financial intermediaries and international risk premia · financial intermediaries and...

TRANSCRIPT

Financial Intermediaries and International Risk Premia

Kyriakos Chousakos∗

October 2017

Abstract

I propose a measure of adjusted leverage as a proxy for the pricing kernel of a representative financialintermediary. Using a simple theoretical framework with information production, I show that in states ofthe world where credit outstanding in the economy is low, financial leverage is not an accurate proxy forthe stochastic discount factor of financial intermediaries. Empirical evidence confirms this theoreticalfinding for an international panel of financial intermediaries. Credit outstanding arises as an importantdeterminant of the stochastic discount factor of a financial intermediary. As a result, the new proposedmeasure incorporates information on both intermediaries’ financial leverage and the amount of credit inthe economy. It is an economically meaningful state variable that is pro-cyclical and predicts financialcrises. I show that a global adjusted leverage factor prices currency portfolios and global equity portfoliosoutperforming benchmark factor models designed to price these assets.

Keywords: Asset Pricing, International Financial Markets, Financial IntermediariesJEL Classification: G2, G12, G15, G24

∗Yale University. Email: [email protected]. I am grateful to my advisors Gary Gorton, Tobias Moskowitz, andJonathan Ingersoll for their guidance and invaluable comments. I thank Oliver Boguth (discussant), Robin Greenwood, TylerMuir (discussant), and Guillermo Ordoñez for helpful comments and suggestions. I also thank Thomas Bonzcek, Arun Gupta,Toomas Laarits, Avner Langut, Adriana Robertson, and participants of the 5th Annual USC Marshall PhD Conference inFinance, the PhD Session of the 2017 Northern Finance Association Annual Conference, and the PanAgora 2017 Crowell PrizeSeminar Series for useful comments. All errors remain my own.

1 Introduction

Financial intermediaries are the primary participants in capital markets. In the foreign exchange market,

international commercial banks acting as securities dealers account for more than 51% of all transactions.1

In the equities market, over the past decades households have been steadily decreasing their direct stock

holdings, while financial intermediaries have been filling the void.2 In the bond market, almost all of the

trading takes place between broker-dealers and large institutional investors in over-the-counter markets.3

Financial intermediaries are sophisticated market participants that carry out complex trading strategies, face

low transactions costs, and continuously update their strategies as new information becomes available. As

a result, financial intermediaries are ideal candidates for the role of the marginal investor in a wide array

of markets which means that their marginal value of wealth is expected to price financial assets in these

markets.4

In this paper, I improve on existing intermediary asset pricing models and study the impact of financial

intermediaries on global capital markets. More specifically, shifting the focus from U.S. only to international

financial intermediaries, I propose and test an empirical proxy for the pricing kernel of a representative global

financial intermediary. This proxy in addition to financial leverage takes into account the amount of credit in

the economy. This is motivated by a simple theoretical framework with information production in which credit

outstanding in the economy along with financial leverage arises as an important determinant of the stochastic

discount factor (SDF) of financial intermediaries. Empirical evidence presented in the paper confirms this

theoretical finding. The proposed measure is an adjusted leverage index which incorporates information

on intermediaries’ financial leverage and the availability of credit in the economy. I show that adjusted

leverage is an economically meaningful state variable that is pro-cyclical and predicts financial crises and

future consumption levels. I find that a global adjusted leverage factor prices currency portfolios and global

equity portfolios outperforming benchmark factor models designed to price these assets. A decomposition of

the global adjusted leverage factor into non-U.S. and U.S. only components reveals that non-U.S. financial

intermediaries are marginal investors in foreign exchange markets as well as in global equity markets.

To motivate the empirical work of this paper, I develop a simple theoretical framework in the spirit

of Gorton and Ordoñez (2014) and Gorton and Ordoñez (2016). The economy comprises three agents –

firms, financial institutions, and households – all of which are risk neutral with respect to lending activities1See, the foreign exchange turnover section of the triennial central bank survey conducted by the Bank for International

Settlements (BIS) in September 2016 (www.bis.org/publ/rpfx16fx.pdf).2See, e.g. Allen (2001), and Sneider et al. (2013).3See, e.g. Edwards et al. (2007) for a breakdown of the percentage of bonds traded over-the-counter and in NYSE.4A growing stream of the literature, both theoretical and empirical, studies the relation between financial intermediaries and

asset prices. I discuss the different approaches in Section 2.

1

with the exception of financial institutions which are risk averse with regard to holding firms’ equity.5 To

produce output, firms need to borrow capital from households through the financial system posting land

as collateral. Both households and financial institutions may produce information regarding the quality of

the collateral backing deposits and loans respectively with the cost of producing information for households

being significantly higher compared to that for financial institutions.6 In this setting, information production

regulates the amount of credit outstanding and deposits in the economy. Both quantities are an increasing

function of expected output and their respective rates of increase depend on the current information production

regime.

In this framework, I show that the relation between the SDF, as described in the model by the marginal

value of wealth of a financial institution, and its financial leverage is not one-to-one and strongly depends on

the level of credit outstanding. An increase in financial leverage does not necessarily indicate a decrease in the

marginal value of wealth for the financial institution. This is primarily observed in times of economic growth,

where credit outstanding is high and financial intermediaries sustain high financial leverage and low marginal

value of wealth as a result of the ample investment opportunities which they can undertake. However, this

is not the case in times of recessions or financial crises, where the amount of credit outstanding is low. In

such times both financial leverage and the marginal value of wealth of a financial institution increase as a

result of an increase in deposits not followed by a similar increase in loans and profitability. According to the

theoretical framework discussed above, it is possible that in a low credit environment an increase in leverage

is associated with an increase in the marginal value of wealth of the financial institution. This implies that

financial leverage is not an accurate empirical proxy for the SDF of a financial intermediary. A number of

empirical findings, summarized below, corroborate this theoretical proposition.

Assets that co-vary with intermediaries’ SDF are riskier and investors require higher premia to compensate

for that risk. In the literature the SDF of financial intermediaries is proxied by leverage innovations of

financial intermediaries (see, e.g. Adrian et al. (2014)) or its reciprocal capital ratio innovations (see, e.g. He

et al. (forthcoming)). I empirically show that for an international panel of countries financial leverage interacts

differently with key characteristics of financial intermediaries, such as future financial assets and stock market

returns, depending on the level of credit outstanding in the economy. When the credit outstanding is high,

financial leverage is positively correlated with the level of future assets reflecting a higher risk bearing capacity

and negatively correlated with market returns indicating lower risk for such investments. On the other hand,5This assumption is primarily motivated by the third Basel Accord (Basel III) according to which secure debt is considered

to be more liquid than equity and as a result the capital requirements for financial institutions holding equities in their balancesheets are higher compared to these for secure debt assets.

6Financial institutions possess superior technology and resources in identifying the quality of collateral posted by firmscompared to that of households.

2

when the credit outstanding in the economy is low the opposite holds true. This finding suggests that a

potential proxy for the SDF of financial intermediaries ought to take into account credit outstanding in the

economy.

I construct a proxy for intermediaries’ SDF by combining information on financial leverage of broker-

dealers with information on economy-wide credit-to-private sector. More specifically, first, I compute a

measure of global financial leverage as the aggregated country level financial leverage weighted by the level of

financial assets of each country. Second, I compute a global measure of credit-to-private sector by aggregating

country level credit-to-private sector figures again weighted by the level of financial assets of each country.

Finally, the global adjusted leverage measure is equal to the negative global leverage innovations when global

credit is less than a threshold value and equal to global leverage innovations otherwise. The threshold is set

at the 25th percentile of a rolling window on the global credit series.

This adjusted leverage measure is directly related to business cycles. Consistent with theoretical and

empirical work suggesting that the marginal value of wealth of a financial intermediary is pro-cyclical (see, e.g.

Brunnermeier and Pedersen (2009) and Adrian and Shin (2010)), adjusted leverage is positively correlated with

changes in real GDP, capital formation, and total factor productivity (TFP) at a country level. In addition,

it predicts financial crises and future levels of durables and non-durables consumption. The relation between

adjusted leverage and business cycles implies that it is an economically meaningful measure summarizing

various aspects of economic activity related to financial intermediaries’ marginal value of wealth. Based on

these properties I argue that this measure can be employed as a reasonable proxy for the SDF of financial

intermediaries.

Using a single factor model, I perform cross-sectional asset pricing tests across a set of international asset

classes. I find that excess returns of currency portfolios and international equity portfolios can be explained

by their exposure to global adjusted leverage. More specifically, the global adjusted leverage factor appears

with a significantly positive price of risk consistently across all test assets. The global adjusted factor model

outperforms benchmark models (see, e.g. Lustig et al. (2011), Menkhoff et al. (2012a), and Menkhoff et al.

(2012b)) which aim to explain the cross-section of currency portfolios, and performs similarly to standard

multifactor models, such as the Fama-French global three factor plus momentum model, which aim to explain

the cross-section of international equity portfolios. The positive price of risk across asset classes is consistent

with the theoretical framework developed in this paper where assets that co-vary with intermediaries’ SDF

are associated with a higher risk premium. My findings suggest that the marginal value of wealth of financial

intermediaries is indeed an important determinant of asset prices.

3

A common criticism of cross-sectional asset pricing tests is that mis-estimated exposures (betas) in the

time-series regressions could be explaining a spurious relationship in the cross-section of returns (see, e.g.

Lewellen et al. (2010)). I address many of the concerns voiced in Lewellen et al. (2010) by conducting a

number of robustness checks. First, I estimate the exposures of test portfolios on the global leverage factor

and find that the adjusted leverage betas increase in a pattern consistent with an increasing adjusted leverage

being associated with higher premia. Second, I construct an adjusted leverage factor-mimicking portfolio and

repeat the asset pricing tests using a longer time-series. The price of risk of the global adjusted leverage

factor remains significantly positive across all test assets with the exception of momentum portfolios. Third,

I perform beta sorts to address the potential criticism that my results only hold for portfolios used in the

tests. I estimate the exposure of country-level market portfolios and country-level financial sector portfolios

on the adjusted leverage factor-mimicking portfolio and measure the spread in average returns of these

portfolios. The resulting spread is positive, suggesting that the adjusted leverage factor is truly priced in the

cross-section. Finally, for all cross-sectional asset pricing tests, I measure the fraction of instances where

a randomly generated factor achieves an explanatory power higher than and pricing error lower than that

generated by the global adjusted leverage factor. I find that for the majority of test assets this fraction is

extremely low (less than 1%).

A number of factors aiming to capture the marginal value of wealth of financial intermediaries have

been proposed in the literature. Adrian et al. (2014) propose a single-factor intermediary SDF. The factor is

a time-series of the shocks to the leverage of securities broker-dealers and carries a large and significantly

positive price of risk. On the other hand, He et al. (forthcoming) propose as a two-factor intermediary SDF.

The first factor is the market and the second is a time-series of the shocks to the equity capital ratio of primary

dealer counterparties of the New York Federal Reserve. Using an extensive set of test assets the authors show

that it carries a consistently positive price of risk. I compare the explanatory power of the global adjusted

leverage factor against that of the factors proposed by Adrian et al. (2014) and He et al. (forthcoming). I

find that the global adjusted leverage factor appears with a consistently positive price of risk across all test

assets and that it outperforms both the leverage factor and the capital factor in the cross-section currencies

and global equities. The better performance of the adjusted leverage factor as compared to that of other

factors proposed in the literature implies that this factor is a more accurate state variable reflecting global

financial intermediaries’ SDF.

This paper is organized as follows: Section 2 discusses the related literature and the contribution of the

paper; Section 3 develops a theoretical framework that motivates the empirical work; Section 4 presents the

data sources; Section 5 presents the construction of the adjusted leverage factor and discusses its properties;

4

Section 6 discusses the empirical methodology and how it relates to theory; Section 7 shows the main findings

of the paper; Section 8 revisits the empirical findings under alternative theoretical frameworks, compares the

performance of global adjusted leverage against other measures proposed in the literature, and decomposes

global adjusted leverage into a non-U.S. and a U.S. only component; and finally Section 9 concludes the

paper.

2 Related Literature and Contribution

This paper is closely related to two main streams of the literature.

First, a large stream of literature studies the relation between financial intermediaries and asset prices.7

Financial institutions are the class of investors whose characteristics most closely align with those of a

representative investor in traditional asset pricing models, and thus the study of their marginal value of wealth

is expected to provide a more instructive stochastic discount factor (SDF).8 Models of intermediary-based

asset pricing link the marginal value of wealth to intermediaries’ funding constraints implying that marginal

utility is high when funding constraints are binding (see, e.g. Brunnermeier and Pedersen (2009), Geanakoplos

(2010), Gromb and Vayanos (2002), and Shleifer and Vishny (1997)). A common theme across these models

is a pro-cyclical intermediary leverage, which implies a positive price of risk.9 In line with this stream of

research, Gabaix and Maggiori (2015) develop a model of exchange rate determination based on capital flows

in financial markets with frictions. Empirically, Adrian and Shin (2010) show that financial intermediaries

adjust their leverage actively according to economic conditions resulting in pro-cyclical leverage. Adrian

et al. (2014) and He et al. (forthcoming) show that shocks to the leverage and capital ratios of financial

intermediaries, respectively, explain a large portion of the cross-sectional variation in the expected returns of

an array of asset classes.10 Finally, DellaCorte et al. (2016a), focusing on the currency market, show that a

global imbalance risk factor (see, e.g. Gabaix and Maggiori (2015)) explains the cross-sectional variation in

currency excess returns.

The contribution of this paper to the financial intermediation literature is twofold. On the theory side,

I deviate from the intermediary-based asset pricing models mentioned above by introducing information7Financial intermediaries play a central role in modern markets. The importance of this role and the need for additional

research has been part of past AFA presidential addresses (see, e.g. Allen (2001), Duffie (2010), Cochrane (2011)).8This approach is in contrast to conventional consumption-based asset pricing models where the marginal investor is the

household (see, e.g. Campbell and Cochrane (1999) and Bansal and Yaron (2004)). Households exhibit limited stock marketparticipation (see, e.g. Vissing-Jørgensen (2002)), pay higher transactions costs, and exhibit a lack of financial sophistication(see, e.g. Calvet et al. (2007)).

9On the other hand, He and Krishnamurthy (2013) and Brunnermeier and Sannikov (2014) propose a central role forintermediaries’ wealth and generate a countercyclical intermediary leverage (negative price of risk).

10Etula (2013), Adrian et al. (2015), Adrian et al. (2013) show that the risk-bearing capacity of U.S. securities broker-dealersis a strong predictor of asset returns (commodities, currencies, equities, and bonds).

5

production by the agents in the economy as in Gorton and Ordoñez (2014) and Gorton and Ordoñez

(2016). More specifically, I propose an alternative mechanism where information production in the economy

determines the amount of credit outstanding in the economy and subsequently the level of financial leverage

and the SDF of financial intermediaries. On the empirical side, I expand the focus from U.S. to international

financial intermediaries, and propose and test the asset pricing properties of an empirical proxy for the

SDF of a global financial intermediary. This measure captures multiple aspects of economic activity ranging

from capital formation to financial crises and future consumption. The paper establishes an economically

meaningful link between the marginal value of wealth of a global financial intermediary and asset prices, thus

relating asset prices to the macroeconomy through the financial intermediaries’ pricing kernel. I deviate from

previously used methodologies in both the dimensions of variable construction and scope of test assets. The

measure of adjusted leverage is computed by aggregating granular (balance sheet) information in tandem

with information on credit-to-private sector from a wide array of countries. This method allows me to obtain

a more accurate representation of the SDF of financial institutions on a global level, since I combine two

pieces of information (balance sheet information and aggregate credit conditions), which leads to a greater

explanatory power over the cross-section of returns.11

Second, another large stream of literature studies international assets’ excess returns. The literature

around currency excess returns has focused on portfolio strategies based on currency characteristics, such as

the interest rate differential (carry trade (see, e.g. Hansen and Hodrick (1980), Meese and Rogoff (1983),

Fama (1984), Koijen et al. (2016))), past returns (momentum and value (see, e.g. Menkhoff et al. (2012b)

and Asness et al. (2013))), and global foreign exchange volatility. Explanations for currency premia include

aggregate consumption growth risk (see, e.g. Lustig and Verdelhan (2007)), currency crash risk and peso

problems (see, e.g. Brunnermeier et al. (2008), Burnside et al. (2011a) and Burnside et al. (2011b)), global

risk (see, e.g. Lustig et al. (2011)), habits (see, e.g. Verdelhan (2010)), and rare disasters (see, e.g. Farhi and

Gabaix (2016))12 The literature around international equity excess returns has focused on documenting the

existence of size, value, and momentum premia in equity markets across the world (see, e.g. Griffin (2002) and

Fama and French (2012)). Global versions of the Fama French three-factor model can explain a large part of

variation in international equity excess returns (see, e.g. Fama and French (2012)). Alternative explanatory

factors related to funding constraints of investors in international financial markets explain cross-country11Prior empirical research uses as proxies for the marginal value of wealth of financial intermediaries the changes in the

leverage ratio (see, e.g. Adrian et al. (2014)), or a measure of the intermediary capital ratio (see, e.g. He et al. (forthcoming)without taking into account the level of the available credit in the economy. The importance of high leverage or low availablecapital varies with respect to the available level of credit in the economy. The marginal utility of an intermediary when bothleverage and credit are high is not the same as when leverage is high and credit is low. In the second case the marginal utility ofan intermediary is higher.

12Additional explanations include the term structure (see, e.g. Bansal (1997), country-specific characteristics such as per-capitaGDP and inflation (see, e.g. Bansal and Dahlquist (2000)), currency volatility (see, e.g. Menkhoff et al. (2012a) and DellaCorteet al. (2016b)), downside risk CAPM (see, e.g. Lettau et al. (2014)), and global imbalances (see, e.g. DellaCorte et al. (2016a)).

6

variation in equity premia (see, e.g Goyenko and Sarkissian (2014) and Malkhozov et al. (2017)).

This paper contributes to the international finance literature and more specifically to the above mentioned

literature on risk factors associated with risk premia in currency and equity markets. I propose an alternative

explanation based on the role of financial intermediaries as marginal investors in these markets. This

explanation is based on an economically meaningful link between the marginal value of wealth of a global

financial institution and excess returns in the cross-section of currency and international equity portfolios.

3 Theoretical Framework

In this section, I develop a two period general equilibrium framework in the spirit of Gorton and Ordoñez

(2014) and Gorton and Ordoñez (2016).

3.1 Setting

The economy comprises three agents, each with a mass 1 – firms, financial institutions, and households –

and two types of goods – capital (numeraire) and land. All agents are risk neutral, apart from the financial

institutions which are risk neutral with regard to their lending activities and risk averse with regard to

holding firms’ equity. As in Gorton and Ordoñez (2014) only firms have access to managerial labor (L∗),

which combined with numeraire (K) produce more numeraire (K ′). The production process is stochastic

with Leontief technology:

K ′ =

A min{K,L∗} with prob. q

0 with prob. (1− q),

where A is a parameter determining output when production process is successful and q is the probability that

the production process is successful. For the purposes of this model I interpret q as the level of technological

innovation. A and q combined describe the efficiency of the production process.

Production is efficient (qA > 1) which means that the optimal amount of numeraire is K∗ = L∗. In this

economy, households begin with an endowment of numeraire K̄ > K∗ which can sustain optimal production.

Financial institutions are the sole owners of firm equity, which makes them the de-facto marginal investors.

Finally, firms own land and are endowed with numeraire in period 1 (K1) but have no means of capital

in period 2. Land is not used in production however it derives its value from the amount of numeraire it

7

produces at the end of the second period. If land is “good,” it yields C units of numeraire at the end of the

second period; if it is “bad,” it does not yield anything. Only a fraction p̂ of land is good.

In this economy, output and technological innovation (q) are non-verifiable, but the quality of land is not.

This makes land valuable as collateral. To receive capital necessary for production, firms pledge a fraction of

land as collateral for the loan they receive from the financial institution. This collateral is pledged in turn by

financial institutions to facilitate deposits from households. In this setting, C > K∗ which means that land

that is “good” can support the optimal capital size (K∗).

In period 1 the agents form beliefs about the fraction of land that is of good quality. To determine

the true quality of land with certainty, households must pay γh, while financial institutions must pay γb,

where γh > γb. This reflects the fact that financial institutions have superior technology compared to that of

households in determining the quality of collateral.

3.2 Optimal Loan for a Single Firm

Firms choose between debt that causes information production about the collateral leading to information-

sensitive debt, and debt that does not induce information production leading to information-insensitive debt.

Information acquisition for the financial institution bears a cost γb. As in Gorton and Ordoñez (2014), I

determine conditions under which debt is information-sensitive or information-insensitive.

3.2.1 Information-Sensitive Debt

In this case, financial institutions discover the true value of the firms’ land at a cost γb. Financial

institutions are risk neutral when it comes to their lending activity which means that they break even:

p(qRbIS + (1− q)xbISCf −Kb) = γb, (1)

where Kb is the actual loan from the financial institution to the firm, RbIS is the face value of the debt, and

xbIS is the fraction of land posted as collateral.

The fraction of collateral that a firm posts is determined by,

RbIS = xbISCf ⇒ xbIS = pKb + γb

pCf.13

13If RbIS > xbISCf , the firm would always hand over the collateral instead of repaying the loan. On the other hand, if

8

Expected profits (net of land value) are

E(π|p, IS) = p(qAKb − xbISCf ) = pK∗(qA− 1)− γb.14 (2)

3.2.2 Information-Insensitive Debt

In this case, financial institutions do not produce information regarding the quality of firms’ land. As

financial institutions are risk neutral with respect to their lending activity and break even,

qRbII + (1− q)pxbIICf = Kb, (3)

where RbII = pxbIICf as with the previous case.

Financial institutions could potentially deviate and privately check the quality of the land prior to

lending capital. The following condition guarantees that they will not deviate since the expected payoff from

producing information is less than the cost (γb):

p(qRbII + (1− q)xbIICf −Kb) < γb ⇒ (1− p)(1− q)Kb < γb.

The financial institution lends the optimal amount of capital (K∗) if the above condition is satisfied for

Kb = K∗. However, if the above condition is not satisfied, the amount of capital is Kb = γb

(1−p)(1−q) or pCf ,

if collateral value is low. Combining the above, the loan level for information-insensitive debt is:

Kb(p, q|II) = min

{K∗,

γb

(1− p)(1− q) , pCf

}. (4)

Expected profits (net of land value) are

E(π|p, II) = pqAKb − xbIIpCf = K(p, q|II)(qA− 1). (5)

Equating profits under information-sensitive debt (equation 2) with profits under information-insensitive

debt (equation 5) allows to pin down the level of the loan under information-sensitive debt:

RbIS < xbISCf the firm would always sell the collateral and repay the loan. This means that RbIS = xbISC

f .14I assume that it is feasible to borrow the optimal amount of capital (K∗), which means that xbIS = pKb+γb

pCf ≤ 1 and thatpK∗(qA− 1) > γb. Combining the two yields the condition qA < Cf/K∗.

9

Kb(p, q|IS) = pK∗ − γb

qA− 1 . (6)

3.3 Optimal Deposits for a Financial Institution

In this setting the owners of capital are households, which deposit their wealth in financial institutions,

which in their turn lend it to firms. The banks choose between deposits that cause information production

about the ability of the bank to repay, and deposits that do not induce information production. Both banks

and households make their decisions simultaneously which means that the household cannot infer the quality

of collateral from observing the bank’s loan. The creditworthiness of the financial institution is determined by

the amount of collateral that the firm has pledged for the loan it received. The cost of information acquisition

for the household is γh.

3.3.1 Information-Sensitive Deposits

In this case, households discover the true value of the financial institution’s loans, backed by firms’ land

as collateral, by incurring the cost γh. Households are risk neutral and break even:

p(qRhIS + (1− q)xhISCb −Kh) = γh (7)

where Kh is the actual amount of deposits in the financial institution, RhIS is the face value of deposits, and

xhIS is the fraction of the financial institution’s loans posted as collateral. For the same reason as before, the

fraction of collateral that the financial institution posts is xbIS = pKh+γh

pCb . Since the collateral posted by the

financial institution is the land that has been posted by the firm to obtain its loan, Cb = Cf .

Expected profits for the financial institution are

E(πb|p, IS) = pxbISCf − pxhISCb = pKb + γb − pKh − γh.15 (8)

3.3.2 Information-Insensitive Deposits

In this contract, financial institutions attract deposits without triggering production of information

regarding their assets. Since households are risk neutral and break even:15Because of the assumption that γh > γb the bank will always produce information before the household does as both q and

p decline.

10

qRhII + (1− q)pxhIICb = Kh, (9)

where RhII = pxhIICb for the same reasons as before, which means that xhII = pKh+γh

pCb .

For the contract to be information-insensitive, no household should have an incentive to deviate. This is

guaranteed by:

p(qRhII + (1− q)xhIICb −Kh) < γh ⇒ (1− p)(1− q)Kh < γh.

As with the information-sensitive loan to the firm, the deposits contract will reach the optimal amount

of capital (K∗) if the above condition is satisfied. If it is not, the amount of deposits will either be

Kh = γh

(1−p)(1−q) , if the financial institution faces credit constraints, or pCb if the collateral value is low. Thus,

Kh(p, q|II) = min

{K∗,

γh

(1− p)(1− q) , pCb

}. (10)

Expected profits for the financial institution are

E(πb|p, II) = pxbIICf − pxhIICb = Kb −Kh. (11)

Equating profits under information-sensitive deposits (equation 8) with profits under information-

insensitive deposits (equation 11) allows to pin down the level of deposits under information-sensitive

debt:

Kh(p, q|IS) = (1− p)KbIS + γh − γb

1− p . (12)

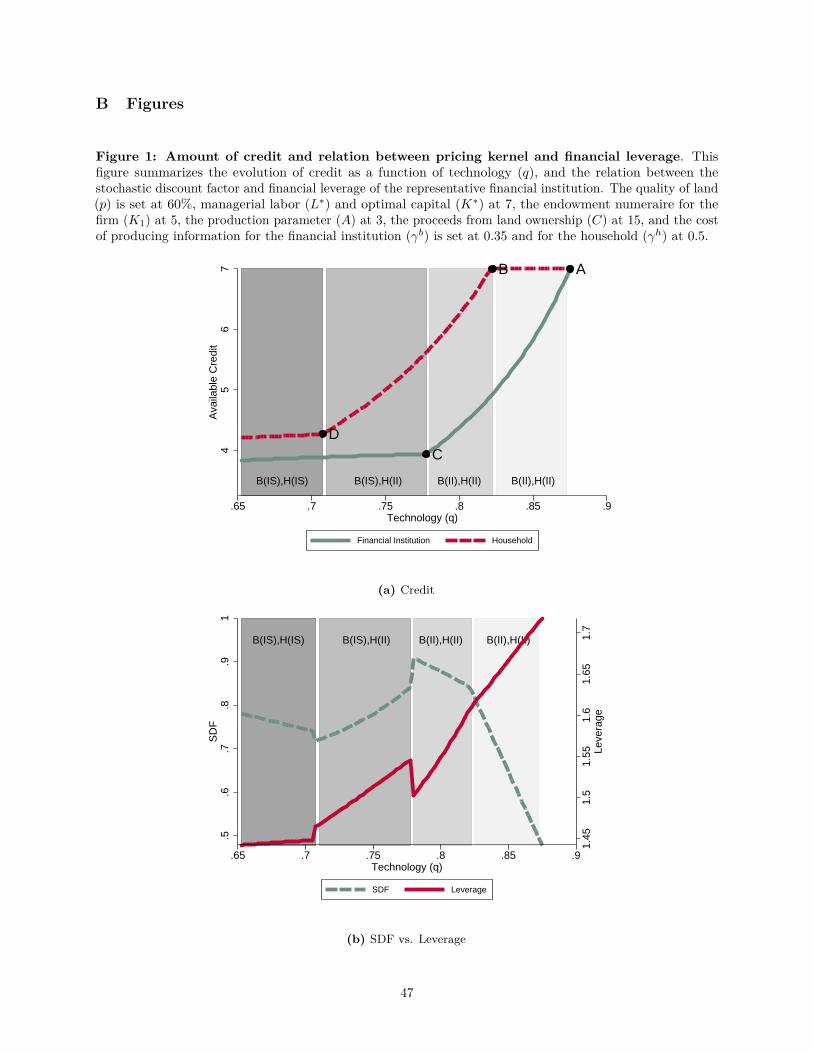

Figure 1a shows the amount of credit in the form of deposits and loans that the household and the

financial institution respectively are willing to make depending on the probability of success of the production

process (q) keeping the fraction of land that is good (p) constant. For the remainder of this section, this

probability will represent technological innovation. The cutoffs in Figure 1a are determined as follows:

Cutoff A occurs at the level of technological innovation below which firms reduce their borrowing so that

they do not induce information production. From above:

11

K∗ = γb

(1− p)(1− q) ⇒ qb,HII = 1− γb

K∗(1− p) . (13)

Cutoff B is determined by the level of technological innovation below which financial institutions reduce

their deposits thus avoiding information production from households. As before:

K∗ = γh

(1− p)(1− q) ⇒ qh,HII = 1− γh

K∗(1− p) . (14)

Cutoff C is obtained after equalizing information-sensitive debt with information-insensitive debt:

γb

(1− p)(1− q) = pK∗ − γb

(qA− 1) . (15)

The positive root of the above quadratic equation (qbIS) is the level of technological innovation below which

financial institutions acquire information about the quality of land that firms post as collateral for their loan.

Cutoff D is obtained similarly for the case of deposits,

γh

(1− p)(1− q) = pK∗ − γb

(qA− 1) + γb − γh

(p− 1) . (16)

The above cutoffs create four distinct regions: (1) Between A and B (B(II), H(II)), both the bank and the

household are information-insensitive (II). Also, bank credit is constrained and firms cannot borrow without

triggering information production, which means that credit rationing takes place in bank lending; (2) Between

B and C (B(II), H(II)), both agents are information-insensitive (II) but credit constraints lead to rationing

in both bank lending and deposits; (3) Between C and D (B(IS), H(II)), the bank is information-sensitive

(IS) and at a cost γb discovers the true value of the land. The household is still information-insensitive and

rationing takes place in deposits; and (4) Below D (B(IS), H(II)), both agents are information-insensitive

with banks producing information about the quality of land and households producing information about the

quality of the assets of the financial institution.16

The amount of credit that is available in the economy to fund firms’ projects is a function of technological

innovation (q), the quality of land (p), and the cost of information production for financial institutions (γb)

and households (γh). For the purposes of this paper, I assume that the quality of land and the cost of16Additional regions become relevant depending on the level of the fraction of land that is good p and the value C of land.

Low collateral value can constrain the amount of deposits and subsequent loan amount, however for high enough levels of p, itbecomes irrelevant.

12

information acquisition remain constant throughout the two periods. Proposition 1 summarizes the relation

between technological innovation and the amount of credit in the economy. The proof is trivial.

Proposition 1. (Effect of technological innovation on credit.)

For fixed values of γb, γh, and p, with γb < γh and K∗ < pCf = pCb:

• Deposits are an increasing function of technological innovation (q) for q < qh,HII and independent of q

otherwise.

• Loans are an increasing function of technological innovation (q) for q < qb,HII and independent of q

otherwise.

3.4 Firm Valuation

As mentioned above, in this economy the financial institutions are the sole owners of firms. They are

risk averse with respect to their equity holdings and risk neutral with respect to their lending activity. This

assumption is motivated primarily by current banking regulation which mandates bank capital requirements

and determines internal risk-management policies. More specifically, according to the Third Basel Accord

(Basel III) equities are deemed substantially less liquid than high quality corporate debt. This means that

equities in intermediaries’ balance sheets require a higher capital provision compared to that required for high

quality corporate debt.17 I derive the stochastic discount factor (SDF) and compute the financial leverage of

financial institutions in a two period general equilibrium framework. Table 1 summarizes the timeline for this

economy. The financial institution maximizes a logarithmic utility function with two terms, a deterministic

component for the first period and a stochastic component for the second period,

max{Ct}2

t=1

Eu(C1, C2) = log(C1) + βElog(C2) (17)

Subject to:

C1 +Kb + γb + V1a1 = (π1(q1) + V1)a0 +Kh (18)

and

Kh + C2 = Kb + π2(q)a1 + pCf (19)17Basel III requires financial institutions and non-bank financial companies deemed systemically important to have enough

high-quality liquid assets (HQLA) which can be quickly liquidated to meet possible future liquidity needs. Assets are classifiedinto three groups (Level 1, Level 2A, and Level 2B) according to their liquidity properties. A total HQLA is computed as theweighted sum of the the asset value times a weight that is consistent with its liquidity group. Haircuts vary from 0% for assets inLevel 1 to 50% for assets in Level 2B. Common equity falls into Level 2B and is subject to a 50% haircut which is significantlyhigher compared to the 15% haircut of high quality (>AA- rating) corporate debt (see, e.g. www.bis.org/publ/bcbs238.pdfand www.bis.org/bcbs/publ/d406.pdf).

13

where Ct is the period t consumption, Kb the amount of the loan to the firm, Kh the amount of deposits

in the financial institution, γb the cost of information acquisition for the financial institution, at the time t

fraction of firm that is held by the financial institution, p the fraction of land that is good, C the numeraire

that land that is good delivers at the end of period 2, and πt(q) the period t firm profits as a function of

technological innovation (q).18

Market clearing requires that a0 = 1, a1 = 1, C1+Kb+γb = π1(q1)+Kh, andKh+C2 = Kb+π2(q)+pCf .

Kh and Kb are determined above.

First order conditions with respect to a1 yield:

V1 = E

(βC1

C2π2(q)

)(20)

which means that the SDF for the financial institution is:

m = Kh −Kb + π1(q1)− γb

Kb −Kh + π2(q) + pCf(21)

Financial leverage is defined as the ratio of assets to assets minus liabilities:

l = Kb + V1

Kb + V1 −Kh(22)

The relation between a financial institution’s SDF and its financial leverage depends on the level of

information acquisition from the household and the financial institution, which in turn is directly related to

the level of technological innovation that the economy experiences. Technological innovation is also directly

related to the level of credit outstanding in the economy (Proposition 1). Hence any relation between a

financial institution’s SDF and its financial leverage across levels of technological innovation holds across

levels of credit outstanding. Proposition 2 summarizes this relation for different “regimes” of information

production defined by the level of technological innovation.19

Proposition 2. (Stochastic discount factor and financial leverage.)

The relation between the SDF of a financial intermediary and its financial leverage depends on the level

of technological innovation (q) and information acquisition from the household and the financial intermediary:18π1(q1) = Aq1K1, and π2(q) = Kb(p, q|II)(qA−1) when bank loans are information-insensitive and π2(q) = pK∗(qA−1)−γb

when bank loans are information-sensitive.19The proof can be found in the appendix.

14

• Bank loans and household deposits are information-insensitive with no credit constraints present (B(II),

H(II)): Leverage is constant and SDF a negative function of technological innovation.

• Bank loans and household deposits are information-insensitive, but credit constraints are present (B(II),

H(II)): Leverage is positively and SDF negatively correlated with technological innovation.

• Bank loans and household deposits are information-insensitive, but deposit and credit constraints are

present (B(II), H(II)): Leverage is positively and SDF negatively correlated with technological innovation.

• Bank loans are information-sensitive and household deposits are information-insensitive with deposit

constraints present (B(IS), H(II)): Both leverage and SDF a positive function of technological innovation

• Bank loans and household deposits are information-sensitive (B(IS), H(IS)): Leverage is positively and

SDF negatively correlated with technological innovation.

Figure 1b provides an illustration of Proposition 2. For a high level of technological innovation and

credit outstanding, the relationship between SDF and financial leverage is negative. An increase in financial

leverage is associated with a decrease in the SDF of the financial institution. This usually represents times

of economic growth where the financial institution is able to sustain a relatively high level of leverage due

to the availability of a large number of profitable investment opportunities and the high level of funding it

secures from the household. However, when technological innovation and credit outstanding is at a relatively

low level and the household does not yet produce information, the relationship between the two variables is

the opposite.20 An increase in financial leverage is associated with an increase in the SDF of the financial

institution. The change in the relationship between the two variables is caused by the fact that the rate of

increase in deposits is higher than that in loans and the valuation of the firm. The increase in funding from

households does not keep up with the improvement in the profitability of investment opportunities in the

economy leading to an increasing leverage ratio and an increasing SDF. This usually represents times of

economic recession or financial crises where the financial institution may have sufficient funding, but not

enough investment opportunities leading to high levels of leverage.

Both Proposition 2 and Figure 1b underline the point that financial leverage is not always an accurate

measure of the SDF of a financial institution. In times when credit is low the relation between the two

variables reverses and a more accurate proxy of the marginal value of wealth of financial institutions should

take that into account. When credit is high, assets that co-vary with leverage are riskier and as a result

should earn higher premia. On the other hand, when credit is low, assets that co-vary with leverage are less20Usually the household does not produce information about the quality of the assets of the financial institution, unless there

is widespread uncertainty about the health of the financial system. Which makes the last case of Proposition 2 less likely to beobserved in the data.

15

risky and should earn lower premia.21 In the following section, I propose an empirical measure that takes

this point directly into account and combines information from both credit and financial leverage.

4 Data

This section describes the data used in the empirical analysis. I provide details on the construction of

the adjusted leverage factor, currency excess returns, currency portfolios, and the macroeconomic variables

used in the empirical tests.

4.1 Leverage Ratio

Intermediary asset pricing models suggest that financial intermediaries are sophisticated investors who

play a leading role in capital markets. They are considered marginal investors which means that their pricing

kernel is relevant for pricing the cross-section of risky assets.22 Motivated by the theoretical framework

developed above, I construct a proxy for the marginal value of wealth which takes into account the leverage

ratios of financial intermediaries and the credit conditions in the economy. I compute leverage ratios for

financial institutions that act as broker-dealers for an international panel (Table 2) using data from Thomson

Reuters WorldScope.23 I delete duplicate entries and data on ADRs. Leverage ratios are computed as follows:

Leverage = log

(Assets

Assets− Liabilities

)(23)

4.2 Assets Portfolios

For the purposes of the asset pricing tests of Section 7.1 I use currency and global equity portfolios.

I construct six forward discount portfolios following the methodology of Lustig et al. (2011). I rank21This relation can reverse if financial institutions face a higher cost of information acquisition on the firms’ assets than

households do (γb > γh). However, this does not seem to be the case in modern economies where financial institutions have aplethora of resources at their disposal to research and identify the quality of the posted collateral.

22There are two approaches to modeling an intermediary pricing kernel each of which has a different theoretical motivation.The first uses intermediary leverage as a proxy for the SDF (see, e.g. Brunnermeier and Pedersen (2009), while the second usesintermediary wealth (see, e.g. He and Krishnamurthy (2013) and Brunnermeier and Sannikov (2014)). Throughout this paper Ifollow the first approach.

23The actual WorldScope industry codes for financial firms used in the analysis are: 4310 for Commercial Banks - Multi-BankHolding Companies (used only for international financial institutions), 4394 for Securities Brokerage Firms, and 4395 forMiscellaneous Financial. Financial institutions classified as commercial banks in the database serve as broker-dealers in manycountries. Commercial Banks - Multi-Bank Holding Companies (4310, U.S only data), Commercial Banks - One Bank HoldingCompanies (4320), Investment Companies (4350), Commercial Finance Companies (4360), Insurance Companies (4370), Landand Real Estate (4380), Personal Loan Company (4390), Real Estate Investment Trust Companies, including Business Trusts(4391), Rental & Leasing (4392), and Savings & Loan Holding Companies (4393) are not included.

16

currencies from low to high interest rates such that portfolio 1 contains currencies with the lowest forward

discounts, and portfolio 6 contains the currencies with the highest forward discounts. The strategy that is

long on portfolio 6 and short on portfolio 1 represents carry trade and constitutes the carry factor (CAR)

that I use in the following asset pricing tests. Currency momentum portfolios are constructed using the

methodology of Menkhoff et al. (2012b). Each month I form six portfolios on the basis of excess currency

returns of the previous n months. Portfolio 1 contains currencies with the lowest prior n month returns,

while portfolio 6 comprises of currencies with the highest prior n month returns. I construct two types of

momentum portfolios, long-term momentum (n = 12 months) and short-term momentum (n = 1 month). The

strategy that is long on short-term momentum portfolio 6 and short on portfolio 1 constitutes the momentum

factor (MOM). I construct value portfolios following the methodology in Asness et al. (2013). As with

currency momentum, I form six portfolios based on the lagged five-year excess return of the currency of

each country in the sample. I assign the lowest lagged returns to portfolio 1 and the highest to portfolio 6.

Global equities portfolios comprise twenty-five international size and value sorted portfolios and the

twenty-five international size and momentum portfolios all obtained from Kenneth French’s online

data library.24

4.3 Macroeconomic Data

In Section 5, I explore the properties of the adjusted leverage measure with respect to macroeconomic

variables. Annual Real GDP and capital formation are from the Penn World Tables (PWT), domestic credit

to private sector, credit to households and credit to corporates are from the World Bank World Development

Indicators. Financial crisis episodes are from Valencia and Laeven (2012). Global imbalances are defined

as the difference between assets and liabilities denominated in the same currency. I construct the measure

of total global imbalances, which is the sum of global imbalances issued in domestic and foreign currency

standardized for the GDP of a country. For additional details see Bénétrix et al. (2015).25 Market returns are

the average market returns at a country level, financial intermediaries returns are the average financial sector

returns at a country level, and global volatility is the average market volatility among an international set of

countries (see, e.g. Chousakos et al. (2016)). In addition, and only for the U.S. economy, I collect data on

credit spreads, per capita consumption on durables, non-durables, and private investment from the Federal

Reserve Economic Data (FRED) maintained by the St. Louis FED. Table 3 summarizes the data used in this

paper.24http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html#International.25The dataset can be found at Philip Lane’s website http://www.philiplane.org/BLSJIE2015data.htm.

17

5 Adjusted Leverage

In the literature the marginal value of wealth of financial institutions is proxied by their financial leverage

and more specifically by seasonally adjusted changes in the level of broker-dealer leverage (see, e.g. Adrian et

al. (2014)). This could be potentially problematic because as discussed in Section 3 financial leverage or its

reciprocal capital ratio does not fully characterize the risk-bearing capacity of financial intermediaries across

all states of the economy. An increase in financial leverage does not necessarily indicate a decrease in the

marginal value of wealth for the financial institution. This could be true in times of economic growth, where

credit outstanding is high and the financial system can sustain high levels of leverage as financial intermediaries

are able to pursue profitable investments and at the same time raise capital if needed. However, this is not

the case in times of recessions or financial crises, where the amount of credit outstanding is low. According

to the theoretical framework discussed above, it possible that in a low credit environment an increase in

leverage is associated with an increase in the marginal value of wealth of the financial institution due to a

lack of profitable investment opportunities. A number of empirical findings, summarized below, suggest that

financial leverage interacts differently with key characteristics of financial intermediaries depending on the

level of credit outstanding in the economy.

The level of assets of financial intermediaries reflects among other factors their risk-bearing capacity.

A high level of assets in intermediaries’ balance sheets is usually the result of higher risk-bearing capacity.

If the financial leverage of an intermediary is a good proxy for its risk-bearing capacity, then the relation

between leverage and the level of future assets is expected to be positive across all states of the economy (see

e.g. Adrian et al. (2014)). The following regression specification provides a test of the above claim:

assetsn,t+q = αn + αt+q + β′Xn,t + γassetsn,t + εn,t+q (24)

where assetsn,t+q is the logarithm of the financial assets of country n at time t + q quarters, Xn,t =

(fin.leveragen,t, fin.leveragen,t × 1(Creditn,t > 75%), fin.leverage× 1(Creditt < 25%))′, fin.leveragen,t

is the logarithm of financial leverage of country n at time t, 1(Creditn,t > 75%) is a dummy variable

representing instances where credit-to-private sector of a given country is higher than the 75th percentile

of the cross-section of credit outstanding values at a given time, 1(Creditn,t < 25%) is a dummy variable

representing instances where credit-to-private sector of a given country is lower than the 25th percentile of

the cross-section of credit outstanding values at a given time, αn represents country fixed effects, and αt+q

time fixed effects.

18

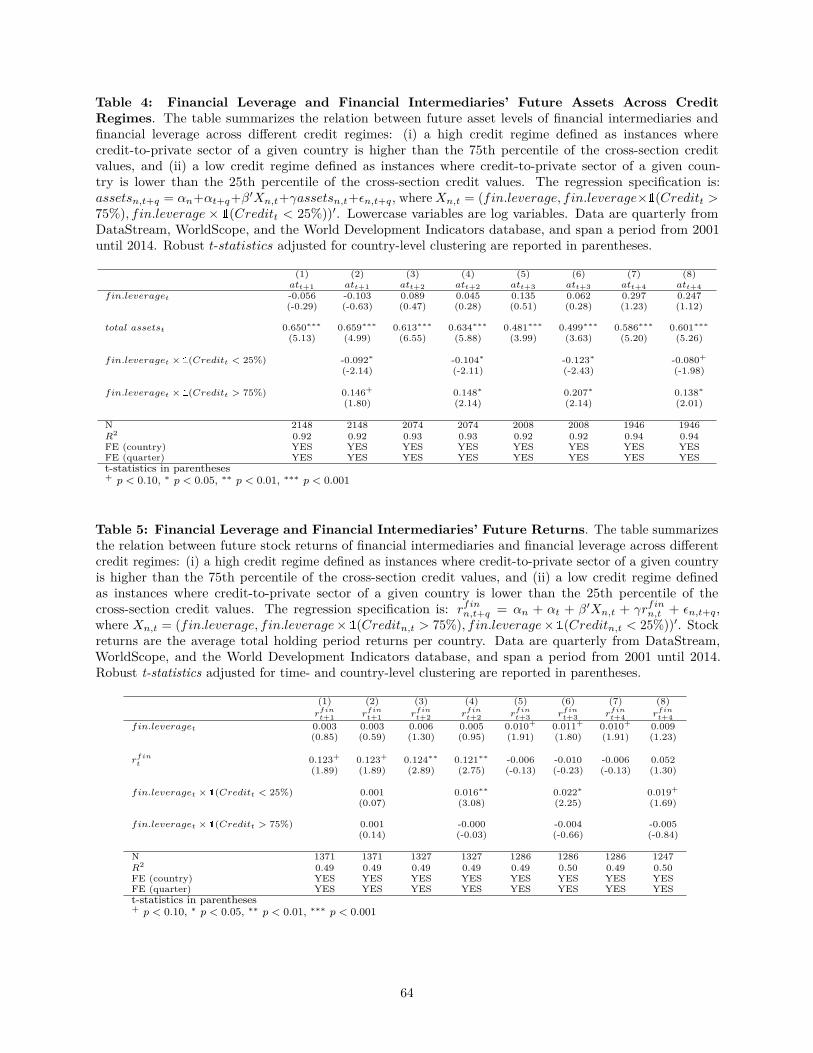

Table 4 shows that the relation between leverage and the level of future assets is not consistently positive

across all states of the economy for an international panel of financial institutions aggregated at the country

level. More specifically, when interacted with the dummy variable 1(Creditn,t > 75%), and the dummy

variable 1(Creditt < 25%), the relationship between financial leverage and future assets is not consistently

positive. In the first case, financial leverage and future levels of assets are positively correlated, suggesting a

higher risk-bearing capacity, while in the second case a negative correlation suggests a lower risk-bearing

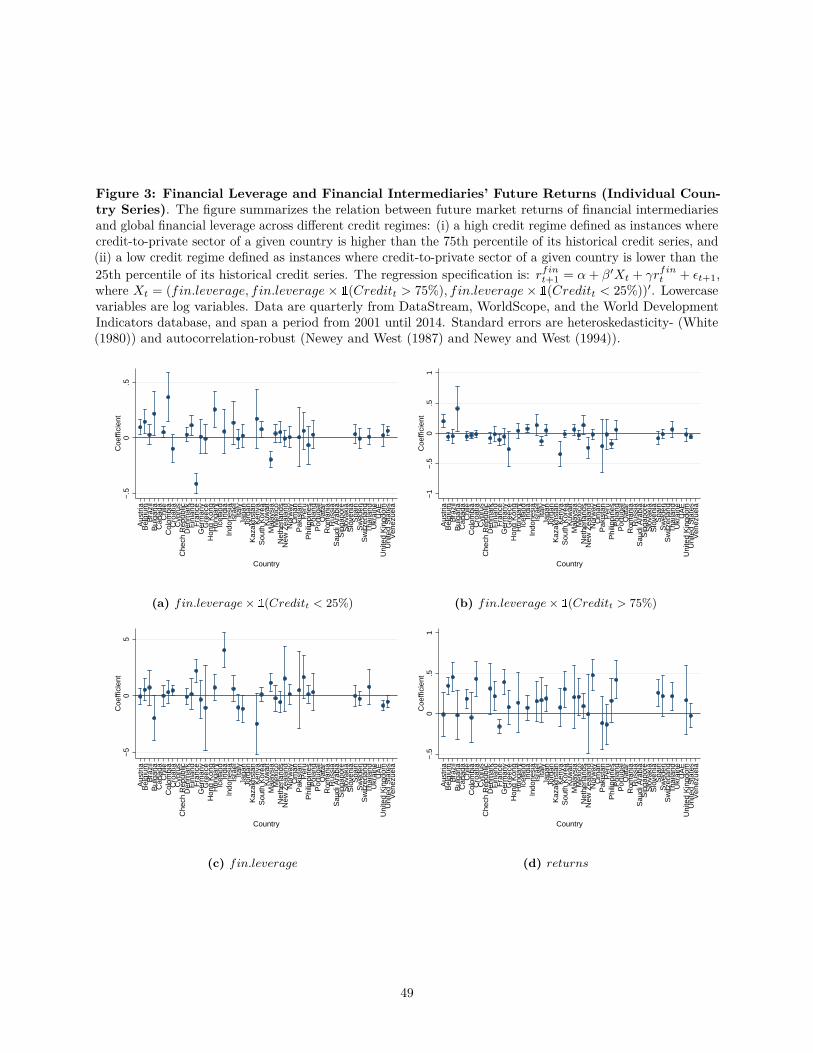

capacity leading to lower future levels of assets.26 Figure 2 confirms the above findings using country level

time-series regressions. When credit is low compared to the historical credit series for the country, the

majority of countries exhibits a negative correlation between leverage and future levels of assets, while the

opposite holds true when credit is high.

Another variable that reflects the risk-bearing capacity of financial institutions is intermediaries’ future

stock returns. According to traditional finance theory, higher expected returns usually reflect riskier

investments. Financial intermediaries that are perceived to be riskier usually face tighter funding constraints

and their risk-bearing capacity is limited. To test this claim I repeat the previous exercise, but now I replace

future assets with future returns. The regression specification is as follows:

rfinn,t+q = αn + αt+q + β′Xn,t + γrfinn,t + εn,t+q (25)

where rfinn,t+q is the logarithm of the market returns of financial intermediaries of country n at time t + q

quarters. Table 5 shows that on an aggregate level, financial intermediaries with high financial leverage

operating in a high credit environment consistently earn lower returns, while similar financial institutions

operating in a low credit environment earn consistently higher returns. This finding suggests that financial

leverage alone does not fully capture intermediaries’ risk-bearing capacity. Financial leverage viewed in

tandem with credit-to-private sector can be considered as a more accurate proxy for the marginal value of

wealth of financial intermediaries.27 As with the case of future assets, Figure 3 confirms the panel regression

findings using country level time-series regressions.

Motivated by the above findings, I propose a measure of a global adjusted leverage, which in addition to

financial leverage takes into account the level of credit-to-private sector at a global level. This measure serves

as a proxy for the marginal value of wealth of financial intermediaries and it is used in the asset pricing

tests of Section 7. I construct the global adjusted leverage index as follows: First, I compute a measure of26The same pattern holds true when focusing only on the U.S. economy (table can be found at the internet appendix).27The same pattern holds true when focusing only on the U.S. economy (Table can be found at the accompanying internet

appendix).

19

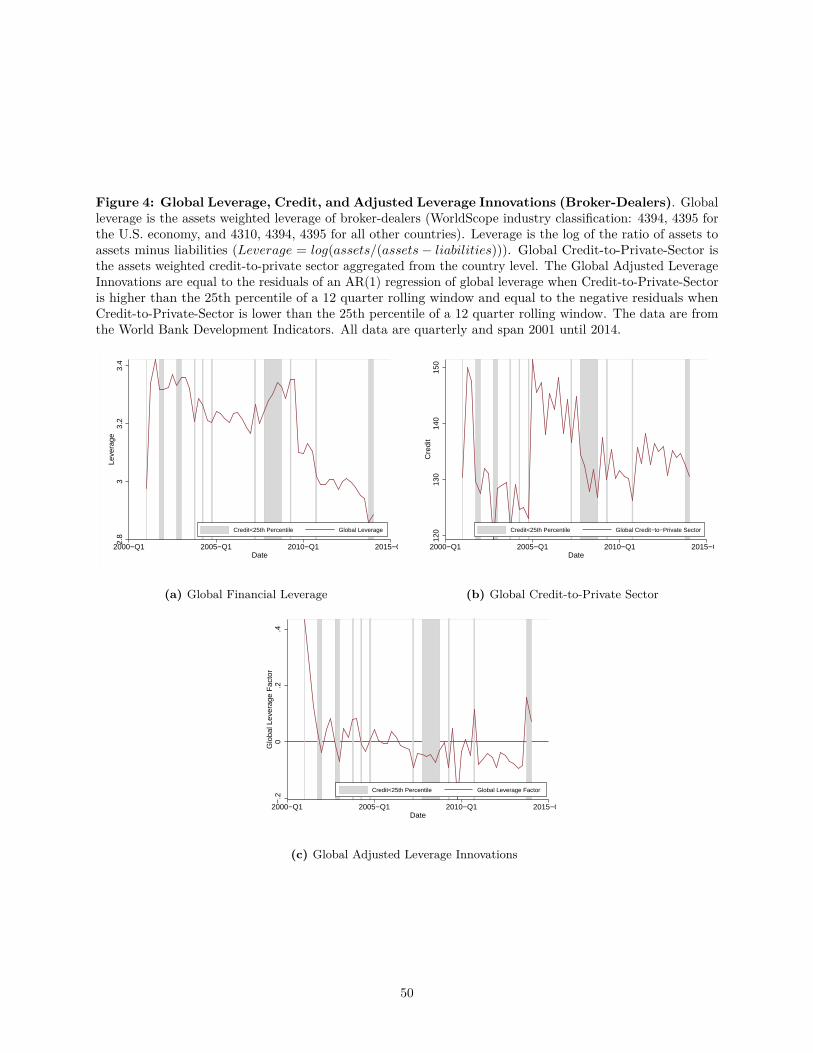

global financial leverage (Figure 4a) as the aggregated country level financial leverage weighted by the level

of financial assets of each country,

Global Leveraget =N∑c=1

wc,tLeveragec,t

where Leveragec,t is the country level financial leverage computed by aggregating firm level financial leverage,

wc,t = Assetsc,t∑N

c=1Assetsc,t

, and Assetsc,t =∑Mi=1 Assetsc,i,t. Second, I compute a global measure of credit-to-

private sector (Figure 4b) by aggregating the country level credit-to-private sector again weighted by the

level of financial assets of each country,

Global Creditt =N∑c=1

wc,tCreditc,t

Finally, the global adjusted leverage measure is equal to the residuals of an AR(1) process on global leverage

when credit-to-private sector is higher than the 25th percentile of a 12 quarter rolling window and equal

to the negative residuals of the same AR(1) process when credit-to-private sector is lower than the 25th

percentile of a 12 quarter rolling window (Figure 4c).28 The AR(1) process is,

Global Leveraget = α+ βGlobal Leveraget−1 + εt

The Adjusted leverage measure is,

Adjusted Leveraget =

−ε̂t if 1(Credit < 25th Percentile) = 1

+ε̂t otherwise.(26)

The rolling window guarantees no forward looking bias in the computation of the measure. Figure 5 shows

how the global adjusted leverage measure compares to innovations in global financial leverage. The correlation

between the two measures is 52.9%.

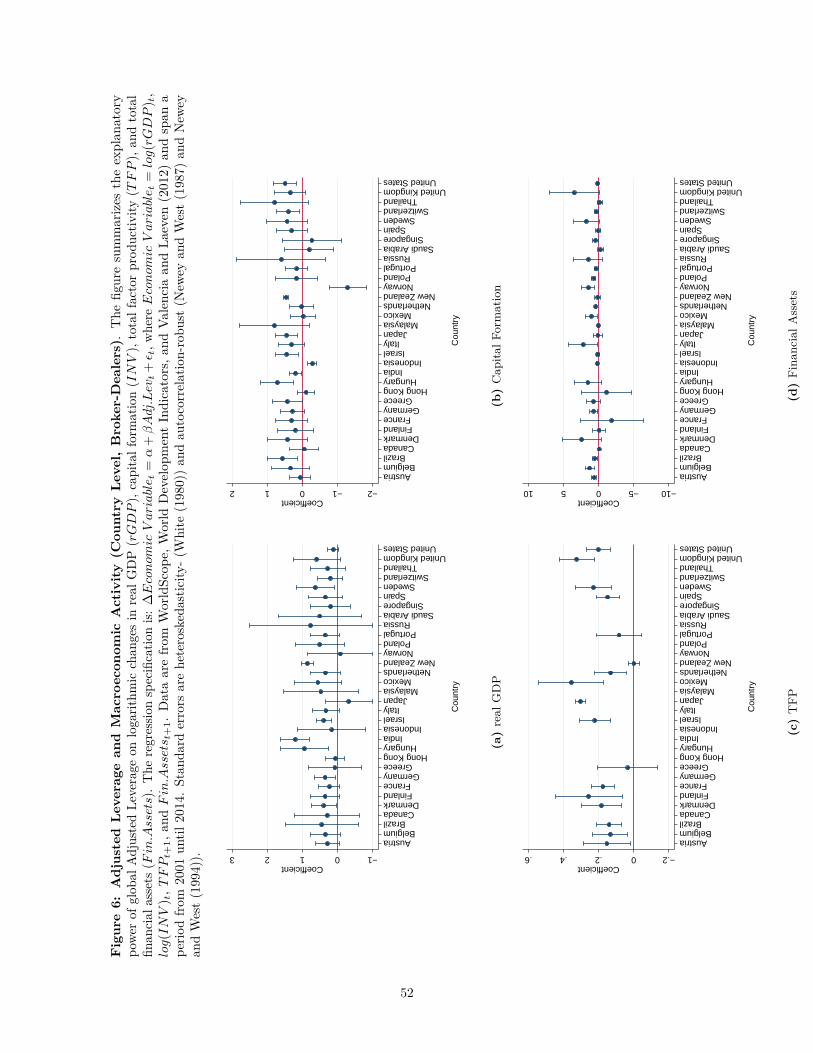

The risk-bearing capacity of financial intermediaries is associated with the state of the macroeconomy. It

is pro-cyclical, which suggests that favorable funding conditions are usually observed in periods with higher

credit outstanding, capital formation, and aggregate output. Adjusted leverage as a proxy for intermediaries’

risk-bearing capacity is expected to exhibit such a pro-cyclical behavior. Using an international panel28An alternative way to derive the adjusted leverage measure would be to compute the residuals of an AR(1) process on the

product of leverage and credit-to-private sector. In results which are available upon request, I show that this alternative adjustedleverage measure shares most of the properties of the adjusted leverage measure discussed above, however the explanatory powerof the second is significantly higher.

20

of observations, I perform a set of country level regressions of macroeconomic variables on the adjusted

leverage measure. Figures 6 and 7 summarize the results. Adjusted leverage is positively correlated with

contemporaneous changes in real GDP, capital formation, total factor productivity (TFP), and future financial

assets. This finding confirms that adjusted leverage is a pro-cyclical measure. In addition, adjusted leverage

is positively correlated with contemporaneous changes in credit to households, while the opposite holds true

for the case of credit-to-corporate entities. An increase in the global risk-bearing capacity is immediately

reflected in credit-to-households, but not in credit-to-corporate entities possibly due to the fact that corporate

loans require a longer assessment period. Total global imbalances are, in general, negatively correlated with

adjusted leverage suggesting that an increase in the global risk-bearing capacity of financial institutions leads

to a net loss of capital to advanced countries such as the U.S., France, and Denmark.29

The adjusted leverage measure incorporates, by construction, information about credit conditions in

the economy. Schularick and Taylor (2012) document that credit growth is a strong predictor of financial

crises. This finding motivates the following tests of the predictive power of adjusted leverage over financial

crises. Using an international panel, I regress the occurrence of a financial crisis on a set of lagged adjusted

leverage observations. I employ both a linear probability model and a logistic regression specification. Table

7 shows that 6-month lagged observations of adjusted leverage negatively predict financial crises. This finding

suggests that, prior to financial crises, financial institutions exhibit a lower risk-bearing capacity. This lower

risk-bearing capacity suggests that financial institutions could potentially adjust their activity to better

prepare themselves for an imminent financial crisis.

The U.S economy is no exception to the above mentioned patterns presented in Figures 6 and 7. Global

adjusted leverage is a pro-cyclical measure, positively correlated to changes in credit-to-households, real

GDP, capital formation, and TFP, while negatively correlated with the occurrence of financial crises and

credit spreads. Figure 8 looks at the relation between adjusted leverage, future per-capita consumption, and

future private investments on an expanding window reaching five years into the future. More specifically,

an increase in adjusted leverage is associated with a short term (1-year) increase in per-capita consumption

both in durables and non-durables, while an increase in adjusted leverage is associated with a medium term

(4,5-year) increase in private investments. This finding further supports the pro-cyclical nature of adjusted

leverage and shows that an increase in the risk-bearing capacity of the financial sector leads to an increase in

lending activity, both in the short- and in the long-term.

From the above findings, I conclude that adjusted leverage can be used as a reasonable proxy for the

marginal value of wealth of a financial intermediary. Adjusted leverage is high when credit conditions are29And possibly to other countries not in the current sample of countries.

21

favorable and low when credit conditions are adverse and leverage is high. It is pro-cyclical (positively

correlated with other measures of credit, real GDP, capital formation, and TFP), which is a characteristic of

marginal value of wealth that is consistent with theory (see, e.g. Brunnermeier and Pedersen (2009)), predicts

financial crises, and correlates with future consumption of durables and non-durables. The pro-cyclical nature

of adjusted leverage implies that this measure increases in good times when funding constraints are lax. In

the following sections, I test the asset pricing properties of this measure for both currency and global equity

portfolios.

6 Adjusted Leverage Factor in an Asset Pricing Setting

In this section I propose a pricing model which attempts to more accurately capture financial intermedi-

aries’ marginal value of wealth. I discuss how it relates to the theoretical framework of Section 3 and describe

the empirical methodology used to test its asset pricing properties.

6.1 Adjusted Leverage as Stochastic Discount Factor

In Section 3, I derived the stochastic discount factor of a financial institution in a two period economy

and discussed its relation with financial leverage across different levels of credit outstanding and technological

innovation, which define a set of information production regimes. More specifically, I show that when

both loans and deposits are information-insensitive, the relation between the stochastic discount factor

of the financial institution and financial leverage is negative, with the first decreasing while the second

increasing as credit outstanding in the economy increases. These information production regimes occur

when credit outstanding and technological innovation in the economy are at a relatively high level. The

increase in financial leverage is associated with a decrease in the marginal value of wealth of the financial

institution mainly due to the increase in the profitability of the firm. On the other hand, when loans are

information-sensitive and deposits are information-insensitive, the relation between the stochastic discount

factor of the financial institution and financial leverage is positive. This information production regime occurs

when credit outstanding and technological innovation are at relatively low levels. Both measures increase as

credit increases due to the fact that the increase in deposits is higher than that of the profitability of the firm.

This means that if SDFt ≈ α− bcLeveraget, then when credit is sufficiently high, assets that co-vary

with leverage are risky and earn a higher risk premium (bc > 0), while when credit is sufficiently low, assets

that co-vary with leverage are less risky and earn a lower risk premium (bc < 0). The proposed global adjusted

22

leverage measure addresses exactly this point by incorporating information from both credit outstanding

and financial leverage. Hence, SDFt ≈ a− b ·Adjusted Leveraget. In Section 7 I discuss the asset pricing

properties of adjusted leverage and show how consistent these properties are with this theoretical framework.

6.2 Empirical Methodology

In this section, I propose a linear factor model which consists of the global adjusted leverage factor. Using

a cross-section of asset returns, I test for the asset pricing properties of this factor using the methodology

proposed by Lewellen et al. (2010). The proposed SDF is linear in the global adjusted leverage factor:

SDFt = 1− b ·Adjusted Leveraget (27)

In the absence of arbitrage opportunities, asset j’s excess return has a price of zero and satisfies the Euler

equation:

E0[Rej,tSDFt

]= 0 (28)

Combining equations 28 and 27 we obtain:

E0[Rej,t

]= bCov

(Rej,t, Adjusted Leveraget

)= λAdj.Levβj,Adj.Lev (29)

where λAdj.Lev = bV ar(Adj.Lev) and βj,Adj.Lev = Cov(Rej,t, Adj.Levt

)/V ar(Adj.Lev). λAdj.Lev is the cross-

sectional price of risk for the global adjusted leverage factor, and βj,Adj.Lev is the exposure of asset j to the

risk-bearing capacity of financial intermediaries.

To test the above model, I employ two-pass regressions. First, I estimate the exposure of each asset j

(βj,f ) to the factors of interest (f) using the following time-series regression specification,

Rej,t = aj + β′j,fft + εi,t

where aj is the constant for asset j; εj,t is a vector of the estimation errors for asset j at time t. Second,

I estimate the price of risk exposure (λf ) to the factors of the model (f) using the following cross-section

regression specification,

E[Rej ] = λ0 + β′i,fλf + αj

where λ0 is the constant of the regression; αi are the estimation errors for asset i.30 I estimate the coefficients30I choose to include the intercept (λ0) since I do not want to impose extra structure into this linear model. I acknowledge a

23

using an OLS specification.

At a minimum level, an asset pricing model is expected to produce small (both economically and

statistically) values for λ0, a statistically significant price of risk exposure (λf ), and pricing errors (αi) close

to zero. I assess the size of pricing errors (i) by computing an adjusted R2 for the cross-sectional regression

performed on the test assets, (ii) by computing the mean absolute pricing error (MAPE), the maximum

pricing error (MAX) and the sum of MAPE and λ0 (TOTAL), and (iii) by testing whether a weighted sum of

squared pricing errors (α′cov(α)−1α ∼ χ2N−K) is statistically different from zero.31 32 I estimate t-statistics

for the price of risk using both the Fama and MacBeth (1973) and Shanken (1992) methodologies.

Lewellen et al. (2010) provide a critique of the robustness of traditional cross-sectional asset pricing

models. They contend that the commonly used asset pricing tests set the bar too low and offer supporting

evidence by generating high values for R2 and low pricing errors (α) by using random noise factors whose

actual explanatory power is zero. In their paper they suggest a number of tests designed to improve the

arsenal of evaluation techniques for asset pricing models. Many of the suggested improvements for model

testing are incorporated into the asset pricing tests that follow.

In the spirit of Lewellen et al. (2010), using bootstrapping I construct confidence intervals for the true

value of the adjusted R2 of the models considered in the analysis.33 Lewellen et al. (2010) motivate this

method by making the observation that even in cases where the actual R2 of a model is zero, it is possible

that the sample adjusted R2 is relatively large, and the opposite, that even when the actual R2 of a model is

one, it is possible that the sample adjusted R2 is significantly less than one. Finally, I estimate and report

the probability that the cross-sectional R2, the mean absolute pricing error (MAPE), and the pricing errors

(α) of the asset pricing models considered in the analysis are higher and lower respectively compared to those

of artificial factors which are constructed by randomly drawing from the empirical distribution of the actual

factors with replacement.34

potential loss in efficiency, but I choose not to sacrifice the robustness of the model by imposing no intercept to it and forcing itto fit the data. This approach allows the model to provide additional information about the data (see, e.g. Cochrane (2005)).

31MAPE = 1N

∑i

|αi|.

32K is the number of factors considered in the model when I estimate cov(α) using the Shanken (1992) correction, and K is 1when we estimate cov(α) using the Fama and MacBeth (1973) approach.

33For the exact details of the method I refer the reader to Lewellen et al. (2010).34I construct 100,000 such factors and compare their performance against that of the actual factors.

24

7 Empirical Findings

7.1 Cross-Sectional Analysis

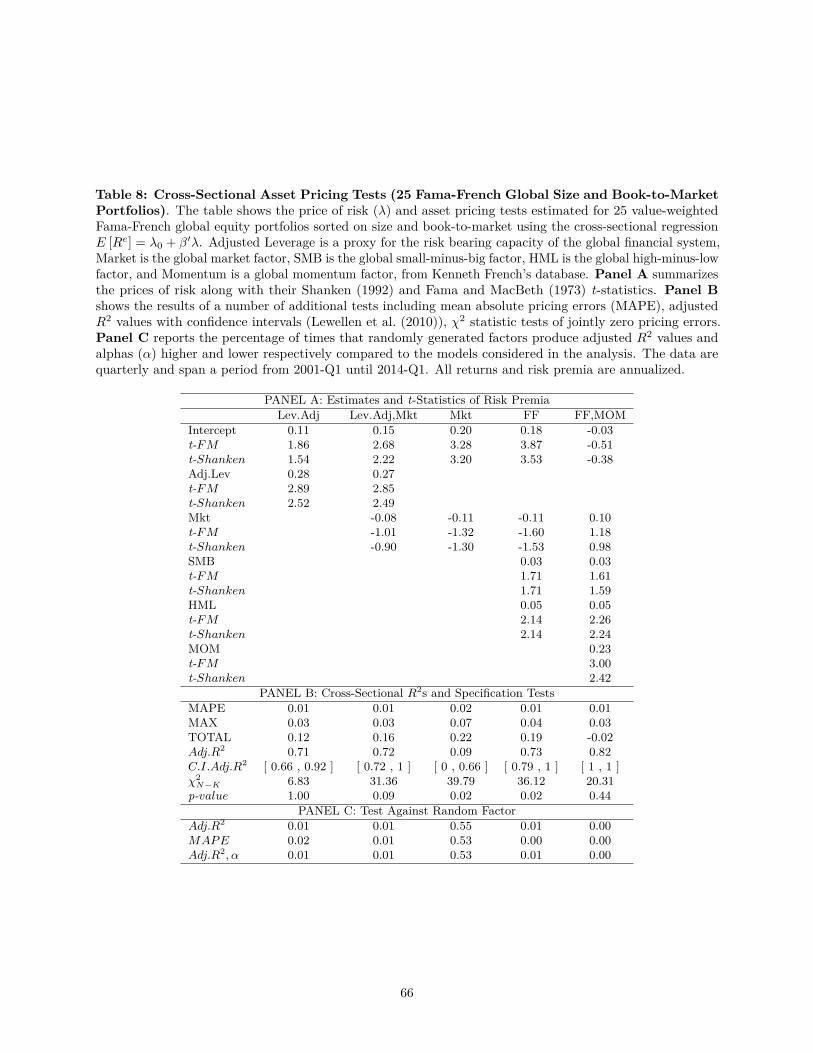

This section presents the main finding of this paper. Excess returns of international asset portfolios

(international equities and currencies) can be understood by their exposure to the global adjusted leverage

factor. The portfolios that I employ for international equities are the 25 global portfolios formed on size and

book-to-market and the 25 global portfolios formed on size and momentum. Table 8 summarizes the results

for the 25 global size and book-to-market portfolios. Panel A summarizes the cross-sectional prices of risk,

Panel B shows a number of specification tests, and Panel C tests the asset pricing properties of the proposed

model against a set of random pricing factors.35 The global adjusted leverage factor appears with a positive

price of risk and outperforms the market factor and the Fama-French three factor model across all metrics.

More specifically, the global adjusted leverage factor model exhibits an adjusted R2 of 71% which is one of

the highest across all other models considered. In addition, the χ2 value the lowest the p-value of the test

does not reject the null of jointly zero pricing errors. The adjusted leverage model performs better than the

Fama-French three factor model in terms of the p-value of the χ2 test; equally well regarding the adjusted

R2, MAPE, and MAX figures; and worse in terms of the value of the intercept. Figure 9 summarizes the

predicted versus realized average returns for the four models considered in Table 8. Figure 9a confirms the

good explanatory power of the global adjusted leverage factor model which is comparable only with that of

the Fama-French factor models (9d).

Focusing next on the 25 global size and momentum portfolios, I again compare the global adjusted

leverage factor model against the market model, the Fama-French three factor model, and the Fama-French

three factor plus momentum model. Table 9 summarizes the results. The findings are almost identical to

the ones presented for currency portfolios and the 25 global size and book-to-market portfolios. The global

adjusted leverage factor appears with a significantly positive price of risk, and outperforms the market model

and the Fama-French three factor model across all metrics. The overall performance of the global adjusted

leverage factor is comparable to that of the Fama-French three factor plus momentum model. Figure 10

confirms the results from Table 9. The predicted versus realized average returns for the test assets of the

global adjusted leverage factor model line up closely on the 45-degree line (10a).

Having tested for the explanatory power of the global adjusted leverage factor in the cross-section of

equity portfolios, I turn to another large set of global assets, that of currencies. Table 10 presents the35The tables summarizing the results of the cross-sectional asset pricing tests follow a format similar to that of Adrian et al.

(2014).

25

results of asset pricing tests using as test assets 24 currency portfolios (6 carry trade, 6 short-term currency

momentum, 6 long-term currency momentum, and 6 currency value portfolios). The factors tested are the

long/short carry portfolio (CAR), a measure of global volatility (VOL), the long/short short-term currency

momentum portfolio (MOM), and the global adjusted leverage factor (Lev.Adj).36 The first three columns of

Table 10 summarize the results of asset pricing tests using factors already proposed in the literature. All

three factors factors appear with statistically significant prices of risk, however the overall explanatory power

of these models is generally low (the highest R2 is that of the momentum factor model and is equal to 47%),

and the null hypothesis of the χ2 test, which tests whether pricing errors are jointly zero, is rejected at the

5% level. Overall, neither of the above three models can sufficiently explain the cross-section of returns

of currency portfolios. The fourth column shows the results for an asset pricing factor model with global

adjusted leverage as the only factor. The price of risk is positive and statistically significant. The adjusted

R2 is 57% with a confidence interval of [0.43, 0.86], and the TOTAL MAPE is 3%. Both metrics are an

improvement compared to those of the models of columns 1 through 3. The χ2 value is significantly lower

compared to that of the other models and the null of pricing errors being jointly zero is not rejected. The

results remain essentially invariable even after the addition of the carry factor into the model (column 5).

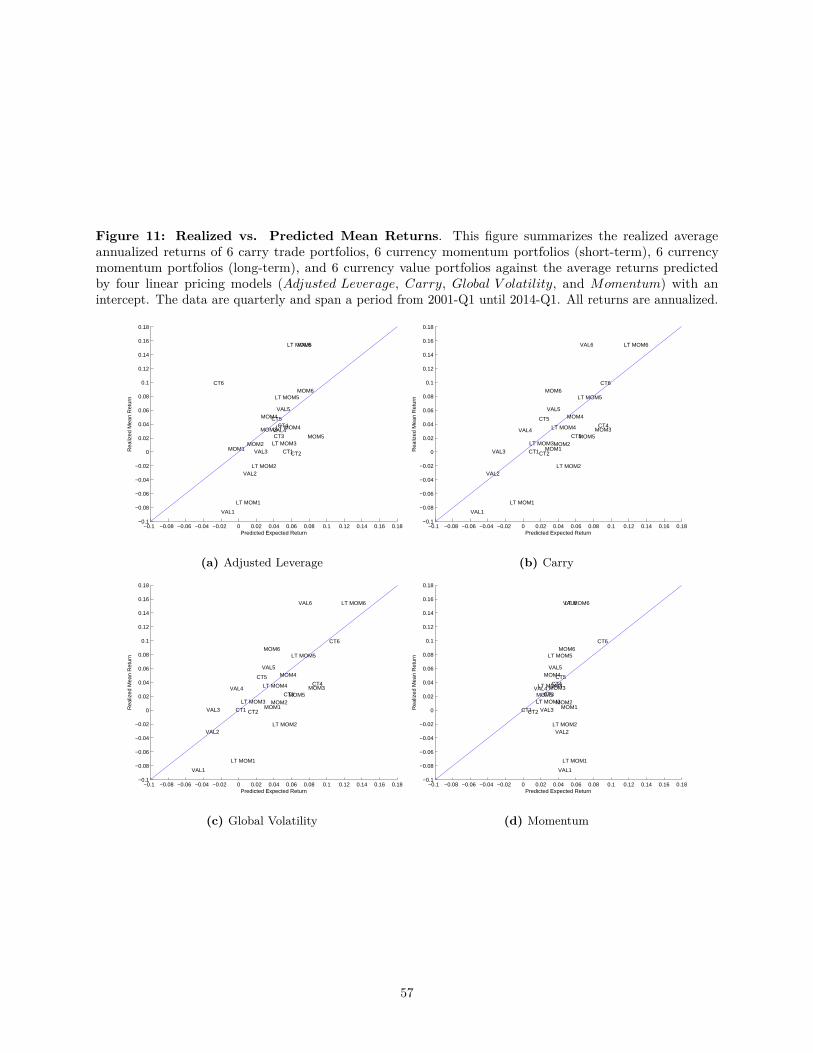

Figure 11 confirms the findings of Tables 8 and 9. The realized versus predicted mean returns using the

global adjusted leverage factor model align closely on the 45-degree line (Figure 11a) yielding the best fit,

followed by that of the momentum factor model (Figure 11a). This comes as no surprise since the global

adjusted leverage factor model exhibits the highest adjusted R2, and the lowest χ2 among all of the models

considered in this exercise.37

Overall, the global adjusted leverage factor explains a large amount of variation in the cross-section of

expected returns of currency and international equities portfolios. It outperforms currency factors, the global

market factor, and the global Fama-French three factor model, whereas it performs equally well with the

global four Fama-French three factor plus momentum model. The price of risk of the global adjusted leverage

factor is positive and of the same order of magnitude across similar test assets. This finding is consistent

with theory and reenforces the argument that the marginal value of wealth of financial intermediaries is an

important component of the determination of asset prices.36See, e.g. Lustig et al. (2011) for the carry trade factor; Menkhoff et al. (2012a), Ang et al. (2006), Adrian and Rosenberg

(2008) for the asset pricing properties of volatility for currencies and equities respectively; Menkhoff et al. (2012b) for momentum.37The low explanatory power of carry, volatility, and momentum seems to be at odds with the asset pricing properties

attributed to them in the literature (see, e.g. Lustig et al. (2011) for carry trade factor; Menkhoff et al. (2012a) for volatility andcarry trade, Menkhoff et al. (2012b) for momentum). This discrepancy is explained by the fact that these factors explain verywell the cross-section of returns of portfolios relevant to the specific strategies from which they were derived. When tested fortheir explanatory power using a wider set of currency portfolios, their explanatory power is lower compared to that of globaladjusted leverage.

26

7.2 Time-Series Analysis

Figure 12 summarizes the results of time-series regressions of the test portfolios’ excess returns on the

adjusted leverage factor. The figures report the estimated coefficients along with a 95% confidence interval,

and the R2 values of the time-series regression for each test portfolio. Figure 12a shows the coefficients for

currency portfolios. The adjusted leverage betas increase in a pattern from left to right as the expected

returns of the currency portfolios increase. This pattern is consistent with the theoretical motivation behind

the construction of the adjusted leverage factor. A portfolio with a higher exposure to adjusted leverage is