financial reporting hot topics: year- end take aways moderator: heidi roth panelists: chris...

TRANSCRIPT

Financial Reporting Hot Topics: Year-End Take Aways

Moderator:

Heidi Roth

Panelists:

Chris Dubrowski

Bill Harlow

Bill Wagner

Financial Reporting Hot Topics: Year-End Take Aways

Moderator:

Heidi Roth

Panelists:

Chris Dubrowski

Bill Harlow

Bill Wagner

SEC Comments

3Copyright © 2010 Deloitte Development LLC. All rights reserved.

Frequent SEC Comments

• Intangible assets / business combinations

• Taxes• Revenue• Segments• Debt and dividend restrictions• Other-than-temporary

impairments• Pensions• Loss contingencies

• Fair value measurements• Financial instruments• Consolidations/VIEs• Financial statement classifications• Capitalized costs• Discontinued operations• Stock compensation• New accounting standards

4Copyright © 2010 Deloitte Development LLC. All rights reserved.

Comments Outside the Financial Statements

•MD&A• Executive overview• Results of operations• Liquidity• Critical accounting policies• Contractual obligations

•Non-GAAP measures•Risk Factors

•Executive compensation and proxy disclosures

• More analysis, performance targets, benchmarking

• Director qualifications, risk and compensation policies

•Material contracts •Disclosure controls and procedures

• Internal control over financial reporting

5Copyright © 2010 Deloitte Development LLC. All rights reserved.

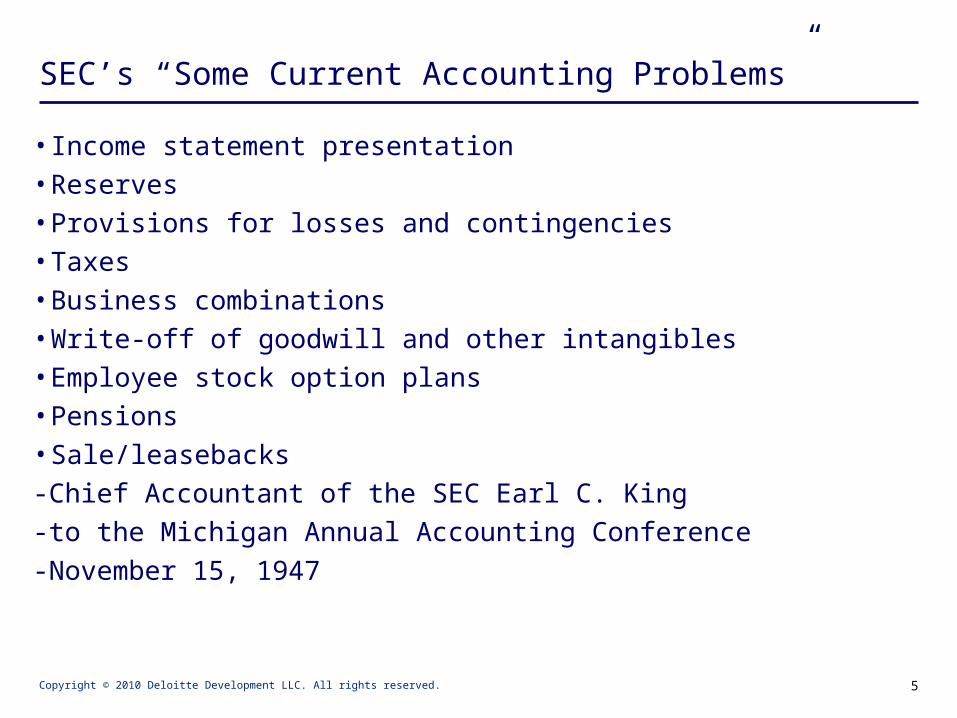

SEC’s “Some Current Accounting Problems”

• Income statement presentation• Reserves • Provisions for losses and contingencies• Taxes• Business combinations• Write-off of goodwill and other intangibles• Employee stock option plans • Pensions• Sale/leasebacks

-Chief Accountant of the SEC Earl C. King

-to the Michigan Annual Accounting Conference

-November 15, 1947

6Copyright © 2010 Deloitte Development LLC. All rights reserved.6

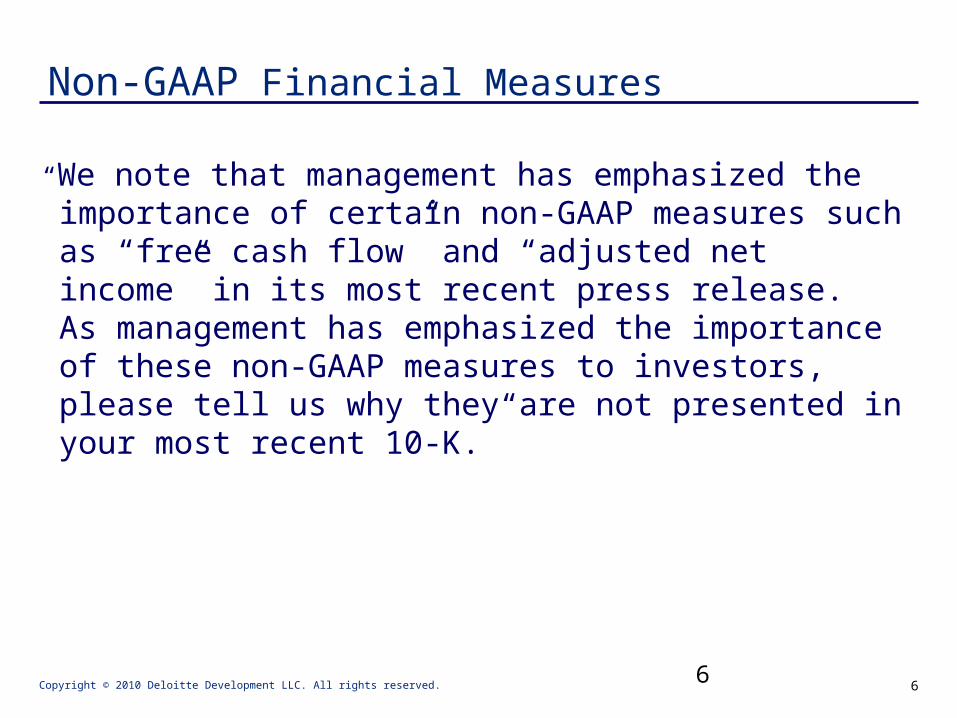

Non-GAAP Financial Measures

“We note that management has emphasized the importance of certain non-GAAP measures such as “free cash flow” and “adjusted net income” in its most recent press release. As management has emphasized the importance of these non-GAAP measures to investors, please tell us why they are not presented in your most recent 10-K.”

7Copyright © 2010 Deloitte Development LLC. All rights reserved.

Impairment – Documentation and Support

“Please provide us with the discounted cash flow model used in your OTTI analysis for (mortgage revenue bonds collateralized by properties A, B and C) as of December 31 and provide supporting commentary for each source of cash flows. Discuss and support the significant assumptions used in the model. Also, please provide us with any independent third party appraisals for (properties A, B and C) and tell us how this information was considered in your discounted cash flow model used in your OTTI analysis.”

8Copyright © 2010 Deloitte Development LLC. All rights reserved.

Liquidity and Capital Resources

“Please provide a comprehensive quantitative analysis of your off-balance sheet arrangements related to your unconsolidated joint ventures that could have a material impact on your future liquidity, particularly in the event that your joint venture partners were unable to meet any of their financial commitments. Address…the financial condition of any significant joint venture partners.”

9Copyright © 2010 Deloitte Development LLC. All rights reserved.

Liquidity and Capital Resources

“We note that your distributions to shareholders and noncontrolling interest holders exceeded cash flows from operations for the current year. Please tell us the sources of cash used to fund these distributions. Additionally, please revise the liquidity section of your MD&A to include a discussion of the sources of cash used to fund distributions.”

10Copyright © 2010 Deloitte Development LLC. All rights reserved.

OP Unit Settlement

“Please disclose within your financial statements the amount that would be paid or the number of shares that would be issued and their fair value of the settlement of the common units of your operating partnership, which are convertible into your common stock on a one-for-one basis or cash, at your option, were to occur at the reporting date.”

11Copyright © 2010 Deloitte Development LLC. All rights reserved.

Critical Accounting Policies

“MD&A disclosures related to critical accounting policies should supplement and enhance the description of the critical accounting policies in the notes to your consolidated financial statements, and are not intended to be a duplication of the footnote disclosure.”

“We see no discussion of any specific judgments or uncertainties associated with your critical accounting policies that would assist readers in assessing the predictive value of your reported financial information.”

12Copyright © 2010 Deloitte Development LLC. All rights reserved.

Dividend Disclosures

“We note that you have included “distributions per share” on the face of your income statement versus in the notes to your financial statements. Tell us how your disclosure complies with the guidance in ASC 260-10-45-5.”

ASC 260-10-45-5:

Per share amounts not required to be presented by this Subtopic that an entity chooses to disclose shall be computed in accordance with this Subtopic and disclosed only in the notes to financial statements…

OK, BUT…

13Copyright © 2010 Deloitte Development LLC. All rights reserved.

Dividend Disclosures (Continued)

S-X 210.10-01(b): “the following additional instructions shall be applicable for purposes of preparing interim financial statements:

(2) If appropriate, the income statement shall show earnings per share and dividends declared per share applicable to common stock.”

14Copyright © 2010 Deloitte Development LLC. All rights reserved.

Significant Unconsolidated Subsidiaries

“Please refer to your disclosure in note XX as it relates to your equity in loss of Joint Venture A. Given the apparent significance of the loss, please explain to us how you considered Rule 3-09 and 4-08(g) of Regulation S-X as it relates to the requirements for separate financial statements and summarized financial information of equity method investees.”

15Copyright © 2010 Deloitte Development LLC. All rights reserved.

Income Statement Geography

“Please tell us how your presentation of interest income within “revenues” complies with Rule 5-03 of Regulation S-X”

“ Reference is made to your presentation of impairment associated with land development activities as a separate line item below other expenses. Please clarify your basis in GAAP for presenting below other operating expenses.”

“In light of your placement of interest expense, please tell us how you have complied with Rule 5-03 of Regulation S-X.”

16Copyright © 2010 Deloitte Development LLC. All rights reserved.

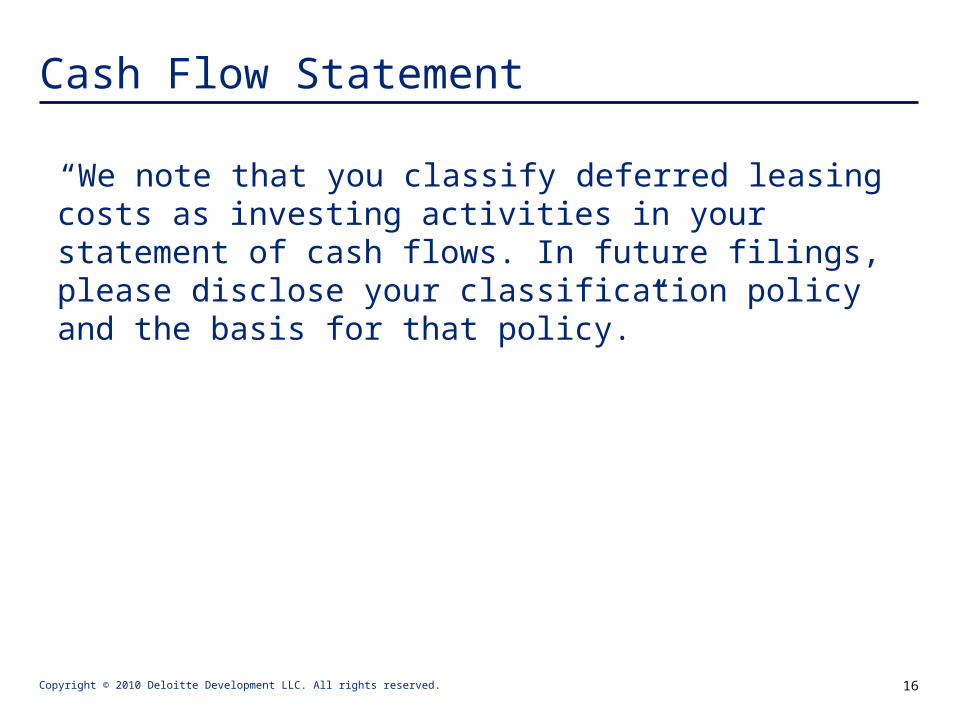

Cash Flow Statement

“We note that you classify deferred leasing costs as investing activities in your statement of cash flows. In future filings, please disclose your classification policy and the basis for that policy.”

17Copyright © 2010 Deloitte Development LLC. All rights reserved.

Litigation

“We note your disclosure, with respect to the XYZ litigation, that you believe the “claim is without merit.” The statement that this claim is without merit is a legal conclusion that you are not qualified to make. Please confirm that you will omit this type of conclusory statement from future filings.”

18Copyright © 2010 Deloitte Development LLC. All rights reserved.

Summarized Quarterly Information Note

“Please revise your quarterly tables to describe the effect of any unusual or infrequently occurring items recognized in each quarter. For example, your table should separately indentify or describe impairments or other significant losses. Please refer to Item 302(a)(3) of Regulation S-K.”

19Copyright © 2010 Deloitte Development LLC. All rights reserved.

Industry Jargon• “Throughout your registration statement, you utilize industry

jargon. For example, please provide a better explanation for “property fundamentals,” “analytics,” “Class A and B+ properties,” “scaled for growth” and “fully integrated multifamily and industrial operating platform.” If you must include jargon that is understood only by industry experts, you must make every effort to concisely explain these terms where you first use them. Please do not use technical terms or industry jargon in your explanations.”

• “Please explain what you mean by “lease-up.” • “You disclose that you “developed” certain properties. Please

disclose what it means to have “developed” these properties.”

• Please explain the phrase “power center.”

FASB’s Revised Exposure Draft FASB’s Revised Exposure Draft on Loss Contingency on Loss Contingency DisclosuresDisclosures

K P M G L L P

David Elsbree

Department of Professional Practice

21

Revised Exposure Draft

• Revised Exposure Draft issued July 20, 2010

• Comments due September 20, 2010

• Proposed effective dates:

― Public entities: fiscal years ending after December 15, 2010 (December 31, 2010 for calendar year-end entities) and in interim and annual periods in subsequent fiscal years

― Nonpublic entities: fiscal years beginning after December 15, 2010 (December 31, 2011 for calendar year-end entities) and in interim and annual periods in subsequent fiscal years

21

© 2010 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG

logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 22051NSS

22

Objective

• An entity shall disclose qualitative and quantitative information about loss contingencies to enable financial statement users to understand:

― The nature of the loss contingencies

― Their potential magnitude

― Their potential timing (if known)

22

© 2010 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG

logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 22051NSS

23

Principles

• In developing the proposed disclosure requirements, the Board decided that:

― During early stages of a contingency’s life cycle, an entity shall disclose information to help users understand the nature, potential magnitude, and potential timing (if known) of loss contingencies. In subsequent reporting periods, more extensive disclosure as additional information becomes available.

― An entity may aggregate disclosures about similar contingencies (e.g., by class or type), so that disclosures are understandable and not too detailed. If provided on an aggregate basis, an entity shall disclose the basis for aggregation.

23

© 2010 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG

logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 22051NSS

24

Threshold for Disclosure

• When assessing materiality, entities may not consider insurance recoveries

• No change in threshold under existing requirements to disclose:

― Asserted claims and assessments whose likelihood of loss is at least reasonably possible

― Unasserted claims or assessments, if it is probable that a claim will be asserted and it is at least reasonably possible that the outcome will be unfavorable

• Example added to implementation guidance on unasserted claims that may require disclosure

― Existence of peer-reviewed studies in reputable scientific journals that indicate potential hazards related to the entity’s products or operations

24

© 2010 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG

logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 22051NSS

25

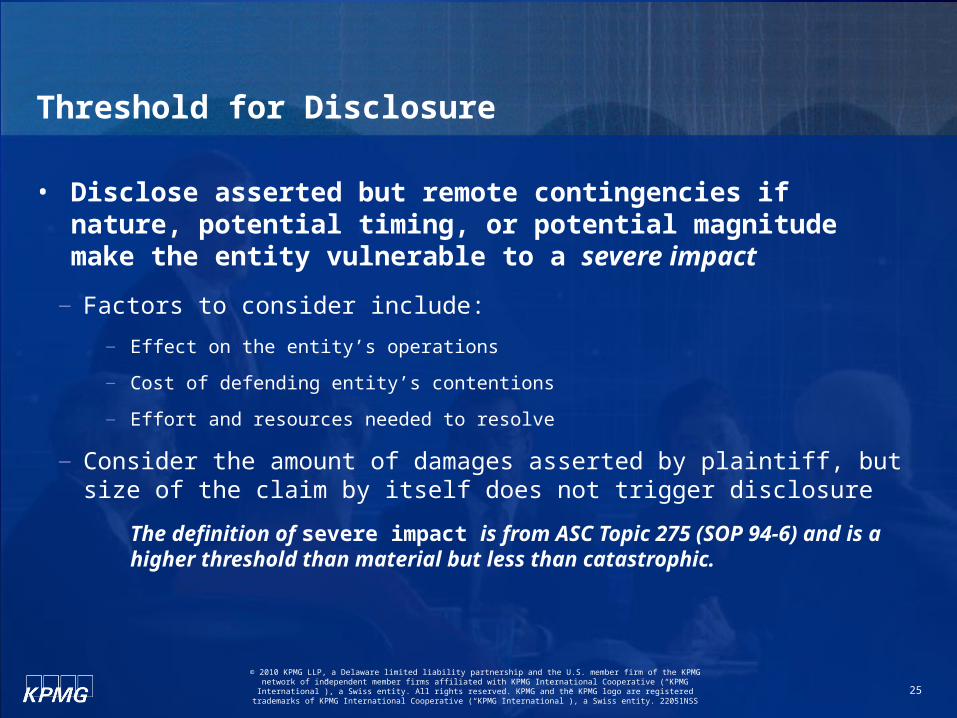

Threshold for Disclosure

• Disclose asserted but remote contingencies if nature, potential timing, or potential magnitude make the entity vulnerable to a severe impact

― Factors to consider include:

― Effect on the entity’s operations

― Cost of defending entity’s contentions

― Effort and resources needed to resolve

― Consider the amount of damages asserted by plaintiff, but size of the claim by itself does not trigger disclosure

The definition of severe impact is from ASC Topic 275 (SOP 94-6) and is a higher threshold than material but less than catastrophic.

25

© 2010 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG

logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 22051NSS

26

Proposed Qualitative Disclosure Requirements

• Information to enable users to understand the loss contingency’s nature and risks

• For asserted litigation contingencies:

― In early stages, at a minimum, the contentions of the parties, for example:

― Plaintiff’s basis for the claim and the amount claimed

― Entity’s defense or statement that not yet formulated

― More extensive disclosure as additional information about a potential unfavorable outcome becomes available

26

© 2010 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG

logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 22051NSS

27

Proposed Qualitative Disclosure Requirements

• For individually material contingencies, enough information to enable users to perform additional research using public sources. For litigation:

― Name of the court of agency in which proceedings are pending

― Date proceedings were instituted

― Principal parties

― Factual basis alleged to underlie proceedings

― Current status

27

© 2010 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG

logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 22051NSS

28

Proposed Qualitative Disclosure Requirements

• If disclosures are aggregated, disclose the basis for aggregation and information to enable users to understand the nature, potential magnitude, and potential timing (if known) of loss.

― For example, if there are a large number of similar claims, consider disclosing the activity (e.g., in a rollforward) in:

― Total number of claims outstanding

― Average amount claimed

― Average settlement amount

• Contingencies need to be sufficiently similar to be included in one class, primarily on the basis of nature, terms, and characteristics

28

© 2010 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG

logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 22051NSS

29

Proposed Quantitative Disclosure Requirements

• Estimate of the possible loss or range of loss and amount accrued, if any

We have produced an analysis indicating that actual damages incurred by Entity B could have been limited to a range of $50,000 to $200,000. Because we are unable to estimate a specific amount within this range as more likely than any other amount, we have accrued the low end of the range, $50,000, as of September 30, 20X2.

• If loss cannot be estimated, a statement to that effect and the reason

At the time of this report, Entity B has not specified an amount claimed for damages, and discovery has not yet begun. We have not completed our analysis of the relevant laws about performance under a contract in these circumstances and have not formulated our defense. As a result, we are unable to estimate a potential loss or range of loss, if any, at this time.

29

© 2010 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG

logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 22051NSS

30

Proposed Quantitative Disclosure Requirements

• Publicly available information (such as claim amount or amount of damages indicated by expert witnesses’ testimony)

During discovery, Entity B has provided an analysis claiming damages of $2 million for lost profits as well as penalties for late delivery to its customer under a contract that required the use of our widgets.

• Other relevant nonprivileged information to enable users to understand the potential magnitude of possible loss

We entered into a contract to provide 1,000 widgets for $1 million to Entity B by December 15, 20X1. Lightning struck our manufacturing plant on November 30, 20X1, and we did not deliver the widgets.

30

© 2010 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG

logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 22051NSS

31

Proposed Quantitative Disclosure Requirements

• Information about possible recoveries if

― Provided to or discoverable by the plaintiff

― A recovery receivable has been recognized

• If the insurance company has denied, contested, or reserved its rights related to the claim for recovery, entities would be required to disclose that fact

Our business interruption insurance carrier has agreed to defend us with a reservation of rights. There is no deductible for defense funding; we have a deductible of $500,000 for actual damage claims, if any.

31

© 2010 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG

logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 22051NSS

32

Tabular Reconciliation

• Tabular reconciliation of recognized (accrued) loss contingencies

― Aggregated by class of contingency

― Description of the significant activity in the reconciliation

― Exclusion of contingencies whose underlying cause and ultimate settlement occur in the same period

― Required in both interim and annual periods

― Exemption for nonpublic entities

32

© 2010 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG

logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity. 22051NSS