financial view: a sustainable business model - roche.com · pdf filesolid margins with a high...

TRANSCRIPT

Financial view:A sustainable business model

Alan Hippe, CFO

Capital allocation and R&D

Continuous productivity improvements

Focus on cash generation and allocation

Solid margins with a high risk / high reward model

3Source: Company reports, Roche analysis; 1 Based on average of fiscal years 2009 - 2011 financials; 2 Based on 2010 data

Core operating profit margin (%)1

Branded pharma sales as % of Group2

Pfizer Astra

Sanofi

Merck

GSK

Novartis

Eli Lilly

Bayer

BMS

Amgen

Abbott

R² = 0.6198

15%

25%

35%

45%

30% 40% 50% 60% 70% 80% 90% 100%

The P&L reflects Roche’s innovation based strategy Low on Marketing, General and Administration

4

33%32%

29%29%

29%29%

28%26%

24%24%

23%18%

Eli LillyNovartis

PfizerBayer

MerckGSK

AstraAbbott

BMSSanofiRoche

Amgen

R&D % sales Core operating profit margin% sales

M&D+G&A % sales

21%20%

19%18%

17%16%

15%14%14%

13%10%

8%

Eli LillyAmgenRoche

BMSMerck

NovartisAstra

SanofiGSK

PfizerAbbottBayer

43%

39%

37%

36%

34%

34%

33%

31%

27%

27%

23%

17%

Pfizer

Astra

Amgen

Roche

Sanofi

Merck

BMS

GSK

Novartis

Eli Lilly

Abbott

Bayer

Source: Company reports, Roche analysis; Figures based on fiscal year 2011 financials

Return on R&D: Historically Roche has delivered

51 Incl. recovery of cost of capital, Roche Pharma. Criteria includes: late stage portfolio, risk adjusted revenues, average profitability

assumed, standard erosion curves

Average # NMEs per year

Required performance to breakeven1, at actual R&D expenses (1996-2005)

Actual Launches 2001-2010

CHF 2.1 bn

1.1

Required peak sales per NME(CHF bn)

R&D productivity: Our plans tell us that we will also be delivering in the future

6

Required peak sales per NME(CHF bn)

Required performance to breakeven1, at actual R&D expenses 2011 onwards

Illustrative

Planned launches 2011-2016

1 Incl. recovery of cost of capital at planning exchange rates, Roche Pharma. Criteria includes: late stage portfolio, risk adjusted revenues, average profitability assumed, standard erosion curves

Average # NMEs per year

Roche: R&D well balanced from a risk & disease point of view

7Source: Bernstein Equity Research, Tufts University and Roche analysis

Industry average probability of success – Phase 0 to Registration

Oncology

Virology

CNS

0% 5% 10% 15% 20% 25% 30%

InflammationMetabolism

2012 Roche budget

R&D spend: Balance between short and long term

8

Research/Discovery

Phase 0 Phase 1 Phase 2 Phase 3 Filing Phase 4

R&D spend by phase

~50% ~50%

Invest for the near term

Invest for the future

Note: Based on 2012 budget

Capital allocation and R&D

Continuous productivity improvements

Focus on cash generation and allocation

Base Increasesuccess rate

Reduce timeto market

"Innovation" Reduce costbase

Innovation+ Efficiency

Productivity improvements: Through Innovation AND continuous Efficiency programs

10Source: Nature Reviews (Eric David, Tony Tramontin and Rodney Zemmel (McKinsey & Co.), Vol. 8, 609, Nature Reviews | Drug Discovery), Roche analysis

Innovation Efficiency

Innovation

Efficiency

Base

Illustrative return

Example: Optimise research at pRED

11

Reduce complexity

Nutley

• Increase investment in late stage

• Leverage support functions

Optimise resource allocation

• Reduce infrastructure costs (support functions / site infrastructure)

• Unify sites for ‘non clinical safety and chemistry’

Re-fine infrastructure

• Close R&D centres (Nutley)

• Co-locate managementTCRC

ShanghaiBasel

Welwyn PenzbergSchlieren

Support CentersStrategic sites

35 3647 42 38

16 18

21 23 238 8

11 11 11

0

20

40

60

80

2009 2010 2011 HY 2012before R&D

prioritisation

HY 2012after R&D

prioritisationPhase I Phase II Phase III + Registration

New Molecular Entities

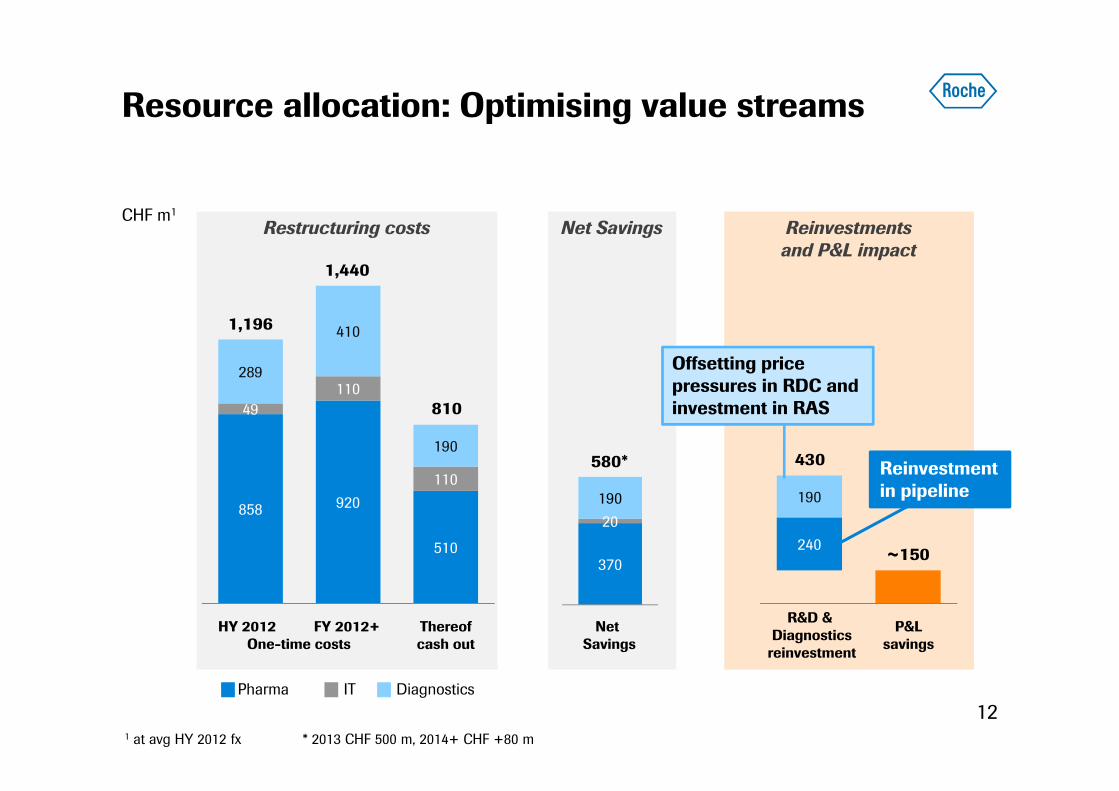

Resource allocation: Optimising value streams

12

Reinvestments and P&L impact

Net SavingsRestructuring costs

858 920

510

49110

110

289

410

190

1,440

810

Thereof cash out

Net Savings

HY 2012 FY 2012+One-time costs

CHF m1

240

190

DiagnosticsPharma IT

R&D & Diagnostics

reinvestment

P&Lsavings

430

~150

1 at avg HY 2012 fx * 2013 CHF 500 m, 2014+ CHF +80 m

370

20190

580*

1,196

Offsetting price pressures in RDC and investment in RAS

Reinvestment in pipeline

Example Development: Productivity initiative in development

13

Roche Genentech Integration

Transactional Outsourcing

Completed efficiency initiatives

-15%

Jan 2010Cost/LIP

2011Cost/LIP

2012Target

Cost/LIP

2015Plan

Ongoing RETHINK D initiativesImprove probability of technical success / reduce risk in trials read outs (ex: use predictive endpoints)

Using modern tools to speed up processes and bring trials closer to patients (ex: collect data directly from patients etc.)

LIP refers to Lifecycle Investment Point

Example: Roche Diabetes Care securing long-term profitability

14

6%4%

2%

2009 2010 2011

Blood GlucoseMonitoring (bGM)

Insulin DeliverySystems

Streamline PortfolioMaximise market uptake

InvestInsulin pumps and CGM

RDC salesGrowth (CER*)

• Restructure and consolidate R&Dorganisation

• "One Global Operations" structure

• Optimise M&D investments

CER=Constant Exchange Rates

Capital allocation and R&D

Continuous productivity improvements

Focus on cash generation and allocation

High operating free cash flow and margin

16

4.81

6.78 6.436.86

7.1721.8%

28.2%26.1%

31.6% 32.0%

HY 2008 HY 2009 HY 2010 HY 2011 HY 2012

Group operating free cash flow (CHF bn) and margin

CER=Constant Exchange Rates

+7% at CER

Managing risks: Accounts receivables in S. Europe

17

Credit Management & Receivables: Managing riskGreece - learning from the past to reduce future risk

18

• Roche experienced strong sales growth trebling in size

• Accounts Receivables (AR) increased too, significantly

• Government had established a pattern of payment every 5 years

AR balance mEUR

• Government issued bonds as payment

• Locally: fast execution to receive bonds ahead of our competitors

• Treasury: anticipated risk and sold into the market

AR balance mEUR AR balance mEUR

History1

• New Credit Policy introduced –Cash on Delivery in Pharma and Dia

• Bonds write down impact 26% however avoided 70% write down experienced by many still holding

Action Impact

1 Situation as of 2010

Credit Management & Receivables: Managing riskSpain – learning from the past to reduce future risk

19

• AR rose significantly with an increase in sales, plus bias of portfolio to hospital sector

• Growing delay of payments from public accounts

• No issues with private accounts

• Escalation of tools used, including

– Individual regional account plans

– Change of commercial policy (CoD)

– Forfaiting (local banks and international funds)

History

• Significant reduction in AR due to “Montoro Plan” (June 2012)

• Focus: avoid future build up

Action Impact

AR balance mEUR AR balance mEURDSO – Public debt

Roche: Favorable risk profile due to sustainable cash flows leading to lower interest expenses

20

0

100

200

300

400

500

600

700

2006 2007 2008 2009 2010 2011 2012

RocheDeutsche BankBNPCitiJPMCredit SuisseUBS

5 year Credit Default Swap (CDS)

Aiming for a sustainable net debt leverage of 0-15%

21

302520151050

Roche

35

S&P rating

Leverage1 (%)

-15 -10 -5-35 -30 -25 -20

TakedaSanofi

Biogen

AZ

Merck

BMSBecton D

NovartisEli Lilly

Pfizer

BayerGilead

Amgen

Abbott

GSK

1 Net Debt / Total Assets (%); 2011 figures for all companies except Roche; Company reports; Bloomberg (June 14; 2012)

2010 (31%)

2011 (25%)

J&J

AA+

AA

AAA

AA-

A+

A

A-

BBB+

BBB

BBB-

BB+

Continuous increase in dividends and pay-out ratio historically

22

0.18 0.20 0.28 0.37 0.48 0.55 0.64 0.75 0.83 0.87 1.00 1.15 1.30 1.451.65

2.00

2.50

3.40

4.605.00

6.00

6.606.80

0%

1%

2%

3%

4%

5%

6%

0

2

4

6

8

'89 '90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11

Pay-out ratio calculated as dividend per share divided by core earnings per share (diluted)

Dividend per share (CHF)

2011Payout ratio

of 55.3%

Dividend yield (%)

Cash

ProfitabilitySalesgrowth

We will continue to show strong commitment to Innovation AND Efficiency

23

Value

Innovation Efficiency