financial innovation -...

TRANSCRIPT

Financial Innovation

What is financial innovation?

• New Products/Services

• New Processes

• New Organizational Forms

Why is financial innovation important?

• Finance is a central input for virtually all productive activity

• Better finance encourages more saving and investment

• Better finance encourages improved productivity ofinvestment decisions

Can Finance Industry Innovate More? Business Week Top 50 Most Innovative Companies, 2006

Source: Business Week

Only one of the top 50 most innovative companies is in the financialservice industry.

Apple Virgin Amazon DaimlerChrysler PepsiCo

Google Samsung Target Infosys Hewlett Packard

3M Sony Honda Ryanair Disney

Toyota DellResearch In

MotionPixar jetBlue

Microsoft IDEO Southwest SonyEricssonW.L. Gore &

Associates

General Electric BMW Porsche Whole Foods Skype Technologies

Procter &

GambleIntel Genentech Capital One FedEx

Nokia eBay Cisco Tesco Bang & Olufsen

Starbucks IKEA Nike Danone Renault

IBM Wal-Mart Motorola BP L'Oreal

Financial Innovations Reduce Volatility Selected Macroeconomic Volatility Before and After FI Period

Source: Jermann and Quadrini 2006

1.7

0.8

2.2

7.4

0.90.90.4

1.1

4.8

0.5

0

1

2

3

4

5

6

7

8

Output TFP Labor Investment Consumption

1952-1983

1984-2005

Percent

$US 370 Trillions Notional Amount Global Over-the-Counter Derivative Market

10,073369,905Total

1,70735,969Others

29420,352Credit Default Swaps

7186,394Commodity

6716,783Equity-Linked

5,549262,296Interest Rate

1,13438,111Foreign Exchange

Market Value ofContracts

US$ Billions

NotionalAmounts

US$ Billions

June 2006

Source: International Monetary Fund

Interest Rate Derivatives By Counterparty and Maturity

44 44

12

3539

27

0

10

20

30

40

50

With OtherDealers

With OtherFinancial Inst.

WithNonfinancial

Customers

Less than 1year

Between 1- 5years

More than 5years

Percent of US$ 262 Trillions Notional Amount, June 2006

By Counterparty By Maturity

Source: International Monetary Fund

Real Estate

79%

Other

21%

\

Real Estate: Largest U.S. Tangible Assets

$47.2 Trillion U.S. Tangible Assets, December 2006

Source: Federal Reserve

2006200520042003200220012000

20

15

10

5

0

-5

-10

3.5

3.0

2.5

2.0

1.5

1.0

% Change from Previous Year Millions

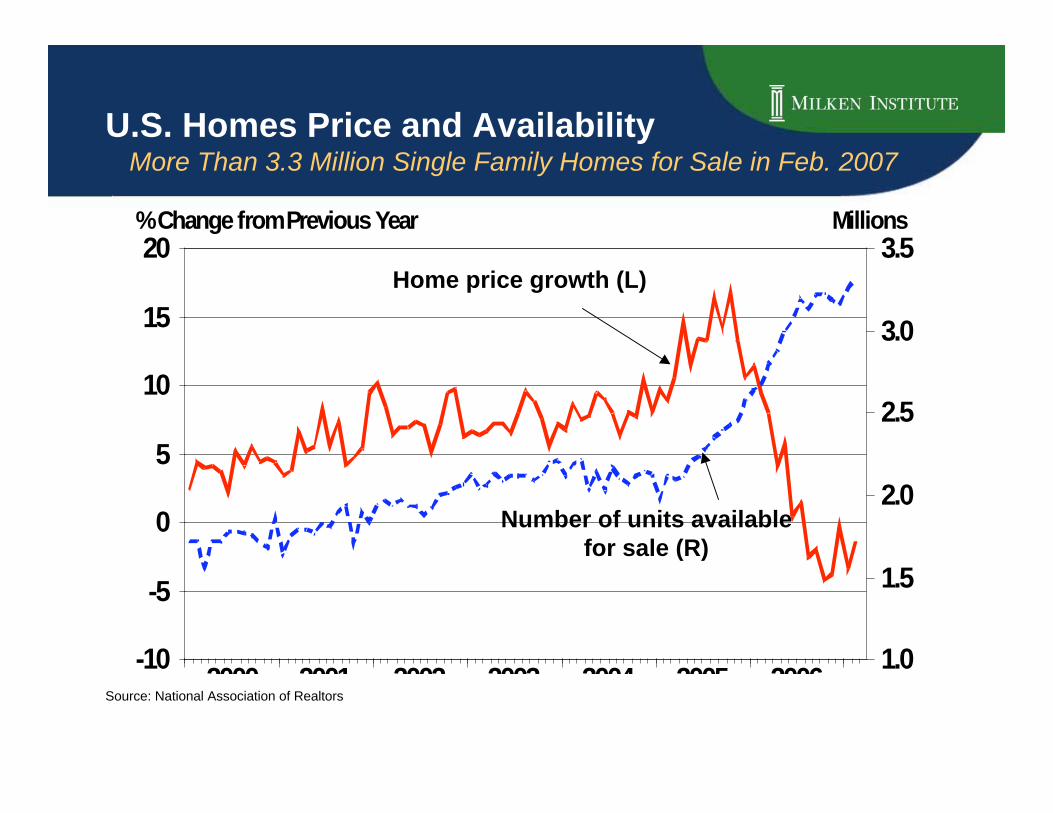

U.S. Homes Price and AvailabilityMore Than 3.3 Million Single Family Homes for Sale in Feb. 2007

Home price growth (L)

Number of units availablefor sale (R)

Source: National Association of Realtors

Homeownership and Adjustable Mortgage

20062004200220001998199619941992

70

69

68

67

66

65

64

63

64

62

60

58

56

54

% of Total U.S. Households % of Total Mortgage

Source: Federal Housing Finance Board and U.S. Census

ConventionalAdjustable Mortgage

Share of Total Mortgage

Homeownership Rate

U.S. Homeownership by Race 68.9 % of Total U.S. Household Own a Home

Source: U.S. Census

47

71

46

54

48

72

50

60

40

45

50

55

60

65

70

75

80

Black White Hispanic Others

1999 2006

% of Household

Number of

homes available

for sale (L)

Average sales

price of existing

homes (R)

1.6

2.1

2.6

3.1

3.6

4.1

140

160

180

200

220

240

260

280

300

Millions $ Thousands

1999 2000 2001 2002 2003 2004 2005 2006

U.S. Homes Price and Availability3.7 Millions Homes and Condos for Sale in January 2007

Source:Source: Economy.com

2.0

2.2

2.4

2.6

2.8

3.0

Dec-98 Dec-99 Dec-00 Dec-01 Dec-02 Dec-03 Dec-04 Dec-05 Dec-06

9

10

11

12

13

14

15

16

Percent of Loans Percent of Loans

Increasing Mortgage Delinquency All Delinquencies: 30, 60 and 90 Days

Source: Mortgage Banker Association

Subprime (R)Dec. 06: 13.3%

Prime (L)Dec. 06 : 2.6%

Weakened Underwriting Standards

LTV>80%

Full

Documentation

(% of Orig.)

With Second

Liens % Interest Only

2003 10.1 48.6 10.9 53.3

2004 20.7 51.2 23.1 71.2

2005 21.7 47.3 26.8 81.4

2006 28.2 33.6 35.3 90.7

2003 33.3 28.1 23.4 56.4

2004 46.8 32.6 39.1 75.0

2005 49.6 28.3 46.9 82.6

2006 55.4 19.0 55.4 87.2

2003 55.6 63.5 9.9 5.3

2004 61.1 59.9 19.1 19.5

2005 64.4 55.9 28.1 31.6

2006 64.0 54.6 31.0 19.9

% of Origination

Pri

me

AR

Ms

Alt

-A

AR

Ms

Su

bp

rim

e

AR

Ms

Year

Source: UBS

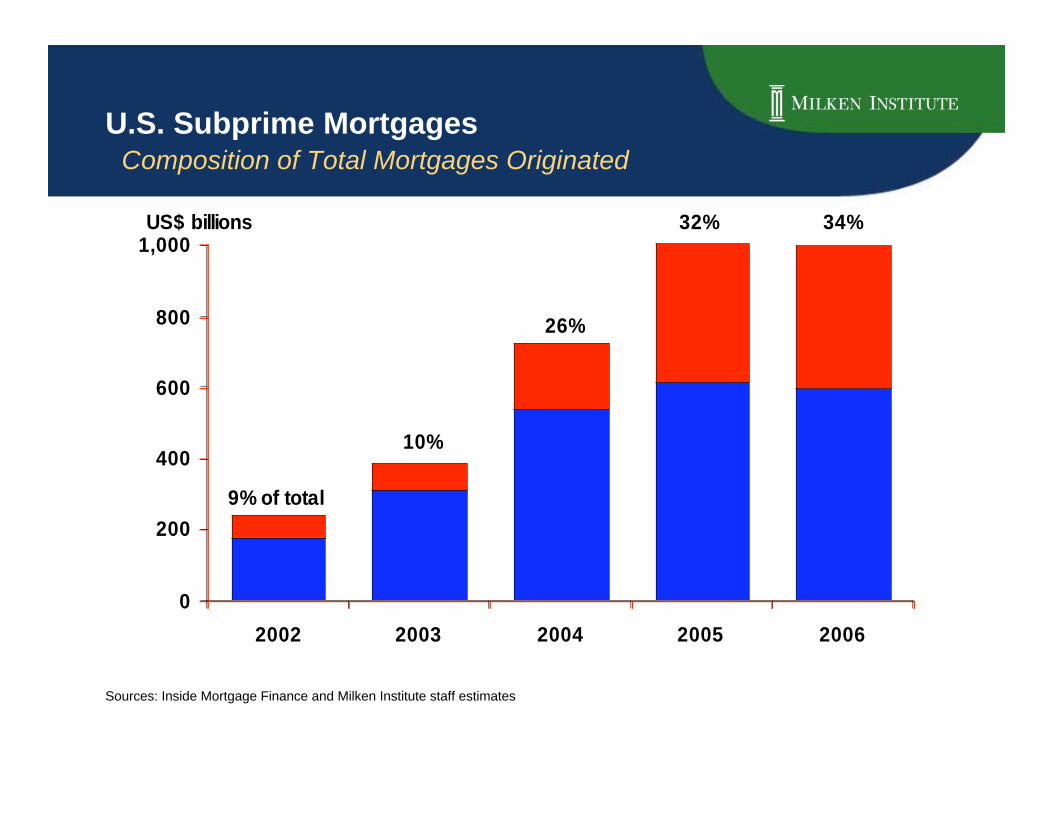

U.S. Subprime Mortgages Composition of Total Mortgages Originated

Sources: Inside Mortgage Finance (adapted from The Economist), Milken Institute staff estimates

0%

20%

40%

60%

80%

100%

2002 2003 2004 2005 2006

S b i "Alt A" T diti l

200620052004200320022001200019991998

8.5

8.0

7.5

7.0

6.5

6.0

5.5

5.0

14

12

10

8

6

Percent YOY % Change

Growth in Mortgage Outstanding andMortgage Rate

$13.3 trillionstotal mortgages

outstanding,December 2006 (R)

30-year fixedconventional mortgage

rate (L)

Source: Federal Reserve and Federal Housing Finance Board

Rising Overall Real Estate Leverage U.S. Household Real Estate Loan To Value

Source: Federal Reserve060196918681

50

45

40

35

30

25

Percent

U.S. Subprime Mortgages Composition of Total Mortgages Originated

Sources: Inside Mortgage Finance and Milken Institute staff estimates

0

200

400

600

800

1,000

2002 2003 2004 2005 2006

S b i "Alt A"

9% of total

10%

26%

32% 34%US$ billions

S&P/Case-Shiller Home Price Composite

0

50

100

150

200

250

Jan-87 Jan-91 Jan-95 Jan-99 Jan-03 Jan-07

Source: Bloomberg

Housing Price Futures Contract

210.2

216.0

215.2

211.4

215.0

206

208

210

212

214

216

218

Nov-06 Dec-06 Jan-07 Feb-07 Mar-07

11/07 Future Contract on S&P Case-Shiller Housing Composite

Source: Bloomberg

Rational or Irrational Exuberance?

Mortgage Debt as a Percentage of GDP

> 50%

20-50%

10-20%

5-10%

< 5%

n/a

2

Source: Lehman Brothers; European Mortgage Federation; Merrill Lynch; World Bank; Bureau of Economic Analysis; IMF; IUHF; HousingFinance; Unicorn Investment Bank; BIS.

FI Transferring Challenge Mexico and U.S. Housing Markets

1.2 1.6 Potential Market per year (Millions of Units)

<1% >50% % of Self-built Housing Stock

- ~50% % of Sub-standard Housing Stock

1900700 Average Square Feet

2.34.5 Persons per Household

72.5 21.5 Households (Millions)

U.S. Mexico

Source: Mexican Housing Overview, U.S. Census, Joint Center for Housing Studies of Harvard University

Largest Commercial Real EstateMarkets Worldwide

World total: >$14 trillion

Source: European Public Real Estate Association, World Bank Organization, FTSE Group

Belgium Switzerland

MexicoS Korea

HKSpain

CanadaUK

GermanyJapan

US

6000

5000

4000

3000

2000

1000

0

40

30

20

10

0

US$ Billion Percent of World Total

0.91.01.41.62.02.62.7

7.27.4

13.5

34.4Total Percentage

Outstanding Residential MortgageBalances in Selected Countries, 2005

Source: US data is from Federal Reserve and other data is from CIA World Factbook, Hypostat 2005

527

1,575

252 47469 654

107

1,606

8,281

1,411

0

2,000

4,000

6,000

8,000

10,000

US Japan Germany France UK Italy Mexico Spain Australia Belgium

US$ Billions

Mortgage Balances Outstanding 2005

Source: US data is from Federal Reserve and other data is from Wall Street Journal, March 20, 2007

36

23

139

3

49

97

37

0

20

40

60

80

100

US HK Taiwan Singapore Malaysia S. Korea Thailand India

Percent of GDP

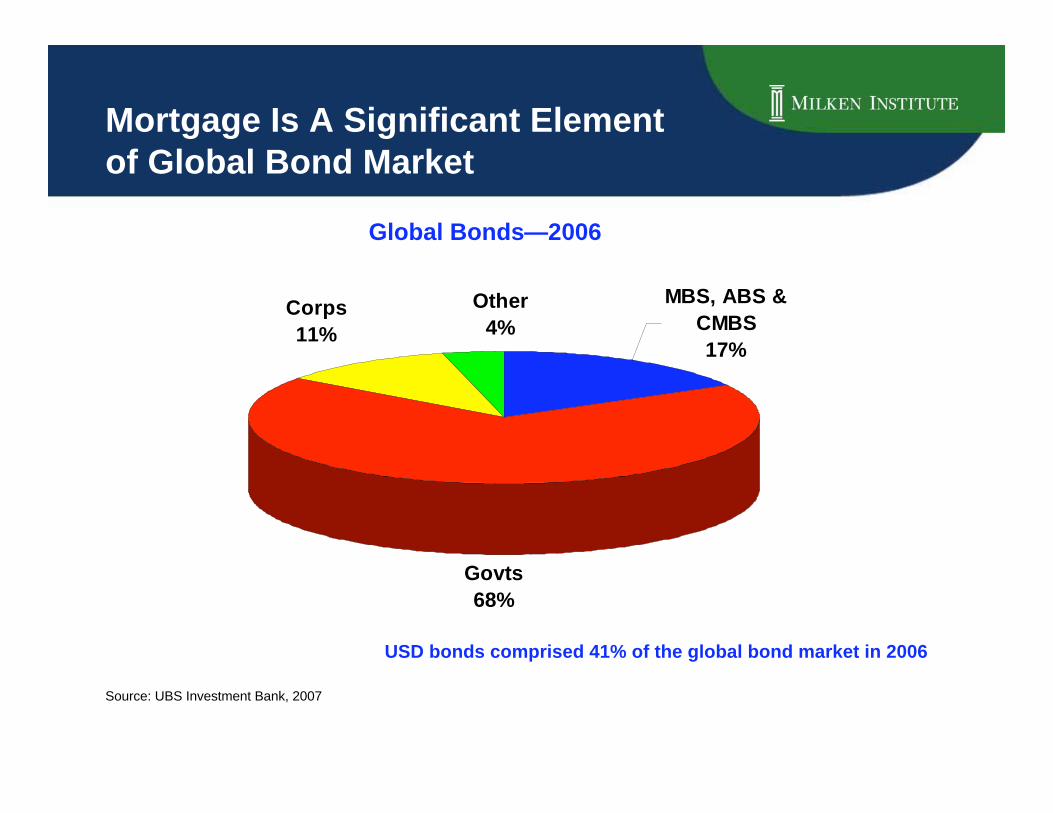

Mortgage Is A Significant Elementof Global Bond Market

Source: UBS Investment Bank, 2007

Global Bonds—2006

MBS, ABS &

CMBS

17%

Govts

68%

Corps

11%

Other

4%

USD bonds comprised 41% of the global bond market in 2006

Characteristics of Mortgage Markets Selected Industrialized Countries

Source: IMF, 2005

Growing Global CommercialMortgage-Backed Securities (CMBS)

Source: www.cmbs.org

17 17 16 26 37

7457 49

7452

7893

169

203

143 8

110.3 3 1

14

19 12

2329

21

34

69

0

0

50

100

150

200

250

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06

Non-US

US

US$ Billions

Global CommercialMortgage-Backed Securities As a Percentage of the Total

Source: GPR, NAREIT, FTSE, EPRA (Dec 2006)

0

2

4

6

8

10

12

World N America Latin America Asia-Pacific Europe

Percent

Implications of Global SocioeconomicChange on Mortgage Markets

Source: United Nations Population Division

2006: 6.4 billion

2050: 9 billion The world’spopulation growthwill occur almostentirely in lessdeveloped regions,which shows hugemortgageopportunities inthese regions

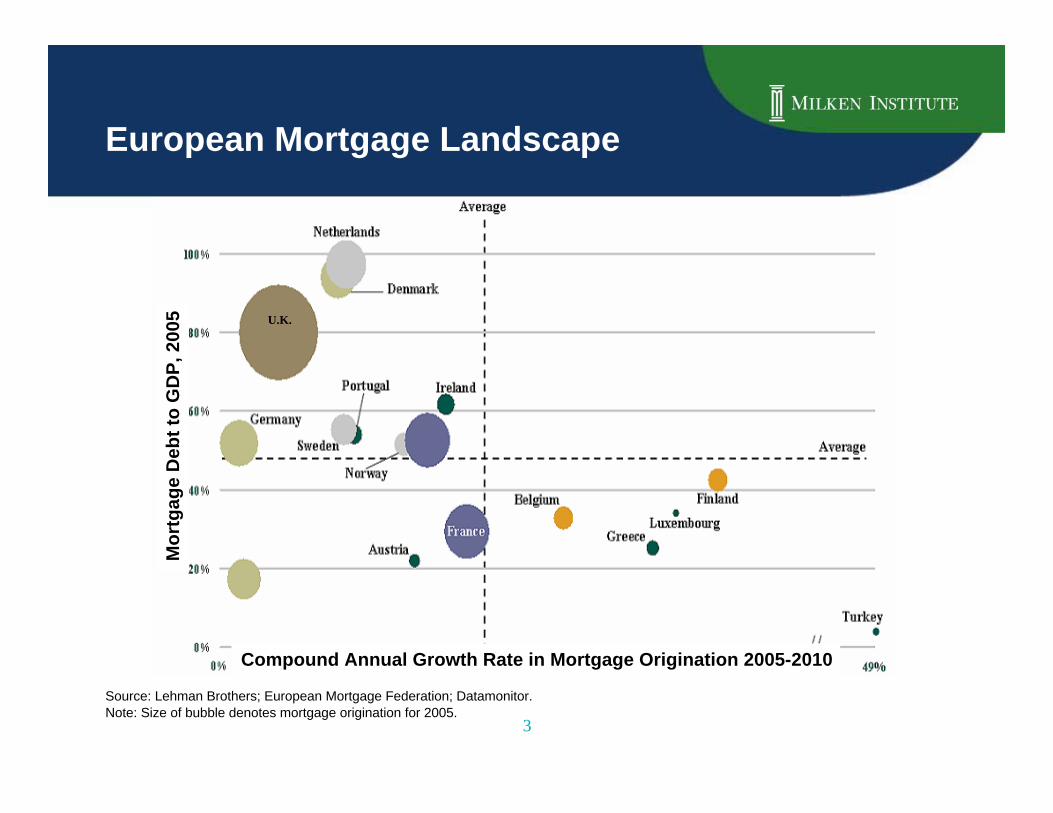

European Mortgage Landscape

3

Source: Lehman Brothers; European Mortgage Federation; Datamonitor.Note: Size of bubble denotes mortgage origination for 2005.

U.K.

Compound Annual Growth Rate in Mortgage Origination 2005-2010

Mo

rtg

ag

e D

eb

t to

GD

P,

20

05

The Asian Mortgage Landscape

4

Source: Lehman Brothers

Note: Size of bubble denotes actual and estimated mortgage origination for 2005; CAGR in mortgage origination estimated by LehmanBrothers.

Compound Annual Growth Rate in Mortgage Origination 2005-2010

Mo

rtg

ag

e D

eb

t to

GD

P,

20

05

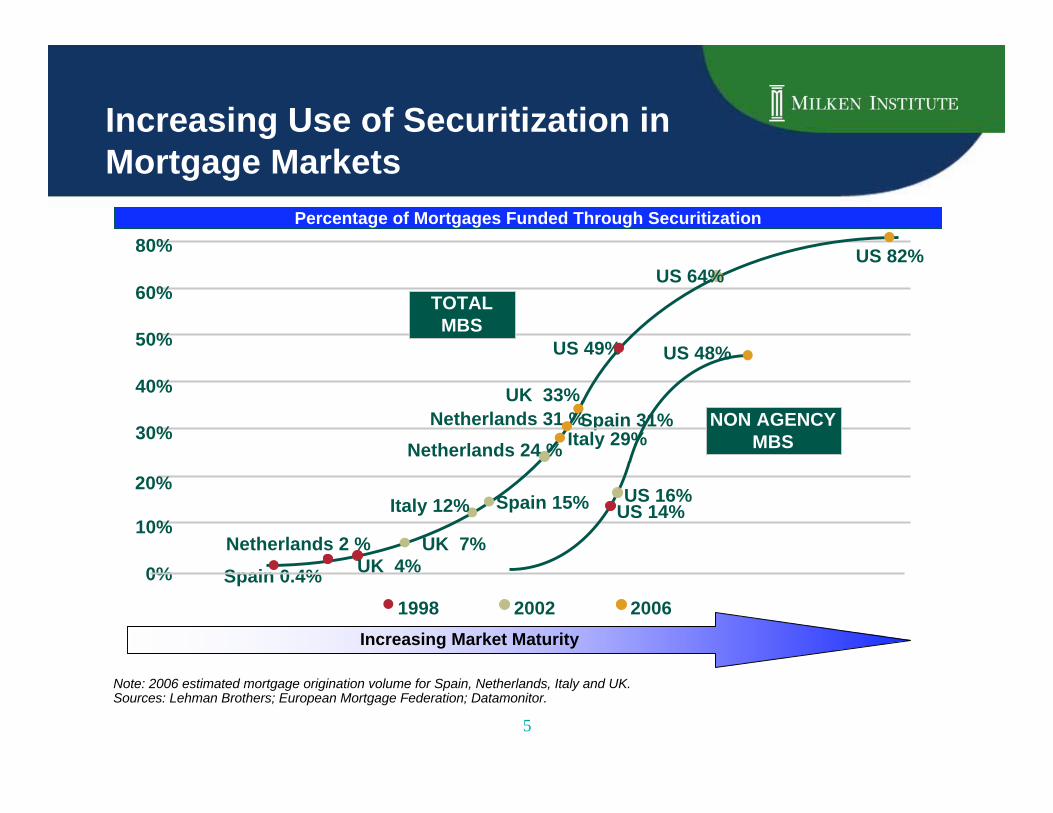

Increasing Use of Securitization inMortgage Markets

Note: 2006 estimated mortgage origination volume for Spain, Netherlands, Italy and UK.Sources: Lehman Brothers; European Mortgage Federation; Datamonitor.

Percentage of Mortgages Funded Through Securitization

UK 33%

Spain 31%

Spain 15%

UK 7%

Spain 0.4%

US 49%

60%

40%

30%

20%

10%

0%

50%

Netherlands 2 %

80%

Increasing Market Maturity

2002 20061998

US 64%US 82%

Netherlands 31 %

Netherlands 24 %

TOTALMBS

NON AGENCYMBS

US 14%US 16%

US 48%

Italy 12%

Italy 29%

UK 4%

5

Capital Market Fundingin Emerging Markets

33

Mortgage BondsStructured

Finance(Asia, CEE)

StructuredFinance

(Latin America,Africa)

ConduitsLiquidityFacilities

Chile China Argentina Argentina India

Colombia Hong Kong Brazil Brazil Jordan

Czech Republic Korea Colombia Colombia Malaysia

Hungary Malaysia Chile Hong Kong Mexico

Kazakstan Philippines Mexico Korea South Africa

Latvia Thailand Panama Trinidad Trinidad

Poland Peru Thailand

Trinidad

Latvia

Russia Morocco

South Africa

Reasons for Mortgage-Backed Securities

• Transform illiquid individual financial assets into liquidand tradable capital market instruments

• Allow mortgage originators to replenish their funds

• Can be used by Wall Street banks to monetize the creditspread

• A more efficient and lower cost source of financing

• Allow issuers to diversify their financing sources

• Allow issuers to remove assets from their balance sheetwhich can help to improve various financial ratios andutilize capital more efficiently

35

Pre-requisites of EffectiveHousing Finance Systems

• Avoidance of Severe Inflation

• An Efficient Property Registration System

• Free Markets in Land and Housing

• Competitive Financial Markets

• Legal Infrastructure That Supports HousingFinance

• Regulatory Infrastructure That Supports theFinancial System

The Four Housing Finance Models

• Commercial Bank Model: Deposit-financed, diversified portfoliolenders

• Mortgage Bank Model: Bond-financed, specialized portfolio lenders

• Contract Savings Model: Specialized institutions (e.g.: Bausparkassen) offering subsidized, loan-linked savingscontracts

• Secondary Market Model: Second-tier institution lending to or purchasing loans from primary lenders

Renewable Energy Consumption Trend United States, 1995-2006

Source: Energy Information Administration/Monthly Energy Review March 2007

060504030201009998979695

4.0

3.0

2.0

1.0

0.0

Quadrillion BTU

Hydro-Electric PowerBiomassOther

Electric PowerTransportation

IndustrialCommercial

Residential

5

4

3

2

1

0

Quadrillion BTU

U.S. Renewable Energy Consumption By Sector, 2006

Source: Energy Information Administration/Monthly Energy Review March 2007

0.50.1

1.6

0.5

3.9

Renewable EnergyNuclear Electric Power

Fossil Fuels

100

80

60

40

20

0

Quadrillion BTU

U.S. Renewable Energy Consumption Compared with Other Resources, 2006

Source: Energy Information Administration/Monthly Energy Review March 2007

85.4

8.2 6.5

Oil Reserves Concentrated inUnstable Regions

Sources: Energy Information Administration

Middle East

60%

Africa

10%

Venezuela

6%

Russia

5%

Other

3%

Canada

14%

United States

2%

Volatile Oil and Natural Gas Prices

Sources: Energy Information Administration

0500959085

$80

$70

$60

$50

$40

$30

$20

$10

$12

$10

$8

$6

$4

$2

$0

US dollars per barrel US dollars per Thousand Cubic

WTI Crude Oil PriceNatural Gas Price

Most Costly Disaster in US History

TOTAL ECONOMIC IMPACT ~ APPROX. $200B USD

Drasticallyreduced tax

revenue base,unemployment,displacement,

bankruptcy

Loss ofapproximately

$500,000 in taxrevenue for each

day riverboatcasinos were

closed

Loss of timberproducts

estimated at $1.3billion; USDAdeclared 31agricultural

disaster areas

Interrupted oilproduction,

importation, andrefining in the Gulfarea had a major

effect on fuelprices

$40 - $60 Billion

$2 – 3 Billion

$15 – 25 Billion

$20 - 25 Billion

$2 - 5 Billion

$1 - 2 Billion

Gross IndustryLoss

1,752

Claims Filed

Additional Sources of Loss

Total

Wind & Surge, Second Landfall

New Orleans Flooding

First Landfall in Florida

Offshore Energy

Loss Component

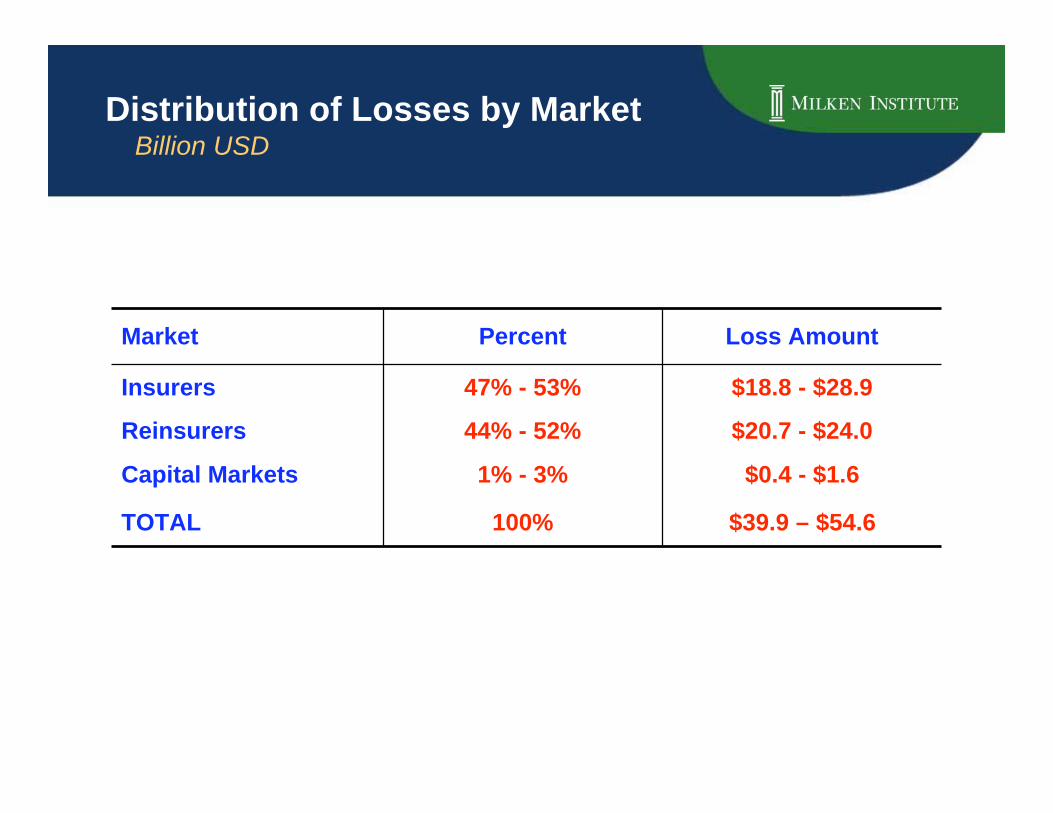

Insurance Industry Loss Estimate September 2005

$0.4 - $1.61% - 3%Capital Markets

100%

44% - 52%

47% - 53%

Percent

$39.9 – $54.6

$20.7 - $24.0

$18.8 - $28.9

Loss Amount

TOTAL

Insurers

Reinsurers

Market

Distribution of Losses by Market Billion USD

Catastrophic Risk on the Rise Global Number of Catastrophic Events, 1979 – 2004

Sources: Allstate Insurance Company

0

50

100

150

200

250

1979 1984 1989 1994 1999 2004

Natural Catastrophes

Man-Made Disasters

Economic Impact of Catastrophes

Sources: Allstate Insurance Company

$25.7 $29.0

$169.6

$15.9$27.0

$52.4 (Est.)

0

50

100

150

200

250

1 2 3

Insured Property Loss

Uninsured Loss and Other Economic Loss

Earthquake

Northridge,

California

(1994)

Hurricanes

Charley, Frances,

Ivan and Jeanne

(2004)

Hurricanes

Katrina, Wilma

and Rita

(2005)

US$ Billions

$41.6 $56.0

$222.0 (Est.)

Larger Impact onEmerging Market Economies

Sources: Allstate Insurance Company

38%

14%12%

8% 7%

3% 3% 2% 2%

Honduras Dominican

Republic

Ecuador Iran Algeria Poland India Mexico Argentina

Hurricane

Flood

Earthquake

1998 1998 1998 1990 1980 1997 1990 1985 1985

Catastrophe Bonds

Insurance Company

(Protection Buyer)

Single Purpose

Reinsurer

(Trust)

Swap Counterparty

Reinsurance Premiums

Reinsurance Contract

Investment Earnings

Security Interest

Reinsurance Recoveries

Investors

(Securities)

Bonds

Proceeds

Interest

Principal (at maturity)

Interest Rate Spread

Insurance Company

(Protection Buyer)

Single Purpose

Reinsurer

(Trust)

Swap Counterparty

Reinsurance Premiums

Reinsurance Contract

Investment Earnings

Security Interest

Reinsurance Recoveries

Investors

(Securities)

Bonds

Proceeds

Interest

Principal (at maturity)

Interest Rate Spread

• Risk-linked debt instruments

• Returns are related to the occurrence of specific naturaldisasters and man-made disasters

Catastrophe Bonds

• First sold in 1997

• 64 catastrophe bonds have been issued

– Total risk limits: $9.68 billion

• Annual issuance peaked in 2003

– $1.73 billion

– Leveled off to slightly over $1 billion since 2003

• Transaction costs are declining

• Usage could increase with certain regulatory and tax changes

• High reinsurance premiums and inadequate global capacity are themain reasons for market limitations.

Why Invest in Catastrophe Bonds?

• For Investors:

• Consistently shown higher returns than similarly ratedcorporate bonds

• Uncorrelated with stock, bond, commodities, and real estatemarkets

• For Insurers:

• Have virtually no credit risk

• Can provide a capacity much larger than the traditionalreinsurance capacity after a mega catastrophic event

• For Individuals:

• Provide means for accessing insurance in “uninsurable”geographic areas

• Increase the supply of capital in financial markets and can beutilized as a financial tool in risk management

Gas, 20.90%

Nuclear, 6.50%

Renewables,

13.10%Coal, 25.10%

Non-Renew.

Waste, 0.20%

Oil, 34.30%

Fuel Shares of World Total PrimaryEnergy Supply 2004

Source: International Energy Agency

Water ShortagesHigh Vulnerability to Water Scarcity

Source:

The global water market is a perfect fitwith Siemens long term business strategy World water market 2004 - 2008, in USD

Operation of municipaland industrial water andwaste water treatment

plants

Source: World Bank, various research institutes

Global facts

Less than 1% of Earth'swater is usable

Population increase of2.5B by 2035 mainly inregions with watershortage

1.5B people do not havesafe water supply; 4B in2025

40% increase in waterconsumption by 2025

316

29

96

473

2008

Systems, Products &

Services

Turnkey /EPC

Oper-ations

CAGR 6%

375

2004

250

40

117

Consulting, Design andEngineering of turn-key

solutions

Systems, products, services(product related and

maintenance)

The annual world water infrastructure market exceeds$400 billion, and is projected to grow at 2x global GDP

The “accessible” water market will growat 8% per year in developing countries Accessible water market 2004 and CAGR by geography, USD and %

375

Total watermarket 2004

6"

10" 5"

15" 4"

20"

29"

24" 6"

151"

8%

3-5%

12%

4-6%

3-5%

7-9%

4-6%3-6%

6-9%

~6%

Accessiblemarket by segment

2004

CAGR2004-2008

Pumps & Valves

Infrastructure

Outsourcedoperations

Turnkey / EPC

Non-chemical watertreatment equipm.

Automation& Metering

Chemicals & chem.treatm. equipm.1)

Maintenance &analytical services

24" Municipal

2" Industrial

Core systems market

5"

1"

Core service market

224

151

In-sourced

opera-tions

Acces-sible

market Developed countriesaccount for 70% of the

market with growth ratesof 3.6% p.a.

Developing countriesshow growth rates of

8.11% p.a.

Siemens WTaddressed market

segment $38BUSD

20502040203020202010200019901980197019601950

100

90

80

70

60

50

40

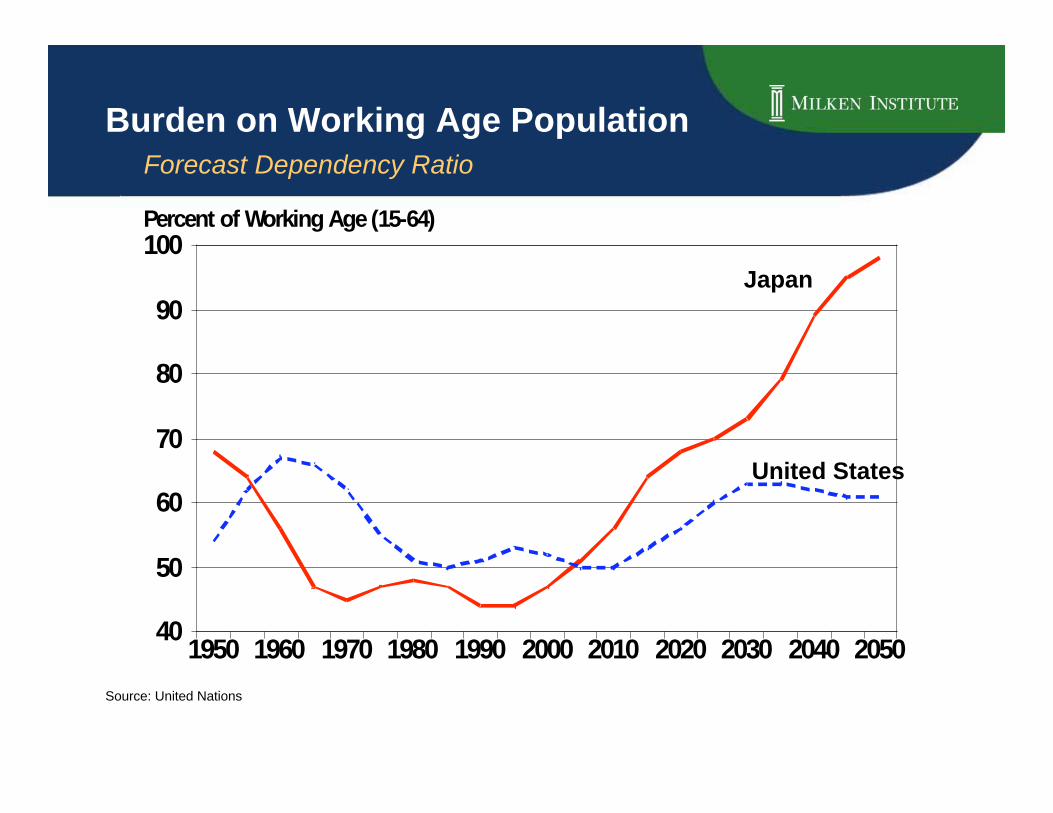

Percent of Working Age (15-64)

Burden on Working Age Population Forecast Dependency Ratio

Japan

United States

Source: United Nations

Dependents - Developed CountriesForecast Dependency Ratio

20502040203020202010200019901980197019601950

80

60

40

20

0

Percent of Working Age (15-64)

Aged 0-14Aged 65+

Source: United Nations

Dependents - Developing CountriesForecast Dependency Ratio

20502040203020202010200019901980197019601950

80

60

40

20

0

Percent of Working Age (15-64)

Aged 0-14Aged 65+

Source: United Nations

Developed

Countries

Developing

Countries

20502040203020202010200019901980197019601950

85

80

75

70

65

60

55

50

45

Percent of Working Age (15-64)

Dependency BurdenForecast Dependency Ratio

Source: United Nations

Most Mature Economies HavePopulations Peaking by 2010

Source: United Nations Population Division

The labor force of Japan is withering and the elderly population—especially females—will expand dramatically.

Most Emerging Economies HaveGrowing Populations

Source: United Nations Population Division

The workforce growth in India will be staggering.The country will generate enormous demand for high-quality real estate of alltypes—residential, retail, industrial, warehouses, hotels, and office buildings.

Projected Age-Related Spending

4.20.155.888.6 G7 Average

5.9-1.843.561.8 United States

4.1-1.540.046.7 United Kingdom

2.2-3.086.4173.1 Japan

1.91.495.1120.4 Italy

3.20.151.571.1 Germany

3.3-0.243.776.1 France

9.05.530.270.8 Canada

(Percentagepoints of GDP)

(% of GDP, 2005)

Age-RelatedSpending, 2005

to 2050

PrimaryBudgetBalance

Net Debt Gross Debt

Source: International Monetary Fund

World Hunger 20% or More Undernourished

Source:

Malaria DistributionWhere Malaria is Endemic

Source:

Tuberculosis Distribution100 or more cases per 100,000 people

Source:

HIV DistributionAdult HIV prevalence of 5% or more

Hepatitis B DistributionPrevalence of 7% or more

Leading Causes of Death-United StatesAs Percent of Deaths by Gender, 2001

Respiratory DiseaseStroke

AccidentsCancer

Heart Disease

35

30

25

20

15

10

5

0

Percent

malefemale

Source:

Most Products that Get to MarketNever Make Enough to Recoup R&D Investment

After-Tax Net Lifetime Sales ($M)

1st 2nd 3rd 4th 5th 6th 7th 8th 9th 10th

New Products Grouped in Tenths According to Financial Success

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

After-tax average R&D Cost

After-Tax Net Lifetime Sales ($M)

1st 2nd 3rd 4th 5th 6th 7th 8th 9th 10th1st 2nd 3rd 4th 5th 6th 7th 8th 9th 10th

New Products Grouped in Tenths According to Financial Success

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

After-tax average R&D Cost

Source: Grabowski, Vernon, and DiMasi, PharmacoEcon 2002

Market Potential for EnergyEfficiency and Clean Technologies

Source: Scenarios for a Clean Energy Future, Oak Ridge National Lab, 2000;

American Council on Renewable Energy (ACORE), December, 2006

0

50

100

150

2006 2020 business as usual 2020 with energy

efficiency and

renewables

Qu

ad

s o

f U

.S.

en

erg

y u

se

The market potential

A Green Loan: A New BusinessModel Rises from An Intersection of Expertise

A New Sandwich:the Energy intermediary Model

2 + 2 = 5: the Energy intermediaryModel Profits from the Synergies

Reorganize Parties to MakeA Significant Change

• Great national concern about energy security and globalwarming

• Sufficient “ready” technologies exist, but the market side

needs incentives to change

• The profit motive will encourage business to adopt new

technologies

• Businesses must adopt financeable plans to adopt newtechnologies

• Businesses must monetize their savings with innovativemetering and contracts

Connection between NationalConcerns and the Role of Capital Markets

Large Risks Remain After the ScienceIs Completed

Source: Martha Amram, Growth Options Insights

Valuations at Key Milestones inDrug Development

• In the traditionalfinancing model,investmentoccurred over life-cycle of drugdevelopment

• In today’smodel, there islittle investmentuntil after ClinicalPhase II

Expected Value Distributionof an IP Portfolio

• We expect the value of a portfolio to be Lognormallydistributed with three primary components

Transaction Structure of YaleUniversity’s Royalty Monetization

Source: Royalty Pharma

Leveraging Foundations toAccelerate Cures

Source: Technology Option Capital, LLC

A Private Company Closes theMarket Gap for Lending Using IP

Source: IP Innovations

Transaction Structure ofAdvanced Purchase Agreements

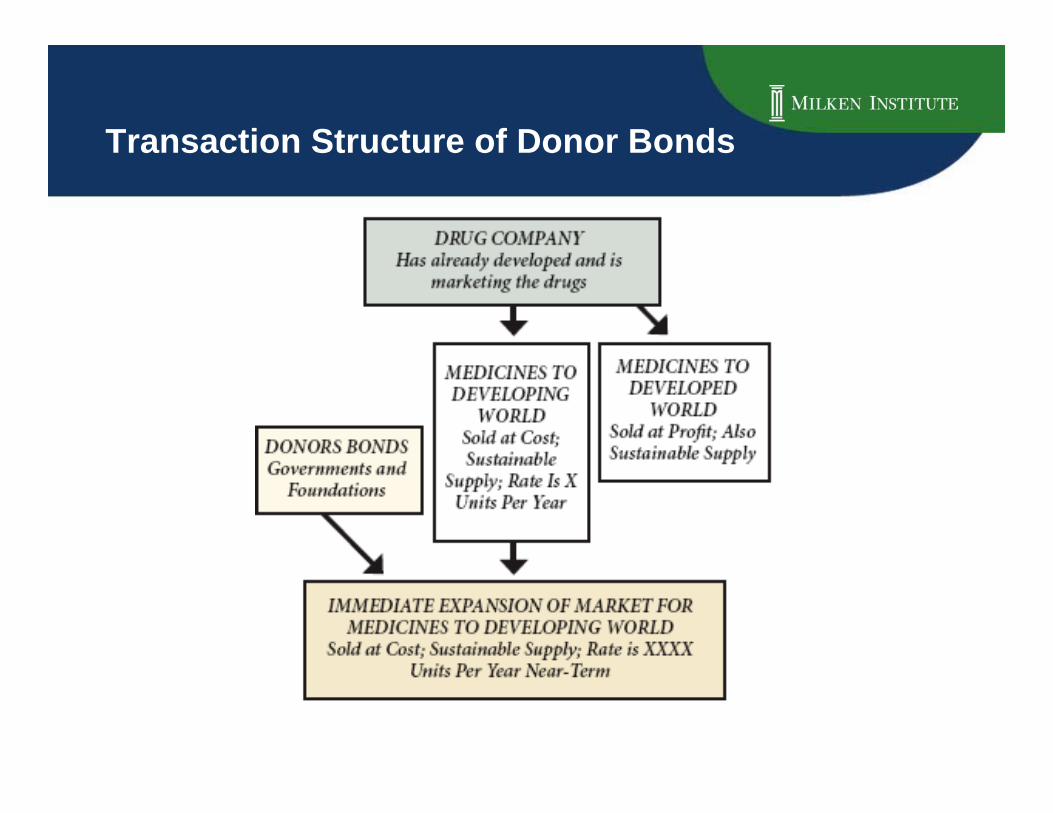

Transaction Structure of Donor Bonds

Financial Innovation: Human Capital andEducation

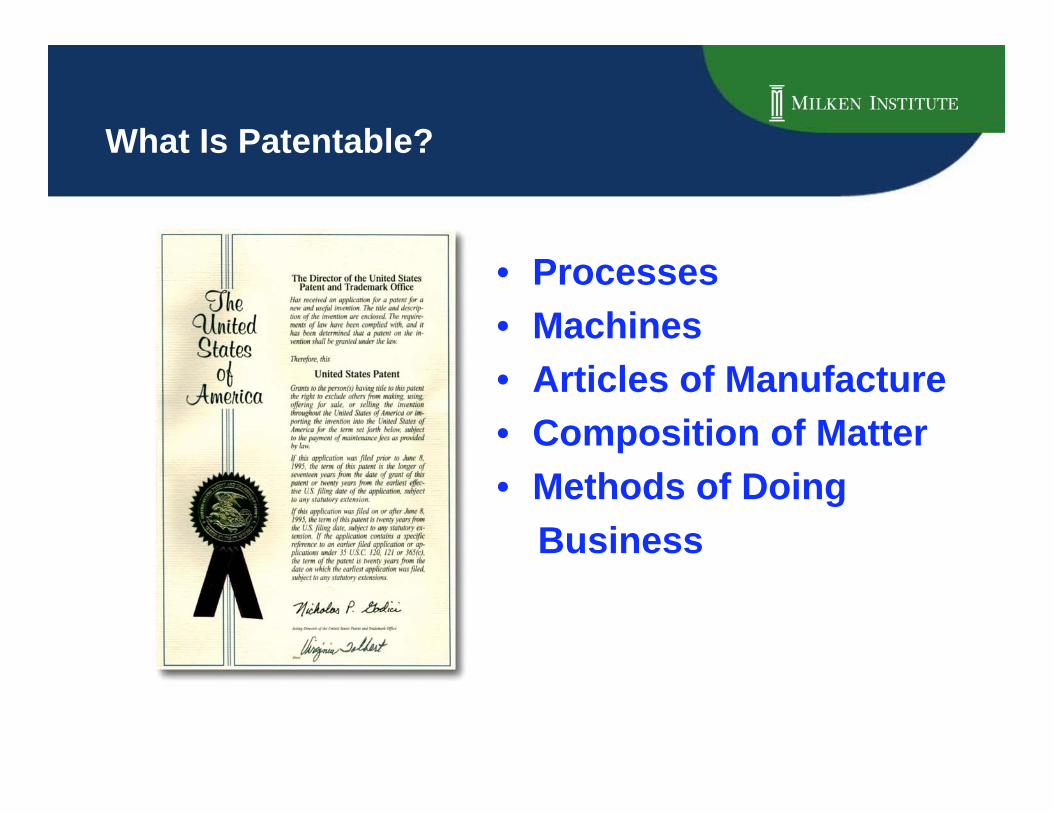

What Is Intellectual Property?

• Patents

• Trademarks

• Know-how

• Copyrights

• Trade Secrets

• Processes

• Machines

• Articles of Manufacture

• Composition of Matter

• Methods of Doing

Business

What Is Patentable?

Methods Commonly Used to ValueIntellectual Property

• Industry Averages orRules-of-Thumb

• Comparable Transactions

• Discounted Cash Flow(DCF)

• Options Value

Wealth Today Residesin Human Capital

• Becker and others estimatethat roughly 70% of anation’s wealth today is inthe form of human capitalrather than physical capital.

• The pecuniary returns toknowledge, education andskill are very high in theUnited States and evenhigher outside the mostdeveloped countries.

Explosive Growth of Patents,But Declining Share of the U.S.

Source: United States Patent and Trademark Office

0

30

60

90

120

150

180

40

50

60

70

80

90

100

Thousands Percent

Number of GrantedPatents (L)

U.S. Resident Share ofGranted Patents (R)

Personal Internal Rate of ReturnHigher Education

ItalyJapan

CanadaGermany

SwedenNetherlands

FranceDenmark

USUK

18

16

14

12

10

8

6

4

Percent

MaleFemale

Source:

DenmarkGermany

JapanCanada

ItalySweden

NetherlandsFrance

USUK

16

14

12

10

8

6

4

2

Percent

MaleFemale

Higher Education by CountrySocial Returns

Source:

Education and Training Pays…

Master’sdegree

Bachelor’sdegree

Associatedegree

Some college,no degree

High schoolgraduate

Some highschool, no

diploma

Unemployment rate in 2000

(Percent)

Median earnings in 2000

(Dollars)

1.6

1.8

2.3

2.9

3.5

6.5

55,300

46,300

35,400

32,400

28,800

21,400

Source:

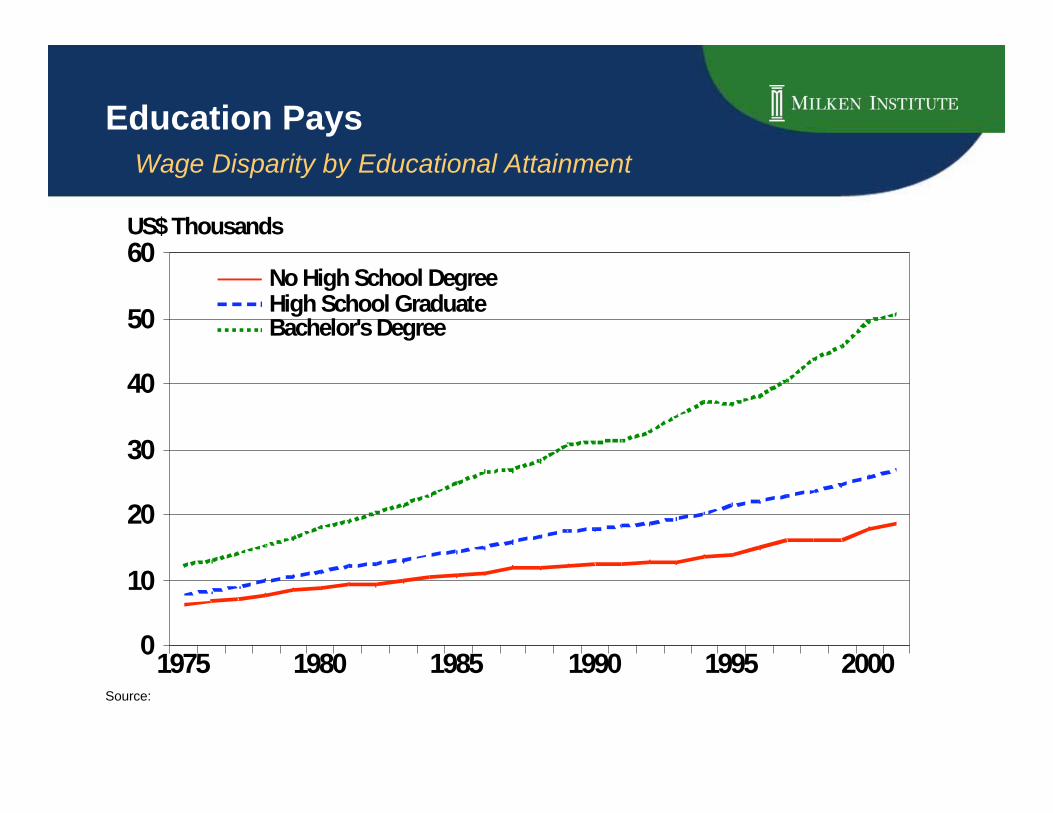

Education Pays

Wage Disparity by Educational Attainment

200019951990198519801975

60

50

40

30

20

10

0

US$ Thousands

No High School DegreeHigh School GraduateBachelor's Degree

Source:

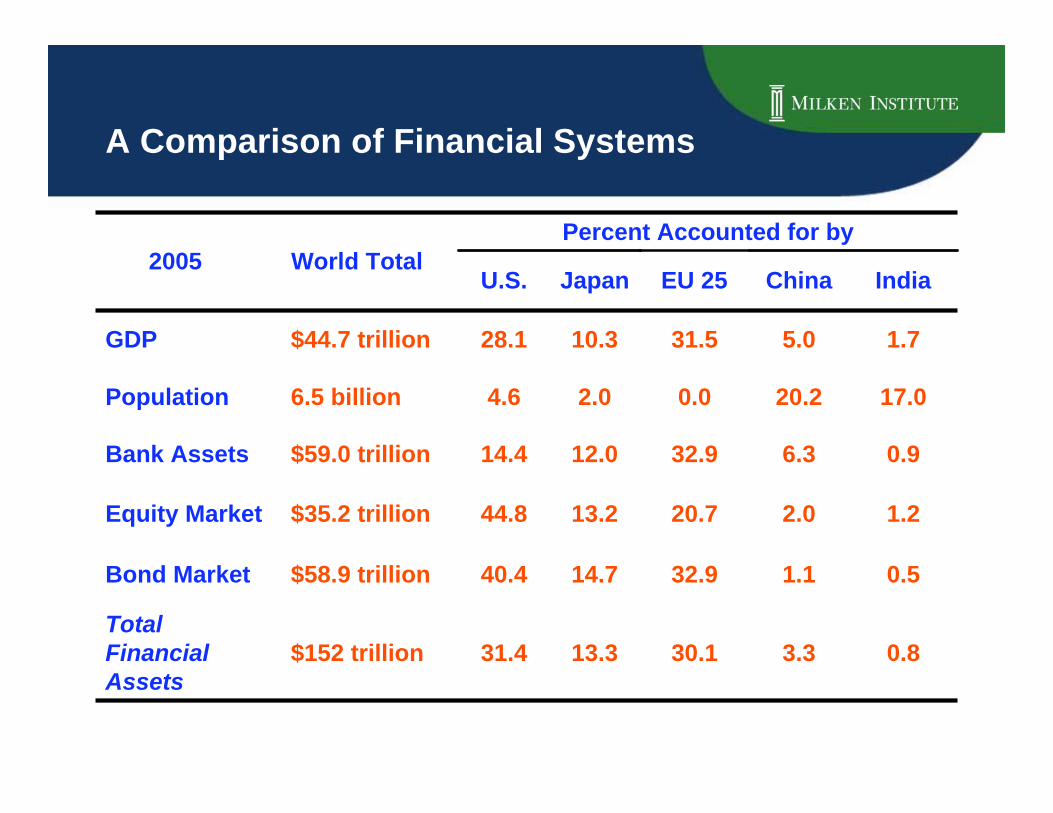

A Comparison of Financial Systems

World Total

31.4

40.4

44.8

14.4

4.6

28.1

U.S.

13.3

14.7

13.2

12.0

2.0

10.3

Japan

0.51.132.9$58.9 trillionBond Market

1.75.031.5$44.7 trillionGDP

Percent Accounted for by2005

0.83.330.1$152 trillionTotalFinancialAssets

1.22.020.7$35.2 trillionEquity Market

0.96.332.9$59.0 trillionBank Assets

17.020.20.06.5 billionPopulation

IndiaChinaEU 25

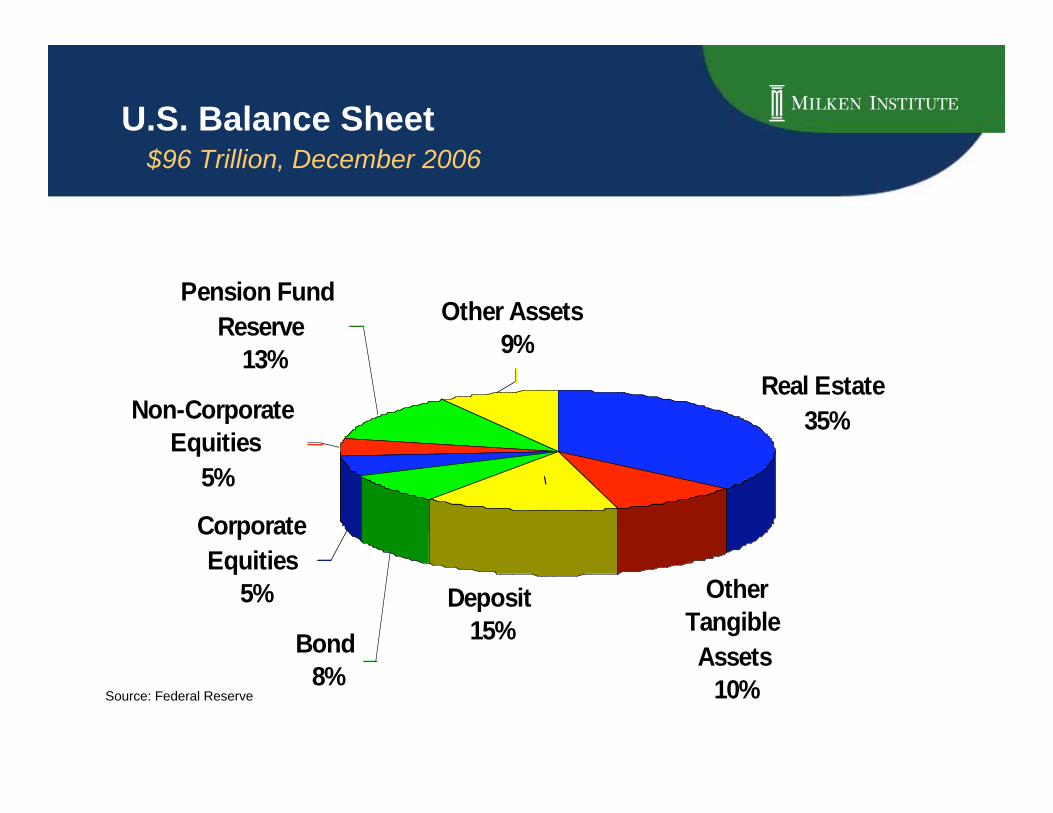

U.S. Balance Sheet $96 Trillion, December 2006

Real Estate

35%

Other

Tangible

Assets

10%

Deposit

15%Bond

8%

Corporate

Equities

5%

Non-Corporate

Equities

5%

Pension Fund

Reserve

13%

Other Assets

9%

\

Source: Federal Reserve

U.S. Financial AssetsDecember 2006: $56 Trillions

Source: Federal Reserve06029894908682

80

60

40

20

0

US$ Trillion

Bonds: Treasury, Agency and Muni Securities, Corporate Bonds, ABSLoans: Bank Loans, Mortgages, Consumer CreditsStocks: Corporate Equities and Mutual Fund Shares

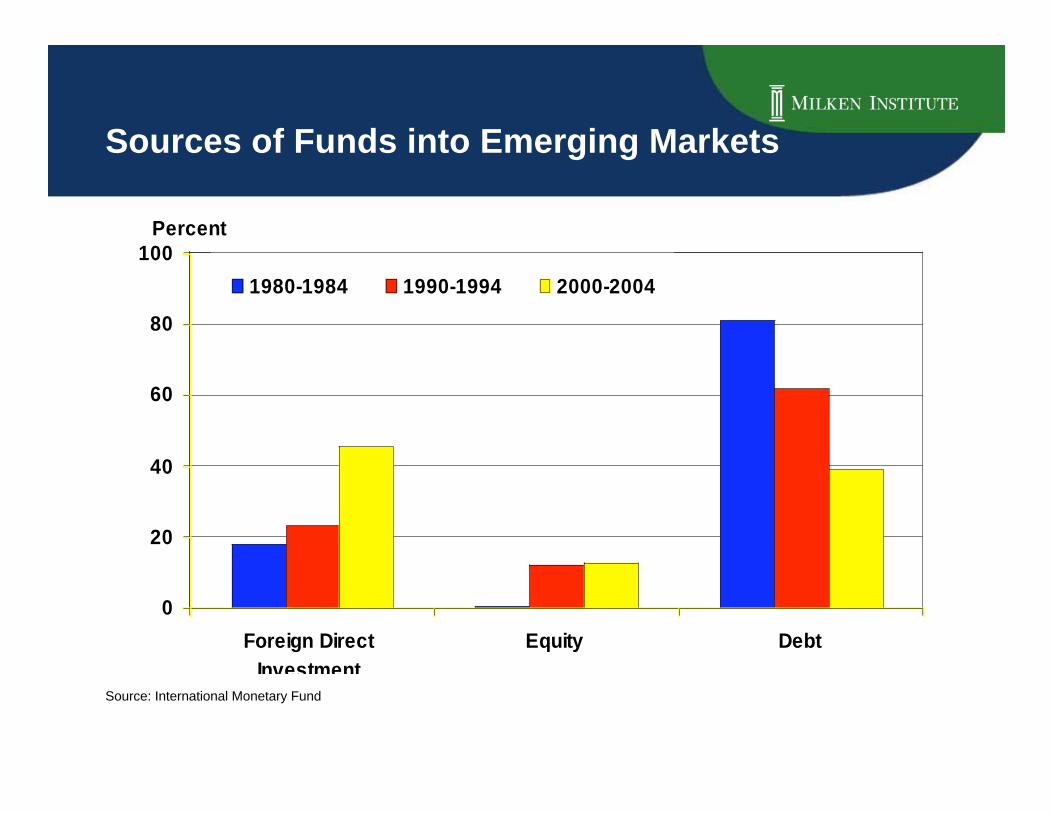

Sources of Funds into Emerging Markets

Source: International Monetary Fund

0

20

40

60

80

100

Foreign Direct

Investment

Equity Debt

1980-1984 1990-1994 2000-2004

Percent

Historical Bond Default Rates

0

20

40

60

80

100

1971 1976 1981 1986 1991 1996 2001 2006

0

3

6

9

12

15Par Value Defaults (L)

Default Rates (R)

US$ Billions Percent

Sources: Altman

Hedge Funds vs. Mutual Funds Number by Domicile Location, 2005

Total = 56,863

United

States

14%

Europe

53%

Asia

21%

Other

Countries

12%

Total = 6,445

United

States

52%

Europe

33%

Off-shore

Centers

8%

Asia

2%

Other

Countries

5%

Hedge Funds Mutual Funds

Source: Hedgefunds.net and MI staff estimates

Hedge Funds vs. Mutual Funds Assets by Domicile Location, 2005

Total = $17.8 Trillion

United

States

50%

Europe

34%

Asia

7%

Other

Countries

9%

Total = $968.7 Billion

United

States

53%Europe

38%

Off-shore

Centers

6%Asia

1%

Other

Countries

2%

Hedge Funds Mutual Funds

Source: Hedgefunds.net and MI staff estimates

968,69024,17712,63457,788371,048503,044All locations of fund assets

(US$ Millions)

1,163000316847Other/Unknown

70167900022Australia/Oceania

96378705010125Africa

3,6412,5541275959257South America

3,8332,390055450938North America

58,3963,81610,7893,38229,75410,655Asia

102,3541,42908,17983,0399,708Europe

303,5291,76428314,74224,426262,315United States

494,11010,7581,55030,622232,905218,275Global

All regions ofdomicile

OtherCountries

AsiaOff

ShoreEuropeUnited States

Region of Domicile

Lo

ca

tio

n o

f A

ss

ets

Total Assets of Hedge Fundsby Domicile and Asset Location

Source: Hedgefunds.net and MI staff estimates

Credit to Households:Retail Loan Penetration Percent of GDP

Source: Merrill Lynch, 2006

Credit to Households:Market Loan Penetration Percent of GDP

Source: Merrill Lynch, 2006

Debit and Credit Card Penetration 2005

Source: Wall Street Journal, March 20, 2007

5444 44

3

71

174

61

0

40

80

120

160

200

S. Korea Brazil China Thailand Mexico Poland India

Percentage of Population

Credit Card Usage to GDP

FinlandNewZealand

Hong KongFrance

U.S.Sweden

IsraelAustralia

IcelandNorway

21

20

19

18

17

16

15

14

Percent of GDP

1515

161616

1718

2020

20

Source:

Remittances Are the Largest Sourceof External Financing in Developing Countries

Source: Global Economic Prospects 2006: Economic Implications of Remittances and Migration (World Bank), World Development

Indicator s 2006, and Global Development Finance 2006

Total Remittances (includingestimated unrecorded remittance)

$199 billion

Remittance to Selected LAC Countriesin 2006

Source: Inter-American Development Bank

23,053

7,373

4,200 3,610 3,316 2,900 2,900

0

5,000

10,000

15,000

20,000

25,000

Mexico Brazil Colombia Guatemala El

Salvador

Ecuador Dominican

Repulic

US $ Millions

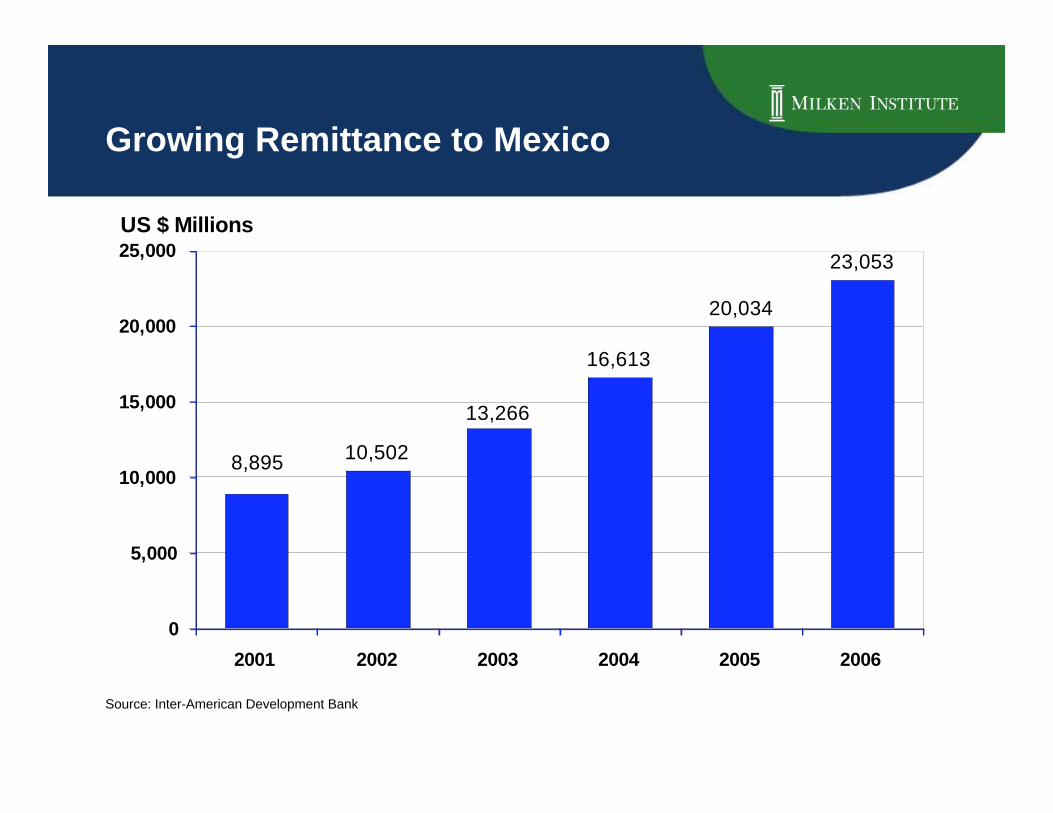

Growing Remittance to Mexico

Source: Inter-American Development Bank

10,502

16,613

20,034

23,053

13,266

8,895

0

5,000

10,000

15,000

20,000

25,000

2001 2002 2003 2004 2005 2006

US $ Millions

Remittance to Latin Americafrom the U.S. in 2006 (US$ Millions)

Source: Inter-American Development Bank

CA$13,191

TX$5,222

NY$3,714

Total:

>$45 billion

0

100

200

300

400

500

600

700

Jan. 85 - Dec. 94Jan. 95 - Dec. 04

Jan. 05 - Mar. 07

Media and Ent.

High Technology

Real Estate

Retail

Healthcare

Energy and Power

Other

US$ Billions

U.S. LBO by Target Industry

Source: SDC

Of which37% wereConsumer

Stable Of which35% wereIndustrial

$506

$307

$653

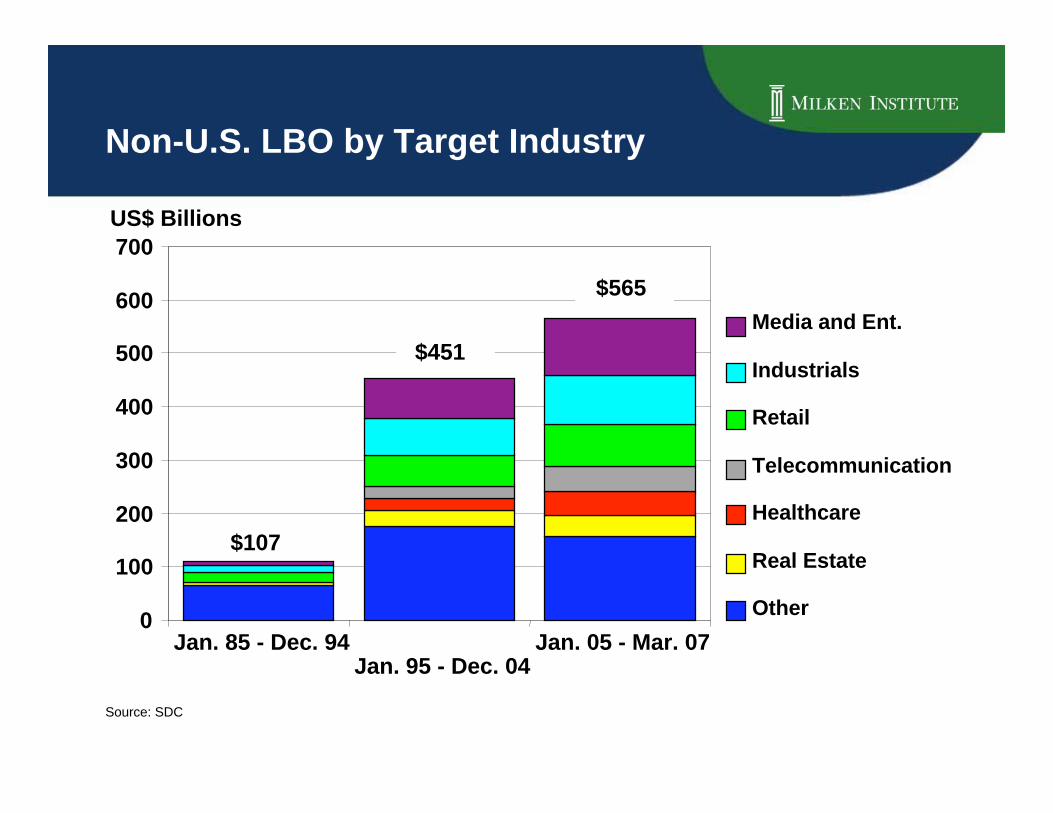

Non-U.S. LBO by Target Industry

Source: SDC

0

100

200

300

400

500

600

700

Jan. 85 - Dec. 94Jan. 95 - Dec. 04

Jan. 05 - Mar. 07

Media and Ent.

Industrials

Retail

Telecommunication

Healthcare

Real Estate

Other

$107

$565

$451

US$ Billions

© 2006 Reproduction or quotation is prohibited withoutthe express written consent of Chicago Climate Exchange,Inc.

Chicago Climate Exchange®

The Use of Markets to SolveEnvironmental Problems and Create Private Wealth

Wealth Creation in the U.S.since World War II

• 1945-70 Manufacturing

• 1970’s Inflation

• 1980’s Asset, liability mgmt., derivatives,commoditization of mortgages and bank debt(Junk Bonds)

• 1990’s High tech, Telecom

• 2000’s Commoditization of air and water

The Commoditization of Air & Water

• Clean Air Act Amendments of 1990 - SO2emission allowance trading

• Kyoto Protocol of 1997 - Greenhouse gas (GHG)emission trading

• Launch of the Chicago Climate Exchange, 2003

• Launch of the Chicago Climate FuturesExchange, 2004

• Water markets – in the Southwest and the GreatLakes

Why Carbon Emissions Trading?

• Proven, least-cost, and comprehensive tool for managingemissions: (CCX as an Emissions Management System)

• Environmental stewardship that rewards environmentalinnovation and strategic planning

• Flexibility, market efficiencies

• Multiple successes: US SO2, lead phase-out (gasoline), NOx,ETS

• Enhances coherent management practices and technologicalinnovation

• Establish value to scare resource

• Carbon price signal

• Reveals hidden assets and hidden costs throughoutoperations

What is the Chicago ClimateExchange?

• The Chicago Climate Exchange (CCX ®) is a

– financial institution which administers the

– world’s first and North America’s only voluntary,legally binding cap and trade system to reduceemissions of all six greenhouse gases, with offsetprojects in North America and worldwide

Role of Price Discovery

• To stimulate inventive activity

• To reorganize corporate financial decision-making

• To monetize hidden assets

Environmental Markets on the Horizon

Water• Western United States

– Snowpack could be reduced by 25% by 2050 in California dueto climate change

– Colorado River delivery system fully allocated and on the brinkof failure

– Runoff declining while demand is increasing

– Water already extensively litigated with more to come

• Northern China

– Has been warned of a water crisis by 2030 when per capitaconsumption is expected to fall below the internationallyrecognized standard for shortage

– Rivers are heavily polluted

– Agriculture impossible in certain regions

Environmental Markets on the Horizon

Water• Middle East

– Water scarcity a significant political issue

– Need to develop peaceful, sustainable solutions between Jordan, Syria,Israel, Palestine, other countries

– Great need for a comprehensive water plan for the countries to sharethe resource

• Africa

– Climate change anticipated to reduce precipitation in regions near theequator

– Water quality problems lead to millions of deaths by infants every year

• Non GHG Pollutants

• Wildlife and Endangered Species

Corporate credit is increasingly tradedin derivative form

0 200 400 600 800 1000 1200 1400

Investmentgrade creditbonds

Credit defaultswaps

US$ billions

Absolute growth (% of baseyear)

Compound Annual GrowthRate

2002

2006

200%

32%

2002

2006

-10%

-2%

Investment grade credit bonds vs. credit default swap trading volumes

North America

Source: Greenwich Associates

Derivatives are de-riskingthe mortgage market

Mortgage derivatives vs. securities volumes

U.S.

Source: Bond Market Association, Isda

Absolute growth (% of baseyear)

Compound Annual GrowthRate

US$ billions

2006

2007F

2007F

2005

2000

191%

519%

87%

191%

149%

11%

0 100 200 300 400 500 600 700 800 900 1000

New Issuanceof AgencyMBS

Volume of Single-name ABS CDSTraded

Volume of ABXTraded

2006

Risk-transfer technology is freeing-upcapital for corporate financing

Source: Bond Market Association, Isda

US$ billions

Absolute growth (% of base year) Compound Annual Growth Rate

2000

2000

2000

2007F

2007F

2007F

633%

3210%

342%

33%

24%

65%

0 50 100 150 200 250 300 350

New IssuanceVolumes for allCDOs

New IssuanceVolumes forStructuredProducts

New IssuanceVolumes for allCLOs

The Role of Risk-transfer Technologyin Meeting the Challenges of Climate Change

United Nations Framework Convention on Climate Change

MT millions

0

20

40

60

80

100

120

140

Q1' 05 Q2' 05 Q3' 05 Q4' 05 Q1' 06 Q2' 06 Q3' 06 Q4' 06 Q1' 07

Cumulative Estimated Annual Reductions of Registered projects since 1/1/05

Cumulative CER issuance since 1/1/05

The Role of Risk-transfer Technologyin Meeting the Challenges of Climate Change

United Nations Framework Convention on Climate Change

Registered project activities by host party, Total: 632