final results fy december 2005 -...

TRANSCRIPT

Final Results FY December 2005

John Dawson and Maddy ScottMarch 23rd 2006

Introduction to Alliance Pharma plc

Floated on AIM in December 2003Building a portfolio of branded prescription products via strategy of

Acquisition (30 brands since 1998)In-house development (2 clinical developments for EU)

Portfolio balancedCore brands – Cash generative, no promotional investmentGrowth brands – incremental growth opportunities requiring investment

Annualised turnover running at £15m, profitableTwo transformational opportunities

Periostat – Enzyme suppressant for periodontitisPosidorm – melatonin for sleep disorders

Historically UK & Ireland – now internationalisingHighly experienced & diverse management team

A history of successful acquisitions

Oct2004

Oct2004

Feb2004

Feb2006

Sep2002

Apr2002

Oct2001

Aug2001

Jan1999

Apr1998

NaseptinNaseptin

Pragmatar

Broflex

Biorphen

Distamine Symmetrel

Slow-K

Alphaderm

Aquadrate

Nu-Seals Acnisal Periostat

Pentrax

Occlusal

Meted

Forceval Hydromol16 Brands

RheumatoidArthiritis

Parkinson’sDisease

Creams forDry skin

& eczema

Enteric Coatedaspirin

4 Dermabrands Periodontitis Rx Multi-

VitaminEmollient

Range

Potassiumdeficiencies

£2.1 M £0.5 M £4.0 M £2.1 M £9.0 M £0.9 M £1.8 M £7.0 M £3.3 MFosteringArrangement

Overview

Financial highlights

Operational highlights

New product pipeline

Implementation of strategy

Outlook

Operational performance

661

2,167

54.3%

12,276

10 months to Dec-05

£000

408

2,261

52.4%

11,826

Yr endFeb-05

£000

Profit pre tax

EBIT

Gross margin %

Turnover

£6.1m £6.3m

£8.3m

£10.4m£11.8m £12.3m

-1.0

1.0

3.0

5.0

7.0

9.0

11.0

13.0

15.0

Feb-01 Feb-02 Feb-03 Feb-04 Feb-05 Dec-05

Sales Performance Full Year

Half Year to Aug-05

Ann

ualis

ed D

ec-0

5 R

esul

t

12 m

onth

s to

Dec

-05

12 m

onth

s to

Dec

-04

10 m

onth

s

Sales – 10 months to December 2005

Syntocinons £1.1m- obstetrics

NutritionForceval £2.4m

Others £2.8m

Periostat £0.3m- dental

Derma £1.6mHydromol 2007 + £1.5m

Symmetrel £1.3m - Parkinsons

Nu-Seals £2.8m- Cardiovascular (IRL)

Sales for the 10 months to December 2005

CORE BRANDS 54% GROWTH BRANDS 46%

Sales: Core brands

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

Jan-0

2Apr-

02Ju

l-02

Oct-02

Jan-0

3Apr-

03Ju

l-03

Oct-03

Jan-0

4Apr-

04Ju

l-04

Oct-04

Jan-0

5Apr-

05Ju

l-05

Oct-05

Monthly SalesMoving Average

£'m

Sales: Growth Brands

0.6

1.1

1.6

2.1

2.6

Jan-0

2Apr-

02Ju

l-02

Oct-02

Jan-0

3Apr-

03Ju

l-03

Oct-03

Jan-0

4Apr-

04Ju

l-04

Oct-04

Jan-0

5Apr-

05Ju

l-05

Oct-05

Nu-Seals 75mg ROI MAT£'m

Note: Sales figures for existing products are based on 12 months sales to December 2005

0.60.70.80.91.01.11.21.31.41.51.6

Jan-0

2Apr-

02Ju

l-02

Oct-02

Jan-0

3Apr-

03Ju

l-03

Oct-03

Jan-0

4Apr-

04Ju

l-04

Oct-04

Jan-0

5Apr-

05Ju

l-05

Oct-05

Symmetrel MAT£'m

£1.3m £1.5m

£3.6m

£5.0m

£6.2m£6.7m

54.3%52.4%48.4%

24.3% 24.3%

43.7%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Feb-01 Feb-02 Feb-03 Feb-04 Feb-05 Dec-05

£m

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

Gross Margin Gross Margin %

Gross Margin Performance

Half Year to Aug-05

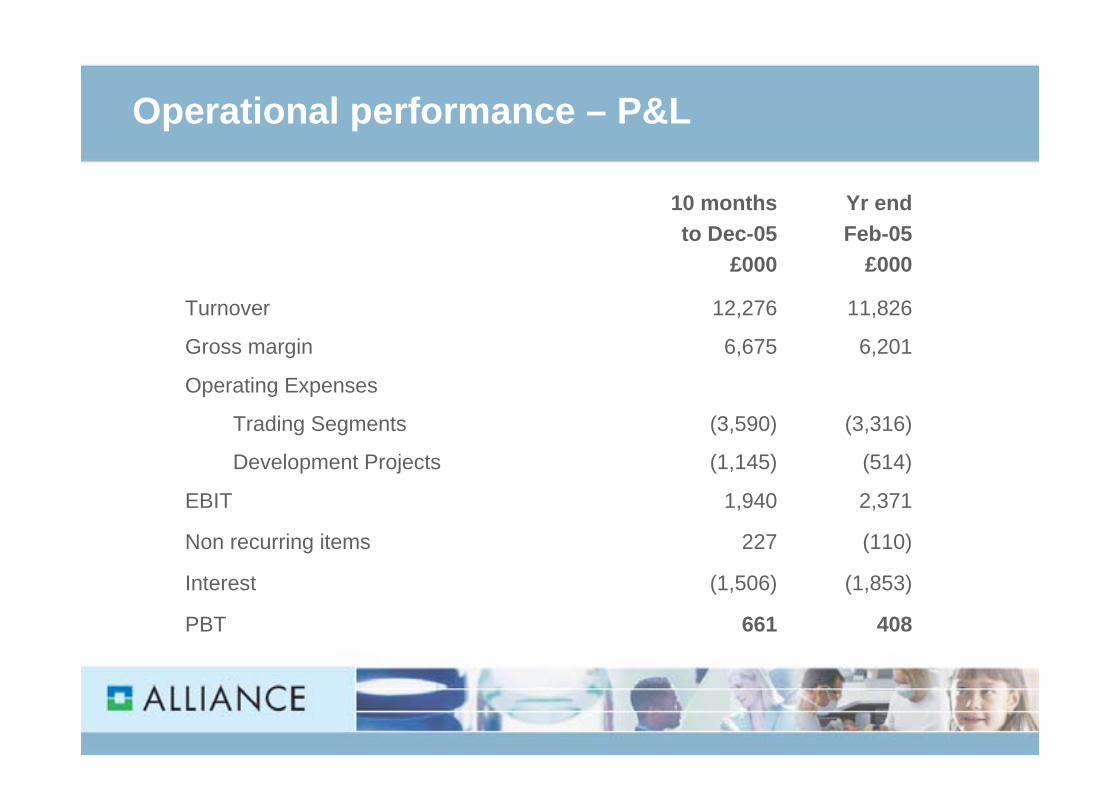

Operational performance – P&L

(110)227Non recurring items

408661PBT

(1,853)(1,506)Interest

2,3711,940EBIT

Operating Expenses

(514)(1,145)Development Projects

(3,590)

6,675

12,276

10 months to Dec-05

£000

(3,316)

6,201

11,826

Yr endFeb-05

£000

Trading Segments

Gross margin

Turnover

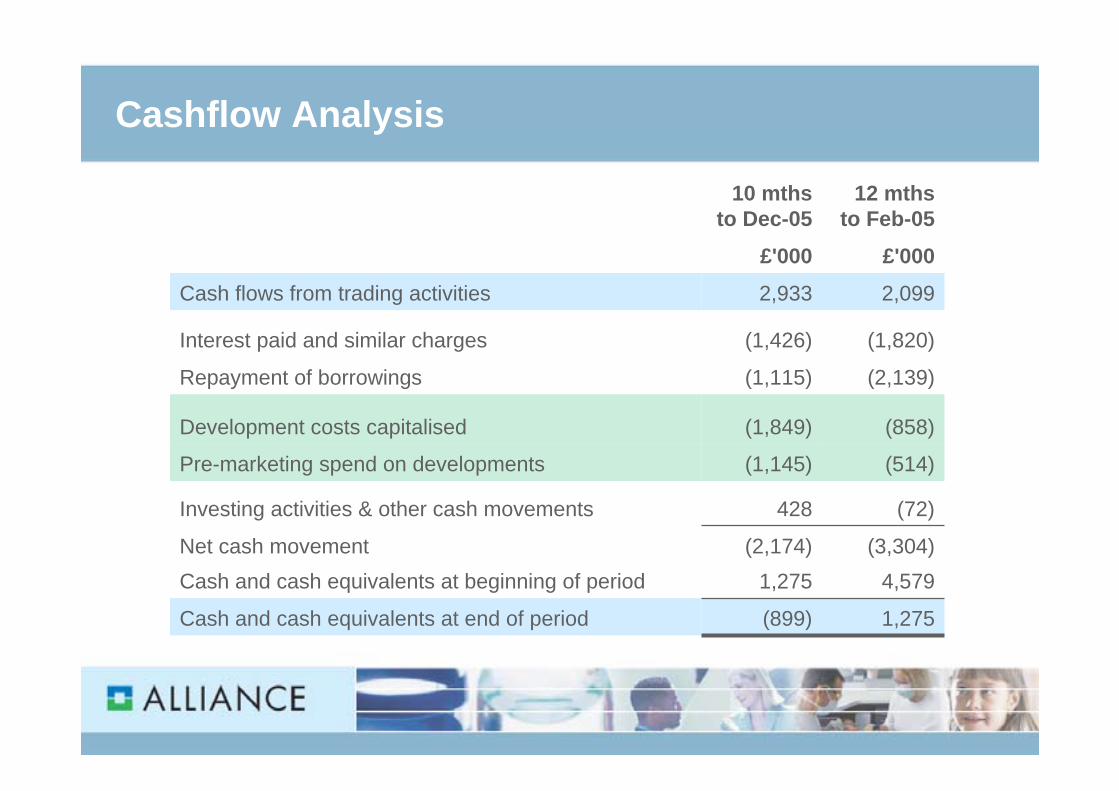

Cashflow Analysis

1,275(899)Cash and cash equivalents at end of period

4,5791,275Cash and cash equivalents at beginning of period(3,304)(2,174)Net cash movement

(72)428Investing activities & other cash movements

(514)(1,145)Pre-marketing spend on developments

(858)(1,849)Development costs capitalised

(2,139)(1,115)Repayment of borrowings

(1,820)(1,426)Interest paid and similar charges

2,0992,933Cash flows from trading activities

£'000£'000

12 mths to Feb-05

10 mths to Dec-05

Balance sheet

1,3463,075Development Costs

26,74926,631Brands acquired

28,40130629,987281Tangible Assets

7,505

(7,500)

(15,821)

(899)

1,738

Dec-05£000

(7,500)Convertible Loan Stock

1,275Cash at Bank

6,824Total Equity

(16,724)Bank Term Loans and borrowings

1,372Net Current Assets

Fixed Assets

Feb-05£000

Financial Highlights

10 month period

Sales growth in line with expectations3.8% in 10 monthsAnnualised 24.6% growth

Gross margin as percentage of sales +2%Higher margin products

Operating expenses being tightly controlled

Profits within expectations at £661k

Operational Highlights

Built dental therapeutic focus

Re-established Forceval brand

Gained critical mass in dermatologyHydromol acquisition

Developed international presence

Built Dental therapeutic focus – Medical Background

Periostat for periodontitisNovel enzyme suppressant action

Oral medication for 3 – 9 months

Adjunctive therapy following routine

treatment in surgery

Established practice in US Grew to $50m in 5 years

Built Dental therapeutic focus – Commercial Potential

Acquired from Collagenex Inc for £1.8m in November 2004

Territories – Expanded EU + 6 othersPossible further extensions

3.3m adults in UK have periodontitis6 months treatment costs ~ £70

Responding to promotion

Built Dental therapeutic focus – Performance to date

Periostat Cash Sales

-5.0

10.015.020.025.030.035.040.045.0

Jun-05 Sep-05 Dec-05

£'00

0

Appointed Head of Dental – April 2005Commenced promotion – August 2005

Partnership with OralDent for general dental practitionersOwn field force calling on dental hospitals

Re-established Forceval BrandForceval & Uniflu (International) Sales

-

100.0

200.0

300.0

400.0

500.0

600.0

Jan-05 Feb-05 Mar-05 Apr-05 May-05 Jun-05 Jul-05 Aug-05 Sep-05 Oct-05 Nov-05 Dec-05

£'00

0

MonthlyMQA

Acquired from company in administration - £7m, Nov 2004Well established but previously neglected

The only multi-vitamin registered as a medicine

Management and support restored to brandNICE endorses nutritional support in hospitals

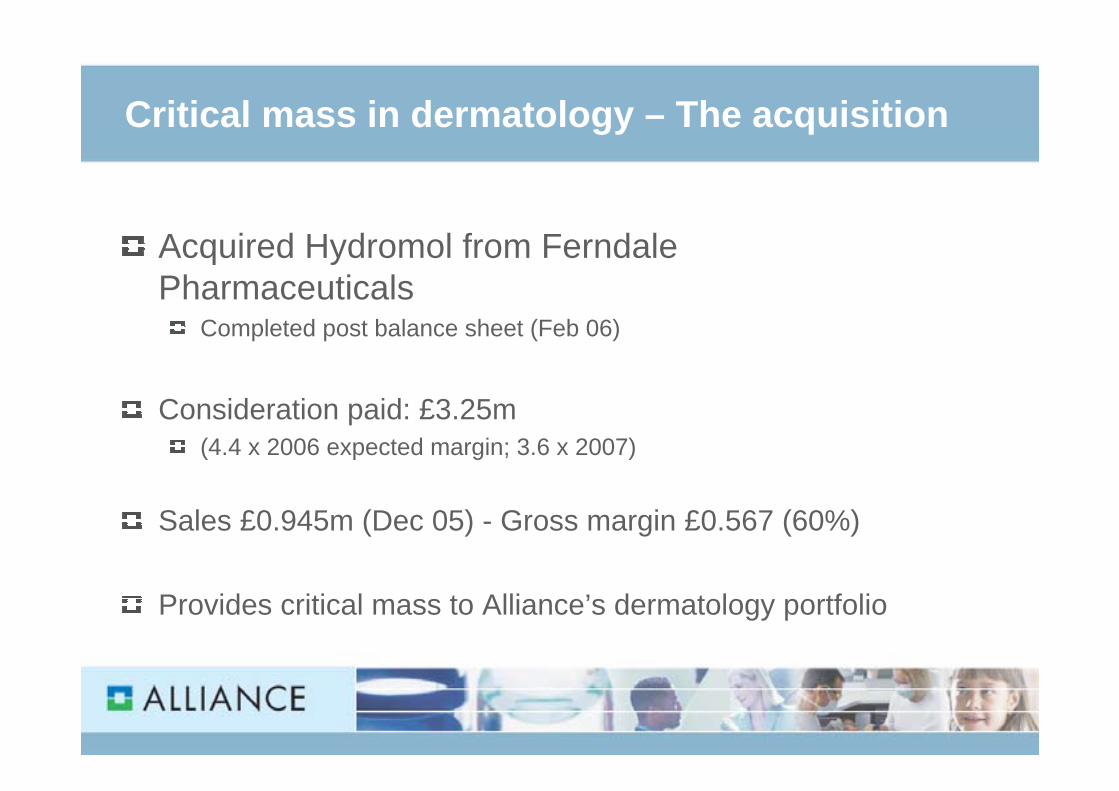

Critical mass in dermatology – The acquisition

Acquired Hydromol from Ferndale Pharmaceuticals

Completed post balance sheet (Feb 06)

Consideration paid: £3.25m (4.4 x 2006 expected margin; 3.6 x 2007)

Sales £0.945m (Dec 05) - Gross margin £0.567 (60%)

Provides critical mass to Alliance’s dermatology portfolio

Critical mass in dermatology – The opportunity

UK Emollient market £99.3m (+10.5%) IMS Dec 05

Growth opportunityA growing emollient range +31% (UK)Ability to introduce line extensionsAbility to widen distribution via network of international distributors

Specialist UK field force increased from 7 to 9

Developed International presence

Gained distributor relationships via acquisitions of Forceval and Periostat

Appointed head of international sales – May 2005

Rejuvenated neglected relationships

Sales: £0.9m Dec 2005

Actively seeking further growth opportunities

New product pipeline: Posidorm - Progress

1.5mg surge-sustained melatonin for sleeping disorders

Started phase III trial programme July 2005Shiftwork sleep disorder

300 patients, randomised, double blind, crossover designSleeping disorders in the elderly with no obvious cause

300 patients, randomised, double blind, crossover design

Toxicology programme running in parallel

Pre-marketing activitiesInternational trade mark registrationMarket researchKOL development

Outlicensing discussions progressing

New product pipeline: Posidorm - Potential

Current sleeping disorder market across EU is £500m

Only 20% of sufferers currently receive treatment

Current treatments with hypnotics – undesirable side effects

Market forecast to expanddouble by 2010 [Frost & Sullivan, 2004]

7-fold increase by 2020 [Espicom 2004]

New product pipeline: Isprelor - Progress

Misoprostol 25mcg vaginal tablet for induction of labour

Previous studies in literature show intra-vaginal misoprostol to be more efficacious than dinoprostone

Development canvassed by RCOG in 2001

Started phase III trial programme January 2005Randomised, open design versus dinoprostone gel1012 patients [50% first pregnancy; 50% second or further pregnancy]Primary endpoint – delivery within 24hours

New product pipeline: Isprelor - Potential

Pre-marketing activitiesInternational trade mark registrationMarket researchKOL development

Successful satellite symposium devoted to misoprostol at RCOG International conference in Cairo, Sept 2005

Niche specialised opportunityCurrent EU market: 700,000 inductions pa; £13m

Out-licensing discussions ongoing

Implementation of StrategyBuilt the business base by low risk brand acquisitions

9 deals in 8 yearsSelectively invested for growth

PeriostatSymmetrelNu-SealsDermatology

Progressed development of new launchesPosidormIsprelor

Developed international presence in measured fashion

6.75.0Gross Margin £m

12.310.4Sales £m

10 Months 20052003 (FY Feb 2004)

Outlook

Building the business baseAcquisition candidates available

Selectively growing brandsPeriostat promotionDermatology promotion

Developing new launchesIsprelor trialsPosidorm developmentOther pipeline assessmentsOut-licensing

Newsflow