financial statement analysis

DESCRIPTION

understanding of financial statements and tools used to analyse themTRANSCRIPT

04. FINANCE DEPARTMENT OF HDFC LIFE

05. A .ConclusionB. RECOMMENDATION AND SUGGESTION

06. ANNEXURE

07. BIBLOGRAPHY

CONTENTS

01. INTRODUCTION PURPOSE OF THE STUDY AIM OF THE STUDY OBJECTIVE OF THE STUDY

02. Organization InformationA .About HDFCSLICB .company profileC. what is insurance?D .scope of insuranceE .objectiveF .Award and accoladeG .product of HDFCSLH .About ULIP

03. Descriptive workA. Factsheet

B. Profiling of prospects C. Mode of contacting prospects

D. Total number of people contacted .

2

Purpose of study

During my summer training in the Housing Development finance corporation standard life insurance company limited (HDFCSL). I have gotten the work of Analyzing financial need and manage the funds of the policies. The main focus area of the company is to manage and focus of customer profit which gets through managing the funds of the policy. Indeed the work of financial analyst is very significant and gives more and more customer assistance to the customer so company can earn customer base and through strong customer base gets more and more policies distribution and company can sell the policies. The main motive of this project is analysis of financials of HDFC LIFE.

HDFCSL is one of India’s leading private insurance companies. It offers both individual and group insurance solution. It is a joint venture between HDFC and a group of company of Standard Life. I have chosen insurance sector as the place for summer training because in these days this sector is in boom and it will never go down. All people invest their money in insurance and get more benefited. In the sector the work of Finance is more challenging then the other sector because there is 17 insurance companies in the market who are giving competition to each other and the work of convince people for investment in respective company is a challenging work and success in the sector proves that the respective person is a good f inance advisor . Today insurance sector India is on boom because all people want to invest. Those who don’t know about investment in share market and don’t want to invest in mutual funds they invest in insurance sector. Insurance sector gives them investment plus risk cover. Those who don’t want to take risk in the investment go to insurance sector. It also gives income tax benefits to the peoples. Insurance company are now launching ULIP plan and gives chance to the investor to choose their investment pattern according to their fund investment table. This fund investment tells us that how much the investor want to take risk. Generally in the ULIP plan, the thesis is that “The more you risk the more you have profit.”

4

AIM OF STUDY

During the summer training I have done my work through telephone calling, natural market, and contact person having gone to their home. In the entire work I have contacted person who is policy holder of the company or willing customer and prospect customers of the company

I found that most of person can earn as well as get insured th rough insurance company and save taxes, life assurance with little effort, which will give him back support as a HEAD of the family in the diverse situation.

This project will help to understand the current market scenario and marketing in stiff competition. Being a student of management I can draw the relevant conclusion from the financial analyze and give the appropriate suggestion to the organization.

The company can take decision according to the suggestions and it will provide better experience to the students for their bright carrier. My project will provide help in these matters which are thus:-

Analyze the people perception about HDFC

Study financial markets and analyze the financials of the company

To find out the competitive edge of the company over the competitors.

OBJECTIVE OF THE STUDY

The project was an attempt to explore the “Analyzing financial need and manage the funds of the policies” in HDFC LIFE. The project was started on 10th June, after knowing all the relevant information about the company insurance product and policies and its competitor’s insurance products in accordance with the prescribed schedule mentioned by management of HDFC LIFE.

The project started in Janakpuri branch where covering all the investors whom funds are down and bearing loss. In this process I meet 90 policy holders who facing loss .I have tried to convince them to continue with company and remain with the company. During my work I found the perception of the people about insurance, what they desire from it, and if they suffer loss than what they think. What the organization should do for the policyholder who suffering from loss. Many of the customer is not aware about the share market and if they suffer loss than they blame either company or agent/sales manager. So I have to manage the customers to remain with us and provide them the best financial solution to them

As I can say this project gives the abstract of my work at HDFC LIFE as financial analyst

Chapter: - 1

INTRODUCTION OF HDFC

LIFEINRODUCTION OF HDFC LIFE

Risk is found everywhere. It cannot be eliminated together, only it can be

minimized. Human life is full of risk. There is a risk when a man walks on the

road, travels in a bus, train or an aero plane and when he is engaged in trade,

profession or business. Also there is a risk when property is destroyed by fire,

flood, earthquakes, etc. Thus, the involvement of risk is inescapable.

4% 20%

35%

41%

Risk

DroughtEarthquakesFloodsStorms

Risk Percentage

Drought 4%

Earthquakes 20%

Floods 35%

Storms 41%

Insurance is a method by which we can spread over the risk. It is a way of

reducing uncertainty of occurrence of an event. Insurance is entirely a method

of co-operative endeavor where in the loss caused by a particular risk is spread

over among a large section of persons. Insurance is a process in which a large

number of persons collect their small contributions, called the premium, in a

pool and out of this losses are paid to the suffering persons.

The Business of insurance is related to the protection of the economic

values of assets. Every asset has a value. The asset would have been created

through the efforts of the owner. The asset is valuable to the owner, because he

expects to get some benefits from it. It is a benefit because it meets some of a

factory or a cow, the product generated by it is sold and income is generated. In

the case of a motor car, it provides comfort and convenience in transportation.

There is no direct income. Both are assets and provide benefits.

INTRODUCTION OF THE COMPANY

HDFC Life Insurance Company Limited. is one of India's leading private

insurance companies, which offers a range of individual and group insurance

solutions. It is a joint venture between Housing Development Finance

Corporation Limited (HDFC Limited), India's leading housing finance

institution and a Group Company of the Standard Life Plc, UK. As on February

28, 2009 HDFC Ltd. holds 72.43% and Standard Life (Mauritius Holding)

2006, Ltd. holds 26.00% of equity in the joint venture, while the rest is held by

others.

HDFC Life believes that establishing a strong and ethical foundation is an

essential prerequisite for long-term sustainable growth. To ensure this, we have

concentrated our focus on expansion of branch network, organizing an efficient

and well trained sales force, and setting up appropriate systems and processes

with optimum use of technology. As all these areas form the basic infrastructure

for establishing the highest possible customer service standards. Our core values

are drilled down to all levels of employees, as these are inviolable. We continue

to promote high integrity in business practices and shun short cuts and unethical

practices, as we wish to be perceived as an institution with high moral standing.

Since our inception in 2000, when the Indian insurance space was opened for

private participation, we have consistently focused on setting benchmarks in all

aspect on insurance business. Beingthe first private player to be registered with

the IRDA and the first to issue a policy on December 12, 2000,

The HDFC was established in 1977, for the purpose of providing the home loan

for long term

HDFC is rated as (AAA) by the CRISIL and ICRA.

In the year 2004, it was awarded DREAM HOME AWARD.

It has got 3rd rank in the investment management, in year 2006.

One of the largest financial institution of India with more then 2 million

satisfied customer base.

HDFC HAS FOLLOWING GROUP COMPANIES

HDFC Ltd.

HDFC Standard life

HDFC Mutual fund

HDFC Securities

HDFC Bank

HDFC realty.com

HDFC CIBIL

HDFC Chubb General Insurance Co. Ltd.

HDFC Centre For Housing Finance

HDFC Distribution

HDFC Intel net

HDFC Securitization

HDFC Deposits

HDFC Home Loans

OUT STANDARD LIFE (U.K)

Founded in 1825, and is now one of the largest life Insurance companies in the

world.

Strong reputation build over 182 years

Currently over 5 mn. policyholders benefiting from the services offered

Europe’s largest mutual life insurer

Values

1.Integrity

Honest and Truthful in every action

Transparency

Stick to principles irrespective of outcome

Be just and fair to everyone.

2.Innovation

Building a store house of treasures through experiences.

Looking at every product and process through fresh eyes everyday.

3.Customer Centric

Understand customer expectations by keeping him as the centre – point.

Listen actively

Understand customer needs and deliver solutions.

Customer interest always supreme.

4.People Care

Genuinely understanding the people we work with.

Guiding their development through training and support.

Helping them develop requisite skills to reach their true potential.

Know them on a personal front.

Create an environment of trust and

Respect for the time of others.

5.Team Work

Whole team takes the ownership of the deliverables.

Consult all involved, understand and arrive at a company Co-operate and sup-

port across departmental boundaries.

Identify strengths and weaknesses according allocate responsibility to achieve

common objectives.

6.Joy and Simplicity

Environment that fosters fun in the form of celebration of individual and team

success.

To encourage work as fun that contributed to personal and organizational devel-

opment.

Joy is also derived through simple processes and forms.

VISION STATEMENTS

“ The most successful and admired life insurance

Company, which means that we are the most trusted

Company, the easiest to deal with, offer the best value

for money, and set the standards in the industry. In

short, “The most obvious choice for all”

Plans

Traditional ULIP

DIFFERENT PLANS OF HDFC SLIC

Traditional

Traditional plan is a life insurance solution that provides the client only guar-

anteed return.

ULIP (Unit Linked Insurance Plan )

Unit Linked insurance plan is a life insurance solution that provides the client

with the benefits of protection & flexibility in investment .It is solution which

provides for life insurance where the policy value at any time varies according

to the value of the underlying assets at the time.

CHAPTER-2

DISCRIPTIVE WORK

LIFE INSURANCE SECTOR:

India is emerging a some of the two of the largest markets in the world for life insurance products, the other being China. In the case of India, the three key drivers of growth are a large insurable population, a high savings rate, roughly at about 25 percent and a low penetration, at a mere 2.3 percent. In the 11 months of fiscal year 2004-05, life insurance companies collected premium worth Rs172 billion and the market grew by a whopping 32.4 per cent during the year. Of this, the public sector Life Insurance Corporation (LIC) had the lion's share of the market with premium totaling Rs134 billion. Private sector players recorded a spectacular growth of 129 percent over the last year, compared to LIC's growth of 18 percent. India's GDP growth rate of 6 percent per annum holds great potential for the sector. According to one estimate real life premium are expected to grow at a compounded annual rate of 15 per cent over the next ten years.

How does India's life insurance market compare with China's? While India's market is currently the fifth largest, China's is the third largest in Asia after Japan and Korea. Low penetration rate of insurance products is common to IndiaandChina-atjustabout2.3 percent. In China, the savings rate is at 35 percent while for India it is a little lower at 25 percent. A large part of the growth of the life insurance market in China was driven by the conversion of bank deposits into endowment products. Demographically China's population is ageing faster than India's FDI in Insurance Sector. The government of India is planning to increase the equity limit for foreign direct investment from the current 26 percent to 49 percent in the insurance sector. Liberalizations of the FDI policy, including the Budget proposals for raising the sector al caps in insurance is one of the main factors for the higher FDI inflows during the current year. In 2003-04 the total FDI inflows in the country touched $3.4 billion. Indian insurance companies have been pushing for the FDI limit to be raised. The current paid-up requirement of Rs1 billion for general insurance and Rs2 billion for life insurance have become difficult targets to achieve for the companies. The companies feel that injection of additional foreign equity would reduce the costs. The sector was liberalized for private players towards the end of 1999. Currently, there are 14 insurance companies, including the key public sector company Life Insurance Corporation, in the life insurance sector and 13 general insurance companies.

Changing Demographics

In1999, according to KSA-Techno park, savings and investments comprised14 percent of an Indian consumer’s expenditure. The other items included grocery (44 percent), personal care items (6 percent), consumer durables (6.6 per cent), clothing and books and music (5 percent each), eating out (8 per cent), movies (1 percent). By 2003, expenditure on savings and investments had declined to just 4.1 percent. The other items included grocery (41percent) , personal care items (7.6 percent), consumer durables (6.6percent), clothing (6.9 percent), eating out (10.8 percent), movies and theatres (4.6percent), books and music (7.6 percent), vacations (3.9 per cent). Clearly, the increased spending on other items have had a huge impact on the amount people are spending on savings and investment products. (Source: Business World’s Marketing White book 2005).

Composition of Household Financial Savings 1991 1996-97 2002-0

Currency 10.6% 8.6% 8.5%

Deposits 33.3% 48.2% 41.5%

Of which Deposits with non banking companies 2.2% 16.4% 1.6%

Share sand debentures 14.3% 6.6% 2.7%

Small savings (central govt. schemes) 13.2% 7% 14.3%

Life insurance 9.5% 10.1% 15.5%

Provident and pension funds 16.9% 19.1% 14.3%

Source: RBI Annual Reports.

Key Players in the Indian Market

While the public sector LIC dominates the Indian life insurance market with nearly 80 percent of the market share. It has 248 branches, 115,000 employees and over 1 million agents. It has also been improving internal processes and systems, upgrading skills of its agency force and managers And developing innovative products. LIC sold 1.69 corers policies during the year compared to 18 lakh policies sold by all the private players.

ICICI Prudential is the leader among the private players with a market share of 6.69 percent after its premium collection totaled Rs11.54 billion. Bajaj Allianz with sales of Rs 4.9 billion had a market share of 2.86 percent. Birla Sun Life with sales of Rs 4.8 billion had a market share of 2.81 percent and SBI Life with premium collection of Rs 3.9 billion, a market share of 2.29 percent. With its combination of aggressive marketing through an agency force and the use of the banking channel, ICICI has emerged as a key player. Initially, the company drove new business by opening branches in new locations. The focus has now shifted to penetrating the locations for increasing market share. The company is also trying to get higher penetration in the High Net Worth segment. The company has seven bank assurance partners and this is the largest contributor to non-agency business. It also has 15 key non-bank partners and 800 financial sales consultants. As of September 2004, it had 90 branches in 60+ locations. It took the initiative in launching non- traditional products such as life-stage products, retirement solutions and child plans. It also focused on Unit Linked Plans (ULIPs) to target new consumer segments. It has a presence in 15 states through partnership arrangements and as of 2003-04, it sold64, 764 policies in rural areas.

HDFC Standard Life has established its branches in 110 locations and is targeting non-metro towns. It is hoping to leverage its “pedigree/parentage” to gain more customer acceptance. As a result, it is focusing on quality – not

39

Just volume growth. It has developed some innovative products like the Loan Cover Term Assurance Plan which provides a lump sum in case of death of the assured life during the term plan. Aimed at the growing segment of home loan takers, the plan helps the family to repay the outstanding loan. Given that HDFC has a huge database of home-loan customers; it can easily tap into this resource to acquire new business. The company is leveragingIts large customer database of home loan and banking clients to cross-sell insurance products.

Birla Sun Life

Birla Sun Life was the first to offer ULIPs in the Indian insurance market. And this has been the primary driver of its growth over the last one year. The company has been investing in customer education and feels that as a result customers don't view ULIPs as mutual funds but long term insurance. As of 2004, the company had 33 branches, 10,274 agents, 79 corporate relationships and 10 bank assurance partners.

Bajaj Allianz has been focusing on second tier towns and cities which are yet to witness the entry of other life insurance players apart from LIC. It is using first mover advantage by opening an office in the most prominent location in a non-metro town. It hires local people who are trained. Its mantra is to develop only the indispensable infrastructure so that it can match the pricing of LIC. Apart from that it claims that it is the only private player to provide policy servicing at the branch level .Standard Chartered is currently its biggest partner followed by Syndicate Bank and Centurion Bank. The biggest challenge that the company faces is the weak infrastructure – particularly transport and communications – in the smaller cities. It is also facing a challenge in terms of banking channels, particularly for customers who bank with cooperative banks, where delays in clearingCheques are in evitable. Tied agencies comprise the biggest channel (68%) of new business acquisitions for Bajaj Allianz. Bank insurance (27%) is the other significant channel of growth for the company.

Product Preferences among Consumers

Pension policies are becoming popular as people prefer to opt for solutions that can offer them a regular income after retirement rather than a lump sum on retirement. Measurable policies for a bulk sum are being bought only for limited single use such as purchase of a house, children’s higher education, marriage, etc. This consumer trend is likely to helpcompanies that offer pension schemes. Term policies are finding favor with

40

Youngsters. Term insurance policies are also finding more and more takers among the younger generation of consumers. Because the offer protection at extremely low costs.

It is assumed that life insurance is purchased only to avail of tax-breaks. But the fact remains that while the tax paying population in the country is just about 20 million, there is a huge population that has not been tapped. Only the urban salaried class who fall in the tax net has been targeted for life insurance policies for tax-saving purposes. The other income-earning classes such as businessmen, professionals, farmers, provide a great opportunity for life insurance marketers. There is a need to tap these customer segments effectively. Currently all their disposable income is going into purchase of consumer durables such as washing machines, TV, refrigerators and mobile phones(as is evident from the fact that spending on savings/investment products has declined from 14 percent to 4 percent in the past decade).

Mutual Funds (MF) have benefited the most during the last two years. Take the example of the Systematic Investment Plans (SIP) of mutual funds. In just one quarter ICICI PRU MF sold 20,000 SIPs and it has the potential of selling about 100,000 new SIPs in a year. There are 33 Mutual Fund companies in the country and based on this trend one could say that the estimated fund in flow in MFs through this route alone could touch the Rs20 billion per month. Due to the good performance of MF during the past 2 years, life insurance companies have lost out to mutual funds.

PROFILING PROSPECT

For the Providing assistance of financial management there are certain criteria for the selection of policy holder. These criteria differ from different insurance company. We can divide the profiling prospect of HDFCSLIC in two ways.Which are thus:-

1.H.N.I (HIGHLY NET WORTH INDIVIDUALS)

Highly net worth individuals are those persons who having yearly income more than 20 lacs and they are specially treated as H.N.I clients and they have provided relationship manager who watching and manage their funds and provided financial advices and updating all information of policies

2.LOYAL CUSTOMERS FUND VALUE AND HAVING DOWN

Every Company Want more and more business and market share and we all know that the work in insurance sector is totally based upon the customer base. The more you have customer the more you earn business. So HDFCSL provide the facility to customers that they can contact with financial assistant in the company and manage their funds which is in loss or customer is not aware about their policies and managing funds also.

TOTAL NO. OF PEOPLE CONTACTED

During the work of financial Assistance I have contacted 100 people including phone calling, meetings, and the other efforts. In these 100 people I have gotten appointment of 65people. In the 65 person I have assisted 39 people. The percentage of converting the profits at 9%.

During the meeting time with the customer these questions are generally asked by them which are thus:-

Which type of this policy in which I m getting loss!

Our premium will charge by your company or

premium is invested or not?

How your policy is working?

How can I believe on you and your company?

Mostly person have still faith in LIC so I have to convince them against theLIC.

RESEARCH METHODOLOGY

ABSTRACT OF MARKET RESEARCH

Marketing Research provides information that assists and organization to define opportunities for product development and market strategy. It works by assessing whether marketing strategies are accurately targeted, and by identifying market opportunities or changes that are required by customers. Market research tends to confirm issues that are well-known in a market initially, but if planned well and effectively it will also identify new opportunities, market niches, or ways by which to improve sales, marketing and communications activities.

WHY MARKET RESEARCH STUDY

The role of market research, therefore, is to reduce uncertainty in decision making, to monitor the effects of decisions taken, and identify the performance of a company or a product in the market. During internship my market survey was related with the distribution enhancement of the insurance policies of HDFCSL. To be more specific, we can list five key uses for market research, namely to:

a. Identify the size, shape, and nature of a market, so as to understand the market and marketing opportunities.b. Test out strategic and product ideas which help to define the most effective customer-led strategies.c. Monitor the effectiveness of strategiesd. It will define when marketing expenditure, promotions and targeting need to be adjusted or improved.

The variety of purposes listed above makes it clear that market research is not simply a “first check.”It is useful ahead of any action, but it also provide same answer of checking and refining views as operations proceed. Companies, especially those for which budget seem tight, who have selected one of these uses for market research are always concerned to make the research a worthwhile investment. Best results come when their marketing and sales planning is influenced by the results of research. In other words, when research pays for itself by providing a basis for change and improvement in operational matters.

RESEARCH METHODOLOGY

Research methodology is a way to systematically solve the research problem.

It may be understood as a science of studying now research is done

systematically. In that various steps, those are generally adopted by a

researcher in studying his problem along with the logic behind them.

It is important for research to know not only the research method but also

know

methodology. ”The procedures by which researcher go about their work of

describing, explaining and predicting phenomenon are called methodology.”

Methods comprise the procedures used for generating, collecting and

evaluating

data. All this means that it is necessary for the researcher to design his

methodology for his problem as the same may differ from problem to

problem. Data collection is important step in any project and success of any

project will be largely depend upon now much accurate you will be able to

collect and how much time, money and effort will be required to collect that

necessary data, this is also important step.

Data collection plays an important role in research work. Without proper data

available for analysis you cannot do the research work accurately.

OBJECTIVE OF PROJECT

My project is being undertaken in HDFCSL in which finance management program and distribution enhancement of insurance policies of HDFCSL has been implemented as a marketing strategy. HDFCSL tied up with world class insurance product.

Primary Objective

The primary objective of my project is to provide Financial assistance and to increase market share of HDFCSL. In the insurance sector the main work is done by the financial planning manager who brings selling for the organization as well providing the best solution for policies which is not in profit. It improves the services of the organization.

Secondary Objective

In this point we can conclude the company objective which is to increase the market share in the insurance sector and this will happens it becomes more beneficiary and reliable to the customer. Customer should have faith on it. It is trying to do it. Today it comes under top 5 insurance companies. It wants to reach on the top.

Working Procedure

In my summer training I have targeted Delhi. I have collected my data some parts of Delhi. Here I have to approach various detail of insurance product of HDFCSL and the other competitor of it, suggestions, its marketing strategy and its advertisement. As a part of marketing research I also have collect the data in order to find out market share of HDFCSL from our sample space. During the period I was in continuous touch with my senior and sales manager and I have to submit daily report of my work and full information about phone calls and questioners. Questionnaire consisting of open ended questions was used for collecting the information.

Sample Area

My working area was Delhi. As we know that those person will invest in insurance sector who are salaried or professional. I have targeted those person who’s age is equal or more than 25.

48

28

Instrument Used

I have collected my data form LIFE ASIA and through phone calling. Life asia is the software which used by every insurance company and this software help me to know the customer details and customer policy information which help me providing best solution through discussion with my seniors.

Types of data collection

There are two types of data collection methods available.

1. Primary data collection

2. Secondary data collection

1) Primary data

The primary data is that data which is collected fresh or first hand, and for first

time which is original in nature. Primary data can collect through personal

interview, questionnaire etc. to support the secondary data.

2) Secondary data collection method

The secondary data are those which have already collected and stored.

Secondary data easily get those secondary data from records, journals, annual

reports of the company etc. It will save the time, money and efforts to collect

the data. Secondary data also made available through trade magazines, balance

sheets, books etc. This project is based on primary data collected through

personal interview of head of account department, head of SQC department and

other concerned staff member of finance department. But primary data

collection had limitations such as matter confidential information thus project is

based on secondary information collected through five years annual report of

the company, supported by various books and internet sides. The data collection

was aimed at study of working capital management of the company

29

We used both methodology i.e. primary and secondary

We take the sample size of 100 POLICY HOLDERS

Sample location is Delhi

This is stratified sampling

30

LIMITATIONS OF THE STUDY

Limitations of the study

Following limitations were encountered while preparing this project:

1) Limited data:-

This project has completed with annual reports; it just constitutes one part of

data collection i.e. secondary. There were limitations for primary data collection

because of confidentiality.

2) Limited period:-This project is based on five year annual reports. Conclusions and

recommendations are based on such limited data. The trend of last five year

may or may not reflect the real working capital position of the company

3) Limited area:-

Also it was difficult to collect the data regarding the competitors and their

financial information. Industry figures were also difficult to get.

31

FINANCE DEPARTMENT

32

CRM is also referred to as Customer Service Management. Generally organizations are more

focused on the path they travel through to reach the success or determined goal. The stages

they traverse includes design, development, marketing, service support, analyzing managerial

track, channeling the development phase, research and development and many more. These

stages of one’s business life are as a whole supported with the Customer Relationship

Management features.

In the field of business development, and short term goal tracking with standard terms and

strategies, one must keep up certain flexible terms of communicational relationship and

managerial provisions among the company employees, customers, and clients and with

various departmental staff and members. This enhances a co-operative and comfortable zone

to make the right move of the company development on time.

Focusing on the marketing department, it is important to realize the important of promoting

one’s products sales via advertisements, and efficient marketing strands with better quality.

Advertising has to be powerful means to reach the targeted customers in a short time span

with less investment for a perfect outcome of the resulting sale. Sale includes product quality,

competitiveness, advertisement, managing the service to meet the requirements of the clients

and many more.

Marketing one’s product means to take the product to the customers who are into the track or

into the field of trade. Sales department is specific in making the product move to the clients

with respect to the deal of sale. This department is more concerned about the sales of the

product that make use of customer service and management terms to keep up good terms on

serving the customers with help-line service to solve problems related to purchase and utility

of products from the company.

Benefits of CRM techniques are more focused towards customer management and services.

Customer relationship management attracts and retains the customers winning the growing

loyalty of the customer and company relationship. CRM processes helps in guiding the way

an organization runs that are targeted generating quality leads, sales and services that are

more focused on the goals and objectives. They help in forming a tie between customer and

organizational relationship that improves the customer satisfaction with the high quality

service and makes the customers feel comfortable to take up business in futurity.

In many industries customers’ experience with a company’s customer service can

significantly affect their overall opinion of the product. Companies producing superior

products may negatively impact their products if they back these up with shoddy service. On

33

the other hand, many companies compete not because their products are superior to their

competitors’ but because they offer a higher level of customer service. In fact, many believe

that customer service will eventually become the most significant benefit offered by a

company because global competition (i.e., increase in similar products) makes it more

difficult for a company’s product to offer unique advantages.

Customer service manifests itself in several ways, with the most common being a dedicated

department to handle customer issues. Whether a company establishes a separate department

or spreads the function among many departments, being responsive and offering reliable

service is critical and in the future will be demanded by customers.

Our Vision & Values

Our Vision

'The most successful and admired life insurance company, which means that we are the most

trusted company, the easiest to deal with, offer the best value for money, and set the

standards in the industry'.'The most obvious choice for all'.

Our Values

Values that we observe while we work:

Integrity

Innovation

Customer centric

People Care "One for all and all for one"

Team work

Joy and Simplicity

ORGANIZATIONAL STRUCTURE-

BRANCH DEVELOPMENT MANAGER

34

EXECUTIVE SALES MANAGER

SR. SALES MANAGER SR. SALES MANAGER

8 TO ASST. SALES MANAGERIN EAH SR. SALES MANAGER

25 TO 35 ADVISORES IN EACHASST. SALES MANAGER

Figure 1.2 Organization Structure

35

INDUSTRY OVERVIEW With an annual growth rate of 15-20% and the largest number of life insurance policies in

force, the potential of the Indian insurance industry is huge. Total value of the Indian

insurance market (2010-11) is estimated at Rs. 550 billion (US$10 billion). According to

government sources, the insurance and banking services contribution to the country's gross

domestic product (GDP) is 7% out of which the gross premium collection forms a significant

part. The funds available with the state-owned Life Insurance Corporation (LIC) for

investments are 8% of GDP. Till date, only 20% of the total insurable population of India is

covered under various life insurance schemes, the penetration rates of health and other non-

life insurances in India is also well below the international level. These facts indicate the

of immense growth potential of the insurance sector. The year 1999 saw a revolution in the

Indian insurance sector, as major structural changes took place with the ending of

government monopoly and the passage of the Insurance Regulatory and Development

Authority (IRDA) Bill, lifting all entry restrictions for private players and allowing foreign

players to enter the market with some limits on direct foreign ownership. Though, the

existing rule says that a foreign partner can hold 26% equity in an insurance company, a

proposal to increase this limit to 49% is pending with the government. Since opening up of

the insurance sector in 1999, foreign investments of Rs.8.7 billion have poured into the

Indian market and 21 private companies have been granted licenses. Innovative products,

smart marketing, and aggressive distribution have enabled fledgling private insurance

companies to sign up Indian customers faster than anyone expected. Indians, who had always

seen life insurance as a tax saving device, are now suddenly turning to the private sector and

snapping up the new innovative products on offer. The life insurance industry in India grew

by an impressive 36%, with premium income from new business at Rs. 253.43 billion during

the fiscal year 2004-2005, braving stiff competition from private insurers. This report "Indian

Insurance Industry: New Avenues for Growth 2012", finds that the market share of the state

behemoth, LIC, has clocked21.87% growth in business at Rs.197.86 billion by selling 2.4

billion new policies in2004-05. But this was still not enough to arrest the fall in its market

share, as private players grew by 129% to mop up Rs. 55.57 billion in 2004-05 from Rs.

24.29 billion in2003-04 Though the total volume of LIC's business increased in the last fiscal

year (2004-2005) compared to the previous one, its market share came down from 87.04 to

36

78.07%. The 14 private insurers increased their market share from about 13% to about 22%

in a year's time. The figures for the first two months of the fiscal year 2005-06 also speak

of the growing share of the private insurers. The share of LIC for this period has further come

down to 75 percent, while the private players have grabbed over 24 percent. There are

presently 12 general insurance companies with four public sector companies and eight private

insurers. According to estimates, private insurance companies collectively have a 10% share

of the non-life insurance market.

I N T RODUC TION

Financial management means procurement of funds at minimum costs and

effective utilization in order to maximize the wealth of shareholders.

The term of financial management refers to its relationship with the closely-

related fields of economics and accounting, its functions, scope and objectives.

Financial management, as an academic discipline, has undergone fundamental

changes in its scope and coverage. In the early years of its evolution it was treated

synonymously with the raising of funds. In the current literature

pertaining to financial management, a broader scope so as to include, in addition to

procurement of funds, efficient use of resources is universally recognized.

Financial management, as an integral part of overall management, is not a totally,

independent area. It draws heavily on related disciplines and fields of study, such as

economics, accounting, marketing, production and quantitative methods. A part from

economics and accounting, finance also draws for its key day to day decisions on

supportive disciplines such as marketing, production and quantitative methods, for

instance, financial managers should consider the impact of new product

development and promotion plans made in the marketing area since their plans will

require capital outlays and have an impact on the projected cash flows.

Finally, the tools of analysis developed in the quantitative methods area are

helpful in analyzing complex financial management problem. Organization makes

37

their planning for the financial sources which are very helpful in the future course

of action.

Taking a commercial business as the most common organizational structure, the key

objectives of financial management would be to:

Create wealth for the business

Generate cash, and

Provide and adequate return on investment bearing in mind the risks that the busi-

ness is taking and the resources invested.

CONCEPT OF FINACING

1. Financial Planning

Management needs to ensure that enough funding is available at the

right time to meet the needs of the business. In the short term, funding may be

needed to invest in equipment, pay employees and fund sales made on credit.

In the medium and long term, funding may be required for significant

additions to the productive capacity of the business or to make acquisitions.

2. Financial Control

Financial control is a critically important activity to help the business ensure that

the business is meeting its objectives.

3. Financial Decision-Making

A key financing decision is whether profits earned by the business should be retained

38

rather than distributed to shareholders via dividends. If dividends are too high, the

business may be starved of funding to reinvest in growing revenues and profits

further.

FINANCIAL DECISIONS

Financial management consists of four major decisions or functions which are as

discussed as below.

1. Investment decision

Investment decision is the long term, strategic policies of an organization. Investment

decisions have a long term effect on the working of an organization.

Thus an enterprise should invest in proposals which maximize share value.

2. Financing decision

There are various sources of capital like equity, preference shares, borrowed funds, and

retained profits. The finance manager has to select a proper mix of owned at the

minimum cost. A financing decision adds to the value to the value of shareholders.

3. Dividend decision

Profits can either be distributed or reinvested into the business. The

proportion of profits that needs to be distributed and that needs to be retained is a crucial

39

decision. It is the job of finance manager to satisfy the shareholders as well as claw

back into the business. This division of profit when done in an optimum manner

maximizes shareholder value.

4. Liquidity decision

An enterprise needs finance for the day today activities for the smooth

functioning. The brand of FM that deals with investments in current assets &

liabilities, in other words investment is the net working capital comprises of the

liquidity decisions.

DEPRECIATION POLICY IN HDFC LIFE

Depreciation is charged as per the below mentioned rates

Asset Rate as per Companies Act

(Written Down Value method)

– WDV

Rate as per Income Tax

Act (Written Down Value

method) – WDV

Buildings Residential Units 1.63 %

Office Premises 1.63 %

(Straight Line Method –

SLM)

Residential units 5 %

Office Premises 10 %

Computers 25 % (SLM) 60 %

Air Conditioners &

Refrigerator

13.91 % 15 %

Furniture & Fixtures 18.10 % 10 %

Office Equipment 13.91 % 15 %

Electrical Installations 13.91 % 15 %

Vehicles (Motor Cars) 25.89 % 15 %

40

41

Companies Act

1. The rate 13.91 % is applicable to Plant and Machinery (applicable to A/C, Office

Equipment and Electrical Installations).

2. The Depreciation under Companies Act for Computers is 16.21 % (SLM). However,

the rate adopted by us is 25 % SLM.

3. Except Computers, all the rates are as per Companies Act.

4. No depreciation is charged in the year of sale.

5. Depreciation is charged for the full year in the year of purchase.

Income Tax Act

1. Machinery and Plant other than the specified – 15 % (applicable to A/C, Office Equip-

ment and Electrical Installations).

2. Rates of premises, computers, vehicles and furniture specified.

3. If the asset is put to use for 180 days or more in a year, 100 % depreciation is provided

during the financial year. If the period is less than 180 days ---50 % depreciation is

provided for tax purposes.

42

FINACIAL STATEMENT FOR THE YEAR 2009-10

1. Cash flow

Particular 2010 2009

Operating activities

Amount received form policy holder 70,817,804 54,747,190

Amount received to reinsurance -312,168 -384,636

Amount paid to policy holder -12,053,422 -5,414,218

Amount paid as commission -5,417,619 -4,136,736

Payment of employee and suppliers -13,207,483 -15,583,363

Deposited with RBI 0 100,00

Income tax paid -309,142 -230,833

Net cash flow from operating activities 39,821,183 29,453,152

Investing activities 155,217,800 68,782,936

Purchases of fix assets -217,752 -581,822

Sales of fix assets 5,444 3,159

Investment -48,767,468 -39,057,231

Interest income 48,17,558 3,805,029

Dividend income 1,338,737 745,975

Net cash flow from investing activities -42,823,481 -35,081,730

Financing activities

Issue of share 1,720,000 5,250,000

Net cash flow from financing activities 1,720,000 5,250,000

Net increase in cash and cash equivalents -1,282,298 -384,578

Cash and cash equivalent as at beginning of the

year

4,108,660 4,493,238

Cash and cash equivalent as at end of the year 2,826,362 0

43

Particular 2010 2009

Liability

Share capital 19,680,000 17,958,180

Reserve fund 552,892 552,892

Credit change a/c 184,435 -77,610

Credit change a/c 205,087 -296,885

policy liabilities 37,666,908 29,092,419

insurance reserve 0- 0

Provision for link liabilities 127,701,636 84,085,083

Add: Fair value change 27,516,164 -15,302,147

total provision 155,217,800 68,782,936

Funds 1,490,013 586,395

funds for provision 1,064,831 531,970

Surplus 0 0

Profit and loss 6,95,56,324 5,51,83,763

Total 216,061,966 117,130,297

Assets

Share holder 6,304,757 4,291,597

policy holder 43,415,382 30,152,727

Assets held to cover link liabilities 155,217,800 68,782,936

Loans 40,366 30,248

Fix assets 1,143,777 1,451,346

Cash and bank 2,826,362 4,108,660

Advance 4,917,758 5,428,699

Current asset 12,28,585 8,820,225

Provision 187,617 208,813

Net working capital 4,725,082 508,321

Miscellaneous expense 14,664,966 11,913,122

Other Asset 0 0

Total 216,610,966 117,130,297

44

3. RATIO ANALYSIS

(A) CURRENT RATIO

CURRENT ASSETS:

Cash and bank balances: 2,826,362

Advances and Other Assets: 4,917,758

CURRENT LIABILITIES: 12,281,585

CURRENT RATIO= CURRENT ASSETS

CURRENT LIABILITIES

2009-10 =77,44,120

12,281,585

=0.63:1

2008-09=95373598820225

=1.08:1

2. BALANCE SHEET

45

2009-2010 2008-20090

0.2

0.4

0.6

0.8

1

1.2

Current Ratio (%)

Comment

Current ratio of HDFC LIFE insurance, has 0.63:1, it means it is less than 1

that indicates firm’s ability to meet current obligations & greater the safety of funds of

short-term creditors. It also indicates the sound solvency of the company is lover.

46

(B) LIQUID RATIO

LIQUID RATIO: = CURRENT ASSETS−STOCK

CURRENT LIABILITIES−BOD∗100

2009-10=77,44,120−15,21,520

12,281,585∗100

= 0.60:1

2008-09=9537359−45,44,600

8820225

= 0.57:1

2009-2010 2008-20090.55

0.555

0.56

0.565

0.57

0.575

0.58

0.585

0.59

0.595

0.6

Column2

Comment

The liquid ratio of HDFC life in 2009 was 0.57 and in 2010 is .60 so increasing the

liquid ratio and company have a good liquid position over the year.

47

(C)Gross profit ratio

GROSS PROFIT RATIO = GROSS PROFIT

NETSALES∗100

2009-10 =70,051,044

31,48,95,290∗100

= 30.25 %

2008-09=55,646,93 0

25,56,98,360∗100

= 21.76%

2009-2010 2009-20100

5

10

15

20

25

30

35

Gross Profit Ratio(%)

Comment:-

The gross profit ratio of HDFC LIFE in 2009 was 21.76% and in 2010 is 30.25% so

increasing the gross profit of HDFE LIFE over the year and company become a strong

in his financial performance.

48

(D) NET PROFIT RATIO

NET PROFIT RATIO=NET PROFIT

NETSALES∗100

2009-10=6,95,56,32431,48,95,290

∗100

= 22.09%

2008-09 =5,51,83,763

25,56,98,360∗100

= 21.58%

2009-2010 2008-200921.3

21.4

21.5

21.6

21.7

21.8

21.9

22

22.1

Net Profit Ratio(%)

Comment:-

The net profit ratio of HDFC LIFE in 2009 was 21.58% and in 2010 is 22.09%

therefore the net profit is increasing. The company have good profit margin. The

company should more and more profit for the future.

49

(E)Net retention ratio

NET RETENTION RATIO=NET PREMIUM

GROSSPREMIUM∗100

2009-10 =6,95,56,32470,051,044

∗100

= 99.29 %

2008-09=55,183,76355,646,93 0

∗100

=99.17%

2009-2010 2008-200999.1

99.12

99.14

99.16

99.18

99.2

99.22

99.24

99.26

99.28

99.3

Net retention ratio(%)

Comment:-

The net retention ratio of HDFC LIFE in 2009 was 99.17% and in 2010 is

99.29% therefore increasing the net retention ratio of the HDFE LIFE. So company

become successful for maintain the premium level over the year.

50

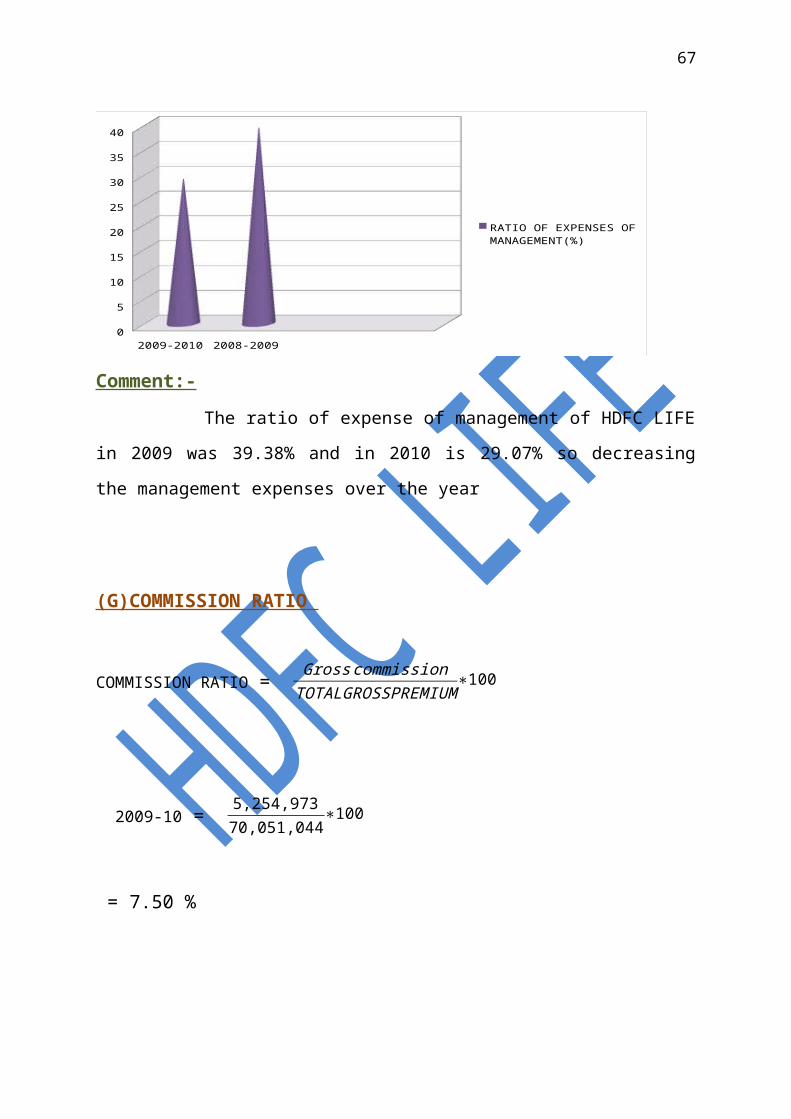

(F)RATIO OF EXPENSES OF MANAGEMENT

RATIO OF EXPENSES OF MANAGEMENT

= MANAGEMENT EXPENSES

TOTALGROSSPREMIUM∗100

2009-10 =20,345,37670,051,044

∗100

= 29.04 %

2008-09 =21,915,90755,646,937

∗100

=39.38%

2009-2010 2008-20090

5

10

15

20

25

30

35

40

RATIO OF EXPENSES OF MANAGEMENT(%)

Comment:-

51

The ratio of expense of management of HDFC LIFE in 2009 was 39.38% and in

2010 is 29.07% so decreasing the management expenses over the year

(G)COMMISSION RATIO

COMMISSION RATIO = Gross commission

TOTALGROSSPREMIUM∗100

2009-10 = 5,254,973

70,051,044∗100

= 7.50 %

2008-09 =4,248,904

55,646,937∗100

=7.64%

2009-2010 2008-20097.4

7.45

7.5

7.55

7.6

7.65

COMMISSION RATIO(%)

52

(H)RATIO OF POLICY HOLDERS’ LIABILITIES TO

SHAREHOLDERS’ FUNDS:

RATIO OF POLICY HOLDERS’ LIABILITIES TO SHAREHOLDERS’ FUNDS :

=POLICY HOLDERS ’ LIABILITIES

SHAREHOLDERS ’ FUNDS :∗100

2009-10 =376669086304757

∗100

= 597.44 %

2008-09=290992419

4291597∗100

= 677.89%

53

2009-2010 2008-2009540

560

580

600

620

640

660

680

RATIO OF POLICY HOLDERS’ LIABILITIES TO SHAREHOLD-ERS’ FUNDS: (%)

(I)RETURN ON INVESTMENT

RETURN ON

INVESTMENT =EBIT

CAPITAL+SURPLUS+RESERVE∗100

2009-10 =5,029,631

19,680,000+552,892∗100

= 24.86%

2008-09 =2751844

19,680,000+552,892∗100

=13.60%

54

2009-2010 2008-20090

5

10

15

20

25

RETURN ON INVESTMENT(%)

Comment:-

The return on investment ratio of HDFC LIFE in 2009 was 13.60% and

in 2010 is 24.86% there increasing the return on investment over the year so company

become a profitable over the year.

(J) DEBT-EQUITY RATIO

DEBT-EQUITY RATIO = LONG−TERMDEBT

SHAREHOLDER ’ SFUND * 100

2009-10 =790592313500494238

∗100

=1.58%

2008-09¿579047751461137821

∗100

=1.25%

55

2009-2010 2008-20090

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

DEBT-EQUITY RATIO(%)

Comment:

The debt-equity ratio of HDFC LIFE in 2009 was 1.25% and in 2010 is 1.58% there

increasing the level of equity against long term debt.

TREND ANALYSES

Asset 2009-2010 2010-2011 2009-2010(%) 2010-

2011(%)

Share holder 6,304,757 4,291,597 100% 68%

policy holder 43,415,382 30,152,727 100% 69%

Assets held to cover

link liabilities

155,217,800 68,782,936 100% 44%

Loans 40,366 30,248 100% 73%

Fix assets 1,143,777 1,451,346 100% 126%

Cash and bank 2,826,362 4,108,660 100% 145%

Advance 4,917,758 5,428,699 100% 110%

Current Asset 12,28,585 8,820,225 100% 717%

56

Provision 187,617 208,813 100% 111%

Net working capital 4,725,082 508,321 100% 10%

Miscellaneous expense 14,664,966 11,913,122 100% 81%

Other Asset 0 0 100%

Total 2,16,610,966 117,130,297 100% 5%

Asset

Liability

Liability 2009-2010 2010-2011 2009-

2010(%)

2010-

2011(%)

Share capital 19,680,000 17,958,180 100% 91%

Reserve fund 552,892 552,892 100% 100%

Credit change a/c 184,435 -77,610 100% 142%

Credit change a/c 205,087 -296,885 100% 42%

policy liabilities 37,666,908 29,092,419 100% 77%

insurance reserve 0- 0 100% 100%

Provision for link

liabilities

127,701,636 84,085,083 100% 0

Add: Fair value change 27,516,164 -15,302,147 100%

57

total provision 155,217,800 68,782,936 100% 44%

Funds 1,490,013 586,395 100% 39%

funds for provision 1,064,831 531,970 100% 49%

Surplus 0 0 100% 100%

Profit and loss 6,95,56,324 5,51,83,763 100% 79%

Conclusion:-

According to trend analysis the hdfc life doing improvement in 2010-2011

compare to 2009-2010 so company is growing in following way

1). The liquid position of the company improving around 145 %

2).The increase in fixed asset is financed by issue of debenture

3).Higher improvement in current asset the compare the two year 717% are

improvement in 2010-2011

COMMON SIZE STATEMENTS

Asset 2010 2010 (%)

Share holder 4,291,597 3.66

policy holder 30,152,727 25.74

Assets held to cover

link liabilities

68,782,936 58.72

Loans 30,248 0.025

Fix assets 1,451,346 1.24

Cash and bank 4,108,660 3.5

Advance 5,428,699 4.63

Current Asset 8,820,225 7.53

58

Provision 208,813 0.18

Net working capital 508,321 4.34

Miscellaneous expense 11,913,122 10.17

Total 117130297 100

TREND ANALYSES

Share Capital

share capital

PARTICULAR 2009-10 2008-09 incre/decre %

Authorised Capital 30,000,000 30,000,000 0 0

Issued Capital 19,680,000 17,960,000 17,20,000 9.57

Subscribed Capital 19,680,000 17,960,000 17,20,000 9.57

Called-up Capital 19,680,000 17,960,000 17,20,000 9.57

59

0

17,2

0,00

0

17,2

0,00

0

17,2

0,00

0

30,000,000 17,960,000 17,960,000 17,960,00030,000,000 19,680,000 19,680,000 19,680,000Authorised

CapitalIssued Cap-

ital Subscribed

CapitalCalled-up

Capital

0

5

10

share capital %

share capital %

CONCLUSION:

in the year 2008-09 the Authorized share capital was 30,000,000 and at current year

the Authorized share capital are same there are no changes arise in Authorized share

capital between two year and Called-up Capital, Subscribed Capital , Issued Capital

were 17,960,000 and in current year increase by 17,20,000 so as compare to the

previous year increase by 9.57 %

RESERVES AND SURPLUS

PARTICULAR 2009-10 2008-09 incre/decre %

Revaluation Reserve 552,892 552,892 0 0

60

2009-10 2008-09 incre/decre %0%

10%20%30%40%50%60%70%80%90%

100%

Revaluation Reserve

Revaluation Reserve

CONCLUSION:

in the year 2008-09 the Revaluation Reserve are 5,52,892 and at current year

are same there are no changes arise in the current year,

Investments – Shareholders

PARTICULAR 2009-10 2008-09 incre/decre %

Government Securities 2,471,702 2,180,149 291,553 13.373077

Equity 457,377 233,783 223,594 95.641685

Debentures / Bonds 208,675 100,531 108,144 107.57279

Investment Properties 757,540 757,540 0 0

Infrastructure 1,108,284 386,899 721,385 186.45305

61

Other Investments 145,085 64,797 80,288 123.90697

CONCLUSION

in the year 2008-09 the investment in Government Securities was 2180149

and at current year are having 2471702 so increase by 291,553 and so 13.37 % are

increase as compare to previous. And Equity, Debentures / Bonds, Investment

Properties, Infrastructure, Other Investments, are increase by respectively 95.64%,

107%,0%, 186% 123%.

Working Capital

current assets 2009-10 2008-09 incre/decre %

Cash 279,148 668,726 -389,578 -58.25674

Deposit Accounts 1,340,581 1,751,354 -410,773 -23.4546

Current Accounts 1,206,633 1,653,161 -446,528 -27.01056

current liabilities 2009-10 2008-09 incre/decre %

Agents’ Balances 422,567 525,903 -103,336 -19.64925

Govern

ment S

ecuriti

es

Equity

Deben

tures / B

onds

Investm

ent P

roperti

es

Infrastr

ucture

Other Inve

stmen

ts0

1,000,0002,000,0003,000,0004,000,0005,000,000

%incre/decre2008-092009-10

62

Premiums received in ad-

vance

296,400 278,748 17,652 6.3326015

Security Deposits 21,441 21,441 0 0

Sundry creditors 5,078,198 3,894,536 1,183,662 30.392889

Claims Outstanding 433,935 198,361 235,574 118.76024

Unallocated Premium 232,117 274,095 -41,978 -15.31513

CONCLUSION:

As compared to previous year, Current Accounts are decrease by as compare to

the previous year respectively,-58%, -19%, 6.33%,0%, 30.39%, in the year 2008-09

the current asset of cash, Deposit Accounts -23%, -27%,. And current liabilities of

Agents’ Balances, Premiums received in advance, Security Deposits, Sundry creditors

are decrease or increase

Comparison of funds for year 2010:

Fund 2009 2010

Growth fund 38 73

Balance manage

fund 32 48

Equity manage 34 62

Agents’

Balances

Premiums r

eceive

d in ad

vance

Secu

rity D

eposit

s

Sundry

credito

rs

Claims O

utstan

ding

Unallocat

ed Prem

ium0%

30%60%90%

% -58.25674491 -23.4545957 -27.01055735 %incre/decre -389,578 -410,773 -446,528 incre/decre2008-09 668,726 1,751,354 1,653,161 2008-092009-10 279,148 1,340,581 1,206,633 2009-10

63

fund

Liquid manage

fund 28 31

Growth fund Balance manage fund

Equity manage

fund

Liquid manage

fund

01020304050607080

20092010

In above diagram comparison of fund’s performance for year 2010.

The above diagram represents the comparison of various funds. The growth

fund in 2009 was 38% and at present in 2010 are 73% so increased by 35%. And

second fund is balance manage fund there was 32%in 2009 and at present jn 2010 is

48% so increase by 16%. And third fund is equity manage fund there was in 2009 was

34% and at present in 2010 are 62% so increase by 28%. And forth fund are liquid

fund there was in 2009 was 28% and present in 2010 are 31% so increase by 4%.

Equity markets

INDICES 31-5-12 30-4-2012 1month rate

of return

1year rate of

return

BSE Sensex 16,219 17,319 -6.35 -12.35

S&P CNX 4,924 5,248 -6.17 -11.44

64

Nifty

BSE 100 4,942 5,268 -6.19 -12.34

BSE Mid

Cap

5,908 6,316 -6.46 -14.50

BSE Small

Cap

6,271 6,765 7.30 -23.86

65

6.Processes

The process should be customer friendly in insurance industry. The speed and accuracy of

payment is of great importance. The processing method should be easy and convenient to the

customers. Installment schemes should be streamlined to cater to the ever growing demands

of the customers. IT & Data Warehousing will smoothen the process flow. IT will help in ser-

vicing large no. of customers efficiently and bring down overheads. Technology can either

complement or supplement the channels of distribution cost effectively. It can also help to

improve customer service levels. The use of data warehousing management and mining will

help to find out the profitability and potential of various customers product segments.

What is Welcome Calling to the customer?

Welcome Calling is a call made to all our new customers to ensure that the policy chosen by

them is as per requirement.

What is the objective of Welcome Calling?

Welcome Calling serves mainly 2 objectives:

First, to contact the customer as per the given contact details thereby ensuring contact ability.

Second, to verify if the customer has fully understood the important features the insurance

plan chosen and whether it suits the customer's requirement, thereby avoiding mis-sale occur-

rences.

66

The process of customer Welcome Calling of customer

A welcome call is made to the customer after the application for insurance policy has been

accepted by the company.

Before disclosing any policy related information, our Customer Service Associate (CSA) will

do a mandatory verification by asking few questions.

If the policy holder is not available, information can be shared with a third party who takes

care of the policy holder's finances, post confirmation from the third party that all the dis-

cussed details will be shared with the Policy Holder.

Once the verification is done, the CSA will inform the customer on all the Key features of the

insurance plan.

Once all the key features have been communicated, the CSA can also make a note of any

query, request or complaint by the customer.

If the customer is not contactable despite multiple attempts, we will send a Welcome Calling

Letter to the communication address of the customer.

Physical Distributions

Distribution is a key determinant of success for all insurance companies. Today, the

nationalized insurers have a large reach and presence in India. Building a distribution

network is very expensive and time consuming. Technology will not replace a distribution

network though it will offer advantages like better customer service. Finance companies and

banks can emerge as an attractive distribution channel for insurance in India. In Netherlands,

financial services firms provide an entire range of products including bank accounts, motor,

home and life insurance and pensions. In France, half of the life insurance sales are made

through banks. In India also, banks hope to maximize expensive existing networks by selling

a range of products.

The physical evidences include signage, reports, punch lines, other tangibles, employee‘s

dress code etc.

67

A. Tangibles: banks give pens, writing pads to the internal customers. Even the

passbooks,chequebooks, etc reduce the inherent intangibility of services.

B. Punch lines: punch lines or the corporate statement depict the philosophy and attitude

ofthe bank. Banks have influential punch lines to attract the customers.

SOME CHANNEL OF DISTRIBUTIONS IN HDFC LIFE

1. Direct SalesDirect Sales ManagerIndividual Sales( Door to Door Marketing )

2. Sales Development Manager’s Induction

Business through Financial Consultants

3. Alternative Induction

Bank Relation( HDFC,SBI,BOB,Andra Bank,AXIS Bank etc...)

4. Corporate Induction

Group SellingCollabration with other Companies

68

conclusion

69

CONCLUSION

Introduction

1. It has got 3rd rank in the investment management, in year 2006One of the largest financial in-

stitution of

2. India with more then 2 million satisfied customer base.

3. The most successful and admired life insurance Company, which means that we are the most

trusted Company, the easiest to deal with, offer the best value for money, and set the stand-

ards in the industry. In short, “The most obvious choice for all

Financial analysis is important aspect of financial management. The study of

financial managementat HDFC LIFE LTD. has revealed that the current ratio

was as per the standard industrial practice but the liquidity position of the

company showed an increasing trend.

70

Finance department

1. The proprietary ratios shows efficient capital structure. Considering the turnover ratios, the management having effective collection system and low investment in stocks.

2. The Depreciation under Companies Act for Computers is 16.21 % (SLM). However, the rate

adopted by us is 25 % SLM.

3. Machinery and Plant other than the specified – 15 % (applicable to A/C, Office Equipment

and Electrical Installations).

4. Current ratio of HDFC LIFE insurance, has 0.63:1 It also indicates the sound solvency of the

company is higher.

5. The net profit ratio in 2009 was 21.58% and in 2010 is 22.09% therefore the net profit is in-

creasing. The company have good profit margin. The company should more and more profit

for the future.

6. Issued Capital were 17,960,000 and in current year increase by 17,20,000 so as compare to

the previous year increase by 9.57 %

71

RECOMMENDATION AND SUGGSTION

72

RECOMMENDATIONS

The HDFC company should now try to identify the gap between current level of customer

service and customer expectations. Some of the strategies being recommended are as

follows:

Brand Building:

HDFC is a very huge Brand in US in Insurance but in India it is not known as a Insurance

brand. So HDFC need to focus on Brand building Activities which can be done through Ad-

vertising, Road shows, Knops, Sponsoring Events in rural & Urban Areas.

Educating the Consumers:

HDFC should take initiative to educate the consumers regarding all these aspects & take

competitive Advantage on this front as its Allocation charges are minimum in the whole In-

dian Insurance Industry.

Need to Increase Market Presence:

It should make more channel partners & do business tie ups with more broking houses &

should hire marketing agencies for aggressive marketing purpose. It can also increase its

Business Units.

Concentration More On Rural Areas :

HDFC need to concentrate more towards the rural areas as 60-70% of India population is

living in rural areas and most of the people in rural areas are not insured so there is a huge

potential in the rural sector.

Product Differentiation:

Offering a product that is distinctly different from other products available in the market by

other insurance players.

More Guaranteed Plans to be Introduced:

73

As we know today the stock market is giving very less return even in last year the return

comes Negative so the company need to introduce some more granted plans so that customer

can invest in them and have assured return on them which ultimately is an edge in competi-

tion in insurance sector.

Need to commence Medical claim Products and General Insurance :

There are very less which are having Medical claim products and also very less companies

providing General Insurance with Life Insurance for example ICICI , Reliance and Bajaj

Allianz so HDFC also need to come in General Insurance business so that they can compete

with these players.

Flexibility:

The companies should make their products flexible for the convenience of their customer.

Hassle Free Service:

All bureaucracy in customer interactions should be eliminated.

Proper Policy Documentation:

Wrong interpretations/ non-awareness of policy document by the customer may have serious

implications in the long term and the possibility of the same should be alleviated by the

company which leads to.

74

Recommendation can be use by the firm for the betterment increased of the firm

after study and analysis of project report on study and analysis of working

capital. I would like to recommend.

1. Company should raise funds through short term sources for short term

requirement of funds, which comparatively economical as compare to long term

funds.

2. Company should take control on debtor’s collection period which is major

part of current assets.

3. Company has to take control on cash balance because cash is non earning

assets and increasing cost of funds.

4. Company should reduce the inventory holding period with use of zero

inventory concepts.

Over all company has good liquidity position and sufficient funds to repayment

of liabilities. Company has accepted conservative financial policy and thus

maintaining more current assets balance. Company is increasing sales volume

per year which supported to company for sustain 2nd position in the world and

number one position in Asia.

75

SUGGESTIONS:

The company should try to increase his financial performance in the future.

The company should try to increased his product cycle.

Stable Managed fund & Secure Managed Fund provide low return. but less risk in Stable

Managed fund & Secure Managed Fund.

Most of the people are not aware about HDFC STANDARD LIFE INSURANCE CO.LTD so they have to

advertise their company and their product.

HDFC LIFE INSURANCE CO.LTD focuses on the urban area so now they have to focus on rural area

also.

HDFC LIFE INSURANCE CO.LTD should try to increase awareness of their UNIT LINK PLAN

The company should increase their distribution network.

76

ANNEXURE

77

QUESTIONNAIRE

PERSONAL DETAILS:

Name:

Mobile Number:

Adress:_______________________________________________________

_____________________________________________________________

_____________________________________________________________

_____________________________________________________________

_______________________________

Occupation: _____________________

Age: ____________________________

1. Of the following what at present are your investment needs?

a. To build a corpus for retirement

b. To save for children education/ marriage

c. To provide for medical emergencies

d. To provide for family financial security

e. To create wealth

f. All of the above

78

2. Which of the following you think as investment for tax- saving?

a. Mutual funds

b. Fixed deposit

c. Insurance

d. Ppf

e. All of the above

3. Have you ever been invested in mutual funds?

a. Yes b. No

4. Have you ever been invested in ulip insurance plans?

a. Yes b. No

5. If you had Rs 1000/- where you prefer to invest

a. Mutual fund

b. Fixed deposit

79

c. Direct equity

d. Life insurance

e. Postal office deposit

6. Out of the following in which Mutual Fund you have invested?

a) HDFC

b) Tata Mutual Fund .

c) Franklin Templeton .

d) Reliance .

e) ICICI Prudential .

f) SBI .

g) Other If any ,Please Specify

7. Out of the following company which company ulip plans you have invested?

a) HDFC LIFE.

b) Tata AIG .

c) BAJAJ ALLIANZE .

d) Reliance .

e) ICICI Prudential .

f) SBI LIFE.

g) Other If any ,Please Specify

8. To how much extent are you satisfied with the services offered by HDFC

LIFE regardingULIP INVESTMENT PLANS?

a) Exteremly satisfied.

b) Satisfied to the lesser extent

d) Dissatisfied to lesser extent

80

e) Extremely dissatisfied.

9. Do you prefer GROWTH FUND OR DIVERSIFY YOUR MONEY in

various fund?

a) growth fund

b) diversify funds

c) Depends upon the risk bearing condition

81

BIBLOGRAPHY

Books Referred

1. Maheshwari, S.N.; Financial Managemen, Principles and Practice, Sultan

Chand & sons, 9th Edition 2004.

2. Maheshwari, S.N.; Elements of Financial Management, Sultan Chand & Sons,

2003 7th Edition.

3. Pandey, I.M.; Financial Management, Vikas Publishing House, 8th Edition,

2001.

4. .Author:Evertt.E.AdamProduction and opration management prentice hall 5th

edition

Websites References

www. hdfclife .com/

www.bimadeals.com › Life Insurance › Life Insurance Companies

www.myinsuranceclub.com › Life Insurance › Companies

www.indiancustomers.in/ company / hdfc -standard- life

www. hdfclife .com/ Children'sPlans / child - insurance - plans .

www. hdfclife .com/savings plans /Whole Life