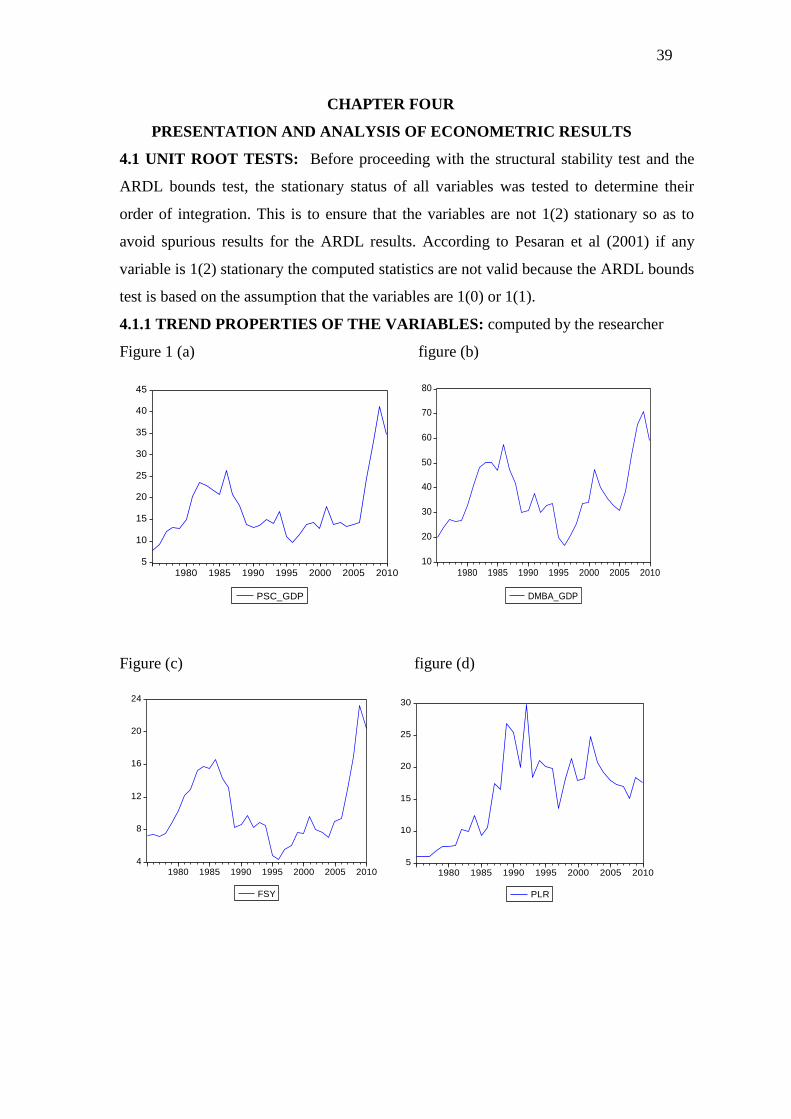

financial deepening and its influence on poverty …

TRANSCRIPT

1

OKEREKE, SAMUEL FELIX

PG/M.SC/09/50580

PG/M. Sc/09/51723

AN ECONOMETRIC ANALYSIS OF THE IMPACT OF

FINANCIAL DEEPENING ON AGGREGATE WELFARE

IN NIGERIA

ECONOMICS

A THESIS SUBMITTED TO THE DEPARTMENT OF ECONOMICS, FACULTY OF

SOCIAL SCIENCES, UNIVERSITY OF NIGERIA, NSUKKA

Webmaster

Digitally Signed by Webmaster‘s Name

DN : CN = Webmaster‘s name O= University of Nigeria, Nsukka

OU = Innovation Centre

AUGUST, 2011

2

AN ECONOMETRIC ANALYSIS OF THE IMPACT OF

FINANCIAL DEEPENING ON AGGREGATE WELFARE

IN NIGERIA

BY

OKEREKE, SAMUEL FELIX

PG/M.SC/09/50580

A RESEARCH WORK SUBMITTED IN PARTIAL

FULFILLMENT OF

THE REQUIRMENT FOR THE AWARD OF MASTER OF

SCIENCE

(M.Sc) DEGREE IN ECONOMICS

DEPARTMENT OF ECONOMICS

SCHOOL OF POST-GRADUATE STUDIES

UNIVERSITY OF NIGERIA, NSUKKA

SUPERVISED BY: O.E ONYUKWU

AUGUST, 2011

3

DEDICATION

I dedicate this research work to God Almighty for leading me so far in life. And to the

memory of my mother, Late Deaconess Glory N. F. Okereke who saw me picking the

form for this program but could not stay alive to see the dream come true.

4

ACKNOWLEDGEMENT

This work and the program at large would not have been a success without the

suggestions, encouragement and other contributions I received from various angles.

I wish to express my immense gratitude to my supervisor Dr. O.E. Onyukwu whose

kindness, attention and co-operation throughout this research period were most

valuable.

In particular, I would like to thank Dr. Mrs. I. S. Madueme of the Department of

Economics, University of Nigeria, Nsukka and Dr Innocent (Oga SPG) for making

out times to read this work and made valuable comments. I would also recognize the

efforts of Dr. Moses Oduh, Mr. Emmanuel Nwosu, and Rev. Fr (Dr) H. E. Ichoku for

their direction and motivation.

I owe a great deal to Sir and Lady Steve Agbo (KSP), his entire family for not just

allowing me used the computers and printers but also for being a friend and mentor.

My appreciation equally goes to my friends and former colleagues, Denis Yunis (the

man from Cameroun), Chijioke Okogbue, Edith Agbo Ekene and Mr Innocent

Nkama, Aunty Chioma Onwugharam and Aunty Eunice.

I acknowledge with gratitude, the moral and financial supports from, Mr. Nwachukwu

Nnamdi of the First Bank, Nsukka, Mr. Emmanuel Ugwa of the Zenith Bank, Afikpo,

Mr. Stephen Ohaka, Mr. Ifeanyi Obijiaku of the PZ-cussons, Lagos, Mr. Okay Okore

(junior), Mr. Kingsley Obi of Eco Bank, Ekwulobia, Mr. Akachukwu Okoye of the

Diamond Bank, Mr. Uchenna Nwachukwu and Mr. Temitope Aluko both of Eko

Bank, Aba. Also, Mr. Victor Fakunye, Mr. Nwankwo Christian (Waja) and Miss Rita

Okonkwo I am deeply grateful to them for their efforts.

To a distinguished friend and brother, Comrade Kalu Nnanna Nwonyuku of the

National Hospital, Abuja, thanks for chatting a path in my life. To a beloved one,

Amarachi Onwugharam, thank you for your support, encouragement and for staying

by my side.

I have a darling father (my all time Boss) to thank, Prophet F.N. Okereke, my elder

sister, Mrs Joy Ekpe, my siblings; Amarachi, Onyinyechi, Sunday and Ihechi. You are

the source of my strength. Finally, I give God all the praise for being the ultimate

source of my possibilities.

Okereke, Samuel F.

August, 2011

5

ABSTRACT

A general way of evaluating the economic welfare of country is through its household

per capita expenditure. Thus, the major purpose for this study is to investigate how the

recent financial deepening processes in Nigeria have impacted on aggregate welfare.

Private per capita consumption expenditure is used to measure aggregate welfare in

this study which serves as a macroeconomic measure of indicators of aggregate

welfare. Financial deepening can affect aggregate welfare in various ways and in

many outcomes. From the existing literature, the channels of influence through which

financial sector deepening affects aggregate welfare are indirectly through growth and

directly through increased access to financial services. Financial deepening is

represented by two variables, the degree of financial intermediation/development

(MS2/GDP) and the ratio of private sector credit to gross domestic product

(PSC/GDP). Three modelled equations, with justifications for each, were estimated

and analysed. With a time series data spanning from 1975 to 2010, a country specific

regression was used.

A dummy variable approach for structural differences was used for the analysis in the

first Model after the necessary conditions of non-stationarity and cointegration had

been satisfied, while the Autoregressive Distributed Lag-Error Correction Model

(ARDL-ECM) was used for the analysis of the second and third Models. The

empirical findings show that there are structural differences in the level of financial

deepening in the country between the pre and post recent financial reform periods in

Nigeria, the bank size represented by (DMBA/GDP) and bank branch distribution

represented by (NBBT) are the outstanding and significant determinants of financial

deepening in Nigeria. Lastly, financial deepening has no direct significant impact on

aggregate welfare, but can go through the financial accessibility indicator-bank branch

distribution.

The policy implications derive from the findings is that, the country should come up

with more policies to improve financial deepening/intermediation and there is need to

formulate financial reform policies that will have a proportionate beneficial welfare

impact on the poor.

6

TABLE OF CONTENT

Title page………………………………………………………………………….. I

Certification………………………………………………………………………. II

Dedication………………………………………………………………………… III

Acknowledgement……………………………………………………………….. IV

Table of content…………………………………………………………………… V

CHAPTER ONE: INTRODUCTION

1.1 Background of the study………… …………………………………………… 1

1.2 Statement of problem…………………………… …………………………….. 8

1.3 Research questions……………………… …………………………………….. 10

1.4 Objective of the study………………………………………………………..... 10

1.5 Hypothesis of the study……………………………………………………...... 10

1.6 Policy relevance……………………….………………………………………. 10

1.7 The scope of the study………………………….……………………………... 11

1.8 Source of Data and Econometric Software Used …………………………….. 11

CHAPTER TWO: LITERATURE REVIEW

2.1 Conceptual Framework………………………………………………………. 12

2.2 Theories of framework deepening and its link to aggregate welfare………… 13

2.2.1 The Indirect channel through growth ...……………………………………. 14

2.2 2 The direct channel through access to financial services …………………... 16

2.3 Empirical literature………………………………………………………….... 19

2.3.1 Cross country evidence…………………………………………………….. 19

2.3.2 Country Specific Evidence ………………………………………………... 22

2.4 Efforts towards deepening the Financial system in Nigeria………………...... 23

2.5 Limitations of previous studies……………………………………………….. 24

CHAPTER THREE: METHODOLGY

3.1 Analytical framework……………………………………………………….... 25

3.2 The model…………………………………………………………………….. 26

3.2.1 Model specification……………………………………………………….... 26

3.2.1Model 1…………………………………………………….. ….………….... 28

3.2.1 Model 2……………………………………………………………………... 28

3.2.1 Model 3…… ……………………………………………………………….. 28

3.2.2 The ARDL-ECM……………………….…………………………………... 28

3.2.3 Unit root …………………………………………………………………..... 28

3.3 Estimation procedure………………………………………………………..... 29

3.4 Justification of the model…………………………………………………...... 29

3.5 Statistical criteria …………………………………………………………….. 30

3.6 Description of Variables……………………………………………………… 30

CHAPTER THREE: PRESENTATION AND ANALYSIS OF ECONOMETRIC

RESULTS

4.1 Unit root tests………………………………………………………………… 32

4.1.2 Trend properties of the variables………..………………………………….. 35

4.2 Result presentations...………………………………………………………… 37

4.3 Bound test for co-integration…………………………………………………. 40

4.4 Interpretation of ARDL results……………………………………………….. 41

4.5 Discussion of findings……………………………………………………….....42

7

4.6 Implications of the findings…………….……………………………………... 43

4.7 Interpretation of Diagnostic tests……………………………………………… 43

CHAPTER FIVE: POLICY RECOMMENDATIONS AND CONCLUSION

5.1 Summary……………………………………………………………………….. 48

5.2 Policy recommendations……………………………………………………….. 48

5.3 Conclusions…………………………………………………………………….. 49

References

Abstract

8

CHAPTER ONE

INTRODUCTION

1.1 BACKGROUND OF THE STUDY:

In recent years, many studies have examined the link between financial deepening and

economic development as well as the link between financial development and poverty

reduction via economic growth from both micro and macro perspectives, example,

Levine (2004), Fitzgerald (2008), Nzotta and Okereke (2009), etc. In this study we depart

from the finance-growth nexus, but still from the macro angle to see if there is a direct

relationship between financial deepening and aggregate welfare. We will look at how

welfare is linked to financial sector deepening and the existing transmission mechanisms.

Few will doubt that income growth through access to financial services leads to

improvement in people‘s lives. Increased income allows people to enhance their living

standards and escape from extreme poverty. From the works of Claessen and Feijen

(2006), without a developed financial sector, for example, domestic savers and foreign

investors would be more hesitant to part with their money to otherwise sound

investments, resulting in lower economic output as measured by GDP and household

welfare. They sressed that a well-developed financial system enables firms to expand

production and provides households with the ability to obtain essential assets like a

house, insure against income shocks, start a company, receive cheaper remittances, and

enjoy a pension when they retire.

As such, the financial sector is an engine of economic growth and household welfare.

Most literature confirmed that financial market plays a vital role in the process of

economic growth and development by facilitating savings and channeling funds from

savers to investors, Nzotta and Okereke (2009). Financial intermediation of growth leads

to financial deepening, which refers to the greater financial resource mobilization in the

formal financial sector and the ease in liquidity constraints of banks and enlargement of

funds available to finance projects, Fisher (1933).

Direct measurement of how well the financial sector performs each of its functions is

difficult. As Ndebbio (2004) observed, it is not possible to observe directly the quality

and quantity of the monitoring services performed by a bank when it extends a loan, at

least not for a large country like Nigeria. Hence, researchers use proxies to measure

financial deepening. Typically used indicators of financial deepening are ratio of MS2

9

(money) to GDP, ratio of private credit extended by commercial banks to GDP, and other

financial assets.

As Ndebbio (2004) observed, only countries with high per capita incomes can experience

rapid growth in financial assets. Such countries are none other than the developed

countries. But what is crucial here is what constitutes the financial assets that wealth-

holders must have as a result of high per capita income. Only when we can identify those

financial assets will we be able to approximate financial deepening adequately. In short,

and for our purpose, we borrow a lift from Ndebbio (2004) in asserting that financial

deepening simply means an increase in the supply of financial assets in the economy.

Therefore, the sum of all the measures of financial assets gives us the approximate size of

financial deepening. That means that the widest range of such assets as broad money,

liabilities of non-bank financial intermediaries, treasury bills, value of shares in the stock

market, money market funds, etc., will have to be included in the measure of financial

deepening. To simply pick the ratio of private sector credit to gross domestic product

(GDP), as done in this study, is because of lack of data on other measures of financial

assets likely to adequately approximate financial deepening in most Sub-Saharan African

countries.

In his study, Ndebbio (2004) noted that if the increase in the supply of financial assets is

small, it means that financial deepening in the economy is most likely to be shallow; but

if the ratio is big, it means that financial deepening is likely to be high. He further went

on to stressed that developed economies are characterized by high financial deepening,

meaning that the financial sector in such countries has had significant growth and

improvement, which has, in turn, led to the growth and development of the entire

economy.

One common problem affecting the growth of development economies is the issue of

―financial shallowness‖ which is seen by many economists as an outcome of the adoption

of inappropriate financial policy. In the 1980‘s, Nigeria alongside other African countries

experienced widespread financial liberalization, interest rate deregulation, the entry of

new banks and the likes, with the intention to deepen the financial sector but ended up

producing financial openness without much financial depth, Collier and Gunning (1999).

They further stressed that the legacy of financial liberalization in these countries was the

establishment of weak banking organizations that were unable to open up the

10

opportunities created by liberalization. Reflecting this in Nigeria saw the country being

relegated to having less financial depth than other developing areas. As a result, banks

were vulnerable to systemic crisis and the systemic risks in the country high. Thus, the

Nigerian banking system was evidently limited in its resources mobilization with an

adverse effect on the economy which hit more on the poor since they are the most

vulnerable and hence financial deepening

This prompted the Central Bank of Nigeria (CBN) to come up with new banking reform

policies in 2005 in a bid to strengthen and increase the financial assets of banks. Banking

reforms are part of financial sector reforms, and financial sector reforms are propelled by

the need to deepen the financial sector and reposition it for growth to become integrated

into the global financial architecture and evolve a banking sector that is consistent with

regional integration requirement, savings mobilization and international best practices,

Nnanna et al (2004).The recent banking sector reforms which experienced consolidation

of banking institutions affected the level of financial deepening in the country.

Consolidation of banks has been the major reform policy instrument being adopted

recently in correcting deficiencies in the financial sector. It ushered in other reform

policies that followed including the bail-out of eight deposit money banks with huge non-

performing loans in 2009.

A review of the financial deepening indicators show that, the depth of the financial sector

as measured by the ratio of MS2 to GDP even though has been fluctuating but has

increased more than previous years. For the period of the study the ratio at the end of

2009 stood at 43.4 per cent and 38.9 per cent for 2010. Bank financing of the economy

measured by the ratio of private sector credit to GDP stood at 33.2 per cent though lower

than that 41.1 per cent of 2009. The intermediation efficiency indicator as measured by

the ratio of currency outside banks to broad money supply was 9.4 per cent compared

with 8.6 per cent at end of December, 2009. The size of the banking system relative to the

size of the economy indicated by the ratio of deposit money banks assets to GDP,

declined from 69.6 per cent at end of December 2009 to 58.8 per cent in 2010, (CBN

2010 annual report). Below is a chart showing the ratio of deposit banks assets to GDP

and a graph showing the ratio of broad money (MS2) to GDP, private sector credit to

GDP.

11

30

40

50

60

70

2000 2002 2004 2006 2008 2010

DMBA_GDP

pe

r ce

nt

Source: computed by the author from the CBN bulletine

From the chart above, although there is a decrease in ratio of deposit money banks assets

to GDP in 2010, the increased in the ratio from 2007 to 2010 is higher than other years.

0

10

20

30

40

50

1975 1980 1985 1990 1995 2000 2005 2010

FD1 FD2

per c

ent

fd1=psc/gdp and fd2=ms2/gdp

Source: computed by the researcher,from CBN-bulletine

12

The graph above shows that the finncial deepening indicators (MS2/GDP and PSC/GDP)

increased from between 2005 and 2006 indicating the recent banking reforms has

impacted on the level of financial deepening in the country.

This shows that in Nigeria, the banking system clearly dominates in the flow of funds and

has an important impact on the level of economic development, Nzotta and Okereke

(2009). They also opined that the reforms in the banking sector impacted positively on

the growth of the financial system. The system moved from a rudimentary one at

inception to a more sophisticated one in 2009 with diverse institutions and operations,

diversified financial assets and an enhanced regulatory framework. Also, Sanusi (2011)

opined that banks by their size were enabled to undertake funding of large ticket project,

especially in infrastructure, oil and gas sectors, through the new window in the enlarged

single obligor limits. With the larger size of the banks also engendered to improved

customer confidence, and the number of bank branches increased from 3,247 in 2003 to

over 5,837 in 2010 and employment in the sector rose from 50,586 in 2005 to 71,876 in

2010. Below is a chart showing total bank branch expansion in Nigeria, from 1975 to

2010. The chart shows that bank branch distribution has increased recently.

A CHART SHOWING NUMBER OF BANK BRANCHES IN NIGERIA

0

1000

2000

3000

4000

5000

6000

1975 1980 1985 1990 1995 2000 2005 2010

NBBT

nbbt=total no of bank branches in Nigeria

Source: computed by the researcher, from CBN- bulletine

However, welfare concerns in Nigeria were primarily related to its general lack of

development and the effects on the society of the economic stringency of the 1980s and

1990s. Given the steady population growth and the decline in incomes since 1980, it was

13

difficult not to conclude that for the mass of the population at the lower income level,

there was profound aggregate welfare loss, Metz (2011). Studies have shown that

household per capita expenditure can provide insight into economic welfare or the living

conditions of the population, Akerele and Adewuyi (2011). The assessment of aggregate

welfare in the country becomes necessary as the financial sector deepens. Households are

important players in the financial sector, both as savers and borrowers. Financial sector

deepening ought to bring direct aggregate welfare improvement in an economy by

increasing returns on and reducing risks of the invested savings of the populace

particularly low income earners, since savings enable poor households to smoothen their

consumption. And by increasing consumption, the demand for goods and services

increases, thus, stimulating more agricultural and industrial production leading to more

jobs and higher economic growth.

It is incontrovertible, that one of the developmental challenges facing the country is how

to reduce the high level of poverty prevailing among her population. Given the current

rate of population and economic growth and the resultant fluctuations in private per

capita consumption expenditure in the country, the preoccupation does not come by

surprise. Indeed, the economy is expected to grow by a minimum of 7.0 per cent per

annum, if the millennium development goal of reducing the level of poverty by half is to

be achieved by 2015.

The poor in the country need to be empowered, for many Nigerians; access to even a

small amount of credit can make a considerable difference in their ability to earn a self

reliant income. Thus, as finance deepens in the country it is necessary to ascertain if the

CBN and other financial regulators have maintained a good balancing between regulating

the financial sector effectively for the determinants of financial deepening to work

effectively at all levels of the economy and providing a good environment that will

promote sufficient and widely accessible financial services with less systemic crises.

Studies have shown that, several indicators of aggregate welfare has fallen dramatically

in the aftermath of a disappointing financial sector reforms, severely affecting the most

vulnerable and poorest people and resulting in a substantial welfare loss, Honohan

(2004b), Jalilian and Kirkpatrick (2001). Although, high and sustainable economic

growth is central to improvement of aggregate welfare, studies by Asenso-Okyere et al

(1993) revealed that promotion of efficient, sufficient and widely accessible financial

services (rural banking inclusive) is a key to achieving pro-poor growth and welfare

gains.

14

Financial deepening can affect aggregate welfare in various ways and in many outcomes.

The three aspects of welfare which could be affected by financial deepening, include;

vulnerability, investment and consumption smoothening, Gloede and Rungruxsirivorn

(2010). Studies have shown that it is not obvious whether financial deepening reduces or

increases vulnerability which is the probability to stay or fall below the poverty line.

According to Gloede and Rungruxsirivorn (2010), a higher amount of credit increases

also the risk of fallen which is well known from corporate finance under the leverage

ratio. Especially in the presence of the current financial crisis one might be tempted to

argue in such a way. In the other hand, there are channels where financial deepening can

improve aggregate welfare. These channels result from the intermediation function of the

financial sector, but the most important channel through which financial sector deepening

leads to direct aggregate welfare improvement is increased access to financial services.

Access to financial services-such as savings- through bank branch distribution can help

firms and households cope with economic shocks, Claessens and Feijen (2006). Most

literature has shown that firms‘ and households‘ access to financial services rises with

financial deepening, Beck et al (2006). A well functioning financial system creates strong

incentives for investment in order to increase productivity. Foster trade and business-

linkages in order to facilitate technology transfer and improved resources used. Provide

broad access to assets and markets in order to build up the asset base of the poor as well

as increase the returns to such assets. Remittances from abroad and domestic transfers are

important source of income for the poor, thus, reducing vulnerability. Where financial

sector deepening leads to lower costs, the poor will benefit from more secure and rapid

transfers, and easier access to transferred funds. Also, they enable the poor to draw down

accumulated savings and borrow to invest in income-enhancing assets and start micro

enterprises, thus, wider access to financial services, generates employment which

increase incomes and welfare gains. And enabling the poor to save in a secure place, the

provision of bank accounts and insurance allows the poor to establish a buffer against

shocks thus, reducing vulnerability and increase the ability of individual and households

to access basic services like health and education and thus having a more direct welfare

benefit impact, DFID (2004).

15

The transmission mechanism works through - the expansion of bank branches especially

in rural areas which will in addition provide support services such as provision of training

and capacity building.

But there are skeptical views on whether financial sector deepening can lead to a

broadening of access to finance services with the resultant aggregate welfare benefits.

Most literature confirms that financial development policies do not serve the poor.

Greenwood and Jovanovic (1990), show that improvement in the financial system may

not automatically lead to improvement in income distribution. They argue that there is an

inverted U-shaped relationship between income inequality and financial deepening. Thus,

the study restricts its analysis of the link between financial deepening and aggregate

welfare using financial accessibility indicators such as, bank branch expansion, savings

rate and cost of acquiring credit. Based on the foregoing discussion, the study is designed

to answer this critical question; are there proportionate aggregate welfare benefits for all

income levels in an economy from financial reforms that strengthen the economy

generally?

1.2 STATEMENT OF PROBLEM:

Although a large body of studies have pointed out that financial deepening produces

faster average growth with welfare implications, Levine (1997, 2005) and Beck et al

(2000), Honohan (2004a), (2004b), Jalilian and KirkPatrick (2005), Beck et al (2007),

Odhiambo (2009) etc. Researchers have not yet determined whether the aggregate

welfare gains of financial deepening benefit the whole population equally or whether it

disproportionally benefits the rich or the poor. If financial deepening intensifies income

inequality, this income distribution effect will hamper the beneficial effects of financial

deepening on the poor.

Thus, theory predicts conflicting predictions on the aggregate welfare implications of

financial deepening. Scholars like Mendoza et al (2007) and others are of the opinion that

if financial reform policies that produce financial deepening are not accompanied with

proper and adequate regulatory framework, sound fiscal and macroeconomic stability,

then financial deepening can have sizeable consequences on the distribution of wealth

and adverse welfare effects.

They stressed that developing countries financial regulators fail to strike an appropriate

balance between regulating the sector effectively for the determinants of financial

deepening to be effective and providing a good environment for financial sector

16

deepening, Levine et al (2000), Holden and Prokopenko (2001), DFID (2004). In addition

some other studies followed a similar reasoning that the indicators of financial deepening

that worked for some developed and developing countries may not work for other

countries. According to these studies while there are large benefits from a well

functioning financial system, financial sector deepening also brings risk which may hit

more on the poor, Banerjee (2009), Zingales (2009). In the opinion of Mendoza et al

(2007), even though financial deepening leads to a significant increase in wealth

inequality in most developed countries, the aggregate welfare consequences are still

positive for these countries. By contrast, in countries with growing financial markets, the

aggregate welfare consequences are negative and the distribution of wealth does not

change much.

However, recent studies on finance deepening in Nigeria especially on recent deepening

efforts have concentrated more on its impact on economic growth, Ndebbio (2004),

Nnanna (2004) and Nzotta and Okereke (2009. These studies imply that once there is

growth it could have an impact on the whole economy. But economists are of the view

that the imperative of growth for welfare improvement does not mean that growth is all

that matters, Fields (2001). Access to financial services is crucial for welfare

improvement, Jalilian and Kirkpatrick (2001), Asenso-okere et al (1993).

Though it is true that in recent times, bank intermediation in formal banking has

improved in terms of speed of response to customers‘ needs and quality of service

rendered in Nigeria as a result of the efforts geared towards the deepening of the financial

system, Sanusi (2011), the same is not available to people in the rural areas. Bank branch

location is heavily biased towards the urban areas with good infrastructures that can fetch

good returns.

In addition, despite the improvements in the banking industry, they are still punctuated

with cases of under-performance of their role. A significant proportion of credit

transactions in Nigeria still take place in the informal markets, despite governments

efforts aimed at channeling credit to the productive sector through the deposit money

banks, Nnanna (2004). According to Soludo (2008), banking services are available to

about 40 percent of the population and more than 60 percent of the poor do not have

access to formal finance and are forced to rely on a narrow range of some risky and

expensive informal services which constraints their ability to participate fully in markets

to increase their income and contribute to economic growth. The business information

17

provider (Business Hallmark 6th

-12th

June,2011), revealed that two years after the CBN

launched the last bank reforms with N620 billion injected into eight banks, N1.7 trillion

toxic assets bought off, the economy is still prostrate, banks not lending and poverty

ravaging the land.

Moreover, at the period of this research, banks are pegging the minimum cash balance for

savings account at N2000 and N5000 in some cases and lending practices curtailed with

emphasis on risk minimization. Moreover, there is still high cost of capital (high interest

rates) and existing anomalies in lending for investment in agricultural production which

is one of the sectors expected to act as a catalyst towards a general aggregate welfare

improvemnet, Aderibigbe (2005). These developments may continue to increase the lack

of financial accessibility of the low income earners and confine them to low-return capital

intensive activities, so that despite being more risk averse they are less diversify. Already,

there have been profound fluctuations in the private consumption expenditure in Nigeria,

Odior and Banuso (2011), implying that private per capita consumption expenditure, a

measure of aggregate welfare will follow the same pattern. There is then a concern issue

that the recent banking sector reform-led financial deepening in Nigeria will have a

similar effect with that of deregulation/financial liberalization period which made

commercial bank accounts inaccessible to most Nigerians, Ayida, (2007), generating

severe welfare implications, which manifest indirectly through their relation with

macroeconomic policies, raising arguments whether financial sector deepening in Nigeria

is having a disproportionate aggregate welfare beneficial impact or broadening access to

financial services.

Thus, it is not clear whether the recent financial deepening processes in Nigeria will have

any aggregate welfare improvement. In view of this, there is the need to empirically

investigate the level of deepening that has occurred in Nigeria and the nature of the

impact on the aggregate welfare. As a result, the following research questions become

imperative.

1.3 RESEARCH QUESTION

I. What is the level of financial deepening that has occurred in Nigeria from 2005 to

2010.

II. What are the determinants of financial deepening in Nigeria?

III. Does financial deepening leads to aggregate welfare improvement in Nigeria?

18

1.4 OBJECTIVE OF THE STUDY: The main objective of this study is to answer one

critical question; are there aggregate welfare benefits from financial reform policies that

strengthen the economy? More specifically, the study intends;

a) To investigate the structural changes in the pre and post-consolidation

periods in Nigeria.

b) To analyze the factors determining the level of financial deepening in Nigeria.

c) To determine the nature of impact financial deepening has on aggregate welfare in

Nigeria.

1.5 HYPOTHESIS OF THE STUDY

a Ho: There are no structural changes in the level of financial deepening in the

Country after 2005.

b Ho: Macro-economic variables do not determine the level of financial deepening in

Nigeria.

c Ho: Financial deepening has no direct impact on aggregate welfare in Nigeria.

1.6 POLICY RELEVANCE:

The wake-up call for financial sector reform should be critically examined especially its

impact in all levels of the economy. This study is important at this level of economic

development when efforts are being made to reposition the financial sector to enable it

play key roles in economic development at all levels of income. It will also help policy

makers and government to know the structural changes that have taken place with the

reform policies on ground in Nigeria. It will also provide useful information that will be

relevance in formulating a more targeted financial reform policy that will be beneficial to

the poor. More so, the study would further add to the existing literature on the link

between finance and aggregate welfare.

1.7 THE SCOPE OF THE STUDY:

This country-specific study covers the periods 1975 to 2010. The choice is based on data

availability and to have enough observations for time series analysis.

1.8 SOURCE OF DATA AND ECONOMETRIC SOFTWARE:

The source of data will be from the CBN – statistical bulletin and the econometric

softwares to be used are Stata-10 and e-view 8.

19

CHAPTER TWO

LITERATURE REVIEW

This section of the study gives the conceptual and theoretical frameworks; discuss

various literatures on the link between finance and poverty reduction with the review of

empirical literature.

2.1 CONCEPTUAL FRAMEWORK

Financial intermediation is defined as the extent to which financial institutions (banks)

bring deficit spending units and surplus spending units together. Such a joining of

spending units is likely to result in more deepening of the financial sector (Goldsmith

1969, Ghani 1992 Greenwood and Jovanovic 1990). Financial intermediation allows for

financial deepening.

According to Shaw (1973) financial deepening involves specialization in financial

functions and institutions and organized domestic institution and markets. For Nnanna

and Dogo (1998) the concept of financial deepening is usually employed to explain a

state of an atomized financial system (i.e.) a financial system which is largely free from

financial repression. According to Fisher (2001), financial deepening refers to the greater

financial resource mobilization in the formal financial sector and the ease in liquidity

constraints of banks and enlargement of funds available to finance projects.

There are many different ways in which the financial sector can be said to ‗deepen‘. For

example;(a) the efficiency and competitiveness of the sector may improve (b) the range

of financial services that are available may increase (c) the diversity of institutions which

operate in the financial sector may increase, (d) the amount of money that is

intermediated through the financial sector may increase,(e) the extent to which capital is

allocated by private sector financial institutions to private sector enterprises responding to

market signals may increase,(f) the regulation and stability of the financial sector may

improve and (e) particularly important from the welfare perspective more of the

population may gain access to financial services. DFID (2004).

Economic activities in the country can be greatly facilitated by modern banking services.

Financial deepening involves the introduction and intensive use of new financial

products. In this context, it is aimed at modernizing the banking system in order to avail

modern banking and financial services in the Nigerian financial market. Financial

deepening cost becomes high when the administrative costs of banks are high. One of the

main reasons for such high cost was the use of traditional management structure and

20

technology methods by these banks. In this scenario, financial deepening in Nigeria was

also aimed at reducing the administrative cost of the banks.

As such, there is no precise definition in the literature of financial sector deepening and

the theoretical and empirical articles reviewed in this study focus on the different aspects

and measures of financial deepening.

2.2 THEORIES OF FINANCIAL DEEPENING AND ITS LINK TO AGGREGATE

WELFARE:

The intellectual framework for financial reforms in developing countries in the 1980s was

provided by the works of Mckinnon (1973) and Shaw (1973). The Mckinnon-Shaw

paradigm contained two essential issues; (1) the financial sector is critical for economic

growth and (2) extensive government controls imposed on the financial sector prevents

financial deepening and impedes the contribution of the sector to development. The first

issue was not all that new, but only reiterated and re-affirmed ideas contained in the

works of earlier writers such as Gurley and Shaw (1955), Patrick (1966) and Goldsmith

(1969). The second issue was innovative, with the M-S thesis systematically detailing the

efficiency and output costs associated with direct sate intervention in the financial system

labeled ―financial repression‖. However, the general notion from their debate is that the

functions of financial institutions in the savings-investment process were spelt out as

being an effective element for the mobilization and allocation of capital by equilibrating

the supply of loan-able funds with the demand for investment funds and the

transformation and distribution of risks and maturities.

We measure the welfare gains from a financial sector reform through its impact on

financial deepening. From Townsend and Ueda (2006) a complex interaction emerges

between financial sector policy and financial deepening in an otherwise simple growth

model. Indeed, based on a model without any government intervention, they show that

regressions may not reveal a true causal link between financial deepening and its effect.

First, financial deepening is an endogenous variable. It is an aggregation of individual

decisions as shown in much of the theoretical literature, for example, Greenwood and

Jovanovic (1990). Second, in all these models, financial deepening occurs jointly with

economic growth and is a transitional phenomenon, before convergence to a long-run

steady state. Transitional dynamics means that the resulting macro data are not stationary.

This forces researchers to view the entire history as a one-sample draw, Townsend and

Ueda (2009). In the model, the financial sector is endowed with two functions, risk

sharing and an efficiency gain in production, as these are typically considered to be the

21

key functions of banks and other financial intermediaries. The financial sector in the

model requires both fixed costs for entry and variable costs for operations. These create

endogenous movements into intermediation: as they save and invest successfully,

households pass a key wealth threshold for participation in the financial system.

However, the popular Kuznets inverted U-hypothesis Kuznets (1955) brought out the

nature of influence that financial sector deepening has on households with low income.

The theory introduced an increase interest in the contribution that financial deepening can

make to income distribution in developing countries. Kuznets suggested that ―to the

extent that financial sector development facilitates more migration from low-income but

more egalitarian agricultural higher income but more unequal modern (industrial and

services) sector it may be expected to increase inequality‖. This he implied that economic

growth may increase inequality at the early stage of development but reduce it at the

mature stage of industrialization. The asset rich classes who can self finance or have easy

access to finance would reap the early harvest of industrialization and thus garner a

higher share of the economic pie, leaving the poor disadvantaged.

Many economists are then of the view that financial intermediary development will have

a disproportionately beneficial aggregate welfare impact. This according to Galor and

Zeira (1973) and Aghion and Bolton (1997) is because information asymmetries produce

credit constrains that are particularly binding on the low income earners as they do not

have the resources to fund their own projects, nor the collateral to access bank credit. As

only the rich are able to overcome these hurdles they serve to perpetuate the initial

distribution of wealth. Other contrary opinions are suggesting that financial sector

development will overcome these imperfections and reduces income inequality, Clarke et

al (2002).

Financial sector policy affects aggregate welfare both directly and indirectly. The direct

way that financial policy can influence the poor‘ income generation and income

stabilization is by increasing their access to financial services, while the indirect channel

works through growth.

2.2.1 THE INDIRECT CHANNEL THROUGH ECONOMIC GROWTH:

A major channel by which financial deepening supports welfare improvement is through

economic growth. The connection between the operation of the financial system and

economic growth has been one of the most heavily researched topics in development

economics. Hundreds of scholarly papers have been written to conceptualize how the

22

development and structure of an economy‘s financial system affect domestic savings,

capital accumulation, technological innovation and income growth or vice versa.

Many believe that economic growth improves aggregate welfare. The impact of growth

on aggregate welfare runs through a number of possible channels. First, economic growth

could generate jobs for the poor. Second, it has been suggested that a higher rate of

growth could reduce the wage differentials between skilled and unskilled labour at a later

stage of development, which benefits the low income earners and which will eventually

enable them to invest more in human capital, Galor and Tsiddon (1996), Perroti (1993).

Fourth, as capital accumulation increases with high economic growth, more funds would

become available to the low income earners for investment purposes Aghion and Boiton

(1997).

During the 1990‘s, the proliferation of quality data on income distribution from many

countries has allowed vigorous empirical testing of standing debates. Researchers such as

Datt and Ravallion (1992), Kekwani (2000) attempted to explain changes in poverty in

terms of a ―growth effect‖, stemming from a change in average income and a

―distribution effect‖ caused by shifts in the Lorenz curve holding average income

constant. They found the growth effect to explain the largest part of observed changes in

poverty. Economists also agreed that the imperative of growth for welfare improvement

should not be misinterpreted to mean that ―growth is all that matters‖. Fields (2001)

qualified that the extent of the impact of growth on poverty alleviation depends on the

growth rate itself and the level of inequality. Growth is a necessity but is in itself not

sufficient for welfare improvements, because besides growth poverty alleviation requires

additional elements. The poor households need to build up their asset base in order to

participate in the growth process. Also, growth needs to be more broad based and

inclusive to reach all segments of society including the poor. Inequality also matters for

welfare improvement and should be on the agenda, Kanbir and Lustig, (1999).

According to Lustig et al (2002), growth and distribution are interconnected in numerous

ways and the effectiveness with which growth translates into welfare improvements

especially poverty reduction depends crucially on the initial level of inequality.

FitzGerald (2006) critically viewed financial sector reforms and economic growth and

pointed that the potential contribution of financial deepening to economic growth is

considerable but cannot be taken for granted. It depends on the construction of the

appropriate institutional structure. Financial sector development according to him can

23

make an important contribution to economic growth and aggregate welfare and without it

development may be constrained even if other necessary conditions are met.

Levine (1997), (2004) identifies five basic functions of financial intermediaries which

give rise to these effects-savings mobilization, risk management, acquiring information

about investment opportunities, monitoring borrowers and exerting corporate control and

facilitating the exchange of goods and services. Scholars such as Claessens and Feijen

(2006) are of the opinion that financial deepening is associated with higher household per

consumption which is an indicator of aggregate welfare. In their opinion as GDP per

capita grows as a result of financial development, households benefit from higher

income, and can consume and invest more in the process. This obviously matters for

household welfare in terms of nourishment, health care, etc.

2.2.2 THE DIRECT CHANNEL THROUGH ACCESS TO FINANCIAL

SERVICES:

In the same manner that financial services increase income growth, expanding the supply

of financial services which can be accessed by the low income earners will increase

income growth for the poor thus having a direct welfare improvement, Jalilian and

Kirkpatrick (2001).

The provision of savings facilities can enable the low income earners to accumulate funds

in a secure place over time in order to finance a relatively large, anticipated future

expenditure or investment and can some times provide a return on their savings, DFID

(2004).

Financial sector deepening reduces information and transaction costs and therefore

allows more entrepreneurs (especially those less well off) to obtain external finance,

improves the allocation of capital and exerts a particular large impact on the poor.

Fields (2001) argued that much would be gained by developing credit and finance

markets since an undeveloped credit market contributes to continued welfare loss,

especially higher income inequality and slower economic growth.

Through better access to credit, the poor are given the opportunity to participate in more

productive endeavors in turn increasing their incomes. Jeanneney and Kpodar (2005)

noted that, progress in financial intermediaries is beneficial to the poor as it offers

genuine opportunities for their savings; Aderibigbe (2005) is of the opinion that easy

access to credit is more beneficial to the poor than interest rate subsidy. He argued that

targeted public sector credit programmes especially if they are subsidized benefit the non-

24

poor far more than the poor. Claessens and Feijen (2006) argued that financial services

can enable households to be more productive in many ways: Households can borrow for

investment not only in real assets—like fertilizer, a tractor, or a computer—but also for

education, health, and other services that add to their productivity and have high

economic returns. As such, access to financial services can enhance individuals‘ nutrition

and health, and can allow them to send their children to school. Self-employed women

with access to financial services are better able to control their economic destiny and gain

more influence in their households and communities, thus often aiding gender equality.

They further stressed that the benefits of financial sector deepening extend beyond

financing investment, and actually often start by offering better and cheaper payments

and savings services. These services allow firms and households to avoid the costs of

barter cash transactions, reduce the costs of remitting funds, and provide the opportunity

to accumulate assets and smooth income.

Similarly, insurance can provide protection against some types of shocks. These facilities

can reduce the vulnerability of the poor and minimize the negative impacts the shocks

can sometimes have on long-run income prospects. Eswaran et al (1990) argued that just

the knowledge that credit will be available to cushion consumption against income

shocks, if a potentially profitable but risky investment should turn out badly can make the

household more willing to adopt more risky technologies. For this same reason, access to

credit and other financial services is likely to decrease the proportion of low risk. Low-

return assets held by poor households for precautionary purpose can enable them invest in

potentially higher risk but higher return assets with overall long-term income enhancing

impacts, Deaton (1991).

There are however, also skeptical views on whether financial sector deepening can lead

to a broadening of access of financial services by the poor especially at early stages.

Some argue that it is primarily the rich and politically connected who would benefit from

improvements in the financial system, Haber (2004). Some support a non-linear

relationship between finance and income distribution. Greenwood et al (1990) show how

the interaction of financial and economic development can give rise to an inverted U-

shaped curve of income inequality and financial intermediary development.

In addition, there are equally disagreement over how to sequence financial sector

deepening in developing countries, in particular the relative importance of developing

25

domestic banks and capital markets and in developing domestic banks the relative

importance of large and small banks.

Justin Lin (2009) has recently argued that developing countries should make small, local

banks the mainstay of their financial system. He argued that what matters most is setting

up a financial sector that can serve the competitive sectors of an economy which in many

poor countries means focusing on activities dominated by small-scale manufacturing

farming and service firms.

Banerjee (2009) argued that a challenge that most developing countries face is to ensure

an adequate supply of risk capital. Small banks may not be in a position to play such an

important role but the stock market in principle can, by directly funding large firms to

reach a global scale and by enabling a venture capital model of funding high scale risk

new ideas.

Moss (2009) argued that stock markets cannot be expected to provide capital for the poor

or even small companies and that local community banks are better placed for serving

such clients. However, he argued that low-income countries are not faced with choosing

between a stock market and small community banks and that government wanting to

create an enabling environment for the private sector should focus on creating a legal and

financial framework to promote access to credit across the spectrum of demand.

Schoar (2009) while agreeing that a competitive banking sector plays an important role in

facilitating firm growth and competition and that equity markets can at best constitute a

small fraction of overall facilitating in developing countries, questioned promoting small

banks as a solution. She argued that scale matters for banks and tiny banks will not be

able to provide sufficient capital to allow small business to grow into large ones.

Levine (2009) agrees that the structure of financial institutions and markets in many

developed economies is inappropriate for many developing economies- which in his view

is supported by considerable evidence but often ignored by policy advisors- and that

appropriate form and function of financial institutions differ depending on a country‘s

legal and political system as well as on the types of economic activities occurring in the

country.

26

2.3 EMPIRICAL LITERATURE:

A substantial body of empirical work assesses the magnitude of the impact of financial

sector deepening, whether certain components of the financial sector (banks or stock

markets) play a particular important role in fostering growth and whether and what extent

financial sector deepening directly bring about aggregate welfare benefits.

2.3.1 CROSS-COUNTRY EVIDENCE:

To examine whether financial sector deepening has any significant impact on aggregate

welfare indicators indirectly through the growth channel, various cross country analysis

show that economic growth and aggregate welfare are needed strongly and positively

correlated, Dollar and Kraay (2002)Ravallion (2004), Ravallion and Chen (1997).

From the poverty angle, Ravallion and Chen (1997) show that a 10 percent increase in the

mean standard of living leads to an average reduction of 31 percent in the proportion of

the population below the poverty line-indicating that growth leads to a welfare

improvement.

Also, Jalilian and Kirkpatrick (2001) examined the link between financial sector

deepening and poverty reduction using data for a sample of 26 countries including 18

developing countries. They used Bank deposit money assets as a measure of financial

deepening. Their results suggest that a 1 percent change in financial deepening raises

growth in the incomes of the poor in developing countries by almost 0.4 percent-a

significant impact.

Honohan (2004a) showed a robust effect of financial depth (measured as the ratio of

private credit to GDP) on headcount poverty incidence. He found that financial sector

deepening is negatively associated with headcount poverty with a coefficient suggesting

that a 10 percent point change in the ratio of private credit to GDP should (even at the

same income level) reduce poverty ratios by 2.5 to 3 percentage point.

Dollar and Kraay (2002) also show that the average income of the poor in a country

defined as those who belong to the poorest quintile of society-rises proportionately with

the country‘s average income based on a data set of countries over 1950 to 1999. They

used such indicators as good rule of law, openness to international trade and financial

depth as determinants of growth and found that they have little systematic effect on the

income that accrues to the bottom quintile.

Other studies looked at the relationship between financial deepening and distribution of

income about which there are competing theories. Greenwood and Jovanovic (1990)

27

argued that there is an inverted u-shaped relationship between income inequality and

financial sector deepening.

Furthermore, although the validity of the Kuznets curve remains a contested issue, a

common empirical finding in the recent literature is that inequality at the country level

has weak correlation with rates of economic growth, Deininger and Squire (1998), Dollar

and Kraay (2002), Ravallion (2001).

Clarke et al (2002) empirically tested these alternative theories about the relationship

between financial sector deepening and income inequality using data from 91 countries

from 1960 to 1995. Their findings support the theory that there is a negative relationship

between financial sector deepening and income inequality rather than an inverted U-

shaped relationship. One of the factors that determine the elasticity of poverty to growth

is initial inequality, Kekwani et al (2000), Ravallion (1997), (2001). Based on data spells

constructed from two household surveys over time for 23 developing countries Ravallion

(1997) estimates the elasticity of poverty with respect to growth and found that the

elasticity declines shapely as the initial inequality rises. He found that for a country with

an initial Gini index of 0.25, one percentage point of growth is likely to lead to a 3.3

percentage point reduction in poverty incidence with much welfare improvement, while

for a country with an initial Gini index of 0.6, one percentage point of growth is likely to

only lead to a 1.8 percentage point reduction in poverty incidence.

A number of empirical studies examined a more direct relationship between financial

sector deepening and welfare indicators, Claessens and Feijen (2006) found that financial

deepening and household expenditures are highly related. Although causality is less clear

than in the case of income, they opined that there is evidence that financial deepening is a

leading indicator for increases in household consumption. The effect is substantial and

can be shown using several statistical methods. They estimated the elasticity of household

consumption with respect to private credit to be between 0.07-0.22, and found out that the

median growth in the private credit to GDP ratio for 178 countries was 1.6 percentage

points per year over the period 1980-2004. They further made an assumption that if

private credit grows by 1.6 percentage points annually for the next 10 years, this elasticity

implies that world household expenditure 10 years from now would be 1.1–3.6

percentage points higher than current levels.

They have further findings using panel data fixed effects regressions with over 4100

observations for 142 countries, they control for government consumption as a share of

28

GDP, trade as a share of GDP, and inflation. And found that 1, 5, and 10 year lagged

values of private credit to GDP have a significant impact on contemporaneous household

expenditure. In addition, they found that average private credit (logs) has a highly

significant impact on the growth of household consumption and average household

consumption (logs) in the period 1980-2004.

Li et al (1998) found that financial depth (measured as the ratio of broad money supply

[m2] to GDP) is associated with lower inequality and also higher income of the lower

80% of the population (i.e. the poor majority) based on data for 40 developed and

developing countries over 1947 to 1994, the regression results suggest that a one percent

standard derivation increase in financial depth would result in an increase of US $ 3,000

in the incomes of the poor but only an increase of US $1,600 in the incomes of the rich.

Beck et al (2004) used data on 52 developing and developed countries over the period

1960 and 1999, to assess whether there is a direct relationship between financial sector

development (measured by credit to the private sector) and changes in income

distribution. They found that the income of the poorest 20% of the population grows

faster (using GDP per capital) in countries with higher financial sector development and

that income inequality falls. Beck et al (2000) examined the influence of financial

intermediary development on income redistribution using the sources of growth linkage

(productivity growth, physical capital accumulation and private savings). While the

linkage between financial sector development and private savings/ capital accumulation

is found to be not robust to alternative specifications they found a robust and positive

relationship between financial development indicators and productivity growth.

Beck et al (2004) show that countries with better developed financial intermediaries

(measured as the ratio of private credit to GDP) experience faster declines in both poverty

and income inequality by disproportionately boosting the income of the poor, hence,

bringing about much welfare benefits.

Claessens and Feijen (2006) also examined whether financial sector deepening plays any

role in achieving millennium development goal (MDG) targets. They found evidence that

financial deepening and greater access to financial services indeed lead to income growth,

a reduction in poverty, undernourishment and better health, education and gender quality.

They concluded that financial services such as savings can help firms and households

cope with economic shocks which lead to improvement in household welfare.

Dehejia and Gatti (2002) found that an increase in access to credit leads to improvement

in household welfare by reducing the extent of child labour. He argued that this is

29

because, in the absence of developed financial markets, poor households with high levels

of income variability are found to resort substantially to child labour to diversify their

sources of income and reduce vulnerability to shocks.

2.3.2 COUNTRY SPECIFIC EVIDENCE:

Evidence from country specific studies shows that the financial sector reforms initiated in

the late 1990s in Pakistan created a favourable environment in which the poor and

middle-class have a better chance of receiving credit from formal institutions, Husain

(2004). In his study of the relationship between financial deepening, savings mobilization

and poverty reduction in Ghana, Quartey (2008) found that financial sector deepening has

a positive impact on poverty which is one of the indicators of aggregate welfare, although

the impact is insignificant in view of the fact that financial intermediaries have not

adequately channeled savings to the pro-poor sectors of the economy.

Burgess and Pande (2005) found that increased savings mobilization and credit provision

in rural areas contributed to welfare gains in rural India. They found that branch

expansion in rural India led to faster growth of non-agricultural output, growth of

agricultural wages and decline in poverty in states that started the period with a lower

level of financial sector deepening. The most important channel through which financial

sector deepening directly affects aggregate welfare is increased access to financial

services. Empirical evidence suggests that firms‘ and households access to financial

services rises with financial deepening. Beck et al (2007). However, studies by Morduch

(1998), Coleman (1999) questioned the rigor and validity of the findings of standard

impact assessments of microfinance institutions highlighting data and methodological

problems. In any case, it is difficult to derive from these studies aggregate results on the

impact of Micro Finance Institutions comparable to those produced by studies using more

formal financial sector deepening indicators, as the diversity of such arrangement and

providers prevents easy generalizations.

In Nigeria, few empirical studies have been carried out on the subject matter. Recently,

Osinubi and Akinyele (2006) carryout an in-depth study of domestic money bank lending

using secondary sourced time-series data from 1970-2003. They suggested that increases

in bank lending rates compound the problem of rising cost of funds in the performance of

the sector. Using endogenous growth model time series techniques and annual date from

1970-2002, Akpan (2004) explored the impact of financial deepening on the rate of

30

economic growth in Nigeria and the empirical results showed a positive impact in

Nigeria.

Nzotta and Okereke (2009) using stepwise least square regression method found that

financial reforms in Nigeria from 1986 to 2007 have a relatively low level of deepening

impact on the financial market. Similar results were shared by Nnanna and Dogo (1999),

and Ayida (2007) where the prime lending rate was used to examine the relationship

between the lending pattern and financial deepening in Nigeria.

2.4 EFFORTS TOWARDS DEEPENING THE FINANCIAL SECTOR IN

NIGERIA.

Nigeria like other African countries was faced with a series of economic problem. Some

of these were high inflation and unemployment, increasing poverty, low economic

growth, high fiscal deficits, and high balance of payment deficits, financial sector

repression and worsening terms of trade. The necessary conditions for growth and

efficient economic management prompted the need for adoption of a consistent,

appropriate macroeconomic policy framework and the existence of high quality

institutions. The introduction of the Structural Adjustment Programme (SAP) in July

1986 was an effort to set the macroeconomic policy framework right. The major financial

sector reform policies implemented were the deregulation of the interest rates, exchange

rate and the liberalization of entry and exit into banking business. Also there was the

establishment of the NDIC, strengthening the regulatory and supervisory institutions etc.

Even though some positive effects in the growth of financial institutions and financial

instruments were recorded during the SAP-era, the systemic risks and vulnerability of the

institutions became higher.

However, in July 2004, the mother of reforms came in Nigeria when 89 banks were

forced to emerge forming 25 universal banks. This was further reduced to 24 banks at the

end of December 2007 with the emergence of Stanbic Bank Plc and IBTC Bank to form

Stanbic IBTC Bank plc. The two major elements of the reform agenda are the

requirement for Nigerian banks to increase their shareholders funds to minimum of

N25billion by the end of December 2005 and consolidation through Mergers and

Acquisition (M and A). Insurance companies were equally mandated to increase their

shareholders funds by December 2007to N10billion for re-insurers, N3billion for general

31

insurers and N2billion for life insurer‘s operators. This exercise has brought about a

reduction in the number of insurance companies from 103 to 71.

2.5 LIMITATIONS OF PREVIOUS STUDIES

The evidence provided in the literature seems to suggest that the subject have become an

important empirical debate amongst researchers and policy makers. Most of the case

studies reviewed focused mainly on poverty. They used cross-section data on countries

that may be diverse, raising the possibility that the empirical findings could be distorted

by heterogeneity biases affecting both financial deepening and poverty. A major

weakness of such country analysis is that its results are only indicative of average trends.

However, some country specific studies did not consider the fact that financial deepening

indicators varies between periods and countires, the same is applicable for measures of

poverty. And, financial deepening is a macro concept while poverty is more of a micro

analysis. Therefore, such country specific finance poverty nexus will be more meaningful

if studied from the angle of finance aggregate welfare link.

Moreso, the effects of financial variables take time to transmit to other variables, most

studies except Odhiamboh did not use the ARDL-ECM in estimating the impact of

financial deepening on aggregate welfare indicators, which has numerous advantages as

specified in chapter three.

Studies on Nigeria have concentrated more on the link between financial deepening and

economic growth. None has gone further to examine the influence that financial

deepening has on aggregate welfare especially, as it concerns the low income earners.

Most of these studies used the traditional financial deepening proxy-MS2/GDP as an

explained variable, Nzotta and Okereke (2009), Nnanna and Dogo (1998), etc. There are

also very few empirical studies which focused on the issue of access to financial services

using bank branches as one way of expressing the impact of financial deepening on

aggregate welfare, which means that this important issue is often overlooked.

This research work fills the gaps that has been overlooked by the literature on country-

specific bias and intends to analyze access to financial services using number of bank

branches.

32

CHAPTER THREE

METHODOLOGY

Macroeconomic variables do not instantaneously transmit to other variables especially

social indicators. This is because when such impact is transmitted, it involves a time lag

between the transmitting variables and the admitting variables. This makes it very vital to

use a dynamic model to capture the essence of such relationship.

3.1 ANALYTICAL FRAMEWORK: Financial deepening as noted before means an

increase in the supply of financial assets in the economy. It is important to develop some

models of the widest range of financial assets, including money. The sum total of all the

financial assets is one broad measure that represents financial deepening. However, King

and Levine (2003) constructed some indicators of financial depth to measure the services

provided by financial intermediaries;

1) Ratio of liquid liabilities to GDP

2) Ratio of credit issued to the private sector to GDP

The range of financial assets to be considered in this study as measures of

financial deepening include, the ratio of private credit to GDP, ratio of broad money

(MS2) to GDP, prime lending rates (PLR), ratio of currency in circulation to money

supply – (expressing the banking habit) and the ratio of deposit money bank assets to

GDP.

Also, from recent existing literature, measures of aggregate welfare in this study will use

private per capita consumption as proxy following Odhiambo (2009), Gloede and

Rungruxsirivorn (2010). Due to unavailability of survey data on household access to and

utilization of financial services, it is not possible to carry out an impact assessment or an

econometric estimation of increased or decreased financial services access on aggregate

welfare. However, the underlying assumption of using private per capita consumption as

a measure of aggregate welfare is that if an individual has been able to access financial

services and repay loans on a continuous basis from/to a given rural financial institutions

that has attained high levels of outreach and sustainability, then it implies that the

individuals well being is improved. Financial access here is defined as the availability of

supply of quality financial services at reasonable costs, Asenso-Okyere et al (1993). The

different dimensions to access include; the dimension of availability to be measured by

bank branch distribution and the second dimension is the question of cost-at what price

are the financial services available?

33

3.2 THE MODEL:

This research work will adopt the ANCOVA model for objective one with the

introduction of dummy variable for objective one in the multiplicative form and the

ARDL model for objectives two and three. The multiplication form dummy will enable

us to differentiate between slope coefficients of the two periods (for objective one). We

shall adopt a single regression equation for objectives one and two and a different

equation for objective three; using OLS estimation because of its reliable traits as the best

unbiased estimator. Its error term has a minimum and equal variance. Hence, in

estimating the first and second objectives, PSC/GDP will appear as endogenous variable

in the financial deepening model and will appear as an explanatory/predetermined

variable in the aggregate welfare model. This is a case of simultaneity bias but in the

form of recursive model; thus, allow the application of OLS, Gujarati (1978).

3.2.1 MODEL SPECIFICATION:

Following Nzotta and Okereke (2009) the functional form specification in investigating

financial deepening is as follows;

PSC/GDP = f(COB/MS2,NBBT,INS, and Dummy)………1

Dummy. D = O period before consolidation (1975-2004), and D=1 period after

consolidation, (2005-2010).

PSC/GDP = f(FS/GDP, DMBA/GDP, NBBT, COB/MS2, PLR)…………………2

And following Quartey (2008), Odhiambo (2009), Gloede and Rungruxsirivorn (2010)

the aggregate welfare equation is;

PPCE = f (GDPPC, NBBT, RGDPGR, PSC/GDP, INF) ……………… (3)

Where PPCE = Private per capita consumption proxy for poverty reduction, and FD =

Financial deepening indicator- PSC/GDP.

Transforming equation 1 into a linear function; PSC/GDP= 0+ 1D1 + 2COB/MS2 +

3NBBT + 4INS + 5(D1COB/ MS2) + ut………..(4)

Were 0 = the constant or the intercept and 1= the differential intercept 6 =

differential slope coefficient for multiplicative case between the dummy and COB/MS2-

indicating by how much the slope coefficient of the reform periods differ from the slope

coefficient of the base period.

34

MODEL 1:

Transforming equation 4 yields

(PSC/GDP)= 0 + 1Dit + 2(COB/MS2) + 3(NBBTt) +

4 (INS)t + 5 (Di COB/MS2)t + Ut……..(5)

Equation 5 is model A for our objective one. The null hypothesis in equation (1) is 1 =

0 and 5 = 0 indicating that there are no structural changes between the two periods, i.e.

the financial deepening index for the two periods are the same.

Equation 2 can be transformed to the model below;

MODEL 2:

(PSC/GDP)t = 0 + 1(PSC/GDP)t-1 + 2 (FS/GDP) t-i + 3 (DMBA/GDP+-j) +

4(NBBT)t-k + 5(COB/MS2t-i) + 6(PLR)t-j + Ut ………………. 6

Equation 6 is model B for our objective two it assumes that all variables are well

behaved, which implies that the variables are stationary at order zero.

= Difference operator

= estimated coefficient

t-I,t-j,t-k,etc unknown lags to be determined.

μ = error term.

MODEL 3:

PPCEt = 0+ 1PPCEt-1 + 2 (GDPPC)t-q + 3(NBBT)t-u +Σ 4(∆FDt-v) +

5( INFt-x) + Vt ………............... (7)

, and otherwise equations 6 and 7 translate to;

(PSC/GDP)t = 0 + 1(PSC/GDP)t-1+ Σ 2(FS/GDP)t-i + Σ 3(DMBA/GDP+-j)

+Σ 4(NBBT)t-k + Σ 5(COB/MS2t-l) + Σ 6( PLR)t-m + ut…………… 8

PPCEt = 0+ 1PPCEt-1+ Σ 2(GDPPC)t-q + Σ 3(NBBTt-u) + Σ 4(∆FDt-v ) +

Σ 5( INFt-x) + Vt……… (9)

If the order of integration is ascertained, then investigation of the presence of a co-

integration amongst the variables will be tested. For models two and three, the F test is

used for testing the existence of long-run relationship. When long-run relationship exit, F

test indicates which variable should be normalized. The null hypothesis of no

35

cointegration among the variables in equations 8 and 9 is Ho: 1= 2= 3= 4

= 5= 6=0 and Ho : 1= 2= 3= 4= 5=0 against the alternative hypothesis, Hi:

1≠ 2≠3 4 ≠ 5≠ 5 ≠ 0 and H1 : 1≠ 2≠ 3≠ 4≠ 5≠0. The F test has a non-

standard distribution which depends on (1) whether the variables included in the model

are 1(0) or 1(1), (ii) the number of regressors and (iii) whether the model contains an

intercept and / or a trend. The test involves asymtotic critical bounds depending on

whether the variables are 1(0) or 1(1) or a mixture of the both. Two sets of critical values

are generated, with one set refers to as the 1(1) series and the other the 1(0) series.

Critical values for the 1(1) series are the referred to as the upper bound critical values

while that of the 1(0) series are reffred to as the lower bound series.

If the F test statistics exceed thier respected critical values we can conclude that there is

evidence of long-run relationship between the variable respective of their order of

integration and vice versa, Pesaran et al (2001).

If the residuals are stationary and a long run relationship is established, then the error

correction estimates can be obtained from equations 8 and 9. On that note, if the unit

roots test indicates evidence of co-integration, then equations 8 and 9 translates to an