fintech’s growing influence on financial services - … · fintech’s growing influence on...

TRANSCRIPT

Global FinTech Report 2017: India insights

67% believe that FinTech poses a substantial risk to their business

95% of incumbents in the financial services industry seek to explore FinTech partnerships

29% expected annual RoI on FinTech-related projects

Redrawing the lines FinTech’s growing influence on financial services

pwc.in/fintechreport

Introduction

FinTech and financial services are coming together

Key emerging technologies are enabling convergence

Managing expectations will be key

Conclusion

Participant profile

Contacts

Contents Key Messages

67% of incumbents are increasingly concerned they are losing revenue to innovators

84% of financial institutions plan to increase internal efforts to innovate

95% expect to increase FinTech partnerships in the next three to five years

More than 60% believe business is at risk

Financial institutions are embracing the disruptive nature of FinTech

Financial institutions are learning to partner and integrate

FinTech and financial services are competing less and coming together

36% of large financial institutions are investing in artificial intelligence)

56% seek to engage with blockchain in some form and eventually make it a part of their core business

51% see new business models as a regulatory barrier to innovation

Investment in enabling technologies will help narrow the gap

Blockchain to move into the mainstream Regulations trigger disruption and innovation

Key emerging technologies are enabling convergence

29% expected RoI on FinTech-related projects

The only way to get returns is to invest to learn

Managing expectations will be key

3

14

4

9

16

15

19

India FinTech Survey 3

IntroductionThe pace of change in financial services seems only to be increasing—as does the urge for the industry to react. The forces shaping this change have led us to reconsider the role of finance, more as an ‘enabler’ than a provider of financial products and services. Mobile money services have proved to be an effective gateway for financial inclusion among the unbanked, a demographic that could evolve into a multi-billion dollar payments volume opportunity. Tomorrow, your bankers or wealth managers will coach you throughout your day to take appropriate financial decisions based on a combination of artificial intelligence (AI) and transaction and contextual data. Frustration and cost will decrease as new business models and emerging technologies are being adopted to streamline on-boarding processes, operations and client communication. The influence that FinTech is having on the market is growing and the long-term potential is even greater.

The FinTech market landscape in India has been dominated by payments and lending companies so far, although other segments, particularly personal finance and enterprise solutions, are poised to gain ground this year. The role of the regulatory bodies in this journey has been crucial. Initiatives like India Stack and National Payments Corporation of India (NPCI) have provided impetus to the FinTech revolution in the nation. Mainstream financial institutions in the country are also rapidly embracing the disruptive nature of FinTech and forging partnerships in an effort to expand their portfolio of services, be able to offer more customer-centric products, and also sharpen operational efficiency and respond to customer demands for more innovative services. Even FinTech funding is moving from a venture capitalist dominated field towards more mainstream investments. Cutting-edge FinTech companies and financial innovation are changing the competitive landscape, and are redrawing the lines of the financial services industry.

This report assesses the continued rise of new business models and emerging technologies in the financial services sector. Our analysis is based on a nationwide survey of 45 Indian financial services and FinTech executives, mapped against a global survey of 1,308 participants from 71 countries, and also includes insights and proprietary data from PwC’s DeNovo platform.

We design our services with a deep focus on our customers and their needs. We believe that disruption is the norm now, and are preparing ourselves for the future. To be able to do so, we monitor FinTech activity closely and embrace innovation from the outside-in

CIO of an Indian retail bank

4 PwC

FinTech and financial services are coming together

FinTech has evolved from start-ups that want to take on and compete with incumbents to a broader ecosystem of different businesses that are, in many cases, looking for partnerships. FinTech start-ups don’t just need capital, they need customers. At the same time, incumbents need new approaches to drive change and deliver innovation.

Our survey also highlights how innovation is coming from outside financial services and being driven by a variety of sources, including tech companies, e-retailers and social media platforms (see Figure 1). While the new partnering approach offers alternative strategies for both new entrants and start-ups, it also carries with it a new set of risks, which we will explore later in this report.

In India, though FinTech start-ups are still viewed as the major drivers of disruption, other players like social/Internet platforms and e-tailers are also driving innovation and the adoption of non-traditional financial services.

The exploding ecosystem

Startups are seen as the maindisruptors, but many have shiftedto B2B models and providingplatforms for Financial Institutions

Social media/Internet platformsare further entrenching their placeas disruptors by leveraging theirlarge client reach to provide newchannels for customer service ndbusiness models

ICT and large tech companiesare also seen as potentially largedisruptors to the FS sector, as theyare able to innovate at a far fasterpace than incumbents

E-retailers are likely to be disruptive by using their large data sets to provide consumer-focused products and services

Financial infrastructure companies should be concerned as more Financial Institutions turn to FinTech infrastructure providers,but they may be seen asenablers of innovation

Traditional Financial

Institutions

E-retailers

Financial infrastructure

companies

Startups

ICT and large tech companies

Social media/Internet platforms

Traditional Financial Institutions need to be the most concerned as they are not seen as a disruptive force, but they are best able toleverage FinTech innovation

Figure 1: Which entities are likely to be the most disruptive in the next five years?

IndiaGlobal

33% 41%

51% 43%

33% 50%

60% 55%

87% 75%

22% 28%

1

FinTech to us is really about the interplay between different players in the ecosystem and how they work together to disrupt the financial services industry.

The power of FinTech lies in collaboration.

Vivek Belgavi India FinTech Leader and Partner, PwC India

India FinTech Survey 5

More than 60% believe business is at riskConsumers are increasingly getting attracted to non-traditional financial service providers, starting with payments and funds transfers. Personal finance and loans are the next avenues that are ripe for disruption in India.

The industry incumbents are privy to this trend and 67% (see Figure 2) of them acknowledge that non-traditional FinTechs pose a threat to their businesses. However, this number is slightly lower than the global average of 80% (see Figure 3)—perhaps an indication that the market in India is not yet as mature as it is globally, particularly in the non-payments segments.

Figure 3: What financial activities do you believe your customers already conduct with FinTech companies?

79%

50%42%

21% 21% 21%

33%

8%

17%

68%60%

56%49%

38% 38%

26%

8% 8%

Payments

96%

84%

IndiaGlobal

Funds transfer

Personal finance

Personalloans

Traditional deposits / savings accounts

Insurance Wealth management

Student loans

Mortgage loans

Other

Innovation is happening outside of the organisation, with emergent technologies being leveraged by start-ups, and if financial institutions want to speed up their innovation they need to significantly increase their collaboration with FinTech companies.

Manoj Kashyap Global FinTech Leader and Partner, PwC US

India

Figure 2: Do you believe that part of your business is at risk of being lost to standalone FinTech companies within the next five years?

(percentages shown correspond to ‘Yes’)

2016 2017

88%

88%

89%82%

93%95%

80%

NA

88%83%

83%

91%

Europe

GlobalNorth America

Latin America

Africa

Asia

69%

67%

6 PwC

Financial institutions are embracing disruption and upping their innovation game

In response to the threat posed by FinTech, financial institutions are rising to the challenge and driving innovation from within. They are putting disruption at the heart of their strategy, as is evident from the fact that 84% of respondents agree with this statement in India. By becoming self-disruptors, financial institutions seek to appropriately respond to innovations and thereby empower their customers on a daily basis. To address customer retention in the context of new ‘FinTech competition’, financial institutions will want to focus on developing faster services, intuitive product design, ease of use and 24/7 accessibility (see Figure 4).

Financial institutions will also need to disrupt their own operations or processes, which will introduce culture and mind-set challenges. In India, 84% of respondents expect to increase internal innovation efforts over the next three to five years, as compared to 77% globally (see Figure 5). This can occur in a variety of ways, including adopting newer technologies such as AI or blockchain, or changing the cultural environment to one that fosters innovation.

Figure 4: What changes do you expect to see in your internal innovation efforts over the next three to five years?

75%

77%

78%

79%

89%

89%

84%

77%

22%

19%

20%

18%

8%

11%

16%

20%

3%

4%

2%

3%

3%

0%

0%

3%

Europe

Asia

North America

Latin America

Oceania

Africa

India

Global

IncreaseStay the sameDecrease

Figure 5: What do you think are the most important areas to address customer retention in the context of new FinTech competition?

Global Payments

1st 2nd 3rd

Banking

Insurance

Asset & Wealth Management

Payments

Banking

Insurance

Asset & Wealth Management

Ease of use, intuitive product design

Ease of use, intuitive product design

Ease of use, intuitive product design

Ease of use, intuitive product design

Faster service

Superior customerservice

Superior customerservice

Cost

24/7accessibility

Faster service

24/7accessibility

24/7accessibility

24/7accessibility

India1st 2nd 3rd

Ease of use, intuitive product design

Ease of use, intuitive product design

Ease of use, intuitive product design

Ease of use, intuitive product design

Faster service

Faster service

24/7accessibility

24/7accessibility

24/7accessibility

Cost

Superior customerservice

PwC has helped an upcoming Indian retail bank to develop its core architecture from the ground up in a modular form while maintaining a sharp focus on customer needs and intuitive product design. This architecture enables the bank to remain agile by testing innovative solutions and adopting them quickly.

Case in point:

India FinTech Survey 7

Financial institutions are learning to partner

FinTech companies create an ecosystem that fosters innovation and enables the democratisation of financial services, bringing in a more data- and customer-focused way of business. Financial institutions have realised the importance of these ecosystems and are attempting to engage with FinTechs and cultivate innovation within their companies.

Adopting effective growth strategies and integrating with FinTech will be essential to partner for innovation. Partnerships with FinTech companies in India are expected to go up from 42% in 2016 to 95% this year on average. This is by far the highest percentage reported across all nations in our global survey (see Figure 6). This clearly elucidates that FinTech is at an inflection point in India and we shall see the ecosystem explode this year.

Globally, a slightly lower majority of participants—82% on average—expect to increase partnerships with FinTech companies over the next three to five years. Partnering with innovators will allow incumbents to outsource part of their R&D and bring solutions to market quickly. FinTech companies also benefit from these partnerships. As they develop new theories and models, in order to test them, they need access to large data sets that incumbents already have. Partnering also gives them access to an existing and large customer base. This is further emphasised by FinTech segments that are starting to transition from purely B2C to B2B. For example, lending through alternative credit decisioning and robo-advisory products, which were initially offered as consumer-facing products, have now begun to be repositioned as integrated platforms within incumbent financial institutions in order to cater to their larger installed client base.

India

Figure 6: Current and expected partnerships per country

Percentage of respondents expecting to increase partnerships over the next three to five years

Percentage of respondents currently engaging in partnerships with FinTech companies

78%81%85% 83%

96%

88%

100%

89%82%

94%

74%

88%

68%

83%90%

82%

64%

81%

74%

95%

83%84%

68%71%

82% 81%81%

72%

91%93%

76%76%

14%

22%25%30%30%31%

36%37%40%40%41%42%42%43%44%44%45%45%50%

52%53%54%55%59%62%62%62%63%64%65%69%

70%

Ger

man

y

Bel

gium

Net

herla

nds

Aus

tral

ia &

New

Zea

land

Sou

th A

fric

a

Can

ada

Finl

and

Sin

gap

ore

Sw

itzer

land

Ind

ones

ia

Rus

sia

Uni

ted

Sta

tes

Taiw

an

Arg

entin

a

Fran

ce

Glo

bal

Pol

and

Uni

ted

kin

gdom

Hun

gary

Ind

ia

Luxe

mb

ourg

Italy

Chi

na m

ainl

and

Irela

nd

Hon

g K

ong

SA

R

Den

mar

k

Mex

ico

Bra

zil

Jap

an

Col

omb

ia

Turk

ey

Sou

th K

orea

Through its proprietary framework for driving innovation, known as the Innovation Management Office, PwC is helping two of its clients drive innovation and growth by helping them identify, partner and co-innovate with FinTech start-ups.

Case in point:

We believe there is immense potential in partnering with FinTech companies. Truly path-breaking ideas can be nurtured through co-working with FinTech start-ups.

Strategy head of an Asian investment bank

8 PwC

…and learning to integrate

Integration will not come easily. There are a host of cultural, technical, operational and regulatory factors that pose challenges to FinTech companies and incumbents.

Differences in business models, management and culture, regulatory uncertainty and security are the prominent challenges that both parties face when they seek to work together (see Figure 7). Financial services incumbents typically face challenges due to legacy systems and compatibility, combined with the adaption of a more innovation-focused culture. Traditionally, the industry has laboured behind a system of checks and balances that can dampen the innovation process. Emerging FinTech companies are generally nimble and are able to adapt quickly due to technology advantages and lack of bureaucracy.

Workplace culture will play a very important role in the coming years and traditional financial services players need to renew their purpose and brand to align with changing expectations in strategic areas such as career path, diversity, flexibility and delivering social value. By implementing a new cultural mind-set, companies will be able to find alternative talent sources that will help drive innovation and make working with FinTech companies less challenging.

Figure 7: When working with financial institutions (or FinTech companies), what challenges do you face?

Challenges faced by incumbents

Challenges faced by FinTech

Other

IT security

Regulatory uncertainty

Differences in management and culture

Differences in business models

IT compatibility

Differences in operational processes

Differences in knowledge/skills

Required financial investments

Other

IT security

Regulatory uncertainty

Differences in management and culture

Differences in business models

IT compatibility

Differences in operational processes

Differences in knowledge/skills

Required financial investments

India

Global

India

Global

58%

54%

40%

40%

34%

37%24%

24%16%

17%21%

3%16%

28%50%

40%39%

34%

36%

33%11%

11%

5%6%

16%

22%

61%

55%

48%44%

16%

47%

32%

42%

37%

For a start-up, it takes very little time to adapt to new circumstances and make changes accordingly. We can work with banks and other traditional financial services companies to help them along their innovation journey. But working with such incumbents is often fraught with challenges, which can range from culture and technology incompatibility to compliance roadblocks.

CEO of an Indian FinTech company

India FinTech Survey 9

FinTech companies are changing the market dynamics by focusing on emergent technologies that have the potential to provide a renewed experience to their customers. As incumbents begin to realise these changes and adapt themselves to the changing dynamics by focusing on these emergent technologies, they will move closer to FinTech, utilise the technologies and respond swiftly to the changing environment and regulations, and ultimately provide a superior experience to their customers.

Investment in enabling technologies will help narrow the gap

FinTech investments in India closely mirror the global scenario. Most incumbents in the industry are focused on data and analytics and mobile and AI technologies (see Figure 8) because, so far, many of them have found it difficult to manage their data and offer customer-centric and insights-driven digital services. However, developments around emergent technologies like chatbots, natural language searches and digital KYC can enable them to enhance and expand their portfolio of services.

Apart from the adoption of solutions that are focused on providing improved client service, there will be a focus on improving efficiency, reducing costs, increasing security and making processes more agile. Cyber security, robotic process automation, biometric identity and blockchain are poised to be the next wave of emerging technologies.

Developments in IoT can be beneficial to financial services too, especially for the insurance sector, which has traditionally been lagging behind in terms of innovation but is ripe for disruption in India. IoT companies like manufacturers of drones and wearables can bring in interesting data partnership propositions which can be leveraged by insurers for augmenting their underwriting and claims processes.

Emerging technologies are enabling convergence

2Figure 8: What are the most relevant technologies for your business that you plan

to invest in within the next 12 months?

5%

14%

21%

21%

21%

24%

26%

36%

55%

69%

4%

14%

14%

20%

21%

30%

32%

34%

51%

74%

Other

Public cloud infrastructure

Internet of things (IoT)

Distributed ledger technologies (e.g. “blockchain”)

Biometrics and identity management

Robotics process automation

Cyber-security

Artificial intelligence

Mobile

Data analytics

Global

India

PwC is working with a couple of IT clients to implement an intelligent chatbot platform for conversational business intelligence (BI). The chatbots will enable the management at both firms to query in natural language and obtain real-time business insights from their data. Over time, the bot will start predicting client information requirements and deliver information without being prompted to.

Case in point:

10 PwC

Innovation trends under industry focus

To help industry players navigate the market, we have identified the main trends in the asset and wealth management, banking, insurance, and transactions and payments services industries over the next five years.

A common thread that emerges across the different industry sectors is the proliferation of data and digital solutions for better customer engagement and increase in straight-through processing. Even in traditionally human relationship driven businesses like corporate banking and wealth management, financial institutions and their customers are gradually opening up to the idea of interacting digitally at least for certain processes and at certain stages of their business journey. Total automation of the customer journey is, of course, difficult. Therefore, a hybrid model of service delivery through human-centric but robo-assisted relationship management is the middle ground that most financial institutions are seeking.

Asset and wealth management

Asset and wealth managers (AWMs) have traditionally been complacent about disruption in their industry even though they recognise that about 40% of their businesses are at risk due to FinTech disruption. Nevertheless, AWMs are not too keen on innovation and some are content to focus on big-ticket business segments as they foresee these as being continued to be driven through human relationships in the future.

AWMs are more receptive to short-term initiatives and investing in technologies that improve their operational efficiency, research tools and analytical abilities.

With the FinTech mind-set is in its infancy in the asset and wealth management industry, achieving the expected RoI will be challenging. This is especially true as AMWs are not taking transformation growth seriously enough.

A key development in this industry is the advent of robo-advisors which enable the provision of such services to small- to medium-ticket investors as well and to a gamut of new investors in the retail segment.

Figure 9: Trends in financial services ranked by importance and likelihood to respond

Likelihood to respond to the trend

Very LikelySlightly likelyMod

erat

ely

imp

orta

ntVe

ry

imp

orta

nt

Leve

l of i

mp

orta

nce

* Also the most relevant trend in Banking** Also a relevant trend for Asset and Wealth Management

123

45

6

8

9

10

71112

Transactions and payments services1. Increase in digital solutions that firms can integrate to

improve operations2. Emergence of new services and solutions for

un(der)served customers3. Enhanced credit underwriting using non-traditional metrics

to determine applicant creditworthiness

Banking4. Increase in use of consumer data to improve value-added

service offerings5. Rise and adoption of next-generation point of sale solutions6. Use of advanced methods, tools and technologies to

improve information security and predict, detect andanalyse fraud

Insurance7. Increased sophistication of data models and analytics to

better identify and quantify risks8. Increased sophistication in methods to reach, engage and

serve customers in a highly targeted manner 9. Rise of aggregators to compare products and services from

different providers

Asset and wealth management10. Increased innovation in research tools and analytical

capabilities to enable better investment decision making11. Increase in digital solutions that firms can integrate to

improve operations12. Shift from technology-enabled human relationships to

digital experiences with human support

India FinTech Survey 11

Banking

Consumer banking will continue to be the epicentre of disruption for the next few years, according to 78% of respondents in our survey. Most of them also see personal loans and personal finance as the businesses most likely at risk of being lost to FinTechs. To address this trend and retain customers, there has to be a renewed focus on intuitive product design, 24/7 availability and faster services.

Interestingly, most banks, even those focused on corporate and investment banking, are looking to partner with FinTech companies to discover avenues to expand their businesses, improve customer service and processes, or cut costs through automation.

In consumer banking, two notable emerging trends that many banks are experimenting with are the enhancement of credit underwriting through alternative data and the enablement of personal finance services through white-labelled applications.

Insurance

Insurance companies (life and non-life) are accelerating their efforts to keep pace with the trends that are reshaping financial services. Insurers are traditionally known to be the most inhibited in terms of innovation, especially in India, with a majority of them still highly dependent on legacy systems and processes. This makes them prime targets for disruption across the entire value chain, right from lead generation and on-boarding to underwriting and claims processing.

Insurers predict that 30% of their businesses may be at risk from FinTechs. This includes not just the core business but also the way business is conducted. Most insurance companies are actively engaged in garnering business through partnerships and marketplaces.

There are two key avenues that insurers are keen to focus on through increasingly sophisticated data models. The first is better identification and quantification of risk and subsequently augmenting underwriting and claims processing, and the second is increased sophistication in reaching out to customers in a targeted manner.

Transactions and payments services

Payments and funds transfer are the areas which are the most disrupted, with 96% of respondents from the payments industry and 79% from the funds transfer industry saying that customers are already using the services of FinTech companies.

However, only 65% of payments and funds transfer companies are concerned about more business moving to FinTechs. This is perhaps because incumbents are now seeing such FinTechs more as partners rather than competitors. Even FinTechs are realising the potential for partnerships and are investing in building up their data platforms through which they can partner with financial services incumbents and provide additional services to their customers.

Payments companies are the most mature in the FinTech world right now, with a few behemoths utilising their scale to expand and provide a novel portfolio of services to their customers—most importantly e-retailing.

12 PwC

Blockchain to move into the mainstream

While blockchain was discovered by the financial services industry due to the advent of bitcoins, the potential of this technology is being explored by various other industries, including energy, telecom and pharma. From being spoken about in hushed tones to now being implemented in core processes, blockchain has transitioned from hype to reality. The process is still underway but as the understanding of the technology increases, blockchain will enter the mainstream and be adopted on a greater scale. In fact, according to PwC’s DeNovo platform, 32 new blockchain companies were founded in India in 2016, as against just 23 in the preceding years.

As blockchain becomes a part of their strategy, more CXOs will become familiar with it. Currently, only 17% of our respondents state that they are very or extremely familiar with it. Therefore, learning is key in this space. Due to the varied degree of understanding of the technology, we will see it being adopted in various time frames and ways across sectors. With the large back-office cost savings and transparency gains that blockchain can provide from a regulatory and audit perspective that blockchain can provide, it is imperative that respondents understand its potential impact on their activities.

Nevertheless, the adoption of blockchain in businesses will not occur overnight. Although 56% of respondents in India state that blockchain is part of their innovation strategy, not many have begun to implement it as part of their core business. There have been sporadic experiments in the form of proofs of concept (PoCs) for specific use cases by large banks. At the end of 2016, a big Indian private bank partnered with a foreign entity to execute India’s first banking transaction on blockchain for trade financing and executing cross-border transactions instantaneously. This move highlights the benefits of using technology that can eliminate unforeseen charges, delays and processing mistakes. 2017 might be the year when blockchain is widely incorporated into core processes.

The most likely use cases for blockchain, as reported by our respondents (see Figure 10), are funds transfer (50%), digital identity (47%) and payments infrastructure (41%).

India

Figure 10: What business use cases do you most likely see blockchain technology useful for?

12%

0%

22%

19%

25%

19%

22%

34%

47%

50%

41%

11%

3%

14%

17%

24%

25%

26%

36%

46%

50%

55%

Do not know

Other

Syndication in lending

Insurance

Securitization

Trade finance

Regulatory compliance and audit

Post trade settlement

Digital identity management

Funds transfer infrastructure

Payment infrastructure

Global

56%seek to engage with

blockchain in some form and eventually make it a part of

their core businessPwC recently executed a PoC for blockchain-based peer-to-peer domestic remittances for an Indian consumer bank. The implementation enables instant transfers between any two nodes in the bank’s network.

Case in point:

India FinTech Survey 13

Regulations trigger disruption and innovation

The term ‘RegTech’ has emerged to characterise innovation and emerging tech focused on solving complex regulatory challenges, enabling smarter regulation, and reducing complexity in existing regulation and compliance. Many competencies can serve in this area, including automation, data and analytics, machine learning and AI, blockchain and cyber security.

Historically, regulation has been viewed as a barrier to entry into financial services. The requirements were complex, burdensome and difficult for small and new organisations to adopt. Now we see the reverse. Many incumbents are hampered by complex processes and governance they have built up around risk and regulation, and many have also developed a significant degree of risk aversion given some of the headline-grabbing issues of the last decade. It’s not surprising, therefore, to find innovation influencing this area.

Regulatory hurdles can cost the world’s largest banks up to 4 billion USD per annum. In line with this, survey respondents in India indicate that regulations on anti-money laundering/know your customer (AML/KYC), digital identity authentication and data storage, privacy and protection are strong barriers to innovation (see Figure 11). This is in keeping with the global trend, although interestingly, in India, regulations around new business models like crowdfunding and peer-to-peer lending were the highest rated barriers. This finding suggests that the Indian regulatory space is perhaps not as mature as that in other global financial hubs. Also, rather than the presence, it is the absence of regulations for new upcoming business models that creates uncertainty and hence dampens innovation.

Regulators are also looking at ways to leverage new technology and analytics to better manage systemic risk and large amounts of data. By accumulating large amounts of data, they are able to analyse and assess the market and develop a landscape for innovation while ensuring that they evolve. The use of blockchain is also a specific area of interest for regulators given the native ‘regulatory capabilities’ that are embedded in the technology. Transactions can be validated on the fly rather than monitored by intermediaries after the fact. We are going to see the deployment of increasingly sophisticated technology that can monitor, capture and analyse a broad set of data, behaviours, and activity. These are likely to ultimately provide a more comprehensive and efficient approach to regulation and risk management, although there may be some speed bumps along the way.

Figure 11: In which areas do you see regulatory barriers to innovation in FinTech?

51%49%

47%

40%

28%

21%

14%

0%

40%

48%50%

54%

30%

24%

17%

3%

New business model

(crowdfunding, peer-to-peer

lending)

OtherCustomer communication

Use of new technology

E-money/Cryptocurrency

Data storage, privacy and protection

Digital identity authentication

AML/KYC

India

Global

Numerous start-ups have been trying to tackle problems and provide efficient solutions related to centralised KYC, cryptocurrencies and peer-to-peer lending in India. However, due to the absence of clear regulations, these companies are uncertain about the validity and efficacy of their business models.

Case in point:

14 PwC

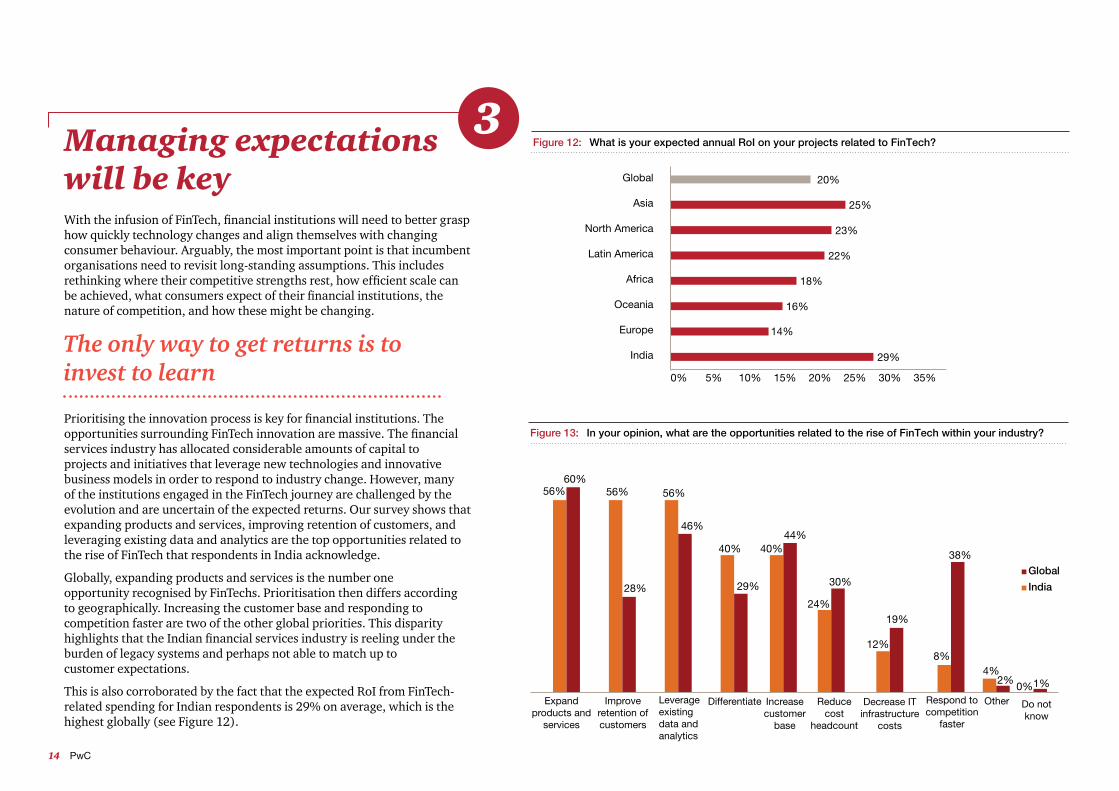

Managing expectations will be keyWith the infusion of FinTech, financial institutions will need to better grasp how quickly technology changes and align themselves with changing consumer behaviour. Arguably, the most important point is that incumbent organisations need to revisit long-standing assumptions. This includes rethinking where their competitive strengths rest, how efficient scale can be achieved, what consumers expect of their financial institutions, the nature of competition, and how these might be changing.

Prioritising the innovation process is key for financial institutions. The opportunities surrounding FinTech innovation are massive. The financial services industry has allocated considerable amounts of capital to projects and initiatives that leverage new technologies and innovative business models in order to respond to industry change. However, many of the institutions engaged in the FinTech journey are challenged by the evolution and are uncertain of the expected returns. Our survey shows that expanding products and services, improving retention of customers, and leveraging existing data and analytics are the top opportunities related to the rise of FinTech that respondents in India acknowledge.

Globally, expanding products and services is the number one opportunity recognised by FinTechs. Prioritisation then differs according to geographically. Increasing the customer base and responding to competition faster are two of the other global priorities. This disparity highlights that the Indian financial services industry is reeling under the burden of legacy systems and perhaps not able to match up to customer expectations.

This is also corroborated by the fact that the expected RoI from FinTech-related spending for Indian respondents is 29% on average, which is the highest globally (see Figure 12).

The only way to get returns is to invest to learn

3

56% 56% 56%

40% 40%

24%

12%8%

4%

0%

60%

28%

46%

29%

44%

30%

19%

38%

2% 1%

Figure 13: In your opinion, what are the opportunities related to the rise of FinTech within your industry?

India

Global

Reduce cost

headcount

Do not know

Respond tocompetition

faster

Increase customer

base

OtherExpand products and

services

Improve retention of customers

Leverage existing data and analytics

Differentiate Decrease IT infrastructure

costs

Figure 12: What is your expected annual RoI on your projects related to FinTech?

29%

14%

16%

18%

22%

23%

25%

20%

0% 5% 10% 15% 20% 25% 30% 35%

India

Europe

Oceania

Africa

Latin America

North America

Asia

Global

India FinTech Survey 15

Conclusion: Innovation aligned with objectivesThe financial services industry will be unrecognisable in five years. The innovators of today will not necessarily be the innovators of tomorrow. As younger generations enter the market, they will expect the same level of service and innovation that they get from the American GAFA (Google, Apple, Facebook and Amazon) or Asian BATX (Baidu, Alibaba, Tencent or Xiaomi) companies. The question that companies then need to ask themselves is: What can I do to ensure that I am not caught at the back of the pack?

To remain at the centre of the financial services industry in the future, your innovation journey should be part of an overall strategic agenda and align with all your company’s objectives. While navigating through regulatory compliance, legacy IT issues, cyber security or talent retention risks, innovation needs to be embedded in all aspects rather than being treated as a separate initiative. A focus on the following six factors will help you solidify your approach to innovation:

• Evaluate emerging technologies Companies need to take a new approach to evaluating the technology coming from innovators. Only by having a team dedicated to monitoring the new technologies globally will companies truly be able to understand their potential for disruption.

• Take a partnership perspective Partnering implies a coming together of skills and talents and learning from each other. However, companies need to ensure that whoever they partner with, be it a tech company or financial institution, is a good fit.

• Integrate to innovate Legacy systems need to be updated to be able to adapt to future environments and innovate. Incumbents should make use of modern cloud-based or open source systems utilised by FinTech companies, and they should work together to integrate new technologies in already existing architecture.

• Create an IT culture that will support innovation Changing an IT culture from one that inhibits innovation to one that is agile and modern will ensure that processes are smooth and new products and services are developed more seamlessly.

• Concentrate on the customer’s voice and shift thinking to outside in Companies need to listen to the customer’s voice. By analysing data from a variety of sources to ensure that they are focused, they will be able to design and develop new products and adapt older ones to be customer-centric.

• Foster a company culture that supports talent and innovation A culture that supports innovation in-house will attract the right talent. Having the right skill sets needed to further innovation will ensure that companies are not caught on the back foot and fall behind.

By focusing on these factors, companies will be able to fully leverage the current and future ecosystems that are being created by innovators. The future financial services industry will be customer-centric, technologically up-to-date, and supportive of internal and external innovation efforts.

16 PwC

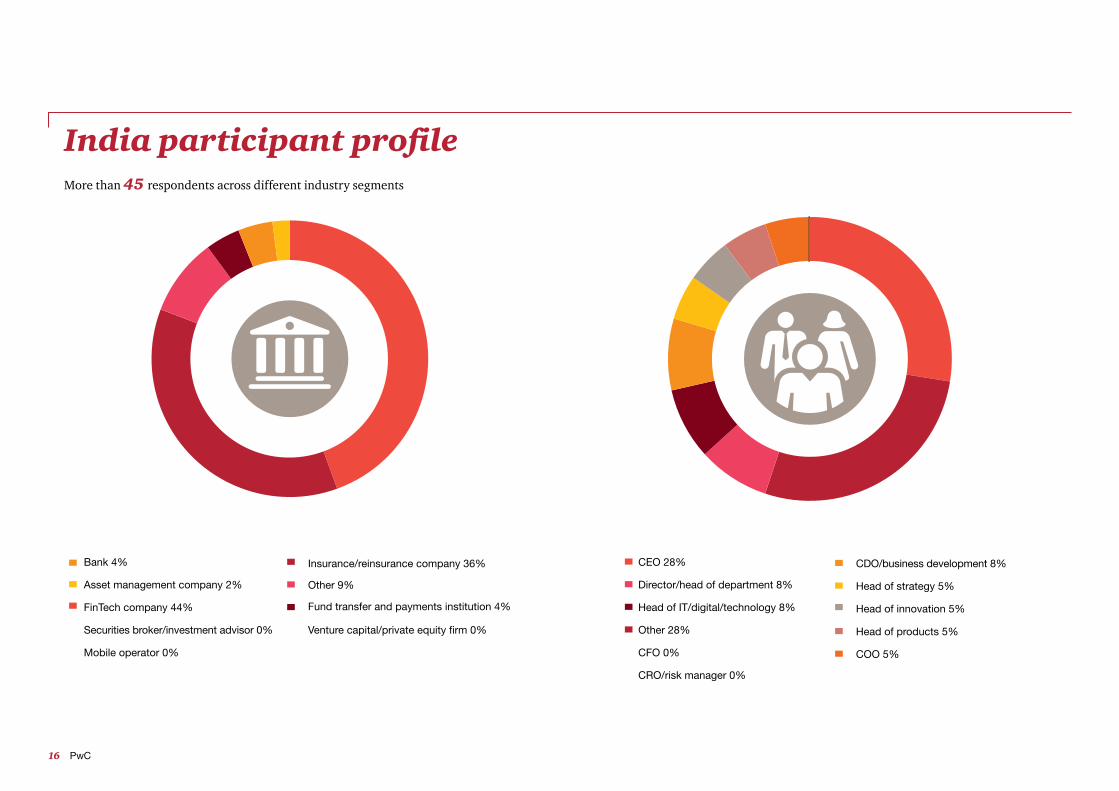

India participant profileMore than 45 respondents across different industry segments

Bank 4%

Asset management company 2%

FinTech company 44%

Insurance/reinsurance company 36%

Fund transfer and payments institution 4%

Other 9%

CRO/risk manager 0%

CEO 28%

Director/head of department 8%

Head of IT/digital/technology 8%

Other 28%

CFO 0%

CDO/business development 8%

Head of innovation 5%

Head of products 5%

COO 5%

Head of strategy 5%

Securities broker/investment advisor 0% Venture capital/private equity firm 0%

Mobile operator 0%

India FinTech Survey 17

Contacts

Vivek Belgavi Partner and India FinTech Leader [email protected]

Mihir Gandhi Director, Payments Transformation [email protected]

Hemant Kshirsagar Manager, FinTech [email protected]

Leadership Contributors

Aiman Faraz Strategy Consultant, FinTech

Pulkit Jain Strategy Consultant, FinTech

About PwCAt PwC, our purpose is to build trust in society and solve important problems. We’re a network of firms in 157 countries with more than 2,23,000 people who are committed to delivering quality in assurance, advisory and tax services. Find out more and tell us what matters to you by visiting us at www.pwc.com

In India, PwC has offices in these cities: Ahmedabad, Bengaluru, Chennai, Delhi NCR, Hyderabad, Kolkata, Mumbai and Pune. For more information about PwC India’s service offerings, visit www.pwc.com/in

PwC refers to the PwC International network and/or one or more of its member firms, each of which is a separate, independent and distinct legal entity in separate lines of service. Please see www.pwc.com/structure for further details.

©2017 PwC. All rights reserved.

pwc.in/fintechData Classification: DC0

This document does not constitute professional advice. The information in this document has been obtained or derived from sources believed by PricewaterhouseCoopers Private Limited (PwCPL) to be reliable but PwCPL does not represent that this information is accurate or complete. Any opinions or estimates contained in this document represent the judgment of PwCPL at this time and are subject to change without notice. Readers of this publication are advised to seek their own professional advice before taking any course of action or decision, for which they are entirely responsible, based on the contents of this publication. PwCPL neither accepts or assumes any responsibility or liability to any reader of this publication in respect of the information contained within it or for any decisions readers may take or decide not to or fail to take.

© 2017 PricewaterhouseCoopers Private Limited. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers Private Limited (a limited liability company in India having Corporate Identity Number or CIN : U74140WB1983PTC036093), which is a member firm of PricewaterhouseCoopers International Limited (PwCIL), each member firm of which is a separate legal entity.

VB/April2017-9302