fitt research european global markets research oil …p) 106/05/2009 fundamental, industry,...

TRANSCRIPT

Europe United Kingdom Oil & Gas

7 December 2009

European Oil Services

Chasing the pendulum

Christyan Malek Research Analyst (+44) 20 754-58249 [email protected]

Lucas Herrmann, ACA Research Analyst (+44) 20 754-73636 [email protected]

Jonathan Copus Research Analyst (+44) 20 754-51202 [email protected]

Deutsche Bank AG/London

All prices are those current at the end of the previous trading session unless otherwise indicated. Prices are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank and subject companies. Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Independent, third-party research (IR) on certain companies covered by DBSI's research is available to customers of DBSI in the United States at no cost. Customers can access IR at http://gm.db.com/IndependentResearch or by calling 1-877-208-6300. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MICA(P) 106/05/2009

FITT Research

Fundamental, Industry, Thematic, Thought Leading DB's Company Research’s Research Committee has deemed this work F.I.T.T for investors seeking differentiated ideas. Here our European team undertakes a '360' analysis on the global oil services industry that leverages unique data sourced from Wood Mackenzie and DB's expansive contract database to reveal the winners and losers of oil service themes & names across 2010-11.

Fundamental: ‘capex pendulum’ should swing back in favour of some but not all

Industry: topline momentum is key driver of company earnings mid-term

Thematic: a unique analysis of appraisal drilling and license terms

Thought leading: deepwater drilling most attractive; E&C winners & losers

Playing the trends: Amec, SPMI & SDRL - top picks offer impressive growth

Co

mp

any

Glo

bal

Mar

kets

Res

earc

h

Europe United Kingdom Oil & Gas

7 December 2009

European Oil Services Chasing the pendulum

Christyan Malek Research Analyst (+44) 20 754-58249 [email protected]

Lucas Herrmann, ACA Research Analyst (+44) 20 754-73636 [email protected]

Jonathan Copus Research Analyst (+44) 20 754-51202 [email protected]

Fundamental, Industry, Thematic, Thought Leading DB's Company Research’s Research Committee has deemed this work F.I.T.T for investors seeking differentiated ideas. Here our European team undertakes a '360' analysis on the global oil services industry that leverages unique data sourced from Wood Mackenzie and DB's expansive contract database to reveal the winners and losers of oil service themes & names across 2010-11.

Deutsche Bank AG/London

All prices are those current at the end of the previous trading session unless otherwise indicated. Prices are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank and subject companies. Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Independent, third-party research (IR) on certain companies covered by DBSI's research is available to customers of DBSI in the United States at no cost. Customers can access IR at http://gm.db.com/IndependentResearch or by calling 1-877-208-6300. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MICA(P) 106/05/2009

FITT Research

Top picks AMEC Plc (AMEC.L),GBP810.00 BuySaipem (SPMI.MI),EUR22.19 BuySeadrill Limited (SDRL.OL),NOK142.10 Buy

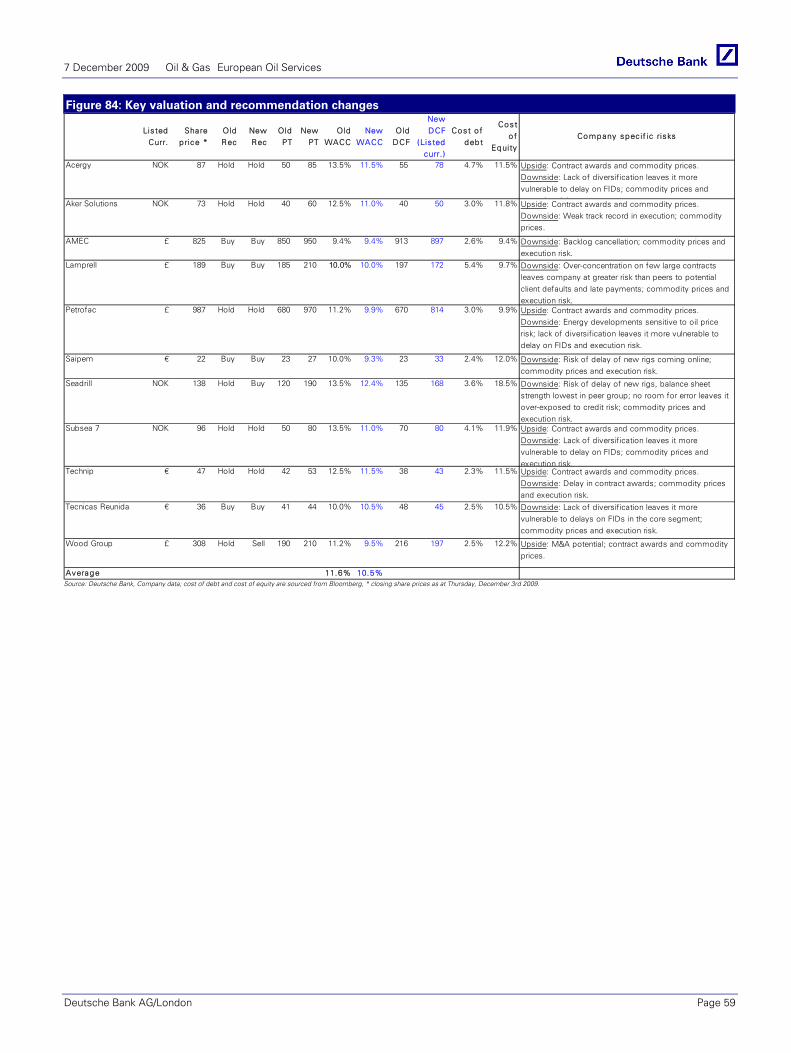

Key changes Ratings/ PT changes From ToAcergy PT NOK 50 NOK 85Aker Solutions PT NOK 40 NOK 60AMEC PT GBp 850 GBp 950Lamprell PT GBp 185 GBp 210Petrofac PT GBp 680 GBp 970Saipem PT E 23 E 27Seadrill PT NOK 120 NOK 190Seadrill rating Hold BuySubsea 7 PT NOK 50 NOK 80Technip PT E 42 E 53Tecnicas Reunidas E 41 E 44Wood Group PT GBp 190 GBp 210Wood Group rating Hold Sell

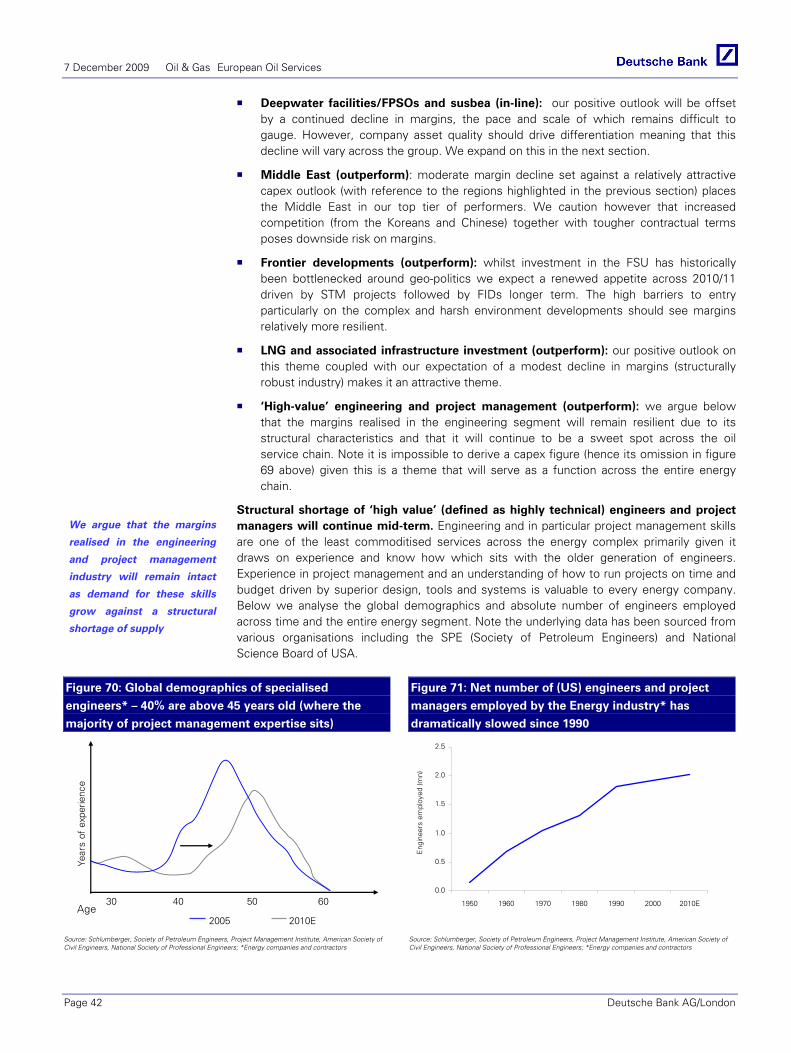

Deepwater appraisal and successful exploration wells drilled globally

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

App

rais

al/ s

ucce

ssfu

l exp

lora

tion

0

20

40

60

80

100

120

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Wel

ls d

rille

dAppraisal/ successful exploration ratio (RHS) Successful exploration Appraisal

Source: Wood Mackenzie, Deutsche Bank

Deepwater rig rate outlook (>2000m)

0200400600800

100012001400160018002000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

E

2010

E

2011

E

WM

dril

ling

days

0

100

200

300

400

500

600

700

Day

rate

('00

0$k/

d)

Drilling days Day rate

Source: Wood Mackenzie, Deutsche Bank

Current expectations for E&C revenue and margin 2009-11E

-40%-35%-30%-25%-20%-15%-10%-5%0%5%10%15%20%25%30%

-350 -300 -250 -200 -150 -100 -50 -

Absolute margin downside 2009-11E(bps)

Ave

rage

cap

ex g

row

th 2

009-

11E

LNG

Deepwater subsea

Refining & Petrochem.

Deepwater Facilities

Frontier Developments

Onshore Upstream

Oil Sands

GTL

Regas Middle East

Shallow water (capex)

Negative margin outlook vs. 2008 study

Decrease in capex momentum vs. 2008 study

Shallow water (opex)

Source: Wood Mackenzie, Deutsche Bank

Fundamental: ‘capex pendulum’ should swing back in favour of some but not all Our annual review of global capex conducted in partnership with Wood Mackenzie (WM) forecasts a moderate decline, in aggregate, across 2009-11 (-3%). The long run oil price implicit in WM’s bottom up analysis is $70/bbl. We kick the foundations to reveal green shoots in both exploration and engineering/construction (E&C) segments. While not immune to heightened macro risks near term their secular characteristics should help drive out-performance for those companies with appropriate exposure.

Industry: topline momentum is key driver of company earnings mid-term We place each company’s industry and regional ‘blueprint’ against our updated outlook. Together with our unique framework that differentiates companies on a number of metrics we forecast, on average, topline growth for the group (9%, 2009-12E) against a relatively cautious view on margin (c. 75bps EBITDA reduction). Our 2009-12E earnings outlook for the sector is 8%.

Thematic: a unique analysis of appraisal drilling and license terms Our proprietary analysis, done in conjunction with WM, reveals a material increase in deepwater licenses awarded relative to last year’s study. Between 2010 and 2014 70% of the world’s deepwater exploration licenses (exc. GoM) are due to expire with a sharp rise expected to occur in 2012. We argue that this should drive an impressive increase in absolute levels of exploration activity. Going forward this would also imply a higher intensity of appraisal drilling (for every successful deepwater exploration well we show that four appraisal wells have been drilled, on average, across this decade with some regions posting double digit figures). Together this forms the basis to our structural view that demand for deepwater rigs (particularly in the ultra-deep) will accelerate across the near to medium term.

Thought leading: deepwater drilling most attractive; E&C winners & losers Based on our analysis of deepwater rig supply/demand we believe that day rates here should reach $600k/day by 2011 (currently c. $500k/day). Across the E&C complex we carve out our most & least favored themes/regions and show how our appraisal drilling outlook has positive implications for contractors’ backlog.

Playing the trends: Amec, SPMI & SDRL - top picks offer impressive growth Amec, Saipem & Seadrill (upgraded to Buy) each possess excellent diversification and exposure to our highest conviction themes and regions. In contrast, WG (downgraded to Sell) appears at the weaker end of the industry spectrum given its relatively poor positioning & business model. We have raised our target sector multiple, which in part drives our PT revisions (pg. 54). Key downside risks include oil prices sinking below $70/bbl for a sustained period and poor execution.

7 December 2009 Oil & Gas European Oil Services

Page 2 Deutsche Bank AG/London

Table of Contents

Executive summary...................................................................................... 3

Exploration and appraisal drilling trends .................................................. 7

Exploration industry dynamics and relative profitability....................... 20

Global engineering and construction outlook......................................... 28

Kicking the foundations reveals some green shoots.............................. 31

E&C industry dynamics and relative profitability ................................... 39

Implications for companies’ earnings outlook 2010 and beyond.......... 45

Sector valuation and company winners and losers................................ 52

Top picks and key recommendation changes ......................................... 55

Appendix A: Valuation matrices ............................................................... 57

Appendix B: Exploration, appraisal and development capex split........ 61

Deepwater drilling activity vs. oil price ................................................... 62

Appendix C: Snapshot of each company’s financing ............................. 63

Appendix D: Shallow water drilling duration.......................................... 66

Appendix E: Regional spread of contracted newbuild rigs.................... 67

Appendix F: NOC/IOC/Independents investment in drilling ................. 68

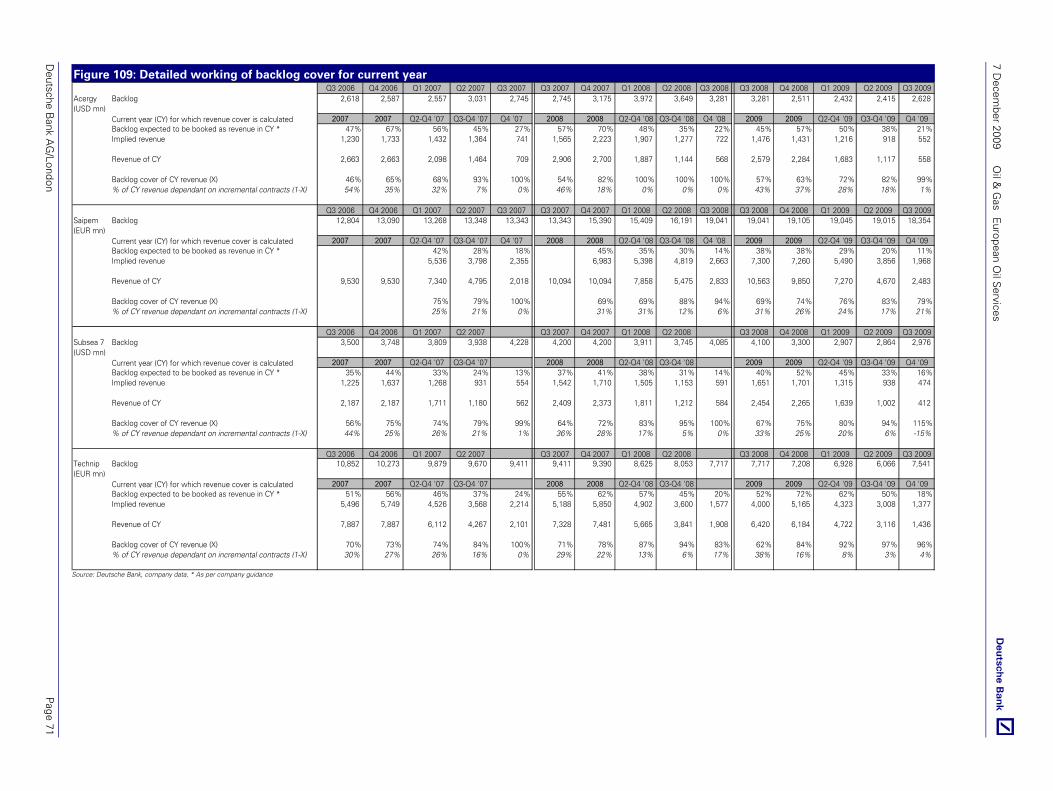

Appendix G: Calculations behind backlog cover analysis...................... 70

Appendix H: Regional split of shallow water capex ............................... 72

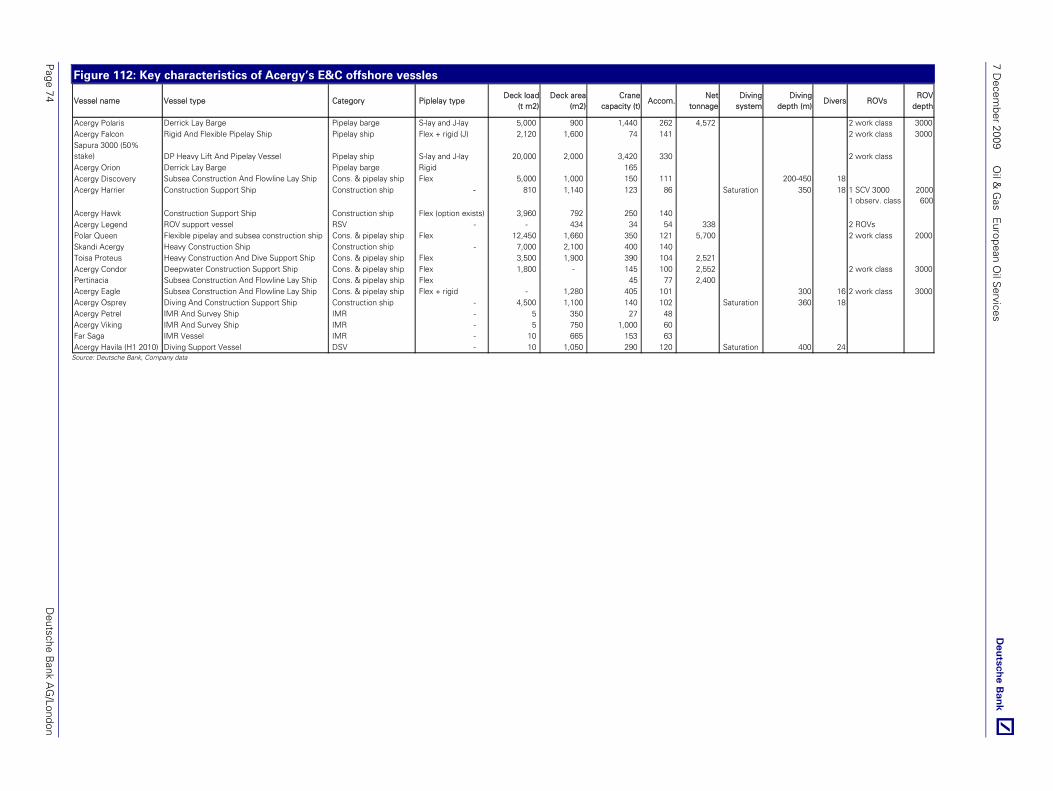

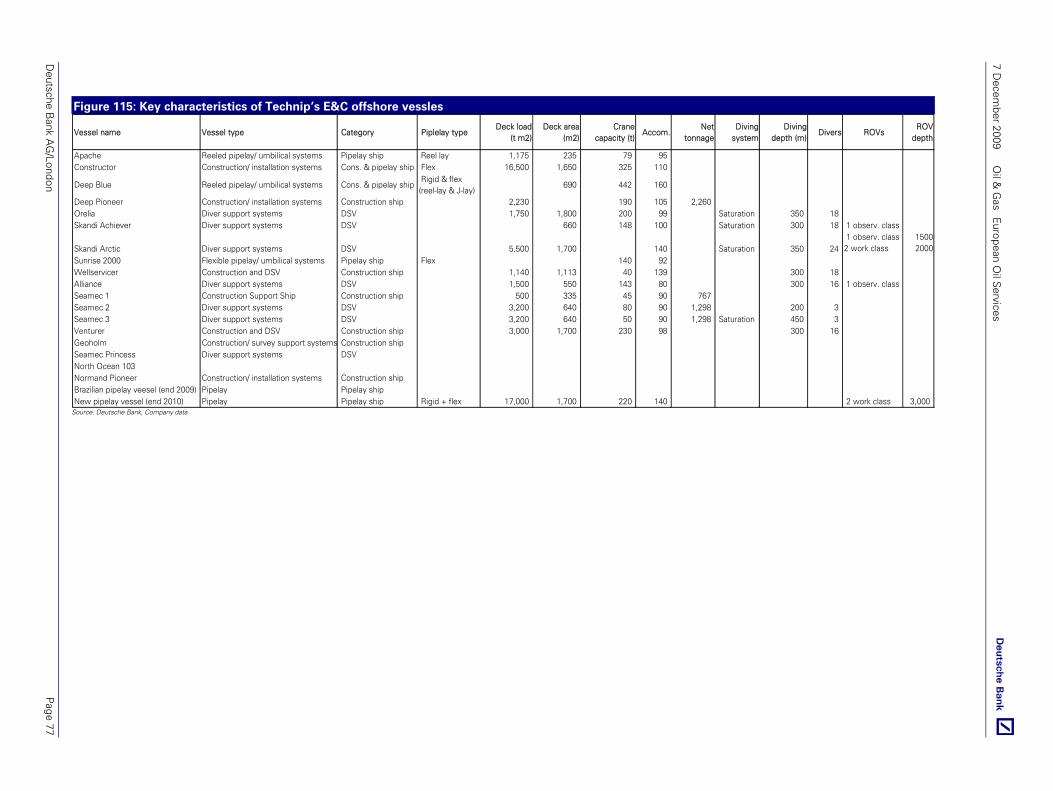

Appendix I: Detailed overview of companies’ fleet ................................ 73

Appendix J: ‘Backlog longevity’ calculation explained .......................... 78

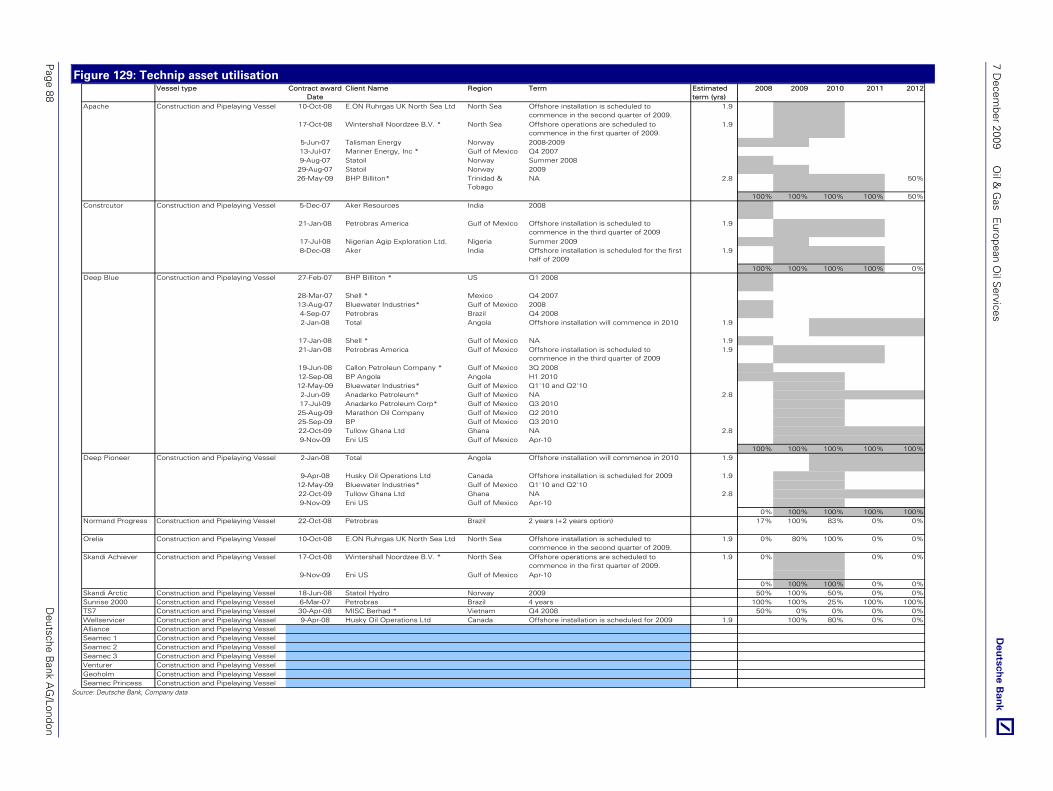

Appendix K: Asset utilisations .................................................................. 80

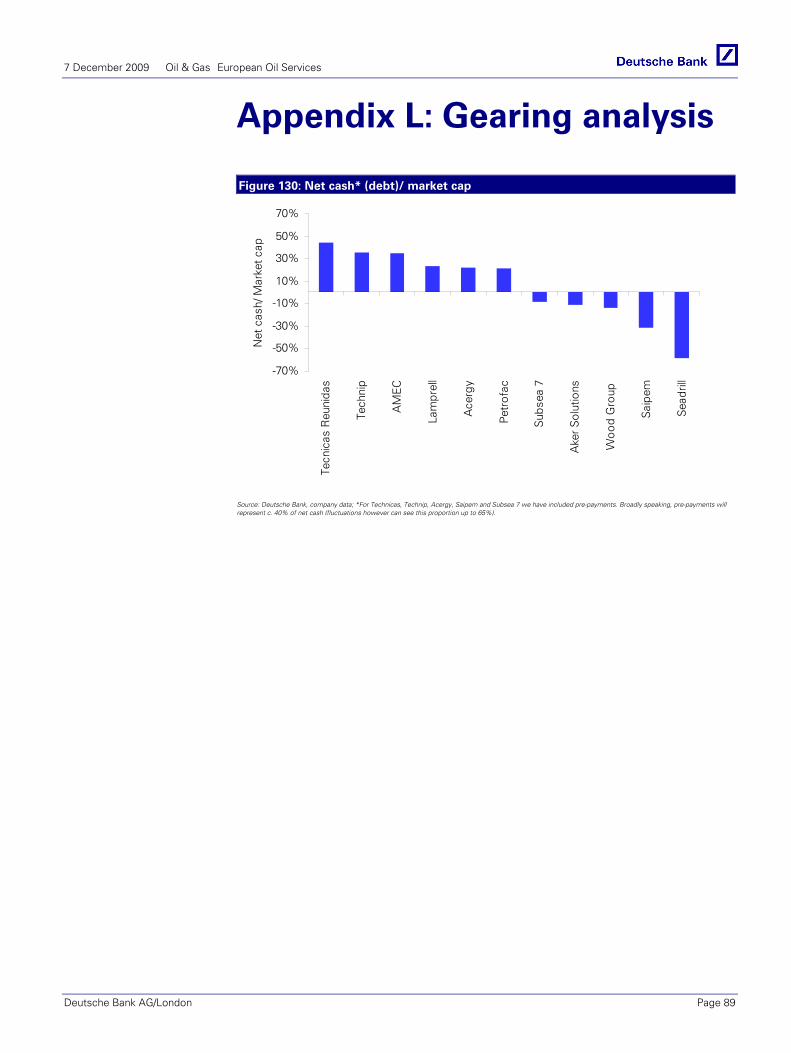

Appendix L: Gearing analysis.................................................................... 89

Appendix M: Contract strategy analysis.................................................. 90

Appendix N: NOC/IOC exposure .............................................................. 92

Appendix O: Licenses awarded by depth (onshore and offshore) ........ 93

Appendix P: Wind power capacity ........................................................... 94

Appendix Q: Strategic analysis of the E&C themes................................ 96

Appendix R: Porter’s 5 forces on key service segments ........................ 98

Appendix S: The CAPEX/OPEX ‘life cycle’ explained ........................... 104

Appendix T: Global oil service spectrum explained ............................. 107

Appendix U: Glossary of terms and simplifications ............................. 110

7 December 2009 Oil & Gas European Oil Services

Deutsche Bank AG/London Page 3

Executive summary Global outlook

Our annual study of global capex conducted in partnership with Wood Mackenzie sees a moderate decline, in aggregate, across 2009-11 (-3% compounded from 2008 levels). Exploration, appraisal and development activity (wellhead operations, drilling and seismic) represents c. 40% of global capex in 2009E with the balance comprising engineering and construction (E&C) spend. In this note we kick the foundations to reveal green shoots in both of these segments which while not immune to heightened macro risks near term, possess secular characteristics that should drive impressive growth in 2010-11 for those companies with appropriate exposure.

Figure 1: Global exploration* and E&C capex outlook

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009E 2010E 2011E

Cap

ex ($

bn)

Exploration, appraisal and development capex E&C capex

Source: Deutsche Bank, Wood Mackenzie; *Appendix B shows exploration, appraisal and development capex split by seismic, wellhead operations and drilling; we estimate that IOC/NOC leasing of drilling rigs (onshore, shallow water and deepwater) represents c.12% of global capex

E&C outlook Cost deflation across the supply chain and delays in Final Investment Decisions (FIDs) has driven a c. 10% drop vs. last year’s outlook (2008-10E). Despite this relatively muted backdrop we reveal a number of ‘sweet spots’ that include deepwater offshore construction (SURF and FPSO/facilities), LNG and OPEX spend (shallow/mid waters). By region, Middle East (Saudi, Kuwait and UAE), SE Asia (Australia and India), Africa (Ghana, Egypt, Angola and Nigeria) and Brazil should emerge as primary drivers of capex. We believe the majority of FIDs here should begin to materialise across H2 2010 and continue through 2011.

Performing strategic analysis of the subsets within this segment drives our absolute and relative outlook of profitability across the E&C complex. The themes we believe will provide out-performance (in terms of capex and margin) across the near to medium term are frontier developments, Middle East, LNG (and associated infrastructure) and ‘high-value’ (defined as highly technical) engineering and project management. Shallow water/conventional OPEX and deepwater facilities/FPSOs/subsea both share impressive capex outlooks but against the potential of excessive margin decline near term this leaves us with a broadly neutral view. Themes we expect will under-perform are shallow water/conventional CAPEX, oil sands and refining and petrochemicals.

The long run oil price

implicit in our bottom up

Wood Mack forecast is

$70/bbl. This is below DB’s

commodities team estimate

of $80/bbl long run

Our analysis shows that

NOCs will become a key

constituent of oil services’

backlog longer term making

them potentially a ‘price

setter’ in the context of a

global capex recovery (NOCs

are expected to represent

40% of global capex and

20% of all contracts signed

across the OFS sector by

2011)

7 December 2009 Oil & Gas European Oil Services

Page 4 Deutsche Bank AG/London

Key risk to our forecast is if FIDs are delayed beyond 2010. Whilst this would place downside pressure on our 2011 estimates we believe the impact should be limited based on our view that IOCs looking to adhere to mid to longer term targets of production would have to invest across 2011/2012. Critical to their reserve replacement will be the need to offset production decline on maturing fields with incrementally new barrels. Having delayed FIDs across 2009-10, we believe IOCs would be under renewed pressure to sustain production at their current levels provided was profitable.

Exploration outlook Demand: rising in deepwater. Proprietary analysis done in conjunction with Wood Mackenzie reveals a threefold increase in the number of deepwater appraisal wells drilled across this decade. We believe this trend is structural based on or analysis that shows a steady rise (since 1995) in: i) deep and ultra-deep appraisal activity (South America and South East Asia appear to be emerging as primary drivers) as IOCs and NOCs place greater focus on developing deepwater acreage. Discoveries in frontier regions across 1996-2000 created a backlog of wells requiring appraisal and triggered a material uplift in appraisal activity relative to exploration. ii) The proportion of wells drilled by independents and NOCs (that arguably possess a different set of criteria to IOCs). iii) The time taken to appraise deepwater wells (in part linked to their increasing depths and complexity).

We have also tracked all exploration licenses awarded since 2000 with a focus on when they are due to expire. We note a material increase in deepwater licenses awarded relative to last year’s study and reveal that between 2010 and 2014 70% of the world’s deepwater exploration licenses (exc. GoM) are due to expire with a sharp rise expected to occur in 2012. We argue that this should drive an impressive increase in absolute levels of exploration activity. Going forward this would also imply a higher intensity of appraisal drilling (for every successful deepwater exploration well we show that four appraisal wells have been drilled, on average, across this decade with some regions posting double digit figures). Together this forms the basis to our structural view that demand for deepwater rigs (particularly in the ultra-deep >2000m) will accelerate across the near to medium term. Our analysis also reveals a robust outlook for shallow water exploration and appraisal drilling based on a material increase in licenses awarded across 2008/09. Onshore activity continues to appear lacklustre. The implications of the above are renewed investment in refurbishment and upgrading of deepwater rig fleet.

Overall, whilst there is downside risk to drill given a potentially worsening macro environment (particularly in the event that license expiries are extended), we believe that near to medium-term exploration and appraisal drilling programs, particularly those in South America, West Africa and South East Asia should be least impacted. This is based, in part, on: i) IOC’s longer-term production targets that are weighted heavily to these regions leaving them with relatively less flexibility to relinquish their license and ii) our analysis in this note that presents a structural case for appraisal drilling that should be sustained at current levels.

Rig supply: tight for the best of them. Our analysis shows that deepwater global rig liquidity (defined as % rigs that are currently un-contracted) has increased from 26% (2008-12E) to 40% (2009-12E) and from 70% to 90% in the shallow water segment (current newbuild schedules suggests a 19% increase in global rig capacity vs. current levels). We believe the ultra deepwater market will demonstrate the best performance as supply/demand fundamentals are expected to tighten again beyond 2010. Having fallen from a record level of $700k/day in 2008 and stabilised around $500k/day, we expect rig rates to rise from 2010 (we forecast $600k/day by 2011) as license expiries loom and exploration/appraisal drilling accelerates. With this in mind, we believe incremental demand for best in class assets (younger, latest generation of rigs) will re-shape the deepwater market as new rig owners gradually displace market share traditionally held by more mature drillers (predominantly US based). We expect downward pressure on rig day rates operating in depths lower than 2000m given the greater availability of (older generation) mid-water fleet partly offset by a robust demand outlook. Shallower water day rates should continue to fall but stabilise

The upward structural shift

in the number of deepwater

wells appraised coupled

with a general rise in

complexity in and around

the wellhead suggests that

appraisal activity will be

sustained at current levels

Overall, whilst there is

downside risk to drill given

a potentially worsening

macro environment

(particularly in the event

that license expiries are

extended), we believe that

near to medium-term

exploration and appraisal

drilling programs,

particularly those in South

America, West Africa and

South East Asia should be

least impacted

Incremental demand for

best in class assets

(younger, latest generation

of rigs) will re-shape the

deepwater market as new

rig owners gradually

displace market share

traditionally held by more

mature drillers

(predominantly US based)

7 December 2009 Oil & Gas European Oil Services

Deutsche Bank AG/London Page 5

towards structurally higher levels than mid-cycle. Elsewhere in the exploration complex, rig construction services emerge as an attractive niche particularly in the Middle East.

Key 2010 trends for the companies We leverage our exhaustive database of contracts to show that since 2004, 70% of all contracts awarded across the E&C sector have comprised of sprint to market projects (STM characterised as brownfield developments that may be monetised relatively quickly and at a lower marginal cost of production than a greenfield project/FID). Whilst STMs are not immune to the volatility in commodity prices, we show that awards of this nature have been instrumental in sustaining the group’s revenue cover for 2009 around historic levels. We argue that the upward shift in shallow and deepwater appraisal drilling highlighted above should spur a proportionate increase in spend directed towards related FEED work and sprint to market projects. As a result we expect 2010 revenue cover for oil service companies exposed to this type of investment (asset light and asset intensive companies alike) to remain robust despite the risk of further potential delays in FIDs across 2010.

Given company management’s general lack of guidance regarding the level of pricing that has been achieved on more recently signed contracts and the apparent lag on company profitability (our analysis reveals it can be anything up to three years) we believe this places downside risk on our renewed margin forecasts for the E&C group (which, on aggregate, assumes some contraction across 2009-11). Variations to this trend will clearly depend on each company’s ability to differentiate both within the respective industry and through the operational efficiencies, strategy and business model underpinning it.

Key recommendations for 2010

We place each company’s industry and regional ‘blueprint’ against our global exploration and E&C projections outlined above. Together with our unique framework that differentiates companies on a number of metrics we model the company’s earnings outlook to 2012 (forecast horizon has been extended from 2011). We forecast, on average, topline growth for the group (9%, 2009-12E) against a more cautious view on margin (c. 75bps EBITDA reduction). Our 2009-12E earnings outlook for the sector is 8%. Our top picks are:

Seadrill: upgraded to Buy, PT NOK 190 (previously 120). Sector leading exposure to deep and ultra-deepwater drilling fuels impressive earning growth (21% 2009-12E CAGR). We argue for an absolute and relative re-rating against the European and US oil services. This should be driven, in part, by its imminent listing in the US (Q1’10) which should help improve investors’ perception of its superior asset quality and deepwater exposure (relative to its most comparable US peers).

Amec: Buy, PT raised to 950p (previously 850p). The company’s unique business model and impressive diversification beyond oil and gas (underpinned by its ‘high-value’ engineering and project management) should drive superior earnings visibility relative to its E&C peers (13% 2009-12 CAGR vs. sector average of 8%).

Saipem: Buy, PT raised to E27 (previously E23). High relative and absolute exposure to several of our preferred themes (including deepwater drilling) drives leading backlog cover and earnings growth across the E&C sector (10% 2009-12 CAGR).

In a scenario where the oil price could sit significantly below $70/bbl for a sustained period of time, we believe the earnings of E&C companies will be negatively impacted beyond 2011 as oil company capex gets pulled back. The reason why our earnings outlook should remain unchanged before then is that existing company backlog provides sufficient revenue cover and that the margins associated with the majority of these projects would have already been contracted (subject to execution performance, of course). Even so, share price sentiment will

We expect 2010 revenue

cover for oil service

companies exposed to

shallow and deepwater of

investment (asset light and

asset intensive companies

alike) to remain robust

despite the risk of further

potential delays in FIDs

across 2010

We believe Saipem, Amec

and Seadrill are optimally

placed across the oil

services chain and

demonstrate superior

earnings growth. In contrast,

Wood Group (downgraded

to Sell) appears at the other

end of the industry

spectrum given its relatively

weak positioning and

business model

7 December 2009 Oil & Gas European Oil Services

Page 6 Deutsche Bank AG/London

be negative (in anticipation of a slowdown in earnings momentum beyond 2010 not to mention the sector’s strong correlation with oil price). Against this backdrop we believe Saipem and Amec would outperform on a relative basis (vs. their E&C peers); Wood Group and Aker Solutions should underperform (we have downgraded Wood Group to a Sell from Hold). On an absolute basis we prefer Seadrill from our entire coverage universe.

Valuation –sector target multiple moved from 2010 to 2011; we continue to argue for a discount against historical multiples

Our 2011E EV/DACF for the sector is currently 7.0x (market cap-weighted) which represents c. 33% discount to the sector’s historical average (2000-08) of 10.5x. Given the decline in both exploration and E&C capex we expect over the near to medium term against what appears to be a slowing in earnings momentum, we believe that our target sector multiple (2011) should trade at a discount to historical multiples.

At the industry level, based on our analysis above we believe the risk (primarily execution and margin compression)/reward (primarily revenue) trade off has shifted more into ‘equilibrium’. However, in light of the lack of visibility surrounding FIDs nearer term linked to the risk of renewed deterioration at the macro level, on balance we argue that our sector target multiple should trade at a 20% discount to the historical average (vs. -50% previously). Improved cashflow visibility to the end of the decade (fuelled by robust sector backlog) coupled with a general improvement in execution and risk sharing between the contractor/client justifies why we believe this sector should not trade at a deeper discount to historical multiples.

Our implied PTs are supported by our DCF valuation in which we assume peak company earnings in 2012 with subsequent linear fade to our mid-cycle scenario in 2015. We have lowered our company WACCs to reflect the reduced market risk premium as well as the relatively lower cost of debt vs. last year’s study. We detail changes in company WACC in Appendix A. This in part drives our price target changes on our universe of stocks (summarised on page 54). We assume a long-term growth rate of 3% which is the average mid-cycle rate since 1990 for the Euro oil services.

Risks

Oil price: whilst impossible to quantify, Wood Mackenzie estimates that 2010/11 E&C capex would be c. 20% lower if oil prices sink to $40/bbl. Russia, North America, Europe and Canada in particular could see an even more exaggerated decline. The Middle East will be the least impacted but nonetheless we would expect to see a slow down. Companies most at risk in this context are Acergy, Susbea 7, Wood Group and Aker Solutions (regional and thematic exposures detailed on pages 46 and 47). In contrast, we believe this downside risk for companies exposed to deepwater drilling will be mitigated by the structural need for operators to drill (near and medium-term) and their longer contract lives that should drive earnings growth well into the next decade.

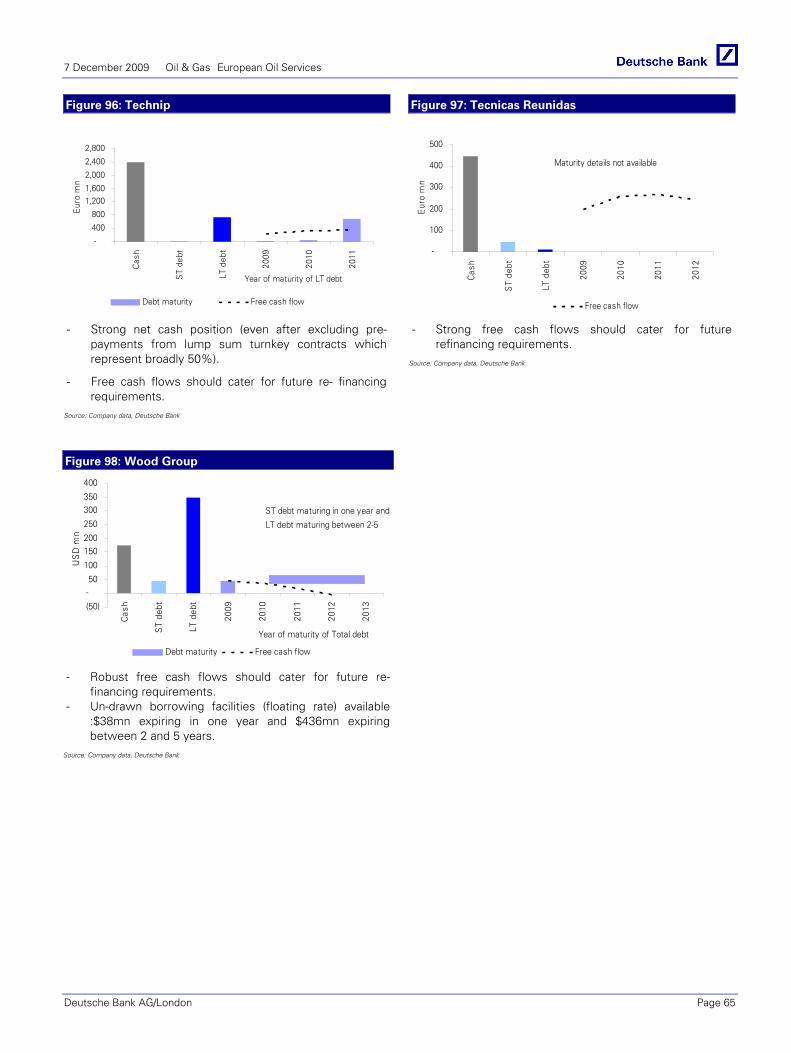

Backlog cancellation (e.g. due to lack of client/contractor funding): Our discussions with Wood Mackenzie and Pegasus Global (leading risk consultants) suggest there is very little probability contracted projects will be cancelled given the healthy state of IOC and NOC balance sheets. In the unlikely event that they do, contractors have the right to file for liquidated damages and take control of all cash pre-payments. Equally we show that the refinancing risk on debt maturities of the companies we cover is low (detailed in Appendix C) and as a result we do not expect them to have cashflow issues in executing their contracts.

Execution: Poor execution is another key industry risk. We believe the potential impact this risk can have on company earnings remains impossible to quantify ahead of any material announcement.

On balance, we argue that

our sector target multiple

should trade at a 20%

discount (vs. -50%

previously) to the historical

average

Key risks are oil price,

backlog cancellation and

execution

7 December 2009 Oil & Gas European Oil Services

Deutsche Bank AG/London Page 7

Exploration and appraisal drilling trends Proprietary analysis done in conjunction with Wood Mackenzie reveals a threefold increase in the number of deepwater appraisal wells drilled across this decade. We believe this trend is structural based on our analysis that shows a steady rise (since 1995) in: i) deep and ultra-deep appraisal activity (South America and South East Asia appear to be emerging as primary drivers) as IOCs and NOCs place greater focus on developing deepwater acreage. Discoveries in frontier regions across 1996-2000 created a backlog of wells requiring appraisal and triggered a material uplift in appraisal activity relative to exploration. ii) The proportion of wells drilled by independents and NOCs (that arguably possess a different set of criteria to IOCs). iii) The time taken to appraise deepwater wells (in part linked to their increasing depths and complexity).

We have also tracked all exploration licenses awarded since 2000 with a focus on when they are due to expire. We note a material increase in deepwater licenses awarded relative to last year’s study and reveal that between 2010 and 2014 70% of the world’s deepwater exploration licenses (exc. GoM) are due to expire with a sharp rise expected to occur in 2012. We argue that this should drive an impressive increase in absolute levels of exploration activity. Going forward this would also imply a higher intensity of appraisal drilling (for every successful deepwater exploration well we show that four appraisal wells have been drilled, on average, across this decade with some regions posting double digit figures). Together this forms the basis to our structural view that demand for deepwater rigs (particularly in the ultra-deep >c. 2000m) will accelerate across the near to medium term. Our analysis also reveals a robust outlook for shallow water exploration and appraisal drilling based on a material increase in licenses awarded across 2008/09. Onshore activity continues to appear lacklustre.

Finally, in this section we argue that the implications of the above are renewed investment in refurbishment and upgrading of deepwater rig fleet (and to a lesser degree shallow and onshore assets).

Appraisal activity represents a discrete yet material driver of drilling demand

In our last FITT report titled ‘Reality Check’ (Oct 2008) we focused on the impact exploration drilling would have on the overall supply/demand outlook for rigs with a particularly emphasis on the deep and ultra-deepwater. We leveraged Wood Mackenzie’s global database of signature bonuses, licenses awarded and drilling days (measured as the time between spudding and completion of the well and a useful indicator of demand to drill) to analyse the outlook for drilling by different depths and respective rig types. We also looked at these licenses with a focus on their expiry profiles. Whilst we revisit these trends and their implications later on in this section our focus to start with is the outlook for shallow water and deepwater (defined as >400m) appraisal drilling and the incremental impact this could have on demand for rig capacity and ultimately day rates.

Simply put, appraisal drilling occurs when the operator has had enough success on an exploration well to want to drill it further. Ultimately it will determine the operator’s decision on whether to develop the well and proceed with an FID (first oil).

Our focus to start with is the

outlook for shallow water

and deepwater (defined as

>400m) appraisal drilling

7 December 2009 Oil & Gas European Oil Services

Page 8 Deutsche Bank AG/London

For every deepwater exploration well, an average four appraisal wells are drilled Figure 2 below shows the number of deepwater appraisal wells vs. successful exploration wells drilled over time. The correlation between the two should not be surprising and we observe the relatively high proportion of appraisal wells drilled subsequent to oil and/or gas being found.

Figure 2: Deepwater appraisal and successful exploration wells drilled globally

0

20

40

60

80

100

120

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Wel

ls d

rille

d

App

rais

al/ s

ucce

ssfu

l exp

lora

tion

Appraisal/ successful exploration ratio (RHS) Successful exploration Appraisal

Source: Wood Mackenzie, Deutsche Bank

Figure 3 shows the relative number of appraisal wells vs. successful exploration wells drilled by region.

Figure 3: Ratio of deepwater appraisal wells drilled vs. successful exploration wells by

region

0

5

10

15

20

25

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Appr

aisa

l/ su

cces

sful

exp

lora

tion

ratio

Africa N America S America South East Asia Australia Average

Source: Wood Mackenzie, Deutsche Bank

We make the following observations from the above:

A structural increase in appraisal activity in relative and absolute terms driven by a greater focus on deepwater acreage by IOCs and NOCs. Discoveries in frontier regions

Our analysis reveals a

relatively high proportion of

appraisal wells drilled

subsequent to oil and/or gas

being found

7 December 2009 Oil & Gas European Oil Services

Deutsche Bank AG/London Page 9

across 1996-2000 created a backlog of wells requiring appraisal and helps explain the divergence between appraisal and exploration drilling during the same period.

The global historic average is around 4 appraisal wells drilled per successful exploration well.

South America and North America (primarily Gulf of Mexico) have both experienced relatively higher appraisal activity vs. other parts of the world. Large discoveries across this decade would have driven the spikes in appraisal drilling relative to exploration.

Secular increase in appraisal drilling should place upside pressure on global demand for deepwater rigs Factors that will influence the degree of appraisal drilling going forward include:

The operator’s desire to establish the well’s commerciality particularly on acreage that is technical challenging (e.g. very deep, remote and/or harsh weather conditions),

An operator’s ambition to achieve first oil as quickly as possible in order to lower the payback period of investment (particularly when the development cycle is difficult to shorten and where there is greater ability to do so during the exploration and appraisal phase),

The well’s proximity to a nearby well(s) that would make it immediately commercial if tied back to existing subsea infrastructure and platform (s),

The fiscal terms set about by the host government which could allow within a certain time frame the participants to be reimbursed on some of the costs incurred during appraisal (vs. exploration which is more often than not fully expensed across the company’s P&L).

No doubt commodity prices will drive operators’ appetite to explore and appraise more wells and a weaker macro environment could see a slowdown in activity. However, we believe the upward trend evidenced above in the number of deepwater wells appraised should stabilise at current levels on an absolute and relative basis. This is supported by our analysis below which shows:

A structural shift in appraisal activity towards deeper waters (figure 4). We also depict this by region (figure 5) and show that South America and South East Asia have emerged as swing players since the start of this decade

Figure 4: Appraisal drilling has gravitated towards mid

and ultra-deep water…

Figure 5: …South America and South East Asia have

emerged as swing players across this decade

-

1,000

2,000

3,000

4,000

5,000

6,000

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Dri

lling

day

s

400-799 800-1199 1200-1599 1600-1999 2000-2399 2400-2799 2800-3199

0

1000

2000

3000

4000

5000

6000

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Dril

ling

days

N America S America Africa E Hemisphere Europe Middle East

Source: Wood Mackenzie, Deutsche Bank; drilling days is defined as the time drilled between spudding & completion of well. Source: Wood Mackenzie, Deutsche Bank; drilling days is defined as the time drilled between spudding &

completion of well.

A higher exploration success rate over time argues for more appraisal work per unit well explored (figure 6 shows the global success rate rising from an average of 15% on average across the first half of the decade to 25% since 2005),

We believe the structural shift

evidenced above in the

number of deepwater wells

appraised will be sustained at

current levels

7 December 2009 Oil & Gas European Oil Services

Page 10 Deutsche Bank AG/London

An increase in the proportion of wells drilled by independents and NOCs since the mid-90’s (figure 7). NOCs’ appetite to explore and appraise will be based on their own (strategic) ambitions for future production. Independents’ incentive to appraise will be linked to their respective drilling schedules (shareholders’ primary focus will be on the company’s exploration and appraisal success).

Figure 6: Exploration success rate (based on commercial

and technical success) has generally improved over

time…

Figure 7: …with a greater proportion of wells drilled by

independents and NOCs

5%

7%

9%

11%

13%

15%

17%

19%

21%

23%

25%

27%

29%

31%

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Expl

orat

ion

succ

ess r

ate

0

50

100

150

200

250

300

350

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Tota

l wel

ls d

rille

d (e

xplo

ratio

n an

d ap

prai

sal)

20%

25%

30%

35%

40%

45%

50%

55%

60%

% In

depe

nden

ts &

NO

Cs

Independent E&P IOC NOC % Independents & NOCs (RHS)

Source: Wood Mackenzie, Deutsche Bank Source: Wood Mackenzie, Deutsche Bank

A gradual increase in the time spent (on aggregate) to drill an appraisal well (figure 8) arguably linked to a general rise in complexity in and around the wellhead,

Figure 8: Average drilling time per well has increased substantially across the decade

30

35

40

45

50

55

60

65

70

75

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008A

vera

ge d

rillin

g da

ys p

er w

ell

Prop

ortio

n of

wel

ls d

rille

d ac

ross

wat

er d

epth

s

2800-3199 2400-2799 2000-2399 1600-1999 1200-1599

800-1199 400-799 Exploration (RHS) Appraisal (RHS) Source: Wood Mackenzie, Deutsche Bank

A counter-argument to our thesis above is that the cumulative experience built by the operator in drilling over the respective acreage could drive higher well flow rates and over time result in fewer wells drilled and within a shorter time frame. We have seen anecdotal evidence of this already in some basins such as Santos, Brazil where IOCs have expressed interest in reducing drilling times going forward. Whilst this dynamic places downside risk on the long run global demand to appraise, for now it appears to be limited to a few regions around the world and specific to only a handful of IOCs.

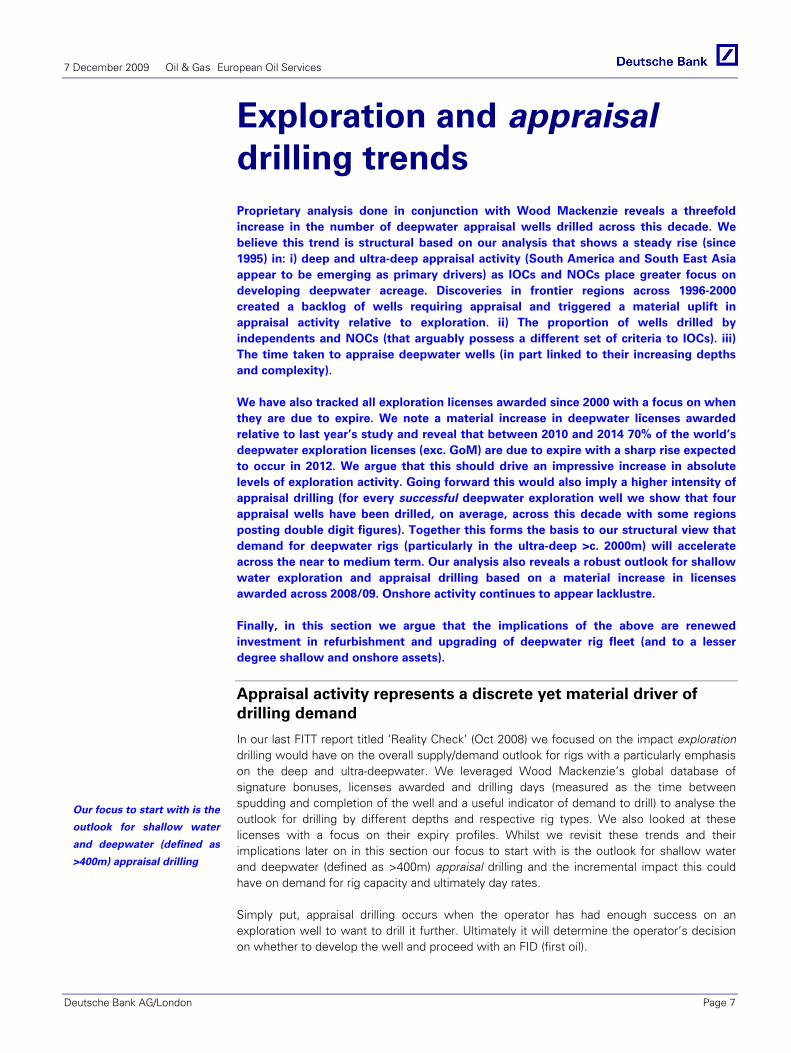

Shallow water and onshore appraisal drilling at parity with exploration Figures 9 and 10 below highlights the volatility in drilling activity for onshore and offshore appraisal drilling with the recent rise fuelled by the increase in commodity prices (we would expect the reverse to occur across 2009 given the sharp drop). Whilst this cyclicality is not surprising, we observe that in contrast to deepwater, the level of appraisal drilling relative to

7 December 2009 Oil & Gas European Oil Services

Deutsche Bank AG/London Page 11

exploration has rarely moved beyond parity. Appendix D shows the aggregate time spent to drill an exploration/ appraisal well.

Figure 9: Shallow water appraisal and successful

exploration wells drilled globally

Figure 10: Onshore appraisal and successful exploration

wells drilled globally

0.4

1.4

2.4

3.4

4.4

5.4

6.4

7.4

8.4

0

100

200

300

400

500

600

700

800

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

App

rais

al/ s

ucce

ssfu

l exp

lora

tion

Wel

ls d

rille

d

Successful exploration Appraisal Appraisal/ successful exploration ratio (RHS)

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

150

200

250

300

350

400

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

App

rais

al/ s

ucce

ssfu

l exp

lora

tion

Wel

ls d

rille

d

Successful exploration Appraisal Appraisal/ successful exploration ratio (RHS)

Source: Wood Mackenzie, Deutsche Bank Source: Wood Mackenzie, Deutsche Bank

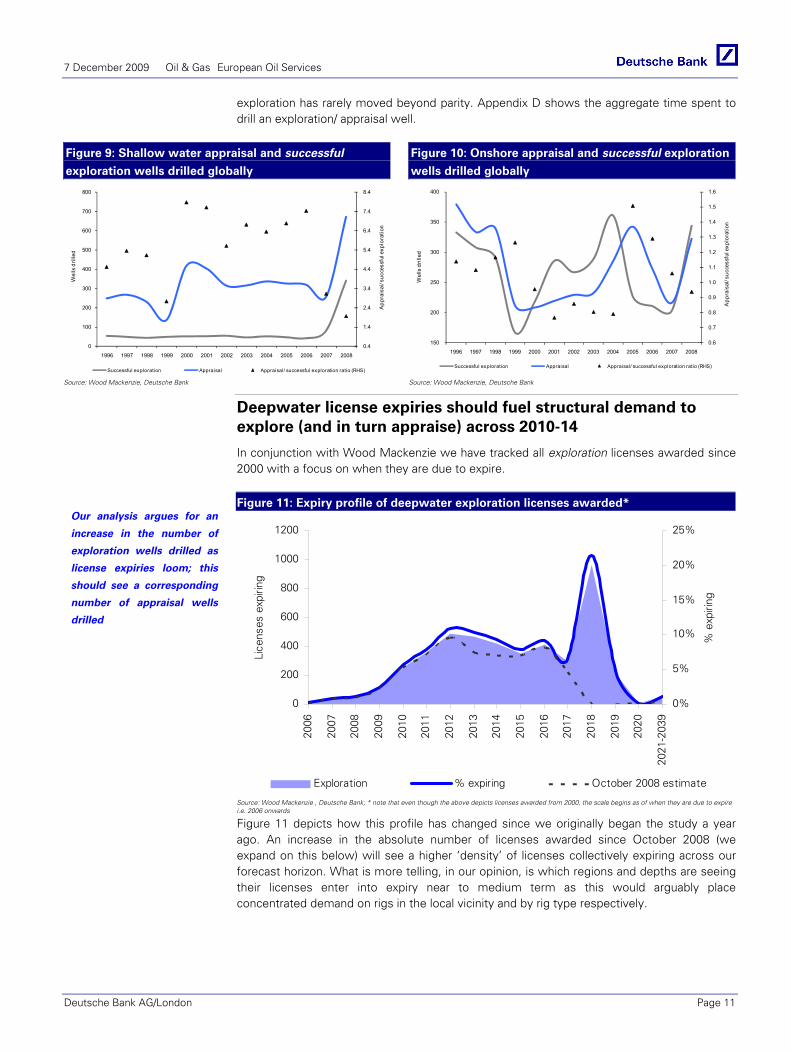

Deepwater license expiries should fuel structural demand to explore (and in turn appraise) across 2010-14

In conjunction with Wood Mackenzie we have tracked all exploration licenses awarded since 2000 with a focus on when they are due to expire.

Figure 11: Expiry profile of deepwater exploration licenses awarded*

0

200

400

600

800

1000

1200

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

-203

9

Lice

nses

exp

iring

0%

5%

10%

15%

20%

25%

% e

xpiri

ng

Exploration % expiring October 2008 estimate

Source: Wood Mackenzie , Deutsche Bank; * note that even though the above depicts licenses awarded from 2000, the scale begins as of when they are due to expire i.e. 2006 onwards

Figure 11 depicts how this profile has changed since we originally began the study a year ago. An increase in the absolute number of licenses awarded since October 2008 (we expand on this below) will see a higher ‘density’ of licenses collectively expiring across our forecast horizon. What is more telling, in our opinion, is which regions and depths are seeing their licenses enter into expiry near to medium term as this would arguably place concentrated demand on rigs in the local vicinity and by rig type respectively.

Our analysis argues for an

increase in the number of

exploration wells drilled as

license expiries loom; this

should see a corresponding

number of appraisal wells

drilled

7 December 2009 Oil & Gas European Oil Services

Page 12 Deutsche Bank AG/London

Figure 12: Given that the majority of the world’s

deepwater rigs* operate outside of GoM…

Figure 13: …we take a closer look at the expiry profile of

deepwater exploration licenses awarded exc. GoM

46%

23%

17%

6%4% 4%

S America GOM E Hemisphere Africa Russia Europe

0

20

40

60

80

100

120

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2020

2021

-203

9

Lice

nses

exp

iring

0%2%4%6%8%

10%12%14%16%18%

% e

xpiri

ng

Exploration % October 2008 estimate

Source: Deutsche Bank, ODS Petrodata; * refers to contracted newbuild deepwater rigs (represents c.17% of all rigs (existing + new) Source: Deutsche Bank, Wood Mackenzie

Between 2010 and 2014, 70% of the world’s deepwater exploration licenses (excluding GoM) are due to expire with an acute rise expected to occur in 2012. We believe the absolute increase in licenses expiring (particularly in 2014) relative to last year’s outlook places additional strain on the world’s deepwater rigs given excess capacity has remained broadly unchanged across the same period.

Figure 14: Breakdown of deepwater exploration licenses expiring by depth excluding

GoM*

0

20

40

60

80

100

120

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2020

2021

- 20

39

Lice

nses

exp

iring

400-799 (Peak 2014) 800-1199 (Peak 2009 & 2014) 1200-1599 (Peak 2009 & 2012)

1600-1999 (Peak 2010, 2012 & 2014) 2000-2399 (Peak 2012) 2400-2799 (Peak 2013)

>2800 (Peak 2009, 2012 & 2015)

Source: Deutsche Bank, Wood Mackenzie, *Given the scale of GoM licenses awards (on average 400/year vs. 40/year elsewhere in the world) and the fact that two thirds of them are below 1500m, we have excluded this region from the chart in order to show clearly the trends occurring in ultra-deep i.e. >c. 2000m

Figure 14 shows that the majority of licenses across all depth intervals are due for expiry over the next five years. The sharp rise in ultra-deepwater (i.e. >c. 2000m) license relinquishments should place additional strain on the demand for these types of rigs (fifth/sixth generation) of which there are far fewer of to relative to shallow and mid-water rigs. We expand on the supply/demand implications of this analysis on day rates in the next section (‘exploration dynamics’).

The sharp rise in ultra-

deepwater (i.e. >c. 2000m)

license expiries should place

additional strain on the demand

for these types of rigs (5th/6th

generation) of which there are

far fewer of to the end of the

decade relative to shallow and

mid-water rigs

7 December 2009 Oil & Gas European Oil Services

Deutsche Bank AG/London Page 13

Figure 15: Breakdown of deepwater exploration licenses expiring by region

0

10

20

30

40

50

60

70

80

90

100

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021-2039

Lice

nses

exp

iring

-200

0

200

400

600

800

1000

1200

Europe (Peak 2009 & 2014) South East Asia (Peak 2012 & 2015)Africa (Peak 2009 & 2013) S America (Peak 2010 & 2012)N America (Peak 2013 & 2017) GOM (Peak 2018) (RHS)

Source: Deutsche Bank , Wood Mackenzie

We draw the following observations from the above:

South America licenses should relinquish between 2010 and 2013. This should see a hike in exploration and subsequent appraisal drilling activity that implies greater demand for rigs near term. Note that the increase in exploration activity triggered by the Tupi find in 2007 de-stabilised the global market for rigs as existing ones gravitated towards South America and un-contracted global rig capacity reduced (mainly driven by new orders placed by Petrobras). Our analysis of all recently built rigs operating globally shows that 27% have been contracted to work in the region over the next five years (detailed in Appendix E).

The majority of the licenses awards in Africa across this decade will expire between 2010 and 2015 which should see operators continue to bid on un-contracted rigs to ensure that their drilling commitments are fulfilled. We note a large number of new licenses that have been awarded over the last 12 months and that broadly 20% of the existing base has been renegotiated (drilling programs extended). Together this has pushed out Africa’s expiry profile towards the middle of next decade (vs. last year’s outlook which showed the majority of licenses in this region expiring by 2012).

Europe (largely represented by the North Sea and Norwegian shelf) should witness a renewed surge in drilling mid to longer term as expiries continue into the next decade (vs. last year’s outlook that showed the majority of licenses relinquishing by 2010)

We show the Gulf of Mexico separately given its much larger scale of licenses awarded vs. the rest of the world (albeit that each license is far smaller in block size). We note that the pressure to drill in this region is less given the first ‘peak’ in expiry does not occur until broadly 2012/13. In addition, oil companies have arguably more flexibility in being able to extend drilling programs here relative to other parts of the world.

Brazil and South East Asia

will emerge as swing

players in the global

demand for deepwater rigs

Europe, Africa and GoM

have all experienced a

material increase in licenses

awarded over the last 12

months. Extensions to

drilling programs have been

most prominent in these

regions. Together this sees

renewed expiries across the

mid term and more regular

peaks

7 December 2009 Oil & Gas European Oil Services

Page 14 Deutsche Bank AG/London

Following a hike in 2009, shallow water and onshore license relinquishments appear to be reducing mid term and with it the pressure to drill ahead of expiry

Figure 16: Expiry profile of shallow water and onshore

licenses awarded from 2000

Figure 17: Breakdown of shallow water and onshore

exploration licenses expiring by region

0

500

1000

1500

2000

2500

3000

2002

2005

2007

2009

2011

2013

2015

2017

2019

2021

-204

0

Cou

nt o

f lic

ense

s ex

pirin

g

0%

5%

10%

15%

20%

25%

% e

xpiri

ng

Exploration % expiring

0

200

400

600

800

1000

1200

2002

2005

2007

2009

2011

2013

2015

2017

2019

2021

-204

0

Lice

nses

exp

iring

0

500

1000

1500

2000

2500

3000

N A

mer

ica

licen

ses

expi

ring

GOM (Peak 2009 & 2013) E Hemisphere (Peak 2008, 2012 & 2015)S America (Peak 2009, 2012 & 2014) Africa (Peak 2010 & 2012)Europe (Peak 2012) Middle East (Peak 2009 & 2011)Russia (Peak 2008, 2011 & 2033) N America (Peak 2022) (RHS)

Source: Deutsche Bank, Wood Mackenzie Source: Deutsche Bank, Wood Mackenzie

Shallow water licenses appear to be generally less periodic in their expiry and having collectively reached a peak this year, the pressure to drill into the end of the decade is reducing. Looking at the regional splits, GoM not surprisingly represents one of the largest constituents of shallow water drilling and is to a large degree driving the downtick in license relinquishments to the end of the decade.

To what extent will volatile macro conditions impact drilling programs being adhered to and the appetite to drill?

What is implicit in the above is that every operator be it oil company or independent will have no choice but to drill in order to fulfil their commitments to the host government. High commodity prices will no doubt influence their appetite to explore and appraise more actively. However, even if oil prices were to fall significantly below current levels the access to reserves (particularly those that offer high net margin barrels) should remain a priority over its near-term commerciality and development. The risk to this assumption is that if credit availability and macro conditions were to worsen, governments themselves (committed to social programs and other fiscal pressures) could in turn pull funding and therefore become more accommodating to drilling programs. This would see license expiries extended easing the pressure for oil companies to explore and appraise.

This decision process would typically be initiated by the host government or National Oil Company. International oil companies that have left their licenses early or exited countries pre-maturely have in the past found it extremely difficult to return. Note it is not uncommon to see them negotiate with their partners including the host government on the grounds that the block acreage yielded very little in the way of discoveries and should not continue to be drilled upon. This is clearly a sensitive discussion but nonetheless one that again removes some of the pressure to remain overly committed to drilling schedules and in particular those that have not been successful.

Overall, whilst there is downside pressure to drill given some uncertainty on the macro environment (particularly in the event that license expiries are extended), we believe that near to medium-term exploration and appraisal drilling programs particularly those in South America, West Africa and South East Asia should be least impacted. This is based on:

1) Wood Mackenzie’s view that these host governments in particular have greater strategic ambition to increase their country’s oil and gas production,

2) IOC’s longer-term production targets are weighted heavily to these regions leaving them with relatively less flexibility to relinquish their licenses,

…the risk to this assumption

is that if macro conditions

deteriorate, then we could

see a reduced willingness

from governments to

explore easing the pressure

on IOCs/NOCs and

independents to drill

Overall, whilst there is

downside pressure to drill

given some uncertainty on

the macro environment

(particularly in the event

that license expiries are

extended), we believe that

near to medium-term

drilling programs

particularly those in South

America, West Africa and

South East Asia should be

least impacted

7 December 2009 Oil & Gas European Oil Services

Deutsche Bank AG/London Page 15

3) Our analysis above that presents a structural case for appraisal drilling that should be sustained at current levels on an absolute basis.

Drilling demand outlook

In this section we model the various datasets provided by Wood Mackenzie’s global exploration database (licenses acreage, signature bonuses, drilling days) to derive an outlook of demand to drill split offshore vs. onshore and also across various depth intervals. The appetite to drill is not homogeneous across the spectrum of depths or indeed onshore and offshore. We combine this analysis with the conclusions derived from our earlier observations on license expiries and outlook for appraisal activity to renew our forecasts for rig day rates offering an alternative to the methodologies adopted by ODS Petrodata and consultancies alike. Figure 18 below shows the increase in deepwater signatures bonuses since the start of the decade. The uplift in shallow water signature bonuses in 2008 is primarily driven by Brazil (Campos and Santos basins) and the US (Alaska Chukchi Sea basin and GoM).

Figure 18: Signature bonuses accelerated across 2006-2008 with an increasing

emphasis on deepwater

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2000 2001 2002 2003 2004 2005 2006 2007 2008

Sig

natu

re b

onus

($m

n)

Onshore Offshore <400m Deepwater >400m

Source: Deutsche Bank, Wood Mackenzie

7 December 2009 Oil & Gas European Oil Services

Page 16 Deutsche Bank AG/London

Figure 19: Shift in licensees awarded (see Appendix O for detailed trends on licenses

awarded) has historically been followed with a similar (directional) change in drilling

days (exploration and appraisal)

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

E

2010

E

2011

E

drill

ing

days

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

licen

ses

(acr

eage

in k

m2)

Onshore Shallow water (0-400m)Deepwater (>400m) licenses awarded (RHS)

Source: Deutsche Bank , Wood Mackenzie; * drilling days is defined as the time drilled between spudding & completion of well.

Shallow water drilling outlook shows mixed signals

Figure 20: Drilling activity in depths 0-199m* Figure 21: Drilling activity in depths 200-399m*

9,000

29,000

49,000

69,000

89,000

109,000

129,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

E

2010

E

2011

E

drilli

ng d

ays

0

50,000

100,000

150,000

200,000

250,000

300,000

licen

ses

(acr

eage

in k

m2)

drilling days licenses awarded

Increase in licenses aw arded expected to fuel drilling activity

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

E

2010

E

2011

E

days

010,00020,00030,00040,00050,00060,00070,00080,00090,000

licen

ses

(acr

eage

in k

m2)

drilling days licenses awarded

Whilst outlook appears lacklustre, activity is expected be driven from a higher base

Source: Wood Mackenzie and Deutsche Bank estimates; *2009 license acreage has yet to be fully updated by WM

Source: Wood Mackenzie and Deutsche Bank estimates; *2009 license acreage has yet to be fully updated by WM

Mid deepwater outlook robust, ultra-deepwater continues to accelerate

Figure 22: Drilling activity in depths 800-1199m* Figure 23: Drilling activity >2000m*

0

5000

10000

15000

20000

25000

30000

35000

40000

0

1000

2000

3000

4000

5000

6000

7000

8000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

E

2010

E

2011

E

Lice

nses

(acr

eage

in k

m2)

days

dril l ing days licenses awarded

Ramp up in licenses awarded across 2007-08 should see an equivalent increase in drilling act ivity across 2010/11 vs. previous years; key regional drivers are South East Asia and Brazil

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

E

2010

E

2011

E

Lice

nses

(acr

eage

in k

m2)

Day

s

Drilling days Licenses awarded

Ultra-deepwater ilicens awards has been a key driver in this unpredented hike across 2006-09. This should see an equivalent increase in drilling activity well into the next decade

Source: Deutsche Bank & Wood Mackenzie; *2009 license acreage has yet to be fully updated by WM Source Deutsche Bank & Wood Mackenzie; *2009 license acreage has yet to be fully updated by WM

7 December 2009 Oil & Gas European Oil Services

Deutsche Bank AG/London Page 17

Figure 24: Deepwater drilling activity will continue to intensify in depths >2000m

0

5000

10000

15000

20000

25000

30000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009E 2010E 2011E

Dee

pwat

er d

rillin

g da

ys

> 2400 2000-2399 1600-1999 1200-1599 800-1199 400-799

Structural shift towards ultra deep water depths in absolute and relative terms

Source: Wood Mackenzie; Deutsche Bank

Onshore drilling outlook appears lacklustre with some support from Middle East and South East Asia

Figure 25: Onshore activity

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

E

2010

E

2011

E

licen

ses

(acg

reag

e in

km

2)

days

drilling days licenses awarded

Source: Wood Mackenzie; Deutsche Bank

Positive implications for rig construction services

Our outlook of rig construction spend (newbuild, upgrade and refurbishment) is based on what has already been flagged by the contractors (drillers and E&C companies) and the degree of additional investment that could materialise. Despite the number of deepwater floater new builds coming on-stream, the relative lack of liquidity here (only c. 40% are accessible vs. 90% for jack-ups) against accelerated drilling activity particularly in the ultra-deepwater suggests that the demand for newbuilds will continue albeit at a reduced pace and scale vs. 2006-08.

This is in contrast to the jack-up rig market (offshore and onshore) that appears readily accessible and in turn should see a more severe decline in newbuild investment vs. 2006-08. Notable exceptions here that place upside pressure particularly on the rate of incremental jack-up rig spend include:

The demand for premium jack-up rigs capable of working in harsh environments as the global incremental supply of oil continues to be sourced from more technically challenging prospects (e.g. in the FSU).

Our outlook for drilling

demand points to a material

rise in ultra-deepwater

drilling. By 2011 we expect

this end of the depth

spectrum to represent 20%

of deepwater drilling days

(vs. 14% 2007)

7 December 2009 Oil & Gas European Oil Services

Page 18 Deutsche Bank AG/London

National oil company investment in rig newbuilds. Figures 26 and 27 show actual capex committed to new builds between 2009 and 2012 sourced by region and origin of the operator; i.e., NOC vs. IOC.

Figure 26: Rig new build spend (2009-12E) by region Figure 27: Rig new build spend (2009-12E) by NOC/IOC

Total 2009-12E capex = $67.5 bn

Asia 19%

Norw ay 23%

South America 19%

Africa1%

US27%

Europe10%

Middle East1%

Total 2009-12E capex = $67.5 bn

IOC (i.e private or publicly listed

drillers)40%

NOC60%

Source: Deutsche Bank, ODS Petrodata Source: Deutsche Bank, ODS Petrodata

On comparing the above to the split of new build spend that occurred between 2003 and 2006, we note that there has been a gradual shift from the traditional investors of rig new builds, such as the US and Europe towards South America, Middle East and Asia. This move has been underpinned by greater participation of NOCs in rig construction and in turn refurbishment/upgrades. Confirming this is our analysis done in conjunction with Wood Mackenzie which shows direct investment by the NOCs in drilling since 1995 (Appendix F).

Robust drilling outlook will continue to support rig upgrade and refurbishment investment particularly for those operating in deepwater This sub sector of rig construction services focuses on extending the life of a rig whether it be through maintenance and/or or extra kitting of equipment to improve its technical capabilities. Volatile commodity prices and general lack of macro visibility has put many refurbishment and upgrade programs on hold, as operators prefer to ‘cold or warm’ stack rigs than upgrade existing fleet. This has been most pertinent within the shallow water drilling segment; deepwater refurbishment has been relatively less impacted. Going forward, we believe that as macro conditions stabilise, we should see renewed interest in rig construction services. Forward demand will be directly correlated to:

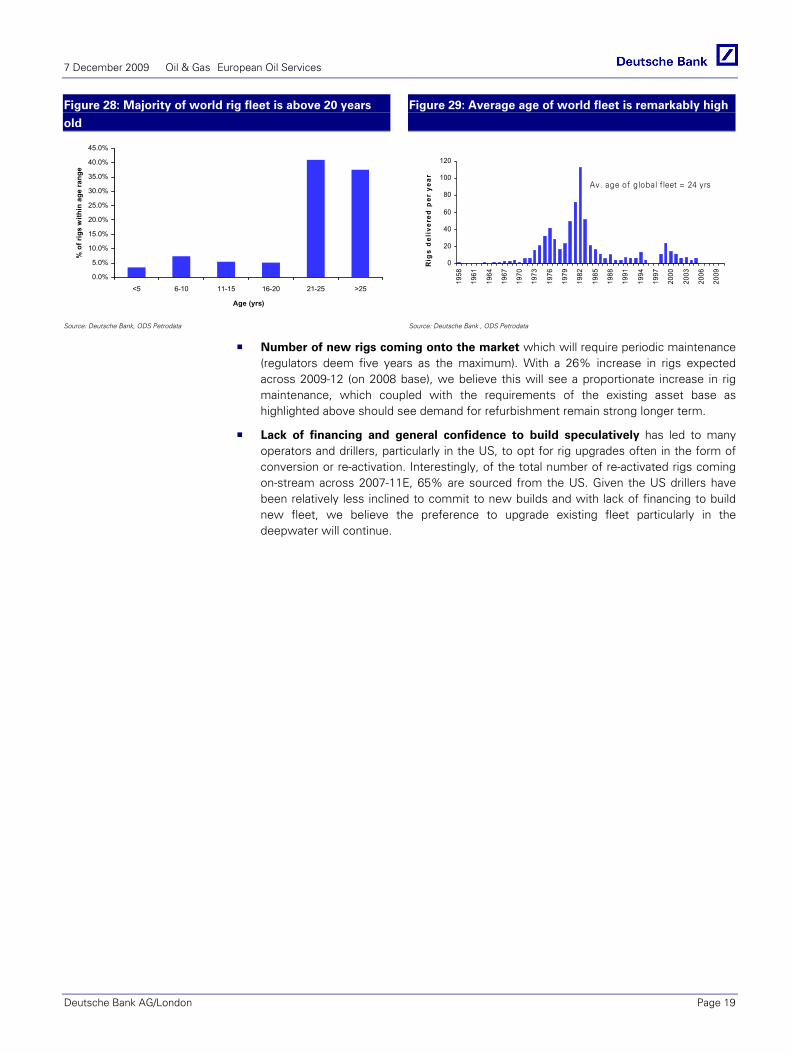

Rig attrition. Figures 28 and 29 show that 38% of global rig capacity is above 25-years-old (typical rig run life is 30 years) suggesting that over the next 10 years, these rigs will require some degree of maintenance. This could vary from refurbishment e.g. replacement of corroded parts (basically returning the rig to its original efficiency and capability thus extending its life) through to enhancement of the rig in order to extract more value from it. It is worth noting that we expect a more pro-active maintenance approach in contrast to earlier parts of the cycle where underinvestment i.e., the bare minimum was accepted (drillers, keen to exploit the strong commodity environment, kept maintenance time as low as possible).

7 December 2009 Oil & Gas European Oil Services

Deutsche Bank AG/London Page 19

Figure 28: Majority of world rig fleet is above 20 years

old

Figure 29: Average age of world fleet is remarkably high

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

<5 6-10 11-15 16-20 21-25 >25

Age (yrs)

% o

f rig

s w

ithin

age

ran

ge

0

20

40

60

80

100

120

1958

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

Rig

s d

eliv

ered

per

yea

r

Av. age of global fleet = 24 yrs

Source: Deutsche Bank, ODS Petrodata

Source: Deutsche Bank , ODS Petrodata

Number of new rigs coming onto the market which will require periodic maintenance (regulators deem five years as the maximum). With a 26% increase in rigs expected across 2009-12 (on 2008 base), we believe this will see a proportionate increase in rig maintenance, which coupled with the requirements of the existing asset base as highlighted above should see demand for refurbishment remain strong longer term.

Lack of financing and general confidence to build speculatively has led to many operators and drillers, particularly in the US, to opt for rig upgrades often in the form of conversion or re-activation. Interestingly, of the total number of re-activated rigs coming on-stream across 2007-11E, 65% are sourced from the US. Given the US drillers have been relatively less inclined to commit to new builds and with lack of financing to build new fleet, we believe the preference to upgrade existing fleet particularly in the deepwater will continue.

7 December 2009 Oil & Gas European Oil Services

Page 20 Deutsche Bank AG/London

Exploration industry dynamics and relative profitability Our analysis shows that deepwater global rig liquidity has increased from 26% (2008-12E) to 40% (2009-12E) and from 70% to 90% in the shallow water segment (current newbuild schedules suggests a 19% increase in global rig capacity vs. current levels). In this section we marry the demand implications of our exploration and appraisal drilling outlook against what appears to be a well supplied market to determine how day rates will evolve by rig class across the near to medium term.

We believe the ultra deepwater market will demonstrate the best performance as supply/demand fundamentals are expected to tighten again beyond 2010. Having fallen from a record level of $700k/day in 2008 and stabilised around $500k/day, we expect rig rates to rise from 2010 (we forecast $600k/day by 2011) as license expiries loom and exploration/appraisal drilling accelerates. With this in mind, we believe incremental demand for best in class assets (younger, latest generation of rigs) will re-shape the deepwater market as new rig owners gradually displace market share traditionally held by more mature drillers (predominantly US based). We expect downward pressure on rig day rates operating in depths lower than 2000m given the greater availability of (older generation) mid-water fleet partly offset by a robust demand outlook. Shallower water day rates should continue to fall but stabilise towards structurally higher levels than mid-cycle. Elsewhere in the exploration complex, rig construction services emerge as an attractive niche particularly in the Middle East.

Drilling services: global rig rate outlook

Analysis and prediction of rig rates will be based on a number of continually changing variables that affect the operators and drillers’ perception of how the market will move. Structural factors that influence spot (or leading edge) and long-term (or contracted) rig rates include:

Outlook of exploration and appraisal drilling demand

Rate of rig replacement defined as the degree with which incremental rig capacity (confirmed new builds and upgrades) will be offset by ageing fleet due to be taken off-stream

Liquidity of the rig market - operators’ willingness to sign up rigs at a premium or discount to the current leading edge is, in part, based on the accessibility of incremental supply, i.e. the proportion of rigs that are not yet locked up into long-term contracts.

We base our short- to medium-term rig rate forecasts on our understanding of the above supply/demand dynamics. Macro and geopolitical factors influencing rig rates include:

Oil and gas prices (higher prices will drive appetite to drill and monetise reserves quickly)

The condition of the global economy and level of GDP growth anticipated worldwide and at the regional level

We believe our near- to mid-term day rate outlook remains intact at sub $70/bbl oil on a sustained basis and against deteriorating macro conditions. This is given the bottom up nature of our demand forecast (linked to the structural dynamics detailed in the last section).

Our day rate model is

demand driven and

dependent on our outlook

for exploration and appraisal

activity; analysing the

degree of supply coming on-

stream and more

importantly operator’s

ability to access spare

capacity, provides a more

complete picture with which

to forecast future day rates

7 December 2009 Oil & Gas European Oil Services

Deutsche Bank AG/London Page 21

DB day rate model

First we analyse supply.... Whilst we have not quantified the impact of supply on day rates we address below,

albeit qualitatively, the extent to which capacity creep could effect our forecast, if at all. Figures 30-33 show the timing, complexity and degree of incremental rig capacity (already commissioned) expected to come on-stream in the medium term. It is worth noting that rigs capable of drilling in deep and ultra deep waters are also operable in mid and shallower waters. Therefore during periods of low utilisation, owners of fifth/sixth generation rigs (semi-submersibles or drillships) may choose to charter them out in reduced depths.

Figure 30: Latest ODS figures suggest a 19% increase in

global capacity by 2012 vs. 2009

Figure 31: Drillships; 73% increase in supply expected

(depths greater than 7500ft)

0

10

20

30

40

50

60

70

2009 2010 2011 2012

Num

ber o

f rig

s

Drillship Jackup Semisubmersible Tenders

155 rigs are currently planned tocome on-stream across 09-12E

0

5

10

15

20

25

30

35

0-2999 3000-4999 5000-7499 7500-9999 >=10000

depth (ft)

Num

ber o

f rig

s

2009 2010 2011 2012

35 Drillships are planned to come onstream across 09-12E

Source: Deutsche Bank and ODS Petrodata Source: Deutsche Bank and ODS Petrodata

Figure 32: Semi-submersibles; 20% increase in supply

expected (bulk occurring at depths >7500ft)

Figure 33: Jackups; 13% increase in supply expected

(bulk occurring at depths b/w 300-400ft)

0

5

10

15

20

25

30

0-2999 3000-4999 5000-7499 7500-9999 >=10000

depth (ft)

Num

ber o

f rig

s

2009 2010 2011 2012

45 Semisubmersible rigs are planned to come onstream across 09-12E

0

10

20

30

40

50

60

0-199 200-300 300-400 >=400

Num

ber o

f rig

s

2009 2010 2011 2012

69 Jackups rigs are planned to come on stream across 09-12E

Source: Deutsche Bank and ODS Petrodata Source: Deutsche Bank and ODS Petrodata

Whilst the rig market appears well supplied into the end of the decade, we highlight below counter dynamics that should remove some of the downside risk on rig utilisations.

Rig attrition. Of the expected 19% increase in global capacity, ODS Petrodata estimates that up to a third of that could potentially be ‘soaked up’ in replacing older rigs forced off stream over the next 5-10 years.

Lack of financing and general confidence to build speculatively. Lack of credit availability and the general reluctance to build new rigs has completely removed speculative capacity this year. Whilst we believe deepwater rigs will continue to be built it will be at depressed pace and scale relative to 2006-09.

7 December 2009 Oil & Gas European Oil Services

Page 22 Deutsche Bank AG/London

Rig liquidity. Figures 34 and 35 show the proportion of new builds that have yet to be contracted.

Figure 34: Jackup new build spare capacity 2009-12E

Figure 35: Semi-submersible and drillship new build

spare capacity 2009-12E contracted Jackups

10%

Number of uncontracted

Jackups90%

Uncontracted semis and drillships,

40%

Contracted semis and drillships,

60%

Source: Deutsche Bank ,ODS Petrodata Source: Deutsche Bank, ODS Petrodata

Despite the number of deepwater floater new builds coming on-stream, the relative lack of liquidity here (c. 40% are accessible) suggests that the market will continue to remain tight in the medium term all else being equal. Conversely, the jack-up rig market (offshore and onshore) appears readily accessible. As the new builds come on stream, we believe this will inevitably place downward pressure on utilisation, assuming that jack-up demand does not vary significantly from current levels.

With regards to the existing rigs already under contract (that could threaten to increase spare capacity dramatically) analysis of the world’s contracted deepwater rigs (detailed further in the next section) shows that the average term length on rigs signed across 2007/08 (>90% of the world’s rigs were re-negotiated during this period) is four years (jackups between 0.5-2 years). Our point here is that spare capacity of existing rigs, at least those drilling in deepwater will not free up before 2011/2012. We believe this should be more than offset by a significant expected up-tick in drilling demand across the same period keeping supply/demand fundamentals robust into the first half of the next decade.