fixed income investors presentation · numerous factors, including those reflected in the form...

TRANSCRIPT

FIXED INCOME INVESTORS PRESENTATIONHere to help you prosper

Q1 2018

2

Important information

In addition to the financial information prepared under International Financial Reporting Standards (“IFRS”), this presentation includes certain alternative performance measures (“APMs”) as

defined in the Guidelines on Alternative Performance Measures issued by the European Securities and Markets Authority on 5 October 2015 (ESMA/2015/1415es) as well as non-IFRS measures

(“Non-IFRS Measures”). The APMs and Non-IFRS Measures are performance measures that have been calculated using the financial information from the Santander Group but that are not

defined or detailed in the applicable financial information framework and therefore have neither been audited nor are capable of being completely audited. These APMs and Non-IFRS Measures

are been used to allow for a better understanding of the financial performance of the Santander Group but should be considered only as additional information and in no case as a replacement of

the financial information prepared under IFRS. Moreover, the way the Santander Group defines and calculates these APMs and Non-IFRS Measures may differ to the way these are calculated by

other companies that use similar measures, and therefore they may not be comparable. For further details of the APMs and Non-IFRS Measures used, including its definition or a reconciliation

between any applicable management indicators and the financial data presented in the consolidated financial statements prepared under IFRS, please see 2018 1Q Financial Report, published as

Relevant Fact on 24 April 2018, Section 26 of the Documento de Registro de Acciones for Banco Santander, S.A. (“Santander”) filed with the Spanish Securities Exchange Commission (the

“CNMV”) on July 4, 2017 (the “Share Registration Document”) and Item 3A of the Annual Report on Form 20-F filed with the U.S. Securities and Exchange Commission of the United States of

America (the “SEC”) on March 31, 2018 (the “Form 20-F”). These documents are available on Santander’s website (www.bancosantander.com).

The businesses included in each of our geographic segments and the accounting principles under which their results are presented here may differ from the included businesses and local

applicable accounting principles of our public subsidiaries in such geographies. Accordingly, the results of operations and trends shown for our geographic segments may differ materially from

those of such subsidiaries.

Santander cautions that this presentation contains statements that constitute “forward-looking statements” within the meaning of the U.S. Private Securities Litigation Reform Act of 1995. Forward-

looking statements may be identified by words such as “expect”, “project”, “anticipate”, “should”, “intend”, “probability”, “risk”, “VaR”, “RRAC”, “RoRWA”, “TNAV”, “target”, “goal”, “objective”,

“estimate”, “future” and similar expressions. These forward-looking statements are found in various places throughout this presentation and include, without limitation, statements concerning our

future business development and economic performance and our shareholder remuneration policy. While these forward-looking statements represent our judgment and future expectations

concerning the development of our business, a number of risks, uncertainties and other important factors could cause actual developments and results to differ materially from our expectations.

These factors include, but are not limited to: (1) general market, macro-economic, industry, governmental and regulatory trends; (2) movements in lo¬cal and international securities markets,

currency exchange rates and interest rates; (3) competitive pressures; (4) technological developments; and (5) changes in the financial position or credit worthiness of our customers, obligors and

counterparties. Numerous factors, including those reflected in the Form 20-F– under “Key Information-Risk Factors”- and in the Share Registration Document–under “Factores de Riesgo”- could

affect the future results of Santander and could result in other results deviating materially from those anticipated in the forward-looking statements. Other unknown or unpredictable factors could

cause actual results to differ materially from those in the forward-looking statements.

Forward-looking statements speak only as of the date of this presentation and are based on the knowledge, information available and views taken on such date; such knowledge, information and

views may change at any time. Santander does not undertake any obligation to update or revise any forward-looking statement, whether as a result of new information, future events or otherwise.

3

Important information

The information contained in this presentation is subject to, and must be read in conjunction with, all other publicly available information, including, where relevant any fuller

disclosure document published by Santander. Any person at any time acquiring securities must do so only on the basis of such person’s own judgment as to the merits or the

suitability of the securities for its purpose and only on such information as is contained in such public information having taken all such professional or other advice as it

considers necessary or appropriate in the circumstances and not in reliance on the information contained in this presentation. No investment activity should be undertaken on

the basis of the information contained in this presentation. In making this presentation available Santander gives no advice and makes no recommendation to buy, sell or

otherwise deal in shares in Santander or in any other securities or investments whatsoever.

Neither this presentation nor any of the information contained therein constitutes an offer to sell or the solicitation of an offer to buy any securities. No offering of securities

shall be made in the United States except pursuant to registration under the U.S. Securities Act of 1933, as amended, or an exemption therefrom. Nothing contained in this

presentation is intended to constitute an invitation or inducement to engage in investment activity for the purposes of the prohibition on financial promotion in the U.K.

Financial Services and Markets Act 2000.

Note: Statements as to historical performance or financial accretion are not intended to mean that future performance, share price or future earnings (including earnings per

share) for any period will necessarily match or exceed those of any prior year. Nothing in this presentation should be construed as a profit forecast.

4

1. Markets and Macroeconomic Environment

2. Santander Business Model & Strategy

3. Capital

4. Asset Quality

5. TLAC Requirements, Liquidity and Funding

6. Concluding Remarks

7. Appendix

UK loan portfolio: Mortgage and Corporate RE

8. Glossary

CONTENT

Markets and

Macroeconomic

Environment

01

6

Markets and Macroeconomic Environment

A favourable macroeconomic and financial environment expected in 2018

World Output 3.9%

Euro Area 2.4%

UK 1.6%

United States 2.9%

Latin America 2.0%

Mexico 2.3%

Brazil 2.3%

(1) World Economic Outlook, April 2018

IMF 2018 GDP Outlook1

Growth in developing and mature markets

Better fundamentals should lead to more resilient and

stable growth cycles

Contained inflation

Interest rate rises will be gradual (2018/2019)

Lower regulatory uncertainty

MATURE MARKETSCyclical macro acceleration

(53% attributable profit)

DEVELOPING MARKETSStructural growth remains strong

(47% attributable profit)

Santander is well-positioned for growth due to its balanced geographic diversification

7

Markets and Macroeconomic Environment

The expansionary cycle in the Spanish economy is expected to continue, backed by employment creation, higher consumption and real estate & investment recovery

Source: Santander Research Department, Bank of Spain

19.617.2

15.514.2

12.6

2016 2017 2018 (e) 2019 (e) 2020 (e)

Annual GDP Growth

Housing pricesUnemployment rate

1.4

3.4 3.33.1

2.9

2.42.1

1.4

2.01.8

2.5 2.42.0

1.7

2014 2015 2016 2017 2018 (e) 2019 (e) 2020 (e)

Spain

Eurozone

Real, %

%

50

60

70

80

90

100

110

Q4'01 Q4'03 Q4'05 Q4'07 Q4'09 Q4'11 Q4'13 Q4'15

Base 100: Q3’07 “peak”

Price index per m2 in real terms

8

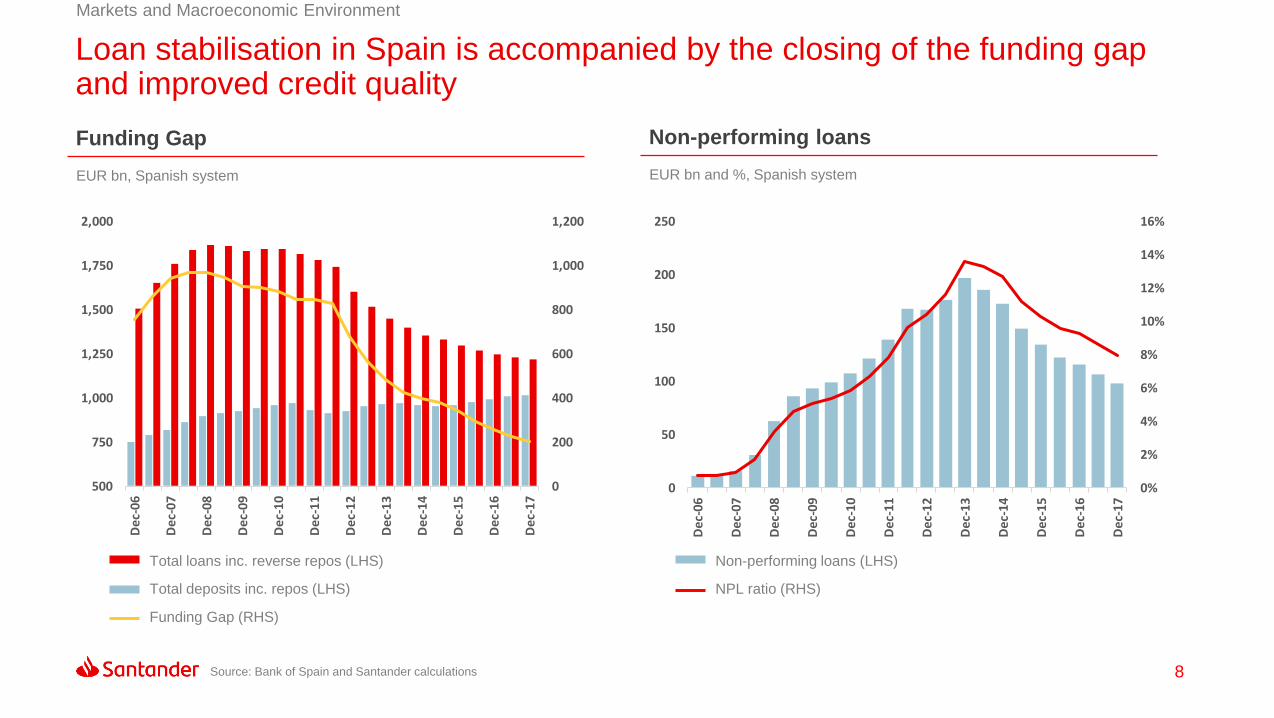

Markets and Macroeconomic Environment

Loan stabilisation in Spain is accompanied by the closing of the funding gap and improved credit quality

Non-performing loans

EUR bn and %, Spanish system

Funding Gap

EUR bn, Spanish system

0

200

400

600

800

1,000

1,200

500

750

1,000

1,250

1,500

1,750

2,000

De

c-0

6

De

c-0

7

De

c-0

8

De

c-0

9

De

c-1

0

De

c-1

1

De

c-1

2

De

c-1

3

De

c-1

4

De

c-1

5

De

c-1

6

De

c-1

7

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

50

100

150

200

250

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Dec

-16

Dec

-17

Total loans inc. reverse repos (LHS)

Total deposits inc. repos (LHS)

Funding Gap (RHS)

Source: Bank of Spain and Santander calculations

Non-performing loans (LHS)

NPL ratio (RHS)

Santander

Business Model &

Strategy

02

10

Our business model has unique competitive advantages

Santander Business Model & Strategy

Customers distributed across geographiesA differential business model

1

2

3

Serving 139 million customers with in-market

SCALE in our core markets drives profitable

growth

Our geographic diversification generates

PREDICTABLE GROWTH in profits,

resulting in lower capital needs

The subsidiary model, with a strong culture of

INNOVATION and collaboration, drives

efficiency and service excellence

Spain 12%

SCF 14%

Poland 3%

Portugal 4%

UK 18%

Brazil 28%

Mexico 11%

Chile 3%

Argentina 2%USA 4%Others 1%

139Million customers

Mar-18

11

Other individuals; 10%

Home mortgages;

36%

Consumer; 16%

SMEs; 11%

Corporates; 17%

GCB; 10%

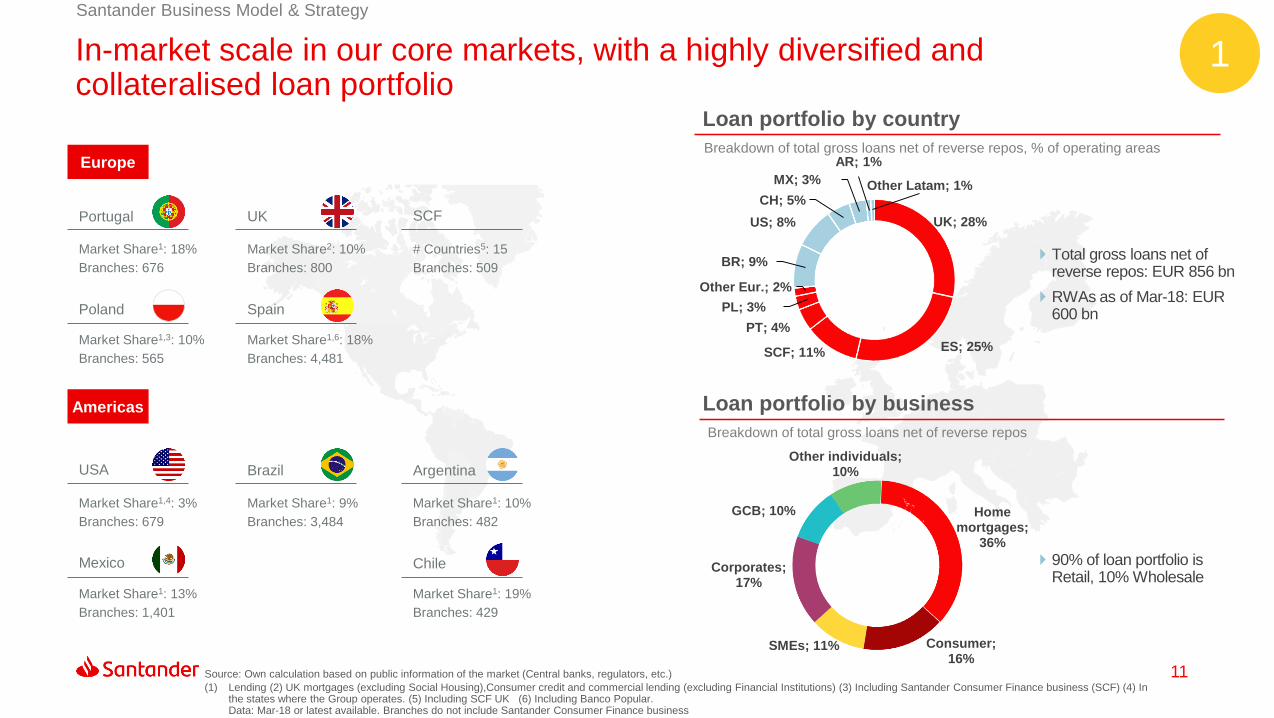

In-market scale in our core markets, with a highly diversified and collateralised loan portfolio

Source: Own calculation based on public information of the market (Central banks, regulators, etc.)

(1) Lending (2) UK mortgages (excluding Social Housing),Consumer credit and commercial lending (excluding Financial Institutions) (3) Including Santander Consumer Finance business (SCF) (4) In the states where the Group operates. (5) Including SCF UK (6) Including Banco Popular. Data: Mar-18 or latest available. Branches do not include Santander Consumer Finance business

Santander Business Model & Strategy

1

USA

Market Share1,4: 3%

Branches: 679

Argentina

Market Share1: 10%

Branches: 482

Brazil

Market Share1: 9%

Branches: 3,484

Market Share1: 19%

Branches: 429

Chile

Market Share1: 13%

Branches: 1,401

Mexico

Americas

Market Share1: 18%

Branches: 676

Portugal UK

Market Share2: 10%

Branches: 800

Market Share1,6: 18%

Branches: 4,481

Spain

Market Share1,3: 10%

Branches: 565

Poland

# Countries5: 15

Branches: 509

SCF

Europe

Loan portfolio by country

UK; 28%

ES; 25%SCF; 11%

PT; 4%

PL; 3%

Other Eur.; 2%

BR; 9%

US; 8%

CH; 5%

MX; 3%

AR; 1%

Other Latam; 1%

Breakdown of total gross loans net of reverse repos, % of operating areas

Total gross loans net of reverse repos: EUR 856 bn

RWAs as of Mar-18: EUR 600 bn

Loan portfolio by business

Breakdown of total gross loans net of reverse repos

90% of loan portfolio is Retail, 10% Wholesale

12

High and recurring pre-provision profit leads to resilient growth through the economic cycle…

PPP/Loans well above most European peers1Resilient profit generation throughout the cycle

Group attributable profit, EUR bn

1. European peers include: Barclays, BBVA, BNP, Deutsche, HSBC, ING, Intesa Sanpaolo, Lloyds, RBS, Société Générale, Standard Chartered, UBS and Unicredit

%, Q1’18, Santander calculations

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

7.6

9.1 8.9 8.9

8.2

5.3

2.3

4.2

5.8 6.0 6.26.6

Santander Business Model & Strategy

2

0.0

0.5

1.2

1.4

1.5

1.6

1.8

1.8

1.9

2.1

2.5

2.5

3.0

3.4

13

… and to stable and predictable growth

Predictable results with the lowest volatility among peers coupled with growth in earnings

1. Source: Bloomberg, with GAAP Criteria. Note: Standard deviation of the quarterly EPS starting from the first available data since Jan’99.

Quarterly reported EPS volatility1

4x10x1x3x4x3x6x-1x-1x3x-2x

Net income increase 1999-2017

717% 335%

128%

112%

91%

79%

51%45%

9%

44%

33%

Santander Business Model & Strategy

2

1499%

93%

76%

75%

74%

68%

65%

64%

61%

60%

60%

58%

58%

54%

53%

49%

48%

47%

UK

EU

EU

EU

EU

UK

US

UK

UK

EU

US

US

US

EU

UK

EU

EU

Operational excellence: allowing us to improve both customer satisfaction and efficiency

…with better cost-to-income than peers1Improving customer satisfaction…

Cost-to-income, Mar-18# of countries in Top 3 for customer satisfaction, Dec-17

5

7

2015 2017

>75% of PBT among

Top 3 in customer

satisfaction

18pp

better than

peer avg.

Source: Company data and Bloomberg

(1) Note: Peers included are Bank of America, Barclays, BBVA, BNP Paribas, Citibank, Deutsche, HSBC, ING, Intesa Sanpaolo, JP Morgan, Lloyds, RBS, Société Générale,

Standard Chartered, UBS, Unicredit and Wells Fargo

Santander Business Model & Strategy

3

15

The 2018 strategy is based around several different pillars

Santander Business Model & Strategy

2018Improve key

metrics

Improve

quality of

results

Strengthen

franchises

Grow

sustainably

Meet Group

objectives

Continue

commercial and

digital

transformation

16

Our commercial and digital transformation is supported by new business models, products and branches…

Santander Business Model & Strategy

Commercial

and digital

transformation

Launch of

Digital On-boarding

and new

Workcafés

First fully digital

bank

FX transfers using

Blockchain

Superdigital

Banking without a

bank

Leader in mobile

payments

Image Credit: Cymon Taylor / RM Sotheby’s

Supertankers

Speedboats

Our Supertankers are being

transformed into digital banks

Profitable growth

Independent Global Platforms.

Led by independent CEOs but

sponsored by Country Heads

Start-up model + Group support

17

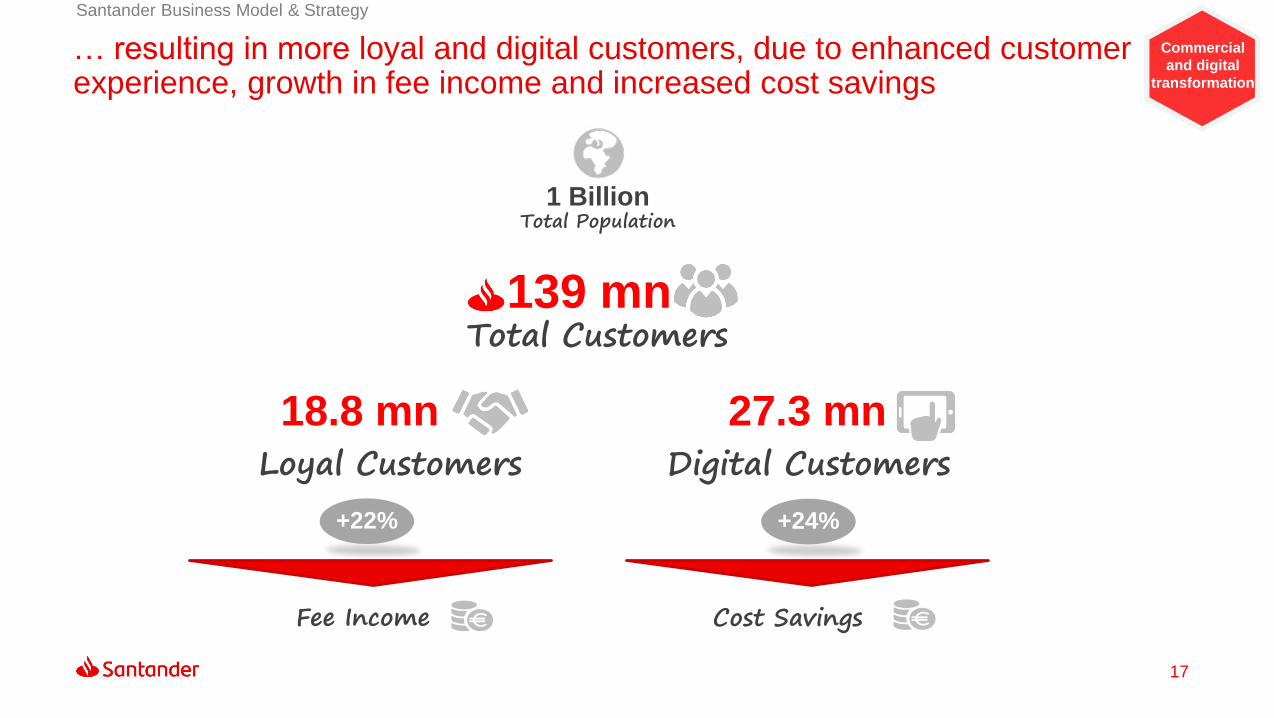

… resulting in more loyal and digital customers, due to enhanced customer experience, growth in fee income and increased cost savings

Santander Business Model & Strategy

Commercial

and digital

transformation

1 BillionTotal Population

Fee Income

+22% +24%

139 mnTotal Customers

18.8 mn 27.3 mn

Cost Savings

Loyal Customers Digital Customers

18

Santander Business Model & Strategy

Meet

Group

objectives2018 Targets2017

Loyal customers (mn) 18.617.3

Digital customers (mn) 3025.4

Fee income1 ~10% CAGR 2015-18

13%

Cost of credit risk 1.2% 2015-18 average

1.07%

Cost-to-income 45-47%47.4%

EPS (EUR) Double digit growth0.40

DPS (EUR)2 Yearly increase0.22

FL CET1 >11%10.84%

RoTE >11.5%

(1) % change in constant euros

(2) Total dividends charged to 2018 earnings are subject to the Board and AGM approval

(3) Underlying RoTE: 11.8%

We are on track to meet our 2018 targets

Q1’18

18.8

27.3

14%

1.04%

47.4%

0.120(Q1’18)

0.23

11.00%

12.4%

Positive trends makes us confident to deliver solid results in 2018

10.4%3

19

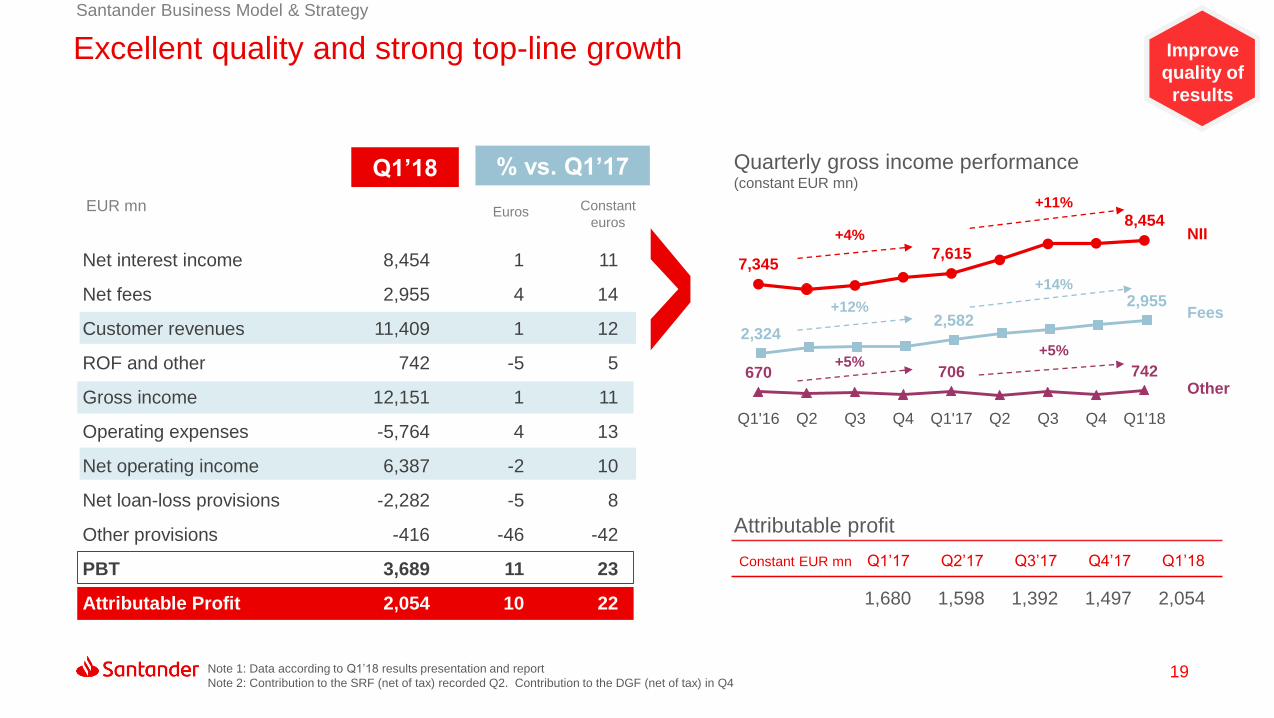

2,3242,582

2,955

7,3457,615

8,454

670 706 742

Q1'16 Q2 Q3 Q4 Q1'17 Q2 Q3 Q4 Q1'18

Excellent quality and strong top-line growth

NII

Fees

Other

Quarterly gross income performance (constant EUR mn)

Note 1: Data according to Q1’18 results presentation and report

Note 2: Contribution to the SRF (net of tax) recorded Q2. Contribution to the DGF (net of tax) in Q4

Net interest income 8,454 1 11

Net fees 2,955 4 14

Customer revenues 11,409 1 12

ROF and other 742 -5 5

Gross income 12,151 1 11

Operating expenses -5,764 4 13

Net operating income 6,387 -2 10

Net loan-loss provisions -2,282 -5 8

Other provisions -416 -46 -42

PBT 3,689 11 23

Attributable Profit 2,054 10 22

EUR mn Constant

eurosEuros

Q1’18 % vs. Q1’17

1,680 1,598 1,392 1,497 2,054

Attributable profit

Santander Business Model & Strategy

Constant EUR mn Q1’17 Q2’17 Q3’17 Q4’17 Q1’18

Improve

quality of

results

+4%

+11%

+12%

+14%

+5%+5%

20

Attributable profit growth is driven by most of our markets

Santander Business Model & Strategy

Grow

sustainably

Attributable profit by geography

EUR mn and % change vs Q1’17 in constant euros

+27%

-21%

+14%

+8%

+1%

+52%

-11%

+3%

+26%

+4%

677

455

323

320

175

151

127

125

66

63

Attributable profit1

(1) Excluding Corporate Centre and Real Estate Activity Spain

51%

UK; 13%

Spain; 18%

SCF; 13%

Portugal; 5%Poland;

2%

USA; 5%

Mexico; 7%

Brazil; 27%

Chile; 6%

Argentina; 3%Other Latam; 1%

EuropeAmericas

49%

Q1’18

21

Better than peer results across key metrics accompanied by improved asset quality

Santander Business Model & Strategy

Improve

key metrics

RoTE

Santander Mar-18, Peers Dec-17

12.4%

9%

Global Peers

47.4%

66%

Global Peers

(1) Banco Popular integration (2) IFRS 9 application

Group’s Asset QualityEfficiency Ratio

Mar-18

Coverage ratio

75

6866 65

70

NPL ratio

3.74

5.37

4.24 4.08 4.02

Mar-17 Jun-17 Sep-17 Dec-17 Mar-18

1.17%

1.04%

Q1'17 Q1'18

Cost of Credit

%

1 2

22

Main opportunities to strengthen growth in our franchises

Popular acquisition: positive delivery on a transformational

deal

SCF: Consolidate our leadership while increasing penetration

in personal loans via digital transformation

UK: Well positioned as the only full-service scale challenger

despite uncertain economic environment

USA: Efficiently relaunching our commercial banking while

improving the risk-return-profile of SCUSA

GCB: Expanding international / trade business &

collaboration revenues

Wealth Management: Strengthen our Asset Management &

Private Banking Unit

Poland: Most profitable bank among peers. Reinforce

presence with Deutsche Bank acquisition

Brazil: We have built a great and improving bank with

sustainable profit and solid organic growth

Argentina: Potential to grow & consolidate market

leadership

Mexico: High potential growth in a stable and largely

untapped market

Chile: Leaders in a stable growth and profitable market

SCF

GCB

WM

Diversification between developed and

emerging markets provides stability as

well as growth opportunities

Santander Business Model & Strategy

Strengthen

franchises

Capital

03

24

11.00%10.91%

10.05%

10.55%

10.84%

Consistent progress on reaching our target of FL CET1 >11% in 2018

Capital

+16 bps

+9 bps +8 bps

-1 bp

Fully loaded CET11

%

(1) 2018 data calculated using IFRS 9 transitory arrangements. Fully loaded IFRS 9 impact would be -23 bps (2) Blackstone (+10 bps); Metrovacesa (-2 bps)

(3) AFS and regulatory impacts (4) Capital destroyed in adverse scenario in bps, EBA stress test 2016

2 3

FL Total capital ratio: 14.66%

FL Leverage ratio: 5.1%

RoRWA : 1.59%

Q1 20181

14.10%

5.0%

1.48%

Q1 2017

0.56%

0.1%

0.11%

Diff.

RoTE : 12.4%12.1% 0.3%

FL CET1 ratio: 11.00%10.66% 0.34%Santander has a high RoTE with strong capital quality:

• The least capital destruction4 among European

peers (-199 bps vs -345 bps)

• Higher density (42% vs 33% in Mar-18)

• Better leverage (5.1 vs 5.0 fully loaded in Mar-18)

+5 bps+9 bps

-18 bps-5 bps

Pro forma ratios with

estimated impacts

25

9.70%

Group Phased-in ratiosMar-18

Regulatory requirement for2018

11.19%

4.50%

1.68%

1.50%

1.79%

1.875%

0.75%

1.50%

2.00%

Group regulatory capital and current distance to MDA

Capital

Current distance to MDA

CET1 CCoB

Pilar II requirement

Minimum Pilar I

AT1

G-SIB buffer

14.66%

T2

8.656%2

required

T2

12.156% Total capitalAT1

2.504%1

CCyB (0.031%)

Comfortable management buffer to MDA of >100 bps in regulatory transitional total capital and CET1 ratios, in line with Santander’s

business model and predictable results

As of Mar-18, the distance to the MDA for 2018 amounts is 2.504%

Significant payment capacity from distributable items: As of Mar-18, ADIs at Santander S.A.

EUR 57.2 bn, ~100x times 2018 full AT1 cost

Regulatory ratios Dec-18Target

Assumed regulatoryrequirement 1 Jan 19 CET1

>11.00%

4.50%

1.50%

2.00%

1.50%

2.50%

1.00%0.20%

CET1

CCoB

Pilar II requirement

Minimum Pilar I

G-SIB buffer

AT1

T2

~130bps4 CCyB

>14.5%

Targeted distance to MDA 1 January 20193

(1) MDA trigger= Group CET1 (11.19%) + AT1 (1.68%) + T2 (1.79%) vs. Regulatory Total Capital (12.166%) = 2.504%. 3.28% 1 year ago.

(2) 8.656% is the MDA threshold which reflects the minimum CET1 to be maintained by the Santander Group as communicated by the ECB on its decision regarding prudential minimum capital

requirements for 2018 following the results of the Supervisory Review and Evaluation Process (SREP) (3) Assuming stability in the minimum requirements.

(4) Assuming the fulfillment of AT1 and T2 during 2018

26

11.00%

1.49%

1.94%

Santander is committed to fulfil the AT1&T2 buckets through the transitional period

Capital

TIER2

TIER1

TIER2

TIER1

>11%

1.5%

2.0%

CET1 Generation2

AT1 issuances to target

T2 issuances to target

~6bps

~1 bp

~10-20

bps

Note: Assuming constant RWAs (1) Total capital ratio fully-loaded IFRS 9 phased-in (2) Net of pro forma estimated impact + organic generation.

All amounts except Mar-18 are targets

14.43%>14.5%

Group FL Total Capital

ratio Mar-181

Group FL Total Capital

ratio 2018E

AT1 issuance to target 1.5% of RWAs is

close to zero assuming constant RWAs.

T2 issuance to target 2% of RWAs

~EUR 0.4 bn

27

FX hedging policy on capital ratio and P&L…

Capital

Group

FL CET1

11.00%

Hedged

Exposure

Dynamic P&L hedging policy

Mitigate impact of FX volatility

Corporate Centre assumes all hedging costs

Manages FX volatility in our FL CET1 ratio

Based on Group regulatory capital and

RWAs

Stable capital ratio hedge Our P&L Policy

28

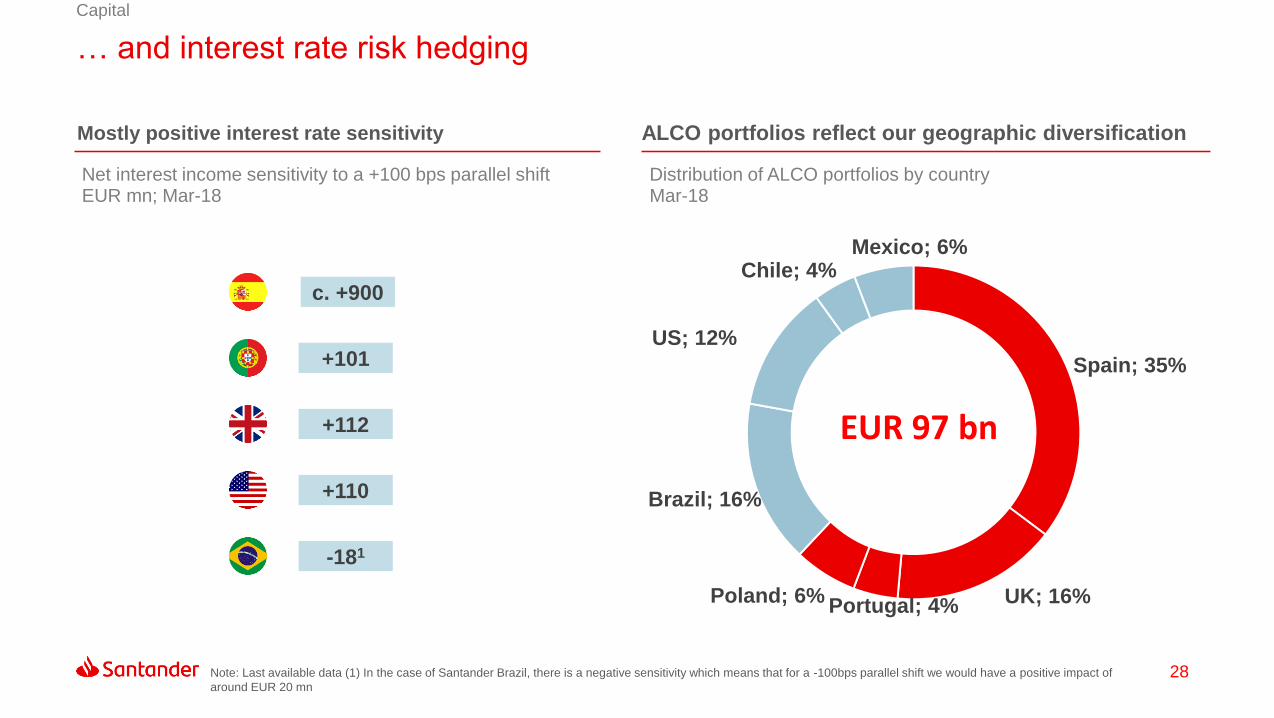

… and interest rate risk hedging

Capital

Spain; 35%

UK; 16%Portugal; 4%Poland; 6%

Brazil; 16%

US; 12%

Chile; 4%Mexico; 6%

EUR 97 bn

Note: Last available data (1) In the case of Santander Brazil, there is a negative sensitivity which means that for a -100bps parallel shift we would have a positive impact of

around EUR 20 mn

ALCO portfolios reflect our geographic diversificationMostly positive interest rate sensitivity

Net interest income sensitivity to a +100 bps parallel shiftEUR mn; Mar-18

Distribution of ALCO portfolios by country Mar-18

+101

+112

+110

-181

c. +900

Asset Quality

04

30

All asset quality ratios improved with cost of credit achieving the Investor Day goals

Asset Quality

Credit quality ratios NPL ratios by country

%

NPL ratio4.36

3.934.08 4.02

2015 2016 2017 Q1 2018

Cost of credit1.25

1.18

1.071.04

2015 2016 2017 Q1 2018

Q4 2017 Q1 2018

Spain 6.32 6.27

SCF 2.50 2.48

Poland 4.57 4.77

Portugal 7.51 8.29

United Kingdom 1.33 1.17

Brazil 5.29 5.26

Mexico 2.69 2.68

Chile 4.96 5.00

Argentina 2.50 2.54

USA 2.79 2.86

Cost of credit ratios by country

% Q4 2017 Q1 2018

Spain 0.30 0.29

SCF 0.30 0.36

Poland 0.62 0.69

Portugal 0.04 0.08

United Kingdom 0.08 0.10

Brazil 4.36 4.35

Mexico 3.08 2.95

Chile 1.21 1.22

Argentina 1.85 2.06

USA 3.42 3.29

%

31

Coverage ratio well situated among European peers with higher collateralisation

Asset Quality

Coverage ratio Coverage vs European Peers

%, Santander Mar-18, Peers1 latest available data

73 74

65

70

2015 2016 2017 Q1 2018

%

34

43

45

50

57

60

63

63

63

66

70

73

78

EU

UK

UK

UK

EU

EU

EU

UK

UK

EU

San

EU

EU

1. European peers include: Barclays, BBVA, BNP, Deutsche, HSBC, ING, Intesa Sanpaolo, Lloyds, RBS, Société Générale, Standard Chartered and Unicredit.

Note: Data taken from banks’ published accounts and definitions may not be homogeneous

32

Continuing the reduction of real estate exposure

Asset Quality

41.1

5.2

30.7

5.2

(1) Spain Real Estate activity

Following the acquisition of Banco Popular, we announced our

intention to reduce Grupo Santander’s NPE

Agreement with Blackstone was completed in March 2018

according to plan:

No material impact on results

Positive impact of 10 bps on the CET1 capital ratio

As a result of this operation the Spain Real Estate unit has an

exposure of EUR 5.2 billion

Gross

value

Jun-17

Blackstone

transaction

and other

Provisions

EUR bn

Real estate exposure1

Net

value

Mar-18

Mar-18EUR bn

Net value

Real estate assets 4.0

Foreclosed assets 2.8

Rental assets 1.2

RE non-performing loans (NPLs) 1.2

RE assets + RE non-performing loans 5.2

We will continue reducing this exposure

in the coming quarters

TLAC Requirements,

Liquidity and

Funding

05

34

TLAC requirements are manageable and an optimisation exercise for Santander

TLAC Requirements, Liquidity and Funding

The TLAC requirements regulation is a “work in progress”. On 23

November 2016, the European Commission published the proposals to

amend the CRD IV and CRR

On the same date, the European Commission also published a proposal

for the amendment of the BRRD regarding the ranking of unsecured debt

instruments in the creditor insolvency hierarchy

(the ‘Senior Ranking Harmonisation Directive’)1

The amendments include measures that will implement the TLAC

requirement into EU and national law

Implementation of the TLAC requirement is expected to phase-in from

1 January 2019: 16% from 1 January 2019 (18% from 2022)

plus applicable capital buffers

Santander has a resolution strategy approach of multiple point of entry

(MPE). The TLAC requirement is expected to be requested at each

resolution entity

Using the Group requirements as a proxy for the aggregate TLAC

requirement

TLAC phase-in requirements

4.5%

14.5%

> 2.5%

1.5%

2.5%

2.0%

8.0%

2.5%

1.0%

Indicative

amount of

Senior Non-

Preferred

subject to

significant

issues still

under

discussion

19.5%Eligible

Senior

2018 Total

Capital

Target

CET1

AT1

T2

TLAC

CCoB3

G-SIB2

Jan 2019 TLAC

phased-in requirements

CRD IV: Capital requirement directive. CRR: capital requirement regulation. BRRD: Bank recovery and resolution directive.

(1) According to proposal of Senior Ranking Harmonisation Directive, Royal Decree-law 11/2017 of 23 June on urgent actions on financial matters was approved

by the Spanish Government, creating the new category of senior non-preferred debt under Spanish Law

(2) G-SIB buffer. (3) Capital Conservation Buffer

35

The Group’s business model combines local knowledge with global best practices through legally, financially and operationally autonomous subsidiaries…

Banco Santander S.A.

Banco

Santander

Totta.

Bank

Zachodni

WBK

Santander

UK Group

Holdings

Santander

Holdings

USA Banco

Santander

BrasilGrupo

Financiero

Mexico Banco

Santander

Chile Banco

Santander

Río

100

%99% 70% 100

%

100

%

89% 75% 67% 99%

Santander

Consumer

Finance

Banco

Popular

100

%

Legal autonomy structure

Dec-17

Legal autonomy: There are no legal commitments that imply financial support.

Financial autonomy: Financial interconnections are limited and at market prices.

Operational autonomy: Shared services are limited and carried out through autonomous factories. Access to FMIs through other

Group entities is very limited.

TLAC Requirements, Liquidity and Funding

36

13

… divided into different resolution groups that can be resolved separately though multiple entry points

MPE resolution strategy

Dec-17, EUR bn

We have defined the Resolution Groups (RGs) mirroring the model of autonomous financial groups so that all entities have

been assigned to one RG

Each RG comprises the entity identified as the entry point in resolution and the entities that belong to it

PE Point of Entry

Resolution Group

Spain (Parent) United Kingdom

Brazil USA

ChileMexicoPoland

Argentina

Size of Resolution Groups (Total assets by geography)

651 361

162 114

58 5032

Portugal

48

SpainPE

PortugalPE

Banking Union

UKPE

PolandPE

European Union 3rd Countries

BrazilPE

MexicoPE

ArgentinaPE

ChilePE

USAPE

TLAC Requirements, Liquidity and Funding

37

Santander’s MPE approach follows its autonomous capital and liquidity model, though there are still issues under discussion with regards to TLAC application

Significant issues still under discussion

Mexico

USA UK

Poland

Chile

Brazil

SantanderS.A.

Argentina

16.64

18.26

19.92

11.19

12.44

15.71

11.11

13.84

13.98

13.20

14.24

15.27

9.73

9.73

12.01

15.30

18.07

18.36

15.31

15.31

16.67

12.53

15.30

17.83

19.39

21.82

24.12

CET1

T1

Total

Portugal

Local figures as of Mar-18 in percent (phased-in)

Final TLAC transposition to EU and

relevant jurisdictions

TLAC level and perimeter of resolution

groups

Eligible Senior debt final treatment

Internal TLAC requirement

Deductions and mitigants final treatment

TLAC Requirements, Liquidity and Funding

38

Santander’s liquidity management is based on the following principles:

Decentralised liquidity model

Needs derived from medium- and long-term activity must be financed by medium- and long-term instruments

High contribution from customer deposits, due to the retail nature of the balance sheet

Diversification of wholesale funding sources by instruments/investors, markets/currencies and maturities

Limited recourse to wholesale short-term funding

Availability of sufficient liquidity reserves, including the discount window / standing facility in central banks to be

used in adverse situations

Compliance with regulatory liquidity requirements both at Group and subsidiary level, as a new conditioning

management factor

TLAC Requirements, Liquidity and Funding

39

Conservative and decentralised liquidity and funding model

Very manageable maturity profileEUR 12 bn1 issued during Q1 2018

EUR bn, Mar-18

US

0

Portugal

0

UK

4.6

SCF

0.7

Chile

0.5

SantanderS.A.

4.7

Argentina

0.3

Poland

0

Brazil

1.3

Mexico

0

2018 2019 2020 2021 2022 2022+

(1) Data include issuances from all units and the following product types covered bonds, senior, senior non-preferred (“Senior TLAC”), preferred stock, subordinated, with period-average exchange rates

EUR bn

Santander

S.A.1.3 1.9 4.2 2.3

6.9

35.3

2018 2019 2020 2021 2022 2022+

UK 2.86.8

10.97.1

3.1

17.5

2018 2019 2020 2021 2022 2022+

SCF 3.0 4.1 3.9 1.6 2.7 0.8

2018 2019 2020 2021 2022 2022+

Brazil 3.0 1.8 2.7 0.0 0.0 0.1

2018 2019 2020 2021 2022 2022+

TLAC Requirements, Liquidity and Funding

40

Santander S.A.’s Funding Plan is focused on TLAC-eligible instruments, following our decentralised liquidity and funding model

Santander S.A. issuances YTDSantander S.A. Funding Plan 2018

(1) Data include issuances from all units and the following product types covered bonds, senior, senior non-preferred (“Senior TLAC”), preferred stock, subordinated, with

period-average exchange rates (2) Excluding securitisations

EUR mn

PUBLIC Product Nom. EUR Maturity Coupon Spread 6M

January SNP 1,250 7 1.13% MS+60bps

February Sub 1,250 10 2.13% MS+110bps

March AT1 1,500 Perp 4.75% MS+409bps

SNP 405 5 US3M+1.12% MS+66bps

SNP 1,014 5 3.85% MS+66bps

SNP 1,014 10 4.38% MS+99bps

Total YTD 6,433

April

PRIVATE Currency Nominal Maturity Reoffer

Q1 2018 EUR 691 7 MS+54bps

1.50 1.00

7-10

1.50 1.25

4.40

AT1 T2 SNP

Funding Plan Issued YTD

EUR bn, Apr-18

TLAC Requirements, Liquidity and Funding

41

Well-funded, prudent and highly liquid balance sheet with high contribution from customer deposits and diversified wholesale instruments

179

24

88

131

857

157

45

767

Assets Liabilities

ST Funding

Securitisations

Equity and other

Net loans to

customers

Financial assets

Fixed assets & other

Deposits

M/LT Funding

Liquidity Coverage Ratio (LCR)

Note: Liquidity balance sheet for management purposes (net of trading derivatives and interbank balances) (1) Provisional data, includes Banco Popular (2) Parent bank

1,124 1,124

Liquidity Balance Sheet

EUR bn, Mar-18

132%

145%2

119%

146%1

Group

Net Stable Funding Ratio (NSFR)

121%

105%2

109%

111%1

Mar-18 Dec-17

TLAC Requirements, Liquidity and Funding

42

The main metrics show the strength and stability the Group’s liquidity position…

Evolution of key liquidity metrics1

(1).- Balance sheet for liquidity management purposes.Note: in 2013 customer deposits include retail commercial paper in Spain (excluding short-term wholesale funding). The 2013 ratios include SC USA by global integration.

Note: all figures as of 2017 include Popular

2013 2014 2015 2016 2017 Q1'18

Net loans / net assets 74% 74% 75% 75% 75% 76%

Net loan-to-deposit ratio (LTD) 112% 113% 116% 114% 109% 112%

Customer deposits and medium-

and long-term funding / net loans118% 116% 114% 114% 115% 113%

Short-term wholesale funding /

net liabilities2% 2% 2% 3% 2% 2%

Structural liquidity surplus / net

liabilities16% 15% 14% 14% 15% 14%

Encumbrance 26% 26% 25% 28% -

LTD and MLT funding metrics by geography

Mar-18

LTD Ratio

(Deposits + M/LT

funding) / Net lending

Spain 88% 142%

Portugal 102% 111%

SCF 243% 66%

Poland 89% 114%

UK 114% 110%

Brazil 101% 122%

Mexico 88% 122%

Chile 143% 95%

Argentina 78% 134%

USA 136% 112%

Group total 112% 113%

TLAC Requirements, Liquidity and Funding

43

… backed by a strong liquidity buffer in every subsidiary

Note: all figures as of 2017 include Popular

Liquidity buffer by subsidiary

Dec-17, EUR bn

54.8

9.86.3

9.06.2

52.6

17.013.2

9.6

5.0 3.91.4

Total Buffer: EUR 188.8 bn

TLAC Requirements, Liquidity and Funding

44

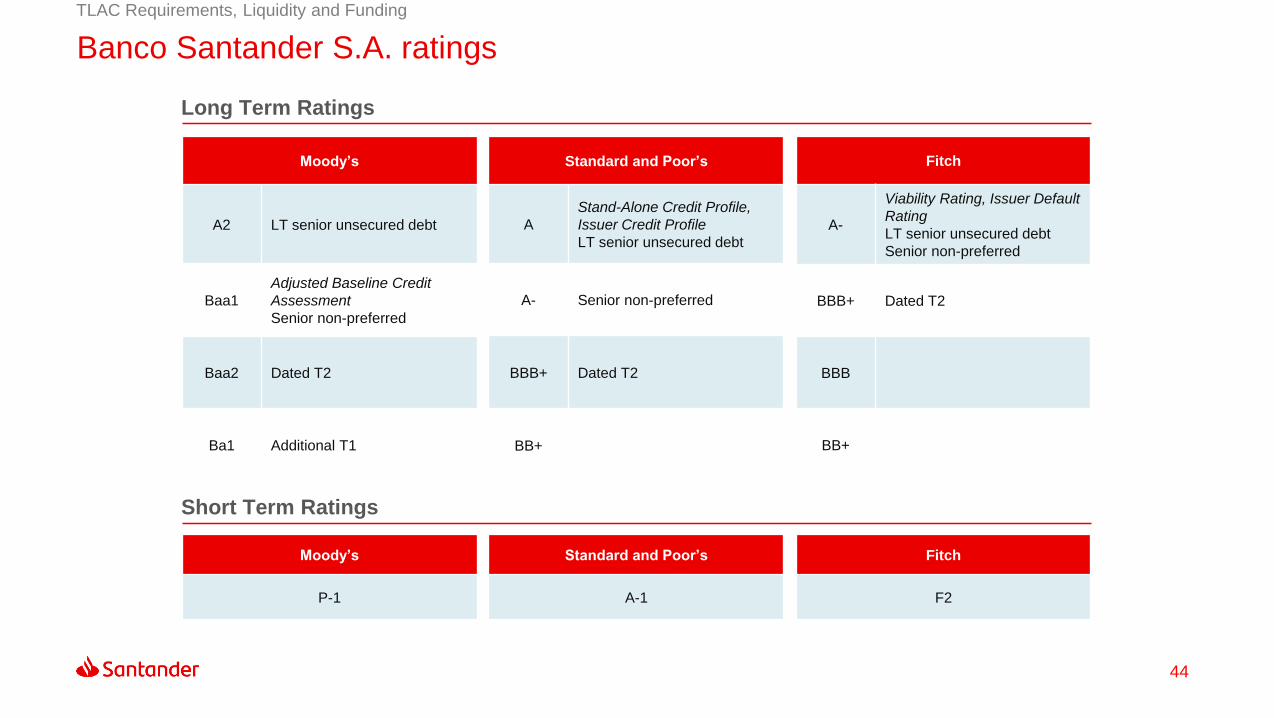

Banco Santander S.A. ratings

Long Term Ratings

Fitch

A-

Viability Rating, Issuer Default

Rating

LT senior unsecured debt

Senior non-preferred

BBB+ Dated T2

BBB

BB+

Standard and Poor’s

A

Stand-Alone Credit Profile,

Issuer Credit Profile

LT senior unsecured debt

A- Senior non-preferred

BBB+ Dated T2

BB+

Moody’s

A2 LT senior unsecured debt

Baa1

Adjusted Baseline Credit

Assessment

Senior non-preferred

Baa2 Dated T2

Ba1 Additional T1

Short Term Ratings

Moody’s

P-1

Standard and Poor’s

A-1

Fitch

F2

TLAC Requirements, Liquidity and Funding

Concluding

Remarks

06

46

Concluding Remarks

The Group’s stable capital generation is supported by strong pre-provision profits providing Santander with a high

capacity to absorb provisions and underpins the Group's capacity to generate future earnings

Strong capital levels in line with Santander’s business model based on geographic diversification, solid market

positions in areas where it operates and independent subsidiary model in terms of capital and liquidity

The Group is well above the regulatory capital requirement with significant payment capacity from distributable

items, while maintaining comfortable margins to conversion and MDA triggers

The Group continues with its objective to organically generate 40bps of fully loaded CET1 per year, maintaining

business growth and dividend payment

TLAC/MREL requirements are manageable and remain a key focus in 2018 and represent an optimisation exercise

for Santander

Comfortable liquidity position: Compliance with regulatory liquidity requirements established at Group and

subsidiary levels ahead of schedule, with high availability of liquidity reserves

Concluding Remarks

Appendix:

UK loan portfolio: Mortgage

and Corporate Real Estate

07

48

Robust retail banking credit performance

Appendix: UK loan portfolio: Mortgage and Corporate RE

Retail Banking NPLs Retail Banking loss allowances and write-offs

2,5202,340

2,105 2,129

Dec-15 Dec-16 Dec-17 Mar-18

1.51%

1.39%

1.25% 1.25%

823

583491

617

Dec-15 Dec-16 Dec-17 Mar-18

Loan loss allowance

Write-offs during the period

NPL ratio

248210 195

47

FY 15 FY 16 FY 17 3M 18

GBP mn GBP mn

Balance of Retail Banking loans (GBP bn)

168.6167.0 169.0 170.6

49

Well diversified CRE portfolio

Credit performance Sector analysis

Stock %, Dec-17

(1) Consists of smaller value transactions, mainly commercial mortgages (2) Excludes standardised portfolio

27

1714 14

12

8

42 2

Office Retail Industrial Mixed use Residential Standardisedportfolio

Hotels andleisure

Student acc Other

NPL ratio 2.00% 0.85%

NPL coverage ratio 32% 78%

Up to 70% LTV 88% 88%

70% to 100% LTV 2% -

> 100% LTV 1% 1%

Standardised portfolio1 7% 8%

Total committed exposure £9.0bn £8.1bn

98% 97%

Development loans 2% 3%

100% 100%

Total with collateral

Dec-16 Dec-17

Dec-16 Dec-17

No new business written above 70% LTV (Dec-16: 0%)

91% written at or below 60% LTV (Dec-16: 95%)

Weighted average LTV on exposures Dec-17: 48% (Dec-16:

50%)2

Average loan size of £4.8 mn at Dec-17 (Dec-16: £4.8 mn)

NPL ratio decreased primarily due to the sale of collateral to

repay two impaired loans, as well as other redemptions and

write-offs of older vintage loans

Appendix: UK loan portfolio: Mortgage and Corporate RE

50

154.9 156.8

7.6 7.7

(5.7)

Dec-17 New business Redemptions& repayments

Internaltransfer

Mar-18

Prime residential mortgage book of GBP 154.9 bn

Mortgage borrower profile Mortgage lending

GBP bnStock %, Dec-17

Fixed rate; 66%Variable Rate; 19%

Standard Variable Rate (SVR); 15%

24

111314

24

32

Northern IrelandScotlandSouth West,Wales and Other

Midlands andEast Anglia

NorthLondonSouth East

Mortgage product profile Geographic distribution

Stock %, Dec-17Stock %, Dec-17

(1) Variable rate includes tracker and base rate linked products (2) Full interest only loans and the element of part-and-part attribution to interest only balances,

excluding BTL mortgages (3) Refer to glossary at www.santander.co.uk/uk/about-santander-uk/investor-relations-glossary for a full definition

c. 77% of maturing mortgages retained3

1

Home movers; 44%

Remortgages; 33%

First time buyers; 19%

Buy to Let; 4%

29% interest only mortgages (Dec-16: 31%)2

Appendix: UK loan portfolio: Mortgage and Corporate RE

51

Consistently prudent mortgage lending criteria

Mortgage loan distribution Loan-to-Value (LTV)

Less than £0.25mn 71.6% 69.1%

£0.25m - £0.5mn 21.3% 23.3%

£0.5m - £1mn 6.3% 6.8%

£1m - £2mn 0.7% 0.7%

Loan size distribution (stock)

0.1% 0.1%

100% 100%

Over £2mn

Dec-16 Dec-17

Average loan size distribution (new business)

London and South East £264k £260k

Rest of UK £144k £146k

All UK £198k £196k

3.16 3.16Loan-to-income multiple1

(1) Average earnings multiple of new business at inception in the periods (2) Unweighted average loan-to-value of all accounts

New lending 65% 62%

Stock 43% 42%

Simple average LTV2

Dec-16 Dec-17

> 85% - 100% 4% 4%

> 100% 1% 1%

Indexed LTV distribution (stock)

New lending % with LTV >85% 17% 19%

24,000 first-time buyers (£4.0bn gross lending)

7,500 BTL mortgages (average LTV of 61%)

Appendix: UK loan portfolio: Mortgage and Corporate RE

Glossary

08

53

Glossary and Acronyms

Glossary

ADIs: Available distributable items

AFS: Available for sale

bn: Billion

Bps: Basis points

CCoB: Capital Conservation Buffer

CCyB: Countercyclical buffer

CET1: Common equity tier 1

DGF: Deposit Guarantee Fund

DPS: Dividend per share

EPS: Earning per share

FL: Fully loaded

G-SIBs: Global Systemically Important Banks

K: thousands

LTV: Loan to Value

LLPs: Loan-loss provisions

MDA: Maximum distributable amount

M/LT: Medium / long term

mn: Million

MXN: Mexican Pesos

NII: Net interest income

NPL: Non-performing loans

n.m.: Non meaningful

PBT: Profit before tax

P&L: Profit and loss

RoRWA: Return on risk-weighted assets

RWA: Risk-weighted assets

RoTE: Return on tangible equity

SCF: Santander Consumer Finance

GCB: Global Corporate Banking

SMEs: Small and Medium Enterprises

SRF: Single Resolution Fund

ST: Short term

SVR: Standard variable rate

TLAC: Total Loss-Absorbing Capacity

TNAV: Tangible net asset value

YoY: Year-on-Year

UK: United Kingdom

US: United States

Thank you.

Our purpose is to help people

and business prosper.

Our culture is based on believing

that everything we do should be