financial fridays financial planning assessment las vegas (2)

TRANSCRIPT

Financial PlanningDevelopments and Opportunities

Leonard C. Wright, CPA/PFS, CGMA, CFP®, ChFC®, CLU®

Money Doctor, American Institute of Certified Public Accountants

360financialliteracy.org

FeedThePig.org

Financial Fridays Financial Literacy App:

Leonard Wright, CPA/PFS

Intention

The Truth In Your Heart

Agenda

Financial Planning – The Process

Business Planning Opportunity – ERISA Plans

Financial Planning – The Elements

Insurance Planning – The Pitfalls and the Leverage

Investment Planning – The Future

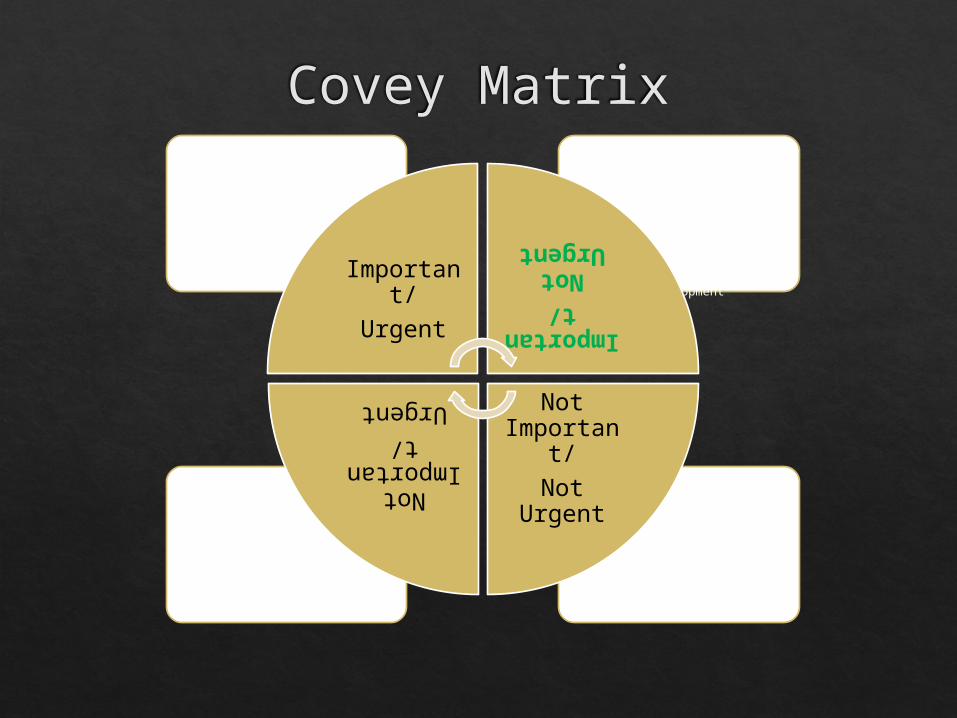

Covey Matrix

• Emails• Junk Mail• Solitaire• Unproductive

activities

• Unimportant call• Unplanned knock

at the door.• Unnecessary or

lengthy meetings.

•Tax Planning•Financial Planning•Estate Planning•Risk Management Planning

• Investment Planning.•College Planning.• Relationship building• Systems Development

•Annual Tax Returns•Form 706•Annual Review/Audit•Extensions.•RMD•Client Report•Payroll Tax Returns

Important/

Urgent Important/Not

Urgent

Not Important

/Not

Urgent

Not Important

/Urgent

Financial Planning

Strategies Tactics Tools

Financial Planning

Mission Vision Values Goals

Financial Planning

• Solutions• Strategies• Tactics• Tools

• Strategies• Tactics• Tools

• Mission• Vision• Values • Goals

• Ensure that STT continue to be consistent with Mission Values and Goals.

Review

IdentifyDevelopImpleme

nt

Courtesy: Legacy Boston

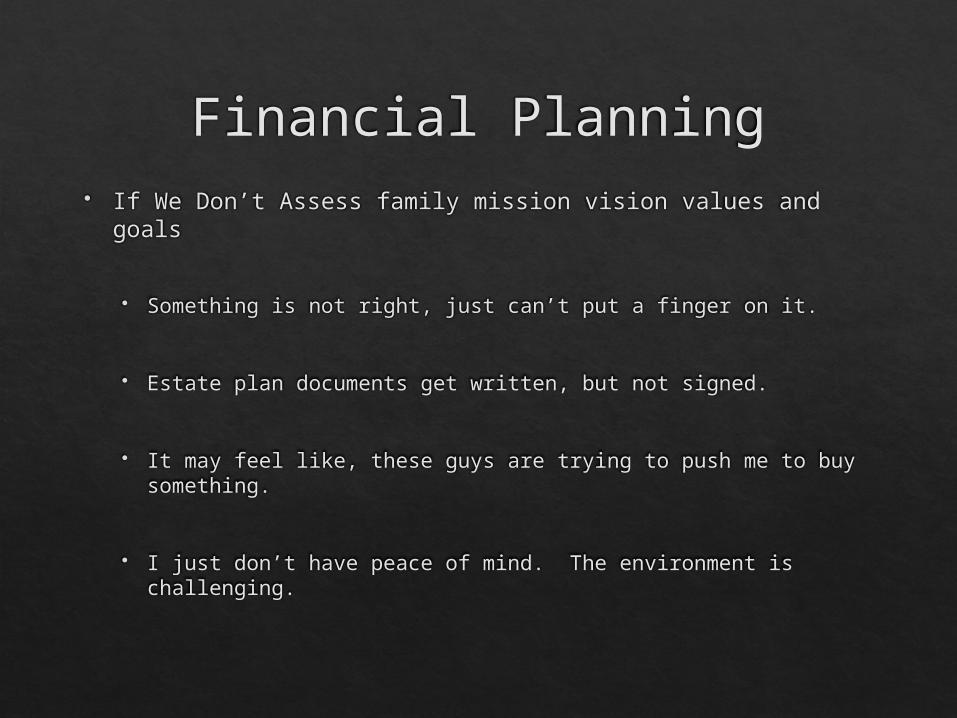

Financial Planning If We Don’t Assess family mission vision values and goals

Something is not right, just can’t put a finger on it.

Estate plan documents get written, but not signed.

It may feel like, these guys are trying to push me to buy something.

I just don’t have peace of mind. The environment is challenging.

The Process of Planning Planning Questionnaire.

Very low focus questions on the stuff you have.

Complexity Questionnaire.

Risk Questionnaire.

Kolbe Questionnaire.

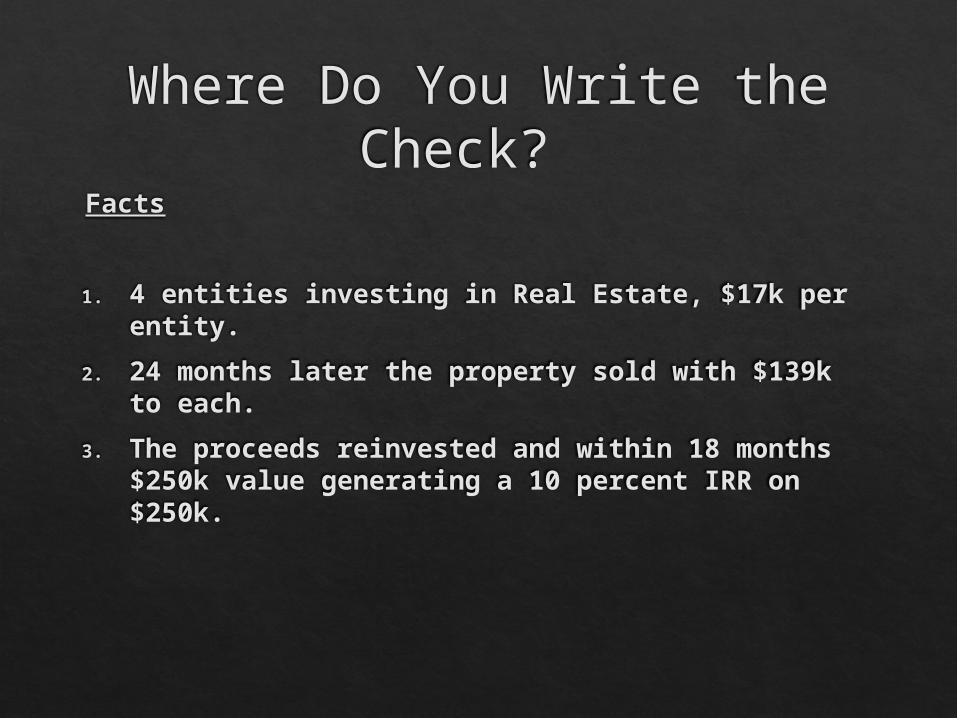

Where Do You Write the Check?

Facts

1. 4 entities investing in Real Estate, $17k per entity.

2. 24 months later the property sold with $139k to each.

3. The proceeds reinvested and within 18 months $250k value generating a 10 percent IRR on $250k.

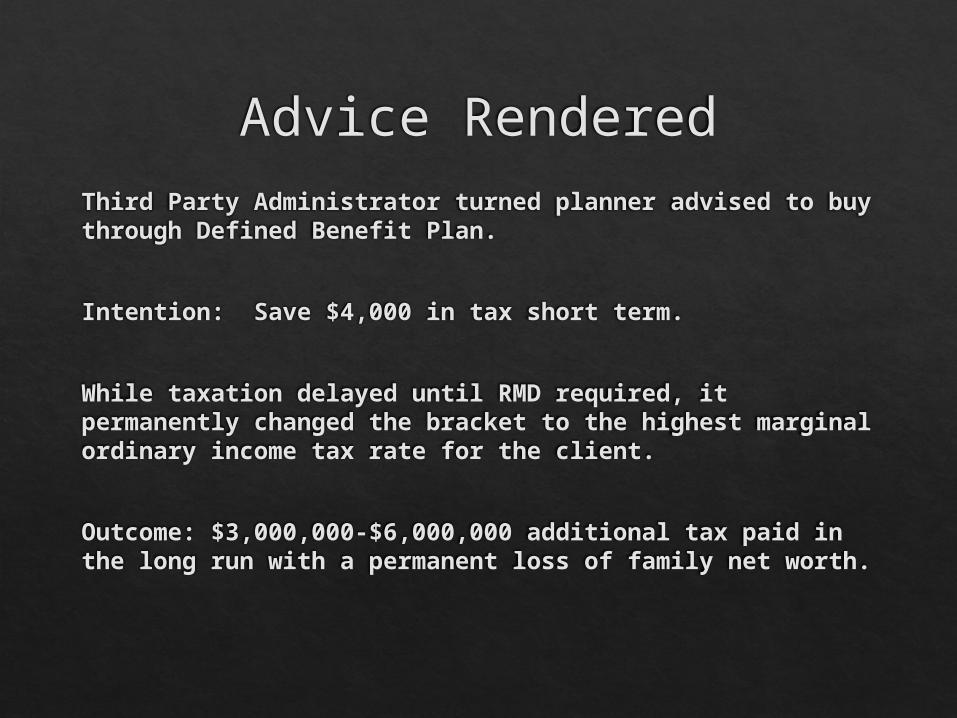

Advice RenderedThird Party Administrator turned planner advised to buy through Defined Benefit Plan.

Intention: Save $4,000 in tax short term.

While taxation delayed until RMD required, it permanently changed the bracket to the highest marginal ordinary income tax rate for the client.

Outcome: $3,000,000-$6,000,000 additional tax paid in the long run with a permanent loss of family net worth.

End ResultAge Defined Benefit

PlanRoth 401k/IRA

70 1,855,000 2,980,000

75 2,455,000 4,799.000

80 4,203,000 7,728,000

85 6,432,000 12,446,000

90 9,661,000 20,045,000

401k/Profit Sharing Plans Firm acts as Trustee.

Can be set up to discriminate under the proper conditions.

If employees below SS Threshold, and combined with Worker’s Comp, the plan can pay for itself through significant savings.

Nearly 100 percent enrollment – including Hispanic speaking populations.

Pre-Programmed to triple the level of retirement plan success.

Creates a retirement liability on an individual basis.

Provides a platform to expand employee benefits/planning.

Allows 4 different investment options

Low cost funds

Tax Free Tax Deferred

Tax Advantage

d

Taxable

What Roth IRA IRA Real Estate BondsRoth 401k 401k Oil and Gas STCG

Muni Bonds Simple IRA Stocks

Life Insurance SEPDividends

Distribution Annuity

Loans DBP

1035 X LTC

Who Low Income Rising Rising Diversifier

A portion for Income Income Safety Rising Income Save for RI Save for RI IncomeEstate Planning RI Distr RI Distr.LTC Planning Annuities

Age 16-80 31-70 31-70 25-100

RMDs No Yes N/A No

Tax at LTCGDistribution None OI STCG OI

Special Rules

Tax Diversification

Number of Tax Diversification OptionsUsed and Kept over the Years.

Level ofHappinessIn Retirement

Elements of a Financial Plan

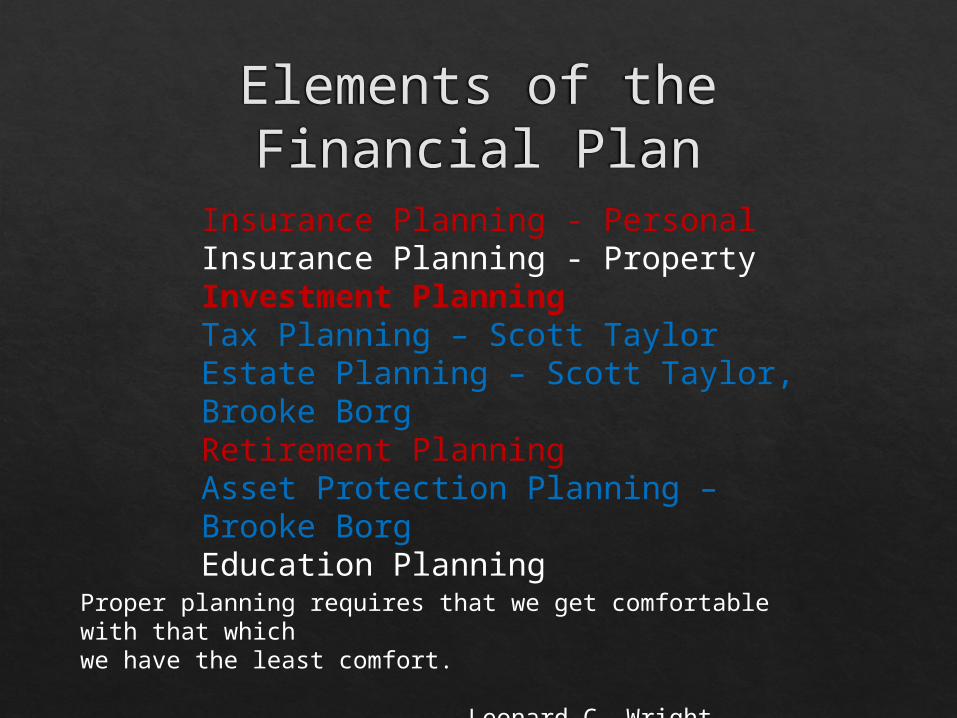

Elements of the Financial Plan

Insurance Planning - PersonalInsurance Planning - PropertyInvestment PlanningTax Planning – Scott TaylorEstate Planning – Scott Taylor, Brooke BorgRetirement PlanningAsset Protection Planning – Brooke BorgEducation Planning

Proper planning requires that we get comfortable with that whichwe have the least comfort.

--Leonard C. Wright, CPA/PFS, CGMA

Insurance Planning

•Mitigating Risk

•Types of Risk

•Preserving Wealth

•Non Qualified Planning Options

Creditor Protection

Tax Free Distribution if planned properly

Tax advantaged accumulation

High flexibility for loans and distributions

Estate planning tool.

Failed Intentions: Read the Contract

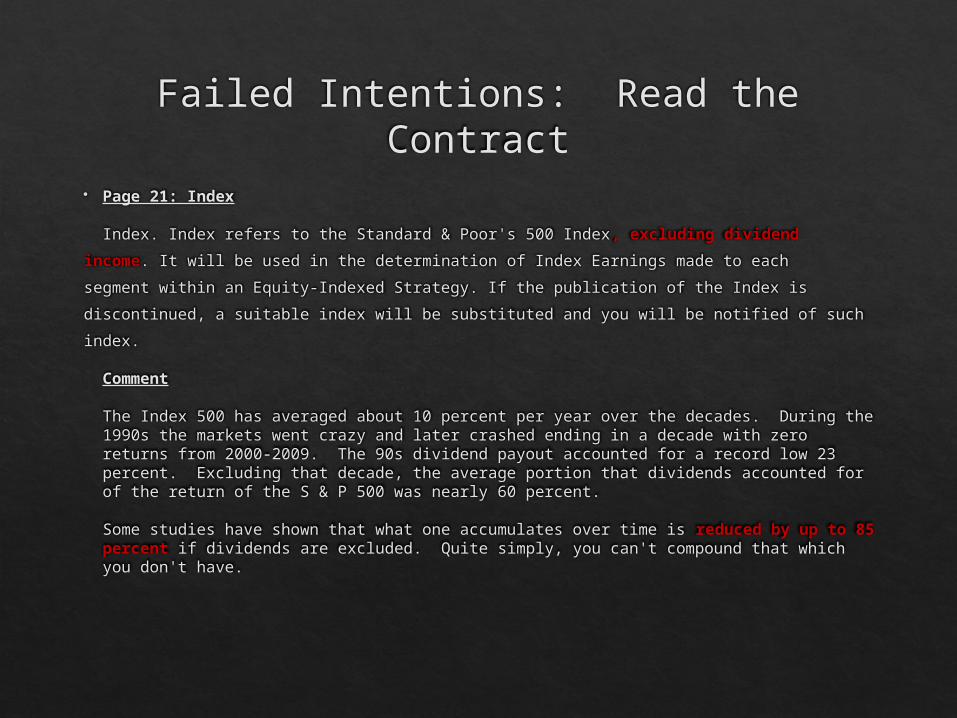

Page 21: Index

Index. Index refers to the Standard & Poor's 500 Index, excluding dividend

income. It will be used in the determination of Index Earnings made to each

segment within an Equity-Indexed Strategy. If the publication of the Index is

discontinued, a suitable index will be substituted and you will be notified of such

index. Comment

The Index 500 has averaged about 10 percent per year over the decades. During the 1990s the markets went crazy and later crashed ending in a decade with zero returns from 2000-2009. The 90s dividend payout accounted for a record low 23 percent. Excluding that decade, the average portion that dividends accounted for of the return of the S & P 500 was nearly 60 percent. Some studies have shown that what one accumulates over time is reduced by up to 85 percent if dividends are excluded. Quite simply, you can't compound that which you don't have.

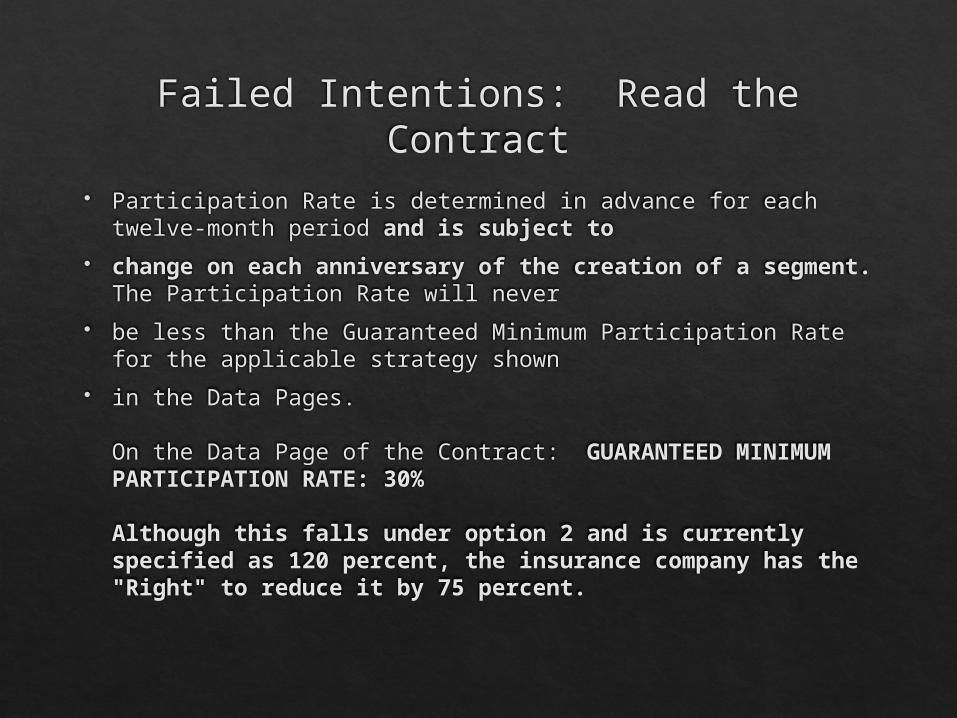

Failed Intentions: Read the Contract

Participation Rate is determined in advance for each twelve-month period and is subject to

change on each anniversary of the creation of a segment. The Participation Rate will never

be less than the Guaranteed Minimum Participation Rate for the applicable strategy shown

in the Data Pages. On the Data Page of the Contract: GUARANTEED MINIMUM PARTICIPATION RATE: 30% Although this falls under option 2 and is currently specified as 120 percent, the insurance company has the "Right" to reduce it by 75 percent.

Failed Intentions: Read the Contract

Overloan Protection Rider According to the rider, you will have 60 days to respond and pay a premium when your policy goes into an excessive "Overloan" status. Failure to do so will result in a cancellation of the rider and the policy shall lapse. You must meet the following conditions for the rider to kick in; over age 75, have the policy for at least 15 years, the loan balance must be more than the face value, and the outstanding debt must be at least 95 percent of the outstanding value less surrender charges. Comment My perspective is that this is a very dicey position for you to be placed in. You fail this test, you could end up with taxable income you don't want to think about. Supposing you had a stroke and your wife was worried about you and did not pay attention to this notice. There are many circumstances that you could have significant issues. The rider stipulates a premium to be paid, but does not state how to calculate it. Nevertheless, this is a tough provision. You have it as long as you can respond within a few weeks. My view is that if they really wanted to give you this rider, they would have built it into the contract and priced for it rather than some sort of premium within a few days to be paid decades down the line. Needless to say, I will be following up with the company to get more specifics on this provision.

Yes I promised Lifetime Income

Some annuity companies are trying to find out how they can get out of paying rich benefits that they can no longer afford to pay.

Allowed insured to pick the most aggressive investments and lose big time.

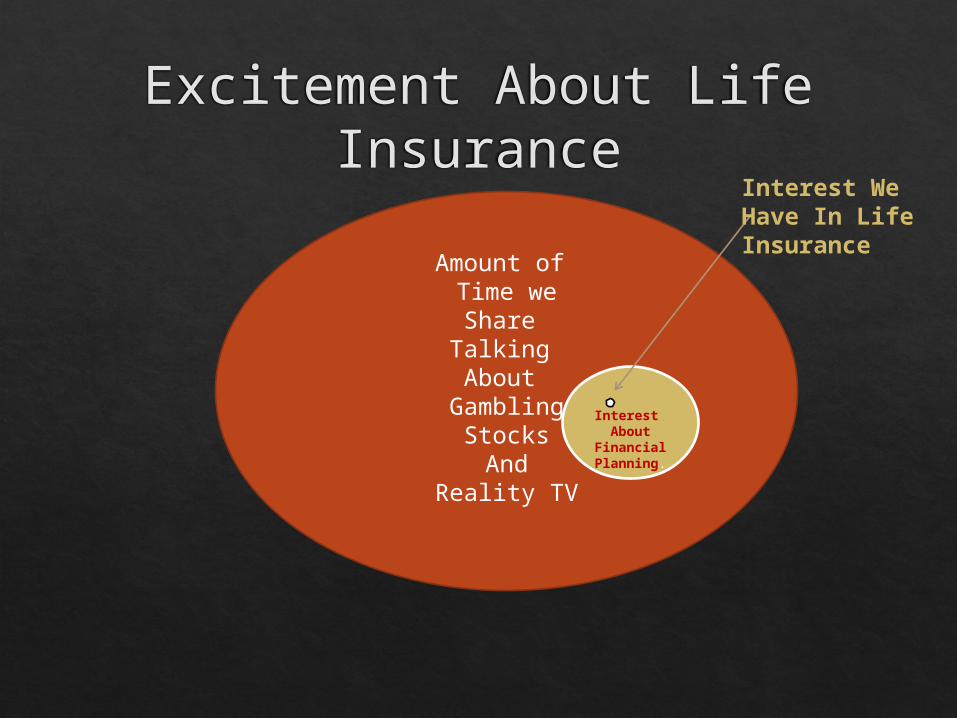

Excitement About Life Insurance

Amount of Time weShare Talking About

GamblingStocks

AndReality TV

Interest About

Financial Planning.

Interest WeHave In LifeInsurance

Opportunity Lost

Benefit ofProper

LifeInsurancePlanning

WhenMatched

To MVVG

Amount Insurance

AgentKnows.

AmountFamily, FriendsAnd StrangersKnow AboutLife Insurance.

Disabled CashTax Advantaged AssetsTax Free Distributions Long Term Care Potential Income Stream (risks)

Life Insurance Quality Assessed

Performance History?

Ratings?

Structure?

Rate Increases?

Contractual Provisions?

In Force Ledgers?

Life Insurance Considerations for Today’s Market

Verify Ownership

Verify who the beneficiaries and contingent beneficiaries are.

Review the Insurance company

Run an in-force ledger

Cash projections for future premiums.

Verify what the purpose of the policy was intended to Accomplish.

Life Insurance Company Issues

Exposure to sub-prime investments in their investmentportfolios.

Exposure to guarantees on variable annuities.

Exposure to inadequate pricing assumptions on issuedpolicies.

Debt listed as equity on the balance sheet. (Surplus Notes)

Move to weaken reserve requirements.

To No Lapse or Not to No Lapse

No cash value

No flexibility

Can’t miss payments or No Lapse provision void. The policy could go to zero value.

Conflicting perspectives within the same firm.

Life Changes over time.

Long Term Care Experience

Likelihood of an event

Age

Resources

http://www.aicpa.org/Press/PressReleases/2012/Pages/AICPA-Offers-Free-Consumer-Webinar-on-Planning-for-Long-Term-Care.aspx?action=print

Long Term Care for Consumers: Planning for Your

Future Health Care in Plain English

Investment Planning

Risk Perception vs.

Risk Tolerance

What is the Market Going To Do?

Important to UnderstandThe PastDow Cycles

1906 103

1923 103

1929 381

1954 381

1967 995

1982 995

2000 11,750

2002 7,286

2007 14,164

2009 6,547

2014 high 18,053

02/06/15: 17,824

Tomorrow ??????http://stockcharts.com/freecharts/historical/djia2000.html

Focus on Noise: Not Connected With Plan

NoiseHHS, SS, Interest Nearly Entire

BudgetJim Cramer

GoldMake 50%Today!

Armageddon Debt 21T

Deficit $400BState Debt 3T

Global and

Investment info

Important:Your PlanYour Life

Complications of Intentions

Confusion between Risk Perception and Risk Tolerance.

Subjectivity. Perspectives. Risk levels not defined. Lack of competency. Ineffective communication. Behavioral Economics

Investment Planning Does your investment portfolio have a job description that is

consistent with your MVVG?

Has an acceptable risk tolerance been developed, and is it reviewed annually?

Is there adequate diversification?

Has the quality of the assets been evaluated?

Have portfolio turnover rates, expense charges, and fees been evaluated?

Leonard Wright, CPA/PFS App

KLAV 1230 AM, Las Vegas Nevada 3-4PMhttp://www.klav1230am.comAll shows are podcastGo to: PBTK.COM

Leonard C. Wright,Scott Taylor,Jason A. ThomasFinancial FridaysUpdates at Leonard C. Wright

Follow at leonardcwright

[email protected]@[email protected]

AICPA Money Doctor: 360financialliteracy.orgFeedthePig.org, TotalTaxInsights.org

CPA DailyFinancial Fridays Daily

Leonard C. Wright, CPA/PFS, CGMA, CFP®, ChFC®, CLU®