first half 2017 revenues - actusnews.com€¦ · first half 2017 revenues ... ericsson video...

TRANSCRIPT

First Half 2017 revenues

July 27, 2017

2ATEME © 1991-2017

Disclaimer

This presentation does not constitute or form part of and should not be construed as any offer for sale of or solicitation of any offerto buy any securities of ATEME, nor should it, or any part of it, form the basis of or be relied on in connection with any contract orcommitment whatsoever concerning ATEME’s assets, activities or shares.

All statements other than historical facts included in this presentation, including without limitations, those regarding ATEME’sposition, business strategy, plans and objectives are forward-looking statements.

The forward-looking statements included herein are for illustrative purposes only and are based on management’s current views andassumptions. Such forward-looking statements involve known and unknown risks. For illustrative purposes only, such risks includebut are not limited to impact of external events on customers and suppliers; the effects of competing technologies competitiongenerally in main markets; profitability of the expansion strategy; litigation; ability to establish and maintain strategic relationshipsin major businesses; and the effect of future acquisitions and investments.

ATEME expressly disclaims any obligation or undertaking to update or revise any projections, forecasts or estimates contained in thispresentation to reflect any change in events, conditions, assumptions or circumstances on which any such statements are based,unless so required by applicable law. These materials are supplied to you solely for your information and may not be copied ordistributed to any other person (whether in or outside your organization) or published, in whole or in part, for any purpose.

3ATEME © 1991-2017

Presenters

Michel ArtièresFounder & Chief Executive Officer

Degree in Engineering from Supelec, Paris, with a specialization in signal processing and telecommunications

R&D in Image Processing and Compression for the French Ministry of Defense

Fabrice Sana Chief Financial Officer

Degrees from the European Business School and ESSEC

Management Control Director for KaravelFinance Controller for AlstomManager at Arthur Andersen / BearingPoint

4ATEME © 1991-2017

1.ATEME2. Market Trends

3. Financial Performance

4. Strategy

5ATEME © 1991-2017

ATEME Factsheet

22 Patents

200 people in 14 countries

700 clients in 100 countries

Public since 2014

Sales & Support Los Angeles

America Ops CenterDenver

Sales & Support NYC

Support Miami

LATAM Ops CenterSão Paulo

Sales & SupportMexico City

SupportBuenos Aires

HQ, Paris

R&D centerRennes

Sales & SupportDubai

Sales & SupportNew Delhi

APAC Ops CenterSingapore

Sales & SupportSeoul

Sales & SupportShenzhen

37.5 M€ in 2016 (+31%)

ATEME designs software video compression solutions to enable innovative live or on demand video delivery

services, while preserving picture quality.

Headquarters

Offices

Sales & SupportSydney

Sales & SupportHô-Chi-Minh

6ATEME © 1991-2017

Over a Century of Combined Domain Leadership

CTO Pierre Larbier• 20+ years of compression innovation. 10 compression patents • DVB, ASTC, SMPTE, AOM Committees & Standards

R&D Thierry Marre• 20+ years of telecom & video engineering • Led +100p SW agile teams

APAC Sales Yoann Poizeau• 10+ years supporting tier-1 service providers• Led Dalet APAC sales

Product Remi Beaudouin• 10+ years in video compression exec management• Lead WW Product Management/Marketing teams

Strategy Yossi Aloni• 20+ years of exec positions with operators. system

vendors and technology providers

Latin America Sales Ezio Sanchez• 20+ years supporting tier-1 service providers• Led NDS, Thomson & Conax Latam sales

North America Sales Chad Hassler• 20+ years supporting tier-1 service providers• Led Scopus & Harmonic sales

EMEA Sales Emmanuel Boureau• 20+ years supporting tier-1 service providers• Led Ericsson & Harmonic sales

7ATEME © 1991-2017

What is Video Compression and Why it Matters

• Compression is a Must. Video is 80% of the internet traffic*.

• The encoding technology is key

• ITU (Geneva) defines international standards MPEG-2 (1994), MPEG-4 (2003), HEVC (2013).

• An intelligent encoder (eg. including objects tracking algorithms) requires less bitrate for the same video quality (or generates a better video quality at a given bitrate).

• The decoder is passive (2 decoders would always display the same video). No innovation there.

Whatever the network (cable, internet, satellite, terrestrial), digital video has to be compressed 500x typically

Uncompressed HD Video

~ 2 Gbits/s Encoder

CompressedHD Video

~ 4 Mbits/s

Decoder

* Cisco Visual Networking Index

8ATEME © 1991-2017

ATEME member of Alliance for Open Media

Internet leaders partnering to standardize AV1 in 2017, a royalty-free alternative to HEVC

Technology Leadership through Standardization Activities

Television Formats

Co-Chairmanship of 2 working groups at ITU for HEVC

Final Performance of the HEVC Standard

ATEME involvement in the standardization activities is unique amongst video compression vendors

9ATEME © 1991-2017

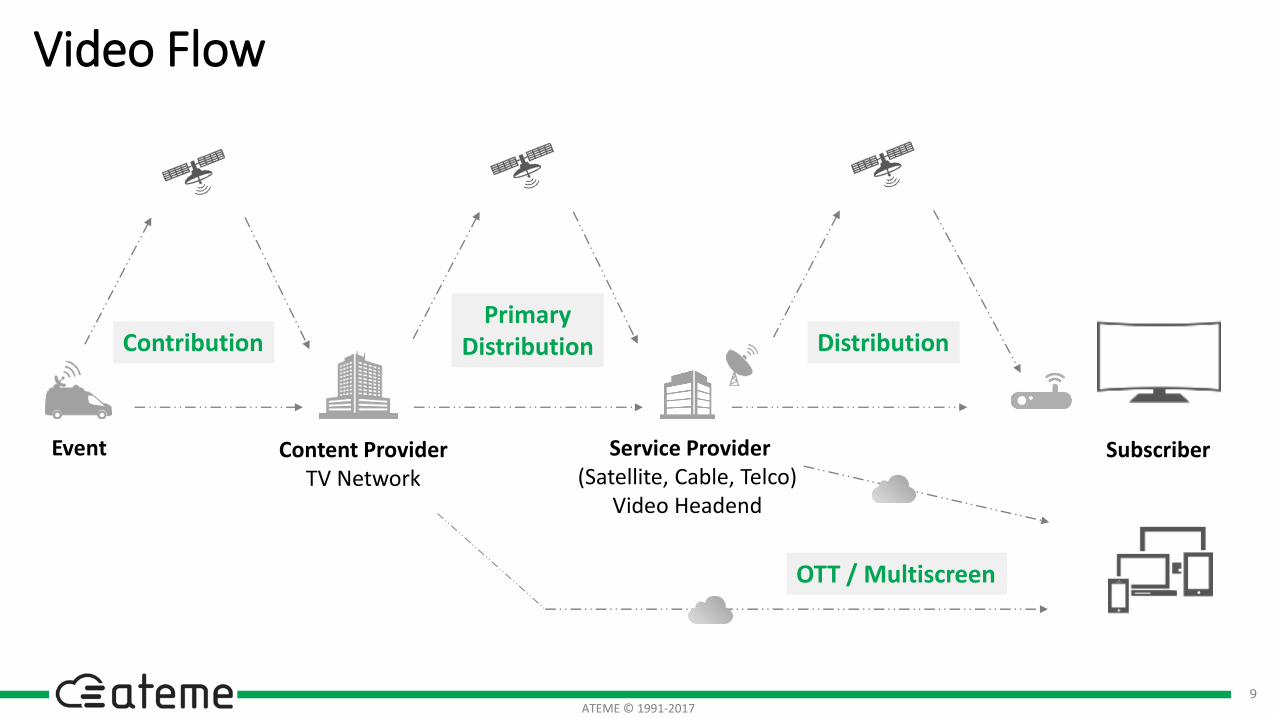

Video Flow

Service Provider(Satellite, Cable, Telco)

Video Headend

Content ProviderTV Network

Event

ContributionPrimary

Distribution Distribution

OTT / Multiscreen

Subscriber

10ATEME © 1991-2017

TV StationEventKyrion encoders in the trucks and decoders at the TV station

Launched in 2007, used for the most prestigious events embeds ATEME

compression software on a FPGA

processor

CLIENTS broadcasters and service providers (direct), truck operators (indirect)

CAPEX (refresh cycle ~ 4 years) + Annual Support &

Maintenance

Ericsson Video Quality, Upgradable (Software)

TECHNOLOGY BUSINESS MODEL COMPETITION USPs

ATEME’s Kyrion Leading the Contribution Market

CLIENTS

11ATEME © 1991-2017

Service Provider (Cable, Telco, Satellite)

Video Headend

Subscribers

TITAN is a virtualized Video Headend software covering all Live and File needs

Launched in 2009 (VOD) and 2011

(Live)

100% ATEME software

Recurring revenues despite perpetual

licenses model+ Annual Support &

Maintenance

Video Quality, Speed / Density,

100% Home Grown Software, Flexibility

Harmonic, Ericsson,

Cisco

TECHNOLOGY BUSINESS MODEL COMPETITION USPs

CLIENTS

ATEME’s TITAN the Distribution and OTT Challenger

12ATEME © 1991-2017

Strategic Partners

Enabling access to Service Providers datacenters

Better exposure, lower cost solution

Enabling transition of Service Providers to datacenters

Better performance (video quality / density)

13ATEME © 1991-2017

1. ATEME

2.Market Trends3. Financial Performance

4. Strategy

14ATEME © 1991-2017

Growing Access to €1B Video Infrastructure Market 2017

€250mPrimary Distribution

€100mContribution

€300mMultiscreen

€350mDistribution

ATEME core segment IPO enabled, Winning now

Segment

Access

ATEMEProduct

Sources : Frost & Sullivan (2014), Company

SW Shift in Progress

15ATEME © 1991-2017

Video Growth DriversContinued Demand for High Efficiency Compression

More Screen Time

TV declines but overall screen time is increasing

Content Explosion

DelinearizationMore channels, more content

Monetization Opportunities

Multiplication of distribution formats

New Distribution Models

Multiscreen, OTT

Ultra HD Television

4K, HDR, WCG, HFR

+13%Daily screen time

from 2011 to 2015

source: eMarketer, Apr. 2015

16ATEME © 1991-2017

Industry Shift to Software, the Revolution in Progress

Today, Service Providers deploy Software Converged Video Headends (Live + VOD, Box + Multiscreen), in a virtualized environment

Legacy Video Headendfor the linear distribution to the box

VOD and Multiscreenseparated infrastructure

Software Virtualized Video Headendrunning on a private cloud

=Software

Virtualized Headend

Running on

Private cloud

+ + Multi-Screen

VOD

10 years ago,Video Head Ends consisted in heterogeneous specialized hardware for each operation

Then,VOD and multiscreen were added and managed as separate operations

Legacy VHE

17ATEME © 1991-2017

Sept 2015

$300-500M (5-7x)

acquires

Sept 2015

$125M (4x)

acquires

Dec 2015

€69M (1x)

acquires

Consolidation Clearing the Way for ATEME

Essentially down from 7 to 4 Players

• US service providers running away from their competitor (Amazon Prime Video)

• Envivio partners are Ericsson competitors

• Redundant employees (Sales worldwide)

• Products end of life confusing clients

• Redundant employees (Rennes R&D)

Ideal

Scenario

for ATEME

March 2017

$1 Bn sales in 2016

to sell its Media Business

18ATEME © 1991-2017

1. ATEME

2. Market Trends

3.Financial Performance4. Strategy

19ATEME © 1991-2017

7 436 10 646

7 544

10 291

2011 2012 2013 2014 2015 2016 2017

Q1 Q2 Q3 Q4

H1 2017 Revenue Acceleration : +40%

€37.5m

€28.6m

€12.3m

€17.9m

€20.6m

€24.8m

+31%

CAGR : +23%

IPO

H1 2017 : +40%

20ATEME © 1991-2017

H1 2017 Regional Performance

+46%

+147%

-3%

+175%

37% of H1 2017

16%of H1 17

EMEA

• Q2 performance almost compensated for the slow start in Q1

• Recent ramp-up of TITAN software with leading European service providers is gaining traction and should drive growth over the coming quarters

USA/Canada

• Continuous Investment• Stronger presence

(Denver office and lab, NYC next)

• Tier1 operators won

Latin America

• Investments made in 2016 to increase market share and footprint are paying off

• Leading service providers deploying TITAN based software solutions to power their video head ends

• Stronger presence (Mexico, Argentina, Peru next)

APAC

• Continuous investment• Reorganized sales and

operations (Singapore, China, Korea)

• New projects with a major global system integrator

17%of H1 17

30%of H1 2017

revenue

21ATEME © 1991-2017

2016 P&LConsolidated data – IFRS –in thousands of euros

2015 2016 % change

Revenue 28,584 37,462 +31.1%

Gross profit 14,987 22,031 +47.0%

Gross margin 52.4% 58.8%

R&D expenses (5,497) (5,661) +3.0%

Sales & marketing expenses (11,054) (12,776) +15.6%

Other G&A expenses (1,464) (1,433) -2.1%

Operating profit (3,028) 2,162 ns

Operating margin -10.6% 5.8%

Financial loss (82) (207) +152.4%

Financial profit 67 10 -85.1%

Exchange effect 579 247 -57.3%

Net profit (2,465) 2,212 ns

Net margin -6.8% 5.9%

+6.4 points increase in gross margin notably thanks to the growth in software sales

Operating expenses contained:

• Slight increase in R&D expenses

• S&M expenses grew not as fast as the topline

€2.2m operating profit

€2.2m net profit : profitable year for the 1st time since the IPO

22ATEME © 1991-2017

IPO July 2014

201620152014

Successful Strategy Since the IPO

2017

Phase 1: 30 hires in 6 months (opened Rennes R&D office)

€12.3m

€-2.5m

€15.0m

€-1.6m

€16.3m

€0.0m

€22.5m

€12.9m

€-1.1m

€11.9m

€-0.9m

Phase 2:Design of TITAN 4 and reorganization of international offices

Phase 3: Commercial launch

165

135

170

€3.8m

Revenues

Net Loss/Profit

Growth acceleration in H2 2016: a 2 years ROI since the IPO

23ATEME © 1991-2017

2016/12/31 Balance Sheet

Consolidated data - IFRS – in thousands of euros

2015 2016A

SSET

SNon-current assets 4,811 5,312

Current assets 20,362 23,156

- o/w stocks 3,366 3,094

- o/w trade receivables 9,436 13,052

Cash and cash equivalents 4,225 4,096

25,173 28,468

LIA

BIL

ITIE

S

Shareholders’ equity 11,749 14,089

Non-current liabilities 4,616 4,300

- o/w non-current financial debt 4,229 3,782

Current liabilities 8,808 10,079

- o/w current financial debt 939 957

- o/w trade payables 3,754 4,20125,173 28,468

24ATEME © 1991-2017

2016 FCFConsolidated data - IFRS – in thousands of euros

2015 2016

Net Profit (Loss) (2,465) 2,212

(-) Elimination of non-cash elements (1,531) (1,841)

Gross cash flow (934) 4,053

(-) Change in Working Capital 2,151 1,690

Cash flow from operations (3,086) 2,363

Cash flow from investing activities (1,994) (1,635)

Cash flow from operating activities and after investment (5,080) 728

New loans and contingent advances 3,535 0

Interest expense (14) (13)

Repayment of loans and contingent advances (795) (907)

Repayment of financial leases (70) (122)

Other financial flows (including factoring) (121) 247

Cash flow from financing activities 2,536 (795)

Currency effect (117) (61)

Net Change in Cash (2,661) (128)

Opening Cash position 6,884 4,222

Closing Cash position 4,222 4,094

Positive Operating Cash Flow : €2.4m

Positive Free Cash Flow : €0.7m

Cash position end of the year : €4.1m

Increase in self-financing capacity

No new loan in 2016

25ATEME © 1991-2017

1. ATEME

2. Market Trends

3. Financial Performance

4.Strategy

26ATEME © 1991-2017

• TITAN Video Head End software components can be reused in the Network to enable new video delivery schemes.

• Clients benefit: huge network infrastructure CAPEX and OPEX savings.

• ATEME benefit: huge TAM expansion ($25 Billion) with limited R&D and Sales costs (same clients).

• Similar strategy applied to firewalls proved very successful at Palo Alto Networks.

Win The Video Headend, Expand to Video Networking

à

Continued Network Investment Not Meeting Video Demand Growth

Video Is Clogging The Networks ATEME Metro Network Video Processing

Video Grows 3-fold 26% CAGR Unveils $14 Billion Infrastructure Plan Enabling Video Growth Using

Existing Network Infrastructure

27ATEME © 1991-2017

20182017Win the Video

Head End market and prepareexpanding to Network

Gross Margin expected up(shift to software)

Targeting double digit operating profit by 2018

Toplineexpected to keep growing in the 30% range (all regions will contribute)

2017-2018 Plan

S&M investments to

win the Video Head End market and prepare expanding

to Network, but

will not grow as fast as the topline

R&D investments to

prepare expanding

to Network, but

will not grow as fast as the topline

28ATEME © 1991-2017

Investors Relations

Next investor dates

Sept. 28, 2017 : 2017 Half-Year Results

Sept. 29,2017 : Investors presentation (Paris)

Nov. 9, 2017 : 2017 Q3 Revenues

Market data

ISIN: FR0011992700 - Ticker: ATEME

Stock price: €18.03 (as of 25 July 2017)

Market cap: €181.7 m (as of 25 July 2017)

Shareholder structureNumber of shares: 10,169,883Potential dilution : up to 441,900 shares

9,1%

12,0%

62,4%

16,5%

ELIGIBLE PEA PME

Business angels

Free float

Founders and management

VCs

Liquidity contract: Gilbert Dupont

0

100 000

200 000

300 000

400 000

500 000

600 000

700 000

3,00 €

5,00 €

7,00 €

9,00 €

11,00 €

13,00 €

15,00 €

17,00 €

19,00 €

21,00 €

Stock price Volume