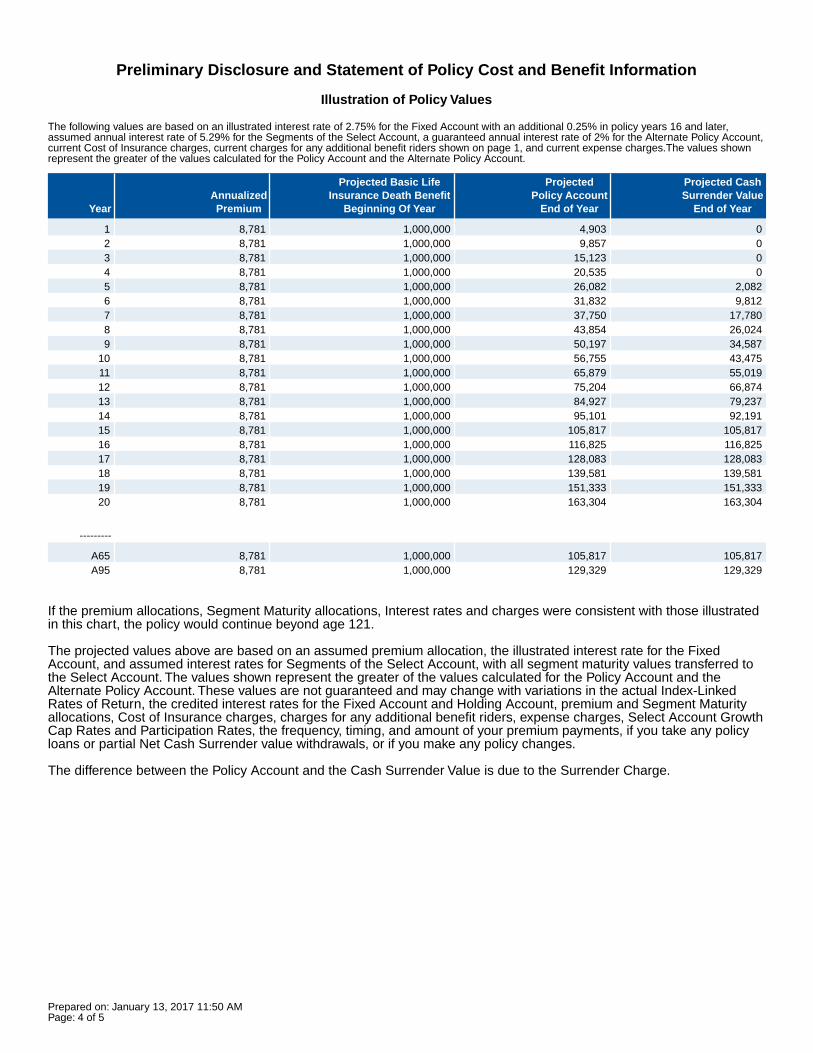

financial strength - first protective · rating is 5th highest of 21; fitch ratings range from aaa...

TRANSCRIPT

32

Financial Strength

GE 114711 (6/16) (Exp. 6/18)Page: 1 of 1

You want to have the confidence that the insurance company you choose has the financial strength tofulfill its obligation to you now and in the future. AXA Equitable and its non New York affiliate, MLOA are part of the global AXA Group2, one of the world's largest financial services organizations3. AXAGroup is a global leader in financial protection strategies and wealth management. AXA Equitable LifeInsurance Company (AXA Equitable, New York, NY), which enjoys an illustrious 150-year history, andMONY Life Insurance Company of America (MLOA) have a shared tradition of helping their customersreach their most important goals. AXA Equitable and MLOA individually, have sole responsibility fortheir own life insurance and annuity obligations and guarantees are based on the claims paying abilityof each entity.

Behind Every Guarantee: Tradition, Strength, StabilityCurrent Financial Strength (Claims-Paying Ability) Ratings of AXA Equitable and MLOA (as of October 2, 2015):

RatingAgency

AXA Equitable Current Rating / Meaning ofCategory / Relative Ranking

MLOA Current Rating / Meaning ofCategory / Relative Ranking

Date Reviewed1

A.M. Best Co. A+ "Superior" 2nd highest of 16 A "Excellent" 3rd highest of 16 08/2015

Fitch AA- "Very Strong" 4th highest of 21 AA- "Very Strong" 4th highest of 21 10/2015

Moody's Aa3 "Excellent" 4th highest of 21 A1 "Good" 5th highest of 21 07/2015

Standard &Poor's

A+ "Strong" 5th highest of 21 A+ "Strong" 5th highest of 21 10/2015

Important - While AXA Equitable Life Insurance Company (AXA Equitable) and MONY Life Insurance Company ofAmerica (MLOA) are affiliated companies, they are each exclusively and entirely responsible for their own claims-payingobligations, and their respective financial strength ratings are exclusively their own. Specifically, AXA Equitable's financialstrength ratings are relevant only to policy/contract holders of AXA Equitable; MLOA's financial strength ratings arerelevant only to policy/contract holders of MLOA. MLOA does not conduct business or offer products in the State of NewYork or in the Commonwealth of Puerto Rico.

1 Date reviewed indicates the last public statement by the rating agency.Ratings are subject to change; contact your financial professional for more details, including information on rating scalesand individual rating sources. The ratings reflected have no bearing on the performance of the variable investment options.Moody's ratings range from Aaa to C, AXA Equitable's Aa3 rating is 4th highest of 21 and MLOA's A1 rating is 5th highestof 21; Standard & Poor's ratings range from AAA to R, AXA Equitable's A+ rating is 5th highest of 21 and MLOA's A+rating is 5th highest of 21; Fitch ratings range from AAA to C, AXA Equitable's AA- rating is 4th highest of 21 and MLOA'sAA- rating is 4th highest of 21; and A.M. Best ratings range from A++ to S, AXA Equitable's A+ rating is 2nd highest of 16and MLOA's A rating is 3rd highest of 16. Moody's applies numerical modifiers 1, 2 and 3 in each rating classification fromAa through Caa. The modifier 1 indicates that the obligation ranks in the higher end of its rating category; the modifier 2indicates a mid-range ranking; and modifier 3 indicates a ranking in the lower end of that rating category. Plus (+) or minus(-) following a rating shows relative standing within the major rating categories. Applicable for Standard & Poor's, Fitch andA.M. Best ratings.

2 "AXA Group" refers to AXA, a French holding company for an international group of insurance and financial servicecompanies, together with its direct and indirect consolidated subsidiaries. MONY Life Insurance Company of America is anindirect, wholly owned subsidiary of AXA.

3 "The World's Largest Public Companies for 2013, Forbes 2000," Forbes magazine. Values calculated in May 2014.Life Insurance sold in New York and Puerto Rico is issued by AXA Equitable Life Insurance Company 1290 Avenue of theAmericas, New York, NY 10104. Life Insurance sold in other jurisdictions is issued by MONY Life Insurance Company ofAmerica (MLOA), (not licensed to solicit or transact business in Puerto Rico nor New York), an Arizona Stock Corporationwith main administrative offices at 525 Washington Blvd., Jersey City, NJ 07310. "AXA" is a brand name of AXA EquitableFinancial Services, LLC and its family of companies, including AXA Equitable Life Insurance Company (NY,NY), MONYLife Insurance Company of America (AZ stock company, administrative office: Jersey City, NJ), AXA Advisors, LLC, andAXA Distributors, LLC. AXA S.A. is a French holding company for a group of international insurance and financial servicescompanies, including AXA Equitable Financial Services, LLC. This brand name change does not change the legal name ofany of the AXA Equitable Financial Services, LLC companies. The obligations of AXA Equitable Life Insurance Companyand MONY Life Insurance Company of America are backed solely by their claims-paying ability.AXA Equitable, MLOA, AXA Advisors and AXA Distributors are subsidiaries of AXA Equitable Financial Services, LLC andAXA Financial, Inc. and do not provide tax or legal advice. Certain types of policies, features and benefits may not beavailable in all jurisdictions or may be different.

Life Insurance: • Is Not a Deposit of Any Bank • Is Not FDIC Insured • Is Not Insured by Any Federal Government Agency• Is Not Guaranteed by Any Bank or Savings Association • Variable Life Insurance May Go Down in Value

1

32

BrightLife® Protectbasic illustrationflexible premium universal life with an index-linked interest option

Narrative PagePrepared For: Valued Client

THIS ILLUSTRATION IS NOT COMPLETE WITHOUT ALL NUMBERED PAGESTHIS ILLUSTRATION IS NOT PART OF THE LIFE INSURANCE POLICY OR CONTRACT

MONY Life Insurance Company of America (MLOA)An Arizona Stock Corporation with its main administrative office at 525 Washington Blvd. Jersey City, NJ 07310

Presented by: John Smith, Delivered in ConnecticutPrepared on: January 13, 2017 11:50 AMMale Preferred Non-Tobacco User Age 50Initial Face Amount: $1,000,000Initial Planned Periodic Premium = $8,781.43Premium Mode: Annual, Riders: NLGInitial Death Benefit Option: A (Level)Minimum Initial Premium: $1,982.50GE 114728 (6/16) (Exp. 6/19), BrightLife Protect, Series 155,GPT-04-2.75%-11.0.0.9-$11,190.00-01-06-W

Policy:BrightLife Protect is a flexible premium universal life insurance policy with a guaranteed interest option called the Fixed Account, and anindex-linked interest option, called the Select Account. A benefit is payable upon the death of the insured person. Deductions from thepremium, and charges applied to the Policy Account are described below. You can make various changes to your Policy includingincreasing or decreasing the Face Amount and changing the premium or death benefit option. You can also make additional premiumpayments subject to applicable tax limits. Although premiums are flexible, depending on actual results, additional premium paymentsmay be necessary to keep the policy in force. The policy may terminate if the net Cash Surrender Value is insufficient to pay the policy'smonthly charges. This is a non-participating policy; no dividends are payable.

The policy values shown reflect the 2% Interest Guarantee Endorsement described below.

Your Policy Charges:Premium charge: There is a front-end premium charge which is deducted before premiums are credited to the Policy Account. On anon-guaranteed basis, 1) in the first two policy years, this charge is 8.00% of gross premiums paid. 2) In policy years 3 and later, 6.00%is deducted from gross premiums paid. For any policy year we guarantee this charge will never be greater than 8.00%. This chargeassumes no requested face amount increases are made. If there is a requested increase in face amount above the previous highestface amount, a similar charge will apply to subsequent premium payments attributed to the increase. If a requested increase in faceamount is shown in this illustration, any such charge has already been reflected in the illustrated policy values and benefits.

Policy Account charges: At the beginning of each month, the following charges (as applicable) are deducted from the Policy Account: amonthly administrative charge, a Cost of Insurance charge, charges for Temporary and Permanent Flat Extras and Rider Costs.

The monthly administrative charge consists of: a fixed charge of not more than $15 (currently $10); plus a charge per $1000 of initialbase policy Face Amount. We will also deduct a monthly administrative charge for each $1000 of requested face amount increase thatrepresents an increase over the previous highest base policy face amount. This charge is based on the attained age of the insured atthe time of the increase. On a guaranteed basis the monthly per $1000 charge will differ between Death Benefit Option A and B and isapplicable until the insured's attained age 121. On a current basis the monthly per $1000 charge is also based on the sex of theinsured and applies during the first 10 policy years and the 10 years following a face amount increase.

The Cost of Insurance (COI) charge is calculated by multiplying the Net Amount at Risk (the Death Benefit minus the Policy Account) bythe monthly COI rate applicable to the insured person at that time. The COI rate generally increases as the insured grows older. Inaddition, the scale of COI rates can change, subject to a guaranteed maximum. A monthly charge is deducted for certain additionalbenefit riders, if elected.

A Surrender Charge applies during the first 15 policy years. Additional surrender charges and a new 15 year period are applicable forrequested face amount increases that represent an increase over the previous highest base policy face amount.

Your Policy Credits:For amounts allocated to the Fixed Account, the balance of your premium and Policy Account not used for the above charges earnsinterest for you. The company has the right to change the interest rates credited to amounts paid into this policy at any time. Theguaranteed minimum interest rate is 2.00% annually. On a non-guaranteed basis there is an interest rate bonus on the portion of theunloaned policy account in the Fixed Account and in the Holding Account; the annual crediting rate is increased by 0.25% in policyyears 16 and later, if the credited rate before the bonus is above the guaranteed minimum crediting rate for the Fixed Account and theHolding Account (The Fixed Account is referred to as the "Guaranteed Interest Account" in your policy and other supplementalmaterial.).

Loans and Partial Withdrawals:You can get cash from the policy through loans and partial withdrawals. Loans and withdrawals reduce the Net Cash Surrender Valueand Net Death Benefit, and may affect the length of time the insurance remains in force. This illustration assumes that loans andwithdrawals are distributed annually, beginning on the policy anniversary of the year in which loans and withdrawals begin. We willdeduct amounts requested as a loan or withdrawal first from the Fixed Account, then from amounts in the Holding Account (based onthe current value of the Holding Account), then on a pro-rata basis from all Segments then in effect (based on current SegmentValues). Anytime there is a deduction from one or more Segments as the result of a loan or withdrawal, we may establish a 12 monthLockout Period, during which amounts would not be transferred into new Segments that would otherwise be available to you. See the"Important Tax Information" page for more information on loans, withdrawals, premium payments, and policy changes.

Page 1 of 21

1

32

BrightLife® Protectbasic illustrationflexible premium universal life with an index-linked interest option

Narrative PagePrepared For: Valued Client

THIS ILLUSTRATION IS NOT COMPLETE WITHOUT ALL NUMBERED PAGESTHIS ILLUSTRATION IS NOT PART OF THE LIFE INSURANCE POLICY OR CONTRACT

MONY Life Insurance Company of America (MLOA)An Arizona Stock Corporation with its main administrative office at 525 Washington Blvd. Jersey City, NJ 07310

Presented by: John Smith, Delivered in ConnecticutPrepared on: January 13, 2017 11:50 AMMale Preferred Non-Tobacco User Age 50Initial Face Amount: $1,000,000Initial Planned Periodic Premium = $8,781.43Premium Mode: Annual, Riders: NLGInitial Death Benefit Option: A (Level)Minimum Initial Premium: $1,982.50GE 114728 (6/16) (Exp. 6/19), BrightLife Protect, Series 155,GPT-04-2.75%-11.0.0.9-$11,190.00-01-06-W

Changes in Face Amount:Face Amount increases are available after the first policy year, but before the insured's attained age 81. The minimum requestedincrease must be at least $10,000. Satisfactory evidence of insurability is required for a Face Amount increase, and the maximum agefor which a face amount increase is permitted may vary based on your underwriting class at that time. We may decline any change thatdoes not conform to our underwriting or policy issue rules then in effect. Face amount increases are not available if Loan Extension is ineffect, or if the increase would cause the policy to exceed our Disability Waiver limits, if that coverage is included on the original policy.Also, face amount increases are not available on policies that have elected the Cash Value Plus Rider or Long-Term Care ServicesRider while either rider is in effect. An increase in face amount may result in a new per $1,000 monthly administrative charge based onthe death benefit option in effect and an additional surrender charge period. Please refer to Your Policy Charges section for furtherdetails.

Face Amount decreases are available after the second policy year, but before the insured's attained age 121. The minimum requesteddecrease is $10,000 and the new face amount cannot be less than the policy minimum Face Amount. Face amount decreases are notavailable if Loan Extension is in effect. See the "IMPORTANT TAX INFORMATION" Section for possible implications.

No Lapse Guarantee (NLG) Rider:The policy includes a No Lapse Guarantee Rider: the policy is guaranteed not to lapse during the first 40 policy years if any policy loanand accrued loan interest does not exceed the Cash Surrender Value. A certain level of premiums must be maintained for theguarantee to be in effect. Paying NLG premiums other than annually will result in higher total NLG premiums.

Loan Extension:If at the beginning of any policy month on or following the policy anniversary nearest the insured person's 75th birthday (but not earlierthan the 20th policy anniversary), the net Cash Surrender Value is not sufficient to cover the monthly deductions, the outstanding loanamount plus accrued loan interest exceeds the greater of the current and initial base policy face amount, the Death Benefit is Option Aand no current or future distribution from the policy will be required to maintain its qualification as life insurance under Section 7702 ofthe Internal Revenue Code, the policy will go on Loan Extension. However, Loan Extension will not go into effect if the policy is in aGrace Period, the Return of Premium Death Benefit Rider is in effect, or any Accelerated Death Benefit Rider or Long-Term CareServices Rider has been exercised. Once on Loan Extension, the policy will not lapse. No new loan or partial withdrawal may be taken,and any premium payments received will be applied as loan repayments. Loan interest will continue to accrue, and if not paid, will beadded to the outstanding loan balance. Under Loan Extension, all riders, endorsements and Segments in the Select Account will beterminated. No Index-Linked Credit will be applicable to the terminated Segments. See the Policy and the Loan Extension Endorsementfor further information.

Charitable Legacy Rider:A Charitable Legacy Rider, if elected at issue, will be made part of your policy. This rider will pay a Charitable Gift Amount to a qualifiedCharitable Organization Beneficiary equal to 1% of the base policy face amount up to a maximum of $100,000, provided that the basepolicy face amount at the time of the insured's death is at least $1,000,000, and this amount will be paid in addition to the base policydeath benefit. You should consult your tax advisor regarding any possible tax consequences.

The illustrated initial base policy face amount of $1,000,000 would be eligible for a Charitable Legacy Rider benefit, if elected, of$10,000 at issue.

Optional Riders Illustrated:None

Key Terms and Definitions:Guaranteed Values: Policy values and benefits based on the illustrated Premium Allocations and Account Value Transfer/SegmentMaturity Allocations that are guaranteed if the Annualized Premium Outlay as shown is paid and no loans, withdrawals, or policychanges other than those shown in this illustration are made. Guaranteed values are based on a guaranteed minimum interest rate of2.00% for the Fixed Account, if applicable, the Segment guaranteed interest rate of 0% for the applicable Select Account, 8%guaranteed front-end premium charge, guaranteed maximum COI charges, guaranteed charges for any benefits or riders and theguaranteed maximum monthly administrative charges.

Page 2 of 21

1

32

BrightLife® Protectbasic illustrationflexible premium universal life with an index-linked interest option

Narrative PagePrepared For: Valued Client

THIS ILLUSTRATION IS NOT COMPLETE WITHOUT ALL NUMBERED PAGESTHIS ILLUSTRATION IS NOT PART OF THE LIFE INSURANCE POLICY OR CONTRACT

MONY Life Insurance Company of America (MLOA)An Arizona Stock Corporation with its main administrative office at 525 Washington Blvd. Jersey City, NJ 07310

Presented by: John Smith, Delivered in ConnecticutPrepared on: January 13, 2017 11:50 AMMale Preferred Non-Tobacco User Age 50Initial Face Amount: $1,000,000Initial Planned Periodic Premium = $8,781.43Premium Mode: Annual, Riders: NLGInitial Death Benefit Option: A (Level)Minimum Initial Premium: $1,982.50GE 114728 (6/16) (Exp. 6/19), BrightLife Protect, Series 155,GPT-04-2.75%-11.0.0.9-$11,190.00-01-06-W

Non-Guaranteed Mid-Point Values: Policy values and benefits based on an average of guaranteed and non-guaranteed charges for anybenefits or riders and interest rates half way between the non-guaranteed rates and the guaranteed minimum rates for the FixedAccount, if applicable, and for the Segments of the Select Account.

Non-Guaranteed Values: Policy values and benefits based on the illustrated Premium Allocations and Account Value Transfer/SegmentMaturity Allocations based on-non-guaranteed charges for benefits and riders and interest rates illustrated. Non-guaranteed values arebased on the current interest rates for the Fixed Account, if applicable and the illustrated interest rates for Segments of the SelectAccount, if applicable, current front-end premium charge, current COI charges and current monthly administrative charges. Theillustrated interest rates, current front-end charge, current COI charges and current monthly administrative charges apply to policiesissued as of the preparation date shown. In general, current COI rates vary depending on Face Amount. Current COI rates may belower at base policy Face Amounts of $250,000 and above. Illustrated interest rates for the Fixed Account, current COI charges andcurrent monthly administrative charges are not guaranteed and may be changed at any time. The illustrated interest rates for segmentsof the Select Account, if applicable, assume that the currently illustrated Growth Cap Rate, Participation Rate and Indexed-Linked Rateof Return will continue unchanged for all years shown. This is not likely to occur. Please refer to the Illustrated Select Account CreditingRates section for further details. If future interest rates are lower or charges are higher than MONY Life Insurance Company ofAmerica's non-guaranteed illustrated interest rates or charges, there may be insufficient policy values to provide the projected non-guaranteed policy values that are shown in this illustration.Policy values and benefits are based on the illustrated Premium Allocationsand Account Value Transfer/Segment Maturity Allocations, non-guaranteed charges for benefits and riders, and the illustrated interestrates. The illustrated interest rates and charges apply to policies issued as of the preparation date shown. In general, current COI ratesvary depending on the Face Amount. Current COI rates may be lower at base policy Face Amounts of $250,000 and above.

Alternative Illustrated Interest Rates: These Non-Guaranteed policy values are based on illustrated interest rates that are equal tothe guaranteed minimum annual interest rate of 2.00% for the Fixed Account if applicable, and the Segment guaranteed minimumannual interest rate of 0% for segments of the Select Account, current front-end premium charges, current COI charges, currentmonthly administrative charges, current charges for any riders, and, if applicable, the monthly segment charge. Current front-endpremium, COI, rider, and monthly administrative charges are not guaranteed and may be changed at any time. If future policycharges are higher than MONY Life Insurance Company of America's non-guaranteed illustrated charges, there may be insufficientpolicy values to provide the projected non-guaranteed policy values that are shown in this illustration.

Current Illustrated Interest Rates: These Non-Guaranteed policy values are based on specified illustrated interest rates for theFixed Account, if applicable, and specified illustrated interest rates for segments of the Select Account, current front-end premiumcharges, current COI charges, current monthly administrative charges, current charges for any riders, and, if applicable, the monthlysegment charge. Illustrated interest rates for the Fixed Account and the Select Account, and current front-end premium, COI, rider,and monthly administrative charges are not guaranteed and may be changed at any time. The illustrated interest rates for segmentsof the Select Account assume that currently illustrated Growth Cap Rates, Participation Rates and Indexed-Linked Rates of Returnwill continue unchanged for all years shown; this is not likely to occur. Please refer to "Maximum Illustrated Crediting Rate" sectionfor further details. If future interest rates are lower, or policy charges are higher than MONY Life Insurance Company of America'snon-guaranteed illustrated interest rates or charges, there may be insufficient policy values to provide the projected non-guaranteedpolicy values that are shown in this illustration.

ADDITIONAL ACTIONS TAKEN BY YOU WITH REGARD TO YOUR POLICY, SUCH AS VARYING THE PREMIUM PAYMENTPATTERN OR TIMING, VARYING PREMIUM ALLOCATIONS OR ACCOUNT VALUE TRANSFER/SEGMENT MATURITYALLOCATIONS, POLICY CHANGES, BORROWING, OR PARTIAL WITHDRAWALS, WILL ALSO AFFECT THE VALUES SHOWN ANDTHE PERIOD OF COVERAGE AND MAY REQUIRE YOU TO MAKE MORE OUT-OF-POCKET PREMIUM PAYMENTS THAN ARESHOWN AND RESULT IN HIGHER OR LOWER TAX PREMIUM LIMITS.

Planned Periodic Premium (PPP): The amount the policy owner plans to pay each modal period as stated in the life insuranceapplication. It is the amount which will be drafted or billed based on the frequency selected. The initial modal Planned Periodic Premiumis shown below.

Page 3 of 21

1

32

BrightLife® Protectbasic illustrationflexible premium universal life with an index-linked interest option

Narrative PagePrepared For: Valued Client

THIS ILLUSTRATION IS NOT COMPLETE WITHOUT ALL NUMBERED PAGESTHIS ILLUSTRATION IS NOT PART OF THE LIFE INSURANCE POLICY OR CONTRACT

MONY Life Insurance Company of America (MLOA)An Arizona Stock Corporation with its main administrative office at 525 Washington Blvd. Jersey City, NJ 07310

Presented by: John Smith, Delivered in ConnecticutPrepared on: January 13, 2017 11:50 AMMale Preferred Non-Tobacco User Age 50Initial Face Amount: $1,000,000Initial Planned Periodic Premium = $8,781.43Premium Mode: Annual, Riders: NLGInitial Death Benefit Option: A (Level)Minimum Initial Premium: $1,982.50GE 114728 (6/16) (Exp. 6/19), BrightLife Protect, Series 155,GPT-04-2.75%-11.0.0.9-$11,190.00-01-06-W

Based on the assumptions of this illustration, an annual premium of $27,673.00 would be required to be paid to the insured's attainedage 121 to guarantee the Initial Face Amount to attained age 121. This amount assumes that no policy changes, partial withdrawals, orloans are made. This amount is based on maximum cost of insurance charges, guaranteed maximum rider charges, guaranteedadministrative charges and minimum guaranteed interest rates. The actual premium required to keep your policy in force on a non-guaranteed basis, based on actual charges deducted and interest credited over the life of the policy, might be lower than the amountshown above. Premiums may need to be limited to conform to the definition of Life Insurance or to avoid Modified Endowment Contractstatus for the policy. See the 'IMPORTANT TAX INFORMATION' section for more information.

Minimum Initial Premium (MIP): The minimum premium due on or before delivery of the policy as illustrated.

7-Pay Premium: If the cumulative premiums paid during the first seven policy years at any time exceed the cumulative "7-PayPremiums", the policy becomes a "Modified Endowment Contract" (MEC). Policy changes and partial withdrawals may also impact your7-Pay Premium and MEC status. See the 'IMPORTANT TAX INFORMATION' section.

Guideline Premium Limit: This limit is defined as the greater of 1) The Guideline Single Premium (GSP), and 2) The sum of theGuideline Level Annual Premiums (GLAP) for the number of years the policy has been in force (but not beyond the insured's attainedage 99). If a premium payment would cause this limit to be exceeded, the excess payment will be returned to you. This ensures that thepolicy meets the definition of life insurance for Federal income tax purposes. Policy changes may impact your guideline premium limit. Certain policy changes such as Death Benefit Option changes, Face Amount decreases and partial withdrawals can cause yourguideline limit to decrease at the time of the change, or in future years, or both. Anytime the limit is decreased to less than thepreviously paid premiums for guideline testing, the excess premium will be forced out and returned to you without regard to your policy'saccount value. In some cases, you may only be able to pay a premium to keep your policy inforce until the end of the policy year.

If your policy is a Modified Endowment Contract (MEC), the amount forced out will be taxable to the extent there is gain in your policyand the taxable amount will be subject to a 10% tax penalty if you are not 59½ or older. See the "Important Tax Information" sectionlater in the illustration. Even if your policy is not a MEC, the amount could be taxable if there is gain in your policy.

Death Benefit Options: "Option A" provides a fixed level Death Benefit equal to the policy's Face Amount. "Option B" provides a DeathBenefit equal to the Face Amount of the policy plus the Policy Account. Under certain conditions, a higher death benefit amount mayapply in order that the policy meet the definition of life insurance for Federal income tax purposes. See the policy for further informationon the availability and effects of changes in Death Benefit Option after issue.

Surrender Charges: The Cash Surrender Value is equal to the Policy Account minus any applicable surrender charge, but will never beless than zero. Actual surrender proceeds will be net of any outstanding policy loan and accrued loan interest. Surrender charges applyduring the first fifteen policy years and may apply for fifteen years after a Face Amount increase.

Underwriting Class: The policy charges illustrated assume this policy is issued on the Preferred Non-Tobacco User underwriting class.Flat extras (additional charges based upon health, avocation, or other underwriting factors) may also be charged on a permanent ortemporary basis. Actual policy charges required for the insurance coverage depend on the outcome of the underwriting process, andmay vary from what is shown on this illustration. If the result is different, your financial professional will give you an illustration based onthe same underwriting class as the policy issued.

Underwriting risk factors, regulatory, and other guidelines may limit the amount of insurance available.

Coverage After Attained Age 120: If this policy is in force and not in default when the insured person reaches age 121, it will remain inforce subject to the policy loan provision. No premium payments, partial withdrawals, changes in Face Amount or changes in deathbenefit option will be permitted after attained age 120 of the insured person. Policy loans, loan repayments and transfers may continueto be made subject to our normal rules as stated in other provisions of the policy pertaining to these items. No deductions for COI oradministrative charges will be made after attained age 120 of the insured person.

Term Conversion: If this product is illustrated pursuant to a term conversion, the exchange is subject to AXA Equitable's or its affiliate'srules then in effect as to plan, age and class of risk. If the new policy does not have the same or similar underwriting risk class as theterm policy, the new policy will have the closest comparable underwriting risk class as determined by AXA Equitable or its affiliate."Same or similar" is based on original underwriting requirements, not necessarily the name of the underwriting rate class.

Page 4 of 21

1

32

BrightLife® Protectbasic illustrationflexible premium universal life with an index-linked interest option

Narrative PagePrepared For: Valued Client

THIS ILLUSTRATION IS NOT COMPLETE WITHOUT ALL NUMBERED PAGESTHIS ILLUSTRATION IS NOT PART OF THE LIFE INSURANCE POLICY OR CONTRACT

MONY Life Insurance Company of America (MLOA)An Arizona Stock Corporation with its main administrative office at 525 Washington Blvd. Jersey City, NJ 07310

Presented by: John Smith, Delivered in ConnecticutPrepared on: January 13, 2017 11:50 AMMale Preferred Non-Tobacco User Age 50Initial Face Amount: $1,000,000Initial Planned Periodic Premium = $8,781.43Premium Mode: Annual, Riders: NLGInitial Death Benefit Option: A (Level)Minimum Initial Premium: $1,982.50GE 114728 (6/16) (Exp. 6/19), BrightLife Protect, Series 155,GPT-04-2.75%-11.0.0.9-$11,190.00-01-06-W

Premiums are assumed to be paid on the first day of each policy year, or on the first day of the selected premium payment period ifother than annual. Policy values, death benefits, and the age shown are as of the end of the policy year. This illustration assumes thatthe currently illustrated non-guaranteed elements and Index-Linked Rate of Return for the Select Account, if applicable, will continue

unchanged for all years shown. This is not likely to occur, and actual results may be more or less favorable than those shown.

Page 5 of 21

1

32

BrightLife® Protectbasic illustrationflexible premium universal life with an index-linked interest option

Narrative SummaryPrepared For: Valued Client

THIS ILLUSTRATION IS NOT COMPLETE WITHOUT ALL NUMBERED PAGESTHIS ILLUSTRATION IS NOT PART OF THE LIFE INSURANCE POLICY OR CONTRACT

MONY Life Insurance Company of America (MLOA)An Arizona Stock Corporation with its main administrative office at 525 Washington Blvd. Jersey City, NJ 07310

Presented by: John Smith, Delivered in ConnecticutPrepared on: January 13, 2017 11:50 AMMale Preferred Non-Tobacco User Age 50Initial Face Amount: $1,000,000Initial Planned Periodic Premium = $8,781.43Premium Mode: Annual, Riders: NLGInitial Death Benefit Option: A (Level)Minimum Initial Premium: $1,982.50GE 114728 (6/16) (Exp. 6/19), BrightLife Protect, Series 155,GPT-04-2.75%-11.0.0.9-$11,190.00-01-06-W

Summary of Index-Linked Option, Holding Account and Fixed Account

BrightLife Protect gives you the opportunity to allocate amounts to the Select Account linked to the performance of one financial index:S&P 500 Price Return index. Amounts may also be allocated to a traditional Fixed Account. We reserve the right to add, change, ordiscontinue indexes available. When you submit premiums we deduct a premium charge, and if you directed them to the SelectAccount, place your net premiums in the Holding Account. Otherwise, amounts are allocated to a Fixed Account where your moneyearns interest. (This illustration assumes amounts are deposited into the Holding Account, any applicable charges are deducted, andthen any remaining amounts are transferred into the Segment on the same day. Therefore, the illustration does not reflect any interestcredited for the time premiums are in the Holding Account.). At the time of issue, you decide the percentage of net premiums toallocate to our Select Account and the Fixed Account. After issue, you may request a change in future premium allocation percentages,or request a transfer of amounts between the unloaned portion of the Fixed Account and the Holding Account. In order to have anyeffect on amounts transferred into segments on the next Segment Start Date, your request must be received at our AdministrativeOffice by the Segment Cut-Off Date specified in the Policy. No transfers from a Segment will be permitted on or after the Segment StartDate until the Segment Maturity Date. We reserve the right to limit the maximum dollar amount that can be included in Segments. Wealso reserve the right to establish a minimum dollar amount that is eligible for transfer into a Segment.

Amounts that you allocate to the Select Account are placed in the Holding Account and then are transferred from the Holding Accountto a Segment at the next available Segment Start Date, if all conditions contained in the Policy are met. The portion of your PolicyAccount in the Holding Account and the Fixed Account will accumulate, after deductions, at rates of interest we determine; such rateswill never be less than the guaranteed minimum interest rate. The portion of your Policy Account in Segments of the Select Accountduring a Segment Term will accumulate, after any deductions, at the Segment Guaranteed Minimum Annual Interest Rate, which is0.00%.

We will apply any Index-Linked Rate of Return based on the performance rate of the S&P 500 Price Return Index to Segments in theSelect Account on the Segment Maturity Date. In accordance with your direction, we will transfer all or a portion of the resultingSegment Maturity Value to the unloaned portion of the Fixed Account or the Holding Account of the Select Account. If you do notprovide direction, we will transfer the entire Segment Maturity Value to the Holding Account of the Select Account. Please refer to yourPolicy for detailed information and conditions.

If your Policy terminates without value, you have the right to request a restoration of benefits, subject to the rules and conditionscontained in the Policy. If the Policy's benefits are restored, you will not be eligible for any Index-Linked Credit in connection withpreviously established Segments.

The S&P 500 Price Return Index is a passively managed index of 500 stocks, from a broad range of industries, considered to berepresentative of the stock market in general. Please note that, while the Index-Linked Rate of Return relies on the performance of anIndex(excluding dividends), it is not possible to invest directly in the Index.

The Holding Account and Fixed Account earn interest at rates we declare periodically; these rates will not be less than the GuaranteedMinimum Interest Rate of 2.00%. We will credit the amount in the Holding Account with the same interest rates we credit to theunloaned portion of the Fixed Account; the current interest rate is 2.75%.

The Indexed Option currently available with this product is:• Select Account

• Segment term: 1 year• Segment Guaranteed Annual Interest Rate: 0.00%• Current Growth Cap Rate: 8.50%• Guaranteed Minimum Growth Cap Rate: 3.00%• Current Participation Rate: 100.00%• Guaranteed Minimum Participation Rate: 100%

S&P®, Standard & Poor's®, S&P 500® and Standard & Poor's 500TM are trademarks of Standard & Poor's and have been licensed for use by MONY Life Insurance Companyof America (MLOA). BrightLife Protect is not sponsored, endorsed, sold or promoted by Standard & Poor's and Standard & Poor's does not make anyrepresentation regarding the advisability of investing in the product.

Throughout this illustration the net policy account values, net cash surrender values and net death benefits which are shown are based upon the greaterof the Policy Account Value and the Alternate Policy Account Value (per the 2% Interest Guarantee Endorsement).

Page 6 of 21

1

32

BrightLife® Protectbasic illustrationflexible premium universal life with an index-linked interest option

THIS ILLUSTRATION IS NOT COMPLETE WITHOUT ALL NUMBERED PAGESTHIS ILLUSTRATION IS NOT PART OF THE LIFE INSURANCE POLICY OR CONTRACT

MONY Life Insurance Company of America (MLOA)An Arizona Stock Corporation with its main administrative office at 525 Washington Blvd. Jersey City, NJ 07310

Presented by: John Smith, Delivered in ConnecticutPrepared on: January 13, 2017 11:50 AMMale Preferred Non-Tobacco User Age 50Initial Face Amount: $1,000,000Initial Planned Periodic Premium = $8,781.43Premium Mode: Annual, Riders: NLGInitial Death Benefit Option: A (Level)Minimum Initial Premium: $1,982.50GE 114728 (6/16) (Exp. 6/19), BrightLife Protect, Series 155,GPT-04-2.75%-11.0.0.9-$11,190.00-01-06-W

Index-Linked Option Key Terms and Definitions:

It is important that you understand how Index-Linked Interest Options work, including both the guaranteed and non-guaranteed featuresbefore allocating amounts to the Select Account.

Index:The index upon which the Index-Linked Credit is based. The Index associated with the indexed option is shown above.

Select Account:The portion of your Policy Account that is comprised of a Holding Account and Segments associated with an indexed option (The SelectAccount is referred to as the "Indexed Account" in your policy and other supplemental material.).

Holding Account:The portion of the Select Account that temporarily holds net premiums and other amounts you request to be allocated or transferred tothe corresponding indexed option. Such amounts will be transferred into a new Segment of the applicable indexed option on theSegment Start Date subject to the conditions described in your policy. This illustration does not reflect any conditions which we do notcurrently impose but have reserved the right to impose in the future.

Segment:A new segment is created when an amount is transferred from the Holding Account into a Segment. A policy can have as many astwelve active segments at any single point in time.

Segment Start Date:The date a Segment is established which is generally on the 15th of each calendar month, provided all conditions stated in the Policyare met. Please refer to your policy for the actual date. This illustration assumes that the dates premiums are paid will coincide withdeclared Segment Start Dates and amounts are credited to the Holding Account, any applicable charges are deducted, and remainingamounts are transferred to a Segment on the same day. This is not likely to occur.

Segment Maturity Date:The date on which a Segment Term is completed and the Index-Linked Credit for that Segment, if any, is included in the Segment Value.

Point-to-Point Method:The Index-Linked Credit is calculated using a point to point method, which compares the value of the Index at two discrete points intime: the Segment Start Date and the Segment Maturity Date.

Index Performance Rate (IPR):This rate represents the percentage change in an Index during a Segment Term.IPR = (B) divided by (A) -1(A) = value of the Index at the close of business on the Segment Start Date(B) = value of the Index at the close of business on the Segment Maturity Date

Growth Cap Rate:This is the maximum rate of return that will be used in the calculation of the Index-Linked Credit. We will determine the Growth CapRate for each Segment of the Select Account on or prior to the Segment Start Date. The Growth Cap Rate for any Segment will notchange during a Segment Term. However, the Growth Cap Rate may vary for each new Segment of the Select Account. Any such ratewill never be less than the Guaranteed Minimum Growth Cap Rate for the indexed option. The illustrated interest rates for Segments ofthe Select Account, if applicable, assume that Growth Cap Rates will remain constant in future years. This is not likely to occur. If futureIndex-Linked Rates of Return are lower than the illustrated interest rates, actual Policy Values may be lower than the projected non-guaranteed values shown in this illustration.

Participation Rate:The percentage of the Index Performance Rate that is used in calculating the Index-Linked Credit. The Participation Rate for anySegment will not change during the Segment Term. However we may change the Participation Rate for new Segments, but such ratewill never be less than the Guaranteed Minimum Participation rate.

Segment Guaranteed Minimum Annual Interest Rate:The guaranteed minimum annual interest rate for a Segment, which is 0.00%.

Page 7 of 21

1

32

BrightLife® Protectbasic illustrationflexible premium universal life with an index-linked interest option

THIS ILLUSTRATION IS NOT COMPLETE WITHOUT ALL NUMBERED PAGESTHIS ILLUSTRATION IS NOT PART OF THE LIFE INSURANCE POLICY OR CONTRACT

MONY Life Insurance Company of America (MLOA)An Arizona Stock Corporation with its main administrative office at 525 Washington Blvd. Jersey City, NJ 07310

Presented by: John Smith, Delivered in ConnecticutPrepared on: January 13, 2017 11:50 AMMale Preferred Non-Tobacco User Age 50Initial Face Amount: $1,000,000Initial Planned Periodic Premium = $8,781.43Premium Mode: Annual, Riders: NLGInitial Death Benefit Option: A (Level)Minimum Initial Premium: $1,982.50GE 114728 (6/16) (Exp. 6/19), BrightLife Protect, Series 155,GPT-04-2.75%-11.0.0.9-$11,190.00-01-06-W

Index-Linked Rate of Return:The rate of return that is used to calculate the Index-Linked Credit. Subject to the Participation Rate and Growth Cap Rate, the Index-Linked Rate of Return reflects any growth in the performance of the Index that exceeds Segment Guaranteed Minimum Annual InterestRate. The Index-Linked Rate of Return will never be less than zero. The formula used in the calculation of the Index-Linked Rate ofReturn is shown below.Index-Linked Rate of Return = [the lesser of (A) x (B) and (C)] - (D)(A) = IPR(B) = Participation Rate(C) = Growth Cap Rate(D) = Segment Guaranteed Minimum Interest Rate

Index-Linked Credit:The amount included in the Segment Value on the Segment Maturity Date. The credit is calculated by multiplying the Segment's Index-Linked Rate of Return by the Segment's Average Monthly Balance at Segment Maturity. The average monthly balance is the average ofthe 12 month end Segment Principal Amounts. Any Index-Linked Credit may be positive or zero, resulting in an increase or no changeto your Policy Account.

Segment Principal Amount:This is the amount that is transferred from the Holding Account to a new Segment as of the Segment Start Date, minus any applicabledeductions. It does not include any Segment guaranteed interest, but does include interest credited to amounts in the Holding Accountprior to Segment Start Date.

Segment Value:The Segment Principal Amount increased by any: (1) Segment Guaranteed Minimum Annual Interest during a Segment Term and (2)Index-Linked Credit on the Segment Maturity Date.

2% Interest Guarantee Endorsement:As briefly stated below, this endorsement provides an additional guarantee that can improve your policy. There is no charge for thisendorsement and it will never result in lower cash value or death benefit.

This endorsement provides an Alternate Policy Account value that is used in addition to the regular Policy Account value to determine ifthe policy values are sufficient to cover the monthly deductions, and to calculate the Net Cash Surrender Value, the maximum amountavailable for policy loans, and the death benefit. It is also used to determine changes in face amount resulting from death benefit optionchanges. It does not increase the amount available for a partial withdrawal.

The unloaned portion of the Alternate Policy Account is credited with fixed and guaranteed interest at the daily equivalent of 2%annually. The loaned portion of the Alternate Policy Account is credited with interest daily, at the same interest rate we credit to theloaned portion of the regular Policy Account, which will never be less than 2% annually. Monthly deductions taken from the AlternatePolicy Account may be different than those taken from the Policy Account.

If the Net Cash Surrender Value is not sufficient to cover the total monthly deductions, your policy will not be in default if the AlternateNet Cash Surrender Value is sufficient to cover the alternate monthly deductions.

If you give up your policy while the insured is living or take a maximum new loan, you will receive the greater of: (1) the Net CashSurrender Value, or (2) the Alternate Net Cash Surrender Value.

If at the time of the insured person's death the Alternate Policy Account Value is greater than the Policy Account Value, we will use theAlternate Policy Account Value to determine the death benefit under the policy. Similarly, if a change in death benefit option isrequested, we will use the greater of the Policy Account Value or the Alternate Policy Account Value to determine the new policy faceamount on the date the change takes effect.

Please refer to your Policy and the Endorsement for more information, including how the Endorsement relates to any other riders orendorsements on your Policy.

Throughout this illustration the net policy account values, net cash surrender values and net death benefits which are shown are basedupon the greater of the Policy Account Value and the Alternate Policy Account Value.

Page 8 of 21

1

32

BrightLife® Protectbasic illustrationflexible premium universal life with an index-linked interest option

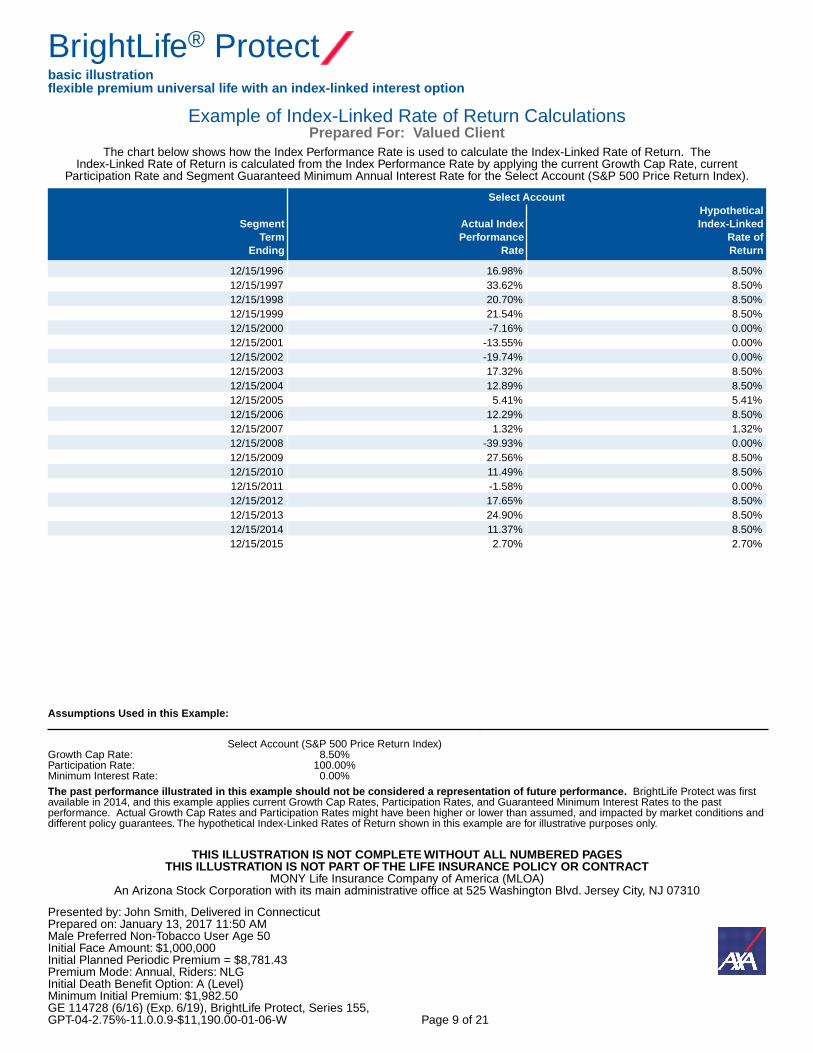

Example of Index-Linked Rate of Return CalculationsPrepared For: Valued Client

The chart below shows how the Index Performance Rate is used to calculate the Index-Linked Rate of Return. TheIndex-Linked Rate of Return is calculated from the Index Performance Rate by applying the current Growth Cap Rate, current

Participation Rate and Segment Guaranteed Minimum Annual Interest Rate for the Select Account (S&P 500 Price Return Index).

THIS ILLUSTRATION IS NOT COMPLETE WITHOUT ALL NUMBERED PAGESTHIS ILLUSTRATION IS NOT PART OF THE LIFE INSURANCE POLICY OR CONTRACT

MONY Life Insurance Company of America (MLOA)An Arizona Stock Corporation with its main administrative office at 525 Washington Blvd. Jersey City, NJ 07310

Presented by: John Smith, Delivered in ConnecticutPrepared on: January 13, 2017 11:50 AMMale Preferred Non-Tobacco User Age 50Initial Face Amount: $1,000,000Initial Planned Periodic Premium = $8,781.43Premium Mode: Annual, Riders: NLGInitial Death Benefit Option: A (Level)Minimum Initial Premium: $1,982.50GE 114728 (6/16) (Exp. 6/19), BrightLife Protect, Series 155,GPT-04-2.75%-11.0.0.9-$11,190.00-01-06-W

Assumptions Used in this Example:

Select Account (S&P 500 Price Return Index)Growth Cap Rate: 8.50%Participation Rate: 100.00%Minimum Interest Rate: 0.00%

The past performance illustrated in this example should not be considered a representation of future performance. BrightLife Protect was firstavailable in 2014, and this example applies current Growth Cap Rates, Participation Rates, and Guaranteed Minimum Interest Rates to the pastperformance. Actual Growth Cap Rates and Participation Rates might have been higher or lower than assumed, and impacted by market conditions anddifferent policy guarantees. The hypothetical Index-Linked Rates of Return shown in this example are for illustrative purposes only.

Select AccountHypothetical

Segment Actual Index Index-LinkedTerm Performance Rate of

Ending Rate Return

12/15/1996 16.98% 8.50%12/15/1997 33.62% 8.50%12/15/1998 20.70% 8.50%12/15/1999 21.54% 8.50%12/15/2000 -7.16% 0.00%12/15/2001 -13.55% 0.00%12/15/2002 -19.74% 0.00%12/15/2003 17.32% 8.50%12/15/2004 12.89% 8.50%12/15/2005 5.41% 5.41%12/15/2006 12.29% 8.50%12/15/2007 1.32% 1.32%12/15/2008 -39.93% 0.00%12/15/2009 27.56% 8.50%12/15/2010 11.49% 8.50%12/15/2011 -1.58% 0.00%12/15/2012 17.65% 8.50%12/15/2013 24.90% 8.50%12/15/2014 11.37% 8.50%12/15/2015 2.70% 2.70%

Page 9 of 21

1

32

BrightLife® Protectbasic illustrationflexible premium universal life with an index-linked interest option

Illustration AssumptionsPrepared For: Valued Client

THIS ILLUSTRATION IS NOT COMPLETE WITHOUT ALL NUMBERED PAGESTHIS ILLUSTRATION IS NOT PART OF THE LIFE INSURANCE POLICY OR CONTRACT

MONY Life Insurance Company of America (MLOA)An Arizona Stock Corporation with its main administrative office at 525 Washington Blvd. Jersey City, NJ 07310

Presented by: John Smith, Delivered in ConnecticutPrepared on: January 13, 2017 11:50 AMMale Preferred Non-Tobacco User Age 50Initial Face Amount: $1,000,000Initial Planned Periodic Premium = $8,781.43Premium Mode: Annual, Riders: NLGInitial Death Benefit Option: A (Level)Minimum Initial Premium: $1,982.50GE 114728 (6/16) (Exp. 6/19), BrightLife Protect, Series 155,GPT-04-2.75%-11.0.0.9-$11,190.00-01-06-W

Premium Allocations:

Select Account (S&P 500 Price Return Index)- Initial Illustrated Crediting Rate: 5.29%- Premium Allocation: 100% from year 1 to 71

Fixed Account- Initial Illustrated Crediting Rate: 2.75%- Guaranteed Rate: 2.00%- Premium Allocation: 0% from year 1 to 71

Unless you have requested otherwise, this illustration assumes we will transfer the entire Segment Maturity Value to theSelect Account on the Segment Maturity Date.

Maximum Illustrated Crediting Rate:

The average annual "look back" rate for the Select Account has been determined by calculating an average annual point-to-point rate of return for all of the 25-year rolling periods that begin on a trading day falling on or after the "look backstarting date" and that end on or before 12/31/2015, assuming that the Current Growth Cap Rate, Current ParticipationRate, and 0% Segment Guaranteed Minimum Interest Rate apply to all hypothetical 1-Year Segments during each rollingperiod.

The maximum illustrated crediting rate for the Select Account has been set equal to its average annual look back rate. The Current Growth Cap Rate and Participation Rate, Look Back Starting Date, Minimum Annual Look Back Rate,Maximum Annual Look Back Rate, Average Annual Look Back Rate, and Maximum Illustrated Crediting Rate are shown inthe table below:

Indexed Option

Growth CapRate/

ParticipationRate

Look BackStarting Date

MinimumAnnual LookBack Rate

MaximumAnnual LookBack Rate

Average AnnualLook Back Rate

MaximumIllustrated

Crediting Rate

Select Account 8.50%/100% 12/31/1949 3.48% 6.76% 5.29% 5.29%

The past performance of the S&P 500 Price Return Index is not intended to predict actual future performance and is notguaranteed. Note that BrightLife Protect was not available for at least part of the historical period analyzed above. Theactual growth cap rate and participation rate of an indexed life insurance product existing over the period analyzed mighthave been higher or lower than assumed in this calculation, and likely would have fluctuated with market conditions,subject to product guarantees.

The maximum illustrated annual crediting rate for the unloaned Fixed Account is the current non-guaranteed annualcrediting rate which is 2.75%.

Page 10 of 21

1

32

BrightLife® Protectbasic illustrationflexible premium universal life with an index-linked interest option

Illustration AssumptionsPrepared For: Valued Client

THIS ILLUSTRATION IS NOT COMPLETE WITHOUT ALL NUMBERED PAGESTHIS ILLUSTRATION IS NOT PART OF THE LIFE INSURANCE POLICY OR CONTRACT

MONY Life Insurance Company of America (MLOA)An Arizona Stock Corporation with its main administrative office at 525 Washington Blvd. Jersey City, NJ 07310

Presented by: John Smith, Delivered in ConnecticutPrepared on: January 13, 2017 11:50 AMMale Preferred Non-Tobacco User Age 50Initial Face Amount: $1,000,000Initial Planned Periodic Premium = $8,781.43Premium Mode: Annual, Riders: NLGInitial Death Benefit Option: A (Level)Minimum Initial Premium: $1,982.50GE 114728 (6/16) (Exp. 6/19), BrightLife Protect, Series 155,GPT-04-2.75%-11.0.0.9-$11,190.00-01-06-W

Any Select Account selected has been projected at its own illustrated rate and the results have been combined with anyvalues in the Fixed Account in this illustration.

The maximum illustrated crediting rate for the Select Account is based on the current Growth Cap Rate and ParticipationRate. We reserve the right to change the Growth Cap Rate and Participation Rate, but they will never be less than theminimums provided in the policy. We will determine the Growth Cap Rate and Participation Rate for each Segment of theSelect Account on or prior to the Segment Start Date. The current charge illustrations assume that the currently illustratedFixed Account and Select Account crediting rates will continue unchanged for all years shown; this is not likely to occur,and actual policy performance will be either more or less favorable than shown. If future interest rates or Index-LinkedRates of Return are lower than the illustrated crediting rates there may be insufficient policy values to provide theprojected current policy values that are shown in this illustration. Please consult with your independent advisors to obtainwhatever advice you deem necessary and appropriate in selecting hypothetical Select Account crediting rates.

Page 11 of 21

1

32

BrightLife® Protectbasic illustrationflexible premium universal life with an index-linked interest option

THIS ILLUSTRATION IS NOT COMPLETE WITHOUT ALL NUMBERED PAGESTHIS ILLUSTRATION IS NOT PART OF THE LIFE INSURANCE POLICY OR CONTRACT

MONY Life Insurance Company of America (MLOA)An Arizona Stock Corporation with its main administrative office at 525 Washington Blvd. Jersey City, NJ 07310

Presented by: John Smith, Delivered in ConnecticutPrepared on: January 13, 2017 11:50 AMMale Preferred Non-Tobacco User Age 50Initial Face Amount: $1,000,000Initial Planned Periodic Premium = $8,781.43Premium Mode: Annual, Riders: NLGInitial Death Benefit Option: A (Level)Minimum Initial Premium: $1,982.50GE 114728 (6/16) (Exp. 6/19), BrightLife Protect, Series 155,GPT-04-2.75%-11.0.0.9-$11,190.00-01-06-W

Policy # (if Known): ________ Numeric Summary and Signature PagePrepared For: Valued Client

SUMMARY VALUES ANNUALIZEDPREMIUM OUTLAY

NET POLICYACCOUNT VALUE

NET CASHSURRENDERVALUE

NET DEATHBENEFIT

FINALYEAR OFCOVERAGE

GUARANTEED VALUES Year 5Year 10Year 20Age 70

$8,781$8,781$8,781$8,781

$1,411$0$0$0

$0$0$0$0

$1,000,000$1,000,000$1,000,000$1,000,000

41414141

NON-GUARANTEEDMID-POINT VALUES

Year 5Year 10Year 20Age 70

$8,781$8,781$8,781$8,781

$12,759$18,562$50$50

$0$5,282$50$50

$1,000,000$1,000,000$1,000,000$1,000,000

41414141

NON-GUARANTEED VALUESASSUMING CURRENTILLUSTRATED INTEREST RATES

Year 5Year 10Year 20Age 70

$8,781$8,781$8,781$8,781

$26,082$56,755$163,304$163,304

$2,082$43,475$163,304$163,304

$1,000,000$1,000,000$1,000,000$1,000,000

all yearsall yearsall yearsall years

X ORIGINAL ILLUSTRATION OR REVISED ILLUSTRATION

Important ConfirmationsI understand that MONY Life Insurance Company of America (MLOA) is relying on me to confirm the following information:

• I understand that the definition of "replace" includes any lapse, exchange, surrender, withdrawal, or borrowing from an existing insurance policy orannuity contract in connection with purchasing a new life insurance policy; it is with this understanding that I have answered the replacementquestion on the application.

• I have received a copy of all numbered pages of this illustration. I have reviewed this illustration and understand that its purpose is to help meunderstand how the policy works, but that it is not part of an insurance contract. I have been informed and understand that 1) actual policy values willprobably be different than shown, 2) any non-guaranteed elements illustrated are subject to change and could be higher or lower, and 3) anyguaranteed values or features may be affected by loans and/or withdrawals I may make.

• If this illustration does not fully conform to the policy I am issued, I will receive a conforming illustration at or prior to the time the policy is delivered.For example, the policy may be issued for a different underwriting class, premium mode or amount, or with different benefits. These and any otherchanges will impact the values illustrated. I will carefully review that conforming illustration upon receipt.

• I understand that this illustration may include an index-linked interest option subject to an index formula, and that changes in the index or applicationof the formula may result in policy benefits that are higher or lower than the illustrated non-guaranteed values, or may require additional premiumpayments to keep a policy in-force. I have been provided with a description any such index formula, and informed how changes in the value of theindex may affect policy benefits, as a part of this illustration.

Signature of Policyowner Date

Signature of Policyowner Date

I certify that this illustration has been presented to the policyowner and that if this illustration doesn't conform to the policy that is issued, I will deliver aconforming illustration as described above at or prior to the time the policy is delivered. I have explained that any non-guaranteed elements illustrated aresubject to change. I have made no statements that are inconsistent with this illustration.

Signature of Associate or Representative Agency Associate Date

Address Phone

Page 12 of 21

1

32

BrightLife® Protectbasic illustrationflexible premium universal life with an index-linked interest option

Narrative PagePrepared For: Valued Client

THIS ILLUSTRATION IS NOT COMPLETE WITHOUT ALL NUMBERED PAGESTHIS ILLUSTRATION IS NOT PART OF THE LIFE INSURANCE POLICY OR CONTRACT

MONY Life Insurance Company of America (MLOA)An Arizona Stock Corporation with its main administrative office at 525 Washington Blvd. Jersey City, NJ 07310

Presented by: John Smith, Delivered in ConnecticutPrepared on: January 13, 2017 11:50 AMMale Preferred Non-Tobacco User Age 50Initial Face Amount: $1,000,000Initial Planned Periodic Premium = $8,781.43Premium Mode: Annual, Riders: NLGInitial Death Benefit Option: A (Level)Minimum Initial Premium: $1,982.50GE 114728 (6/16) (Exp. 6/19), BrightLife Protect, Series 155,GPT-04-2.75%-11.0.0.9-$11,190.00-01-06-W

Column Definitions Report:

Year-Age The policy year and the Insured's age as of the end of the year.

Annualized PremiumOutlay

The annualized premium that you have indicated that you plan to pay.

Net Policy AccountValue

An interest earning account created by the policyowner's premiums net of premium charges. ThePolicy Account is credited with interest at rates guaranteed not to be less than guaranteedinterest rates for the Fixed Account and Holding Accounts, if applicable and the GuaranteedInterest Rate for the Select Account Segments, if applicable annually as well as any applicableIndex-Linked Credit. Interest is applied to the Policy Account after deducting the following:monthly administrative charges, COI charges, charges for any riders, and charges for policychanges (if any). See 'Your Policy Charges' section for further information. The Net PolicyAccount is the Policy Account net of loans and loan interest.

Net Cash SurrenderValue

The value of the Policy Account, less the Surrender Charge and any outstanding policy loan andaccrued loan interest.

Net Death Benefit The amount that will be paid to the beneficiary of the base policy upon proof of death of theInsured. The Net Death Benefit illustrated is calculated as an end of policy year value, and is netof any outstanding loan, accrued loan interest, and liens. The actual Net Death Benefit payable isdetermined as of the date of the Insured's death.

Year of Life Expectancy The highlighted policy year (#) denotes the illustrated insured's life expectancy based on theinsured's issue age and the 2008 Valuation Basic Table.

Throughout this illustration the net policy account values, net cash surrender values and net death benefitswhich are shown are based upon the greater of the Policy Account Value and the Alternate Policy Account Value

(per the 2% Interest Guarantee Endorsement).

Page 13 of 21

1

32

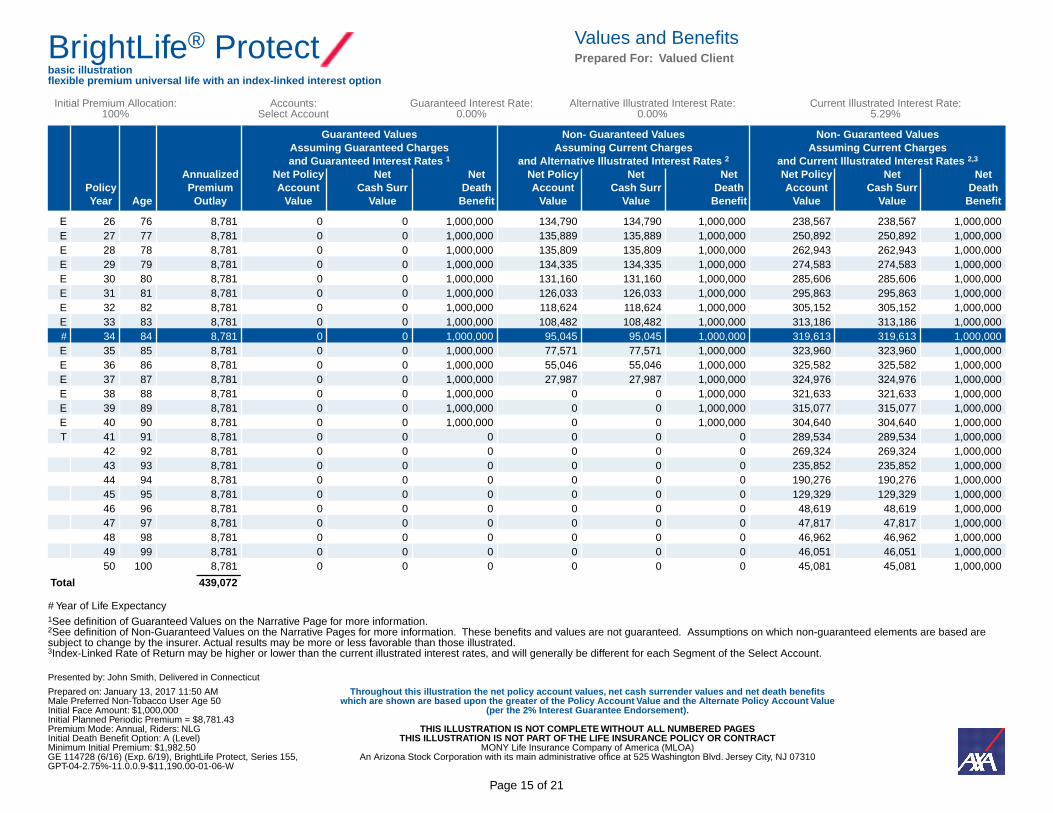

Values and BenefitsPrepared For: Valued ClientBrightLife® Protect

basic illustrationflexible premium universal life with an index-linked interest option

Initial Premium Allocation:100%

Accounts:Select Account

Guaranteed Interest Rate:0.00%

Alternative Illustrated Interest Rate:0.00%

Current Illustrated Interest Rate:5.29%

Presented by: John Smith, Delivered in Connecticut

Throughout this illustration the net policy account values, net cash surrender values and net death benefitswhich are shown are based upon the greater of the Policy Account Value and the Alternate Policy Account Value

(per the 2% Interest Guarantee Endorsement).

Prepared on: January 13, 2017 11:50 AMMale Preferred Non-Tobacco User Age 50Initial Face Amount: $1,000,000Initial Planned Periodic Premium = $8,781.43

THIS ILLUSTRATION IS NOT COMPLETE WITHOUT ALL NUMBERED PAGESTHIS ILLUSTRATION IS NOT PART OF THE LIFE INSURANCE POLICY OR CONTRACT

MONY Life Insurance Company of America (MLOA)An Arizona Stock Corporation with its main administrative office at 525 Washington Blvd. Jersey City, NJ 07310

Premium Mode: Annual, Riders: NLGInitial Death Benefit Option: A (Level)Minimum Initial Premium: $1,982.50GE 114728 (6/16) (Exp. 6/19), BrightLife Protect, Series 155,GPT-04-2.75%-11.0.0.9-$11,190.00-01-06-W

# Year of Life Expectancy1See definition of Guaranteed Values on the Narrative Page for more information.2See definition of Non-Guaranteed Values on the Narrative Pages for more information. These benefits and values are not guaranteed. Assumptions on which non-guaranteed elements are based aresubject to change by the insurer. Actual results may be more or less favorable than those illustrated.3Index-Linked Rate of Return may be higher or lower than the current illustrated interest rates, and will generally be different for each Segment of the Select Account.

Guaranteed Values Non- Guaranteed Values Non- Guaranteed ValuesAssuming Guaranteed Charges Assuming Current Charges Assuming Current Chargesand Guaranteed Interest Rates 1 and Alternative Illustrated Interest Rates 2 and Current Illustrated Interest Rates 2,3

Annualized Net Policy Net Net Net Policy Net Net Net Policy Net NetPolicy Premium Account Cash Surr Death Account Cash Surr Death Account Cash Surr DeathYear Age Outlay Value Value Benefit Value Value Benefit Value Value Benefit

E 1 51 8,781 958 0 1,000,000 4,700 0 1,000,000 4,903 0 1,000,000E 2 52 8,781 1,666 0 1,000,000 9,289 0 1,000,000 9,857 0 1,000,000E 3 53 8,781 2,018 0 1,000,000 14,016 0 1,000,000 15,123 0 1,000,000E 4 54 8,781 1,977 0 1,000,000 18,705 0 1,000,000 20,535 0 1,000,000E 5 55 8,781 1,411 0 1,000,000 23,339 0 1,000,000 26,082 2,082 1,000,000E 6 56 8,781 195 0 1,000,000 27,975 5,955 1,000,000 31,832 9,812 1,000,000E 7 57 8,781 0 0 1,000,000 32,567 12,597 1,000,000 37,750 17,780 1,000,000E 8 58 8,781 0 0 1,000,000 37,123 19,293 1,000,000 43,854 26,024 1,000,000E 9 59 8,781 0 0 1,000,000 41,684 26,074 1,000,000 50,197 34,587 1,000,000E 10 60 8,781 0 0 1,000,000 46,211 32,931 1,000,000 56,755 43,475 1,000,000E 11 61 8,781 0 0 1,000,000 53,005 42,144 1,000,000 65,879 55,019 1,000,000E 12 62 8,781 0 0 1,000,000 59,647 51,317 1,000,000 75,204 66,874 1,000,000E 13 63 8,781 0 0 1,000,000 66,319 60,629 1,000,000 84,927 79,237 1,000,000E 14 64 8,781 0 0 1,000,000 73,051 70,141 1,000,000 95,101 92,191 1,000,000E 15 65 8,781 0 0 1,000,000 79,911 79,911 1,000,000 105,817 105,817 1,000,000E 16 66 8,781 0 0 1,000,000 86,616 86,616 1,000,000 116,825 116,825 1,000,000E 17 67 8,781 0 0 1,000,000 93,103 93,103 1,000,000 128,083 128,083 1,000,000E 18 68 8,781 0 0 1,000,000 99,335 99,335 1,000,000 139,581 139,581 1,000,000E 19 69 8,781 0 0 1,000,000 105,304 105,304 1,000,000 151,333 151,333 1,000,000E 20 70 8,781 0 0 1,000,000 110,944 110,944 1,000,000 163,304 163,304 1,000,000E 21 71 8,781 0 0 1,000,000 116,414 116,414 1,000,000 175,675 175,675 1,000,000E 22 72 8,781 0 0 1,000,000 121,377 121,377 1,000,000 188,156 188,156 1,000,000E 23 73 8,781 0 0 1,000,000 125,791 125,791 1,000,000 200,738 200,738 1,000,000E 24 74 8,781 0 0 1,000,000 129,569 129,569 1,000,000 213,375 213,375 1,000,000E 25 75 8,781 0 0 1,000,000 132,638 132,638 1,000,000 226,035 226,035 1,000,000

219,536Total

Page 14 of 21

1

32

Values and BenefitsPrepared For: Valued ClientBrightLife® Protect

basic illustrationflexible premium universal life with an index-linked interest option

Initial Premium Allocation:100%

Accounts:Select Account

Guaranteed Interest Rate:0.00%

Alternative Illustrated Interest Rate:0.00%

Current Illustrated Interest Rate:5.29%

Presented by: John Smith, Delivered in Connecticut

Throughout this illustration the net policy account values, net cash surrender values and net death benefitswhich are shown are based upon the greater of the Policy Account Value and the Alternate Policy Account Value

(per the 2% Interest Guarantee Endorsement).

Prepared on: January 13, 2017 11:50 AMMale Preferred Non-Tobacco User Age 50Initial Face Amount: $1,000,000Initial Planned Periodic Premium = $8,781.43

THIS ILLUSTRATION IS NOT COMPLETE WITHOUT ALL NUMBERED PAGESTHIS ILLUSTRATION IS NOT PART OF THE LIFE INSURANCE POLICY OR CONTRACT

MONY Life Insurance Company of America (MLOA)An Arizona Stock Corporation with its main administrative office at 525 Washington Blvd. Jersey City, NJ 07310

Premium Mode: Annual, Riders: NLGInitial Death Benefit Option: A (Level)Minimum Initial Premium: $1,982.50GE 114728 (6/16) (Exp. 6/19), BrightLife Protect, Series 155,GPT-04-2.75%-11.0.0.9-$11,190.00-01-06-W

# Year of Life Expectancy1See definition of Guaranteed Values on the Narrative Page for more information.2See definition of Non-Guaranteed Values on the Narrative Pages for more information. These benefits and values are not guaranteed. Assumptions on which non-guaranteed elements are based aresubject to change by the insurer. Actual results may be more or less favorable than those illustrated.3Index-Linked Rate of Return may be higher or lower than the current illustrated interest rates, and will generally be different for each Segment of the Select Account.

Guaranteed Values Non- Guaranteed Values Non- Guaranteed ValuesAssuming Guaranteed Charges Assuming Current Charges Assuming Current Chargesand Guaranteed Interest Rates 1 and Alternative Illustrated Interest Rates 2 and Current Illustrated Interest Rates 2,3

Annualized Net Policy Net Net Net Policy Net Net Net Policy Net NetPolicy Premium Account Cash Surr Death Account Cash Surr Death Account Cash Surr DeathYear Age Outlay Value Value Benefit Value Value Benefit Value Value Benefit

E 26 76 8,781 0 0 1,000,000 134,790 134,790 1,000,000 238,567 238,567 1,000,000E 27 77 8,781 0 0 1,000,000 135,889 135,889 1,000,000 250,892 250,892 1,000,000E 28 78 8,781 0 0 1,000,000 135,809 135,809 1,000,000 262,943 262,943 1,000,000E 29 79 8,781 0 0 1,000,000 134,335 134,335 1,000,000 274,583 274,583 1,000,000E 30 80 8,781 0 0 1,000,000 131,160 131,160 1,000,000 285,606 285,606 1,000,000E 31 81 8,781 0 0 1,000,000 126,033 126,033 1,000,000 295,863 295,863 1,000,000E 32 82 8,781 0 0 1,000,000 118,624 118,624 1,000,000 305,152 305,152 1,000,000E 33 83 8,781 0 0 1,000,000 108,482 108,482 1,000,000 313,186 313,186 1,000,000# 34 84 8,781 0 0 1,000,000 95,045 95,045 1,000,000 319,613 319,613 1,000,000E 35 85 8,781 0 0 1,000,000 77,571 77,571 1,000,000 323,960 323,960 1,000,000E 36 86 8,781 0 0 1,000,000 55,046 55,046 1,000,000 325,582 325,582 1,000,000E 37 87 8,781 0 0 1,000,000 27,987 27,987 1,000,000 324,976 324,976 1,000,000E 38 88 8,781 0 0 1,000,000 0 0 1,000,000 321,633 321,633 1,000,000E 39 89 8,781 0 0 1,000,000 0 0 1,000,000 315,077 315,077 1,000,000E 40 90 8,781 0 0 1,000,000 0 0 1,000,000 304,640 304,640 1,000,000T 41 91 8,781 0 0 0 0 0 0 289,534 289,534 1,000,000

42 92 8,781 0 0 0 0 0 0 269,324 269,324 1,000,00043 93 8,781 0 0 0 0 0 0 235,852 235,852 1,000,00044 94 8,781 0 0 0 0 0 0 190,276 190,276 1,000,00045 95 8,781 0 0 0 0 0 0 129,329 129,329 1,000,00046 96 8,781 0 0 0 0 0 0 48,619 48,619 1,000,00047 97 8,781 0 0 0 0 0 0 47,817 47,817 1,000,00048 98 8,781 0 0 0 0 0 0 46,962 46,962 1,000,00049 99 8,781 0 0 0 0 0 0 46,051 46,051 1,000,00050 100 8,781 0 0 0 0 0 0 45,081 45,081 1,000,000

439,072Total

Page 15 of 21

1

32

Values and BenefitsPrepared For: Valued ClientBrightLife® Protect

basic illustrationflexible premium universal life with an index-linked interest option

Initial Premium Allocation:100%

Accounts:Select Account

Guaranteed Interest Rate:0.00%

Alternative Illustrated Interest Rate:0.00%

Current Illustrated Interest Rate:5.29%

Presented by: John Smith, Delivered in Connecticut

Throughout this illustration the net policy account values, net cash surrender values and net death benefitswhich are shown are based upon the greater of the Policy Account Value and the Alternate Policy Account Value

(per the 2% Interest Guarantee Endorsement).

Prepared on: January 13, 2017 11:50 AMMale Preferred Non-Tobacco User Age 50Initial Face Amount: $1,000,000Initial Planned Periodic Premium = $8,781.43

THIS ILLUSTRATION IS NOT COMPLETE WITHOUT ALL NUMBERED PAGESTHIS ILLUSTRATION IS NOT PART OF THE LIFE INSURANCE POLICY OR CONTRACT

MONY Life Insurance Company of America (MLOA)An Arizona Stock Corporation with its main administrative office at 525 Washington Blvd. Jersey City, NJ 07310

Premium Mode: Annual, Riders: NLGInitial Death Benefit Option: A (Level)Minimum Initial Premium: $1,982.50GE 114728 (6/16) (Exp. 6/19), BrightLife Protect, Series 155,GPT-04-2.75%-11.0.0.9-$11,190.00-01-06-W

# Year of Life Expectancy1See definition of Guaranteed Values on the Narrative Page for more information.2See definition of Non-Guaranteed Values on the Narrative Pages for more information. These benefits and values are not guaranteed. Assumptions on which non-guaranteed elements are based aresubject to change by the insurer. Actual results may be more or less favorable than those illustrated.3Index-Linked Rate of Return may be higher or lower than the current illustrated interest rates, and will generally be different for each Segment of the Select Account.

Guaranteed Values Non- Guaranteed Values Non- Guaranteed ValuesAssuming Guaranteed Charges Assuming Current Charges Assuming Current Chargesand Guaranteed Interest Rates 1 and Alternative Illustrated Interest Rates 2 and Current Illustrated Interest Rates 2,3

Annualized Net Policy Net Net Net Policy Net Net Net Policy Net NetPolicy Premium Account Cash Surr Death Account Cash Surr Death Account Cash Surr DeathYear Age Outlay Value Value Benefit Value Value Benefit Value Value Benefit

51 101 8,781 0 0 0 0 0 0 44,047 44,047 1,000,00052 102 8,781 0 0 0 0 0 0 42,946 42,946 1,000,00053 103 8,781 0 0 0 0 0 0 41,772 41,772 1,000,00054 104 8,781 0 0 0 0 0 0 40,521 40,521 1,000,00055 105 8,781 0 0 0 0 0 0 39,188 39,188 1,000,00056 106 8,781 0 0 0 0 0 0 37,768 37,768 1,000,00057 107 8,781 0 0 0 0 0 0 36,254 36,254 1,000,00058 108 8,781 0 0 0 0 0 0 34,642 34,642 1,000,00059 109 8,781 0 0 0 0 0 0 32,923 32,923 1,000,00060 110 8,781 0 0 0 0 0 0 31,092 31,092 1,000,00061 111 8,781 0 0 0 0 0 0 29,141 29,141 1,000,00062 112 8,781 0 0 0 0 0 0 27,062 27,062 1,000,00063 113 8,781 0 0 0 0 0 0 24,847 24,847 1,000,00064 114 8,781 0 0 0 0 0 0 22,486 22,486 1,000,00065 115 8,781 0 0 0 0 0 0 19,971 19,971 1,000,00066 116 8,781 0 0 0 0 0 0 17,291 17,291 1,000,00067 117 8,781 0 0 0 0 0 0 14,435 14,435 1,000,00068 118 8,781 0 0 0 0 0 0 11,392 11,392 1,000,00069 119 8,781 0 0 0 0 0 0 8,149 8,149 1,000,00070 120 8,781 0 0 0 0 0 0 4,694 4,694 1,000,00071 121 8,781 0 0 0 0 0 0 1,013 1,013 1,000,00072 122 0 0 0 0 0 0 0 1,066 1,066 1,000,00073 123 0 0 0 0 0 0 0 1,123 1,123 1,000,00074 124 0 0 0 0 0 0 0 1,182 1,182 1,000,00075 125 0 0 0 0 0 0 0 1,244 1,244 1,000,000

623,482Total

Page 16 of 21

1

32

BrightLife® Protectbasic illustrationflexible premium universal life with an index-linked interest option

Information PagePrepared For: Valued Client

THIS ILLUSTRATION IS NOT COMPLETE WITHOUT ALL NUMBERED PAGESTHIS ILLUSTRATION IS NOT PART OF THE LIFE INSURANCE POLICY OR CONTRACT

MONY Life Insurance Company of America (MLOA)An Arizona Stock Corporation with its main administrative office at 525 Washington Blvd. Jersey City, NJ 07310

Presented by: John Smith, Delivered in ConnecticutPrepared on: January 13, 2017 11:50 AMMale Preferred Non-Tobacco User Age 50Initial Face Amount: $1,000,000Initial Planned Periodic Premium = $8,781.43Premium Mode: Annual, Riders: NLGInitial Death Benefit Option: A (Level)Minimum Initial Premium: $1,982.50GE 114728 (6/16) (Exp. 6/19), BrightLife Protect, Series 155,GPT-04-2.75%-11.0.0.9-$11,190.00-01-06-W

Death Benefit OptionDeath Benefit Option A (level)

Account Values Transfer / Segment MaturityNone

Benefits and Riders Included:NLG - No Lapse Guarantee Rider:Maximum NLG Rider Period: 40 years (subject to NLG Premium requirements).

Applicable Footnotes:Footnotes are illustrated in order of occurrence for each year they are applicable

Guaranteed Values Non-Guaranteed Values Non-Guaranteed Values

Guaranteed Interest Rate Alternative Illustrated Interest Rate Current Illustrated Interest Rate

Year 1 - Footnote(s): E Year 1 - Footnote(s): E Year 1 - Footnote(s): EYear 2 - Footnote(s): E Year 2 - Footnote(s): E Year 2 - Footnote(s): EYear 3 - Footnote(s): E Year 3 - Footnote(s): E Year 3 - Footnote(s): EYear 4 - Footnote(s): E Year 4 - Footnote(s): E Year 4 - Footnote(s): EYear 5 - Footnote(s): E Year 5 - Footnote(s): EYear 6 - Footnote(s): E Year 38 - Footnote(s): EYear 7 - Footnote(s): E Year 39 - Footnote(s): EYear 8 - Footnote(s): E Year 40 - Footnote(s): EYear 9 - Footnote(s): E Year 41 - Footnote(s): T

Year 10 - Footnote(s): EYear 11 - Footnote(s): EYear 12 - Footnote(s): EYear 13 - Footnote(s): EYear 14 - Footnote(s): EYear 15 - Footnote(s): EYear 16 - Footnote(s): EYear 17 - Footnote(s): EYear 18 - Footnote(s): EYear 19 - Footnote(s): EYear 20 - Footnote(s): E

Page 17 of 21

1

32

BrightLife® Protectbasic illustrationflexible premium universal life with an index-linked interest option

Information PagePrepared For: Valued Client

THIS ILLUSTRATION IS NOT COMPLETE WITHOUT ALL NUMBERED PAGESTHIS ILLUSTRATION IS NOT PART OF THE LIFE INSURANCE POLICY OR CONTRACT

MONY Life Insurance Company of America (MLOA)An Arizona Stock Corporation with its main administrative office at 525 Washington Blvd. Jersey City, NJ 07310

Presented by: John Smith, Delivered in ConnecticutPrepared on: January 13, 2017 11:50 AMMale Preferred Non-Tobacco User Age 50Initial Face Amount: $1,000,000Initial Planned Periodic Premium = $8,781.43Premium Mode: Annual, Riders: NLGInitial Death Benefit Option: A (Level)Minimum Initial Premium: $1,982.50GE 114728 (6/16) (Exp. 6/19), BrightLife Protect, Series 155,GPT-04-2.75%-11.0.0.9-$11,190.00-01-06-W

Applicable Footnotes:Footnotes are illustrated in order of occurrence for each year they are applicable

Guaranteed Values Non-Guaranteed Values Non-Guaranteed Values

Guaranteed Interest Rate Alternative Illustrated Interest Rate Current Illustrated Interest Rate

Year 21 - Footnote(s): EYear 22 - Footnote(s): EYear 23 - Footnote(s): EYear 24 - Footnote(s): EYear 25 - Footnote(s): EYear 26 - Footnote(s): EYear 27 - Footnote(s): EYear 28 - Footnote(s): EYear 29 - Footnote(s): EYear 30 - Footnote(s): EYear 31 - Footnote(s): EYear 32 - Footnote(s): EYear 33 - Footnote(s): EYear 34 - Footnote(s): EYear 35 - Footnote(s): EYear 36 - Footnote(s): EYear 37 - Footnote(s): EYear 38 - Footnote(s): EYear 39 - Footnote(s): EYear 40 - Footnote(s): EYear 41 - Footnote(s): T

Explanation of Footnotes Used In This Illustration

E Where zero net policy account value is shown, the policy is being kept in force under the No Lapse Guarantee Rider orLoan Extension Endorsement.

T Based on the assumptions of this illustration, the policy terminates without value. Adverse tax consequences could occur ifa policy with loan is surrendered or permitted to terminate.

Additional Premium Information:Initial 7-Pay Premium: $55,370.00Minimum Initial Premium (MIP): $1,982.50Initial Guideline Single Premium: $257,046.26Initial Guideline Level Annual Premium: $22,336.78Initial Annual 40 year NLG Premium: $7,870.10Definition of Life Insurance: Guideline Premium Test

Business Strategies Services Qualified? NoPolicies issued to a business entity, or for a business-related or business/employer-sponsored purpose qualify for enhanced financial reporting services,at no additional cost, which facilitate support of your plan's administration. Ask your advisor for details.

Page 18 of 21

1

32

BrightLife® Protectbasic illustrationflexible premium universal life with an index-linked interest option

Important Tax InformationPrepared For: Valued Client

THIS ILLUSTRATION IS NOT COMPLETE WITHOUT ALL NUMBERED PAGESTHIS ILLUSTRATION IS NOT PART OF THE LIFE INSURANCE POLICY OR CONTRACT

MONY Life Insurance Company of America (MLOA)An Arizona Stock Corporation with its main administrative office at 525 Washington Blvd. Jersey City, NJ 07310