finance lecture 5. keating f&a 5-2 spring 2008 outline lecture 5 the allure of leverage present...

TRANSCRIPT

Finance Lecture 5

Keating F&A 5-2 Spring 2008

Outline Lecture 5

• The Allure of Leverage

• Present Value Calculations

• Bond Valuation

• Stock Valuation

Keating F&A 5-3 Spring 2008

Operational Leverage MeansReplacing Variable Costs With Fixed

• Example: Automation replaces workers

• With more fixed costs, firm profits vary more with revenue

Revenue increases can be highly profitable Revenue decreases are very damaging (since the firm has so many fixed costs)

• In a governmental context, even labor can sometimes be viewed as a fixed cost if you can’t easily lay people off

Keating F&A 5-4 Spring 2008

Comparably, Financial LeverageMeans Taking On More Debt

• Debt is a fixed cost Interest payments do not vary with sales volume

• The same investment, e.g., in new plant and equipment, provides much more upside and downside to stockholders when there is debt financing

A small revenue drop can sharply reduce stockholder equity A revenue increase flows directly to a smaller number of stockholders

Keating F&A 5-5 Spring 2008

Trading Stock On Margin Is Another

Example Of Financial Leverage• Not content with simply buying stock the old-fashioned way, some investors buy yet more stock by borrowing funds from brokers

• “Margin call” – When the stock declines and the broker demands more money or stock sales to cover borrowing

• Margin traders are often blamed, fairly or unfairly, for stock market crashes and volatility

• Margin trading is not recommended for individual investors

Keating F&A 5-6 Spring 2008

Financial Leverage Works If InvestmentReturn Exceeds Borrowing Costs

• In expected value terms, financial leverage is reasonable if expected return on new asset exceeds interest rate

Given interest payments are tax deductible, this criterion is often fairly straightforward to fulfill

• Indeed, one might wonder why more firms don’t make more use of leverage

Keating F&A 5-7 Spring 2008

There Can Be An Adverse Feedback LoopBetween Leverage And Federal Deposit Insurance

• Suppose there is a savings and loan that is teetering on the edge of failure, e.g., a lot of questionable loans

If depositors are federally insured, they don’t much care Stockholders are looking at little-to-nothing in bank liquidation if nothing is done

• This teetering S&L might be tempted to increase its leverage (i.e., pay higher interest to draw in more deposits) then make high-risk, high interest loans

If loans are paid back, S&L returns to profitability and stockholders make (potentially a lot of) money If loans default, S&L fails and stockholders get nothing, but government pays off depositors Moral Hazard of the “Walking Dead”

Keating F&A 5-8 Spring 2008

Outline Lecture 5

• The Allure of Leverage

• Present Value Calculations

• Bond Valuation

• Stock Valuation

Keating F&A 5-9 Spring 2008

Interest Rates ImpactInvestment Desirability

Year 0: Pay $100Year 1: Receive $57Year 2: Receive $57

Is this a good investment?

Keating F&A 5-10 Spring 2008

Present Value Puts Investment FlowsIn Today’s Dollars, Using Interest Rate

Example: 5% interest

Desirable, PV>0

PV 100 57

1.0557

1.0525.99 0

Keating F&A 5-11 Spring 2008

Higher Interest Rates MakeGiven Investments Less Desirable

Example: 10% interest

Undesirable, PV<0

PV 100 57

1.157

1.12 1.07 0

Keating F&A 5-12 Spring 2008

An Annuity Pays A Fixed Amount

For A Fixed Number Of YearsYear 1: $100Year 2: $100Year 3: $100Year 4: $100Year 5: $100Year 6: $100

If interest rates are 7%,

PV 1001.07

100

1.072100

1.073100

1.074100

1.075100

1.076476.65

Keating F&A 5-13 Spring 2008

Outline Lecture 5

• The Allure of Leverage

• Present Value Calculations

• Bond Valuation

• Stock Valuation

Keating F&A 5-14 Spring 2008

Basic Bond Valuation Is JustA Present Value Calculation

PV INT

(1 kd )t

t1

N

M

(1 kd )N

dkis today’s prevailing market rate of interest on debt of this sort

Keating F&A 5-15 Spring 2008

Basic Bond Valuation Is JustA Present Value Calculation

Example: 5% annual coupon bond, maturing in 2017 with $1000 principal,current interest rate is 7%

57.88007.1

1000

07.1

50

07.1

5007.1

50

07.1

50

07.1

50

07.1

5007.1

50

07.1

50)2009,1_(

887

6543

2

JanPV

Note: Present Value determined by currentinterest rates, not interest rate when issued

Keating F&A 5-16 Spring 2008

Bond Values Can Fluctuate

• Changing market interest rates,

• Changing perception of default probability

• Call potential

dk

Keating F&A 5-17 Spring 2008

Bond Values Fall IfMarket Interest Rates Rise

Value of 5% coupon bond paying $1000 principal in 2017

0

200

400

600

800

1,000

1,200

1,400

1,600

0 0.02 0.04 0.06 0.08 0.1 0.12 0.14

Market Interest Rate

Pre

sent Val

ue

of B

ond

Keating F&A 5-18 Spring 2008

Bonds Further From Maturity HaveGreater Interest Rate Sensitivity

Both bonds have 5% coupon; maturity varies

0

500

1,000

1,500

2,000

2,500

3,000

0 0.05 0.1 0.15

Market Interest Rate

Pre

sent Val

ue

of B

ond

Bond Maturing in 2017

Bond Maturing in 2037

Keating F&A 5-19 Spring 2008

Outline Lecture 5

• The Allure of Leverage

• Present Value Calculations

• Bond Valuation

• Stock Valuation

Keating F&A 5-20 Spring 2008

Preferred Stock Is ValuedBasically Like A Perpetual Bond

• Holder gets fixed payment (ifcorporation chooses to make it),no possibility of increase

• Payments can be skipped withoutbankruptcy

• PV Dpskps

Keating F&A 5-21 Spring 2008

Common Stock Valuation Is LessStraightforward Than Bond

Valuation• Dividends might increase

• Holder gets capital gain if stocklater appreciates

• Even stocks not currently payingdividends might be expected tosomeday generate sizabledividends (e.g., Amazon)

Keating F&A 5-22 Spring 2008

Ultimately, Common StockholdersHave To Expect Dividends

Value of Stock = PV of expectedfuture dividends

Po^

Dt

(1 ks )t

t1

skis today’s expected rate of return on equity of this sort

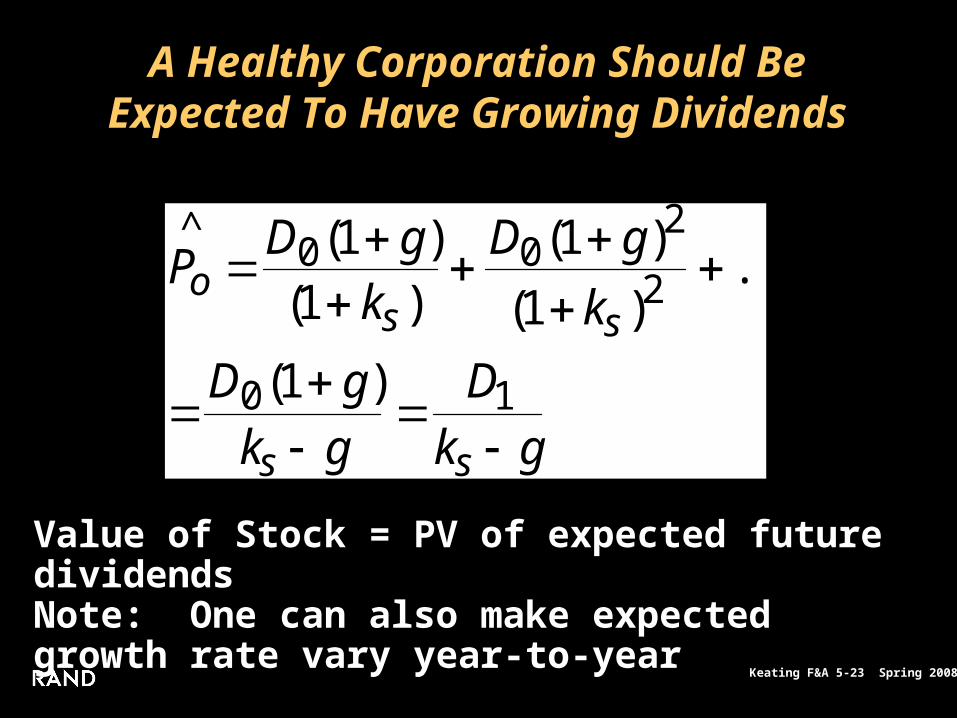

Keating F&A 5-23 Spring 2008

A Healthy Corporation Should BeExpected To Have Growing Dividends

Value of Stock = PV of expected future dividendsNote: One can also make expected growth rate vary year-to-year

Po^

D0(1 g)(1 ks )

D0(1 g)2

(1 ks )2 ...

D0(1 g)ks g

D1ks g

Keating F&A 5-24 Spring 2008

Various Factors CanChange A Stock’s Price

• Current dividend level (+)

• Expected dividend growth rate (+)

• Required return ( ) given perception of stock’s riskiness (-)

sk