financial instability and the fed’s crisis response

TRANSCRIPT

Financial Instability and the Fed’s Crisis Response

James Andrew Felkerson

Bard College

Fed Balance Sheet 2008-

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

20

08

-01

-02

20

08

-03

-12

20

08

-05

-21

20

08

-07

-30

20

08

-10

-08

20

08

-12

-17

20

09

-02

-25

20

09

-05

-06

20

09

-07

-15

20

09

-09

-23

20

09

-12

-02

20

10

-02

-10

20

10

-04

-21

20

10

-06

-30

20

10

-09

-08

20

10

-11

-17

20

11

-01

-26

20

11

-04

-06

20

11

-06

-15

20

11

-08

-24

20

11

-11

-02

20

12

-01

-11

20

12

-03

-21

20

12

-05

-30

20

12

-08

-08

20

12

-10

-17

20

12

-12

-26

20

13

-03

-06

20

13

-05

-15

20

13

-07

-24

20

13

-10

-02

20

13

-12

-11

20

14

-02

-19

20

14

-04

-30

20

14

-07

-09

20

14

-09

-17

Total Assets

Loans

Federal Ageny Debt Securities

Agency MBS

Treasuries

Repo

Other Credit

Introduction

• Two tools:– Interest Rates

– Large Scale Asset Purchases (LSAPs)• So-called “QE”

• My interest is with the effects of LSAPs on systematic risk.

• Interest rates come into the picture and may be important for other reasons, but will not be emphasized here.

Interest Rates Since the Crisis

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

20

08

-01

-01

20

08

-04

-01

20

08

-07

-01

20

08

-10

-01

20

09

-01

-01

20

09

-04

-01

20

09

-07

-01

20

09

-10

-01

20

10

-01

-01

20

10

-04

-01

20

10

-07

-01

20

10

-10

-01

20

11

-01

-01

20

11

-04

-01

20

11

-07

-01

20

11

-10

-01

20

12

-01

-01

20

12

-04

-01

20

12

-07

-01

20

12

-10

-01

20

13

-01

-01

20

13

-04

-01

20

13

-07

-01

20

13

-10

-01

20

14

-01

-01

20

14

-04

-01

20

14

-07

-01

30yr Conventional Mortgage

Effective Fed Funds Rate

10yr Treasury Constant Maturity

Target FF (Upper band)

LSAPs Since the Crisis

• Contention between the distinction between “pure QE” and LSAPs (credit easing)

• From Bernanke, “The Crisis and the Policy Response:– “…in a pure QE regime the focus of policy is the

quantity of bank reserves; the composition of loans and securities on the asset side of the central bank’s balance sheet is incidental.”

– “In contrast, the Federal Reserve’s credit easing approach focuses on the mix of loans and securities it holds and on how this composition of assets affects credit conditions for households and businesses.”

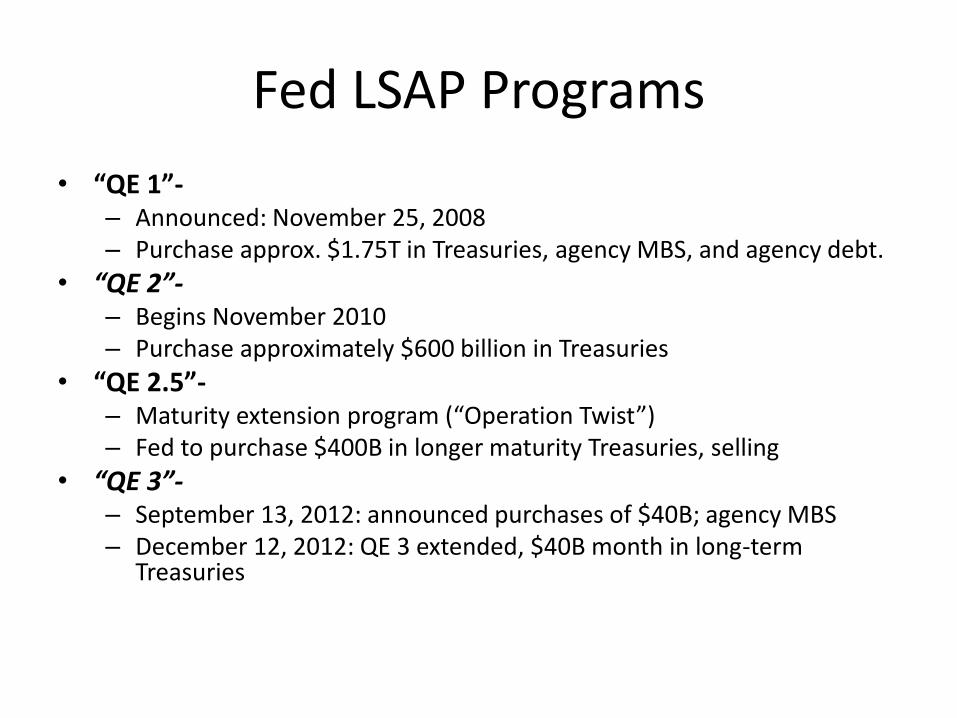

Fed LSAP Programs

• “QE 1”-– Announced: November 25, 2008– Purchase approx. $1.75T in Treasuries, agency MBS, and agency debt.

• “QE 2”-– Begins November 2010– Purchase approximately $600 billion in Treasuries

• “QE 2.5”-– Maturity extension program (“Operation Twist”)– Fed to purchase $400B in longer maturity Treasuries, selling

• “QE 3”-– September 13, 2012: announced purchases of $40B; agency MBS– December 12, 2012: QE 3 extended, $40B month in long-term

Treasuries

Global LSAP Programs

Central Bank Peak size (billion USD) Share of economy (%)

Federal Reserve $3,152 22.1

BOE $596 26.3

ECB $432 3.5

BOJ $2,193 37.3

Source: Fawley and Neely, 2013, “Four Stories of Quantitative Easing”***Numbers as of end of 2012***

MBS Issuance 1996-

0.0

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

3500.0

4000.0

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Total mortgage-related issuance

Agency MBS

Agency CMO

Nonagency MBS

85

90

95

100

105

1101

/3/1

1

2/3

/11

3/3

/11

4/3

/11

5/3

/11

6/3

/11

7/3

/11

8/3

/11

9/3

/11

10

/3/1

1

11

/3/1

1

12

/3/1

1

1/3

/12

2/3

/12

3/3

/12

4/3

/12

5/3

/12

6/3

/12

7/3

/12

8/3

/12

9/3

/12

10

/3/1

2

11

/3/1

2

12

/3/1

2

1/3

/13

2/3

/13

3/3

/13

4/3

/13

5/3

/13

6/3

/13

7/3

/13

8/3

/13

9/3

/13

10

/3/1

3

11

/3/1

3

12

/3/1

3

1/3

/14

FHLMC 30yr Pass Throughs, Last and Fed Purchase Prices

2.5 last 3.0 last 3.5 last 4.0 last 4.5 last 2.5 purchase 3.0 purchase 3.5 purchase 4.0 purchase 4.5 purchase

85

90

95

100

105

1101

/3/1

1

2/3

/11

3/3

/11

4/3

/11

5/3

/11

6/3

/11

7/3

/11

8/3

/11

9/3

/11

10

/3/1

1

11

/3/1

1

12

/3/1

1

1/3

/12

2/3

/12

3/3

/12

4/3

/12

5/3

/12

6/3

/12

7/3

/12

8/3

/12

9/3

/12

10

/3/1

2

11

/3/1

2

12

/3/1

2

1/3

/13

2/3

/13

3/3

/13

4/3

/13

5/3

/13

6/3

/13

7/3

/13

8/3

/13

9/3

/13

10

/3/1

3

11

/3/1

3

12

/3/1

3

1/3

/14

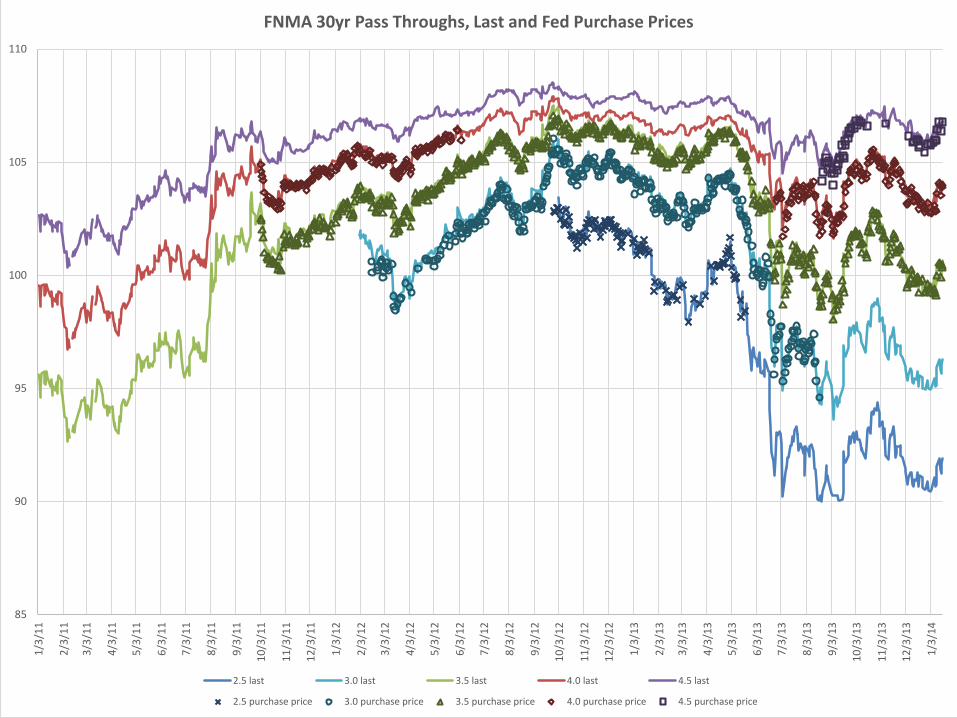

FNMA 30yr Pass Throughs, Last and Fed Purchase Prices

2.5 last 3.0 last 3.5 last 4.0 last 4.5 last

2.5 purchase price 3.0 purchase price 3.5 purchase price 4.0 purchase price 4.5 purchase price

90

95

100

105

110

1151

/3/1

1

2/3

/11

3/3

/11

4/3

/11

5/3

/11

6/3

/11

7/3

/11

8/3

/11

9/3

/11

10

/3/1

1

11

/3/1

1

12

/3/1

1

1/3

/12

2/3

/12

3/3

/12

4/3

/12

5/3

/12

6/3

/12

7/3

/12

8/3

/12

9/3

/12

10

/3/1

2

11

/3/1

2

12

/3/1

2

1/3

/13

2/3

/13

3/3

/13

4/3

/13

5/3

/13

6/3

/13

7/3

/13

8/3

/13

9/3

/13

10

/3/1

3

11

/3/1

3

12

/3/1

3

1/3

/14

GNMA I 30yr Pass Throughs, Last and Fed Purchase Prices

3.0 close 3.5 close 4.0 close 3.0 purchase price 3.5 purchase price 4.0 purchase price

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

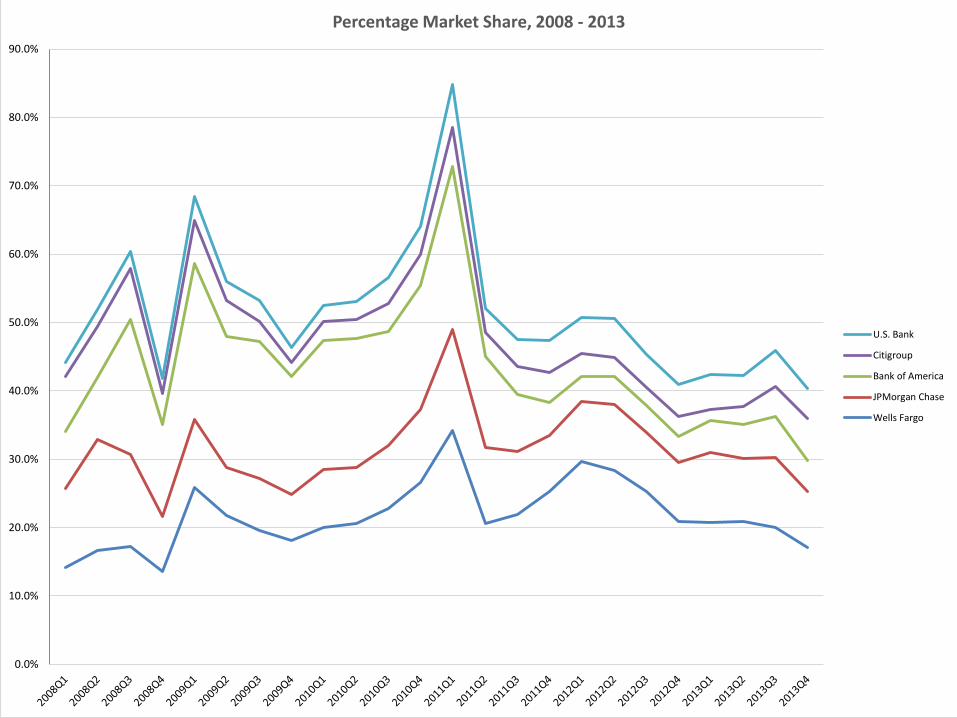

Percentage Market Share, 2008 - 2013

U.S. Bank

Citigroup

Bank of America

JPMorgan Chase

Wells Fargo

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

1000.0

Total Quarterly Mortage Orginations, in billions

Total originations

U.S. Bank

Citigroup

Bank of America

JPMorgan Chase

Wells Fargo

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

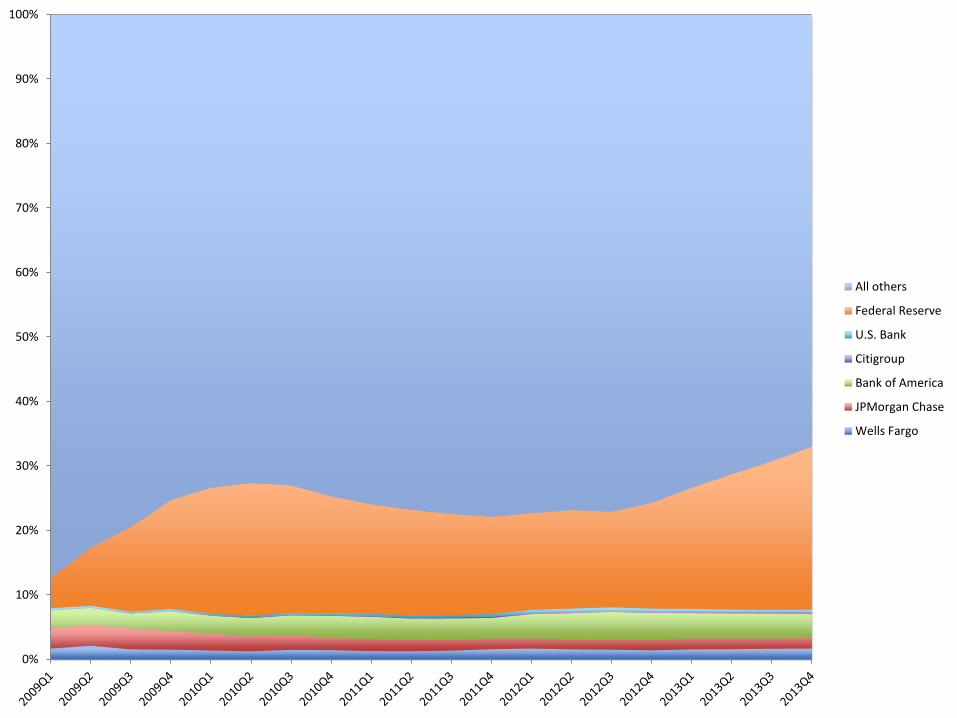

All others

Federal Reserve

U.S. Bank

Citigroup

Bank of America

JPMorgan Chase

Wells Fargo

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

Percentage of Total U.S. Depository Institution Agency MBS Holdings by Five Largest Mortgage Originators

C

USB

JPM

WFC

BAC

0.000

0.200

0.400

0.600

0.800

1.000

1.200

1.400

1.600

1.800

2.000

Ratio of Agency MBS UPB to Total Equity (Regulatory) Capital

Wells Fargo

JP Morgan

Bank of America

Citigroup

US Bank

-

200.00

400.00

600.00

800.00

1,000.00

1,200.00

1,400.00

1,600.00

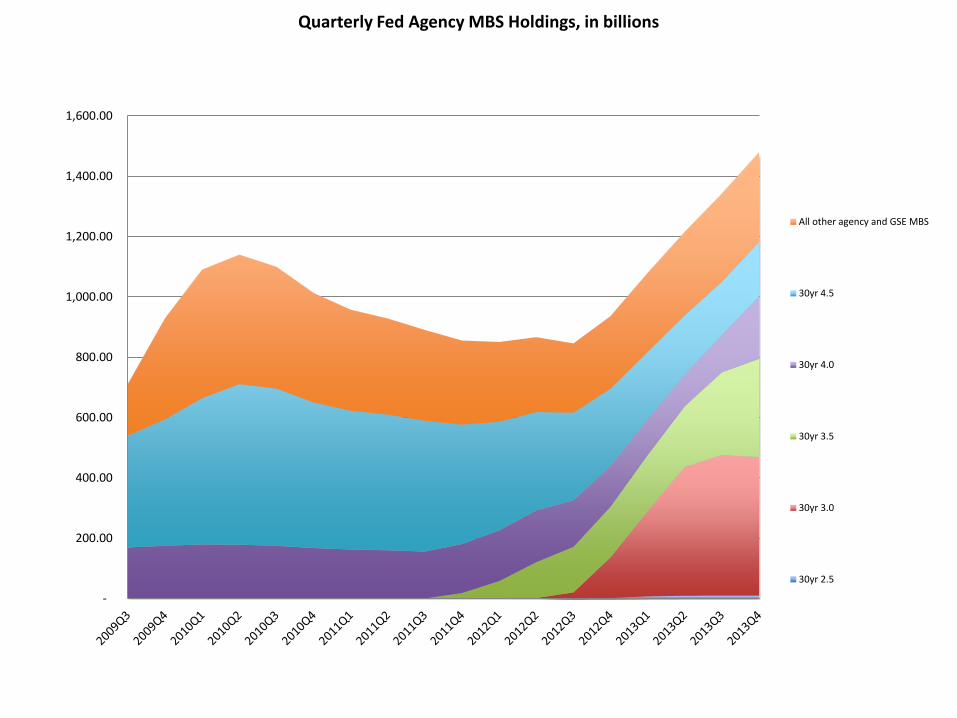

Quarterly Fed Agency MBS Holdings, in billions

All other agency and GSE MBS

30yr 4.5

30yr 4.0

30yr 3.5

30yr 3.0

30yr 2.5

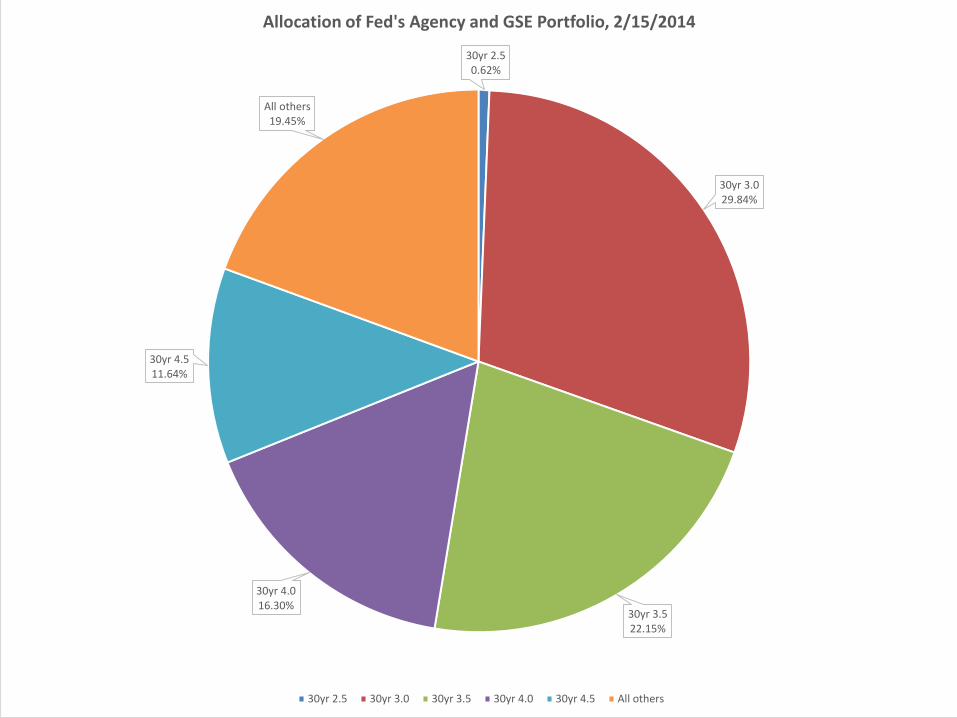

30yr 2.50.62%

30yr 3.029.84%

30yr 3.522.15%

30yr 4.016.30%

30yr 4.511.64%

All others19.45%

Allocation of Fed's Agency and GSE Portfolio, 2/15/2014

30yr 2.5 30yr 3.0 30yr 3.5 30yr 4.0 30yr 4.5 All others

-12.00% -10.00% -8.00% -6.00% -4.00% -2.00% 0.00% 2.00%

FNMA 30yr 2.5

FHLMC 30yr 2.5

FNMA 30yr 3.0

FHLMC 30yr 3.0

GNMA 30yr 3.0

GNMA 30yr 2.5

GNMA 30yr 3.5

FHLMC 30yr 3.5

FNMA 30yr 3.5

GNMA 30yr 4.0

FNMA 30yr 4.0

FHLMC 30yr 4.0

GNMA 30yr 4.5

FNMA 30yr 4.5

GNMA 30yr 6.0

FHLMC 30yr 4.5

GNMA 30yr 6.5

GNMA 30yr 5.0

GNMA 30yr 5.5

FHLMC 30yr 5.0

FNMA 30yr 5.0

FNMA 30yr 6.5

FHLMC 30yr 5.5

FNMA 30yr 5.5

FHLMC 30yr 6.5

FNMA 30yr 6.0

FHLMC 30yr 6.0

% Gain/ Loss GSE and Agency Pass Throughs

% Change from 1/1/2013 % Change from 1/1/2012

Final Considerations

• Must consider Treasury/Congress actions: most importantly the significant increase in conforming loan limits during crisis; allowed banks to move mortgages off balance sheet.

• But, the Fed encouraged the production of mortgages, which benefits banks:– By providing a residual buyer– By protecting banks initially from contraction

(prepayment) risk and, now, from extension (contraction risk)

• But, in the end, are we done with Fed intervention in mortgage markets?