financial statements under ind as - … · financial statements under ind as: ... (towards...

TRANSCRIPT

FINANCIAL STATEMENTS UNDER IND AS:

OVER ALL CONSIDERATIONSOctober 2016

Titre de la présentation1

CONSTITUENTS OF ‘FINANCIAL STATEMENTS’

• Balance sheet

• Statement of profit and loss (title not entirely representative of contents)

• Statement of changes in equity (new)

• Cash flow statement

• Notes

FORM AND CONTENT OF FINANCIAL STATEMENTS

• Prescribed by newly-inserted Division II of Schedule III to the Companies Act 2013 in respect of

- Balance sheet- Statement of profit and loss- Statement of changes in equity

• No format prescribed for cash flow statement

- To be prepared in accordance with Ind AS 7, Cash Flow Statements- No illustrative format in Ind AS 7 (unlike AS 3)

FORMAT OF BALANCE SHEET

• Vertical form- First, ‘Assets’- Then, ‘Equity and Liabilities’

• Current – Non-current classification of assets and liabilities- Definitions of current and non-current assets and liabilities essentially the

same as in pre-revised Schedule III

• A larger number of items of assets and liabilities required to be presented on the face of balance sheet, e.g. disclosure also required of- Goodwill- Investment Property- Break-up of financial assets such as investments, trade receivables, loans,

etc.

• ‘Equity’ to be classified on the face of balance sheet into- Equity share capital- Other equity

EQUITY OR LIABILITY? (IND AS 32)

• Depends on nature of contractual obligations and rights of issuer rather than legal form of instrument : A preference share could warrant classification as a liability Conversely, a debenture could warrant classification as equity

• A single instrument may contain both a liability and an equity component (‘compound financial instrument’)

• Broadly speaking, the primary determinant is whether contractually, the issuer is or may be obliged to make payment in cash or other financial asset (towards principal, interest or dividend) to the holder If yes, a liability Else, equity

• If a convertible debenture (or other convertible instrument) is convertible into a variable number of equity instruments of issuer, it is a financial liability rather than equity

Company K issues preference shares to an investor. As per the terms of issue, the preference shares shall be mandatorily redeemed at the expiry of five years from the date of their issue. The shares carry a cumulative dividend of 8% per annum and the terms of issue specifically stipulate that any unpaid dividend shall be paid at the time of redemption, subject to availability of profits.

EQUITY OR LIABILITY? (IND AS 32)

Company D issues preference shares to a group of investors. As per the terms of issue, each preference share shall be mandatorily converted into 5 equity shares at the expiry of four years from the date of issue. The preference shares carry a non-cumulative dividend of 8% per annum. In the jurisdiction in which Company D operates, declaration and payment of dividend on preference shares is at the discretion of the issuer.

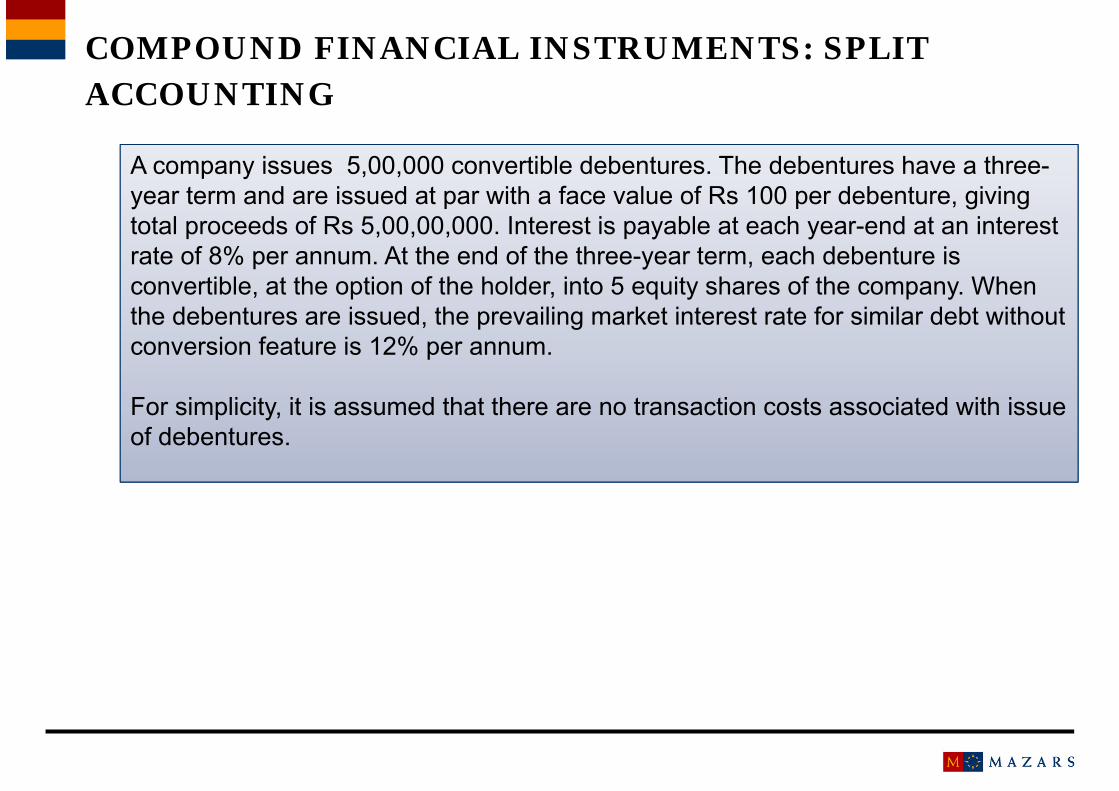

A company issues 5,00,000 convertible debentures. The debentures have a three-year term and are issued at par with a face value of Rs 100 per debenture, giving total proceeds of Rs 5,00,00,000. Interest is payable at each year-end at an interest rate of 8% per annum. At the end of the three-year term, each debenture is convertible, at the option of the holder, into 5 equity shares of the company. When the debentures are issued, the prevailing market interest rate for similar debt without conversion feature is 12% per annum.

For simplicity, it is assumed that there are no transaction costs associated with issue of debentures.

COMPOUND FINANCIAL INSTRUMENTS: SPLIT ACCOUNTING

Maximum potential cash outflows associated with debentures (Rs)

At the end of Year 1 (interest) 40,00,000At the end of Year 2 (interest) 40,00,000 At the end of Year 3 (interest) 40,00,000 At the end of Year 3 (principal) 5,00,00,000

Liability componentPresent value of above cash outflows at 12%= 4,51,96,340

Equity component (balance)5,00,00,000 minus 4,51,96,340 = 48,03,660

COMPOUND FINANCIAL INSTRUMENTS: SPLIT ACCOUNTING (contd.)

Interest would be accrued on the liability component at 12% p.a. as follows:

COMPOUND FINANCIAL INSTRUMENTS: SPLIT ACCOUNTING (contd.)

Opening bal. of liability Interest @ 12% Interest paid

Year 1 4,51,96,340 54,23,560 40,00,000

Year 2 4,66,19,900 55,94,390 40,00,000

Year 3 4,82,14,290 57,85,710 40,00,000

EQUITY OR LIABILITY?

• Treatment of interest, dividends, losses and gains relating to a financial instrument

- Depends on whether it is classified as equity or as liability

E.g., dividend on preference shares classified as liability will be a charge in determining profit or loss

• Change in classification from equity to liability (or liability to equity) due to adoption of Ind ASs may have a significant impact on debt-equity ratio and reported profits of many companies

TREATMENT OF TRANSACTION COSTS

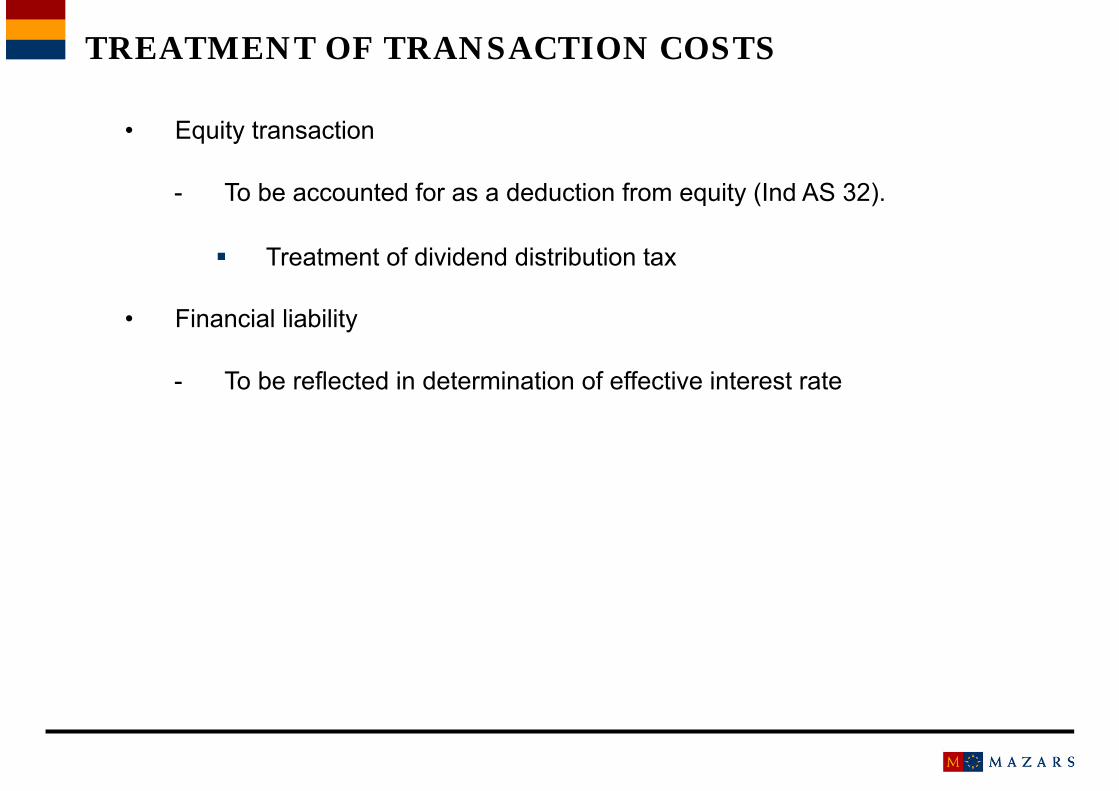

• Equity transaction

- To be accounted for as a deduction from equity (Ind AS 32).

Treatment of dividend distribution tax

• Financial liability

- To be reflected in determination of effective interest rate

STATEMENT OF PROFIT AND LOSS

• In effect, has two sections (though not so titled in the format):

- ‘Profit or loss’ section, ending with ‘profit/(loss) for the period’- ‘Other comprehensive income’ (OCI) section- ‘Total comprehensive income for the period’ also required to be presented

• Internationally, title used is ‘statement of profit or loss and other comprehensive income’

• EPS calculations are with reference to profit or loss for the period and not with reference to total comprehensive income for the period

CONCEPT OF ‘COMPREHENSIVE INCOME’

Comprehensive income –

Increase or decrease in net worth (or equity or net assets) during a period otherwise than on account of transactions with shareholders in their capacity as owners, e.g., fresh capital infusion, distribution of dividends

CONCEPT OF ‘COMPREHENSIVE INCOME’

At the end of Year 1, Company X is incorporated with a share capital of 1,000. There is no other activity during Year 1. The company’s balance sheet at the end of Year 2 shows the following position (no dividend has been paid during the year):

PPE (land) at fair value (cost 40) 50PPE (other items) at cost less depreciation 70Investments in listed shares at fair value (cost 300) 360Current assets (debtors, inventories) 550Cash and cash equivalents 150Year-end total assets 1,180

Borrowings 60

Year-end net worth 1,120

Comprehensive income for the period - 120

OTHER COMPREHENSIVE INCOME

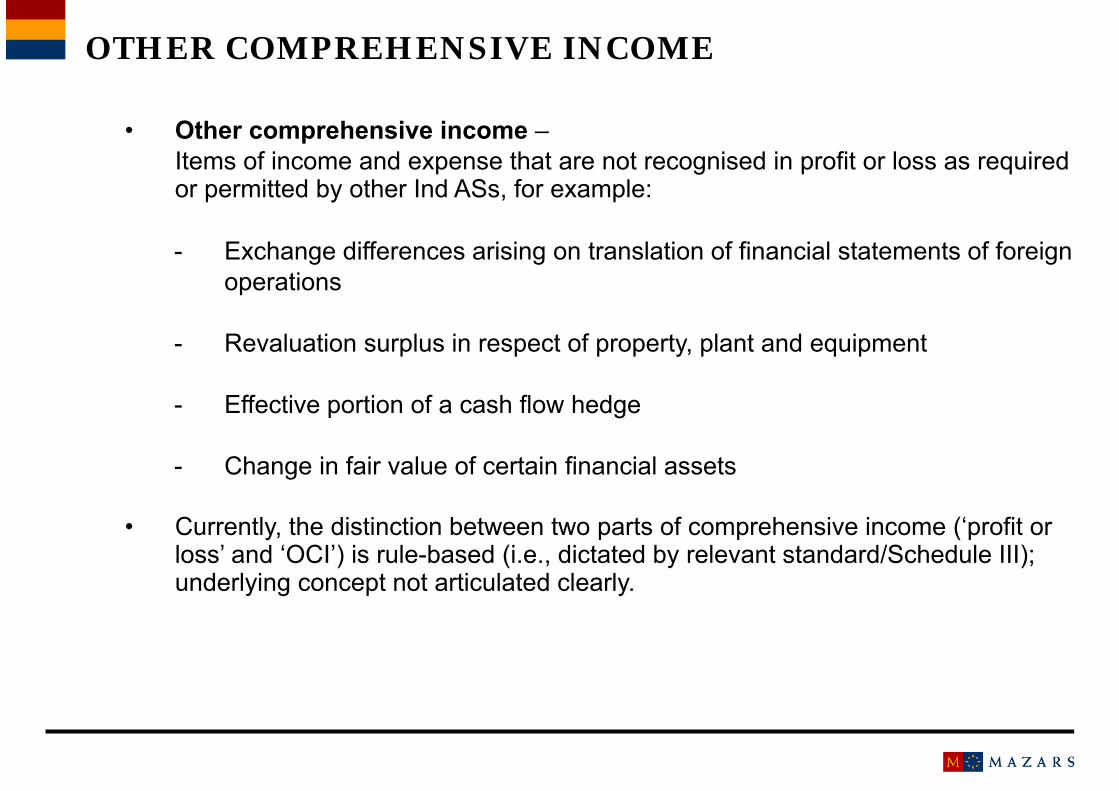

• Other comprehensive income –Items of income and expense that are not recognised in profit or loss as required or permitted by other Ind ASs, for example:

- Exchange differences arising on translation of financial statements of foreign operations

- Revaluation surplus in respect of property, plant and equipment

- Effective portion of a cash flow hedge

- Change in fair value of certain financial assets

• Currently, the distinction between two parts of comprehensive income (‘profit or loss’ and ‘OCI’) is rule-based (i.e., dictated by relevant standard/Schedule III); underlying concept not articulated clearly.

OTHER COMPREHENSIVE INCOME (contd.)

• Ind AS/Schedule III

- Require some items of OCI to be subsequently recycled to profit or loss, e.g. exchange differences arising on translation of financial statements of a foreign operation

- Prohibit recycling of other items to profit or loss, e.g., surplus arising on revaluation of property, plant and equipment

• What is to be recycled to profit or loss is dictated by relevant standard/Schedule III; underlying concept not articulated clearly.

‘PROFIT OR LOSS’ SECTION

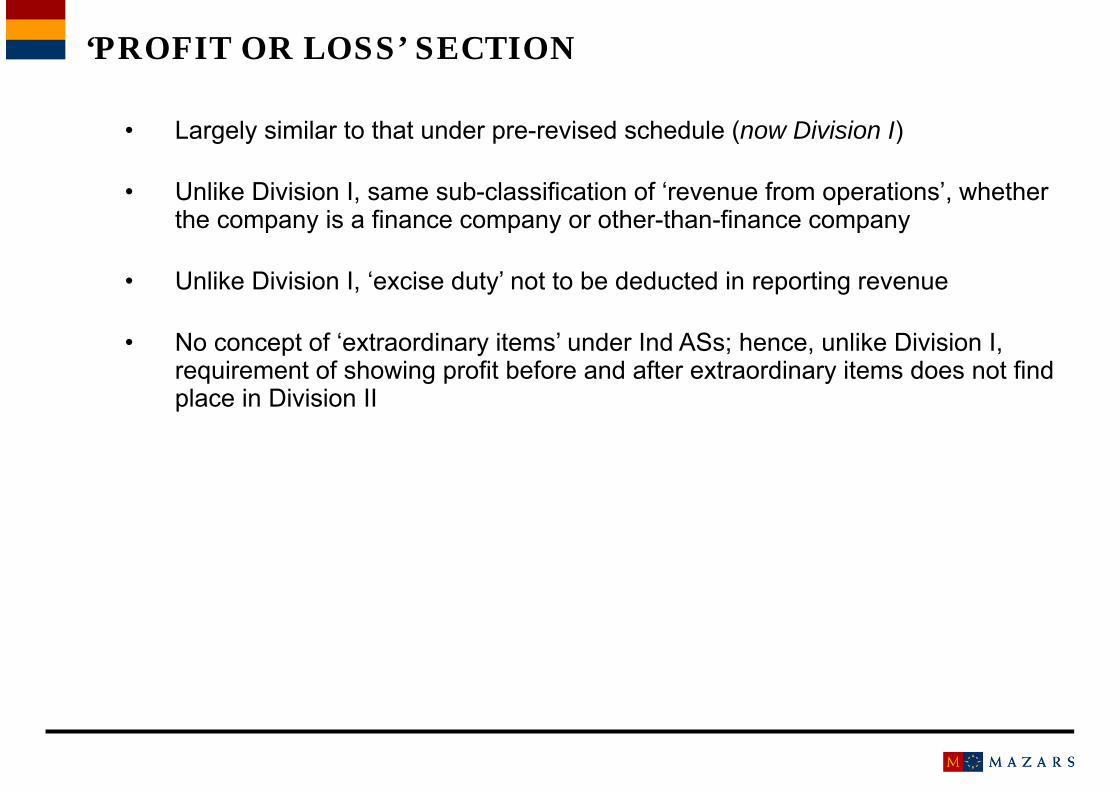

• Largely similar to that under pre-revised schedule (now Division I)

• Unlike Division I, same sub-classification of ‘revenue from operations’, whether the company is a finance company or other-than-finance company

• Unlike Division I, ‘excise duty’ not to be deducted in reporting revenue

• No concept of ‘extraordinary items’ under Ind ASs; hence, unlike Division I, requirement of showing profit before and after extraordinary items does not find place in Division II

STATEMENT OF CHANGES IN EQUITY

• Provides a reconciliation between opening and closing balance of equity share capital and each item of other equity by showing movements during the year

• Examples of items of ‘other equity’ listed in Division II

- Share application money pending allotment

- Equity component of compound financial instruments

- Money received against share warrants

- Each item of ‘Reserves and surplus’ e.g. Capital Reserve, Securities Premium Reserve, Retained Earnings, etc.

- Each item of ‘other comprehensive income’ e.g., Effective portion of cash flow hedges Revaluation surplus Exchange differences on translation of financial statements of foreign

operations

NOTES

• Details of various items of assets, liabilities, income, expenses and items of equity to be given in notes – largely similar to those in Division I

• Additional information relating to value of imports, value of imported/indigenous raw materials etc consumed, expenditure in foreign currency, dividend remittances in foreign exchange, earnings in foreign exchange

- Not required to be presented

CHANGES IN ACCOUNTING POLICIES (IND AS 8)

• An accounting policy shall be changed only if the change:

- is required by an Ind AS; or

- results in the financial statements providing reliable and more relevant information (‘voluntary change’)

• For a voluntary change, disclosure also required of the reasons why applying the new accounting policy provides reliable and more relevant information.

EFFECTING CHANGES IN ACCOUNTING POLICIES

• Unless impracticable

- A change in accounting policy resulting from the initial application of an Ind AS to be accounted for in accordance with its transitional provisions, if any.

- In other cases (i.e. when the Ind AS does not include transitional provisions or when an accounting policy is changed voluntarily), the change to be applied retrospectively, i.e. as if the changed policy had always been applied.

Impracticable -- the entity cannot apply a requirement after making every reasonable effort to do so

RETROSPECTIVE CHANGE IN ACCOUNTING POLICY

• Involves

- adjustment of opening balance of each affected component of equity for the previous period presented,

- restatement of comparative amounts for previous period presented

as if the new policy had always been applied

• Requires distinguishing information that

- provides evidence of circumstances that existed on the date(s) as at which the transaction/event/condition occurred, and

- would have been available when the financial statements for that prior period were authorized for issue from other information.

• Hindsight not to be used when applying new policy

IMPRACTICABILITY OF RETROSPECTIVE APPLICATION

• Retrospective application to a prior period is impracticable if it is not practicable to determine cumulative effect on the amounts in both opening and closing balance sheets for that period.

• Reasons for impracticability of retrospective application–

- non-availability of data to apply new policy and impracticability to recreate it;

- retrospective application requires assumption about management’s intent in the prior period

- retrospective application requires significant estimates of amounts and it is impossible to distinguish information that was available at the time of approval of prior period’s financial statements from other information

• Where full retrospective application not practicable, apply new policy from the earliest date practicable (which may even be the beginning of the current year.)

CORRECTION OF PRIOR PERIOD ERRORS

• Material prior period errors to be corrected retrospectively, unless impracticable.

• Correction involves

- restating comparative amounts for the previous period presented;

- for errors that occurred before the previous period presented, opening balances of assets, liabilities and equity for the previous period presented to be restated

• ‘Impracticable’ has the same connotation as in the case of retrospective application of a new accounting policy

CHANGES IN ACCOUNTING POLICIES/ERROR CORRECTION/RECLASSIFICATIONS

• A balance sheet at the beginning of the preceding period to be presented in following cases (thus, three sets of balance sheet figures to be presented) in following situations if such balance sheet is materially affected:

- Retrospective application of accounting policy

- Retrospective correction of errors

- Reclassification of items in financial statements

POST-BALANCE SHEET DATE EVENTS

• Unlike AS 4, Ind AS 8 requires disclosures in financial statements about events after the end of reporting period that are indicative of conditions that arose after the reporting period (‘non-adjusting events after the reporting period’).

• Following disclosures to be made for each material category of such events:

- the nature of the event; and

- an estimate of its financial effect, or a statement that such an estimate cannot be made.

• If dividends to holders of equity instruments are declared after the reporting period, those dividends not to be recognised as a liability at the end of the reporting period.

CONCEPT OF ‘FAIR VALUE’ UNDER IND AS

DateTitre de la présentation

FAIR VALUE

• Many Ind ASs require valuation of specific types of assets or liabilities at fair value or on fair value based measurements (e.g. fair values less costs to sell)

• Ind AS 113 applies to determination of fair value in applying Ind ASs (subject to limited exceptions)

- Principles and requirements seek to achieve uniformity, objectivity (as far as possible) and transparency

• Fair value

- Represents price at which an orderly transaction to sell the asset or to transfer the liability would take place between market participants at the measurement date under current market conditions (i.e. an exit price at the measurement date from the perspective of a market participant that holds the asset or owes the liability).

- Is a market-based measurement, not an entity-specific measurement.

KEY DIFFERENCESIND AS vs. EXISTING PRACTICES

October 2016

Titre de la présentation29

01MEASUREMENT OF FINANCIAL ASSETS AND LIABILITIES

DateTitre de la présentation

IND AS 109

• Comprehensive standard dealing with recognition, classification, measurement and de-recognition of financial assets and liabilities; also deals with hedge accounting

• Complements

Ind AS 32, Financial Instruments : Presentation

Ind AS 107, Financial Instruments : Disclosures

• Applicable to most financial assets and financial liabilities

• Scope much larger than that of Accounting Standard (AS) 13, Accounting for Investments

• Drastically changes accounting for financial instruments, particularly most financial assets

Date31 Titre de la présentation

MEASUREMENT OF INVESTMENTS

• Ind AS 109 not directly applicable to investments in subsidiaries, joint ventures and associates

• At initial recognition, an investment to be classified as

- subsequently measured at amortised cost, or- subsequently measured at fair value through other comprehensive income

(FVTOCI), or- subsequently measured at fair value through profit or loss (FVTPL)

• Classification dependent on

- entity’s business model for managing the investments, and- contractual cash flow characteristics of the investment

• Initial recognition generally at fair value plus transaction costs

- Transaction costs not included in the case of FVTPL investments

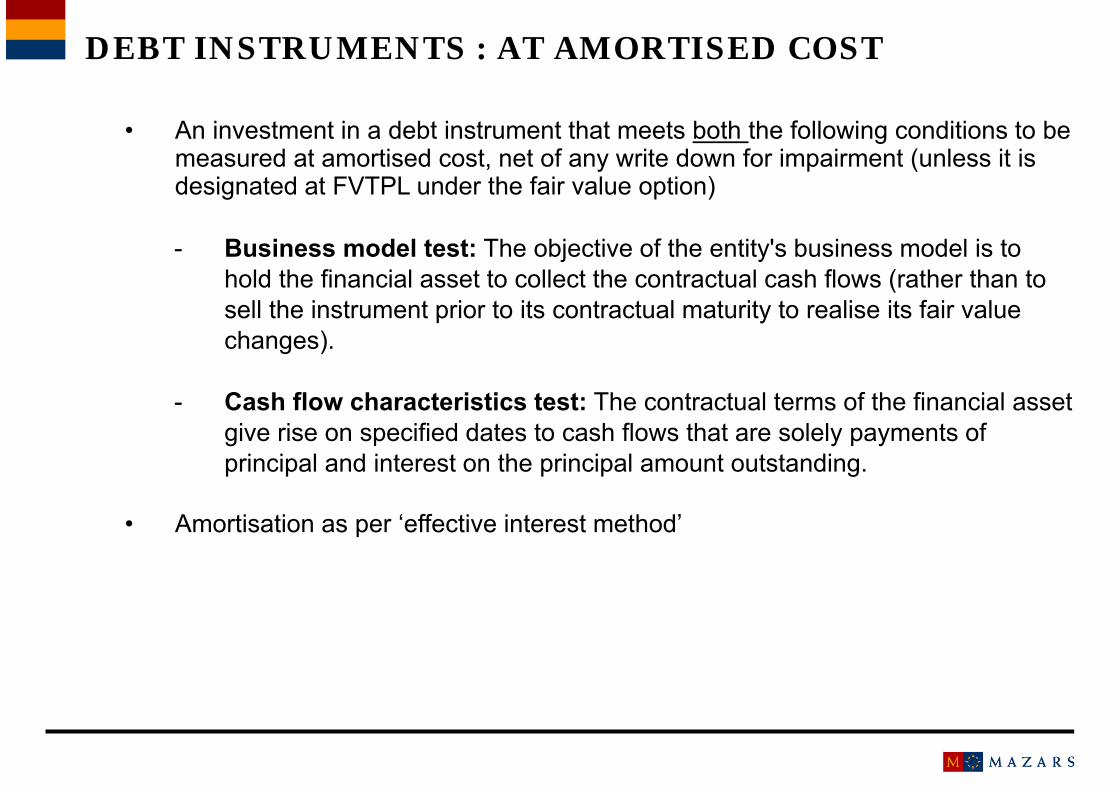

DEBT INSTRUMENTS : AT AMORTISED COST

• An investment in a debt instrument that meets both the following conditions to be measured at amortised cost, net of any write down for impairment (unless it is designated at FVTPL under the fair value option)

- Business model test: The objective of the entity's business model is to hold the financial asset to collect the contractual cash flows (rather than to sell the instrument prior to its contractual maturity to realise its fair value changes).

- Cash flow characteristics test: The contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding.

• Amortisation as per ‘effective interest method’

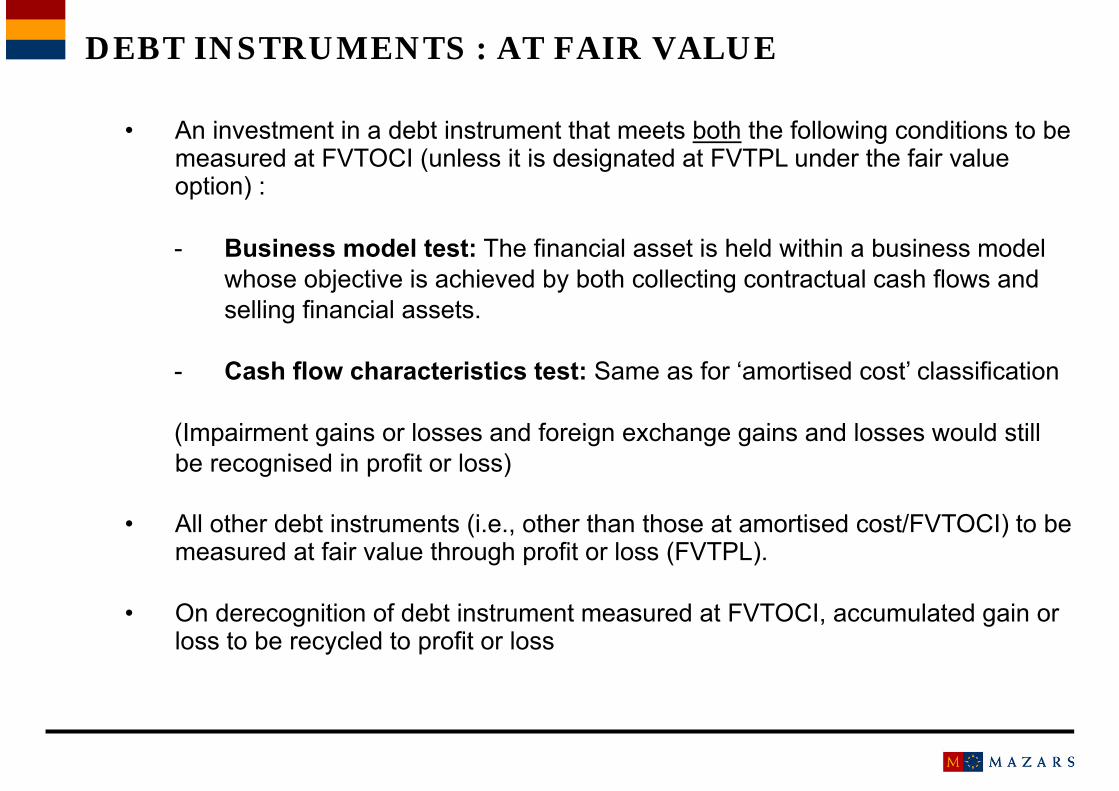

DEBT INSTRUMENTS : AT FAIR VALUE

• An investment in a debt instrument that meets both the following conditions to be measured at FVTOCI (unless it is designated at FVTPL under the fair value option) :

- Business model test: The financial asset is held within a business model whose objective is achieved by both collecting contractual cash flows and selling financial assets.

- Cash flow characteristics test: Same as for ‘amortised cost’ classification

(Impairment gains or losses and foreign exchange gains and losses would still be recognised in profit or loss)

• All other debt instruments (i.e., other than those at amortised cost/FVTOCI) to be measured at fair value through profit or loss (FVTPL).

• On derecognition of debt instrument measured at FVTOCI, accumulated gain or loss to be recycled to profit or loss

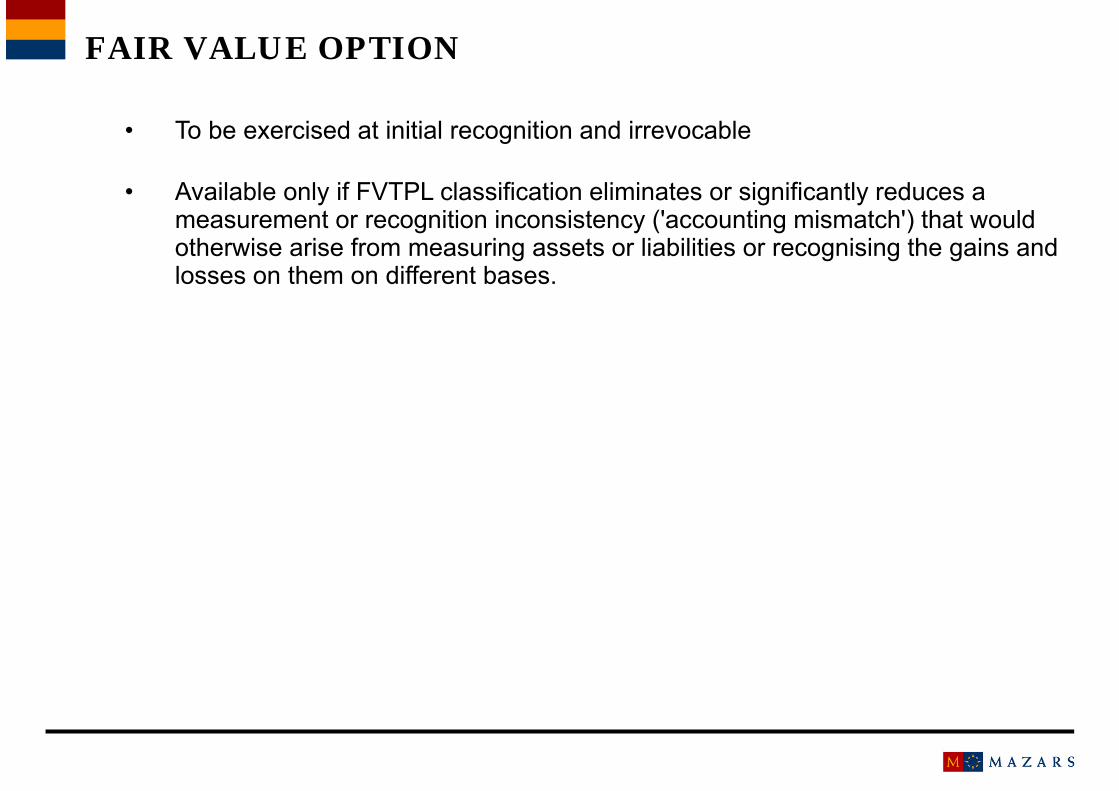

FAIR VALUE OPTION

• To be exercised at initial recognition and irrevocable

• Available only if FVTPL classification eliminates or significantly reduces a measurement or recognition inconsistency ('accounting mismatch') that would otherwise arise from measuring assets or liabilities or recognising the gains and losses on them on different bases.

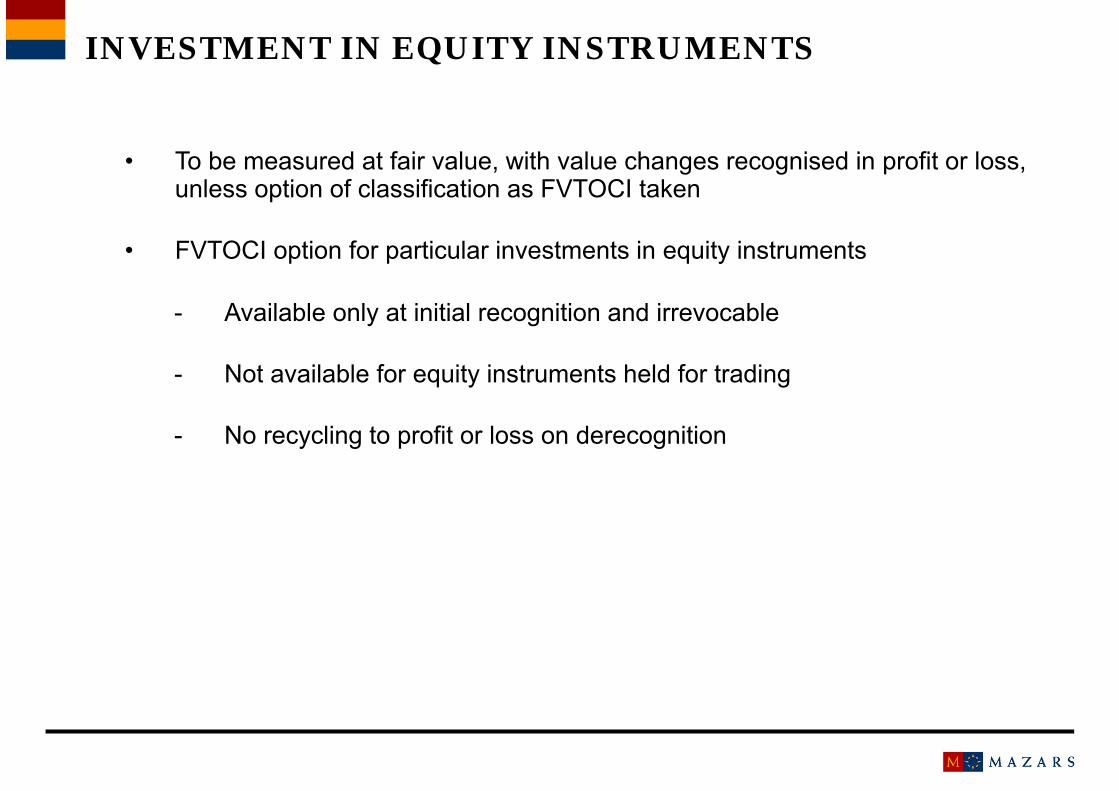

INVESTMENT IN EQUITY INSTRUMENTS

• To be measured at fair value, with value changes recognised in profit or loss, unless option of classification as FVTOCI taken

• FVTOCI option for particular investments in equity instruments

- Available only at initial recognition and irrevocable

- Not available for equity instruments held for trading

- No recycling to profit or loss on derecognition

DERIVATIVES

• To be measured at fair value, with value changes recognised in profit or loss unless the derivative is a hedging instrument in an eligible hedging relationship.

TRADE RECEIVABLES/LOANS GIVEN

• Would generally warrant classification as ‘subsequently measured at amortised cost’.

• Initial measurement generally at fair value plus transaction costs; as per Ind AS 18 in case of trade receivables

TRADE PAYABLES/LOANS AND OTHER BORROWINGS TAKEN

• Initial recognition at fair value plus transaction costs (transaction costs not included in the case of liabilities at fair value through profit or loss)

• Subsequent measurement generally at amortised cost

• Classification as measured at FVTPL also available in limited cases, e.g., in situations of ‘accounting mismatch’

• Gains and losses on financial liabilities designated as at FVTPL to be split as follows:

- Change in fair value attributable to changes in credit risk of the liability –generally to be presented in OCI; no subsequent recycling from OCI to profit or loss

- Remaining amount of change -- presented in profit or loss.

INVESTMENTS IN SUBSIDIARIES/ JOINT VENTURES/ ASSOCIATES (IN STAND-ALONE FINANCIAL STATEMENTS OF INVESTOR)

• Subject to some exceptions, in stand-alone financial statements, investments in subsidiaries, joint ventures and associates can be accounted for either:

- at cost, or

- in accordance with Ind AS 109

• An entity to apply same accounting for each category of investments

- No definition of ‘category’

02SHARE-BASED PAYMENTS(IND AS 102)

Date

MAJOR DIFFERENCES

• Scope not limited to share-based payments to employees; applicable to most share-based payments

- Limited scope exclusions, e.g., transactions in which the entity acquires goods as part of the net assets acquired in a business combination

• Requirements relating to share-based payments to employees different from those of ICAI’s Guidance Note in two major respects:

- Equity-settled share-based payments to be measured with reference to fair value of instruments granted as of the grant date

Intrinsic value method not permitted except where grant-date fair value of equity instruments cannot be estimated reliably

- Option of straight-line recognition of compensation cost in case of graded vesting not provided

03CONCEPT OF CONTROL UNDER IND AS

DateTitre de la présentation

CONCEPT OF ‘CONTROL’ UNDER IND AS

• Control

“An investor controls an investee when it is exposed, or has rights, to variable returns from its involvement with the investee and has the ability to affect those returns through its power over the investee” (Ind AS 110, Consolidated Financial Statements)

• Only one party can have ‘control’ of investee at any point of time

Date44 Titre de la présentation

ELEMENTS OF ‘CONTROL’: POWER, VARIABLE RETURNS, LINKAGE

• Power of ‘investor’ over ‘investee’- An investor has power over an investee when the investor has existing

rights that give it the current ability to direct the relevant activities- ‘Relevant activities’ – “activities of the investee that significantly affect the

investee’s returns”

• Variability of returns, i.e., investor is exposed to, or has rights to, variable returns from its involvement with the investee- In effect, means that the investor is exposed to risks and/or rewards of

performance of the investee

• Link between ‘power’ and ‘returns’- Investor’s ability to affect its returns from its involvement with the investee

through its power over the investee- If investor is acting as agent, this link is missing

Date45 Titre de la présentation

RELEVANT ACTIVITIES

• For most entities such as manufacturing/trading entities, a range of operating and financing activities are ‘relevant activities’, e.g.,

- selling and purchasing of goods or services- managing financial assets during their life (including upon default)- selecting, acquiring or disposing of operating assets- determining a funding structure or obtaining funding

Date46 Titre de la présentation

THE CRITICAL QUESTION

• In most cases, assessment of control issue primarily involves determining whether investor has power over investee’s relevant activities

- Variability assessment is mostly straightforward (e.g., when investor holds equity instruments of the investee), though it may involve complexities in some cases

- Linkage (between power and returns) is also generally clear, but may require more in-depth analysis where there is delegation of power (e.g., where an asset manager has control)

Date47 Titre de la présentation

POWER

• Power arises from rights such as the following:

- Rights in the form of voting rights (or potential voting rights) of an investee;

- rights to appoint or remove members of the investee’s key management personnel who have the ability to direct the relevant activities;

- other rights (such as decision-making rights specified in a management contract) that give the holder the ability to direct the relevant activities.

Date48 Titre de la présentation

POWER WITH MAJORITY VOTING RIGHTS

• Where –

- the relevant activities are directed by a vote of the holder of the majority of the voting rights, or

- a majority of the members of the governing body that directs the relevant activities are appointed by a vote of the holder of the majority of the voting rights,

the investor with majority voting power has power over relevant activities of the investee except in limited circumstances, e.g. where voting rights are not substantive

POWER WITHOUT MAJORITY VOTING RIGHTS

• Potential voting rights

- Consider only those potential voting rights that are substantive

• Rights arising from other contractual arrangements, including an agreement with other vote holders

• De facto power

DE FACTO POWER - WITHOUT MAJORITY VOTING RIGHTS

• Depends on all facts and circumstances including the size of the investor’s holding of voting rights relative to the size and dispersion of holdings of the other vote holders and number of votes cast at previous shareholders’ meetings- the more voting rights an investor holds, the more likely that the investor has

‘power ‘- the more voting rights an investor holds relative to other vote holders, the

more likely that the investor has ‘power’ - the more parties that would need to act together to outvote the investor, the

more likely that the investor has ‘power’

An investor holds 47 per cent of the voting rights of an investee. The remaining voting rights are held by thousands of shareholders, none individually holding more than 1 per cent of the voting rights. None of the shareholders has any arrangements to consult any of the others or make collective decisions.

WHETHER DE FACTO POWER ?

Investor A holds 44 per cent of the voting rights of an investee. Two other investors each hold 26 per cent of the voting rights of the investee. The remaining voting rights are held by four other shareholders, each holding 1 per cent. There are no other arrangements that affect decision-making.

WHETHER DE FACTO POWER ?

Entity X, entity Y and various small shareholders hold 35%, 40% and 25% voting power respectively in entity A. Entity Y and majority of small shareholders have attended and voted at the past general meetings. At entity A’s most recent general meeting entity Y did not vote and entity X had sufficient votes to elect three of its named directors to a board of nine directors, being all of the board members that were put forward for election in the current year. All other matters put to a vote of the shareholders were for routine business and the proposals of executive management were carried out.

WHETHER DE FACTO POWER ?

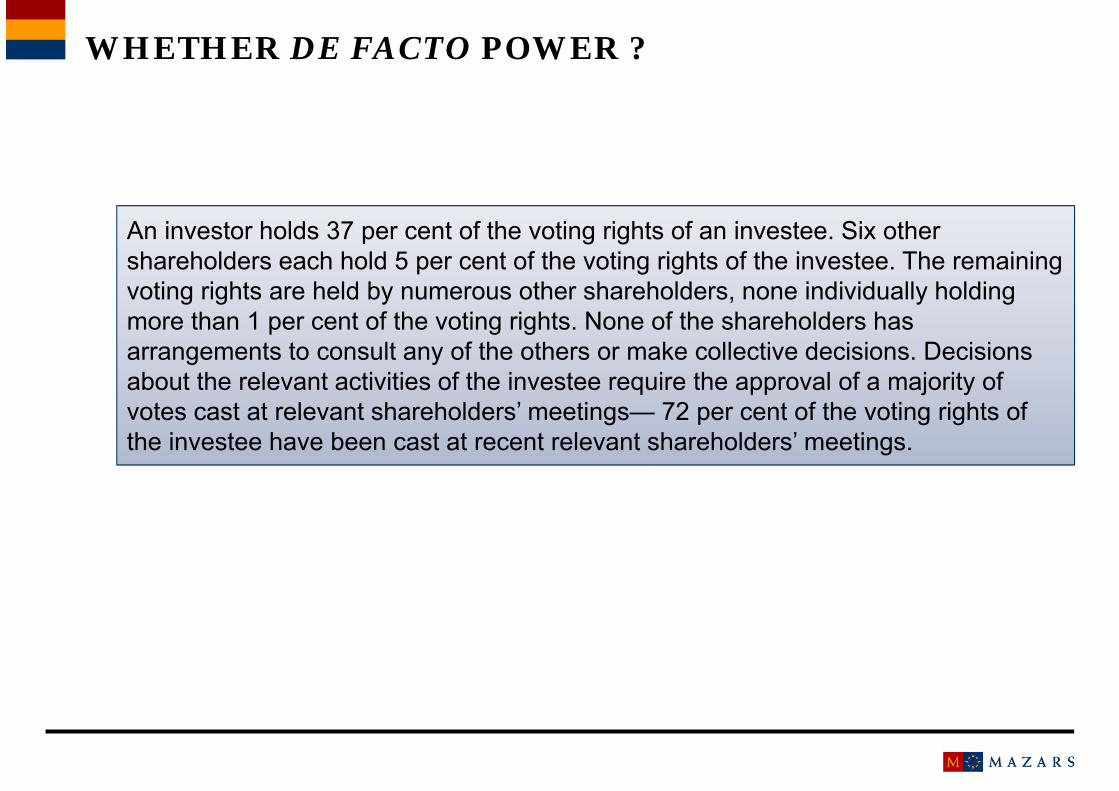

An investor holds 37 per cent of the voting rights of an investee. Six other shareholders each hold 5 per cent of the voting rights of the investee. The remaining voting rights are held by numerous other shareholders, none individually holding more than 1 per cent of the voting rights. None of the shareholders has arrangements to consult any of the others or make collective decisions. Decisions about the relevant activities of the investee require the approval of a majority of votes cast at relevant shareholders’ meetings— 72 per cent of the voting rights of the investee have been cast at recent relevant shareholders’ meetings.

CONTROL ISSUE UNRESOLVED

• If it is not clear, having considered all the relevant factors, that the investor has power, the investor does not control the investee.

04BUSINESS COMBINATIONS(IND AS 103)

DateTitre de la présentation

BUSINESS COMBINATIONS: PRE-IND AS ACCOUNTING

• Addressed by AS 14 which deals only with accounting for amalgamations, i.e., where one company gets merged with another company

• Two methods of accounting:

- Pooling of interests method Transferee to recognise assets, liabilities and reserves and surplus of

transferor at book values as per transferor’s books (at appointed date); any difference between share capital of transferor and share capital of transferee issued in lieu thereof to be adjusted in reserves

- Purchase method Transferee to recognise assets and liabilities of transferor at book values

as per transferor’s books or with reference to their fair values (at appointed date); any difference between consideration and net assets to be debited to goodwill (or credited to capital reserve)

BUSINESS COMBINATIONS: PRE-IND AS ACCOUNTING

• Pooling of interests method to be applied if all of the five specified conditions met

- One of the conditions is that no adjustment to book values of transferor's assets or liabilities is intended to be made when they are incorporated into books of transferee

• If any one or more of the specified conditions is not met, purchase method to be applied

IND AS 103 “BUSINESS COMBINATIONS”

• Barring limited exceptions, applies to all transactions or other events in which an acquirer obtains control of one or more businesses

- Business - An integrated set of activities and assets that is capable of being conducted and managed for the purpose of providing a return in the form of dividends, lower costs or other economic benefits directly to owners.

Date59 Titre de la présentation

MODES OF EFFECTING BUSINESS COMBINATIONS

• Various modes, choice being based on legal, taxation or other factors

• Some examples (Y Ltd assumed to be a business in all cases):

- X Ltd acquires one or more (or even all) operating divisions of Y Ltd- X Ltd acquires all the shares in Y Ltd and Y Ltd merges into X Ltd- X Ltd acquires a controlling stake in Y Ltd

• Acquisition of a subsidiary attracts business combination accounting only in consolidated financial statements of parent

BUSINESS COMBINATION ACCOUNTING: OVERALL APPROACH

• Combination of entities or businesses under common control

- A business combination involving entities or businesses in which all the combining entities or businesses are ultimately controlled by the

same party or parties both before and after the business combination (e.g. amalgamation of one fellow subsidiary with another), and

that control is not transitory.

- Combined entity to apply ‘pooling of interests’ method (manner of application similar to AS 14)

• Other business combinations included within scope of the standard

- Acquirer to apply ‘acquisition’ method

Date61 Titre de la présentation

RECOGNITION AND MEASUREMENT OF ASSETS AND LIABILITIES

• Identifiable assets acquired and liabilities assumed – subject to some exceptions, to be measured at acquisition-date fair values - Identifiable assets or liabilities may include items not previously recognized

by acquiree, e.g., in-process R&D, self-generated brands, off-market element of operating lease contracts

• Contingent liabilities of acquiree, which were not recognized by acquiree because it was not probable that an outflow of resources embodying economic benefits will be required to settle the obligation, also to be recognized if their acquisition-date fair values can be measured reliably

• Consideration transferred – to be measured generally at acquisition-date fair value

• If consideration exceeds the amount of identifiable net assets, excess is ‘goodwill’

• If the amount of identifiable net assets exceeds consideration, excess is ‘bargain purchase’ gain; to be credited to capital reserve

ACQUISITION-RELATED COSTS

• Generally, to be expensed in the periods in which the costs are incurred and the services are received

- Exception: costs to issue debt or equity to be recognized in accordance with Ind AS 32 and Ind AS 109.

05CONSOLIDATED FINANCIAL STATEMENTS(IND AS 110)

DateTitre de la présentation

SUBSIDIARIES TO BE CONSOLIDATED

• A parent required to prepare CFS to consolidate all subsidiaries, with the exception of post-employment benefit plans or other long-term employee benefit plans to which Ind AS 19, Employee Benefits, applies

- No exemption on grounds of (i) temporary control or (ii) restrictions on distributions to parent

CONSOLIDATION PROCEDURES: MAJOR DIFFERENCES FROM AS 21

• Determination of goodwill/capital reserve arising on acquisition of subsidiary – to be based largely on fair values (as per Ind AS 103)

• Financial statements of parent and subsidiaries to be used for consolidation to have same reporting date, unless impracticable.

- Even if impracticable, difference between the date of the subsidiary’s financial statements and that of CFS to be no more than three months (six months under AS 21)

• CFS to be prepared using uniform accounting policies for like transactions and other events in similar circumstances.

- No exemption on ground of impracticability of applying uniform accounting policies

CONSOLIDATION PROCEDURES

• Ind AS 12, Income Taxes, to be applied to temporary differences that arise from the elimination of profits and losses resulting from intra-group transactions.

- As per AS 21, tax expenses of parent and subsidiaries are simply clubbed

• Profit or loss and each component of other comprehensive income to be allocated between the owners of the parent and to the non-controlling interests, even if this results in the non-controlling interests having a negative balance.

- Under AS 21, minority shareholders’ interests cannot be negative

06JOINT ARRANGEMENTS(IND AS 111)

Dateion

CLASSIFICATION OF JOINT ARRANGEMENTS

• Under Ind AS 111

- Joint operations- Joint ventures

• Under AS 27, ‘joint ventures’ are classified into

- Jointly controlled operations- Jointly controlled assets- Jointly controlled entities

• Generally speaking:

- ‘Jointly controlled operations’ and ‘jointly controlled assets’ as per AS 27 would be ‘joint operations’ under Ind AS 111.

- ‘Jointly controlled entities’ as per AS 27 may be either ‘joint operations’ or ‘joint ventures’ under Ind AS 111

ACCOUNTING BY ‘JOINT OPERATORS’

Similar to accounting for jointly controlled assets/jointly controlled operations under AS 27.

ACCOUNTING BY ‘JOINT VENTURERS’

• Subject to limited exceptions, a joint venturer to account for investment in a joint venture using the equity method

- Above requirement applies even if the joint venturer does not prepare consolidated financial statements

- Manner of application of equity method (which is also applicable to associates) has some significant differences vis-à-vis AS 23

- Proportionate consolidation method not allowed

• Treatment in joint venturer’s separate financial statements – at cost or as per Ind AS 109

THANK YOU

Titre de la présentation72