first time homebuyer

TRANSCRIPT

FIRST-TIMEHOME BUYERS

GUIDE

Who’s buying and why?If you’re keen on buying a new home soon, you’re not alone.

Young Canadians feel that housing is still a good investment,

according to Home Ownership polls. Nearly 76% of those aged 25-

34 believe that owning a house or condo is a very good

investment. Forty-three per cent of 18-to-24 year olds say they are

considering purchasing a home in the next two years.

The housing market also generates a lot of economic activity in

Canada. Not just home selling and buying and construction but

also for those industries connected to housing such as legal

services, moving companies, landscaping companies, home

improvement companies, etc. Each year, approximately 620,000

households move into newly-purchased homes in Canada.

However, the process can be overwhelming. It doesn’t have to be

if you put together a team of experts who will guide you through

the steps.

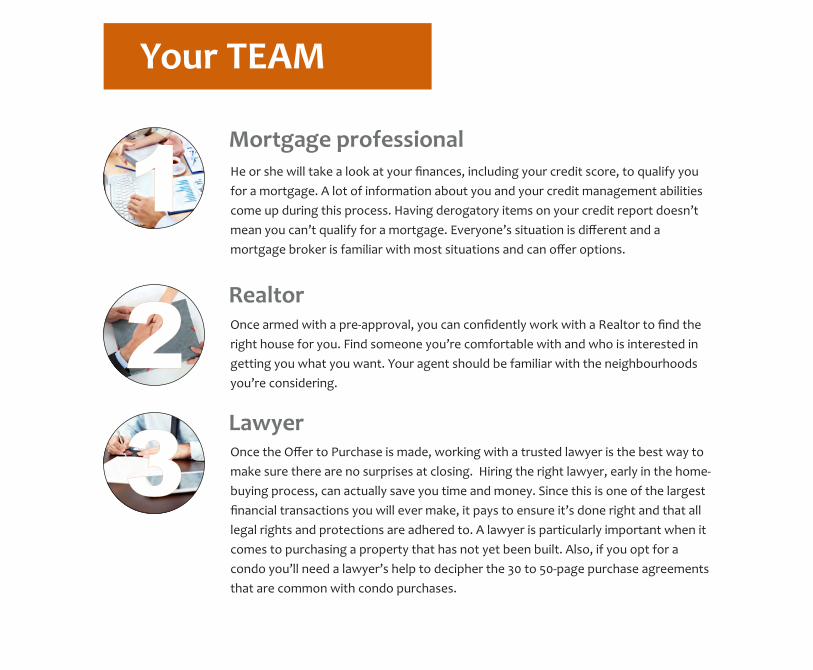

Once the Offer to Purchase is made, working with a trusted lawyer is the best way to

make sure there are no surprises at closing. Hiring the right lawyer, early in the home-

buying process, can actually save you time and money. Since this is one of the largest

financial transactions you will ever make, it pays to ensure it’s done right and that all

legal rights and protections are adhered to. A lawyer is particularly important when it

comes to purchasing a property that has not yet been built. Also, if you opt for a

condo you’ll need a lawyer’s help to decipher the 30 to 50-page purchase agreements

that are common with condo purchases.

Mortgage professional

Realtor

Lawyer

He or she will take a look at your finances, including your credit score, to qualify you

for a mortgage. A lot of information about you and your credit management abilities

come up during this process. Having derogatory items on your credit report doesn’t

mean you can’t qualify for a mortgage. Everyone’s situation is different and a

mortgage broker is familiar with most situations and can offer options.

Once armed with a pre-approval, you can confidently work with a Realtor to find the

right house for you. Find someone you’re comfortable with and who is interested in

getting you what you want. Your agent should be familiar with the neighbourhoods

you’re considering.

1

3

2

Your TEAMBuying a home for the first time should be an exciting time but it can be a

stressful experience -- there’s a lot to consider when starting out. A home is

likely the largest purchase you’ll make in your life and it’s likely the largest

financial contract you’ll have to sign.

Who’s buying and why?If you’re keen on buying a new home soon, you’re not alone.

Young Canadians feel that housing is still a good investment,

according to Home Ownership polls. Nearly 76% of those aged 25-

34 believe that owning a house or condo is a very good

investment. Forty-three per cent of 18-to-24 year olds say they are

considering purchasing a home in the next two years.

The housing market also generates a lot of economic activity in

Canada. Not just home selling and buying and construction but

also for those industries connected to housing such as legal

services, moving companies, landscaping companies, home

improvement companies, etc. Each year, approximately 620,000

households move into newly-purchased homes in Canada.

However, the process can be overwhelming. It doesn’t have to be

if you put together a team of experts who will guide you through

the steps.

Once the Offer to Purchase is made, working with a trusted lawyer is the best way to

make sure there are no surprises at closing. Hiring the right lawyer, early in the home-

buying process, can actually save you time and money. Since this is one of the largest

financial transactions you will ever make, it pays to ensure it’s done right and that all

legal rights and protections are adhered to. A lawyer is particularly important when it

comes to purchasing a property that has not yet been built. Also, if you opt for a

condo you’ll need a lawyer’s help to decipher the 30 to 50-page purchase agreements

that are common with condo purchases.

Mortgage professional

Realtor

Lawyer

He or she will take a look at your finances, including your credit score, to qualify you

for a mortgage. A lot of information about you and your credit management abilities

come up during this process. Having derogatory items on your credit report doesn’t

mean you can’t qualify for a mortgage. Everyone’s situation is different and a

mortgage broker is familiar with most situations and can offer options.

Once armed with a pre-approval, you can confidently work with a Realtor to find the

right house for you. Find someone you’re comfortable with and who is interested in

getting you what you want. Your agent should be familiar with the neighbourhoods

you’re considering.

1

3

2

Your TEAMBuying a home for the first time should be an exciting time but it can be a

stressful experience -- there’s a lot to consider when starting out. A home is

likely the largest purchase you’ll make in your life and it’s likely the largest

financial contract you’ll have to sign.

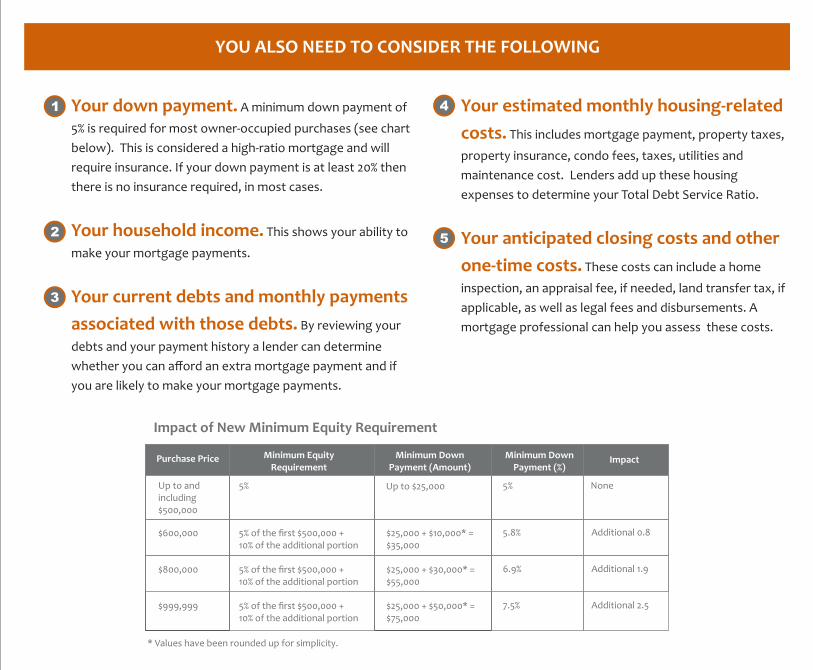

Impact of New Minimum Equity Requirement

Purchase Price Minimum Equity Requirement

Minimum Down Payment (Amount)

Minimum Down Payment (%)

Impact

Up to and including$500,000

$600,000

$800,000

$999,999

5%

5% of the first $500,000 + 10% of the additional portion

5% of the first $500,000 + 10% of the additional portion

5% of the first $500,000 + 10% of the additional portion

Up to $25,000

$25,000 + $10,000* =$35,000

$25,000 + $30,000* =$55,000

$25,000 + $50,000* =$75,000

5%

Additional 2.5

5.8%

6.9%

7.5%

None

Additional 0.8

Additional 1.9

* Values have been rounded up for simplicity.

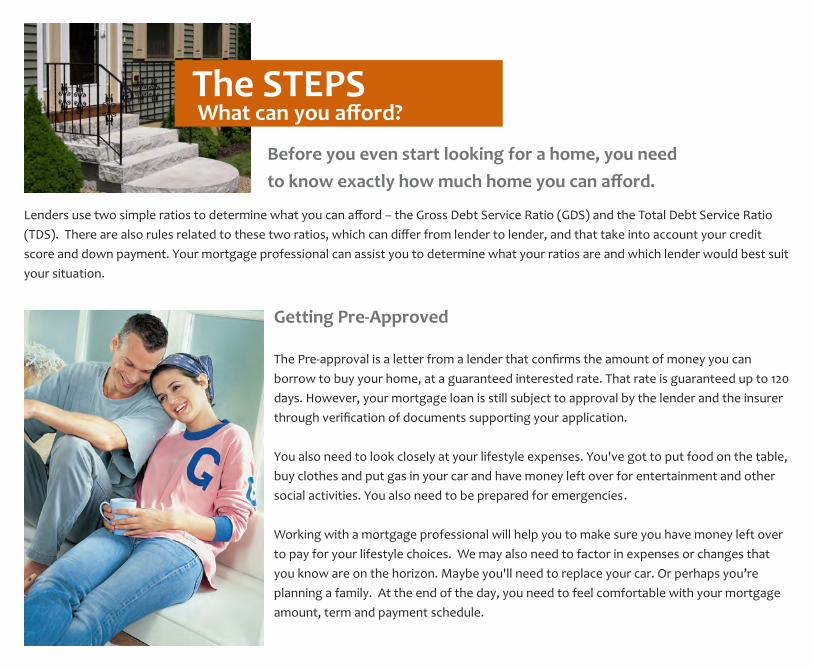

Ÿ A minimum down payment of Your down payment.5% is required for most owner-occupied purchases (see chart

below). This is considered a high-ratio mortgage and will

require insurance. If your down payment is at least 20% then

there is no insurance required, in most cases.

Ÿ This shows your ability to Your household income.make your mortgage payments.

Ÿ Your current debts and monthly payments

associated with those debts. By reviewing your

debts and your payment history a lender can determine

whether you can afford an extra mortgage payment and if

you are likely to make your mortgage payments.

YOU ALSO NEED TO CONSIDER THE FOLLOWING

2

1

3

The STEPSWhat can you afford? Ÿ Your estimated monthly housing-related

costs. This includes mortgage payment, property taxes,

property insurance, condo fees, taxes, utilities and

maintenance cost. Lenders add up these housing

expenses to determine your Total Debt Service Ratio.

Ÿ Your anticipated closing costs and other

one-time costs. These costs can include a home

inspection, an appraisal fee, if needed, land transfer tax, if

applicable, as well as legal fees and disbursements. A

mortgage professional can help you assess these costs.

4

5

.

Impact of New Minimum Equity Requirement

Purchase Price Minimum Equity Requirement

Minimum Down Payment (Amount)

Minimum Down Payment (%)

Impact

Up to and including$500,000

$600,000

$800,000

$999,999

5%

5% of the first $500,000 + 10% of the additional portion

5% of the first $500,000 + 10% of the additional portion

5% of the first $500,000 + 10% of the additional portion

Up to $25,000

$25,000 + $10,000* =$35,000

$25,000 + $30,000* =$55,000

$25,000 + $50,000* =$75,000

5%

Additional 2.5

5.8%

6.9%

7.5%

None

Additional 0.8

Additional 1.9

* Values have been rounded up for simplicity.

Ÿ A minimum down payment ofYour down payment.5% is required for most owner-occupied purchases (see chart

below). This is considered a high-ratio mortgage and will

require insurance. If your down payment is at least 20% then

there is no insurance required, in most cases.

Ÿ This shows your ability toYour household income.make your mortgage payments.

Ÿ Your current debts and monthly payments

associated with those debts. By reviewing your

debts and your payment history a lender can determine

whether you can afford an extra mortgage payment and if

you are likely to make your mortgage payments.

YOU ALSO NEED TO CONSIDER THE FOLLOWING

2

1

3

The STEPSWhat can you afford? Ÿ Your estimated monthly housing-related

costs. This includes mortgage payment, property taxes,

property insurance, condo fees, taxes, utilities and

maintenance cost. Lenders add up these housing

expenses to determine your Total Debt Service Ratio.

Ÿ Your anticipated closing costs and other

one-time costs. These costs can include a home

inspection, an appraisal fee, if needed, land transfer tax, if

applicable, as well as legal fees and disbursements. A

mortgage professional can help you assess these costs.

4

5

.

Is it the size of the home or the neighbourhood? A

condominium that is closer to your work may be preferable to a

larger home with a longer commute. How close are you to

schools, entertainment, daycare facilities? Do you want to be

next to a park or next to a power station? Walk the

neighbourhoods you are interested in and talk to the people in

the area.

The home inspection is a critical part of the process, so do your

research. Ask for referrals about home-inspection companies.

There are now additional special inspections that you can pay

for to check for mould, termites, video-camera inspections of

the drainage system and even infrared scanners that can check

whether there is sufficient insulation or moisture or perhaps

even electrical problems that may lie behind walls. It will cost

more for this but should result in fewer problems after closing.

Be prepared to ask your Realtor the hard questions like

basement flooding problems or mould or roof leaks, even if the

leaks have been repaired. Ask about any adverse

neighbourhood conditions.

The PURCHASE

What is most IMPORTANT to you

when buying your FIRST HOME?

Is it the size of the home or the neighbourhood? A

condominium that is closer to your work may be preferable to a

larger home with a longer commute. How close are you to

schools, entertainment, daycare facilities? Do you want to be

next to a park or next to a power station? Walk the

neighbourhoods you are interested in and talk to the people in

the area.

The home inspection is a critical part of the process, so do your

research. Ask for referrals about home-inspection companies.

There are now additional special inspections that you can pay

for to check for mould, termites, video-camera inspections of

the drainage system and even infrared scanners that can check

whether there is sufficient insulation or moisture or perhaps

even electrical problems that may lie behind walls. It will cost

more for this but should result in fewer problems after closing.

Be prepared to ask your Realtor the hard questions like

basement flooding problems or mould or roof leaks, even if the

leaks have been repaired. Ask about any adverse

neighbourhood conditions.

The PURCHASE

What is most IMPORTANT to you

when buying your FIRST HOME?

Blake Wilson Mortgage Broker

Phone: 902.329.3835Fax: 1.877.621.4913

Email: [email protected] www.blakewilson.ca

The Value of Working with BLAKE WILSON