impact assessment concentrates on conflicts associated withthe implementation and running of waste management concepts.

The following conflicts were identified as most relevant and will be investigated in detail:

Conflict between local political decision makers and local industry;Conflict between local political decision makers and local waste managementservices (local traditions of waste management);Conflict between local political decision makers and local citizens/companiesproducing municipal waste (waste producers);Conflict between local political decision makers of different communities forming aunion with regard to waste management;Conflict between local political decision makers and academics.

Based on this concept a questionnaire will be developed to measure the impact of theproposed waste management concepts on the different stakeholders involved. Theresults of this actor-based impact assessment will allow local wasteauthorities/politicians to fine-tune the recommendations of the technical impactassessment to minimise the socio-economic impacts. Furthermore the findings will helpto develop a public awareness strategy to ensure a successful, and as unproblematic aspossible implementation of the new waste-management concept.

Ecologie additionally participated in ail project meetings of the first year.

1.1.3. SAPM

Concerning WP2, the work was started through investigations in literature to seekdescriptions of treatment technologies and collection systems.

Efforts have been focused on evaluation of cross-consistency of systems for collection,related changes in waste to be treated and disposed of, and technologies for treatmentand disposal.

This establishes a "mobile target" of investigations, since data-mining about collectionsystems provided for a wide data set according to which deep changes in nature,composition, calorific value and percentage of biodégradables in residual waste is to beexpected as a consequence of collection systems that are factually implemented.

6/36

Holiwast First Management Report

This required more time than previously planned in order to define the boundaryconditions for adoption of technologies to process biodégradables or dispose of residualwaste, which is one key focus of the life-cycle investigation to follow.

Details about such changes in composition of waste and related consequences in termsof processability, energy recovery, fulfilment of landfill diversion targets, etc, will bepresented at the interim meeting

As a consequence, an extra time window was required in order to:

finalise investigations on expected results of schemes for separate collection interms of change of amount and composition of residual waste,

match them with the proposed list of technologies to be considered in modelling.

D2-1 Report on waste management options, was prepared; the Report includes:A list and description of Waste management technologies currently adopted, including«emerging» technologies, and an evaluation of these technologies with particularreference to flexibility, scaling down of quantities, consistency with legislations,affordability, environmental effects, reliability.A draft version of D2-1 was uploaded on the web site in early May. It was revised afterpartners' contributions concerning a review of the layout; also, a more detaileddescription of conventional technologies (grate incineration, fluidized bed incinerationand rotary kiln) was provided for the chapter "Options for thermal treatment" with acontribution by TU Vienna. Other changes followed, also in parallel to ongoing activitiesof WP2 and relationships to other WPs, and concerned the following topics: figures formaterial flow (including air and water) for principal technologies (incineration), PAYTcharges applied to collection schemes, finalisation of tables describingadvantages/disadvantages and "conditions" for different options for treatment of residualwaste. The final revision is being finalised and will be loaded on the website.

A draft was also prepared for D2-2, concerning suitable schemes on waste managementstrategies in the 3 case-studies (key elements for the choice); the deliverable is beingfinalised and uploaded on the Project website.

For WP3 SAPM researchers collected and elaborated the data set for wastemanagement system currently adopted in Turin, including information on collectionsystems, recycling and disposal, waste flows and mass balances at the treatmentplants. Data were sourced from the public waste management company (AMIAT),through correspondence and on-site visits. Data were transferred to the WP leader inorder to organise the input data set for the concerned case study and updated asplanned for the simulator.

Deliverable D3_2 was critically reviewed and the description of the study case Turin(detailed in Deliverable D3_2) was checked; additional data/information were alsoprovided.

Details about the composition and operation of collection teams in urbanised areaswhere collected and sent to the WP leader in order to support in-depth preparation ofoperating details of the Simulator. Collection teams have been described for thecollection at the doorstep of: residual waste, foodwaste, paper, plastics (i.e. light.Packaging) and collection of glass at bring-banks.

A specific support was given in order to complete the information necessary for thesimulator and simulate optimal performances of MBT treatment of MSW, compostingand anaerobic digestion of Biowaste from separate collection. Specific data wereprovided regarding:

7/36

Holiwast First Management Report

This required more time than previously planned in order to define the boundaryconditions for adoption of technologies to process biodégradables or dispose of residualwaste, which is one key focus of the life-cycle investigation to follow.

Details about such changes in composition of waste and related consequences in termsof processability, energy recovery, fulfilment of landfill diversion targets, etc, will bepresented at the interim meeting

As a consequence, an extra time window was required in order to:

finalise investigations on expected results of schemes for separate collection interms of change of amount and composition of residual waste,

match them with the proposed list of technologies to be considered in modelling.

D2-1 Report on waste management options, was prepared; the Report includes:A list and description of Waste management technologies currently adopted, including«emerging» technologies, and an evaluation of these technologies with particularreference to flexibility, scaling down of quantities, consistency with legislations,affordability, environmental effects, reliability.A draft version of D2-1 was uploaded on the web site in early May. It was revised afterpartners' contributions concerning a review of the layout; also, a more detaileddescription of conventional technologies (grate incineration, fluidized bed incinerationand rotary kiln) was provided for the chapter "Options for thermal treatment" with acontribution by TU Vienna. Other changes followed, also in parallel to ongoing activitiesof WP2 and relationships to other WPs, and concerned the following topics: figures formaterial flow (including air and water) for principal technologies (incineration), PAYTcharges applied to collection schemes, finalisation of tables describingadvantages/disadvantages and "conditions" for different options for treatment of residualwaste. The final revision is being finalised and will be loaded on the website.

A draft was also prepared for D2-2, concerning suitable schemes on waste managementstrategies in the 3 case-studies (key elements for the choice); the deliverable is beingfinalised and uploaded on the Project website.

For WP3 SAPM researchers collected and elaborated the data set for wastemanagement system currently adopted in Turin, including information on collectionsystems, recycling and disposal, waste flows and mass balances at the treatmentplants. Data were sourced from the public waste management company (AMIAT),through correspondence and on-site visits. Data were transferred to the WP leader inorder to organise the input data set for the concerned case study and updated asplanned for the simulator.

Deliverable D3_2 was critically reviewed and the description of the study case Turin(detailed in Deliverable D3_2) was checked; additional data/information were alsoprovided.

Details about the composition and operation of collection teams in urbanised areaswhere collected and sent to the WP leader in order to support in-depth preparation ofoperating details of the Simulator. Collection teams have been described for thecollection at the doorstep of: residual waste, foodwaste, paper, plastics (i.e. light.Packaging) and collection of glass at bring-banks.

A specific support was given in order to complete the information necessary for thesimulator and simulate optimal performances of MBT treatment of MSW, compostingand anaerobic digestion of Biowaste from separate collection. Specific data wereprovided regarding:

7/36

Holiwast First Management Report

the input/outputs of the mechanical step of MBT when changing thecompositions of MSW (starting amount and composition of MSW), and derivingthe totals of different waste materials passing through / or remaining above thesieve hole.input matrix with mass flows (% of input) built on a review of site-specific massflows across Europe (direct assessment + sourced data from literature); the typeof treatment-plants investigated were:

o pre-treatment of residual/mixed MSW: splitting; biodryingo recovery of Biowaste from sep. collection: composting; anaerobic

digestion (including post-composting)

Regarding WP4: preliminary data regarding the MSW flows and the identification ofdifferences between the waste management systems of the three study cases arereported in WP 2_2.

Regarding WP5: support was provided to the WP leader to have preliminary contactswith potentially involved speakers and stakeholders for the final Conference in Poland.Literature data regarding PAYT charges in Italian cases were exchanged.

Regarding WP7: a specific support was given in order to develop a consistentprogramme of the final conference in June 2007; three guest-speakers were singled outfor participation in the event on the basis of relevance of their experience to thesurveyed issues. The invited expert addressing the topic of current trends in MSWdisposal in EU Member States has been preliminary contacted; contact details havebeen delivered to the Project Partner GIG, responsible for the event. A contact list ofinvitation to be sent to National experts from public authorities and private institutions iscurrently being updated.

1.1.4. TU Vienna

WP2

The draft version of D2-1: "Report on waste management options" was criticallyreviewed. Suggestions concerning layout of chapters was made. Major improvementswere made to the chapter "Options for thermal treatment". The introduction into thermaltreatment lists the objectives and relevant parameters for thermal treatment in general.Furthermore the different conventional technologies (grate incineration, fluidized bedincineration and rotary kiln) were described.

Based on existing plants (Grate Incineration plant Spittelau, Vienna; Fluidised BedIncineration Plant RVL-Lenzing; Rotary Kiln Shaft for Cement Production, Mannersdorf)in Austria the function was explained and illustrated with construction schemes.

Figures of the total material flow (including air and water) for each technology weredrawn and described. These figures give a quick overview of major inputs (waste,chemicals, raw materials, air and water) and outputs (residues, off-gas and waste water)of the different technologies.

The content of D2-2: "Possible schemes on waste management strategies in the threecase studies" was discussed and potentials and disadvantages possible technologies inthe case study scenarios were estimated.

WP3

The calculation of mass and substance balances for the case studies in Tollose(Denmark), Katowice (Poland) and Turin (Italy) have been derived by BRGM.Contributions from our side are done by comments on the first draft of flow sheetsespecially by defining the system boundaries of the case study regions. Municipal solid

8/36

Holiwast First Management Report

the input/outputs of the mechanical step of MBT when changing thecompositions of MSW (starting amount and composition of MSW), and derivingthe totals of different waste materials passing through / or remaining above thesieve hole.input matrix with mass flows (% of input) built on a review of site-specific massflows across Europe (direct assessment + sourced data from literature); the typeof treatment-plants investigated were:

o pre-treatment of residual/mixed MSW: splitting; biodryingo recovery of Biowaste from sep. collection: composting; anaerobic

digestion (including post-composting)

Regarding WP4: preliminary data regarding the MSW flows and the identification ofdifferences between the waste management systems of the three study cases arereported in WP 2_2.

Regarding WP5: support was provided to the WP leader to have preliminary contactswith potentially involved speakers and stakeholders for the final Conference in Poland.Literature data regarding PAYT charges in Italian cases were exchanged.

Regarding WP7: a specific support was given in order to develop a consistentprogramme of the final conference in June 2007; three guest-speakers were singled outfor participation in the event on the basis of relevance of their experience to thesurveyed issues. The invited expert addressing the topic of current trends in MSWdisposal in EU Member States has been preliminary contacted; contact details havebeen delivered to the Project Partner GIG, responsible for the event. A contact list ofinvitation to be sent to National experts from public authorities and private institutions iscurrently being updated.

1.1.4. TU Vienna

WP2

The draft version of D2-1: "Report on waste management options" was criticallyreviewed. Suggestions concerning layout of chapters was made. Major improvementswere made to the chapter "Options for thermal treatment". The introduction into thermaltreatment lists the objectives and relevant parameters for thermal treatment in general.Furthermore the different conventional technologies (grate incineration, fluidized bedincineration and rotary kiln) were described.

Based on existing plants (Grate Incineration plant Spittelau, Vienna; Fluidised BedIncineration Plant RVL-Lenzing; Rotary Kiln Shaft for Cement Production, Mannersdorf)in Austria the function was explained and illustrated with construction schemes.

Figures of the total material flow (including air and water) for each technology weredrawn and described. These figures give a quick overview of major inputs (waste,chemicals, raw materials, air and water) and outputs (residues, off-gas and waste water)of the different technologies.

The content of D2-2: "Possible schemes on waste management strategies in the threecase studies" was discussed and potentials and disadvantages possible technologies inthe case study scenarios were estimated.

WP3

The calculation of mass and substance balances for the case studies in Tollose(Denmark), Katowice (Poland) and Turin (Italy) have been derived by BRGM.Contributions from our side are done by comments on the first draft of flow sheetsespecially by defining the system boundaries of the case study regions. Municipal solid

8/36

Holiwast First Management Report

waste fractions are selected and important indicators are chosen for the environmentalassessment. The actual flow sheets of the status quo scenarios have been checked onplausibility concerning the waste quantities and emission data. Several email contactswhile reviewing the calculations took place. Questionnaires concerning cost data of thetreatment plants in the case study regions are merged with the questionnaires of BRGM.

WP4

Objectives:

WP4 includes the objective to extract mass and substance balances of three wastemanagement systems from simulation results of WP 3 according to methodology ofmaterial flow analysis (MFA).

Secondly, three waste management systems have to be evaluated by applying Cost-Benefit- (CBA) and Cost-Effectiveness-Analysis (CEA), which consider possible criteriasuch as greenhouse gas emissions, conservation of resources, critical air volume etc..The selected methods cover emissions to water, air and soil.

Additionally, know how of MFA has to be transferred to the partners.

Deliverable:

D4-1: "Evaluation of the costs/benefits and costs/effectiveness of the three wastemanagement systems" (month 18)

Progress

Transfer of know-how on the methodology of material flow analysis to the other partnersinvolved the preparation of a short "Methodology Manual" including instructions and anexample to determine mass balances. Furthermore a presentation on MFA was held byProfessor P.H. Brunner during the orientation meeting in Vienna on the 17"^ of October.

The overall definition of the current waste management situation according to themethodology of MFA started based on the information given by the simulations ofBRGM (indirectly by 2.-0 LCA, GIG and SAPM). Flow sheets are created which show agraphical solution of the importance of flows for the goods (e.g. wastes, residues)between the processes (waste treatment facilities) and each substance (e.g. heavymetals, dioxins) separately using the software STAN.

The two methodologies which will be used in this project to evaluate the environmentalimpacts of waste management scenarios have been defined. The cost-benefit-analysisscheme is developed and approaches for the cost-effectiveness-analysis are decided. Aliterature review on former CBA studies showed a variety of results for different wastemanagement concepts.

External effects as produced emissions of waste treatment plants and their monétisationmethod will influence the case study calculations of the CBA significantly. Suggestionsfrom 2.-0 LCA Consultants have been done to use the "Stepwise monetary endpolntvalues". Due to a comparison of these data and existing literature values as avoidanceand damage costs showed major differences. However, the last choice of monétisationis not done yet.

A catalogue of the hierarchy of waste management targets leads to a set of indicators(emissions produced, energy used, land use,...) which will define the total weightedeffectiveness of a measure (e.g. best available technique, change of type of collection)compared to the current waste management scenario.

9/36

Holiwast First Management Report

waste fractions are selected and important indicators are chosen for the environmentalassessment. The actual flow sheets of the status quo scenarios have been checked onplausibility concerning the waste quantities and emission data. Several email contactswhile reviewing the calculations took place. Questionnaires concerning cost data of thetreatment plants in the case study regions are merged with the questionnaires of BRGM.

WP4

Objectives:

WP4 includes the objective to extract mass and substance balances of three wastemanagement systems from simulation results of WP 3 according to methodology ofmaterial flow analysis (MFA).

Secondly, three waste management systems have to be evaluated by applying Cost-Benefit- (CBA) and Cost-Effectiveness-Analysis (CEA), which consider possible criteriasuch as greenhouse gas emissions, conservation of resources, critical air volume etc..The selected methods cover emissions to water, air and soil.

Additionally, know how of MFA has to be transferred to the partners.

Deliverable:

D4-1: "Evaluation of the costs/benefits and costs/effectiveness of the three wastemanagement systems" (month 18)

Progress

Transfer of know-how on the methodology of material flow analysis to the other partnersinvolved the preparation of a short "Methodology Manual" including instructions and anexample to determine mass balances. Furthermore a presentation on MFA was held byProfessor P.H. Brunner during the orientation meeting in Vienna on the 17"^ of October.

The overall definition of the current waste management situation according to themethodology of MFA started based on the information given by the simulations ofBRGM (indirectly by 2.-0 LCA, GIG and SAPM). Flow sheets are created which show agraphical solution of the importance of flows for the goods (e.g. wastes, residues)between the processes (waste treatment facilities) and each substance (e.g. heavymetals, dioxins) separately using the software STAN.

The two methodologies which will be used in this project to evaluate the environmentalimpacts of waste management scenarios have been defined. The cost-benefit-analysisscheme is developed and approaches for the cost-effectiveness-analysis are decided. Aliterature review on former CBA studies showed a variety of results for different wastemanagement concepts.

External effects as produced emissions of waste treatment plants and their monétisationmethod will influence the case study calculations of the CBA significantly. Suggestionsfrom 2.-0 LCA Consultants have been done to use the "Stepwise monetary endpolntvalues". Due to a comparison of these data and existing literature values as avoidanceand damage costs showed major differences. However, the last choice of monétisationis not done yet.

A catalogue of the hierarchy of waste management targets leads to a set of indicators(emissions produced, energy used, land use,...) which will define the total weightedeffectiveness of a measure (e.g. best available technique, change of type of collection)compared to the current waste management scenario.

9/36

Holiwast First Management Report

Questionnaires to impose cost data for the CBA of the current waste managementtechnologies are prepared and sent to the partners from the case study countries. Ourpartners mentioned that these questionnaires are too detailed. Hence, it would takemonths to ask for all the data. In other words, alternatively literature data have to beused.

WP5

Overlapping of proposed work between WP 4 and WP 5 was discussed. WP 4 will focuson costs and the impacts to the environment. WP 5 will focus on acceptability and theability of implementation of policy decision.

WP7

On the 22nd and 23rd of March 2006 the annual meeting of the Austrian Waste Waterand Waste Management Association took place in Vienna. Therefore, we designed aposter to present and advertise the HOLIWAST project.

1.1.5. ULund

Reflecting upon the structure of the project, the IIIEE primarily concentrates its efforts inprogressing WP1, for which the IIIEE serves as the lead participant.

Due to the delay of the start of the project, works related to the first two deliverables ofthe WP1 were conducted in parallel. While preparing the first deliverable (D1-1: Reviewof policy instruments) mainly via literature review, study visits to three case communitieswere conducted, in close collaboration with the partners from the respective countries(SAPM, LCA 2,-0 and GIG) to collect materials for the second deliverable (D1-2:Evaluation of applied policy instruments in case studies). The final draft for D1-1 wascompleted and put on the project website in May 2006 (month 9). The IIIEE has beenproceeding with the draft for D1-2 and intends to complete it by mid October.

The work of the IIIEE related to WP5 concerns the assistance of the leader (Ecologie) indeveloping the questionnaires for the socio-economic assessment of the cases, as wellas addressing some of the questions during the study visit to the case community.

Concerning WP6, the content of D1-1 takes into consideration, to the extent possible,the request of the leader of WP6 (LCA 2,-0) to facilitate the direct usability of the contentof the D1-1 in the final decision making tool.

1.1.6. 2.-0 LCA

2.-0 LCA has been involved mainly in WP1 and WP3 as contact to waste managementauthorifies for the collection of data for the simulator of Tollose. It supplied a report ofinterview and national Danish data on waste management. Data concerning thetreatment plants have been collected by contact to the regional waste managementorganisation Novaren. Interviews have been conducted or are in progress with allrelevant stakeholder groups i.e. citizens, city council, municipal technical staff, wastecollection contractor, the municipal recycling station and Novaren. Data on wastetreatment are extracted from yeariy accounts and green accounts from Noveren andfrom average data in Denmark from the Danish EPA. Interviews with DEPA andDAKOFA/affalddanmark has been conducted to get overview of policy instruments and

10/36

Holiwast First Management Report

Questionnaires to impose cost data for the CBA of the current waste managementtechnologies are prepared and sent to the partners from the case study countries. Ourpartners mentioned that these questionnaires are too detailed. Hence, it would takemonths to ask for all the data. In other words, alternatively literature data have to beused.

WP5

Overlapping of proposed work between WP 4 and WP 5 was discussed. WP 4 will focuson costs and the impacts to the environment. WP 5 will focus on acceptability and theability of implementation of policy decision.

WP7

On the 22nd and 23rd of March 2006 the annual meeting of the Austrian Waste Waterand Waste Management Association took place in Vienna. Therefore, we designed aposter to present and advertise the HOLIWAST project.

1.1.5. ULund

Reflecting upon the structure of the project, the IIIEE primarily concentrates its efforts inprogressing WP1, for which the IIIEE serves as the lead participant.

Due to the delay of the start of the project, works related to the first two deliverables ofthe WP1 were conducted in parallel. While preparing the first deliverable (D1-1: Reviewof policy instruments) mainly via literature review, study visits to three case communitieswere conducted, in close collaboration with the partners from the respective countries(SAPM, LCA 2,-0 and GIG) to collect materials for the second deliverable (D1-2:Evaluation of applied policy instruments in case studies). The final draft for D1-1 wascompleted and put on the project website in May 2006 (month 9). The IIIEE has beenproceeding with the draft for D1-2 and intends to complete it by mid October.

The work of the IIIEE related to WP5 concerns the assistance of the leader (Ecologie) indeveloping the questionnaires for the socio-economic assessment of the cases, as wellas addressing some of the questions during the study visit to the case community.

Concerning WP6, the content of D1-1 takes into consideration, to the extent possible,the request of the leader of WP6 (LCA 2,-0) to facilitate the direct usability of the contentof the D1-1 in the final decision making tool.

1.1.6. 2.-0 LCA

2.-0 LCA has been involved mainly in WP1 and WP3 as contact to waste managementauthorifies for the collection of data for the simulator of Tollose. It supplied a report ofinterview and national Danish data on waste management. Data concerning thetreatment plants have been collected by contact to the regional waste managementorganisation Novaren. Interviews have been conducted or are in progress with allrelevant stakeholder groups i.e. citizens, city council, municipal technical staff, wastecollection contractor, the municipal recycling station and Novaren. Data on wastetreatment are extracted from yeariy accounts and green accounts from Noveren andfrom average data in Denmark from the Danish EPA. Interviews with DEPA andDAKOFA/affalddanmark has been conducted to get overview of policy instruments and

10/36

Holiwast First Management Report

Strategies and action plans applied in Denmark as well as implementation of relevant EUdirectives at national and local level.

For WP6, 2.-0 LCA consultants has started development of the decision supportsoftware (web-based) including presentation for the partner meeting in August. The toolis organized around a flow diagram incorporating stakeholders, policy instruments andconstraints, waste composition, technologies for waste collection and treatment, impactassessment, feedback and interpretation.

1.1.7. GIG

WP1: Policy Instruments - 1 person-month

GIG has contributed in the studies of policy instruments in waste management carriedby ULund in Poland (in Katowice and Warsaw). Interviews of all relevant stakeholders(Ministry of Environment, Regional Government, Municipality of Katowice, TreatmentFacility, Waste Management Company - MPGK and citizens) were conducted withorganisational support of GIG. GIG assisted ULund in studies of Polish documentsconcerning policy instruments and notes from interviews.

WP2: Technologies - 1,2 person-months

GIG has been focused on analysis of waste management technologies currently used inKatowice as well as future development plans, described in existing documents (e.g.Plan of Waste Management for Katowice City).

WP3: Simulations -2,4 person-months

Based on relevant questionnaires, input data for simulation of current state of theKatowice waste management system have been collected. The data collection wasperformed in close cooperation with the Municipality of Katowice and the main wastemanagement company MPGK. To get detailed information interview of the wastetreatment facilities have been conducted. A synthetic diagram on municipal wastemanagement in Katowice as well as detailed flow sheet for the year 2003 was prepared.Waste management strategies and action plans for years 2005 - 2015 on national,regional and Katowice city levels have been overviewed.

WP4: Costs/benefits - 0.5 person-months

GIG has prepared input data necessary for CBA of current waste management systemin Katowice.

WPS: Socio-eeonomy - 0.6 person-months

GIG has been collected data and information for analysis socio-economic aspects ofcurrent waste management system in Katowice.

WP7: Dissemination - 0.5 person-months

The date of an international conference on EC Waste Policy on June 11-12, 2007 wasestablished. The place of conference will be Auditorium Maximum in Cracovia, Poland.Participation of about 100 people from EU 25 is planned. Draft of preliminaryprogramme and budget of conference has been prepared.

On 20 April 2006, in Katowice small workshop related to waste policy has beenorganised. During the workshop the idea, objectives, targets and expected results ofHOLIWAST project were presented by GIG (presentation in Polish). In the workshoptook part representatives of Municipality of Katowice, Waste Company - MPGK, WasteTreatment Facilities in Katowice, ULund and GIG.

The information about the HOLIWAST project in Polish is on the GIG website:http://www.glg.katowlce.pl/gig/projety_euroA/i_ramowy.php

11/36

Holiwast First Management Report

Strategies and action plans applied in Denmark as well as implementation of relevant EUdirectives at national and local level.

For WP6, 2.-0 LCA consultants has started development of the decision supportsoftware (web-based) including presentation for the partner meeting in August. The toolis organized around a flow diagram incorporating stakeholders, policy instruments andconstraints, waste composition, technologies for waste collection and treatment, impactassessment, feedback and interpretation.

1.1.7. GIG

WP1: Policy Instruments - 1 person-month

GIG has contributed in the studies of policy instruments in waste management carriedby ULund in Poland (in Katowice and Warsaw). Interviews of all relevant stakeholders(Ministry of Environment, Regional Government, Municipality of Katowice, TreatmentFacility, Waste Management Company - MPGK and citizens) were conducted withorganisational support of GIG. GIG assisted ULund in studies of Polish documentsconcerning policy instruments and notes from interviews.

WP2: Technologies - 1,2 person-months

GIG has been focused on analysis of waste management technologies currently used inKatowice as well as future development plans, described in existing documents (e.g.Plan of Waste Management for Katowice City).

WP3: Simulations -2,4 person-months

Based on relevant questionnaires, input data for simulation of current state of theKatowice waste management system have been collected. The data collection wasperformed in close cooperation with the Municipality of Katowice and the main wastemanagement company MPGK. To get detailed information interview of the wastetreatment facilities have been conducted. A synthetic diagram on municipal wastemanagement in Katowice as well as detailed flow sheet for the year 2003 was prepared.Waste management strategies and action plans for years 2005 - 2015 on national,regional and Katowice city levels have been overviewed.

WP4: Costs/benefits - 0.5 person-months

GIG has prepared input data necessary for CBA of current waste management systemin Katowice.

WPS: Socio-eeonomy - 0.6 person-months

GIG has been collected data and information for analysis socio-economic aspects ofcurrent waste management system in Katowice.

WP7: Dissemination - 0.5 person-months

The date of an international conference on EC Waste Policy on June 11-12, 2007 wasestablished. The place of conference will be Auditorium Maximum in Cracovia, Poland.Participation of about 100 people from EU 25 is planned. Draft of preliminaryprogramme and budget of conference has been prepared.

On 20 April 2006, in Katowice small workshop related to waste policy has beenorganised. During the workshop the idea, objectives, targets and expected results ofHOLIWAST project were presented by GIG (presentation in Polish). In the workshoptook part representatives of Municipality of Katowice, Waste Company - MPGK, WasteTreatment Facilities in Katowice, ULund and GIG.

The information about the HOLIWAST project in Polish is on the GIG website:http://www.glg.katowlce.pl/gig/projety_euroA/i_ramowy.php

11/36

Holiwast First Management Report

1 .2. Explanatory note on major cost items

For ail partners, the major cost item in the Holiwast project is person-month cost.

12/36

Holiwast First Management Report

1 .2. Explanatory note on major cost items

For ail partners, the major cost item in the Holiwast project is person-month cost.

12/36

Holiwast First Management Report

1.3. Overview of costs

Table 3: Budget vs. Actual Costs

Cost Budget Follow-up Table *) total budget figures- not EC funding

Contract N': 006509

PARTI -CIPANTS

BRGM

Ecologie

SAPM

IWA

tils*

2.-0 LCA

GIG

TOTAL

TYPE ofEXPENDITURE(as defined byparticipants)

Total Pereon-month

Personnel costs

Travels

Other direct costs

Audits

Total Costs

Total Pervon-month

Personnel costs

Travels

Total Cottl

Total Person-month

Personnel costs

Travels

Total Costs

Total Pervon-month

Personnel costs

Travels

Other direct costs

20% Overtieads

Total Costs

Total Panon'-month

Personnel costs

Travels

20% Overheads

Total Costs

Total PerBon-month

Personnel costs

Travels

Total Costs

Total Porson-month

Personnel costs

Travels

Other direct costs

Total Costs

Total Person-month

Personnel costs

Travels

Other direct costs

20% Overheads

Audits

Total Costs

Acronym: HOLIWAST | Date:

BUDGET

23 97

267250

11300

10000

20000

308550

12.5

139374

8000

147374

15

93300

8000

101300

15

67500

8000

5000

16100

96600

11.5

65560

9000

14900

89460

11

122650

8000

130650

15

75000

8000

15000

98000

103.97

830634

60300

30000

31000

20000

971934

ACTUAL COSTS (EUR)

Period 1

t

11.15

108 654.20

2807.12

1378.01

112839.33

6.47

42279.87

1867.95

44147.82

10

60778.6

2233.11

63011.71

6.5

25326.4

2786.48

5622.58

33735.46

5228323.73

3385.21

6341.79

38050.73

1.01

11209.47

1182.89

12392.36

6.3

30052.99

2994.12

33047.11

46 63

306625.26

17256.88

137801

11964.37

0

337224.52

Period 2

b1

0

0

0

0

0

0

0

0

Total

t<

11.15

108 654.20

2807.12

1378.01

0

112839.33

6.47

42279.87

1867.95

44147.82

10

60778.6

2233.11

63011.71

6.5

25326.4

2786.48

0

5622.58

33735.46

5.2

28323.73

3385.21

6341.79

38050.73

1.01

11209.47

1182.89

12392.36

6.3

30052.99

2994.12

0

33047.11

46.63

306625.26

17256.88

1378.01

11964.37

0

337224.52

Pet. spent

Yearl

i't

47%

41%

25%

14%

0%

37%

52%

30%

23%

30%

67%

65%

28%

62%

43%

38%

35%

0%

35%

35%

45%

43%

38%

43%

43%

9%

9%

15%

9%

42%

40%

37%

0%

34%

45%

37%

29%

5%

39%

0%

35%

YearU2

1+b1/«

47%

41%

25%

14%

0%

37%

52%

30%

23%

30%

67%

65%

28%

62%

43%

38%

35%

0%

35%

35%

45%

43%

38%

43%

43%

9%

9%

15%

9%

42%

40%

37%

0%

34%

0%

0%

0%

0%

0%

0%

Remaining Budget(EUR)

-1

12.82

158595.8

8492.88

8621.99

20000

195710.67

6.03

97094.13

6132.05

103226.18

5

32521.4

5766.89

38288.29

8.5

42173.6

5213.52

5000

10477.42

62864.54

6.3

37236.27

5614.79

8558.21

51409.27

9.99

111440.53

6817.11

118257.64

8.7

44947.01

5005.88

15000

64952.89

57.34

524008.74

43043.12

28621.99

19035.63

20000

634709.48

13/36

Holiwast First Management Report

1.3. Overview of costs

Table 3: Budget vs. Actual Costs

Cost Budget Follow-up Table *) total budget figures- not EC funding

Contract N': 006509

PARTI -CIPANTS

BRGM

Ecologie

SAPM

IWA

tils*

2.-0 LCA

GIG

TOTAL

TYPE ofEXPENDITURE(as defined byparticipants)

Total Pereon-month

Personnel costs

Travels

Other direct costs

Audits

Total Costs

Total Pervon-month

Personnel costs

Travels

Total Cottl

Total Person-month

Personnel costs

Travels

Total Costs

Total Pervon-month

Personnel costs

Travels

Other direct costs

20% Overtieads

Total Costs

Total Panon'-month

Personnel costs

Travels

20% Overheads

Total Costs

Total PerBon-month

Personnel costs

Travels

Total Costs

Total Porson-month

Personnel costs

Travels

Other direct costs

Total Costs

Total Person-month

Personnel costs

Travels

Other direct costs

20% Overheads

Audits

Total Costs

Acronym: HOLIWAST | Date:

BUDGET

23 97

267250

11300

10000

20000

308550

12.5

139374

8000

147374

15

93300

8000

101300

15

67500

8000

5000

16100

96600

11.5

65560

9000

14900

89460

11

122650

8000

130650

15

75000

8000

15000

98000

103.97

830634

60300

30000

31000

20000

971934

ACTUAL COSTS (EUR)

Period 1

t

11.15

108 654.20

2807.12

1378.01

112839.33

6.47

42279.87

1867.95

44147.82

10

60778.6

2233.11

63011.71

6.5

25326.4

2786.48

5622.58

33735.46

5228323.73

3385.21

6341.79

38050.73

1.01

11209.47

1182.89

12392.36

6.3

30052.99

2994.12

33047.11

46 63

306625.26

17256.88

137801

11964.37

0

337224.52

Period 2

b1

0

0

0

0

0

0

0

0

Total

t<

11.15

108 654.20

2807.12

1378.01

0

112839.33

6.47

42279.87

1867.95

44147.82

10

60778.6

2233.11

63011.71

6.5

25326.4

2786.48

0

5622.58

33735.46

5.2

28323.73

3385.21

6341.79

38050.73

1.01

11209.47

1182.89

12392.36

6.3

30052.99

2994.12

0

33047.11

46.63

306625.26

17256.88

1378.01

11964.37

0

337224.52

Pet. spent

Yearl

i't

47%

41%

25%

14%

0%

37%

52%

30%

23%

30%

67%

65%

28%

62%

43%

38%

35%

0%

35%

35%

45%

43%

38%

43%

43%

9%

9%

15%

9%

42%

40%

37%

0%

34%

45%

37%

29%

5%

39%

0%

35%

YearU2

1+b1/«

47%

41%

25%

14%

0%

37%

52%

30%

23%

30%

67%

65%

28%

62%

43%

38%

35%

0%

35%

35%

45%

43%

38%

43%

43%

9%

9%

15%

9%

42%

40%

37%

0%

34%

0%

0%

0%

0%

0%

0%

Remaining Budget(EUR)

-1

12.82

158595.8

8492.88

8621.99

20000

195710.67

6.03

97094.13

6132.05

103226.18

5

32521.4

5766.89

38288.29

8.5

42173.6

5213.52

5000

10477.42

62864.54

6.3

37236.27

5614.79

8558.21

51409.27

9.99

111440.53

6817.11

118257.64

8.7

44947.01

5005.88

15000

64952.89

57.34

524008.74

43043.12

28621.99

19035.63

20000

634709.48

13/36

Holiwast First Management Report

1 .4. Overview of person-months

Table 4: Person-Months Status Table^

Person-Month Status TableCONTRACT N': 6509

ACRONYM: HOLIWAST

PERIOD: 1

WP1:

Policy InstrumentsWP2:

TechnologiesWP3:

SimulationsWP4:

Costs/benefitsWPS:

Socio-EconomyWP6:

Decision aid toolWP7:

DisseminationWPO:

Coordination

Total Person-month

Actual WPtoUl:Planned WP total:

Actual WP total:Planned WP total:

Actual WP total:Planned WP total:

Actual WP total:Planned WP total:

Actual WP total:Planned WP total:

Actual WP total:Planned WP total:

Actual WP total:Planned WP total:

Actual WPtoUl:Planned WP total:

Actual total:Planned total:

OTAL:

7.5

9

10.41

13

13.26

17

4.89

13

5.42

16

1.21

20

2.97

13

1

1.97

46.66

103

BRGM Ecologie

0

1

2

1

5.65

7

0.5

1

0

2

0

6

2

4

1

1.97

11.15

23.97

2.3

2

0

0

0

0

0.25

0.5

3.85

8

0

1

0.07

1

0

0

6.47

12.5

SAPMUVienrULund2.-0LC/

0

0

6

7

3

4

0.5

1

0

0

0.5

2

0

1

0

0

10

15

0

0

1.07

2

1.55

2

3.14

8

0.47

1

0

1

0.3

1

0

0

6.53

15

4.2 0

5 0

0 0.14

0 1

0 0.66

0 1

0 0

0.5 0

0.5 0

3 0

0.5 0.21

2 7

0 0

1 1

0 0

0 0

5.2 1.01

11.5 10

GIG

1

1

1.2

2

2,4

3

0.5

2

0.6

2

0

1

0.6

4

0

0

6.3

15

AC TOTALS

0

0

0.16

0.15

0.07

0.15

1.66

1.12

1.07

0.04

0

0

0.03

0

0

0

2.99

1.46

AC TU ACUVienna Lund

0.16

0.15

0.07

0.15

1.66

1.12

0.07 1

0.04

0.03

0

1.99 1

1.46 0

1 .5. Impact of major deviations

There is a major deviation on the project time schedule. The official start of the projectwas 1^' august 2005 but the contract was received only late in August (the letter is dated17 August), when most partners were in summer holidays. In September, there hasbeen major difficulties in getting all signatures for the consortium agreement, mainly forfinancial reasons (% retention of the pre-financing by BRGM, maximum reimbursementfor audit costs). The discussions and negotiations between partners went on during 3months and the pre-financing could not be distributed before December. In reality, thekick-off meeting (1-2 September) and the orientation meeting (17 October) allowed aslow start of the project during this period. Altogether, the estimated delay at the start ofthe project may be estimated to 4 months.

Another disadvantage for rapid recovery of the initial delay lies in the organisation of theproject: nearly ail WPs are dependant on the case studies. It was decided at the kick-offmeeting to concentrate the work of the "individual assessments" (WP1 - policyinstruments and WP2 - technologies) on situations encountered in the case studies andthe opportunities of their evolutions. WP4 and WP5 use the results of WP3. WP6

^ For AC contractors, a tabular overview of all resources employed on the project and a globalestimate of all costs

14/36

Holiwast First Management Report

1 .4. Overview of person-months

Table 4: Person-Months Status Table^

Person-Month Status TableCONTRACT N': 6509

ACRONYM: HOLIWAST

PERIOD: 1

WP1:

Policy InstrumentsWP2:

TechnologiesWP3:

SimulationsWP4:

Costs/benefitsWPS:

Socio-EconomyWP6:

Decision aid toolWP7:

DisseminationWPO:

Coordination

Total Person-month

Actual WPtoUl:Planned WP total:

Actual WP total:Planned WP total:

Actual WP total:Planned WP total:

Actual WP total:Planned WP total:

Actual WP total:Planned WP total:

Actual WP total:Planned WP total:

Actual WP total:Planned WP total:

Actual WPtoUl:Planned WP total:

Actual total:Planned total:

OTAL:

7.5

9

10.41

13

13.26

17

4.89

13

5.42

16

1.21

20

2.97

13

1

1.97

46.66

103

BRGM Ecologie

0

1

2

1

5.65

7

0.5

1

0

2

0

6

2

4

1

1.97

11.15

23.97

2.3

2

0

0

0

0

0.25

0.5

3.85

8

0

1

0.07

1

0

0

6.47

12.5

SAPMUVienrULund2.-0LC/

0

0

6

7

3

4

0.5

1

0

0

0.5

2

0

1

0

0

10

15

0

0

1.07

2

1.55

2

3.14

8

0.47

1

0

1

0.3

1

0

0

6.53

15

4.2 0

5 0

0 0.14

0 1

0 0.66

0 1

0 0

0.5 0

0.5 0

3 0

0.5 0.21

2 7

0 0

1 1

0 0

0 0

5.2 1.01

11.5 10

GIG

1

1

1.2

2

2,4

3

0.5

2

0.6

2

0

1

0.6

4

0

0

6.3

15

AC TOTALS

0

0

0.16

0.15

0.07

0.15

1.66

1.12

1.07

0.04

0

0

0.03

0

0

0

2.99

1.46

AC TU ACUVienna Lund

0.16

0.15

0.07

0.15

1.66

1.12

0.07 1

0.04

0.03

0

1.99 1

1.46 0

1 .5. Impact of major deviations

There is a major deviation on the project time schedule. The official start of the projectwas 1^' august 2005 but the contract was received only late in August (the letter is dated17 August), when most partners were in summer holidays. In September, there hasbeen major difficulties in getting all signatures for the consortium agreement, mainly forfinancial reasons (% retention of the pre-financing by BRGM, maximum reimbursementfor audit costs). The discussions and negotiations between partners went on during 3months and the pre-financing could not be distributed before December. In reality, thekick-off meeting (1-2 September) and the orientation meeting (17 October) allowed aslow start of the project during this period. Altogether, the estimated delay at the start ofthe project may be estimated to 4 months.

Another disadvantage for rapid recovery of the initial delay lies in the organisation of theproject: nearly ail WPs are dependant on the case studies. It was decided at the kick-offmeeting to concentrate the work of the "individual assessments" (WP1 - policyinstruments and WP2 - technologies) on situations encountered in the case studies andthe opportunities of their evolutions. WP4 and WP5 use the results of WP3. WP6

^ For AC contractors, a tabular overview of all resources employed on the project and a globalestimate of all costs

14/36

Holiwast First Management Report

synthesises all findings. So far, the whole project work is roughly linked to the speed atwhich data may be obtained from the authorities in charge of waste management in thecase studies, and thus the speed of achievement of W P 3 .

So far, a lot of efforts have been m a d e to speed the data acquisition from the casestudies. Mainly all partners have been involved in the process and to date, thedeliverables due on month 12 have been delivered on month 14. This concerns D12 ,D22, D32, D51 , as shown in the figure.

Yeari2 | 3 | 4 | 5 | 6 | 7 | 8

Year 23 | 4 | 5 6 | 7 | 8 | 9|10l1ÎTi2

W P ÜCoordination

D01D02

DQ4f D05f

WP1Analysis of policy

instruments

¡D12

W P 2Analysis of waste

treatment technologies

D22

WF3Scope definition and

calibration of assessmenttools

D32 533 D34

W P 4Environmental Efficiency

W P 5Socio-economicconsequences

WPBDecision Support

|D61 D62 D63J

W P 7Dissemination and

Valorisation

A s a consequence, delays must be expected on subsequent deliverables.

W P 3 : As D 3 2 presenting the actual situation is 2 months late, D33, presenting theresults of the scenarios should be delayed by 2 months as well as D34 .

W P 4 : O n 4 t h July 2006 TU-Vienna requested a transfer of 2 person months from yearone to year two. Additionally 3 person months more than proposed not exceeding thetotal personnel budget have been requested. This additional time will be needed in yeartwo when the data sets of the three case studies are complete and the calculations ofthe cost-benefit analysis and the cost-effectiveness analysis can be done. This wasaccepted by the scientific officer Mr. V . Vulturescu per email to the coordinator Mr. J.Villeneuve on 10 th July 2006. In the meantime the actual personnel costs for NinaTruttmann are calculated and w e have to reduce the additional person month from 3 to 2month to maintain the proposed budget. The results of this change have no negativeeffects on the quality of the reports and the total costs of the project will not exceed theoriginal target.

W P 3 is delayed- In W P 4 w e have to extract relevant mass and substance balances fromW P 3. Therefore D4-1 will be delayed - depending on the availability of the completescenario data of the case studies - approximately 1 month (month 19).

W P 5 : The work on the actor-based impact assessment, including the interviews of thestakeholders in the regions, can only begin when the technical recommendations for thedifferent waste management concepts in the regions in Italy, Poland and Denmark are

15/36

Holiwast First Management Report

available. Hence WP5 is highly contingent on WP3 and a delay of the deliverable D5-2cannot be excluded.

16/36

Holiwast First Management Report

available. Hence WP5 is highly contingent on WP3 and a delay of the deliverable D5-2cannot be excluded.

16/36

Holiwast First Management Report

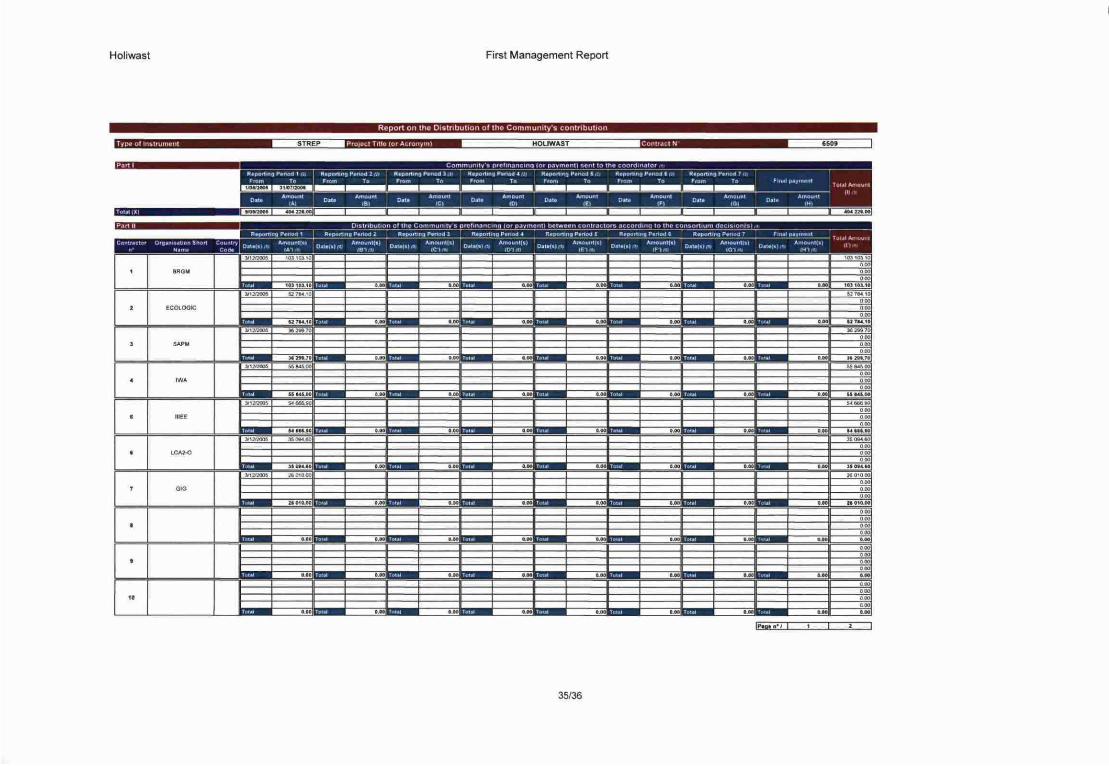

2. SECTION 2: F O R M C FINANCIAL STATEMENT

2.1. BRGM

Form C - Modal of Flmnciil Statamánt per Activity {to b» mi« a by ««ti i

Type of instrument

Project Title (or Acronym)

Contractor's Legal Name

Legal Type

Contact Person

Telecopy

Cost model used

(AD'FCof FCF)

•06509

B U R E A U DE R E C H E R C H E S G E O L O G I Q U E S ET MINIERES

Other

M VILLENEUVE Jacaues lAÜRifRT^L^L^L^L^L^L^L^L^I^I^H33-2-38643062 [^Sl^L^L^L^L^L^L^L^L^L^L^L^H

^ ^ ^ ^ ^ ^ ^ ^ ^ ^ ^ ^ ^ ^ ^ ^ ^ ^ H Indirect costs/Roai or Fisr R.irn of JD>, or Dixxrr

33-2-38643629

i Villeneuve ©brom.fr

Real indicad cosí

1- R M O u r c « (Third o.rtvfleill

Are ¡here any resources made avBilabte on the bans of a prior agreement wffi ifurd parties identified in Annex 1 of tne contract? (Yes/Nol \Ho

It Y e s please provide irva following, information

Third Party I IY1] Legat Uni™-

Third Party 21Y2) Legal Name

Third Party 3 {Yl) Legal N a m e

Third Party 4 (Y4) Legal N a m e

Cost model used

Cost model used

Cost model used

Cos! model used

2- Declaration of «liolbl« coat» lin €1

f and t entioned in Article II25 and/or nPlease complete only the activity covered by tha mlêvart friffrunwnt fand lype of action) indicated abovcontractIt you are a contractor using the additional cost model fAC)•Indícate only your additional eligibh coati, except tor Management of the Consortium Activity for which you may indicate your full eligible costs.

- do not declare eligible direct additional costs speafically covered t>y contributions /rom third parties as mentioned in Aflc/aj 11.20 and 11.23.* tnd b ot the contractIf you are a contractor uirng a Ml cost model fFOFCF). indícate your full eligible coala.The costs declared should distinguish between direct end indirect costs

tf necessary, adjustments to previous pertodf« may be included where appropriate

lent of the

Consortium

Other SpecificActivities IF) •

Direct costs

01 «ix. Ik

llrjirPCt COStS

Ätl|ustment5

Píriodis)

Total coils

57137.71

42743.09

99B80 80 000 000 0 00: ' ó.oo

1

I

o.oi

7564 60

5393 73

12958 53 to o o K o oo

64702 51

0 00

48136.82

0 00

112839 33

000

0 00

000

0 00

000

3- Daclaration ol rBC»lp» (In €1

If you are a contractor using the additional cost model (flCJ. Indicate only receipts conered by Article II23 c of if» contractIf you are a contractor using a fuHcost model IFCJFCF) indícate recvipts covered by Article II23 ot the contractIf a receipt Is not allocated to an activity

17/36

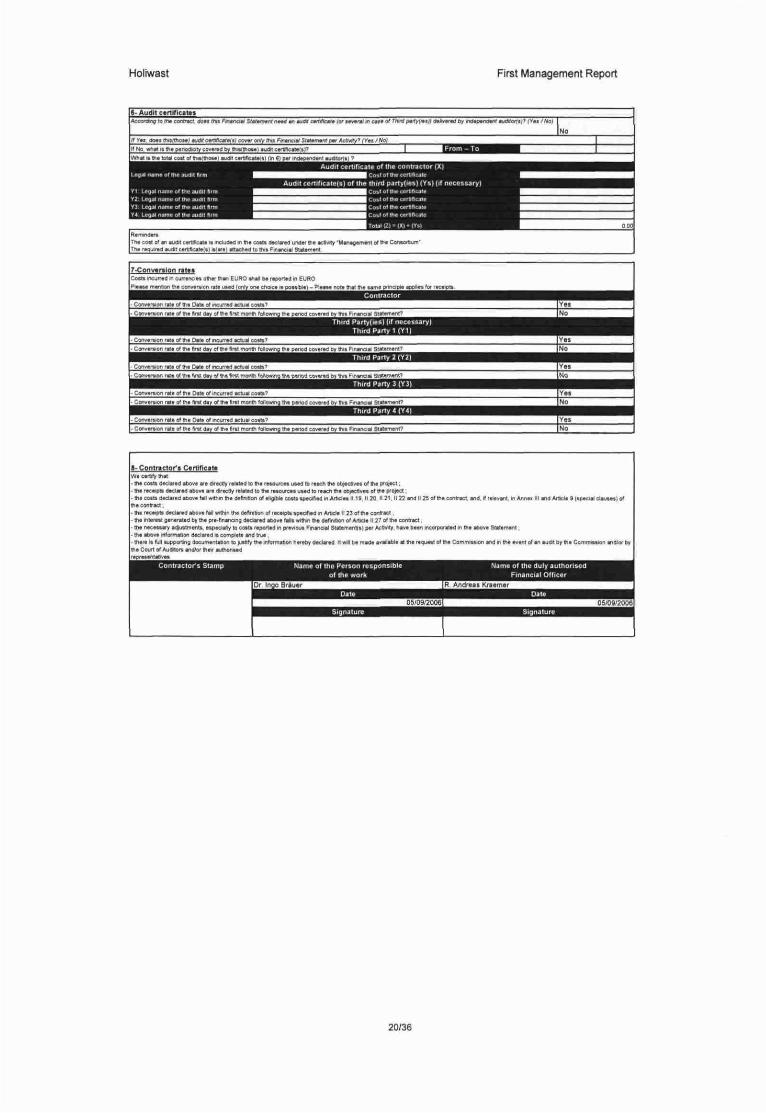

Holiwast First Management Report

1- Audit c*rtmc*M*ic&voYno" '0 *"e cwtiwcr tinos

II Ytt d o « Uvifinc») tudt c

rr hio what it the panodcnv co

What • fia total coat ut thialth

U M I ftrwKMf St«

tnifiaititi covtr

eraä by triiaithoii

ïaa) audrt eartrftea

emenln.

laudilc

ala) (m

a*tf f> audit cerrfcere lût H 4

tnàncial STattmmrrt pur Adivity

•rtrficawai»

1 H > independent aurMorla) '

r* « c « * si n»*,wrtyft»l) B . / ™ « 6 , J - W a w r « . ™ ^íofl«! ' (V. . / N o )

No'<Vai/«ol

1 UffiiHl^a^a^a^LVJ

fha coal of an audit cortrtcat* it includad m [ha caata d a d v a d u n M f lha activity 'Uanagamanl of fta Conaortiurr'

Tha ragnraa audii cjmflcaWti rtiir») attacfiad to thu financial Statamar«

7-Conv*r*ion ntt*

Coao incurred in cunnciH o»«r Vían EURO ("all ba reportad in E U R O

Plaaaa rtuntion ft« e a m r n o n ran M M lonly ont enwe« n p o m a » ) - Pia nota mat ffn lanía pnnciçta applia» fo

Data M meutrta Kiuai cotn?

si Bu h p 3 » ol Tu Bin montfi foil wing m . ptnoa cov««d by fui FtfiHiciMl

I of Bit Yat dav of B W drat marrih fDiDwind V w panod covffrad bv Vit Fin,

- CorivsrarDn rat« of the I

- CoTiYflfSfOn rato of Ihí 1

at* of m e

tt Hay o

urradactu

UiafrrBm

M cost»'

onth folio* no Eha p*nof cohered bv 7it Financial Statamanf

Yas

No

Wi• Bl

-Ü1

-Bl

•th

•th

• th

-Hi

-fl

tha

Corrtr.ctor'tartity that

a c n a a«lai

a racaiptn d*c

a coalm Oeclar

a racaipB dada mura at Q « ^ «

t Certtfl

d abava ar

artd aloya

. 1 .

diracHy rtlatad to lha n i s u r c « u n d to rtadi tha oB|act>vat ol lha projet,

ara Dlractly reatadlo tha resourc« used to raach Via

d a c ó « tall «thin m a dafinrDon ol alipMa coatt tpacrflad In A n d

aradacova faU w<!hi

at*d by tb« pra-Hna

a ntc»«sarv ad}UfttrnantiL

a above inform

ara la fu» <upp<Court of AudrE

Mentatlvaa

•ton dada

ortiriQ docu

X » mdfar 0

•apacjal

aú im co

Tltnwyo

m a tfeflration Dtr«arpn>p*cifiadiri A i W a l

nang d«clir«d tbo»» IWt within ü n d*ürxeon

' to cotia reportad in prevlout Financial stala

TI plata and tnja .

lojubtify tht infotrnabon haraby daclafsd It

" " "

bjactjvfl« of tha ptoftd,»111« 1120 1121. llîîandllîi °"t™contrac1. and. It ralavant. <n *

13 ol m a contract.

olArvclal l^olthaconnct.

mani(K) par AcovrTy hava baan mcorporaTed in th* above Statement

«ill Da tntOt availab>a aE trie ra<iLJ*BI of tha Committion and m the av

n n » III and A m d i « (tCKlal d a u a « ) of

mt or an audrt by ft« Coffimnion «nd)or by

Contractor's Stamp Nûme or m e duly authorised

Financial Officer

M Jacq e VILLENEUVE

05/00/2006

M Pierre Louis KIRCHER

18/36

Holiwast First Management Report

2.2. Ecologie

F o r m C - M o d « I o( Financial S t a f rrwnt p«r Activity no p»fi»»a b y n c n cpntuctori

Type of instrumentProject Tille (or Acronym)

Coniractor's Legal Narria

Legal Type

Contact Person

Telecopy

Cost mode! used

(ACHFCorFCF|

¡Specific Targeted Pr

IHOLIWASTT y p e Of Action ¡U necassúry)

¡ECOLOGIC - INSTITUT FUER INTERNATIONALE U N D EUROPAEISCHE UMWELPQLITIK a G m b H

¡Non-profil

¡Dr Ingo Brauer

•49 -30 -86880-100

Telephone

E-m.nl

Indirect COS1S("«.W oi fix

+49-3O-B6SB0-110

¡Real in dira ci cost

I-R»»ourc»i IThird p«rtvfi«i))

u/sO/a on Ihn basis of a prior agreement with rntrd parties idsnJi/iBdin Annan taltha canina'1 í'

2- D«clamtlon of »lintblt co»tt lln Ou s compisís on/yjn» activity covered Ay H w roísvínl inaffumení ¡ami typa ot action) intficsfatí a ù o « »nú as mendonad m Article 'f 2S anû/0'in Annaias 1 tndlltoltha

contraer

If you a « a contracta' utinç tht additional coat mo<MI ¡AC)

• mOtcate only you/ additional eMoiW» coitt, atcapt lor Managamant oí die Con«offium Activity lor irnicn you may mBicala your full eligible costs,

• do not àactv* »ligibla diract additional costs specifically coveiaO by contnbutiona from ft/ri »irtm as mentioned in Aitictaa II20 and II23 a and b of tba contract

it you ara a contractor using a tu« cost modal ¡FC/FCF) indicate your full eligible coils

Tht costs üaclaitd should distinguish between direct and indirect cottt

If necessary, adjustmants to pfoviouo panodia} ma/ be included where appropriate

27807«

163«.38

44147 82 0 00 0 00 0 00

¡

ooe 0 00

Va D D B o oo ODD

27807 44

a oo1634Û 38

0 00

44147 82

0 00

0 00

0 00

0.00

0 00

3- Declaration of receloU (in ()If you area contractor u>mg the additional cott model (ACj.

It you area contracto' uting a hü cost model ffC/FCFJ indi

•eceipt is not allocated to an activity

ate only receipts covered By Article II 23 c otthe contract

racarp/i covered By Arttctv '.' 23 of the centrad

4- C u t I« ration of intereit aanerited by the pre-financina (in <l

To be completed only by the coordinator

r\g JfltJvjncgJ ycu rgcaivgiT Úy In» C o |No

5- Request of FPfi Financial contnbulmn fin €)

For tfra pqnod in? FPfl Community fining*> contnbuuon r•got

19/36

Holiwast First Management Report

t- Audit ctrtHlcaMiAccorctno la fft* cortfiact

II Ymi D » i ini.llhos.1 n

if No what n m e penada

W h « n m * tstai cou of tr

T1 " LpyjE n a m e of the 4

V3. Lcgjl n a m e of the JL

The cotT of on audrt carnfi

Th« required audi cartfrci

7-Conv»r»ion r»t#*

Plana menoon Lhs conv*

• Conversion ruta of th> L

Jo*s " * • ri/uncKi Swifntnf

-íflf ceiVt¡e*t*4*> cow Ofíiy ifiiS

i tov*r»d by ïiis(lho«a1 ludí

dit •rm • •

F^ianatV Sf* im#rW p * - Äcfjv»^' fY

certmcjna(ï)'

€) per iF4»p*ndinf iudlar(a) ?

af* 0/Ttunípefttfut)) 09UWWÙ ûy ind«p*ndwir «udííoíTiJ'f/ei /ría.;

M/rVoj

^ ^ ^ ^ • ^ ^ ^ ^ ^ i-rom - in ^ ^ ^ ^ H

Audit certJticate o( the contractor {X)

Audit certifícalas) ot the

cate il included m the coitt dad ved under m e activity ~MHn*fl*rn*rts(i) t>(a>*) » K h M to mie Financial Statiirent

H omer I w E U R O ehal be rapcrtaif In E U R O

m o n raw u H d (only ona choice npoulblel-Plaau not» that ttit

• T * of incurred tetuií cotit?

' Convinion riti at the Pnf d>v ot Ihï flrif mofiffi follow

tiiifd partyfies) (Ys( (il nECessary)

Cmtollhr cerüBcato ^ ^ ^ ^ ^ H

Coslofttucirrtllicate ^ ^ ^ ^ ^ M

• > . . « • • ' - . ^ ^ ^ ^ ^ ^

T«.l 1« > «l + IV.l I^I^I^H

....hac-aunr

lame principie apoliaifor raceipti

Contracior

g tht penad covjrtd tiy tt it F<n*no•i s u t . m e n i '

No

YesNo

Third Pariy(iFt) |tl neces

Third Parly 1 (Ï1)

• ConvaniDn

- Convmion

^•1-jj 'J li *l\l

• Concisión

- Convvilon

fue of ffii D m of incurn

m t o f t h e Data of incurra

rat* of th* fir« dav al th*

••••i

rate of the fir« day gf Pr*

d Ktuai cotí»1'

d BCIU« CHtt^

Ini moniri following ilia par

d KtU«i CQtt* '

ñrmE month lotto*

• •fing m a P C

•E

•

«3d

covered by Ihi

• • •• • •covtrid tr» itn

Third Party 2 (Y2)

Third Pany 3 (Y3|

Third Party 4 (Y4|

Fmancial State rtwnl'

Yes

YesNo

Y as

No

No

<-Contr»ctDrJ» C«rttflcif

untí f"t

cotlx declared «bova artdirtctlr r *MUd ta ti* rsuurc« w e d to r«Kh ttit oDjccttvn of tie project,

- Ih* iKnpti d*cln*d tbavt ara directly ralaUS to in rnourcei uaed to K M m e ctijactivH of Hit pojad,

coan deder*d aQove tali within the de"n«on ol rti^bl* cost» > » o f e d in Artidn II Id II10. II 2\. 1132 and II2S of Ihe centrad »nd. It releiint, m Armai lit ai>d Ancla * (»p»cwl clauwi) of

onlract.

receipt» declirad abevs lall within Die deftnigon of raceiptupiciliedin Aitcle H 23 D i m e contract.

- ITis mta it» gsnaralaQ by th* pre-financing Oaclared above M l a n n m » ïie definnionol Amela II 27 of the contrae!.

n o c e m r y adjuttment» Mptrnlly lo coata «poflad in pinioui Finmäel Staum«nt(il p*t Acïmty hav*ba*nincofporaleilino>a »bo*« Statement,

- bi* aba** informaDon ó>clved i« complele and true .

srê I« full njppwmad«üm.<il»tw!toiut0fyttí»info<misofi nereby deaorM ItwIlbonKla • • * » ! » • ri thariauHtof th* Commission «na jn m e event of an audilDyihe C o m m m i o n moja- b

Court of AudfTor« and/or Ihsii aumon«*d

rapnmnfartlva»

20/36

Holrwast First Management Report

2.3. SAPM

Form C - M o d » I of flmnciil S Ule ment per Aelivily (to Btfllltd t y n n e

Type of instrumentProjet Title [or Acronym)

Contractor's Legal N a m eLegal Type

Contaci PersonTelecopy