financecounsel - samalin group, new york | …samalingroup.com/wp-content/uploads/2016/01/sic...2003...

TRANSCRIPT

Westchester: 297 King Street Chappaqua, NY 10514 914.666.6600 FAX: 914.666.6602 Toll-free: 888 SICOUNSEL (742.6867)410 Park Avenue, 15th Floor New York, NY 10022 212.750.6200 FAX: 212.750.6208

Social Security for the Self-Employeed

Volume II, Issue 1

Finance Focus is published quarterly by Samalin Investment Counsel FINANCE

FOCUSThe Tax Impact of a 529 RolloverThirty-four states offer some sort of tax deduction or tax credit for contributions made to a 529 plan. But in 29 of those 34 states, the tax break is available only for contribu-tions made to an in-state plan. Only Arizona, Kansas, Maine, Missouri, and Pennsylvania give residents a tax break for contributing to any state’s plan. If you own an out-of-state 529 plan, you may be missing out on this tax break advantage, and it may be worthwhile to do some research and consider rolling your out-of-state plan to an in-state one. The tax break can be a real plus, but the quality of the 529 plan (its investment options and fees, in particular) is important, too. If you’ve already opened an out-of-state 529 plan a while ago, you may want to revisit that decision because 529 plans can change over time. If your state now offers a better plan, check with the plan or a tax professional to see if there are tax advantages to rolling funds over. Many states do not provide a tax break for inbound 529 rollovers, but some do. States that do may limit deductions to just the contri-bution portion of the out-of-state 529 or let you deduct the entire amount including earnings.

529 plans are tax-deferred college

distribution of earnings will be subject to ordinary income tax and subject to a 10% federal penalty tax. (Continued on page 2)

If you thought that running a successful business on your own was hard enough already, think again. As a

someone who operates a trade, business or profes-sion, (either by yourself or as a partner), you are required to pay self-employment tax as well as income tax. Self-employment tax consists of Social Security and self-employment taxes, similar to those 1

23

withheld from the pay of most wage earners. Failure to comply with IRS regulations may result in your busi-ness operations being jeopardized. The following are a few key facts to keep in mind:

The Social Security tax rate for 2013 is 15.3% on self-employment income up to $113,700. Should your net earnings exceed $113,700, you continue to payonly the Medicare portion of the Social Security tax, which is 2.9%. Starting this year, the Medicare tax rate for net earnings in excess of $200,000 ($250,000 for

You need to have worked and paid Social Security taxes for a certain length of time to get Social Security

equivalent to 40 credits). In 2013, if your net earnings are $4,640 or more, you earn the yearly maximum of four credits. If your net earnings are less than $4,640,you could still earn credit (depending on how you report your earnings).

Certain income does not count for Social Security

your net earnings. These include dividends from shares of stocks and interest on bonds, interest from loans, rentals from real estate, and income received from limited partnerships.

Tax law is ever-changing and can be quite complex. It is highly

recommended that you consult with

tax-related questions or concerns.

FINANCEFOCUS

The recent low interest rate environment has resulted in lower iinvestments. Relying on yields alone may not generate the cash -quirements in retirement. If you are looking to generate more income, consider adding dividend paying stocks to your retirement portfolio. Dividend stocks may provide income through dividend payments afrom stock price appreciation. Further, these dividend payments may soften losses during turbulent markets, particularly when investors incur negative returns. This means that when dividends are paid out, they act as a cushion and are positive whether stock returns are positive or negative. The image compares the annual income return for the S&P 500, Dividend Composite and Dividend Leaders index over the past 10 years. As seen in the image, dividend-paying stocks produced higher income returns relative to the S&P 500 over this time period. The 10-year average income return for the S&P 500 was 2.1%, compared with the Dividend Composite and Dividend Leaders indexes, which returned 3.2% and 4.5%, respectively. Stocks that pay dividends may serve as an income source while also providing investors with exposure to the growth potential of the stock market. Consult adding dividend paying investments to your portfolio. Past performance is no guarantee of future results. Dividends a -

An investor should consider the investment objectives, risks, and charges and expenses associated with municipal fund securities before investing. More information about municipal

read carefully before investing. Tax law is ever-changing and can be quite complex. It is highly recommended that you consult with a legal, tax,

concerns.

Income Gaption does not eliminate the risk of experiencing investment losses. This is for illustrative purposes only and not indicative of any investment. An investment cannot be made directly in an index. Government bonds are guaranteed by the full faith and credit of the United States government as to the timely payment of principal and inter-est, while stocks are not guaranteed and have been more volatile than the other asset classes. Income return and total return are represented by the compound annual return over the time period analyzed. The Morningstar Dividend Composite Index captures the performance of all stocks in the U.S. Market Index have the ability to sustain their divi-dend payment. Stocks in the index are weighted in proportion to the total pool of dividends available to investors. The Morningstar Dividend Leaders Index captures the performance of the 100 highest yielding stocks that have a consistent record of dividend payment and have the ability to sustain their dividend payments. Stocks in the index are weighted in proportion to the total pool of divi-dends available to investors.

S&P 500 is represented by the Standards & Poor’s 500®, which is an unmanaged group of securities and con-sidered to be representative of the U.S. stock market in general. Morningstar Dividend Composite is represented by the Morningstar Dividend Composite Index, and Morningstar Dividend Leaders by the Morningstar Dividend Leaders Index.

7

6

5

4

3

2

1

02003 2004 2005 2006 2007 2008 2009 2010 2011 2012

8% Income Return Morningstar Morningstar Dividend Dividend2003-2002 S&P Composite Leaders

Income Return 2.1% 3.2% 4.5%Total Return 7.1% 7.6% 6.9%Standard Deviation 18.3% 15.8% 17.7%

Income Returns 2003-2012

The Tax Impact of a 529 Rollover(Continued from page 1)

Questions to Ask Before P Aying o ff A Mor tg Age

investment assets and where you hold them are also important considerations. The case for invest-ing in the market rather than prepaying the mortgage gets even stronger if you hold your investments within the confines of a tax-sheltered vehicle and/or you’re ea ning matching dollars on your contribu-tions. On the flip side, portfolios that are heavy on cash and fixed-income securities, especially thosethat are fully taxable from year to year, are less likely to out earn mortgage interest rates.

How diversified are you?Some homeowners think of their houses as a retirement-savings vehicle: When it comes time to retire, they’ll cash in their equity and downsize to a smaller place. However, the past several years have taught many homeowners that’s easier said than done. Many haven’t been able to sell when they wanted, and they also haven’t been able to receive anything close to the prices they were expecting. Pairing home equity with more liquid stock and bond assets may give you a lot more fle -ibility to ride out downturns in the housing market.

How much is your mortgage-interest deduction saving you? Many homeowners assume that it’s wise to hang on to their mortgages because of the tax deduction they can take on their interest. But that deduction shrinks as the years go by because home loans are front -loaded toward interest payments. People who have been able to pay down a mortgage for many years may be overestimating the amount of taxes they’re saving by having a mortgage, and itemizing deductions may not be saving them much versus the standard deduction. Diversification does not eliminate the risk of experiencing inv stment losses. Government bonds are guaranteed by the full faith and credit of the U.S. government as to the timely payment of prin-cipal and interest, while stocks are not guaranteed and have been more volatile than bonds. Please consult with a financial and tax professional for advice spec fic to your situation

The decision to pay off a mortgage or invest in the market is far from black and white. For those who are close to retirement and already have plenty of other liquid financial assets, paying o f a mortgage could be a wise use of cash. Such homeowners aren’t likely to be saving a lot because of their mortgage-interest deductions, which tend to be more valuable early in the life of the loan than in the later years, and their investment-asset mixes might be skewing toward low returning cash and bonds, not stocks. Moreover, many retirees concur that reducing their in-retirement overhead by retiring debt reduces worries and frees up cash for travel and other pursuits. For others, however, a mortgage pay down might not be the right answer. Although it might seem comforting to own your home free and clear, there’s invariably a trade-off involved. You’re reducing your investments in more liquid assets in favor of an asset that’s not liquid at all. A happy medium for many households might be to balance modest prepayments of mortgage principal with ongoing contributions to retirement-plan accounts. Here are some questions to think through as you make this important decision for your household.

Is your retirement plan on track? Before paying off a mortgage you may want to spend some time evaluating the viability of your retirement plan. Paying off a mortgage rather than investing in the market may mean having fewer liquid assets for retirement. However, with lower household expenses, you may be able to step up your future retirement-plan contributions; having a paid-off home will also mean that your in-retirement costs may be lower. Time horizon is an important aspect of decision-making here. Those with more years until retirement can better harness the compounding benefits of investmentassets, whereas those nearing or in retirement and expecting to begin drawing on their invest-ment assets might not get such a big bang from investing more. What’s your investment mix, and where are you holding it? The composition of your

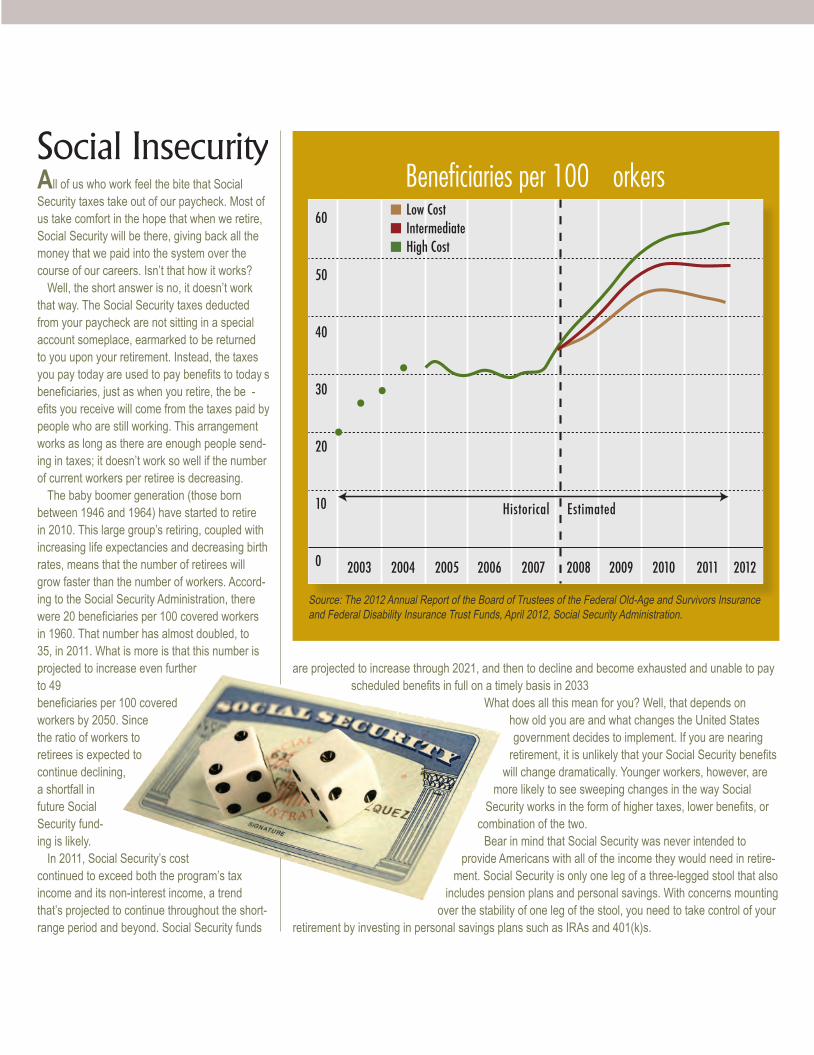

Social Insecurity

All of us who work feel the bite that Social Security taxes take out of our paycheck. Most of us take comfort in the hope that when we retire, Social Security will be there, giving back all the money that we paid into the system over the course of our careers. Isn’t that how it works? Well, the short answer is no, it doesn’t work that way. The Social Security taxes deducted from your paycheck are not sitting in a special account someplace, earmarked to be returned to you upon your retirement. Instead, the taxes you pay today are used to pay benefits to today s beneficiaries, just as when you retire, the be -efits you receive will come from the taxes paid bypeople who are still working. This arrangement works as long as there are enough people send-ing in taxes; it doesn’t work so well if the number of current workers per retiree is decreasing. The baby boomer generation (those born between 1946 and 1964) have started to retire in 2010. This large group’s retiring, coupled with increasing life expectancies and decreasing birth rates, means that the number of retirees will grow faster than the number of workers. Accord-ing to the Social Security Administration, there were 20 beneficiaries per 100 covered workersin 1960. That number has almost doubled, to 35, in 2011. What is more is that this number is projected to increase even further to 49beneficiaries per 100 coveredworkers by 2050. Since the ratio of workers to retirees is expected to continue declining, a shortfall in future Social Security fund-ing is likely. In 2011, Social Security’s cost continued to exceed both the program’s tax income and its non-interest income, a trend that’s projected to continue throughout the short-range period and beyond. Social Security funds

are projected to increase through 2021, and then to decline and become exhausted and unable to pay scheduled benefits in full on a timely basis in 2033

What does all this mean for you? Well, that depends on how old you are and what changes the United States government decides to implement. If you are nearing

retirement, it is unlikely that your Social Security benefitswill change dramatically. Younger workers, however, are

more likely to see sweeping changes in the way Social Security works in the form of higher taxes, lower benefits, or

combination of the two. Bear in mind that Social Security was never intended to

provide Americans with all of the income they would need in retire-ment. Social Security is only one leg of a three-legged stool that also

includes pension plans and personal savings. With concerns mounting over the stability of one leg of the stool, you need to take control of your

retirement by investing in personal savings plans such as IRAs and 401(k)s.

Social InsecurityBeneficiaries per 100 orkers

Source: The 2012 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds, April 2012, Social Security Administration.

60

50

40

30

20

10

0 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

n Low Costn Intermediaten High Cost

Historical Estimated

FINANCEFOCUS

Encountering stock market losses early in one’s retirement years can deliver a blow to an equity-heavy portfolio. If you’ve determined that your equity weighting is extremely aggres-sive relative to your risk appetite, reducing risk by altering your portfolio’s asset allocation may be essential. The need to reduce the risk of your portfolio doesn’t mean you have to move money directly from stocks to bonds. As you cut back on your equity exposure, it may be wise to move money into cash and/or short-duration bonds (duration is a measure of interest-rate sensitivity), then slowly and systematically move it into the bond market over a period of several months or years. This way, you may be able to obtain a range of purchase prices for your new bond holdings. It’s important to think about what you’re trying to achieve by transitioning your portfolio to bonds as retirement draws near. Lower risk and liquidity may be the answer. One potential way to obtain both is to take some of the money you would oth-erwise have earmarked for bonds and use it to pay down debt, even low-interest mortgage debt. If having a paid-down mortgage will reduce your expenses in retire-ment, you will be reducing the need to raise cash from your portfolio to meet in-retirement living expenses.

Don’t Pay Tax TwiceReinvestment can be a crucial component of the wealth accumulation process, as the reinvested amount compounds and grows over time. Yet if you are reinvesting dividends and capital gains (“distributions”) in funds you hold in your taxable account, it can be important to ensure that you’re not paying more tax than necessary. You pay tax on those distributions in the year in which you receive them. But if you don’t keep good records, you could end up paying tax on those distributions again when you sell. For example, say you bought 1,000 shares of a fund for your taxable account at the end of 2011; you paid $18 per share for a total of $18,000. In 2012, with the share price still at $18, the fund made a dividend distribution of $0.50 per share, or $500 for your 1,000 shares. You’d owe tax on the $500 on your 2012 taxes, whether you reinvested the money or took the cash in hand. (The taxes would be deferred if you held the fund in a tax-sheltered account). If you reinvested the money in the fund, you’d now own 1,027.78 shares: your original 1,000 plus the nearly 28 additional shares that you were able to buy (at $18) with the $500 dividend distribution. If you sell now, with the fund’s net asset value at $20, you’d think you’d owe taxes on your $2,555.56 profit ($20,555.56minus $18,000), right? Wrong. You would only owe taxes on $2,055.56 ($20,555.56 minus $18,000 minus $500). Otherwise, the $500 dividends would be taxed twice. Investments are subject to risk of principal and risk of loss. Dividends are not guaranteed. Retirement accounts are tax-deferred vehicles designed for retirement savings. Any with-drawals of earnings will be subject to ordinary income tax and, if taken prior to age 59½, may be subject to a 10% federal tax penalty. This should not be considered tax or financialplanning advice. Please consult a tax and/or financial professional for advice specific to youindividual circumstances.

Bonds: Tips To Keep Fr om Ge TTin G pinched

Diversification does not eliminate the risk ofexperiencing investment losses. Stocks are not guaranteed and have been more volatile than other asset classes. Bonds are subject to credit/default risk, which is risk associated with the issuer failing to meet its contractual obligations either through a default or credit downgrade. Bonds are sensitive to interest rate changes. In general, the price of a debt security tends to fall when interest rates rise and rise when interest rates fall. Securities with longer maturities and mortgage securities can be more sensitive to interest rate changes.

Westchester: 297 King Street Chappaqua, NY 10514 914.666.6600 FAX: 914.666.6602 Toll-free: 888 SICOUNSEL (742.6867)Manha� an: 410 Park Avenue, 15th Floor New York, NY 10022 212.750.6200 FAX: 212.750.6208

West ches ter297 King Street Chappaqua, NY 10514

Manha t t an410 Park Avenue15th Floor New York, NY 10022

About SICounSel

Samalin Investment Counsel, LLC (SICoun-sel) is a fee-only, nationally recognized SEC registered investment advisory firm. Withoffices in Chappaqua N and NYC, we specialize in wealth management, pre and post divorce financial planning, retirementplanning, and other related financial services

According to a U.S. Government Account-ability Office report*, between 1997 and 2005,roughly 43% of Social Security-eligible individu-als began taking benefits within one month ofturning 62, even though waiting until their full retirement age (65) would have translated into a substantially higher payout. Between2000 and 2006, only 6% of retirees with definedcontribution plans such as 401(k) and 403(b) plans chose to move their assets into an annu-ity upon retirement.* One key reason why so few retirees opt for annuities is loss of control. In contrast with traditional investments that you can alter and tap whenever you see fit, a keypremise behind annuities is that you fork over a lump sum in exchange for a stream of pay-ments throughout your life. Another reason is that payouts from single-premium immediateannuities are currently low relative to historic norms (depressed by increasing longevity and the current low interest-rate environment). But this doesn’t mean annuities should be avoided altogether. Consider these strategies when purchasing an immediate annuity. Consider Your Needs: Retirees who have a substantial share of their lifetime living expens-es accounted for via pension income or Social Security may want to diversify into investments with a higher level of control and the opportuni-

ty to earn a higher rate of return, such as stocks. Those who don’t have a substantial source of guaranteed retirement income may find greaterutility from annuity products. Build Your Own Ladder: One of the key attrac-tions of sinking a lump sum into an annuity is the ability to receive a no-maintenance, pension-like stream of income, which may be appealing for retirees who don’t have the time or inclination to manage their portfolios on an ongoing basis. However, a slightly higher maintenance strategy of laddering multiple annuities can help mitigate the risk of sinking a sizable share of your portfolio into an annuity. Such a program would give you the opportunity to diversify your investmentsacross different insurance companies, therebyoffsetting the risk that an insurance company would have difficulty meeting its obligations. Ho -ever, such a strategy would entail multiple annuity charges, associated with each annuity in the ladder, which could be substantial and adversely impact your total annuity payout. Consider More Flexible Options: Fixed-rateimmediate annuities are typically the cheapest and most transparent, but they’re also the most beholden to whatever interest-rate environment prevails at the time the purchaser signs the contract. Some annuities, however, address the current yield-starved climate by allowing for an

Strategies for Combating Low Annuity Yieldsinterest-rate adjustment if and when interest rates head back up. Such products offer an appealing safeguard to those concerned about buyingan annuity with interest rates as low as they are now, but the trade-off is that the initial payout on such an annuity would tend to be lower than the payout on an annuity without such a feature. The examples presented herein are for informa-tional purposes only, are not representative of any specific annuity and do not constitute investmentadvice. Annuities are suitable for long-term invest-ing, particularly retirement savings. Annuity risks include market risk, liquidity risk, annuitization risk, tax risk, estate risk, interest-rate risk, inflation risk,death and survivorship risk, and company failure risk. Withdrawal of earnings will be subject to ordi-nary income tax and, if taken prior to age 59½, may be subject to a 10% federal tax penalty. Additional fees and investment restrictions may apply for living benefit options. iolating the terms and condi-tions of the annuity contract may void guarantees. Consult a financial advisor and tax advisor beforepurchasing an annuity.

*Report cited: U.S. Government Accountability Office, Reportto the Chairman, Special Committee on Aging, U.S. Senate: “Retirement Income: Ensuring Income throughout Retirement Requires Difficult Choices,” June 20 1