financing food incubators 2008 community food security coalition/foodbin conference carol coren...

TRANSCRIPT

Financing Food Incubators2008 Community Food Security Coalition/FoodBin Conference

Carol Coren Business Association Mentor

Financing is a Function Of Mission and Structure

•Financial Stability relies on multi-sectoral support for a business enabling environment equipped to support food industry entrepreneurs

•Financial Resources will be affected by program and service capacity, capital and the appeal of your vision for the incubator

•Financial Planning must explore a variety of revenue streams that often rely on collaborations and partnerships

2

Food Incubator Mission

Provide a business enabling environment for entrepreneurs involved in a far reaching, lucrative, industry with unrelenting performance and technology requirements

3

Shoals Commercial Culinary Center, ALPhoto: Business Week 2007

Vision and Value Propositions• Support Local

Economic Growth• Create Jobs• Link local entrepre-

neurs to the food industry value chain

• Forge partnerships with public service programs, suppliers , consumers and businesses

4

Artisan Baking Center Kitchen Innovations, NYPhoto: Business Week 2007

5

Performance Benchmarks Attract Support

• Does it deliver a service that the marketplace has failed to provide at affordable prices and acceptable quality.

• Does it play a role as an economic development driver.• Does it serve as a core component of the value chain

that brings foods from farms to forks: locally, regionally, nationally, internationally? How?

Northwest Ohio Cooperative Kitchen, OHPhoto: Business Week, 2007

Financing is A BALANCING ACT

What you do and why you do it

Your ability to do what you do: Direct Services, Technical Support, Equipment Maintenance, Storage, Distribution, Square Footage, etc.

•What you have and how it is distributed:•Assets •Liabilities• Net Assets

Establishing and maintaining a balance among these three critical components is essential to an organization's long-term health and viability.

Incubators Are Social Enterprises

Organization or venture that advances its social mission through entrepreneurial, earned income strategies and operates as a

•For Profit Business

•Non Profit Organization

•Hybrid Organization8La Cocina, CA

Photo: Business Week

9

Do Traditional Business Structures Fit?

IndividuaIndividuall

PartnershipPartnership LLCLLC C-CorpC-Corp Co-opCo-op

controlcontrol OwnerOwner PartnersPartners OwnersOwners ShareholdersShareholders, board & , board & elected elected officersofficers

Members, board Members, board elected from elected from membershipmembership

capitalcapital ownerowner Partners. Liability up Partners. Liability up to value of propertyto value of property

Owners. Owners. Liability Liability limited to limited to investment in investment in businessbusiness

Equity raised Equity raised by selling by selling sharesshares

Equity from Equity from membersmembers

earningearningss

Profits to ownerProfits to owner Shared gain(loss) by Shared gain(loss) by partners, based on partners, based on partnership partnership agreementagreement

Shared by Shared by ownersowners

Gain(loss) Gain(loss) distributed to distributed to shareholders shareholders as dividendsas dividends

Allocated to Allocated to members based members based on business on business done w/co-op in done w/co-op in that yearthat year

taxestaxes Taxed once as Taxed once as income of income of ownerowner

Taxed once as Taxed once as income of partnersincome of partners

Taxed once Taxed once either as either as partnership or partnership or corporationcorporation

Taxed twiceTaxed twice Taxed once: as Taxed once: as income of co-op income of co-op when earned, or when earned, or income of income of members when members when allocatedallocated

lifelife Tied to ownerTied to owner Tied to partnership. Tied to partnership. PerpetualPerpetual Continuing Continuing existenceexistence

PerpetualPerpetual

Hybrid Business Structures• MODELSo New Generation Cooperativeso Limited Private Partnershipso L3Cso Public-Private Partnerships o Tri-Sector Partnership

• BENEFITSo Community Engagemento Flexible Profit Objectives o Financial Advantages for Stakeholders (Taxes,

Subsidies, Markets)o Economies of Scale 10

St. Paul Kitchen, MNPhoto: St. Paul Star Tribune

New Generation Cooperatives• Used primarily for value-added processing of

agricultural commodities • Equity to fund start-up and growth is financed

through the sale of delivery rights: If $20 million is needed for equity capital and the capacity of the facility is 5 million bushels then the price per delivery right share is $4 per share

• Characteristics: 1. delivery rights are contracted and tied to the level of investment 2. membership is limited to those who purchase delivery rights 3. higher levels of equity investment by individual members is required 4. shares that provide delivery rights can be transferred and can fluctuate in

value.

5. Marketing agreements outline duties of both the members and the cooperative toward each other with respect to the delivery, quality, and

quantity of producers’ commodities. . 11

Limited Private Partnerships• Partnership limited to 35 partners • Scale allows avoidance of SEC Registration• Enjoy protections similar to LLCs (limited

partners enjoy protection from liability) • Often have timetable for existence and

dissolve or alter when that timeframe expires• Typically form to invest in real estate, oil and

gas drilling, research and development, equipment leasing, and other businesses.

12

13

: L3C: Low-Profit Limited

Liability Co. THE FOR-PROFIT WITH A NONPROFIT SOUL• Have the liability protection of a corporation, the flexibility of a partnership and the ability to be sold in pieces.

• Bylaws provide mission statement indicating that the enterprise is to further a socially beneficial purpose

• NOT tax-exempt but eligible for a philanthropic Program Related Investment (PRI) loan or infusion of capital

• VT now permits this structure and firms can form thereo L3C is the same as organizing as a LLC with a requirement that the

designation be indicated when the articles of organization are filed and the name of the enterprise declares

o must include the “brand mark” word L3C o www.americansforcommunitydevelopment.org

Public Private Partnerships• Agreement between public agency and a private

sector entity, often regarding the provision of public services or infrastructure.

o Example: Riverside CA Library: City owns buildings and Library Systems and Services, Inc., a Maryland firm operates the system and is responsible for all library employees, except for the county librarian, janitorial service, and landscape maintenance.

o Oregon State University owns OR Food Innovation Center and leases portion of it to the Oregon Department of Agri- culture for labs and testing.

14

Wasco Specialty Kitchen, WA

Public Private Development Partnerships

Potential to Operate As An Economic Development Service ProviderPublic sector entity enters into partnership

with private sector agency to develop a product, to put a new technology to use or develops a service to address problem such as

15

o Need for a health product to treat a disease found only in poor and developing nations

o Need to introduce a new production technology or product such as a “Gatorade”

o Need to advance applications of a security technologies to monitor status of food while it is being shipped.

o Need to transfer technology from a government research lab to the marketplace.

Overbrook Environmental Education Center (OEEC) Kitchen , PA

16

Tri-Sector Partnerships Business entities, nonprofit organizations and

government working together to organize, start and operate programs that put communities at the centre of development, and deliver real and sustainable benefits for all. This model is used throughout the world for development purposes.

Jubilee Project, TN

Myths About Nonprofit Financing

1. Start-up success relies on grant-getting and raising contributions 2. There is a grant for every problem and a program for every need3. Budget transfers can serve in lieu of a

line of credit and be repaid4.Endowment funds are without strings5.Qualified customers are lined up at the

door

Pacific Gateway Center, HI

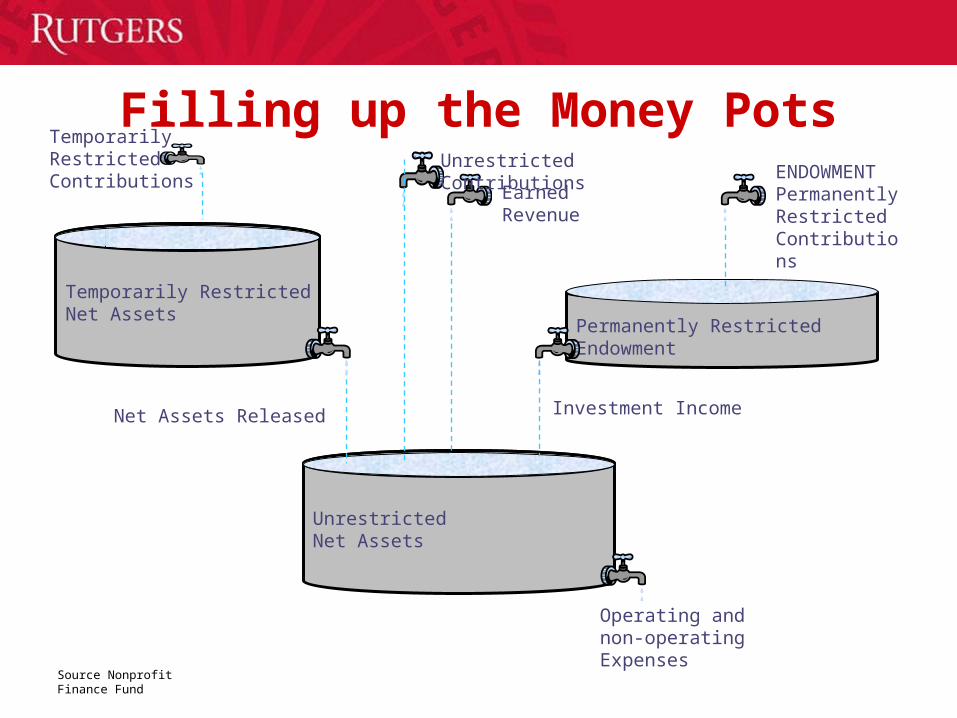

UnrestrictedNet Assets

Financing Incubators Needs Three Full Pots!

Temporarily RestrictedNet Assets Permanently Restricted

Net Assets

Unrestricted Revenue Earned Contributed

Temporary and Restricted Revenue Purpose Timing

Permanent Restricted Revenue

Source Nonprofit Finance Fund

Temp. restricted revenue has met donor-imposed restrictions

Breakdown of Revenue: Earned vs. Contributed

Natural classification of expenses

Determine true Operating Surplus / Deficit

Non-operating revenue segregated and placed “below the operating line”

OPERATING ACTIVITYOperating Revenue

Unrestricted Temporarily Permanent Total

Earned Investment income $7 - - 7 Program Fees & Tickets 410 - - 410 Rental Income 30 Government earned 10 - - 10 Earned operating revenue 457 457

Contributed Individual 248 - - 248 Foundations & Corporations 162 58 - 220 Government 47 - - 47 Special events, net 44 - - 44 Net Assets Released from Restrictions 152 (152) - 0 Contributed operating revenue 653 (94) 559

Total Revenue 1,110 (94) - 1,016

Operating Expenses Personnel 550 - - - Professional Fees 39 - - - Occupancy 90 - - - Interest - - - - Support 490 - - -

Total Expenses 1,169 - - 1,169

Surplus/Deficit Before Depreciation (59) - - (59) Depreciation Expense 93 - -Surplus/Deficit After Depreciation (152) - - (152)

NON-OPERATING ACTIVITIESUnrestricted non-operating revenue/expenses 597 (597) - 0 (e.g. capital campaign receipts/releases)

Net gain (loss) on sale of assets - - - 0

Change In Net Assets 445 (691) 0 (246)

ABC CenterSTATEMENT OF ACTIVITIES (REVISED)

Years ended June 30, 2003($ in Thousands)

Source Nonprofit Finance Fund

20

Statement of Activities Reveals• Revenue Dynamics: Where does the

organization’s money come from? Is it well diversified or at risk? Do revenue streams appear reliable/consistent?

• Cost Dynamics: What levers does the organization have in its control to manage expenses? How hard is it to tighten the belt? Is management responsive to operating changes and prepared to make difficult decisions?

• Profitability & Savings: Does the organization cover its costs? How large are surpluses/deficits relative to revenue? Is the agency saving? If so, is it enough?

La Cocina, Kitchen, CA

CASH FLOWS & INCOME STATEMENT INFLUENCES

BALANCE SHEET

Statement of Activities

EarnedContributed

Revenue

Expenses

PersonnelProfessionalOccupancyInterestSupport

Change in Net Assets

YR 2 Financial Position

Surplus/Deficit Net Assets

Surplus/Deficit Net Assets

LiabilitiesLiabilities

Cash

Assets

Statement of Cash Flows

Cash flows from operating

Cash flows from investing

Cash flows from financing

Beginning Cash

Ending Cash

Surplus/Deficit Net Assets

Surplus/Deficit Net Assets

LiabilitiesLiabilities

Cash

Assets

YR 1 Financial Position

Source Nonprofit Finance Fund

22

Health of Assets: • Is the distribution of assets appropriate, given

the core business? • Is the organization investing in its fixed assets? • How “leveraged” are they? • What is the composition of net assets? • How much is unrestricted and liquid?

Liquidity: • Does the agency have enough cash to cover

current obligations? • How well are they managing receivables? • Are they asking others to “pay the bills?”

Statement of Position Reveals:

UnrestrictedNet Assets

Filling up the Money PotsTemporarily Restricted Contributions

Temporarily RestrictedNet Assets

Net Assets Released

Permanently RestrictedEndowment

Investment Income

Earned Revenue

Unrestricted Contributions

Operating and non-operating Expenses

ENDOWMENT Permanently Restricted Contributions

Source Nonprofit Finance Fund

24

1. Run Leaner and Make Money2. Grow3. Launch an earned income venture4. Liquidate Assets5. Build an endowment 6. If your purpose is to spin off

businesses, devise a way to capitalize from your clients’ success for a Reserve Fund

Financial Instability Solutions:Ways to Fill the Money Pots

25

Ways Your Incubator Might Grow

Transformative Organic None Negative

• Presumably no change in business model

• The most predictable option (and least likely to fail)

• Still requires planning and environmental changes affect business results

• Change in business model is incremental, if at all

• Funded with surpluses, debt

• No “golden rule,” but seldom greater than 10-15% sustained annual rate

• May or may not change business model

• Often the hardest to manage, as old cost structure becomes obsolete

• Financial implications are not as obvious as one might think

• Changes the way you conduct business

• Typically requires

outside/one-time source of funding/financing

• May or may not represent large percentage growth

Source Nonprofit Finance Fund

26

Liquidation is Easier Than It Sounds

• Incubator’s commitment to property and equipment is integral to program delivery

• Being a landlord of sorts is one of your businesses: perhaps you should treat it as a subsidiary. Then If something breaks, the landlord that you established for this purpose can fix it.

• Reserves restricted for ongoing maintenance and replacements might cause complications if the building or equipment is gone.

Former Nuestra Culinary Ventures, MAPhoto: Erik Jensen for Boston Globe

27

• The return on investment involved in raising an endowment might not be as great as the return from other fundraising efforts

oA sizable endowment is required to yield significant interest and dividends

o $1 million principal @ 5% will yield $50,000 per year (gross)

• Building and managing endowments can take energy away from mission and programs

• An unrestricted INVESTMENT FUND might provide greater flexibility and not demand the management reporting and diligence that an endowment gift requires

Are Endowment Funds A Safety Net?

Board and Staff Commitments to Financing

• Review the fundamental concepts and structure of nonprofit financial statements

• Understand how to analyze this information for your own organization

• Present and Explain your financial information to your staff, constituents, board and potential funders

• Find and implement ways to generate recurring revenue from your intellectual property investment in your clients and your communities

28Kitchen Incubator (Kitchen Inc.), TX

29

For Further Information

• Contact Information:Lou Cooperhouse, DirectorDiane Holtaway, Associate Director, Business

DevelopmentCarol Coren, Business Association Mentor

• PH: 856-459-1900• 450 E. Broad Street Bridgeton, NJ 08302• foodinnovation.rutgers.edu