financial planning for life

TRANSCRIPT

FINANCIALPLANNING

FORLIFE

LIFE NOW

• EARNING• AIMLESS SPENDING• WEEKENDS,Travels etc.• GET-TOGATHERS,PARTIES etc.

• UNNECESSARY PURCHASES• AIMLESS INVESTMENTS

HOW MUCH YOU ARE SAVING

• Bare minimum: 10 • Good: 10-25%• Very Good: 25-50%• Excellent: Above 50%

Why Financial Planning?

Financial Planning

InflationFuture cost of important

goals would be much higher than present

Lack of planning is the biggest cause of

financial stress

Traditional investment not as attractive

Changing Life Stage & Life Style NeedsVacation, Gizmos, Car,

House, Children…

INDICATIVE FINANCIAL PLANYou are expected to save 50% of your annual income

To Insure your life is your first priorityYou require Life insurance equal to twelve times of your annual

incomeResidue should be invested as followsEquity/Mutual FundsRecurring DepositGoldLand/Property but with due precaution

TO GROW A RETIREMENT CORPUS INVEST IN

EQUITY (Blue chip) 40% DEBT 50% GOLD 5% CASH 5%

ALTERNATIVE TO THE ABOVE IS MUTUAL FUNDS

Financial Planning is incomplete without Life Insurance

Through Life Insurance one has to set up Goals for:

• How much life insurance one needs to protect his family if something was to happen to him

• Children,s education and marriage• Emergency Medical Expenses• As a thumb rule you should have insurance as

8 times of your annual earnings

ESTATE ACCUMULATIONDURING THE EARNING PERIOD

• HOUSE/FLAT/LAND• GOLD/SILVER• PROVIDEND FUND/GRATUITY• SHARES/DEBENCHORS• MUTUAL FUNDS• NATIONAL SAVINGS CERTIFICATES• VEHICLES

• Retirement planning means making sure you will have enough money to live on after retiring from work.

• Should be the best period of your life, when you can literally sit back and relax.

• To achieve a hassle-free retired life, you need to make prudent investment decisions during your working life

• Planning for retirement is as important as planning your career and marriage.

• Compulsory savings in provident fund through both employee and employer.

• It may not be enough to support you throughout your retirement.

• Life takes its own course and from the poorest to the wealthiest, no one gets spared. "Everyone grows older". We get older every day, without realizing. However, we assume that old age is never going to touch us.

• The future depends to a great extent on the choices you make today. Right decisions with the help of proper planning, taken at the right time will assure smile and success at the time of retirement.

• Nuclear families and its attendant insecurity.• Increasing uncertainties in personal and

professional life.• The growing trends of seeking early

retirement and rising health risks are among few important risks.

• Falling interest rates and the sustained increase in the cost of living.

• If you are young, retirement may be the last thing on your mind. But if you think you have a long way to go for to plan for retirement, think again.

It is never too early to prepare for retirement, especially if you want to maintain the same standard of living that you would have got accustomed to by then.

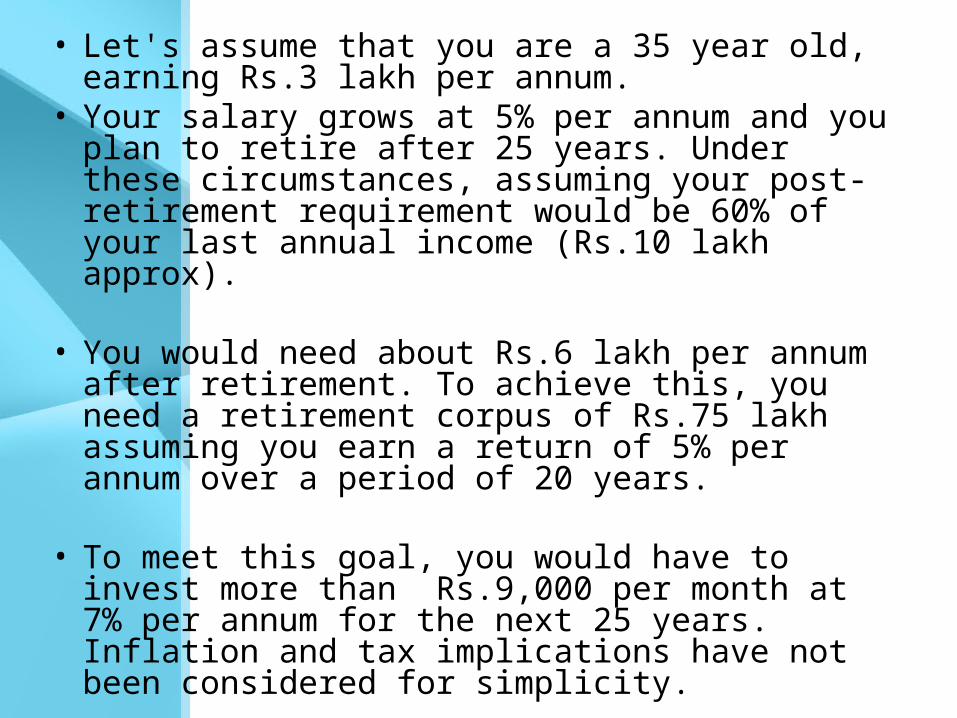

• Let's assume that you are a 35 year old, earning Rs.3 lakh per annum.

• Your salary grows at 5% per annum and you plan to retire after 25 years. Under these circumstances, assuming your post-retirement requirement would be 60% of your last annual income (Rs.10 lakh approx).

• You would need about Rs.6 lakh per annum after retirement. To achieve this, you need a retirement corpus of Rs.75 lakh assuming you earn a return of 5% per annum over a period of 20 years.

• To meet this goal, you would have to invest more than Rs.9,000 per month at 7% per annum for the next 25 years. Inflation and tax implications have not been considered for simplicity.

• The key to a financially independent future is "sooner the better".

• Cautious investors not only save, they save early and regularly. . The catch is to make the power of compounding work one's benefit.

• Retirement should be kept as a top priority because;

• if one does not keep it at the top one might end up depending on one's children, which probably no one would relish.

• Saving and investing regularly makes a big difference at the time of retirement. Investing at regular intervals builds your retirement fund over time and helps you to minimize risk and gives a tension free retirement-a time to pursue your hobbies, fulfill your dreams and passions.

• Saving and investing regularly makes a big difference at the time of retirement. Investing at regular intervals builds your retirement fund over time and helps you to minimize risk and gives a tension free retirement-a time to pursue your hobbies, fulfill your dreams and passions.

This is the usual picture of a soon to be retired person.

Retired is being twice tired, I have thought

first tired of working.then tired of not

Richard Armour

• High percentage of people die during their first year of retirement .One of the reasons being psychological trauma. A sense of feeling that you’re a worn out individual and should be placed in the corner of the house sitting idle most of the time.

• Retirement is the point where a person is not in any kind of employment/ bussiness /occupation

• This usually happens upon reaching a determined age ,when physical conditions do not allow the person to work any more

RETIREMENT IS A PROCESS • People frequently underestimate of this

transition• At least 1/3of retirees experience difficulty

making the transition to retirement• Planning makes a difference

The following changes can be viewed as a normal part of aging

• Decreased cognitive capacity• Increased depression• Increased fears of illness • Increased agitation• Decreased performance speed

TWO STAGES OF RETIREMENT PLANNING

Pre-retirement planningPost-retirement planning

Need for retirement Planning

• Increased life span• Unintended contingencies• Increasing medical cost• Diminishing trend of joint family

system

LIFE EXPECTENCY

Life expectancy is the measure ruler of retirement planning.

With the increasing life expectency,high standards of living and high expectations for the upcoming future,pressure is building up for fund allocation,to meet up the needs of retirement.

Longivity of life expectancy has to be kept in mind while making out a retirement plan

PREPARE PSYCHOLOGICALLY

WHAT IS YOUR ATTITUDE TOWARDS RETIREMENT

Is it an ending, a beginning or both

FEW WAYS TO STAY ACTIVE

Physical activityMeet friends

Help grandkidsGo on a Holiday

Social WorkUse Your Skills

Pen themJoin course

Today’s Retirement• Presents many complex social emotional and

financial issues• Marriage and other familial and social

relationships• Care giving responsibilities and living

arrangements• Role Loss/Gain• Decreased abilities and loss of independence• Grief• Time Management• Rework• Fixed/Reduced income

Prepare for family change• How will you realign your marital relationship?• How will you renegotiate the division of household

chores?• What activities will you do jointly and individually?• How will you set limits and boundaries around your

new found free’time?• What care giving tasks will you have to assume?• Are you meeting your own needs as well as those of

others?

Retirement Impacts Marital Life• Lack of consensus on retirement expectations

will cause problems

• Wives complain of husbands invading their ‘domen’ and requiring attention

PREPARE FOR SOCIAL CHANGES• With whom you will keep in touch?• From whom do you receive support?• To whom do you provide support?• How do you plan to meet new friends?• How will you keep in touch with old friends

and former work colleagues?

ESTATE PLANNING WITH RETIREMENTPLANNING

• ESTATE PLANNING IS THE PROCESS OF DISPOSING OF AN ESTATE

• VARIOUS TOOLS OF ESTATE PLANNING ARE USED LIKE WILLS,TRUSTS,GIFTS Etc.

BEFORE THE DAY OF YOUR RETREMENT• PAY ALL DUES• PAY ALL OUTSTANDING BILLS• PAY ALL OUTSTANDING LOANS

ON RETIREMENT WHAT SHALL BE WITH YOU

• FIXED ASSETS»HOUSE/FLAT/LAND

• LIQUID ASSETS»PROVIDENT FUND»GRATUITY»FIXED DEPOSITS»LEAVE ENCASHMENT

Which are the investment avenues for your liquid assets

• MISBANK DEPOSITS

• CO-OP. SOCIETIES• NSC• SHARES/DEBENCHORES• MUTUAL FUNDS• PENSION SCHEMES

DIVIDE LIQUID ASSETS EQUILLY AND NOMINATE RESPECTIVE HEIRS

DO NOT NOMINATE MINORS

HOW TO DISPOSE OF GOLD/SILVER

• SELL THE ORNAMENTS IN YOUR LIFE TIME

• ENCASH IT

• DIVIDE IT EQUALLY AMONGST YOUR HEIRS

HOW TO DISPOSE OF YOUR HOUSE/FLAT/LAND ETC.

VEHICLESOTHER HOUSEHOLD ARTICLES

Discuss and achieve common consensusAmongst

Sons/DaughtersIn-laws

IF YOU INTEND TO REWORKINVESTMENT AGENCIES

TEACHINGGENERAL ADMISTRATION EXECUTIVE

LEGEAL PRACTICEIF YOU INTEND TO DO SOCIAL WORK

JOIN NGOMARRIAGE BUREAU

START SOME ACTIVITY IN YOUR LOCALITY

Become a Saver, Wise Spender and better Investor