financial guaranty insurance company years ended december ... · s tatutory-basis f inancial s...

TRANSCRIPT

S T A T U T O R Y - B A S I S F I N A N C I A L S T A T E M E N T S

Financial Guaranty Insurance Company Years Ended December 31, 2013 and 2012 With Report of Independent Auditors

Ernst & Young LLP

Financial Guaranty Insurance Company

Statutory-Basis Financial Statements

Years Ended December 31, 2013 and 2012

Contents

Report of Independent Auditors.......................................................................................................1

Statutory-Basis Balance Sheets ........................................................................................................3 Statutory-Basis Statements of Operations .......................................................................................4 Statutory-Basis Statements of Changes in Capital and Surplus (Deficit) ........................................5 Statutory-Basis Statements of Cash Flows ......................................................................................6 Notes to Statutory-Basis Financial Statements ................................................................................7

1

Report of Independent Auditors

The Board of Directors Financial Guaranty Insurance Company

We have audited the accompanying statutory-basis financial statements (the “financial statements”) of Financial Guaranty Insurance Company (the “Company”), which comprise the balance sheets as of December 31, 2013 and 2012, and the related statements of operations, changes in capital and surplus (deficit), and cash flows for the years then ended, and the related notes to the financial statements.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in conformity with accounting practices prescribed or permitted by the New York State Department of Financial Services (“NYSDFS”), as well as those accounting practices detailed in the NYSDFS Guidelines. Management also is responsible for the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free of material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design the audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

A member firm of Ernst & Young Global Limited

Ernst & Young LLP 5 Times Square New York, NY 10036-6530

Tel: +1 212 773 3000 Fax: +1 212 773 6350 ey.com

2

Basis for Adverse Opinion on U.S. Generally Accepted Accounting Principles

As described in Note 4 to the financial statements, to meet the requirements of the NYSDFS, the financial statements have been prepared in conformity with accounting practices prescribed or permitted by the NYSDFS, as well as those accounting practices detailed in the NYSDFS Guidelines, which practices differ from U.S. generally accepted accounting principles. The variances between such practices and U.S. generally accepted accounting principles and the effects on the accompanying financial statements are described in Note 4. The effects on the accompanying financial statements of these variances are not reasonably determinable but presumed to be material.

Adverse Opinion on U.S. Generally Accepted Accounting Principles

In our opinion, because of the effects of the matter described in the preceding paragraph, the statutory-basis financial statements referred to above do not present fairly, in conformity with U.S. generally accepted accounting principles, the financial position of Financial Guaranty Insurance Company at December 31, 2013 and 2012, or the results of its operations or its cash flows for the years then ended.

Opinion on Statutory-Basis of Accounting

However, in our opinion, the statutory-basis financial statements referred to above present fairly, in all material respects, the financial position of Financial Guaranty Insurance Company at December 31, 2013 and 2012, and the results of its operations and its cash flows for the years then ended in conformity with accounting practices prescribed or permitted by the NYSDFS, as well as those accounting practices detailed in the NYSDFS Guidelines.

Adoption of Accounting Practices as detailed in the NYSDFS Guidelines

As disclosed in Note 4 to the statutory-basis financial statements, the Company changed its accounting practices to reflect the NYSDFS Guidelines effective August 19, 2013, and applied it prospectively. Our opinion is not modified with respect to this matter.

ey February 21, 2014

A member firm of Ernst & Young Global Limited

3

Financial Guaranty Insurance Company

Statutory-Basis Balance Sheets

(Dollars in Thousands, Except Per Share Amounts)

December 31, 2013 2012 Admitted assets Bonds $ 1,365,097 $ 1,296,051 Common stock 15,218 Other invested assets 16,520 22,371 Short-term investments 566,540 676,681 Cash and cash equivalents 18,298 8,395 Total cash and invested assets 1,981,673 2,003,498 Accrued investment income 15,054 14,376 Other assets 1,731 2,722 Receivable from parent and subsidiaries 827 241 Total admitted assets $ 1,999,285 $ 2,020,837 Liabilities and capital and surplus (deficit) Liabilities:

Losses $ 1,367,388 $ 3,863,104 Loss adjustment expenses 42,422 33,326 Unearned premiums 122,546 172,151 Provision for reinsurance 24,287 Contingency reserves 367,178 543,822 Accounts payable and accrued expenses 8,520 8,115 Payable for securities 10,738 Federal and foreign income tax payable 544 143 Ceded balances payable 351

Total liabilities 1,932,885 4,631,750 Capital and surplus (deficit):

Common stock, par value $1,500 per share; 10,000 shares authorized, issued, and outstanding 15,000 15,000

Redeemable preferred stock, par value $1,000 per share; 3,000 shares authorized, issued and outstanding 300,000 300,000

Paid-in surplus – 439,881 Unassigned deficit (248,600) (3,365,794)

Total capital and surplus (deficit) 66,400 (2,610,913) Total liabilities and capital and surplus (deficit) $ 1,999,285 $ 2,020,837

See accompanying notes.

4

Financial Guaranty Insurance Company

Statutory-Basis Statements of Operations

(Dollars in Thousands)

Year Ended December 31, 2013 2012 Premiums earned $ 95,876 $ 70,908 Loss reserve release 2,467,498 972,547 Loss adjustment reserve (expense) release (39,778) 5,012 Other underwriting expenses (50,965) (45,518) Ceding commission income (expense) 104 (7,986) Underwriting income 2,472,735 994,963 Net investment income 51,810 46,995 Net realized capital (losses) gains, net of tax of $0, for the

years ended December 31, 2013 and 2012 (38,283) 5,220 Net investment gain 13,527 52,215 Other income 23,455 18,956 Income before all other federal and foreign income taxes 2,509,717 1,066,134 Federal and foreign income tax expense (benefit) 910 (325) Net income $ 2,508,807 $ 1,066,459

See accompanying notes.

5

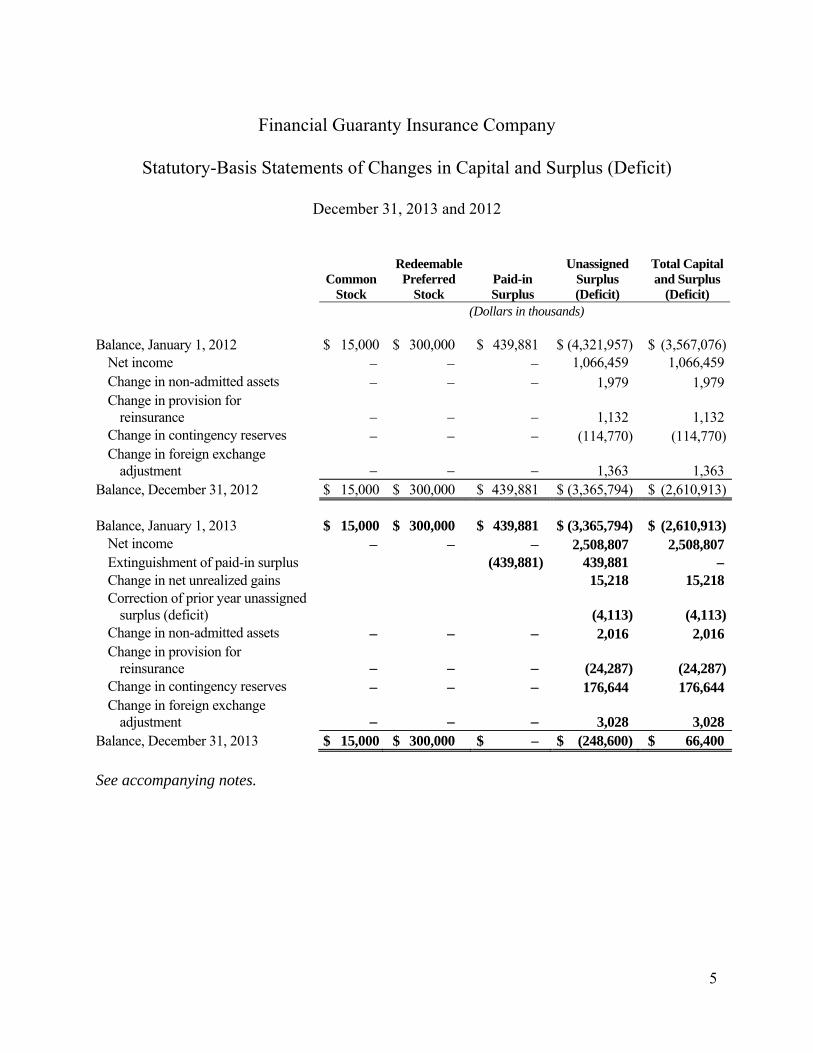

Financial Guaranty Insurance Company

Statutory-Basis Statements of Changes in Capital and Surplus (Deficit)

December 31, 2013 and 2012

Common

Stock

Redeemable Preferred

Stock Paid-in Surplus

Unassigned Surplus (Deficit)

Total Capital and Surplus

(Deficit) (Dollars in thousands) Balance, January 1, 2012 $ 15,000 $ 300,000 $ 439,881 $ (4,321,957) $ (3,567,076)

Net income 1,066,459 1,066,459 Change in non-admitted assets 1,979 1,979 Change in provision for

reinsurance 1,132 1,132 Change in contingency reserves (114,770) (114,770)Change in foreign exchange

adjustment 1,363 1,363 Balance, December 31, 2012 $ 15,000 $ 300,000 $ 439,881 $ (3,365,794) $ (2,610,913) Balance, January 1, 2013 $ 15,000 $ 300,000 $ 439,881 $ (3,365,794) $ (2,610,913)

Net income 2,508,807 2,508,807 Extinguishment of paid-in surplus (439,881) 439,881 – Change in net unrealized gains 15,218 15,218 Correction of prior year unassigned

surplus (deficit) (4,113) (4,113)Change in non-admitted assets 2,016 2,016 Change in provision for

reinsurance (24,287) (24,287)Change in contingency reserves 176,644 176,644 Change in foreign exchange

adjustment 3,028 3,028 Balance, December 31, 2013 $ 15,000 $ 300,000 $ – $ (248,600) $ 66,400

See accompanying notes.

6

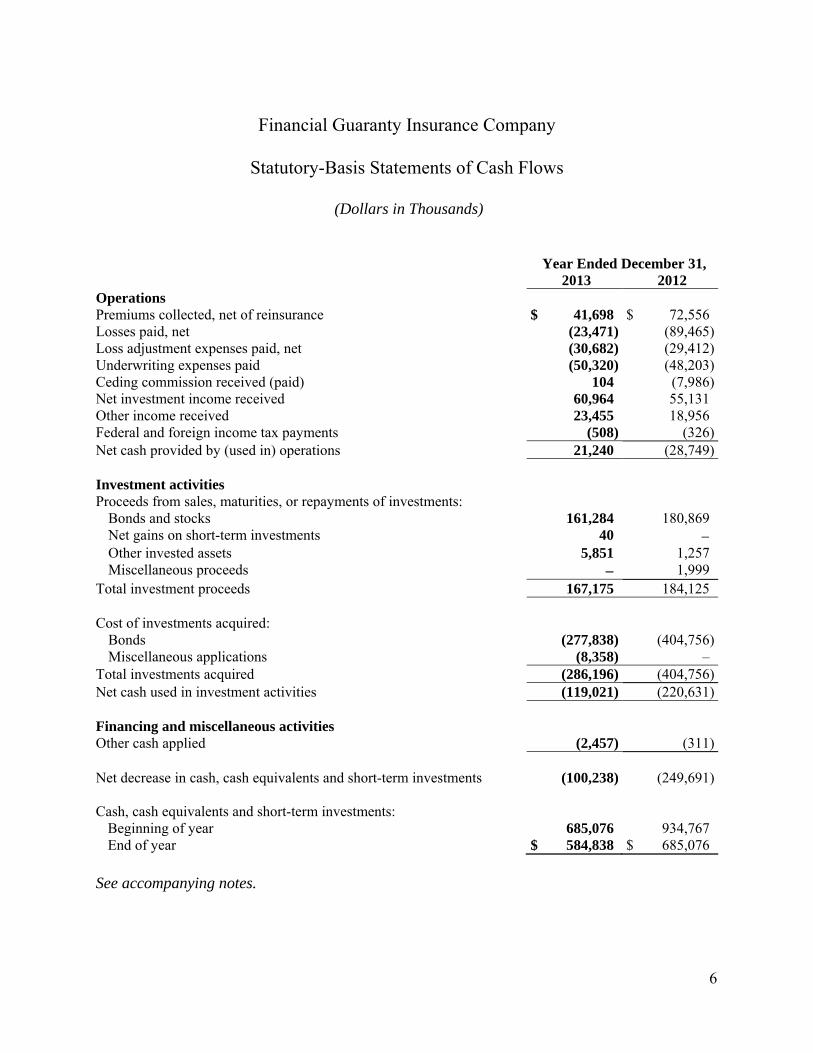

Financial Guaranty Insurance Company

Statutory-Basis Statements of Cash Flows

(Dollars in Thousands)

Year Ended December 31, 2013 2012 Operations Premiums collected, net of reinsurance $ 41,698 $ 72,556 Losses paid, net (23,471) (89,465)Loss adjustment expenses paid, net (30,682) (29,412)Underwriting expenses paid (50,320) (48,203)Ceding commission received (paid) 104 (7,986)Net investment income received 60,964 55,131 Other income received 23,455 18,956 Federal and foreign income tax payments (508) (326)Net cash provided by (used in) operations 21,240 (28,749) Investment activities Proceeds from sales, maturities, or repayments of investments:

Bonds and stocks 161,284 180,869 Net gains on short-term investments 40 Other invested assets 5,851 1,257 Miscellaneous proceeds 1,999

Total investment proceeds 167,175 184,125 Cost of investments acquired:

Bonds (277,838) (404,756)Miscellaneous applications (8,358) –

Total investments acquired (286,196) (404,756)Net cash used in investment activities (119,021) (220,631) Financing and miscellaneous activities Other cash applied (2,457) (311) Net decrease in cash, cash equivalents and short-term investments (100,238) (249,691) Cash, cash equivalents and short-term investments:

Beginning of year 685,076 934,767 End of year $ 584,838 $ 685,076

See accompanying notes.

7

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements

December 31, 2013

1. Organization and Background

Financial Guaranty Insurance Company (the “Company” or “FGIC”), a New York stock insurance corporation, is a wholly owned subsidiary of FGIC Corporation (“FGIC Corp.”), a Delaware corporation. The Company previously issued financial guaranty insurance policies insuring public finance, structured finance and other obligations. The Company is responsible for administering its outstanding policies in accordance with the Rehabilitation Plan (defined below), any NYSDFS Guidelines (defined in Note 2 below) and applicable law. The Company is no longer engaged in the business of writing new insurance policies. The Company’s primary regulator is the New York State Department of Financial Services (the “NYSDFS”), which assumed the functions and authority of the New York State Insurance Department (the “NYSID”). FGIC UK Limited (“FGIC UK”), a wholly owned United Kingdom insurance subsidiary of FGIC, previously issued financial guaranties covering public finance, structured finance and other obligations. FGIC UK, whose primary regulator is the UK Prudential Regulation Authority, is responsible for administering its outstanding guaranties in accordance with the terms and conditions of such guaranties and applicable law. FGIC UK is no longer engaged in the business of writing new financial guaranties.

Based on FGIC’s reported statutory surplus deficit as of September 30, 2009, on November 24, 2009, the NYSID issued an order pursuant to Section 1310 of the New York Insurance Law (the “NYIL”) requiring FGIC, effective that day, to suspend paying any and all claims, to cease writing any new policies and to operate only in the ordinary course of business and as necessary to effectuate its plan to eliminate its policyholders’ surplus deficit (the "1310 Order"). FGIC developed a comprehensive surplus restoration plan that it submitted to the NYSID, but ultimately FGIC was unable to implement that plan. By petition of the Superintendent of Financial Services of the State of New York (the “Superintendent”) based on FGIC’s statutory insolvency and its inability to eliminate its policyholders’ surplus deficit, the Supreme Court of the State of New York (the “Rehabilitation Court”), on June 28, 2012, issued an order pursuant to Article 74 of the NYIL (“Article 74”) placing FGIC in rehabilitation (the “Rehabilitation Order”). On June 11, 2013, the Rehabilitation Court approved the First Amended Plan of Rehabilitation for FGIC, dated June 4, 2013, together with all exhibits and the plan supplement thereto (collectively, the "Rehabilitation Plan"). The Rehabilitation Plan became effective on August 19, 2013 (the "Effective Date"), whereupon FGIC's rehabilitation proceeding terminated, the 1310 Order was lifted and FGIC resumed possession of its property and conduct of its business subject to the limitations described in the Rehabilitation Plan (See Note 2).

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

8

1. Organization and Background (continued)

FGIC Corp. commenced a proceeding under Chapter 11 of the United States Bankruptcy Code on August 3, 2010, and FGIC Corp. emerged from that proceeding on April 19, 2013 (the “Chapter 11 Effective Date”). On the Chapter 11 Effective Date, the transactions contemplated under the Plan of Reorganization for FGIC Corp. were consummated. None of the subsidiaries or affiliates of FGIC Corp., including FGIC, was a debtor in FGIC Corp.’s Chapter 11 case.

2. FGIC Rehabilitation Proceeding

On June 28, 2012, the Rehabilitation Court issued the Rehabilitation Order (i) appointing the Superintendent as rehabilitator of FGIC (the “Rehabilitator”), (ii) directing the Rehabilitator to take possession of the property and assets of FGIC and to conduct the business thereof, and (iii) directing the Rehabilitator to take steps towards the removal of the causes and conditions that made FGIC’s rehabilitation proceeding (the “Rehabilitation Proceeding”) necessary. FGIC consented to the commencement of the Rehabilitation Proceeding and, upon such commencement, the board of directors of FGIC resigned. The Rehabilitation Proceeding was styled as In the Matter of the Rehabilitation of Financial Guaranty Insurance Company, Index No. 401265/2012.

Subsequent to the Rehabilitation Order, and as part of the Rehabilitation Proceeding, the Rehabilitator developed the Rehabilitation Plan. The goal of the Rehabilitation Plan is to treat FGIC’s policyholders in a fair and equitable manner while at the same time removing the causes and conditions that made the Rehabilitation Proceeding necessary.

On June 11, 2013, the Rehabilitation Court issued an order pursuant to Article 74, among other things, (i) approving the Rehabilitation Plan and authorizing its implementation, (ii) approving the forms of amended and restated charter and amended and restated by-laws for FGIC filed as part of the Rehabilitation Plan, which constitute the charter and by-laws for FGIC as of the Effective Date, (iii) approving the Novation Agreement (defined below) and the consummation of the transactions contemplated thereby, (iv) approving an initial cash payment percentage (“CPP”) of 17.25% subject to adjustment by the Rehabilitator in his sole discretion on or before the Effective Date (by notice dated on the Effective Date, the Rehabilitator set the initial CPP at 17.00%), (v) terminating the Rehabilitation Proceeding on the Effective Date without further order of the Rehabilitation Court, and (vi) providing that on the Effective Date, FGIC shall resume possession of its property and conduct of its business subject to the limitations described in the Rehabilitation Plan.

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

9

2. FGIC Rehabilitation Proceeding (continued)

On the Effective Date, FGIC emerged from the Rehabilitation Proceeding as a solvent insurance company under the NYIL and the Rehabilitation Plan became the exclusive means for resolving and paying (i) all policy claims, whenever arising, (ii) all other claims arising during, or relating to, the period prior to the Effective Date and (iii) all equity interests in FGIC in existence as of the date of the Rehabilitation Order (June 28, 2012), in each case other than claims (including policy claims) paid in full by FGIC prior to the date of the Rehabilitation Order. The Rehabilitation Plan designated six categories of claims and equity interests that are covered by the Rehabilitation Plan: secured claims; administrative expense claims; policy claims; non-policy claims; late-filed claims and equity interests. Claims arising during or relating to the period on and after the Effective Date (other than policy claims) are not covered by the Rehabilitation Plan and will be resolved and paid by FGIC in the ordinary course of business. FGIC continues to be subject to oversight by the NYSDFS pursuant to the NYIL and the additional requirements set forth in the Rehabilitation Plan (including any guidelines the NYSDFS has or may issue to carry out the purposes and effects of the Rehabilitation Plan (“NYSDFS Guidelines”)).

As of the Effective Date, any and all policies in force as of the Effective Date (except for the policies novated by the Novation Agreement (defined below)) were automatically modified by the Rehabilitation Plan. The Rehabilitation Plan, including the restructured policy terms attached to the Rehabilitation Plan as Exhibit B (the “Restructured Policy Terms”), supersedes any and all provisions of each policy that are inconsistent with the Rehabilitation Plan. FGIC is responsible for administering, reviewing, verifying, reconciling, objecting to, compromising or otherwise resolving all claims (including policy claims) not resolved prior to the Effective Date, in each case in compliance with the Rehabilitation Plan and any applicable NYSDFS Guidelines.

With respect to any policy claim permitted by FGIC, pursuant to the Rehabilitation Plan and the applicable policy (as modified by the Rehabilitation Plan), FGIC shall be obligated to pay in cash to the applicable policy payee only an upfront amount equal to the product of the then-existing CPP and the amount of such permitted policy claim. The portion of such permitted policy claim not paid or deemed to be paid by FGIC generally will comprise a deferred payment obligation (“DPO”) with respect to the applicable policy. The DPO with respect to any policy generally represents the aggregate amount of all permitted policy claims under such policy minus the aggregate amount paid, or deemed to be paid, in cash by FGIC with respect to such policy (other than DPO Accretion, defined below) from and after the Effective Date, subject to further adjustments as provided in the Rehabilitation Plan. From and after the Effective Date, each

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

10

2. FGIC Rehabilitation Proceeding (continued)

policy with an outstanding DPO accrues an amount (“DPO Accretion”) based on such DPO (using the balance then applicable pursuant to the Rehabilitation Plan) at a rate of 3% per annum on a daily basis on the basis of a 365-day year. All DPO Accretion shall be calculated on a simple basis, and no DPO Accretion shall be added to the amount of any DPO. The DPO for any policy and any related DPO Accretion shall only be payable by FGIC when, if and to the extent provided in the Restructured Policy Terms and the Rehabilitation Plan. In the absence of an upward adjustment of the CPP, FGIC shall have no obligation to pay any portion of any DPO or DPO Accretion.

The Rehabilitator set the initial CPP at 17.00%. FGIC is required to re-evaluate the CPP (at least annually) pursuant to the procedures set forth in the Restructured Policy Terms to determine whether the CPP should remain the same or be adjusted upward or downward (each, a “CPP Revaluation”). All CPP Revaluations shall require review and approval by the board of directors of FGIC, and any change in the CPP (among other things) shall require the approval of the NYSDFS.

In January 2014, FGIC made its first payments in cash totaling $255.5 million to policyholders for permitted policy claims related to the period from the 1310 Order through the Effective Date at the then-current CPP of 17.00%. The Company will continue to pay permitted claims in accordance with the Rehabilitation Plan.

The percentage of permitted policy claims that FGIC ultimately pays in cash in accordance with the Rehabilitation Plan, and the timing of any such payments, are subject to various factors and the outcome of future events, including the performance of FGIC’s insured and investment portfolios and the results of FGIC’s litigation and other loss mitigation efforts, and no assurance can be given with respect to the amount of any such percentage or the timing of any such payments. Based on the magnitude of FGIC’s accrued and projected policy claims, while the CPP may increase over time, FGIC expects to make payments in cash pursuant to the Rehabilitation Plan of only a fractional portion of its permitted policy claims and it does not expect to make any payments pursuant to the Rehabilitation Plan with respect to non-policy claims or equity interests.

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

11

2. FGIC Rehabilitation Proceeding (continued)

In an effort to mitigate its liabilities and increase recoveries for policyholders, as part of the Rehabilitation Plan, FGIC entered into a Novation Agreement dated as of September 14, 2012 (the “Novation Agreement”) with National Public Finance Guarantee Corporation (“National Public”), pursuant to which the parties agreed, subject to approval of the Rehabilitation Court and the other terms of such agreement, to novate the National Public Reinsured Policies (as defined below) from FGIC to National Public. Pursuant to a Reinsurance Agreement dated as of September 30, 2008, National Public provided FGIC with reinsurance on FGIC policies covering U.S. public finance credits with total net par in force of approximately $92.6 billion as of the Effective Date (collectively, the “National Public Reinsured Policies"). On June 11, 2013, the Novation Agreement was approved by the Rehabilitation Court. The novation of the National Public Reinsured Policies and the other transactions contemplated by the Novation Agreement became effective on the Effective Date, whereupon (i) National Public (rather than FGIC) became the issuer of the National Public Reinsured Policies and became directly responsible for all obligations under the National Public Reinsured Policies and (ii) FGIC was released from all obligations under the National Public Reinsured Policies.

In a further effort to mitigate its liabilities and increase recoveries for policyholders, FGIC entered into agreements (the “CDS Commutation Agreements”) with all counterparties to credit default swaps (“CDS”) insured by FGIC whose CDS had not previously been terminated (as well as Société Générale, whose CDS had been terminated but which termination was at that time the subject of litigation between FGIC and Société Générale) (collectively, the “CDS Counterparties”), pursuant to which the CDS Counterparties and FGIC agreed, subject to approval by the Rehabilitation Court and the other terms of such agreements, to terminate all of the CDS Counterparties’ FGIC-insured CDS and the related FGIC policies, and to mutually release all related obligations, claims and liabilities, in exchange for payments by FGIC aggregating approximately $176.4 million. On December 19, 2012, the Rehabilitation Court approved the CDS Commutation Agreements and FGIC made such payments, whereupon the CDS and the related FGIC policies were terminated and FGIC and the CDS Counterparties were released from all obligations, claims and liabilities thereunder or relating thereto.

References to and descriptions of provisions of the Rehabilitation Plan (and related agreements) and orders of the Rehabilitation Court included in these financial statements are merely summaries thereof, and do not contain all information necessary to fully understand such provisions and orders. Please refer to the specific terms, requirements and conditions of the Rehabilitation Plan (and related agreements) and orders of the Rehabilitation Court for a full understanding thereof, which in all cases shall govern, rather than any summary description contained in these financial statements.

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

12

3. Assessment of the Company’s Ability to Continue as a Going Concern

As a result of uncertainties associated with the Rehabilitation Plan prior to the Effective Date, including the risk that the Rehabilitator at any time prior to the Effective Date may have determined that efforts to rehabilitate the Company would be futile and may have sought to convert the Rehabilitation Proceeding into a liquidation proceeding under Article 74, management concluded that there was substantial doubt about the ability of the Company to continue as a going concern. On the Effective Date, FGIC emerged from the Rehabilitation Proceeding as a solvent company with its policies restructured in a manner intended to ensure that it remains solvent. As a result, these uncertainties about the ability of the Company to continue as a going concern were removed. The Company’s financial statements as of and for the years ended December 31, 2013 and 2012 were prepared assuming the Company continues as a going concern and did not include any adjustment that might have resulted from its inability to continue as a going concern as described above.

4. Significant Accounting Policies

The accompanying financial statements of the Company have been prepared in conformity with statutory accounting practices prescribed or permitted by the NYSDFS as well as those accounting practices detailed in NYSDFS Guidelines, as described below (“SAP”). The preparation of financial statements in conformity with SAP requires management to make estimates and assumptions that affect the amounts reported in the financial statements and the accompanying notes. Actual results could differ from those estimates, and those differences could be material.

SAP differs in some respects from accounting principles generally accepted in the United States (“GAAP”). The effects of the variances from GAAP on the accompanying statutory-basis financial statements have not been determined for the years ended December 31, 2013 and 2012, but are presumed to be material. Significant accounting policies and variances from GAAP, where applicable, are as follows:

Pursuant to the provisions of the Rehabilitation Plan, the NYSDFS has issued NYSDFS Guidelines that define certain accounting practices for FGIC for reporting periods ending on or after the Effective Date. In accordance with such NYSDFS Guidelines, for reporting periods ending on or after the Effective Date, FGIC will record loss reserves at the applicable reporting date in an amount equal to the excess of (i) the amount of FGIC’s admitted assets minus FGIC’s

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

13

4. Significant Accounting Policies (continued)

minimum required statutory surplus to policyholders at the reporting date (the “Minimum Surplus Amount,” currently $66.4 million) over (ii) the sum of FGIC’s statutory reserves excluding loss reserves (e.g., unearned premiums, contingency reserves, loss adjustment expense reserves) and other liabilities. In accordance with such NYSDFS Guidelines, the loss reserve amount comprises the total amount of (i) the sum, net of reinsurance, of (x) the total amount of all policy claims submitted to FGIC in accordance with the Rehabilitation Plan that are unpaid (excluding any portions of such policy claims that are being disputed by FGIC) and (y) the net present value of the total amount of all policy claims that the Company expects to receive in the future in accordance with the Rehabilitation Plan (using the prescribed statutory discount rate which is based on the average rate of return on FGIC’s admitted assets) (such sum is referred to as the “Claims Reserve”), (ii) the DPO for all policies at such reporting date and (iii) the DPO Accretion for all policies at such reporting date, minus an adjustment (the “Policy Revision Adjustment”) in an amount that will permit FGIC to report a surplus to policyholders at such reporting date equal to the Minimum Surplus Amount (See Note 10, Loss Reserves – December 31, 2013).

As of the Effective Date, FGIC extinguished its paid-in surplus of $439.9 million through a transfer to unassigned deficit.

Investments

Investments in bonds and common stock are valued in accordance with the requirements of the National Association of Insurance Commissioners (“NAIC”).

Bonds are generally stated at amortized cost, with premiums and discounts amortized to net income using the effective interest method over the remaining term of the securities. Bonds with NAIC ratings of 3 or lower are carried at the lower of amortized cost or fair value as determined by the Securities Valuation Office. Under GAAP, bonds are designated at purchase as either held-to-maturity or available-for-sale. Held-to-maturity bonds are reported at amortized cost and bonds designated as available-for-sale are reported at fair value with unrealized gains and losses reported in stockholders equity, net of tax.

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

14

4. Significant Accounting Policies (continued)

Under SAP, investments in wholly owned subsidiaries are recorded based on the underlying equity adjusted to a statutory basis and reported as common stock investments, not to exceed 50% of the Company’s statutory surplus or 60% of surplus to shareholders, whichever is higher. Changes in the value of subsidiaries are recorded as unrealized gains and losses and reported as a component of unassigned surplus. Under SAP, the reporting entity can discontinue applying the equity method when the investment in a subsidiary is reduced to zero, and SAP does not provide for additional losses unless the reporting entity has guaranteed obligations of the investee or is otherwise committed to provide further financial support for the investee. Under GAAP, subsidiaries are consolidated with the Company.

Short-term investments, including Class 1 NAIC money market securities, are stated at amortized cost, which approximates fair value. Realized gains and losses on the sale of investments are determined based on the specific identification method.

All single class and multi-class mortgage-backed/asset-backed securities are valued at amortized cost using the interest method, including anticipated prepayments. Prepayment assumptions are obtained from dealer surveys or internal estimates and are based on the current interest rate and economic environment. All such securities are adjusted for the effects of changes in prepayment assumptions on the related accretion of discount or amortization of premium of such securities using the retrospective method.

Investments (excluding investments in wholly owned subsidiaries) that are determined to be other-than-temporarily impaired are reduced to realizable value, establishing a new cost basis, with a charge to realized loss at such date. The Company has determined that it either has the intent to sell or it is more likely than not that it will be required to sell its bonds before recovery of their amortized cost basis. Therefore, all unrealized losses are recorded through earnings and the new cost basis is not adjusted for subsequent recoveries in fair value.

Fair Value Measurements

The Company discloses the fair value of its investments in bonds, other invested assets, short-term investments and other financial instruments in accordance with Statement of Statutory Accounting Principles (“SSAP”) 100, Fair Value Measurements (“SSAP 100”), which requires the use of a fair value hierarchy with the highest priority given to quoted prices in active markets. The general disclosure requirements are for those items measured and reported at fair value in

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

15

4. Significant Accounting Policies (continued)

the balance sheet. Securities that are reported at amortized cost, but for which amortized cost equals fair value (such as a bond with a recognized other-than-temporary impairment on the reporting date) would not be included in the disclosures. SSAP 100 also requires certain disclosures of fair value measurements and valuation techniques, where practicable to determine, for financial instruments not carried at fair value in the balance sheet. SSAP 100 does not require companies to distinguish between recurring and non-recurring fair value measurements, which is required under GAAP.

Cash and Cash Equivalents

The Company considers all bank deposits and all certificates of deposit with maturities of three months or less at the date of purchase to be cash equivalents. Cash equivalents are carried at cost, which approximates fair value. In the event that a highly liquid security is determined to be impaired, the security is adjusted to fair value in accordance with NAIC regulations. Under GAAP, these securities are adjusted to fair value and included in cash and cash equivalents.

Other Invested Assets

Other invested assets are comprised of FGIC-insured residential mortgage-backed securities (“RMBS”) that were purchased by FGIC as part of its loss mitigation efforts. Under SAP, these securities are carried at the lower of amortized cost or fair value as these are rated NAIC 3 or below. Under GAAP, these securities are carried at fair value.

Premium Revenue Recognition

For SAP, premiums collected in a single payment at policy inception are earned in proportion to the scheduled principal and interest payments over the legal lives of the insured bonds. Premiums collected periodically are reflected in income pro rata over the period covered by the premium payment. Under GAAP, premiums are earned in proportion to the amount of insurance protection provided over the expected life for homogeneous pools and over the legal life for non-homogeneous pools of policies. The liability for unearned premiums is reflected net of reinsurance. Ceded premiums are earned in a manner consistent with the underlying policies. Under GAAP, ceded unearned premiums are reported as an asset. When an obligation insured by the Company is refunded prior to the end of the expected policy coverage period, any remaining

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

16

4. Significant Accounting Policies (continued)

unearned premium is recognized at that time. A refunding occurs when an insured obligation is legally defeased or retired prior to stated maturity. Net premiums earned on refundings were $52.5 million and $20.2 million for the years ended December 31, 2013 and 2012, respectively.

Non-admitted Assets

Certain assets are charged directly against surplus, but are reflected as assets under GAAP. Such assets principally include prepaid expenses, property and equipment, and adjusted gross deferred tax assets. The Company recorded non-admitted assets of $0.5 million and $2.5 million at December 31, 2013 and 2012, respectively.

Ceded Balances Payable

Reinsurance receivables are netted against ceded balances payable on the statutory-basis balance sheets. Under GAAP, reinsurance receivables are classified as an asset.

Loss Adjustment Expense Reserve

A reserve for loss adjustment expense is recorded as a liability on the balance sheet. The loss adjustment expense reserve represents management’s best estimate of the ultimate future net cost, determined using internally developed estimates, of the efforts involved in managing and mitigating existing and future policy claims. Such loss adjustment expense reserve is not subject to a Policy Revision Adjustment. The Company’s loss adjustment expense reserve is disclosed as part of Note 12.

Contingency Reserves

Contingency reserves are computed on the basis of statutory requirements for the security of all policyholders, regardless of whether loss contingencies actually exist. The Company establishes contingency reserves in accordance with the NYIL, which is consistent with the requirements of SSAP 60, Financial Guaranty Insurance. Changes in the contingency reserve are charged directly to surplus. Under GAAP, contingency reserves are not required.

During 2013, the Company applied to the NYSDFS to adjust its contingency reserves to reflect changes in its exposure and was granted permission to decrease contingency reserves by $277.5 million.

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

17

4. Significant Accounting Policies (continued)

Federal Income Taxes

Deferred tax assets and liabilities are recognized to reflect the tax impact attributable to temporary differences between the financial statement carrying amounts of assets and liabilities and their respective tax bases.

Deferred tax assets and liabilities are measured using statutory tax rates expected to apply to taxable income in the years in which temporary differences are expected to be recovered or settled and are recorded as a component of surplus. Under SAP and GAAP, a valuation allowance is established for deferred tax assets that are not expected to be realized. Under SAP, a net deferred tax asset is subject to limitations and may be non-admitted.

The Company recognizes accrued interest and penalties related to unrecognized tax benefits where the ultimate recognition is uncertain.

Reinsurance

A liability is recorded for uncollateralized amounts due from unauthorized reinsurers. Changes in this liability are charged or credited directly to unassigned surplus. Amounts due from unauthorized reinsurers that are secured by letters of credit or trust agreements are not included in this liability. Under GAAP, an allowance for amounts deemed uncollectible would be established through a charge to earnings.

Ceded loss reserves are calculated as reductions of the related reserves rather than assets, as would be required under GAAP. Prospective losses are accounted for on a basis consistent with that used in accounting for the original policies issued, the terms of the reinsurance contracts, and the terms of the Rehabilitation Plan, which provides that payments are due in full from reinsurers with respect to any permitted policy claims covered by the reinsurance without regard to (i) the timing or amount of any cash payment made by FGIC on the underlying claims, (ii) the modification pursuant to the Rehabilitation Plan of FGIC’s obligations to pay such Permitted Claims in cash or (iii) any language in the applicable reinsurance agreements that would contradict this result. The net loss reserve amount is reduced to give effect to such reinsurance.

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

18

4. Significant Accounting Policies (continued)

Ceded loss adjustment expense reserves and unearned premiums ceded to reinsurers have been reported as reductions of the related reserves rather than as assets, as would be required under GAAP. Prospective reinsurance premiums and loss adjustment expenses are accounted for on bases consistent with those used in accounting for the original policies issued and the terms of the reinsurance contracts.

Consolidation

The accounts and operations of the Company’s subsidiaries are not consolidated with the accounts and operations of the Company, as would be required under GAAP.

As part of its structured finance business, the Company insures debt obligations or certificates issued by special purpose entities. Under SAP, the Company does not consolidate the assets and liabilities of a variable interest entity (“VIE”). Under GAAP, the Company is required to consolidate the assets and liabilities of a VIE if the Company is determined to be the primary beneficiary because it directs the significant activities of and holds an economic interest in the entity.

Foreign Currency Translation

The Company has foreign branches in the United Kingdom and France. The Company has determined that these are foreign operations with transactions in their respective local currencies, which are their functional currencies. Accordingly, the assets and liabilities of these foreign branches are translated into U.S. dollars at the rates of exchange existing at the balance sheet date, and the associated revenues and expenses are translated into U.S. dollars at the weighted average exchange rate for the period. These foreign exchange gains (losses) are recorded as unrealized capital gains and losses within capital and surplus (deficit) under SAP and as other comprehensive income under GAAP.

Statements of Cash Flow

The statutory-basis statements of cash flow are presented in a specified format, which differs from the format prescribed under GAAP. Cash, cash equivalents, and short-term investments in the statements of cash flow represent cash balances and investments with initial maturities of one year or less. Under GAAP, the corresponding caption of cash and cash equivalents includes cash balances and investments with initial maturities of three months or less.

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

19

4. Significant Accounting Policies (continued)

Comprehensive Income

Comprehensive income is not determined under SAP.

Property and Equipment

Property and equipment consists of office furniture, fixtures, computer equipment and software that are reported at cost less accumulated depreciation for GAAP reporting. Under SAP, these assets are non-admitted.

Reclassifications

Certain 2012 amounts in the Company’s statutory-basis financial statements have been reclassified to conform to the 2013 statutory-basis financial statement presentation.

Correction to Prior Year Unassigned Surplus (Deficit)

The Company’s January 1, 2013 surplus balance has been reduced by $4.1 million to reflect the correction of an error in prior reporting periods in the recording of impairments on loan-backed securities. These securities were impaired in earlier years, but the recovery of a portion of the impairment was erroneously recorded in prior years.

5. Financial Guaranty Contracts

The expected future premiums shown below are based on various prepayment, collection and other assumptions and circumstances as of December 31, 2013, and actual premiums collected could differ materially. In addition, the expected future premiums shown below do not give effect to policy terminations that have occurred after, or may occur after, December 31, 2013, which could materially reduce the actual premiums collected.

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

20

5. Financial Guaranty Contracts (continued)

The following is a roll-forward of the undiscounted expected future premiums for the years ended December 31, 2013 and 2012:

Year Ended December 31, 2013 2012 (In Thousands) Beginning expected future premiums $ 318,548 $ 404,309 Premium payments received (34,022) (47,855) Adjustments for changes in expected premiums, including

impact of terminations and FX movement

(93,482)

(37,906) Ending expected future premiums $ 191,044 $ 318,548

The following is a schedule of undiscounted premiums expected to be collected on financial guaranty contracts as of December 31, 2013:

Undiscounted Premiums

Expected to be Collected

(In Thousands)Quarter ended March 31, 2014 $ 4,326 June 30, 2014 4,896 September 30, 2014 4,946 December 31, 2014 4,939 Total 2014 19,107 Year ended December 31, 2015 18,124 December 31, 2016 15,307 December 31, 2017 13,383 December 31, 2018 11,074 Five years ended December 31, 2023 43,359 December 31, 2028 30,098 December 31, 2033 23,191 December 31, 2038 11,359 December 31, 2043 4,767 December 31, 2048 1,275

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

21

5. Financial Guaranty Contracts (continued)

The following table presents the expected unearned premiums and the expected future premium earnings on non-installment policies as of and for the periods presented:

Expected Future Premium Earnings

Total Expected Future

Unearned Premiums Upfront

Other Non – Installment

Premium Earnings

In thousands December 31, 2013 $ 122,546 $ – $ – $ – Quarter ended March 31, 2014 120,256 1,157 1,133 2,290 June 30, 2014 118,545 781 930 1,711 September 30, 2014 115,142 2,564 839 3,403 December 31, 2014 113,605 861 676 1,537 Year ended December 31, 2015 106,247 5,797 1,561 7,358 December 31, 2016 99,717 5,416 1,114 6,530 December 31, 2017 94,280 4,970 467 5,437 December 31, 2018 88,327 5,632 321 5,953 Five years ended December 31, 2023 58,041 28,711 1,575 30,286 December 31, 2028 42,026 14,917 1,098 16,015 December 31, 2033 20,189 21,337 500 21,837 December 31, 2038 6,928 12,761 500 13,261 December 31, 2043 2,610 4,294 24 4,318 December 31, 2048 4 2,606 2,606 December 31, 2053 4 4

The remaining amount of unearned premiums that would have been recorded if all premiums had been received at inception amounted to $129.5 million as of December 31, 2013.

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

22

6. Fair Value Measurements

SSAP 100 specifies a fair value hierarchy based on whether the inputs to valuation techniques used to measure fair value are observable or unobservable. Observable inputs reflect market data obtained from independent sources, while unobservable inputs reflect the Company’s assumptions about market participants’ assumptions based on the best information available in the circumstances. The fair value hierarchy prioritizes model inputs into three broad levels: quoted prices for identical instruments in active markets are Level 1 inputs; quoted prices for similar instruments in active markets, quoted prices for identical or similar instruments in markets that are not active, and model-derived valuations in which all significant inputs and significant value drivers are observable in active markets are Level 2 inputs; and model-driven valuations in which one or more significant inputs or significant value drivers are unobservable are Level 3 inputs.

The Company did not report any securities at fair value on the balance sheets as of December 31, 2013 and 2012.

Transfers among levels 1, 2 and 3 are recognized at the end of the period when the transfer occurs. The Company reviews the classification of financial instruments in levels 1, 2 and 3 quarterly to determine whether a transfer is necessary.

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

23

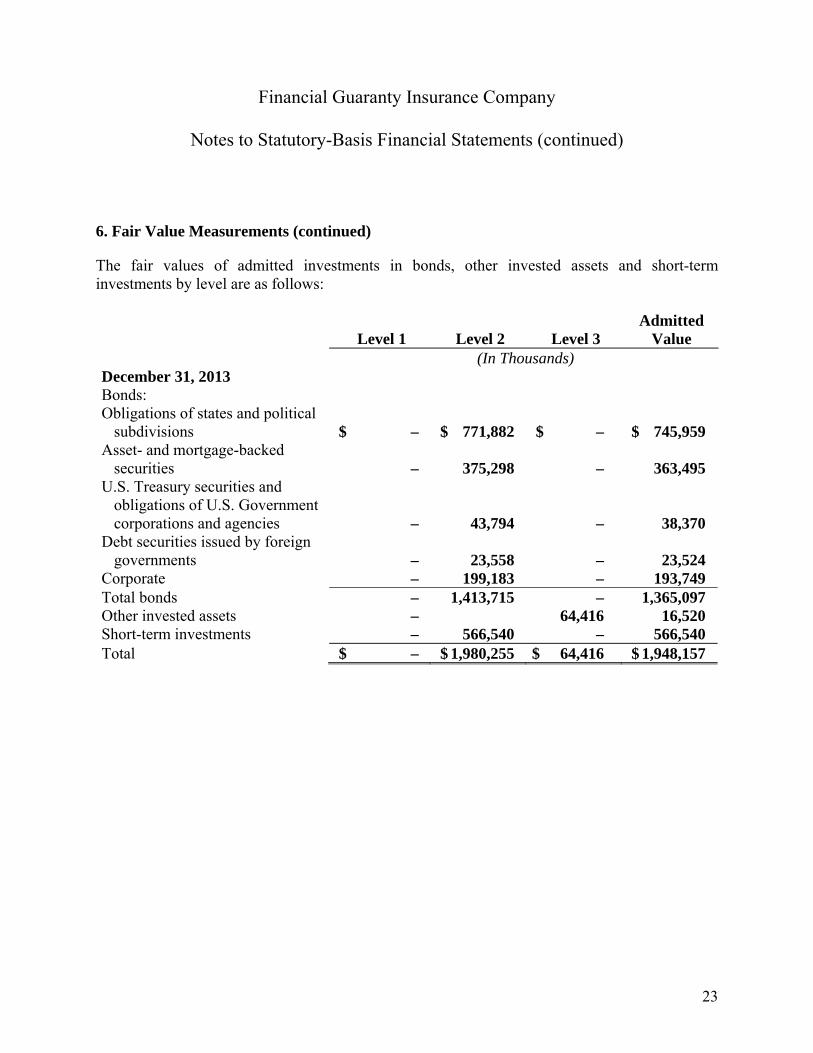

6. Fair Value Measurements (continued)

The fair values of admitted investments in bonds, other invested assets and short-term investments by level are as follows:

Level 1 Level 2 Level 3 Admitted

Value (In Thousands) December 31, 2013 Bonds: Obligations of states and political

subdivisions $ – $ 771,882 $ – $ 745,959 Asset- and mortgage-backed

securities – 375,298 – 363,495 U.S. Treasury securities and

obligations of U.S. Government corporations and agencies – 43,794 – 38,370

Debt securities issued by foreign governments – 23,558 – 23,524

Corporate – 199,183 – 193,749 Total bonds – 1,413,715 – 1,365,097 Other invested assets – 64,416 16,520 Short-term investments – 566,540 – 566,540 Total $ – $ 1,980,255 $ 64,416 $ 1,948,157

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

24

6. Fair Value Measurements (continued)

Level 1 Level 2 Level 3 Admitted

Value In thousands December 31, 2012 Bonds: Obligations of states and

political subdivisions $ – $ 776,894 $ – $ 723,948 Asset- and mortgage-backed

securities –

383,751

– 359,532

U.S. Treasury securities and obligations of corporations and agencies – 49,109 – 38,533

Debt securities issued by foreign governments – 32,427 – 31,899

Corporate – 152,279 – 142,139 Total bonds – 1,394,460 – 1,296,051 Other invested assets – – 55,922 22,371 Short-term investments – 676,681 – 676,681 Total $ – $ 2,071,141 $ 55,922 $ 1,995,103

There have been no transfers in and out of Level 3 during the period.

(a) Fair Value of Financial Instruments

The following methods and assumptions were used by the Company in estimating fair values of financial instruments. Fair values estimated based upon internal valuation models are not necessarily indicative of the amount the Company could realize in a current market exchange.

Bonds: Fair values for bonds are based on quoted market prices, if available. If a quoted market price is not available, fair value is estimated using quoted market prices for similar securities. Because many bonds do not trade on a daily basis, information and other data, including benchmark curves, benchmarking of like securities and matrix pricing, are utilized to value the securities. Inputs to the valuation process include benchmark yields, reported trades, broker/dealer quotes, issuer spreads, two-sided markets, benchmark securities, bids, offers and other reference data. Any investments in preferred or common stock of unaffiliated entities are valued consistent with the method used to value bonds.

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

25

6. Fair Value Measurements (continued)

Short-Term Investments: Short-term investments are carried at amortized cost, which approximates fair value.

Cash and Cash Equivalents: Cash and cash equivalents are carried at cost, which approximates fair value.

Other Invested Assets: Any of the Company’s investments in bonds that are classified as NAIC rated 3 through 6 are recorded at the lower of amortized cost or fair value as determined by the Securities Valuation Office. Fair value of other invested assets is based on third-party proprietary pricing models. These models consider inputs such as expected cash flows, estimated prepayment speeds and estimated default rates for each security or for similar securities as well as the Company’s financial guaranty to pay the CPP and its own credit rating. Because these significant inputs are not observable, these assets are considered Level 3.

(b) Financial Instruments for which Measurement of Fair Value is Not Practicable

Financial Guaranty Insurance Contracts: The carrying value of financial guaranty insurance contracts includes loss reserves, unearned premiums, premiums receivable and ceded balances payable. Loss reserves have been determined in accordance with the statutory accounting practices prescribed by NYSDFS Guidelines and comprise the total amount of (i) the Claims Reserve, (ii) the DPO for all policies and (iii) the DPO Accretion for all policies, minus the Policy Revision Adjustment.

The fair value of the Company’s financial guaranty insurance contracts accounted for as insurance was not practicable to determine. The Company has not developed or obtained valuation models, and the cost of developing valuation models necessary to make the estimate or of obtaining an independent valuation appears excessive considering that the Company no longer writes insurance contracts but rather is responsible for administering its outstanding guaranties in accordance with the terms and conditions of such guaranties and applicable law. The calculation would be based on management’s estimate of what a similarly rated financial guaranty insurance company would demand to acquire the Company’s in-force book of financial guaranty insurance business. This amount would be based on pricing assumptions management would observe for portfolio transfers that have occurred in the financial guaranty market. It would include adjustments to the carrying value

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

26

6. Fair Value Measurements (continued)

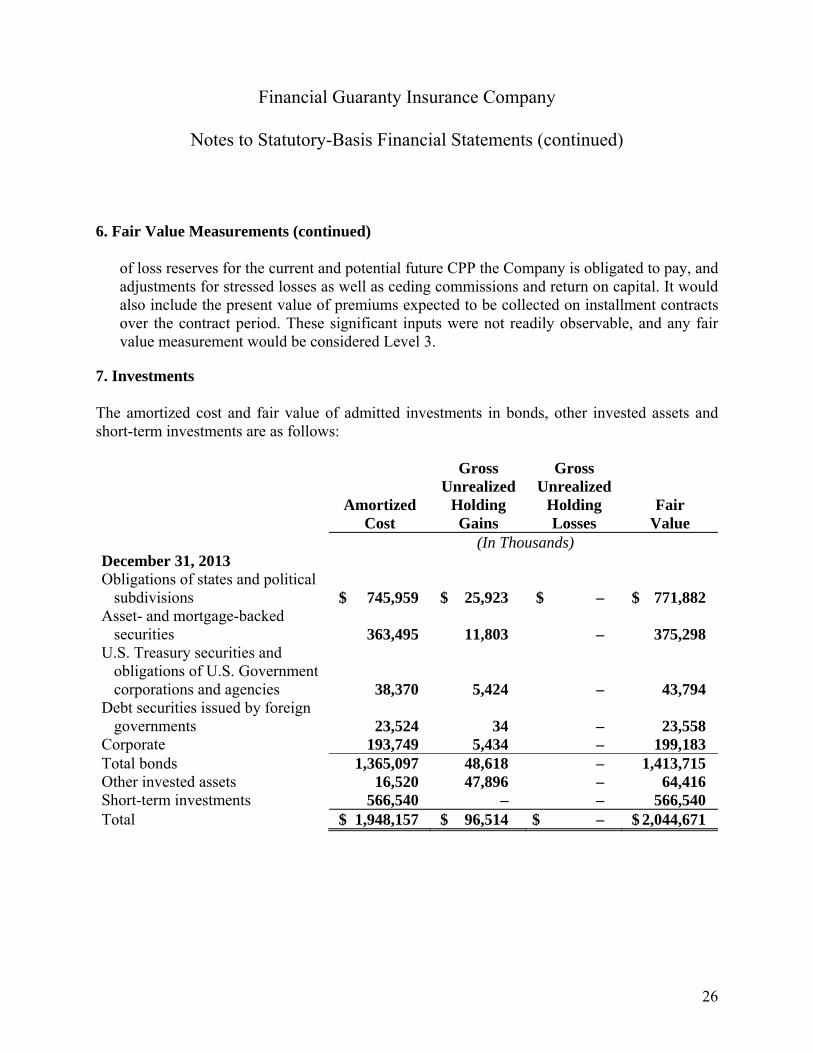

of loss reserves for the current and potential future CPP the Company is obligated to pay, and adjustments for stressed losses as well as ceding commissions and return on capital. It would also include the present value of premiums expected to be collected on installment contracts over the contract period. These significant inputs were not readily observable, and any fair value measurement would be considered Level 3.

7. Investments

The amortized cost and fair value of admitted investments in bonds, other invested assets and short-term investments are as follows:

Amortized

Cost

Gross Unrealized

Holding Gains

Gross Unrealized

Holding Losses

Fair Value

(In Thousands) December 31, 2013 Obligations of states and political

subdivisions $ 745,959 $ 25,923 $ – $ 771,882 Asset- and mortgage-backed

securities 363,495 11,803 – 375,298 U.S. Treasury securities and

obligations of U.S. Government corporations and agencies 38,370 5,424 – 43,794

Debt securities issued by foreign governments 23,524 34 – 23,558

Corporate 193,749 5,434 – 199,183 Total bonds 1,365,097 48,618 – 1,413,715 Other invested assets 16,520 47,896 – 64,416 Short-term investments 566,540 – – 566,540 Total $ 1,948,157 $ 96,514 $ – $ 2,044,671

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

27

7. Investments (continued)

Amortized Cost

Gross Unrealized

Holding Gains

Gross Unrealized

Holding Losses

Fair Value

(In Thousands) December 31, 2012 Obligations of states and political

subdivisions $ 723,948 $ 52,946 $ – $ 776,894 Asset- and mortgage-backed

securities 359,532 24,219 – 383,751 U.S. Treasury securities and

obligations of U.S. Government corporations and agencies 38,533 10,576 – 49,109

Debt securities issued by foreign governments 31,899 528 – 32,427

Corporate 142,139 10,140 – 152,279 Total bonds 1,296,051 98,409 – 1,394,460 Other invested assets 22,371 33,551 – 55,922 Short-term investments 676,681 – – 676,681 Total $ 1,995,103 $ 131,960 $ – $ 2,127,063

The Company has determined either that it does not intend to hold certain fixed income securities until their fair value exceeds their amortized cost or that it intends to sell, or it is more likely than not that the Company will be required to sell, certain fixed income securities before recovery of their amortized cost basis. The Company has recorded other-than-temporary impairment (“OTTI”) of $39.1 million and $1.3 million on its fixed income securities for the years ended December 31, 2013 and 2012, respectively. OTTI is included in “Net realized capital gains or losses net of tax” in the statutory-basis statements of operations and represents the difference between the amortized cost bases of these securities and their fair values at the balance sheet date.

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

28

7. Investments (continued) In accordance with SSAP 43R, the Company is required to categorize its OTTI on loan-backed and structured securities based upon the reason for which the Company recognized an OTTI. The following summarizes those securities held at December 31, 2013 and 2012 for which the OTTI was recorded during the years ended December 31, 2013 and 2012:

Year Ended December 31, 2013 2012 (In Thousands)

Intent to sell $ 11,252

$ 65

Inability to retain the investment in the security for a period of time sufficient to recover the amortized cost basis – –

Present value of the cash flows expected to be collected is less than the amortized cost basis of the security – –

Total OTTI on loan-backed and structured securities $ 11,252 $ 65 The amortized cost and fair value of investments in bonds at December 31, 2013, by contractual maturity date, are shown below. As asset and mortgage-backed securities are generally more likely to be prepaid than other fixed maturity securities, they are shown separately. Expected maturities may differ from contractual maturities because borrowers may have the right to call or prepay obligations with or without call or prepayment penalties.

Amortized

Cost Fair

Value (In Thousands) Due in one year $ 31,589 $ 31,969Due after one through five years 219,300 227,864Due after five years through ten years 273,077 281,360Due after ten years 477,636 497,224Asset- and mortgage-backed securities 363,495 375,298Total $ 1,365,097 $ 1,413,715

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

29

7. Investments (continued)

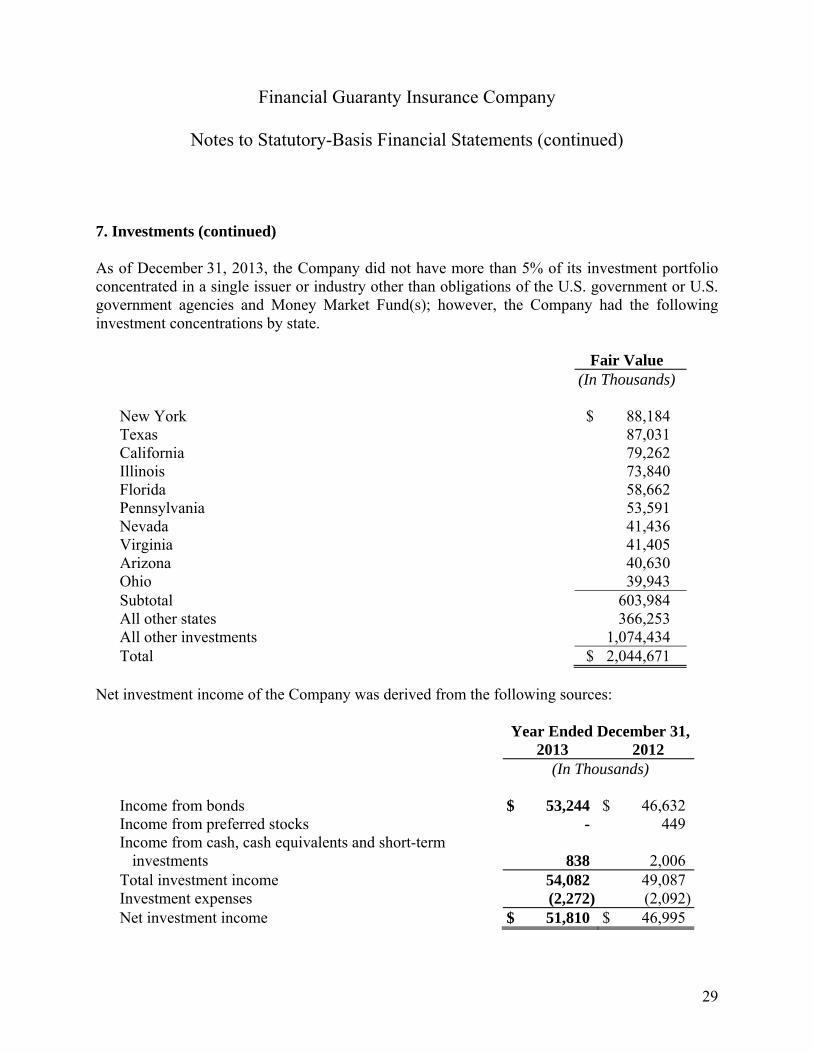

As of December 31, 2013, the Company did not have more than 5% of its investment portfolio concentrated in a single issuer or industry other than obligations of the U.S. government or U.S. government agencies and Money Market Fund(s); however, the Company had the following investment concentrations by state.

Fair Value (In Thousands) New York $ 88,184 Texas 87,031 California 79,262 Illinois 73,840 Florida 58,662 Pennsylvania 53,591 Nevada 41,436 Virginia 41,405 Arizona 40,630 Ohio 39,943 Subtotal 603,984 All other states 366,253 All other investments 1,074,434 Total $ 2,044,671

Net investment income of the Company was derived from the following sources:

Year Ended December 31, 2013 2012 (In Thousands) Income from bonds $ 53,244 $ 46,632 Income from preferred stocks - 449 Income from cash, cash equivalents and short-term

investments

838

2,006 Total investment income 54,082 49,087 Investment expenses (2,272) (2,092)Net investment income $ 51,810 $ 46,995

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

30

7. Investments (continued)

For the years ended December 31, 2013 and 2012, proceeds from sales of investments in bonds carried at amortized cost were $30.4 million and $17.5 million, respectively. For the years ended December 31, 2013 and 2012, gross realized gains of $0.8 million and $0.9 million, respectively, were realized on such sales. For the years ended December 31, 2013 and 2012, gross realized losses of $0 and $0, respectively, were realized on such sales. For the years ended December 31, 2013 and 2012, proceeds from sales of investments in preferred stock were $0 and $9.4 million, respectively. For the year ended December 31, 2012, gross realized gains and gross realized losses of $5.6 million and $0, respectively, were realized on such sales.

Investments in cash, cash equivalents, short-term investments and bonds carried at amortized cost of $25.3 million and $24.2 million as of December 31, 2013 and 2012, respectively, were on deposit with various regulatory authorities.

The carrying values of the Company’s investment in the equity of subsidiaries were $15.2 million and $0 as of December 31, 2013 and 2012, respectively. Included in the change in net unrealized gains or losses for the years ended December 31, 2013 and 2012 were gains of $15.2 million and $0, respectively, related to the change in carrying values of the Company’s investments in subsidiaries.

8. Income Taxes

The Company files a consolidated U.S. federal income tax return with FGIC Corp. The method of allocation between FGIC Corp. and FGIC is determined under an amended and restated income tax allocation agreement approved by the NYSDFS, and is based upon separate return calculations.

The Company has applied to the Internal Revenue Service for a change in accounting method (“CAM”) for the computation of tax basis loss reserves as of January 1, 2013. The CAM was requested to align the Company’s tax basis loss reserves with the Internal Revenue Code by recognizing only those loss reserves in “payment mode,” defined as those policies for which an event of default has already occurred under the terms of the insurance contract. The weight of authority would not support a tax loss reserve deduction for policies where a default or any other event that creates a legal liability under the terms of the insurance contract has not yet occurred (i.e., “non-payment mode” reserves), irrespective of whether such a reserve may be appropriate under the relevant statutory accounting guidance. In such case, there is no actual loss for which a tax deduction is permitted. Under SAP, there has been no change in the Company’s method of calculating the Claims Reserve.

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

31

8. Income Taxes (continued)

The following is a reconciliation of current federal income taxes computed on income before provision for federal and foreign income taxes at the statutory rate and the provision for current federal income taxes.

Year Ended December 31, 2013 2012 (In Thousands) Income tax expense at the statutory rate, computed on

income before provision for federal and foreign income taxes $ 878,401 $ 373,147

Tax effect of: Tax-exempt interest (8,740) (7,562) NOL adjustment for FGIC Corp.’s cancellation of debt 72,171 Change in valuation allowance (941,654) (371,717) Other, net 732 5,807 Expense (benefit) for federal and foreign income taxes $ 910 $ (325)

The composition of total tax expense (benefit) for the years ended December 31, 2013 and 2012 is as follows:

Year Ended December 31, 2013 2012 (In Thousands) Current:

Federal $ – $ – Foreign 910 (325)

Federal and foreign income tax expense (benefit) $ 910 $ (325) There was no change in net deferred income taxes, inclusive of non-admitted assets, for the years ended December 31, 2013 and 2012.

As of December 31, 2013, the Company had a domestic net operating loss (“NOL”) carryforward of $2.0 billion for federal income tax purposes, which will be available (subject to the limitations discussed below) to offset future taxable income. If not used, the NOL will start expiring in 2029 through 2032 depending on the originating year.

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

32

8. Income Taxes (continued)

FGIC’s ability to utilize its NOLs could be limited after an “ownership change” under Section 382 of the Internal Revenue Code (“Section 382”). Section 382 limits the ability of a corporation that experiences an ownership change to utilize its NOLs and certain built-in losses after the ownership change. An ownership change is generally any change in ownership of more than 50 percentage points of a corporation’s stock over a rolling 3-year period. Generally under Section 382, upon an ownership change, the amount of taxable income that a corporation can offset by its “pre-change losses” (which include its NOLs) is restricted to an annual amount equal to the equity value of the corporation immediately prior to the ownership change multiplied by the long-term tax-exempt rate.

Notwithstanding Section 382’s restriction on a corporation’s use of NOLs, Section 382 provides significant relief to a corporation if an ownership change occurs in the context of a Chapter 11 case. Specifically, section 382(l)(5) of the Internal Revenue Code provides that a corporation under the jurisdiction of a court in a Chapter 11 case is not subject to the general limitations imposed by Section 382 if historic stockholders and/or the corporation’s “qualified creditors” own at least 50% of the total value and voting power of the corporation’s stock after the ownership change occurs (the “Section 382(l)(5) Exception”). The ownership change of FGIC Corp. and FGIC that occurred on the Chapter 11 Effective Date when the then existing equity in FGIC Corp. was cancelled and creditors of FGIC Corp. acquired the new equity of reorganized FGIC Corp., as well as the possession of the property and assets of FGIC by the Rehabilitator during the Rehabilitation Proceeding, qualified for the Section 382(l)(5) Exception.

The amount of federal income taxes incurred and available for recoupment in the event of future losses is $0.

In accordance with SSAP 101, Income Taxes, A Replacement of SSAP No. 10R and SSAP No. 10 (“SSAP 101”), the Company evaluates its deferred income tax asset to determine if valuation allowances are required. SSAP 101 requires that companies assess whether valuation allowances should be established based on the consideration of all available evidence using a “more likely than not” standard. In making such judgments, significant weight is given to evidence that can be objectively verified. Management believes it is more likely than not that the amortization of the net unearned premium reserve, collection of future installment premiums on contracts already written, and income from the investment portfolio will not generate sufficient taxable income to realize the entire deferred tax asset that currently exists. Accordingly, a full valuation allowance was established against the Company’s domestic net deferred tax asset of $724.7 million as of December 31, 2013. The Company will continue to analyze the need for a valuation allowance on a quarterly basis.

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

33

8. Income Taxes (continued)

The Company’s tax returns are subject to routine audits by the Internal Revenue Service and other taxing authorities; however, there are currently no audits for any tax periods in progress. Management believes the Company remains subject to income tax examinations for the years 2010, 2011 and 2012.

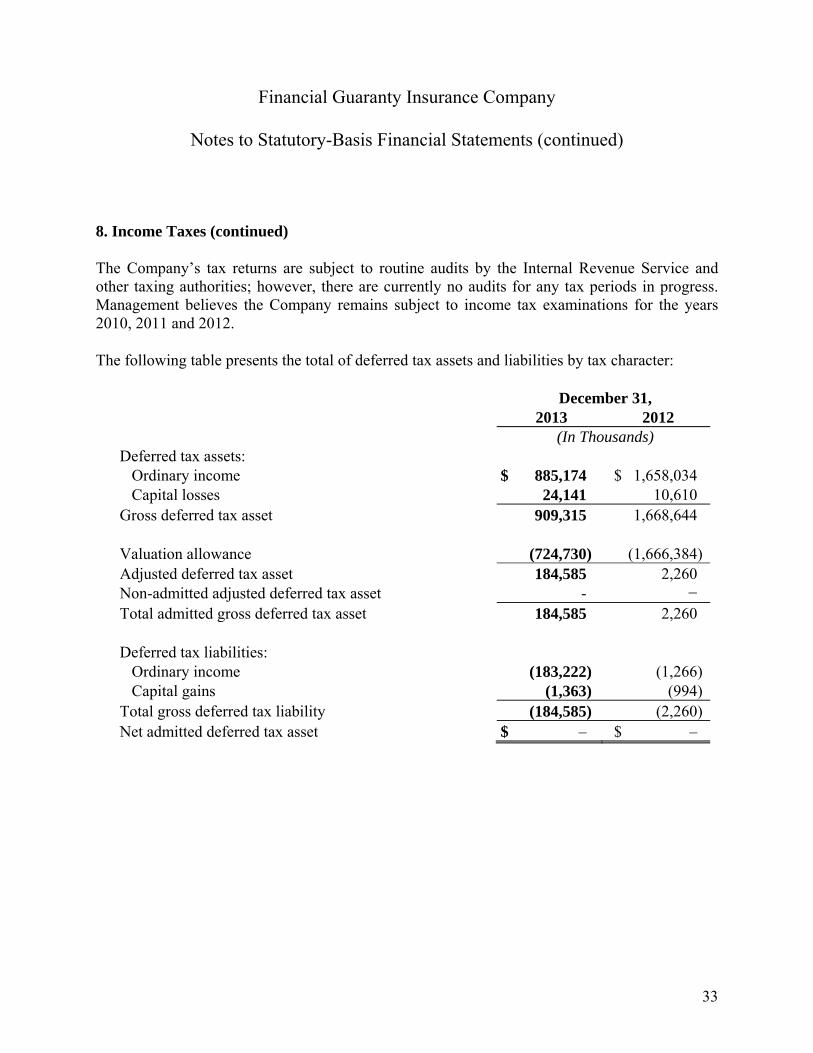

The following table presents the total of deferred tax assets and liabilities by tax character:

December 31, 2013 2012 (In Thousands) Deferred tax assets:

Ordinary income $ 885,174 $ 1,658,034 Capital losses 24,141 10,610

Gross deferred tax asset 909,315 1,668,644 Valuation allowance (724,730) (1,666,384)Adjusted deferred tax asset 184,585 2,260 Non-admitted adjusted deferred tax asset - − Total admitted gross deferred tax asset 184,585 2,260 Deferred tax liabilities:

Ordinary income (183,222) (1,266)Capital gains (1,363) (994)

Total gross deferred tax liability (184,585) (2,260)Net admitted deferred tax asset $ – $ –

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

34

8. Income Taxes (continued)

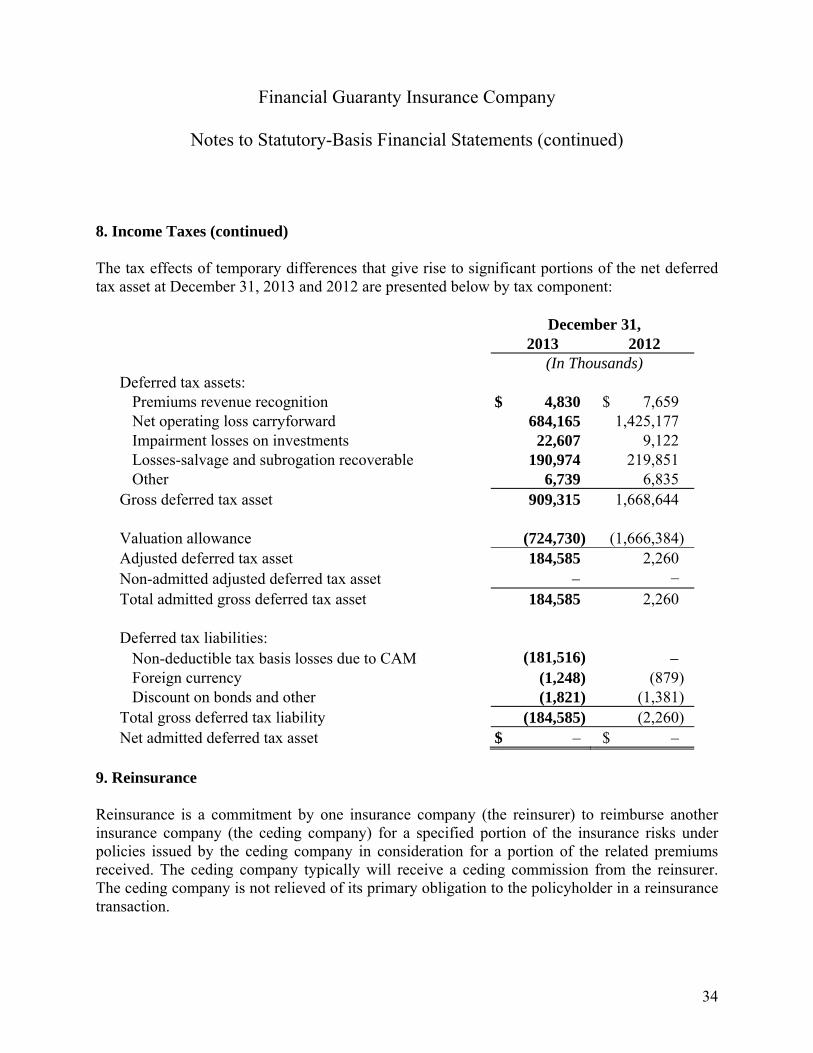

The tax effects of temporary differences that give rise to significant portions of the net deferred tax asset at December 31, 2013 and 2012 are presented below by tax component:

December 31, 2013 2012 (In Thousands) Deferred tax assets:

Premiums revenue recognition $ 4,830 $ 7,659 Net operating loss carryforward 684,165 1,425,177 Impairment losses on investments 22,607 9,122 Losses-salvage and subrogation recoverable 190,974 219,851 Other 6,739 6,835

Gross deferred tax asset 909,315 1,668,644 Valuation allowance (724,730) (1,666,384) Adjusted deferred tax asset 184,585 2,260 Non-admitted adjusted deferred tax asset – Total admitted gross deferred tax asset 184,585 2,260 Deferred tax liabilities:

Non-deductible tax basis losses due to CAM (181,516) Foreign currency (1,248) (879) Discount on bonds and other (1,821) (1,381)

Total gross deferred tax liability (184,585) (2,260) Net admitted deferred tax asset $ – $ –

9. Reinsurance

Reinsurance is a commitment by one insurance company (the reinsurer) to reimburse another insurance company (the ceding company) for a specified portion of the insurance risks under policies issued by the ceding company in consideration for a portion of the related premiums received. The ceding company typically will receive a ceding commission from the reinsurer. The ceding company is not relieved of its primary obligation to the policyholder in a reinsurance transaction.

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

35

9. Reinsurance (continued)

The Company used reinsurance to increase its capacity to write insurance for obligations of large, frequent issuers; to meet internal, rating agency or regulatory single risk limits; to diversify risk; and to manage rating agency and regulatory capital requirements. The Company arranged reinsurance on both a facultative (transaction-by-transaction) basis and on a proportional share basis.

As a primary insurer, the Company is required to fulfill all its obligations to policyholders under its policies (as modified by the Restructured Policy Terms and other Rehabilitation Plan provisions) even where a reinsurer fails to perform its obligations under the applicable reinsurance agreement. The Company regularly monitors the financial condition of its reinsurers. The Company evaluated the financial condition of its reinsurers and recorded a provision for reinsurance of $24.3 million and $1.1 million at December 31, 2013 and 2012, respectively.

Under most of the Company’s reinsurance agreements, the Company has the right to reassume all the exposure ceded to a reinsurer (and receive all the remaining unearned premiums ceded) in the event of a ratings downgrade of the reinsurer or the occurrence of certain other events. In certain of these cases, the Company also has the right to impose additional ceding commissions.

Under certain reinsurance agreements, the Company holds collateral in the form of letters of credit or trust accounts. Such collateral totaled $210.7 million at December 31, 2013 and can be drawn on in the event of default by a reinsurer.

The effects of reinsurance on premiums written and earned are as follows:

Year Ended December 31, 2013 2012 Written Earned Written Earned (In Thousands) Direct premiums $ 38,053 $ 181,728 $ 43,234 $ 188,788 Assumed premiums:

Affiliates (83) (129) 3,479 4,370 Non-affiliates – – – –

Ceded premiums: Affiliates – – – – Non-affiliates 8,599 (85,723) 25,642 (122,250)

Net premiums $ 46,569 $ 95,876 $ 72,355 $ 70,908

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

36

9. Reinsurance (continued)

In January 2013, following approval by the Rehabilitation Court and the satisfaction of all other conditions to closing, Radian Asset Assurance Inc. (“Radian”) paid approximately $52.3 million to FGIC pursuant to a reinsurance commutation agreement entered into by FGIC and Radian in November 2012 (the “Radian Commutation Agreement”), and FGIC reassumed approximately $732.8 million of par exposure and $38.3 million of loss reserves previously ceded to Radian. In accordance with SSAP 62, Property and Casualty Reinsurance (“SSAP 62”), FGIC recognized a net underwriting gain of approximately $3.3 million from the completion of the Radian Commutation Agreement during the year ended December 31, 2013. Also during 2013, FGIC completed several reinsurance commutation agreements with certain other reinsurance companies to settle all obligations between FGIC and the respective reinsurers relating to the subject reinsurance agreements and related reinsurance. Pursuant to these commutation agreements, FGIC received a total of $1.4 million from reinsurers, and FGIC reassumed approximately $52.7 million of par exposure previously ceded to these reinsurers. In accordance with SSAP 62, FGIC recognized an underwriting gain of approximately $0.1 million from the completion of these reinsurance commutation agreements in the year ended December 31, 2013.

In October 2012, FGIC and American Overseas Reinsurance Company Limited, a reinsurance company formerly known as RAM Reinsurance Company (“AORe”), completed a reinsurance commutation agreement (the “AORe Commutation Agreement”) to settle all of their obligations to one another under various reinsurance agreements. Pursuant to the AORe Commutation Agreement, AORe paid $64.8 million to FGIC, and FGIC reassumed approximately $4.3 billion of par exposure previously ceded to AORe. In accordance with SSAP 62, FGIC recognized an underwriting gain of approximately $0.8 million from the completion of the AORe Commutation Agreement in the year ended December 31, 2012.

The amount deducted from unearned premiums for reinsurance ceded to other companies was $10.7 million and $612.2 million at December 31, 2013 and 2012, respectively. The amount of commissions that would be required to be returned by the Company if all reinsurance was canceled was $3.1 million and $124.7 million at December 31, 2013 and 2012, respectively. The amount deducted from loss reserves for reinsurance ceded was $203.6 million and $76.1 million at December 31, 2013 and 2012, respectively. The amount of loss adjustment expenses for reinsurance ceded was $3.2 million and $1.4 million for December 31, 2013 and 2012, respectively.

Amounts payable or recoverable for reinsurance on paid or unpaid losses are not subject to periodic or maximum limits.

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

37

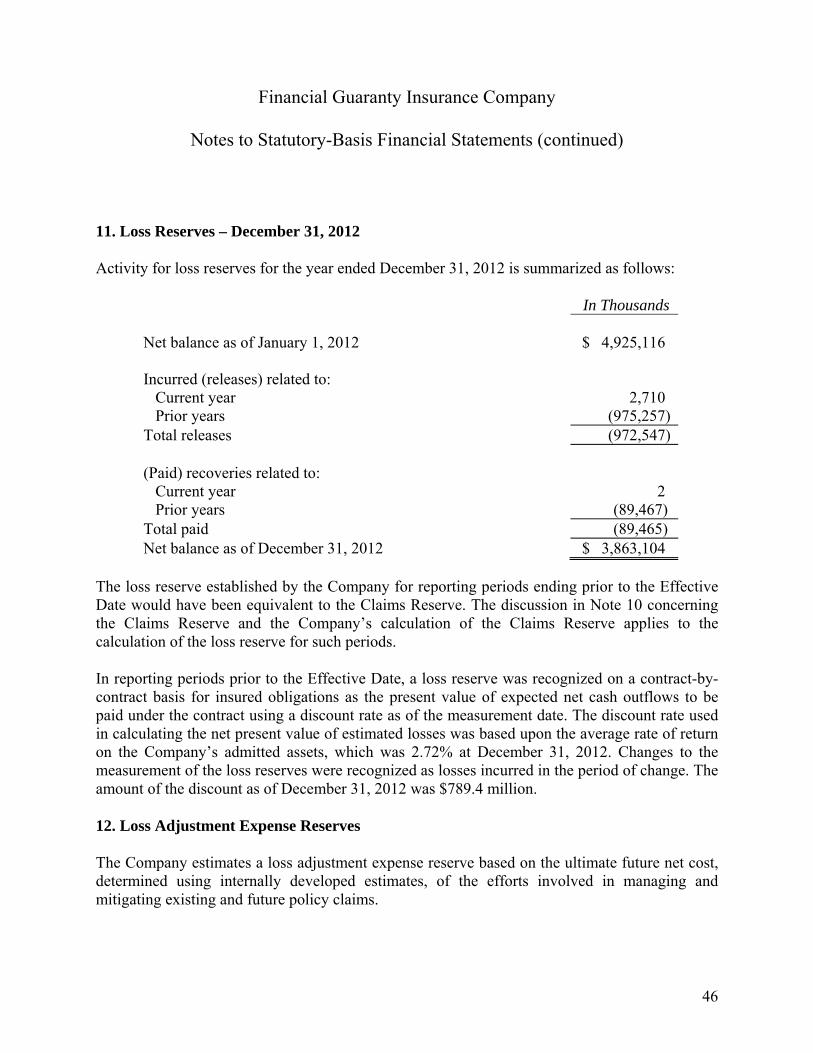

10. Loss Reserves – December 31, 2013

In accordance with NYSDFS Guidelines, FGIC records loss reserves for any reporting period ending on or after the Effective Date in an amount equal to the excess at the applicable reporting date of (i) the amount of FGIC’s admitted assets minus FGIC’s Minimum Surplus Amount (currently $66.4 million) over (ii) the sum of FGIC’s statutory reserves excluding loss reserves (e.g., unearned premiums, contingency reserves, loss adjustment expense reserves) and other liabilities. The loss reserve amount comprises the total amount of (i) the Claims Reserve, (ii) the DPO for all policies and (iii) the DPO Accretion for all policies, minus the Policy Revision Adjustment. The Policy Revision Adjustment shown in the table below is prescribed by NYSDFS Guidelines and reflects the reduction in the loss reserve components necessary to reflect a Minimum Surplus Amount of $66.4 million. Under GAAP, unpaid losses are reported on a gross basis (i.e., before reinsurance), and are discounted based on the risk-free rate for the anticipated shortfall in excess of the related unearned premium revenue, and the Policy Revision Adjustment is not recognized.

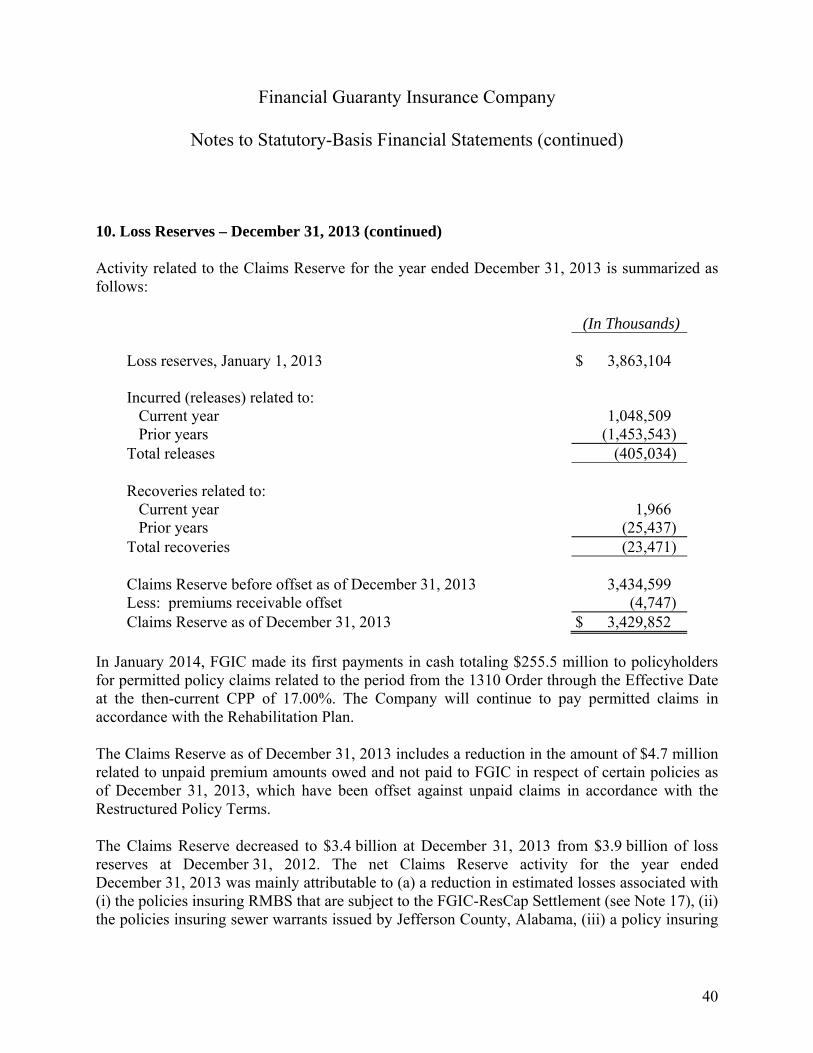

The loss reserve components as of December 31, 2013 are summarized as follows:

(In Thousands) Claims Reserve $ 3,429,852

DPO DPO Accretion Total 3,429,852 Policy Revision Adjustment (2,062,464)

Loss reserve as of December 31, 2013 $ 1,367,388

Financial Guaranty Insurance Company

Notes to Statutory-Basis Financial Statements (continued)

38

10. Loss Reserves – December 31, 2013 (continued)

Claims Reserve

The Claims Reserve is calculated on a policy-by-policy basis for insured obligations as the sum, net of reinsurance, of (x) the total amount of all policy claims submitted to FGIC in accordance with the Rehabilitation Plan that are unpaid as of December 31, 2013 (excluding any portion of such policy claims that are being disputed by FGIC) and (y) the net present value of the total amount of all policy claims the Company expects to receive in the future in accordance with the Rehabilitation Plan determined as of December 31, 2013 (using the prescribed statutory discount rate which is based upon the average rate of return on the Company’s admitted assets, which was 2.92% at December 31, 2013). The amount of the discount as of December 31, 2013 was $960. million. For reporting periods ending prior to the Effective Date, the loss reserve established by the Company would have been equivalent to the Claims Reserve.

Permitted policy claims that are paid by FGIC in accordance with the Rehabilitation Plan are not included in the Claims Reserve; the DPO portion of such claims will, however, be reflected in the DPO balance. No permitted policy claims were paid by FGIC pursuant to the Rehabilitation Plan on or prior to December 31, 2013.

The net present value of the total amount of all policy claims the Company expects to receive in the future is determined for each policy using internally developed cash flow projections or other methods for estimating losses and represents an estimate of the anticipated shortfall between (1) the insured payments of principal and interest due on the insured obligations and (2) the insured payments of principal and interest due on the insured obligations that are anticipated to be made by the issuer or other obligor of the insured obligations, including payments from the projected cash flows from, and proceeds to be received on, any collateral or other security supporting the insured obligation and/or other anticipated recoveries and/or premiums expected to be earned and/or collected in the future.