finance 30210: managerial economics cost analysis

Post on 19-Dec-2015

232 views

TRANSCRIPT

Finance 30210: Managerial Economics

Cost Analysis

Here’s the overall objective for the supply side

Factor Markets

Production Decisions

Product Markets

Supply/Demand Determines Factor prices (We have covered this)

Factor Usage/Prices Determine Production Costs (We are here now)

Demand determines markup over costs (Coming soon!)

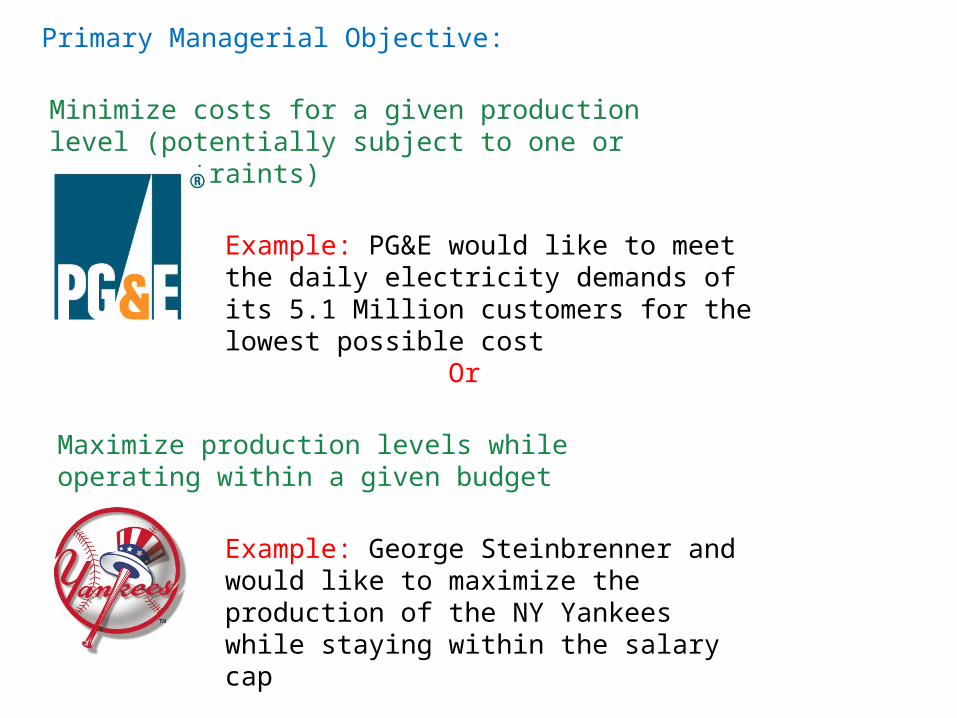

Primary Managerial Objective:

Minimize costs for a given production level (potentially subject to one or more constraints)

Or

Maximize production levels while operating within a given budget

Example: PG&E would like to meet the daily electricity demands of its 5.1 Million customers for the lowest possible cost

Example: George Steinbrenner and would like to maximize the production of the NY Yankees while staying within the salary cap

The starting point for this analysis is to think carefully about where your output comes from. That is, how would you describe your production process

,...,, 321 XXXFQ Production Level

“is a function of”

One or more inputs

A production function is an attempt to describe what inputs are involved in your production process and how varying inputs affects production levels

Note: We are not trying to perfectly match reality…we are only trying to approximate it!!!

Some production processes might be able to be described fairly easily:

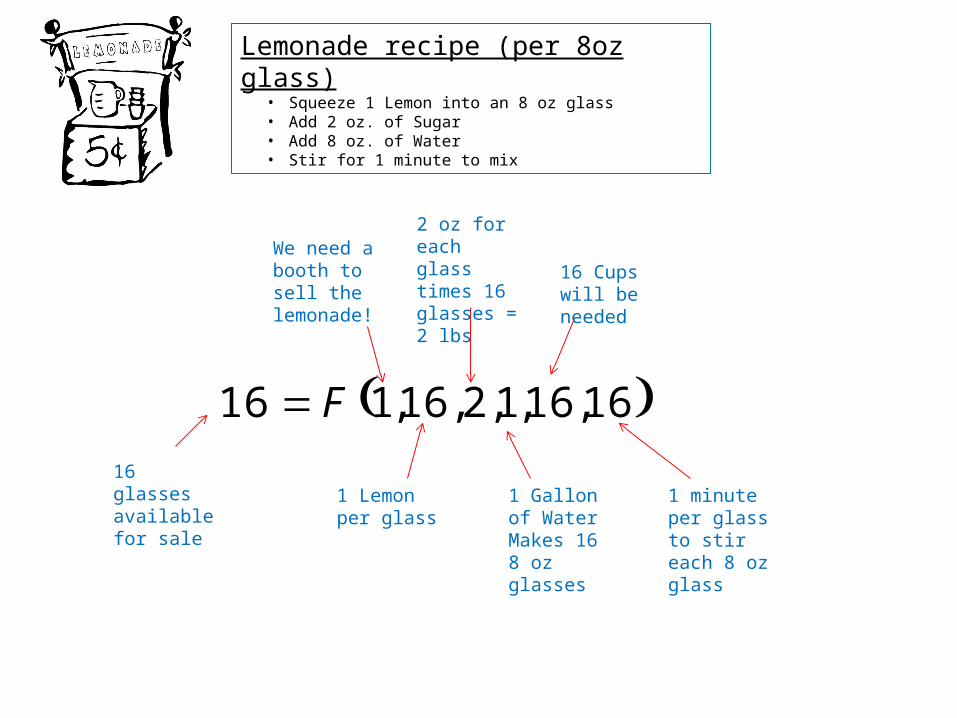

TCWSLBFQ ,,,,,

8 Oz. Glasses of Lemonade

Booth(s)

Lemons

Sugar (Lbs)

Water (Gallons)

Your Time (Minutes)

Paper Cups

With a fixed recipe for lemonade, this will probably be a very linear production process

Lemonade recipe (per 8oz glass)• Squeeze 1 Lemon into an 8 oz glass• Add 2 oz. of Sugar• Add 8 oz. of Water• Stir for 1 minute to mix

16,16,1,2,16,116 F

1 Gallon of Water Makes 16 8 oz glasses

1 minute per glass to stir each 8 oz glass

16 Cups will be needed

2 oz for each glass times 16 glasses = 2 lbs

1 Lemon per glass

We need a booth to sell the lemonade!

16 glasses available for sale

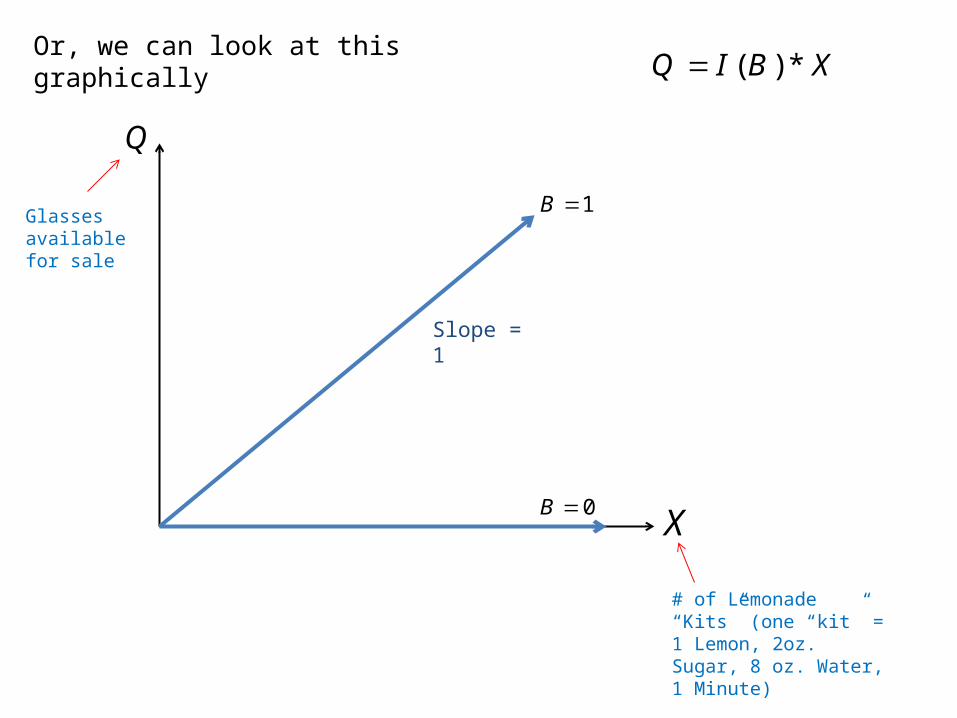

In fact, we could write the production function very compactly:

XBIQ *)(

Lemonade recipe (per 8oz glass)• Squeeze 1 Lemon into an 8 oz glass• Add 2 oz. of Sugar• Add 8 oz. of Water• Stir for 1 minute to mix

# of Lemonade “Kits” (one “kit” = 1 Lemon, 2oz. Sugar, 8 oz. Water, 1 Minute)

Indicator Function

1 ,1

0 ,0)(

Bif

BifBI

Q

X

XBIQ *)(Or, we can look at this graphically

1B

0B

Slope = 1

# of Lemonade “Kits” (one “kit” = 1 Lemon, 2oz. Sugar, 8 oz. Water, 1 Minute)

Glasses available for sale

Some production processes might be more difficult to specify:

How would you describe the production function for the business school?

,..., 21 XXFQ

Output(s)Input(s)

How would you describe the production function for the business school?

What is the “product” of Mendoza College of Business? YOU ARE!

Degrees

Undergraduate (BA)

1 Year MBA (MBA)

2 Year MBA (MBA)

South Bend EMBA (MBA)

Chicago EMBA (MBA)

Finance

Accounting

Marketing

Management

Masters of Accountancy (MA)

Masters of Nonprofit Administration (MA)

How would you describe the production function for the business school?

How would you characterize the “inputs” into Mendoza College of Business

Facilities• Classroom Space• Office Space• Conference/Meeting Rooms Personnel

• Faculty (By Discipline)• Administrative • Administrative Support• Maintenance

StaffEquipment• Information Technologies• Communications• Instructional Equipment

Capital Inputs

Labor Inputs

How would you describe the production function for the business school?

Have we left out an output?

Notre Dame, like any other university, is involved in both the production of knowledge (research) as well as the distribution of knowledge (degree programs)

LaborCapitalF ,Research

Degrees

Should the two outputs be treated as separate production processes?

LaborCapitalF ,Research

Degrees

The next question would be: What is your ultimate objective?

Is Notre Dame trying to maximize the quantity and quality of research and teaching while operating within a budget?

Is Notre Dame trying to minimize costs while maintaining enrollments, maintaining high research standards and a top quality education?

OR

Does it matter?

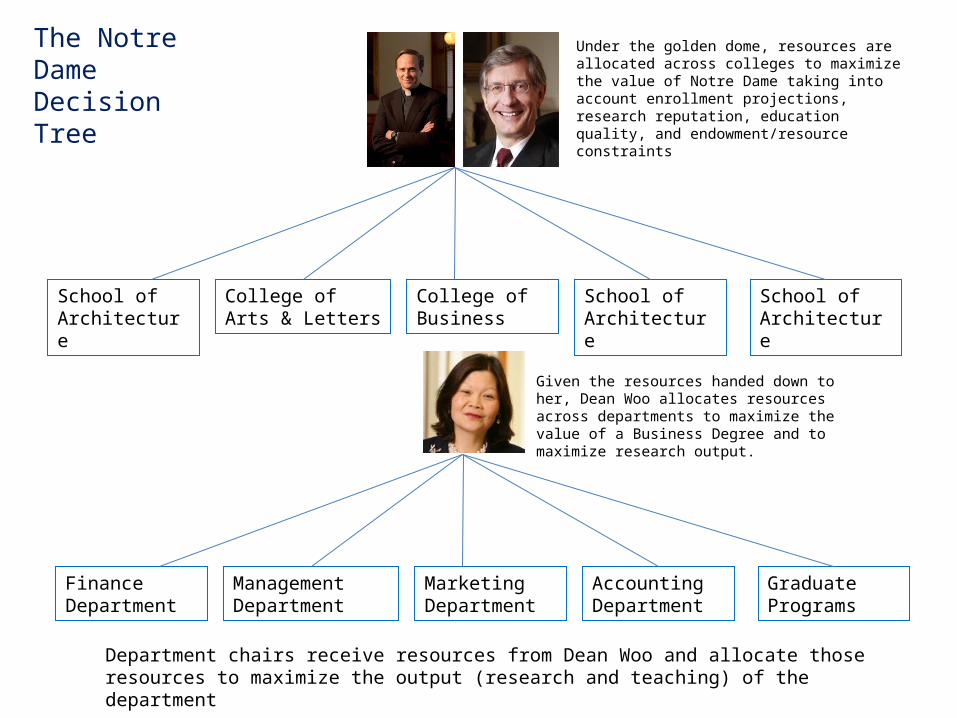

School of Architecture

College of Arts & Letters

College of Business

School of Architecture

School of Architecture

Finance Department

Management Department

Marketing Department

Accounting Department

Graduate Programs

Under the golden dome, resources are allocated across colleges to maximize the value of Notre Dame taking into account enrollment projections, research reputation, education quality, and endowment/resource constraints

The Notre Dame Decision Tree

Given the resources handed down to her, Dean Woo allocates resources across departments to maximize the value of a Business Degree and to maximize research output.

Department chairs receive resources from Dean Woo and allocate those resources to maximize the output (research and teaching) of the department

Another issue has to do with planning horizon.

Different resources are treated as unchangeable (fixed) over various time horizons

Now 6 mo 1 yr 2 yr 5 yr 10 yr

It could take 6 months to install a new computer network

It takes 1 year to hire a new faculty member

It might take 5 years to design/build a new classroom building

Tenured faculty are essentially can’t be let go

Shorter planning horizons will involve more factors that will be considered fixed

From here on, lets keep things as simple as possible…

You produce a single output. There is no distinction as far as quality is concerned, so all we are concerned with is quantity. You require two types of input in your production process (capital and labor). Labor inputs can be adjusted instantaneously, but capital adjustments require at least 1 year

LKFQ ,

Total Production

“Is a function of”

Capital (Fixed for any planning horizon under 1 year

Labor (always adjustable)

Some definitions LKFQ ,

Marginal Product: marginal product measures the change in total production associated with a small change in one factor, holding all other factors fixed

L

QMPL

K

QMPK

Average Product: average product measures the ratio of input to output

L

QAPL

K

QAPK

Elasticity of Production: marginal product measures the change in total production associated with a small change in one factor, holding all other factors fixed

L

LL AP

MP

L

Q

%

%K

KK AP

MP

K

Q

%

%

Over a short planning horizon, when many factors are considered fixed (in this case, capital), the key property of production is the marginal product of labor.

LKFQ , L

QMPL

For a given production function, the marginal product of labor measures how production responds to small changes in labor effort

Q

L

),( LKF

Q

L

),( LKF

OR

Diminishing Marginal Returns: As labor input increases, production increases, but at a decreasing rate

Increasing Marginal Returns: As labor input increases, production increases, but at an increasing rate

0),( LKFll0),( LKFll

Consider the following numerical example:

32 0029.3. LLKQ We start with a production function defining the relationship between capital, labor, and production

Capital is fixed in the short run. Let’s assume that K = 1

32 0029.3.1 LLQ

Suppose that L = 20.

8.96200029.203.1 32 Q

32 0029.3. LLKQ

96.8

Maximum Production reached at L =70

Labor

Qua

ntity

Increasing Marginal Returns

Decreasing Marginal Returns

Negative Marginal Returns

Now, let’s calculate some of the descriptive statistics

Labor (L) Quantity (Q) MPL APL Elasticity

0 0 --- --- ---

1 .2971 .2971 .2971 1

2 1.1768 .8797 .5884 1.495

3 2.6217 1.4449 .8739 1.653

4 4.6114 1.9927 1.1536 1.727

5 7.1375 2.5231 1.4275 1.7674

32 0029.3. LLKQ

Recall, K = 1

L

QMPL

L

QAPL

L

LL AP

MP

The properties of the marginal product of labor will determine the properties of the other descriptive statistics

1L

LL AP

MPElasticity of production less than one indicates MP<AP (Average product is falling)

Elasticity of production greater than one indicates MP>AP (Average product is rising)

1

MP hits a maximum at L = 35

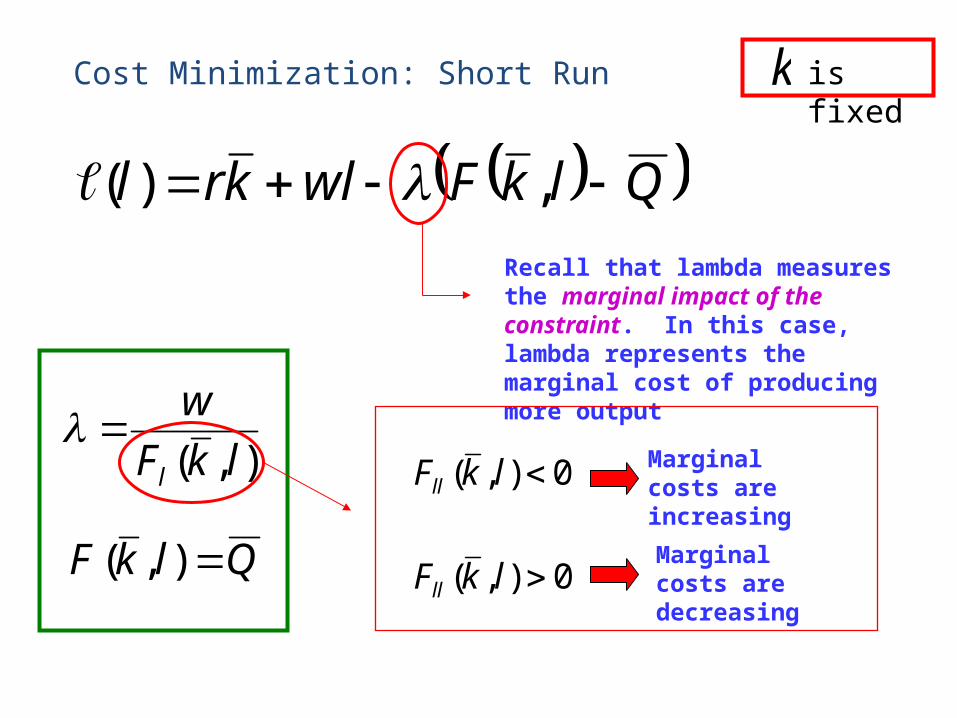

Cost Minimization: Short Run

The cost function for the firm can be written as

wlkrCostsTotal Given the costs of the firm’s inputs, the problem facing the firm is to find the lowest cost method of producing a fixed amount of output

QlkF

tosubject

wlkrMinl

),(

Capital costs are fixed in the short run!

Cost Minimization: Short Run k is fixed

QlkFwlkrl ,)(

0),()( lkFwl ll

First Order Necessary Conditions

),( lkFQ

),( lkF

w

l

QlkF ),(

Remember…this needs to be positive!!

Marginal costs refer to changes in total costs when production increases

dQ

wlkrdMC

Q

wl

Q

kr

Q

wlkrAC

Average (Unit) costs refer to total costs divided by total production

Average fixed costs fall as output increases

With capital fixed, marginal costs are only influenced by labor decisions in the short run

Cost Minimization: Short Run k is fixed

QlkFwlkrl ,)(

),( lkF

w

l

QlkF ),(

Recall that lambda measures the marginal impact of the constraint. In this case, lambda represents the marginal cost of producing more output

0),( lkFll

0),( lkFll

Marginal costs are increasing

Marginal costs are decreasing

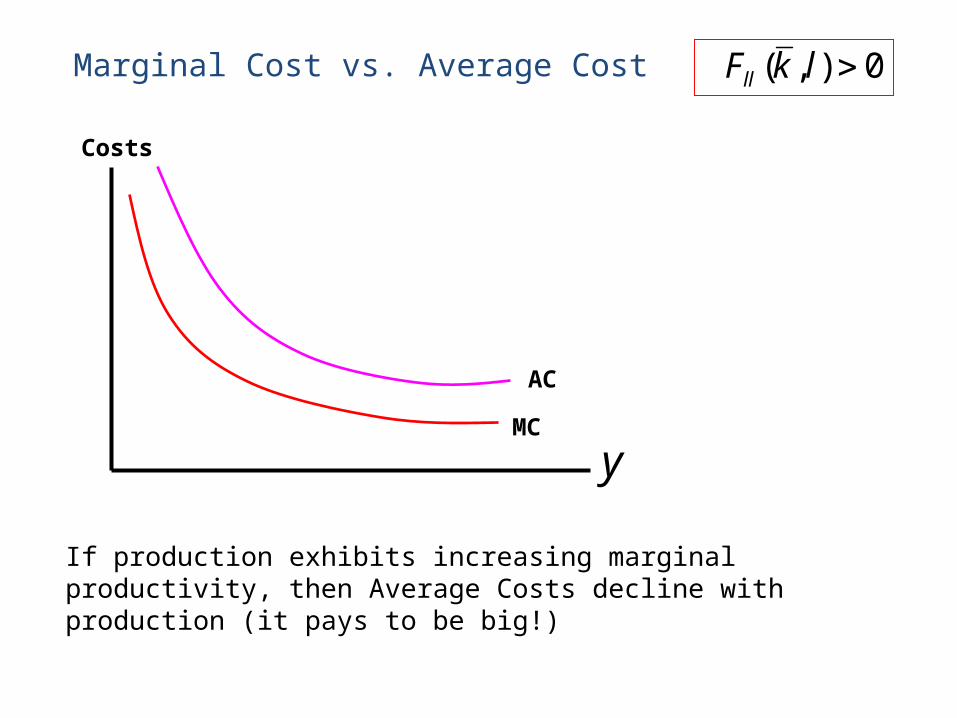

Marginal Cost vs. Average Cost

y

Costs

MC

AC

Minimum AC occurs where AC=MC

0),( lkFll

When AC is greater than MC, AC Falls

When AC is less than MC, AC rises

Marginal Cost vs. Average Cost

y

Costs

MC

AC

0),( lkFll

If production exhibits increasing marginal productivity, then Average Costs decline with production (it pays to be big!)

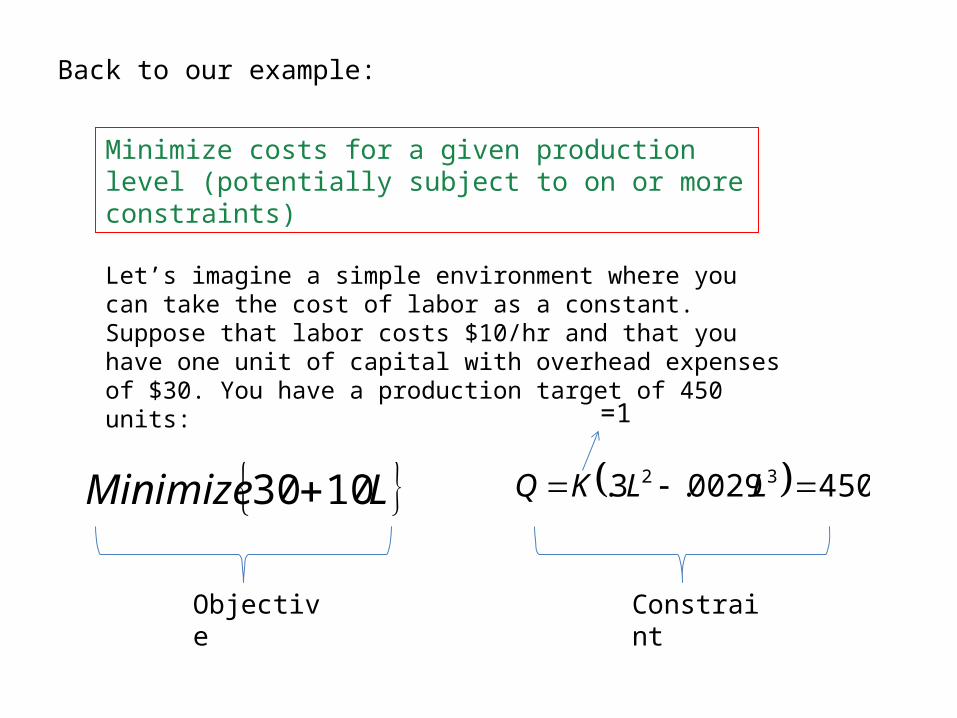

Back to our example:

Minimize costs for a given production level (potentially subject to on or more constraints)

Let’s imagine a simple environment where you can take the cost of labor as a constant. Suppose that labor costs $10/hr and that you have one unit of capital with overhead expenses of $30. You have a production target of 450 units:

4500029.3. 32 LLKQ LMinimize 1030

Objective Constraint

=1

4500029.3. 32 LLKQ

450 Units of production requires 60 hours of labor (assuming that K=1)

Labor

Qua

ntity

450

With only one variable factor, there is no optimization. The production constraint determines the level of the variable factor.

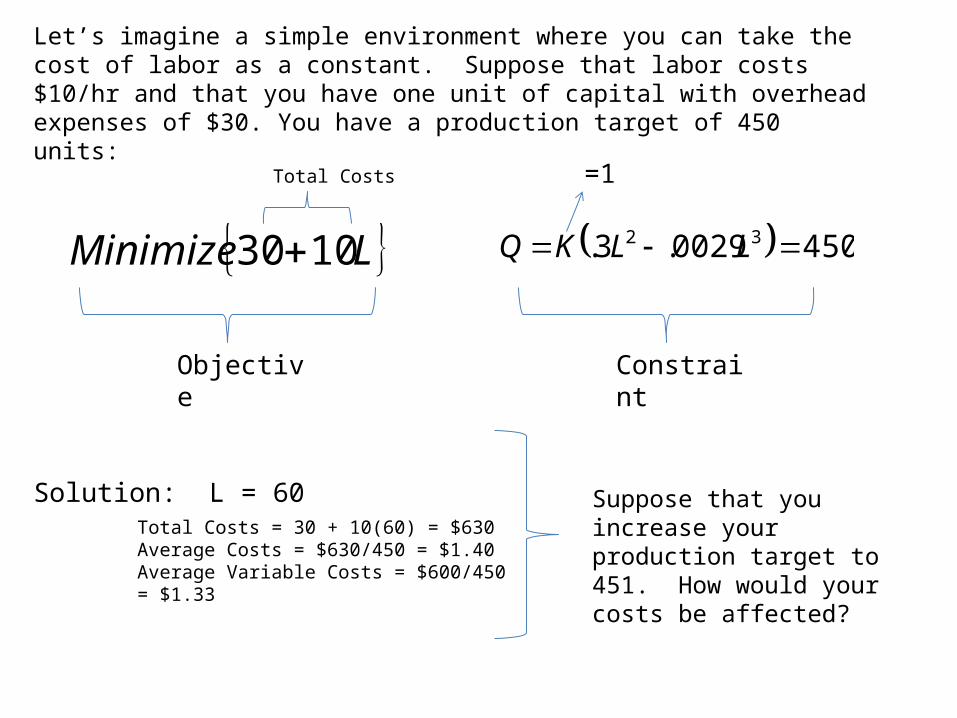

Let’s imagine a simple environment where you can take the cost of labor as a constant. Suppose that labor costs $10/hr and that you have one unit of capital with overhead expenses of $30. You have a production target of 450 units:

4500029.3. 32 LLKQ LMinimize 1030

Objective Constraint

=1

Solution: L = 60

Total Costs

Total Costs = 30 + 10(60) = $630Average Costs = $630/450 = $1.40Average Variable Costs = $600/450 = $1.33

Suppose that you increase your production target to 451. How would your costs be affected?

Labor (L)

Quantity (Q)

MPL APL W MC AVC

0 0 --- --- --- ---

1 .2971 .2971 .2971 10 33.65 33.65

2 1.1768 .8797 .5884 10 11.36 16.99

3 2.6217 1.4449 .8739 10 6.92 11.44

4 4.6114 1.9927 1.1536 10 5.01 8.66

60 450 4.68 7.5 10 2.13 1.33

L

QMPL

If the marginal product of labor measures output per unit labor, then the inverse measures labor required per unit output

L

QAPL

LAP

w

Q

wLAVC

We also know that the average variable cost is related to the inverse of average product

LMP

wMC

1L

LL AP

MPElasticity of production less than one indicates MP<AP (Average product is falling)

Elasticity of production greater than one indicates MP>AP (Average product is rising)

MC<AVC. Average Variable Cost is falling

MC>AVC. Average Variable Cost is Rising

MC hits a minimum at L = 35

Properties of production translate directly to properties of cost

Labor

For now, we are only dealing with the cost side, but eventually, we will be maximizing profits.

4500029.3. 32 LLKQ LMinimize 1030

Objective Constraint

=1Total Costs

We just minimized costs of one particular production target. Maximizing profits involves varying the production target (knowing that you will minimize the costs of any particular target). There should be one unique production target that is associated with maximum profits:

Maximum Profits MCMR

Q

TCMC

Q

TRMR

LMP

wMC wMPMR L *

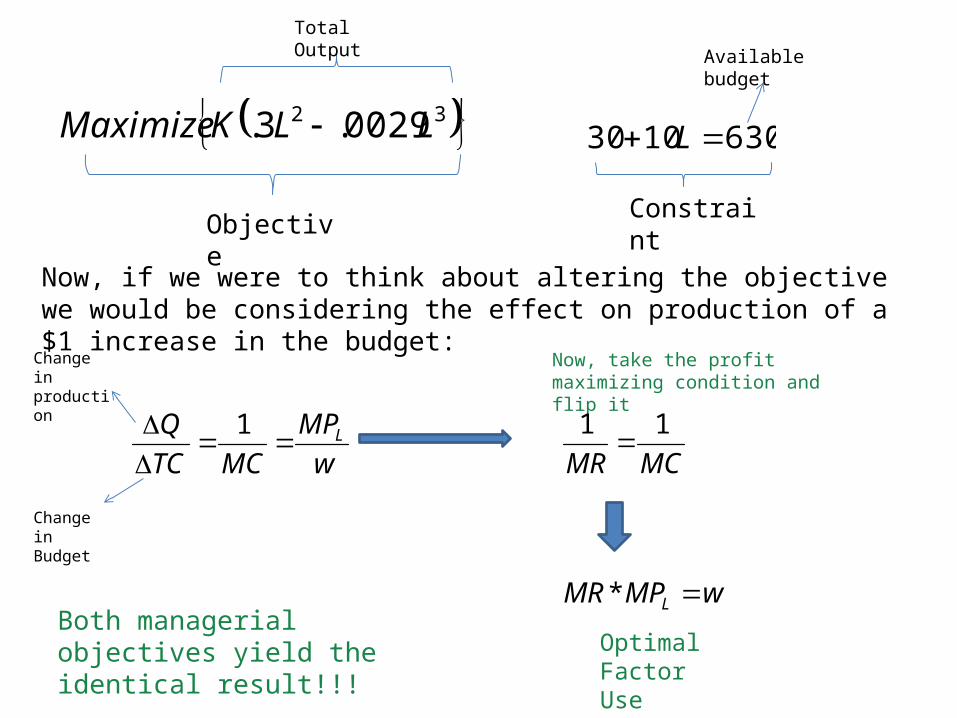

Optimal Factor Use

6301030 L 32 0029.3. LLKMaximize

ObjectiveConstraint

Total Output

Maximize production levels while operating within a given budget

Recall the alternative management objective:

Let’s imagine a simple environment where you can take the cost of labor as a constant. Suppose that labor costs $10/hr and that you have one unit of capital with overhead expenses of $30. You have a production budget of $630:

Available budget

$630 budget restricts you to 60 hours of labor (assuming that overhead = $30)

Labor

Cos

t

630

Just like before, there is no optimization. The budget constraint determines the level of the variable factor.

6301030 L

6301030 L 32 0029.3. LLKMaximize

ObjectiveConstraint

Total Output Available budget

Now, if we were to think about altering the objective we would be considering the effect on production of a $1 increase in the budget:

w

MP

MCTC

Q L 1

Change in production

Change in Budget

Now, take the profit maximizing condition and flip it

MCMR

11

wMPMR L *

Optimal Factor Use

Both managerial objectives yield the identical result!!!

Capital

Labor

An isoquant refers to the various combinations of inputs that generate the same level of production

450Q

L = 33

K = 30

L = 13

K = 2

Capital

Labor

A key property of production in the long run has to do with the substitutability between multiple inputs.

450Q

The Technical rate of substitution (TRS) measures the amount of one input required to replace each unit of an alternative input and maintain constant production

L

K

K

LTRS

Capital

Labor

Recall some earlier definitions:

450QL

K

K

L

MPTRS

MP

L

QMPL

K

QMPK

Marginal Product of Labor Marginal Product of Capital

K

L

If you are using a lot of capital and very little labor, TRS is small

The elasticity of substitution measures curvature of the production function (flexibility of production)

k

l'

k

l

k

l

TRSkl

%

%

k is variableLong Run Characteristics

Capital

Labor

Capital

Labor

Technical rate of Substitution measures the degree in which you can alter the mix of inputs in production. Consider a couple extreme cases:

Perfect substitutes can always be can always be traded off in a constant ratio

Perfect compliments have no substitutability and must me used in fixed ratios

20Q20Q

Cost Minimization: Long Run

QlkF

tosubject

wlrkMinlk

),(

,

k is variable

QlkFwlrkkl ,),(

Cost Minimization: Long Run

QlkFwlrkkl ,),(

0),(),( lkFwl ll

First Order Necessary Conditions

),( lkFQ

0),(),( lkFrl kk ),(

),(

lkF

lkF

w

r

l

k

),(),( lkF

r

lkF

w

kl

Again, back to our example

Let’s imagine a simple environment where you can take the cost of labor and the cost of capital as a constant. Suppose that labor costs $10/hr and that capital costs $30 per unit. You have a production target of 450 units:

4500029.3. 32 LLKQ LKMinimize 1030

Objective Constraint

Total Costs

Now we have two variables to solve for instead of just one!

4500029.3. 32 LLKQ

Consider two potential choices for Capital and Labor

L = 33K = 2TC = 30*2 + 33*10 = $390AC = $390/450 = $0.86

L = 13K = 30TC = 30*30 + 13*10 = $1030AC = $1030/450 = $2.29

This procedure is relatively labor intensive

This procedure is relatively capital intensive

With more than one input, there should be multiple combinations of inputs that will produce the same level of output

Capital

Labor

450Q

33

2

Total Cost = 30*2 + 33*10 = $390

4500029.3. 32 LLKQ LKMinimize 1030

Suppose that we lowered production by 1 unit by decreasing labor. What would happen to costs?

LMP

wMC

$10

20MC = $.50

Capital

Labor

450Q

33

2

4500029.3. 32 LLKQ LKMinimize 1030

Now, let’s increase production by one unit to get back to our initial production level by increasing capital

k

k

MP

PMC

$30

212

MC = $.50

MC = $.14

By altering the production process slightly, we were able to maintain 450 units of production and save $0.36!

Capital

Labor

450Q

33

2 15

11

14.212

30

k

k

MP

P

50.20

10

LMP

w

11.127

30

k

k

MP

P

12.86

10

LMP

w

Here, we have too much capital. We can save costs by substituting labor for capital

Here, we have too much labor. We can save costs by substituting capital for labor

Capital

Labor

450Q

4

22

4500029.3. 32 LLKQ LKMinimize 1030

28.106

30

k

k

MP

P

27.36

10

LMP

w

Total Cost = 30*4 + 10*22 = $340Average Cost = $.75

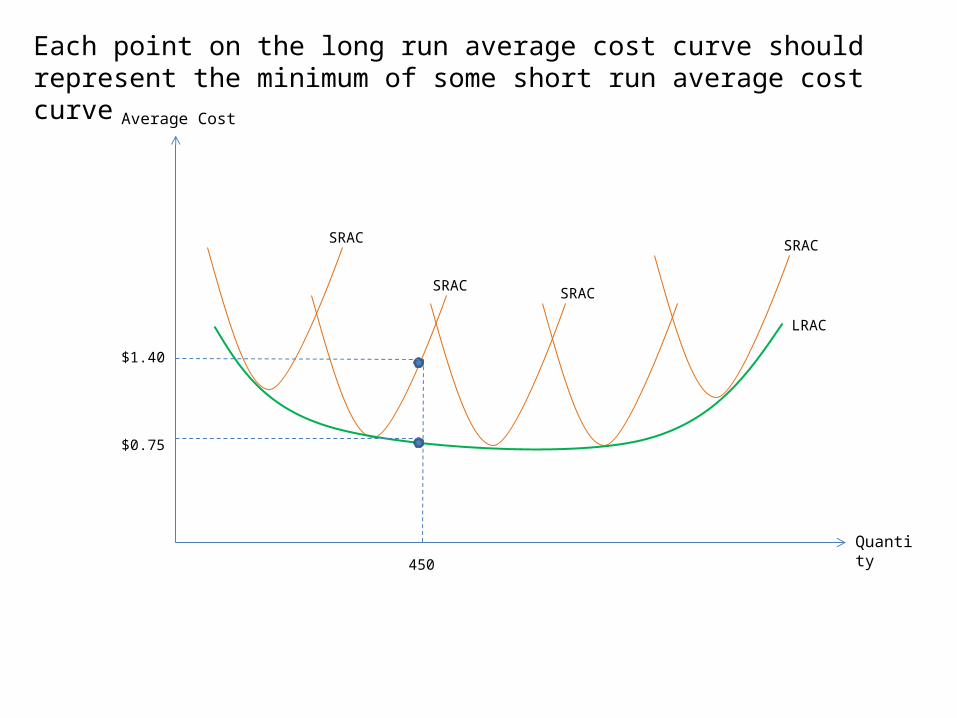

Short Run vs. Long Run

4500029.3. 32 LLKQ LKMinimize 1030

Solution: L = 60 (K Fixed at 1)

Total Costs = 30 + 10(60) = $630Average Costs = $630/450 = $1.40Average Variable Costs = $600/450 = $1.33

Solution: L = 22, K = 4

Total Cost = 30*4 + 10*22 = $340Average Cost = $.75

Long Run Average Cost will always be less than or equal short run average costs due to the increased flexibility of inputs

LK

k

MP

w

MP

PMC

LMP

wMC

Average Cost

Quantity

SRAC

SRAC SRAC

SRAC

LRAC

Each point on the long run average cost curve should represent the minimum of some short run average cost curve

450

$1.40

$0.75

Suppose that the price of labor rises to $50

4500029.3. 32 LLKQ LKMinimize 5030

Solution: L = 60 (K Fixed at 1)

Total Costs = 30 + 10(60) = $630Average Costs = $630/450 = $1.40Average Variable Costs = $600/450 = $1.33

00.2$5

10

LMP

wMC

Solution: L = 60 (K Fixed at 1)

Total Costs = 30 + 50(60) = $3,030Average Costs = $3,030/450 = $6.73

00.10$5

50

LMP

wMC

In the short run, factor price changes can’t be avoided without affecting the production target, so costs are very sensitive to factor price changes

Capital

Labor

450Q

10

13

Suppose that the price of labor rises to $50

76.39

30

k

k

MP

P

80.62

50

LMP

w

4500029.3. 32 LLKQ LKMinimize 5030

In the long run, if your production technique is flexible, you can avoid cost increases!

4

22

Total Costs = 30(10) + 50(13) = $950Average Costs = $630/450 = $2.11

l

k l

w

w

mc

Elasticity of substitution determines the response of costs to changes in input prices

Low elasticity of substitution means that production is very inflexible

Low price elasticity means that factor demands don’t respond to factor prices

Costs are very sensitive to factor price changes

l

k l

w

w

mc

Elasticity of substitution determines the response of costs to changes in input prices

High elasticity of substitution means that production is very flexible

High price elasticity means that factor demands respond significantly to factor prices

Costs are very insensitive to factor price changes

Capital

Labor

450Q

22

4

As you expand production in the long run, you are adjusting both factors, so your costs will not depend on marginal products!

500Q

550Q

600Q

In the long run, we are not looking for increasing or decreasing marginal returns, but instead, we are looking for increasing or decreasing returns to scale

32 0029.3. LLKQ

Recall the production function we have been working with.

8.96200029.203.1 32 Q

1 Unit of capital and 20 units of labor generate 96.8 units of output.

Suppose we double our inputs

588400029.403.2 32 QDoubling the inputs more than doubles production! We call this increasing returns to scale

Increasing Returns to Scale

y

Costs

MC

),(2)2,2( lkFlkF

AC

Marginal costs are always less than average costs

Costs are decreasing (it pays to be big)

y

Costs MC

),(2)2,2( lkFlkF

AC

Decreasing returns to Scale

Marginal costs are always greater than average costs

Costs are increasing (it pays to be small)

Constant Returns to Scale

y

Costs

MC = AC

),(2)2,2( lkFlkF

Marginal costs are always equal to average costs

Costs are constant (size doesn’t matter)