fixed income technical strategy note: equities

TRANSCRIPT

23 March 2018

TECHNICAL STRATEGY NOTE: EQUITIES

Neels Heyneke

Senior Strategist

Tel : +27 11 535 4041

Mehul Daya

Strategy: Research Analyst

Tel : +27 11 295 8838

23 March 2018

TECHNICAL STRATEGY NOTE:

EQUITIES

NEELS HEYNEKE

Senior Strategist

Tel : +27 11 535 4041

MEHUL DAYA

Strategy: Research Analyst

Tel : +27 11 295 8838

23 March 2018

TECHNICAL STRATEGY NOTE: EQUITIES

Neels Heyneke

Senior Strategist

Tel : +27 11 535 4041

Mehul Daya

Strategy: Research Analyst

Tel : +27 11 295 8838

23 March 2018

FIXED INCOME CREDIT|SOUTH AFRICADCM TRENDS

NTHULLENG MPHAHLELE

Analyst

Tel : +27 11 294 7032

JONES GONDO

Senior Credit Research Analyst

Tel : +27 11 295 4484

DCM TRENDS | 23 MARCH 18 | PAGE 2

TABLE OF CONTENT

Overview of Nedbank’s New Credit Publications 2018 3

Issuances Volume 4

Redemptions 1H18 9

Spread Development 12

Bond Curves 16

Ratings Distribution 18

Contacts 21

ACCESS: CREDIT DATABOOK

Content

DISCLAIMER

The information furnished in this report, brochure, document, material, or communication (“the Commentary”), has been prepared by Nedbank Limited (acting through its

Nedbank Corporate and Investment Banking division), a registered bank in the Republic of South Africa, with registration number: 1951/000009/06 and having its registered

office at 135 Rivonia Road, Sandton, Johannesburg (“Nedbank”). The information contained herein may include facts relating to current events or prevailing market conditions

as at the date of this Commentary, which conditions may change and Nedbank shall be under no obligation to notify the recipient thereof or modify or amend this

Commentary. The information included herein has been obtained from various sources believed by Nedbank to be reliable and expressed in good faith, however, Nedbank

does not guarantee the accuracy and/or completeness thereof and accepts no liability in relation thereto.

Nedbank does not expressly, or by implication represent, recommend or propose that any securities and/or financial or investment products or services referred to in this

Commentary are appropriate and or/or suitable for the recipient’s particular investment objectives or financial situation. This Commentary should not be construed as

“advice” as contemplated in the Financial Advisory and Intermediary Services Act, 37 of 2002 in relation to the specified products. The recipient must obtain its own advice

prior to making any decision or taking any action whatsoever.

This Commentary is neither an offer to sell nor a solicitation of an offer to buy any of the products mentioned herein. Any offer to purchase or sell would be subject to

Nedbank’s internal approvals and agreement between the recipient and Nedbank. Any prices or levels contained herein are preliminary and indicative only and do not

represent bids or offers and may not be considered to be binding on Nedbank. All risks associated with any products mentioned herein may not be disclosed to any third party

and the recipient is obliged to ascertain all such risks prior to investing or transacting in the product or services. Products may involve a high degree of risk including but not

limited to a low or no investment return, capital loss, counterparty risk, or issuer default, adverse or unanticipated financial markets fluctuations, inflation and currency

exchange. As a result of these risks, the value of the product may fluctuate. Nedbank cannot predict actual results, performance or actual returns and no guarantee,

assurance or warranties are given in this regard. Any information relating to past financial performance is not an indication of future performance.

Nedbank does not warrant or guarantee merchantability, non-infringement or third party rights or fitness for a particular purpose. Nedbank, its affiliates and individuals

associated with them may have positions or may deal in securities or financial products or investments identical or similar to the products.

This Commentary is available to persons in the Republic of South Africa, financial services providers as defined in the FAIS Act, as well as to other investment and financial

professionals who have experience in financial and investment matters.

All rights reserved. Any unauthorized use or disclosure of this material is prohibited. This material may not be reproduced without the prior written consent of Nedbank, and

should the information be so distributed and/or used by any recipients and/or unauthorized third party, Nedbank disclaims any liability for any loss of whatsoever nature that

may be suffered by any party by relying on the information contained in this Commentary.

Certain information and views contained in this Commentary are proprietary to Nedbank and are protected under the Berne Convention and in terms of the Copyright Act 98

of 1978 as amended. Any unlawful or attempted illegal copyright or use of this information or views may result in criminal or civil legal liability.

All trademarks, service marks and logos used in this Commentary are trademarks or service marks or registered trademarks or service marks of Nedbank or its affiliates.

Nedbank Limited is a licensed Financial Services Provider and a Registered Credit Provider (FSP License Number 9363 and National Credit Provider License Number NCRCP 16).

DCM TRENDS | 23 MARCH 18 | PAGE 3

DCM Trends

We have reorganised our approach to credit research for the South African market. Our aim is to provide the market with high

quality credit perspectives which are timely, concise, and incisive.

1. DCM Trends & Databook: Essential data and statistics on South Africa’s primary debt capital market. A simple and easy-

to-read reference pack. These will be published monthly (The Databook will be available as a link in the DCM Trends

report).

2. Credit Insights: Timely, issuer-specific credit opinions that are situational or event-driven. Published on an ad hoc basis.

3. Credit Thematic Reviews: A technical or fundamental review of topical credit themes or emerging trends as they apply to

South Africa’s credit market. Published on an ad hoc basis.

4. Quarterly Commentary: A cross-cutting, contextual review of the South African economy from a credit perspective and a

critical discussion of key credit events and themes emerging over the last quarter.

CREDIT|SOUTH AFRICA

DCM Trends Credit Databook

Credit Insights Thematic Reviews

Quarterly Commentary

Monthly Publication

Ad hoc Publication

Publications 2018

DCM TRENDS | 23 MARCH 18 | PAGE 4

-

20

40

60

80

100

120

140

160

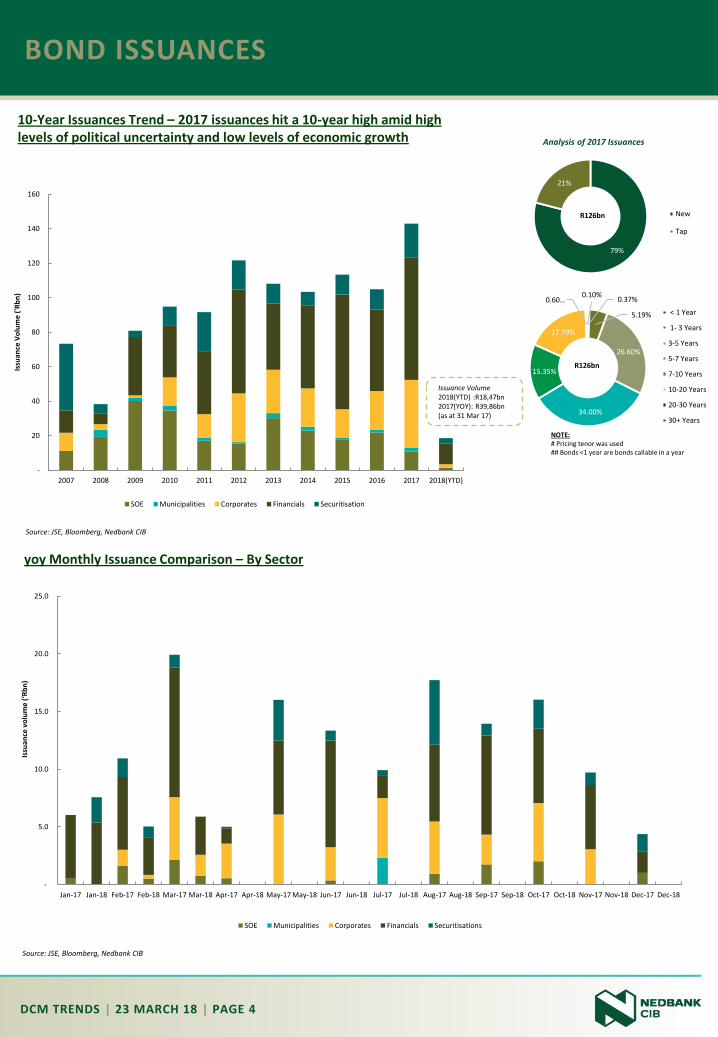

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018(YTD)

Issu

ance

Vo

lum

e ('

Rb

n)

SOE Municipalities Corporates Financials Securitisation

BOND ISSUANCES

Analysis of 2017 Issuances

10-Year Issuances Trend – 2017 issuances hit a 10-year high amid high levels of political uncertainty and low levels of economic growth

yoy Monthly Issuance Comparison – By Sector

Source: JSE, Bloomberg, Nedbank CIB

Issuance Volume 2018(YTD) :R18,47bn2017(YOY): R39,86bn (as at 31 Mar 17)

Source: JSE, Bloomberg, Nedbank CIB

-

5.0

10.0

15.0

20.0

25.0

Jan-17 Jan-18 Feb-17 Feb-18 Mar-17 Mar-18 Apr-17 Apr-18 May-17 May-18 Jun-17 Jun-18 Jul-17 Jul-18 Aug-17 Aug-18 Sep-17 Sep-18 Oct-17 Oct-18 Nov-17 Nov-18 Dec-17 Dec-18

Issu

ance

vo

lum

e (‘

Rb

n)

SOE Municipalities Corporates Financials Securitisations

79%

21%

R126bn New

Tap

0.37%

5.19%

26.60%

34.00%

15.35%

17.79%

0.60…0.10%

R126bn

< 1 Year

1- 3 Years

3-5 Years

5-7 Years

7-10 Years

10-20 Years

20-30 Years

30+ Years

NOTE:# Pricing tenor was used## Bonds <1 year are bonds callable in a year

DCM TRENDS | 23 MARCH 18 | PAGE 5

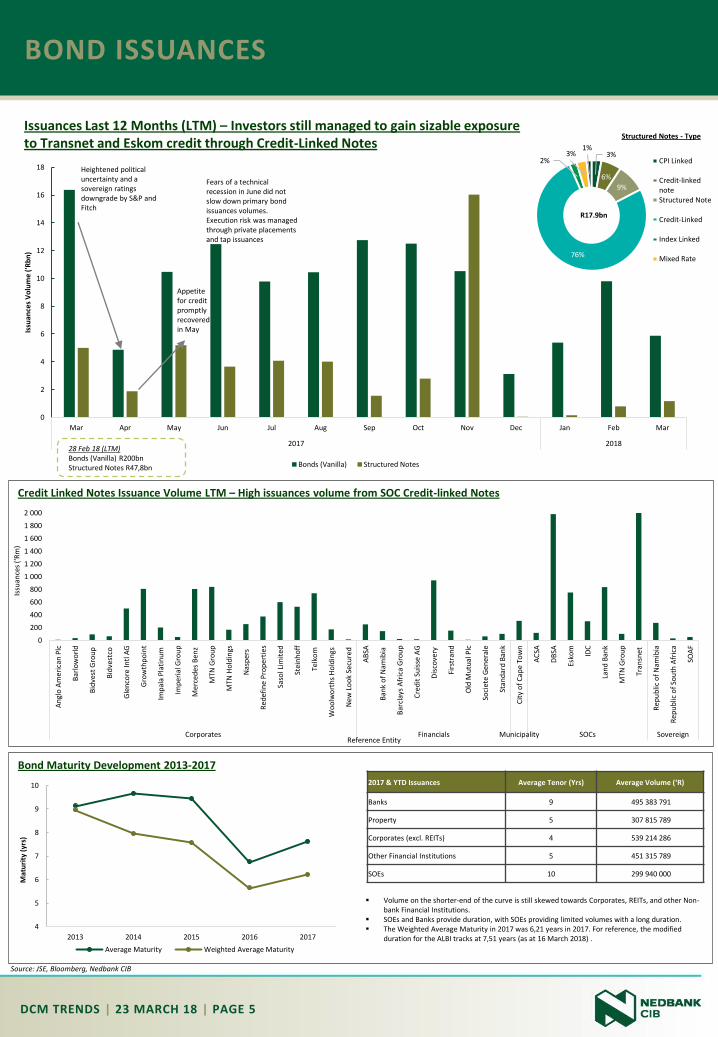

0

2

4

6

8

10

12

14

16

18

Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

2017 2018

Issu

ance

s V

olu

me

('R

bn

)

Bonds (Vanilla) Structured Notes

BOND ISSUANCES

Issuances Last 12 Months (LTM) – Investors still managed to gain sizable exposure to Transnet and Eskom credit through Credit-Linked Notes

Source: JSE, Bloomberg, Nedbank CIB

Appetite for credit promptly recovered in May

Fears of a technical recession in June did not slow down primary bond issuances volumes. Execution risk was managed through private placements and tap issuances

28 Feb 18 (LTM)Bonds (Vanilla) R200bnStructured Notes R47,8bn

Bond Maturity Development 2013-2017

4

5

6

7

8

9

10

2013 2014 2015 2016 2017

Mat

uri

ty (

yrs)

Average Maturity Weighted Average Maturity

Structured Notes - Type

Volume on the shorter-end of the curve is still skewed towards Corporates, REITs, and other Non-bank Financial Institutions.

SOEs and Banks provide duration, with SOEs providing limited volumes with a long duration. The Weighted Average Maturity in 2017 was 6,21 years in 2017. For reference, the modified

duration for the ALBI tracks at 7,51 years (as at 16 March 2018) .

2017 & YTD Issuances Average Tenor (Yrs) Average Volume (‘R)

Banks 9 495 383 791

Property 5 307 815 789

Corporates (excl. REITs) 4 539 214 286

Other Financial Institutions 5 451 315 789

SOEs 10 299 940 000

Credit Linked Notes Issuance Volume LTM – High issuances volume from SOC Credit-linked Notes

Heightened political uncertainty and a sovereign ratings downgrade by S&P and Fitch

3%

6%

9%

76%

2%3%

1%

R17.9bn

CPI Linked

Credit-linkednoteStructured Note

Credit-Linked

Index Linked

Mixed Rate

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

An

glo

Am

eri

can

Plc

Bar

low

orl

d

Bid

vest

Gro

up

Bid

vest

co

Gle

nco

re In

tl A

G

Gro

wth

po

int

Imp

ala

Pla

tin

um

Imp

eria

l Gro

up

Mer

ced

es B

enz

MTN

Gro

up

MTN

Ho

ldin

gs

Nas

per

s

Red

efin

e P

rop

erti

es

Saso

l Lim

ited

Stei

nh

off

Telk

om

Wo

olw

ort

hs

Ho

ldin

gs

New

Lo

ok

Secu

red

AB

SA

Ban

k o

f N

amib

ia

Bar

clay

s A

fric

a G

rou

p

Cre

dit

Su

isse

AG

Dis

cove

ry

Firs

tran

d

Old

Mu

tual

Plc

Soci

ete

Gen

eral

e

Stan

dar

d B

ank

Cit

y o

f C

ape

Tow

n

AC

SA

DB

SA

Esko

m

IDC

Lan

d B

ank

MTN

Gro

up

Tran

snet

Rep

ub

lic o

f N

amib

ia

Rep

ub

lic o

f So

uth

Afr

ica

SOA

F

Corporates Financials Municipality SOCs Sovereign

Issu

ance

s (‘

Rm

)

Reference Entity

DCM TRENDS | 23 MARCH 18 | PAGE 6

19.35

13.41

9.00

6.545.75

5.10 4.83 4.70 4.50 4.34 4.043.38 3.21

2.50 2.50 2.40 2.26 2.00 1.85 1.76

0

5

10

15

20

25

Vo

lum

es (

'Rb

n)

Issuer

BOND ISSUANCES

Top 20 Issuers LTM – Banks, Corporates, and REITS driving bond issuance volumes

Source: JSE, Bloomberg, Nedbank CIB

Top Issuers YTD (January - March 2018) – Banks continue dominating the issuance volume tally, including capital instruments issued out of group holding companies and the refinancing of existing debt

Source: JSE, Bloomberg, Nedbank CIB

MBSA’s issuance volumes and pricing are comparable to banks.

4.50

3.00

2.402.30

2.00

1.101.00

0.76 0.75 0.73 0.680.60

0.500.40

0.30

0.03

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

Issu

ance

Vo

lum

e ('

Rb

n)

Issuer

DCM TRENDS | 23 MARCH 18 | PAGE 7

BOND ISSUANCES – 2018 YTD

Financials

Corporates

Source: JSE, Bloomberg, Nedbank CIB

Bond Code

Issuer NameStandardized

RatingTap/New

IssueDate of Issue

Expected Maturity

Pricing Tenor

Amount Issued (ZAR Bln)

Spread at issue

Reference Benchmark

Coupon Type Payment Rank

SBS60Standard Bank of South Africa

LtdAA+ New 18-Jan-18 18-Jan-23 5 1,50 156 3m Jibar Floating Sr Unsecured

FRX31 FirstRand Bank Ltd AA+ Tap 19-Jan-18 21-Jan-31 13 0,05 177 R213 Fixed Sr Unsecured

IBL77 Investec Bank Ltd AA+ Tap 19-Jan-18 25-Nov-20 3 0,18 165 3m Jibar Floating Sr Unsecured

FRX24 FirstRand Bank Ltd AA+ Tap 31-Jan-18 10-Dec-24 7 0,03 125 R186 Fixed Sr Unsecured

FRX30 FirstRand Bank Ltd AA+ Tap 31-Jan-18 31-Jan-30 12 0,07 155 R2030 Fixed Sr Unsecured

FRX32 FirstRand Bank Ltd AA+ Tap 31-Jan-18 31-Mar-32 14 0,33 164 R2032 Fixed Sr Unsecured

FRJ23 FirstRand Bank Ltd AA+ New 31-Jan-18 31-Jul-23 5 0,67 145 3m Jibar Floating Sr Unsecured

FRJ20 FirstRand Bank Ltd AA+ Tap 31-Jan-18 20-Sep-20 3 2,11 100 3m Jibar Floating Sr Unsecured

FRJ25 FirstRand Bank Ltd AA+ Tap 31-Jan-18 09-Mar-25 7 0,45 200 3m Jibar Floating Sr Unsecured

FRJ22 FirstRand Bank Ltd AA+ Tap 06-Feb-18 07-Mar-22 4 0,16 155 3m Jibar Floating Sr Unsecured

SBT201 Standard Bank Group Ltd BBB New 12-Feb-18 13-Feb-23 5 3,00 314 3m Jibar FloatingSubordinated

Unsecured

NBK44B Nedbank Ltd AA+ New 15-Feb-18 15-Feb-21 3 0,86 120 3m Jibar Floating Sr Unsecured

NBK45B Nedbank Ltd AA+ New 15-Feb-18 15-Feb-23 5 0,37 145 3m Jibar Floating Sr Unsecured

NBK46B Nedbank Ltd AA+ New 15-Feb-18 15-Aug-25 8 0,40 165 3m Jibar Floating Sr Unsecured

NBK47B Nedbank Ltd AA+ New 15-Feb-18 15-Feb-28 10 0,78 190 3m Jibar Floating Sr Unsecured

FRX32 FirstRand Bank Ltd AA+ Tap 19-Feb-18 31-Mar-32 14 0,05 194 R2032 Fixed Sr Unsecured

FRJ22 FirstRand Bank Ltd AA+ Tap 20-Feb-18 07-Mar-22 4 0,08 155 3m Jibar Floating Sr Unsecured

FRJ23 FirstRand Bank Ltd AA+ Tap 28-Feb-18 31-Jul-23 5 0,51 145 3m Jibar Floating Sr Unsecured

SBS47 Standard Bank AA+ Tap 08-Mar-18 09-Mar-18 5 0,30 184 3m Jibar Floating Sr Unsecured

INLV05 Investec Bank Ltd BB+ New 15-Mar-18 22-Mar-23 5 0,35 515 3m Jibar Floating Jr Subordinated

Bond Code

Issuer NameStandardized

RatingTap/New

IssueDate of

issueExpected Maturity

Pricing Tenor

Amount Issued (ZAR Bln)

Spread at issue (bps)

Reference Benchmark

Coupon Type Payment Rank

IPF24 Investec Property Fund Ltd A New 05-Feb-18 05-Feb-23 5 0,30 170 3m Jibar Floating Sr Unsecured

CGR38 Calgro M3 Development Ltd N/R New 13-Feb-18 13-Feb-21 3 0,03 400 3m Jibar Floating Sr Unsecured

NTC22 Clindeb Investments Pty Ltd A+ New 15-Feb-18 15-Feb-21 3 0,19 155 3m Jibar Floating Sr Unsecured

NTC23 Clindeb Investments Pty Ltd A+ New 15-Feb-18 15-Feb-23 5 0,57 175 3m Jibar Floating Sr Unsecured

HPF11 Hospitality Property Fund Ltd A+ New 19-Feb-18 31-Mar-23 5 0,60 195 3m Jibar Floating Secured

BAW29 Barloworld Ltd AA+ New 22-Feb-18 22-Feb-23 5 0,40 180 3m Jibar Floating Sr Unsecured

MBP039Mercedes-Benz South Africa Pty

LtdAAA New 23-Feb-18 23-Feb-21 3 0,50 115 3m Jibar Floating Sr Unsecured

MBP040Mercedes-Benz South Africa Pty

LtdAAA New 23-Feb-18 23-Feb-23 5 0,50 130 3m Jibar Floating Sr Unsecured

MBP039Mercedes-Benz South Africa Pty

LtdAAA New 23-Feb-18 23-Feb-21 3 0,50 115 3m Jibar Floating Sr Unsecured

MBP040Mercedes-Benz South Africa Pty

LtdAAA New 23-Feb-18 23-Feb-23 5 0,50 130 3m Jibar Floating Sr Unsecured

GRT24G Growthpoint Properties AAA New 09-Mar-18 03-Sep-23 5 0,3 139 3m Jibar FloatingSnr Unsec Green

Bond

GRT25G Growthpoint Properties AAA New 09-Mar-18 03-Sep-25 7 0,24 169 3m Jibar FloatingSnr Unsec Green

Bond

GRT26G Growthpoint Properties AAA New 09-Mar-18 03-Sep-28 10 0,56 200 3m Jibar FloatingSnr Unsec Green

Bond

RDFB13 Redefine Properties AA+ New 13-Mar-18 12-Mar-21 3 0,3 140 3m Jibar Floating Sr Unsecured

RDFB14 Redefine Properties AA+ New 13-Mar-18 12-Mar-23 5 0,43 160 3m Jibar Floating Sr Unsecured

State-Owned Enterprises

Bond Code

Issuer NameStandardized

RatingTap/New

IssueDate of issue

Expected Maturity

Pricing Tenor

Amount Issued (ZAR Bln)

Spread at issue (bps)

Reference Benchmark

Coupon Type Payment Rank

NRA028South African National Road

Agency SOC LtdAA- Tap 22-Feb-18 30-Nov-28 11 0,50 299 R186 FIXED Sr Unsecured

LBK26 Land Bank AA+ New 23-Mar-18 23-Mar-21 3 0,245 149 3m Jibar Floating Sr Unsecured

LBK27 Land Bank AA+ New 23-Mar-18 23-Mar-23 5 1,50 215 3m Jibar Floating Sr Unsecured

DCM TRENDS | 23 MARCH 18 | PAGE 8

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Vo

lum

e ('

Rm

)

2016 2017 2018

24%

76%

CP (Structured)

CP (Vanilla)

CP ISSUANCES

Monthly CP (Vanilla) Issuances Trend

Source: JSE, Bloomberg, Nedbank CIB

Vanilla vs Structured CP Issuances LTM

Source: JSE, Bloomberg, Nedbank CIB

R51.2bn

Bond Code Tap/New IssueDate of

issueExpected Maturity

Pricing Tenor (Days)

Amount Issued (ZAR Bln)

Spread at issue (bps)

IVA721 New 09-Jan 23-Apr 104 0,264 Zero coupon

IVA721 Tap 10-Jan 12-Apr 92 0,08 Zero coupon

IVA722 New 15-Jan 19-Apr 94 0,293 Zero coupon

MAQ116 New 16-Jan 09-Feb 23 0,3 Zero coupon

IVA723 New 18-Jan 26-Apr 98 0,395 Zero coupon

IVA722 Tap 22-Jan 19-Apr 87 0,15 Zero coupon

IVA723 Tap 22-Jan 26-Apr 94 0,15 Zero coupon

IPFC17 New 26-Jan 26-Apr 90 0,274 Zero coupon

MAQ117 New 31-Jan 31-Jan 360 0,46 90

IVA724 New 01-Feb 03-May 92 0,365 Zero coupon

IVA726 New 08-Feb 17-May 99 0,3 Zero coupon

CGR37 New 08-Feb 08-Feb 360 0,015 170

MAQ118 New 09-Feb 29-Apr 80 0,195 Zero coupon

IVA727 New 15-Feb 24-May 99 0,368 Zero coupon

IVA726 Tap 15-Feb 17-May 92 0,1 Zero coupon

MAQ119 Tap 19-Feb 19-Mar 30 0,3 Zero coupon

VKC23 New 20-Feb 20-Aug 180 0,14 70

VKC24 New 20-Feb 20-Feb 360 0,1 110

IVA728 New 22-Feb 31-May 98 0,237 Zero coupon

IVA729 New 22-Feb 07-Jun 105 0,22 Zero coupon

EPFC37 New 02-Mar 04-Mar 362 0,09 115

GPT44 New 06-Mar 06-Jun 90 0,50 Fixed

VKC25 New 06-Mar 05-Jun 89 0,077 55

PMM43 New 07-Mar 28-Feb 359 0,25 135

DENG77 New 13-Mar 27-Sep 198 0,02 120

DENG78 New 13-Mar 27-Sep 198 0,01 Fixed

LBK25 New 23-Mar 25-Mar 367 0,500 110

CP (Vanilla) Issuances YTD

Source: JSE, Bloomberg, Nedbank CIB

Summary of issuances2016: R27bn2017: R38,4bn2018(YTD): R6,5bn

DCM TRENDS | 23 MARCH 18 | PAGE 9

REDEMPTIONS – 1H18

Financials

Source: JSE, Bloomberg, Nedbank CIB

Corporates

Source: JSE, Bloomberg, Nedbank CIB

0

500

1000

1500

2000

2500

IBL66 IBL22 ABFN07 ABS10 BCJ12 BWZ18B ABLS3 IBL39 IBL49 LGL03 SBK9 RCSB05 FRX18 IV08 IV09 CBL23 NBK27B IBL91 IBL103 IBL68

12-Mar 15-Mar 17-Mar 23-Mar 27-Mar 31-Mar 02-Apr 03-Apr 10-Apr 12-Apr 14-Apr 30-Apr 18-May 01-Jun 02-Jun 08-Jun 29-Jun

ZAR Mil.

Sum of Issued Amount Sum of Outstanding AmountIssued Amount Outstanding Amount

Nedbank Auction (12 Feb. 2018): Looking to raise R2bn (with option to upsize to R2.5bn), Floaters across 3yr, 5yr, 7.5yr and 10yr tenors

Price Guidance: 3yr: 110-120bps5yr: 135-145bps7.5yr: 160-170bps10yr: 180-195bps

Auction Result: Book Size R6.154bn, Issuance R2,403bnNBK44: 3yr 857MM J+120NBK45: 5yr 372MM J+145NBK46: 7.5yr 398MM J+165NBK47: 10yr 776MM J+190

0

500

1000

1500

2000

2500

AD

CB

01

RD

FB02

NTC

16

MB

F05

4

BEE

R0

2

VK

E05

EPF0

09

IPL7

TPD

A0

3

EQS0

6

EQS0

7

MB

F04

5

IPF1

2

JDG

04

SHS2

8

SSA

05

EQS0

5

MB

P3

4

HIL

B03

VK

E06

REB

01

REB

02

EPF0

02

BSR

17

KA

P00

5

SHS2

3

CIG

04

08-Mar 11-Mar 22-Mar 27-Mar 28-Mar 30-Mar 05-Apr 09-Apr 13-Apr 15-Apr 16-Apr 25-Apr 29-Apr 02-May08-May 21-May 28-May 19-Jun 29-Jun 30-Jun

ZAR Mil.

Sum of Issued Amount Sum of Outstanding AmountIssued Amount Outstanding Amount

Netcare Auction (12 Feb. 2018): Looking to raise R700mln, Floaters across 3yr and 5yr tenors

Price Guidance: 3yr: 150-160bps5yr: 170-180bps

Auction Result: Book Size R1,935bn, Issuance R761mlnNTC22: 3yr 189MM J+155NTC23: 5yr 572MM J+175

Redefine Auction (7 March 2018): Looking to raise R600mln (with option to upsize to R750mln), Floaters across 3yr and 5yr tenors

Price Guidance: 3yr: 140-150bps5yr: 160-170bps

Auction Result: Book Size R1,896bn, Issuance R727mlnRDFB13: 3yr 299MM J+140RDFB14: 5yr 428MM J+160

Summary

R42,8bn of bonds issued are scheduled for redemption or call in the remainder of 1H18. About 20% has already been redeemed orrolled.

Redemptions are concentrated in financial (47%) and corporate (34%) notes.

First Rand has already issued about R5bn in new and tap notes this year

MBSA has R3,75bn maturing across three notes in March and April. The corporate has already raised R1bn in new notes this year through private placements.

DCM TRENDS | 23 MARCH 18 | PAGE 10

REDEMPTIONS – 1H18

State-Owned Enterprises

Source: JSE, Bloomberg, Nedbank CIB

Source: JSE, Bloomberg, Nedbank CIB

0

500

1000

1500

2000

2500

3000

3500

4000

4500

IDCP05 LBK19 DVF18 ES18 COJ04

14-Mar 23-Mar 30-Mar 20-Apr 05-Jun

ZAR Mil.

Sum of Issued Amount Sum of Outstanding AmountIssued Amount Outstanding Amount

Table 1: 1H18 2018 Scheduled Calls/Redemptions

Bond Code Issuer SectorIssued Amount

(Rm) Outstanding Amount

('Rm) % Outstanding

Amount Issue date Maturity Date

EPFC30 Emira Property Fund Ltd Corporate 182,00 0,00 0% 2017/02/22 2018/03/02

ADCB01 Adcorp Holdings Ltd Corporate 400,00 0,00 0% 2013/03/08 2018/03/08

RDFB02 Redefine Properties Ltd Corporate 614,00 614,00 100% 2013/03/11 2018/03/11

IBL66 Investec Bank Ltd Financial 125,00 125,00 100% 2015/03/12 2018/03/12

IDCP05 Industrial Development Corp of South Africa Ltd SOE 500,00 500,00 100% 2013/03/14 2018/03/14

IBL22 Investec Bank Ltd Financial 70,00 70,00 100% 2011/03/15 2018/03/15

ABS10 Absa Bank Ltd Financial 928,00 928,00 100% 2011/03/17 2018/03/17

ABFN07 Absa Bank Ltd Financial 1176,00 1047,00 89% 2011/03/17 2018/03/17

NTC16 Clindeb Investments Pty Ltd Corporate 600,00 600,00 100% 2013/03/22 2018/03/22

BCJ12 Bank of China Ltd/Johannesburg Financial 2200,00 2200,00 100% 2017/03/22 2018/03/23

LBK19 Land & Agricultural Development Bank of South Africa SOE 755,00 755,00 100% 2017/03/23 2018/03/23

BWZ18B Bank Windhoek Ltd Financial 180,00 180,00 100% 2015/03/27 2018/03/27

MBF054 Mercedes-Benz South Africa Pty Ltd Corporate 250,00 250,00 100% 2017/03/27 2018/03/27

BEER02 SABSA Holdings Pty Ltd Corporate 1000,00 1000,00 100% 2013/03/28 2018/03/28

VKE05 Vukile Property Fund Ltd Corporate 100,00 100,00 100% 2013/03/28 2018/03/28

DVF18 Development Bank of Southern Africa Ltd SOE 1295,00 1295,00 100% 2014/09/30 2018/03/30

EPF009 Emira Property Fund Ltd Corporate 60,00 60,00 100% 2016/09/30 2018/03/30

ABLS3 Residual Debt Services Ltd Financial 515,00 0,00 0% 2011/03/31 2018/03/31

Land Bank Auction (19 March 2018): Looking to raise R1.5bn (with option to upsize to R2bn), Floaters across the 1yr, 3yr and 5yr tenors

Price Guidance: 1yr: 95-110 bps3yr: 135-150bps5yr: 200-215 bps

Auction Result: Book size R3,252bn, Issuance R2,015bn LBK25: 1yr 500MM J+100bpsLBK26: 3yr 245MM J+149bpsLBK27: 5yr 1270MM J+215bps

DCM TRENDS | 23 MARCH 18 | PAGE 11

REDEMPTIONS – 1H18

Table 1: 1H18 2018 Scheduled Calls/Redemptions cont

Source: JSE, Bloomberg, Nedbank CIB

Bond Code Issuer Sector Issued Amount (Rm) Outstanding Amount

('Rm) % Outstanding Amount Issue date Maturity Date

IBL39 Investec Bank Ltd Financial 193,00 193,00 100% 2012/04/02 2018/04/02

IBL49 Investec Bank Ltd Financial 1169,00 1169,00 100% 2013/04/02 2018/04/02

LGL03 Liberty Group Ltd Financial 1000,00 1000,00 100% 2012/10/03 2018/04/03

TPDA03 Commissioner Street 5 RF Ltd Corporate 800,00 800,00 100% 2012/10/11 2018/04/05

IPL7 Imperial Group Pty Ltd Corporate 750,00 750,00 100% 2013/04/05 2018/04/05

EQS07 enX Corp Ltd Corporate 106,00 106,00 100% 2013/04/09 2018/04/09

EQS06 enX Corp Ltd Corporate 340,00 340,00 100% 2013/04/09 2018/04/09

EQS06 enX Corp Ltd Corporate 340,00 340,00 100% 2013/04/09 2018/04/09

SBK9 Standard Bank of South Africa Ltd/The Financial 1500,00 1500,00 100% 2006/04/10 2018/04/10

RCSB05 BNP Paribas Personal Finance South Africa Ltd Financial 170,00 170,00 100% 2013/04/12 2018/04/12

MBF045 Mercedes-Benz South Africa Pty Ltd Corporate 1500,00 1500,00 100% 2015/04/13 2018/04/13

FRX18 FirstRand Bank Ltd Financial 1581,00 1551,00 98% 2010/04/14 2018/04/14

JDG04 JD Group Ltd/South Africa Corporate 300,00 0,00 0% 2013/04/15 2018/04/15

IPF12 Investec Property Fund Ltd Corporate 100,00 0,00 0% 2015/04/15 2018/04/15

SHS28 Steinhoff Services Ltd Corporate 300,00 0,00 0% 2015/11/13 2018/04/15

SSA05 Sappi Southern Africa Pty Ltd Corporate 500,00 500,00 100% 2013/04/16 2018/04/16

ES18 Eskom Holdings SOC Ltd SOE 4000,00 2338,84 58% 2009/04/20 2018/04/20

EQS05 enX Corp Ltd Corporate 900,00 600,00 67% 2012/04/25 2018/04/25

MBP34 Mercedes-Benz South Africa Pty Ltd Corporate 2000,00 2000,00 100% 2015/04/29 2018/04/29

IV08 Investec Bank Ltd Financial 200,00 200,00 100% 2008/04/30 2018/04/30

IV09 Investec Bank Ltd Financial 200,00 200,00 100% 2008/04/30 2018/04/30

HILB03 Hyprop Investments Ltd Corporate 450,00 450,00 100% 2013/05/02 2018/05/02

VKE06 Vukile Property Fund Ltd Corporate 380,00 380,00 100% 2015/05/08 2018/05/08

CBL23 Capitec Bank Ltd Financial 500,00 500,00 100% 2015/05/18 2018/05/18

REB01 Rebosis Property Fund Ltd Corporate 230,00 230,00 100% 2015/05/21 2018/05/21

REB02 Rebosis Property Fund Ltd Corporate 100,00 100,00 100% 2016/07/22 2018/05/21

EPF002 Emira Property Fund Ltd Corporate 300,00 300,00 100% 2014/05/30 2018/05/28

NBK27B Nedbank Ltd Financial 1427,00 1427,00 100% 2015/06/01 2018/06/01

IBL91 Investec Bank Ltd Financial 100,00 100,00 100% 2016/06/02 2018/06/02

COJ04 City of Johannesburg South Africa Municipal 1733,00 1733,00 100% 2006/06/05 2018/06/05

IBL103 Investec Bank Ltd Financial 150,00 150,00 100% 2017/06/09 2018/06/08

BSR17 Basil Read Ltd Corporate 50,00 0,00 0% 2015/06/19 2018/06/19

SHS23 Steinhoff Services Ltd Corporate 400,00 0,00 0% 2015/06/29 2018/06/29

IBL68 Investec Bank Ltd Financial 130,00 130,00 100% 2015/06/29 2018/06/29

KAP005 KAP Industrial Holdings Ltd Corporate 240,00 240,00 100% 2016/06/29 2018/06/29

CIG04 Consolidated Infrastructure Group Ltd Corporate 134,00 134,00 100% 2014/06/30 2018/06/30

DCM TRENDS | 23 MARCH 18 | PAGE 12

SPREAD DEVELOPMENT

February/March 2018 Spread Development

Source: JSE, Bloomberg, Nedbank CIB

Standard Bank Group’s Tier 2 bond (SBT201) spread of 314bps cleared at the top-end of price guidance (295-315bps). We think this follows from the last price point, which was FirstRand’s R2,75bn issue at 315bps in September 2017. We note that these bonds were issued in different market windows. The FirstRand note was issued prior to the 2017 MTBPS, while the Standard Bank note was issued just before the National Budget Speech 2018.

Nedbank set a new price point for its Tier 2 notes, with its spread clearing towards the lower-end of price guidance (275-350bps) at 305bps. Both Standard Bank and Nedbank issued at the Holdco-level. Investors seem comfortable with the structural subordination (given the strong bid appetite), but perhaps the high demand for these assets is keeping the spread differential between the Opco and Holdco sub-debt issuances at nil. The trajectory for sub-debt is for further spread tightening, if the issuance window is timed correctly, with perhaps a psychological barrier at J+300bps for Tier 2 notes.

Netcare’s NTC22 and NTC23 auction finished 5bps below the previous clearing levels of similar bonds issued in mid-2017 (NTC20, 3yr, J+160 ; NTC21, 5yr, J+180).

0

100

200

300

400

500

600

0

0.5

1

1.5

2

2.5

3

3.5

AA+ N/R AA+ AAA AA+ A+ AA+ AA+ AA+ A+ AA+ AA+ A AAA AA+ A+ AAA AA+ BBB+ BB+ AA+ AAA AAA AA+ AA+ AA- AAA BBB

SBS37 CGR38 FRJ22 MBP039NBK44B NTC22 SBS47 IBL110 RDFB13 HPF11 BAW29 FRJ23 IPF24 MBP040NBK45B NTC23 GRT24GRDFB14 NGL04 INLV05 NBK46BGRT25G ES33 FRX32 NBK47BNRA028GRT26G SBT201

Sr Unsecured Sr Unsecured Secured Sr Unsecured Subordinated . Sr Unsecured Sr Unsecured Subordinated

1- 3Years

3-5 Years 5-7 Years 7-10 Years 10-20 Years

Spre

ad (

bp

s)

Vo

lum

e ('

Rb

n)

Bonds (Vanilla) - Amount Issued ('Rbn) Bonds (Vanilla) - Spread at issue (bps)

Jr Subordinated

DCM TRENDS | 23 MARCH 18 | PAGE 13

0

50

100

150

200

250

300

350

400

450

500

0

0.2

0.4

0.6

0.8

1

1.2

FBJ20ZFNB

NamibiaLtd

BPPF02BNP

ParibasPersonal

Finance SA

CBL27Capitec

IBL100Investec

ABFN20Absa

SBS54SBSA

KST01 PSGKonsult

Treasury

IBL104Investec

IBL106Investec

BPPF04BNP

ParibasPersonal

Finance SA

SBS59SBSA

BCJ15 Bankof China

GBL03Grindrod

Bank

BCJ16 Bankof China

LHL27LetshegoHoldings

NBK44BNedbank

IBL110Investec

AA- AAA A AA- AA- AA- A- AA- AA AAA AA+ AAA BBB+ AAA A- AA+ AA+

20-Mar-17 22-Mar-17 12-May-17 24-May-17 30-May-17 12-Jun-17 12-Jul-17 17-Jul-17 04-Aug-17 15-Sep-17 09-Oct-17 09-Nov-17 16-Nov-17 08-Dec-17 13-Dec-17 15-Feb-18 07-Mar-18

Spre

ad

Vo

lum

e

Amount Issued ('Rbn) Spread at issue (bps)

Mixed rate note

SPREAD DEVELOPMENT

3-Year New Issuances – Financials

Source: JSE, Bloomberg, Nedbank CIB

3-Year New Issuances – Corporates and State-Owned Enterprises

Source: JSE, Bloomberg, Nedbank CIB

Secured Not guaranteed

Sr. UnsecuredNot guaranteed

Sr. UnsecuredGuaranteed

Sr. UnsecuredGuaranteedSr. Unsecured

Guaranteed

0

50

100

150

200

250

300

350

400

450

0

0.5

1

1.5

2

2.5

GR

T18

Gro

wth

po

int

IPF2

0 In

vest

ec P

rop

erty

Fu

nd

TFS1

44 T

FSA

LBK

17

Lan

d B

ank

RD

FB10

Red

efin

e

MB

F05

5 M

BSA

DV

F20B

DB

SA

SHS3

0 St

ein

ho

ff

MB

P03

6 M

BSA

VK

E09

Vu

kile

Pro

per

ty F

un

d

BA

W2

5 B

arlo

wo

rld

KA

P00

9 K

AP

MB

P03

7 M

BSA

EPF0

11

Emir

a

PM

M38

Pre

miu

m P

rop

erti

es

BID

07 B

idve

stco

SHS3

2 St

ein

ho

ff

MTN

06 M

TN

CG

R3

2 C

algr

o

NTC

20

Net

care

APF

05 A

ccel

erat

e P

rop

erty

Fu

nd

MB

F05

7 M

BSA

DV

F20C

DB

SA

TL22

Tel

kom

LBK

22

Lan

d B

ank

KA

P01

0 K

AP

CG

R3

3 C

algr

o

WH

L01

Wo

olw

ort

hs

Ho

ldin

gs

MTN

08 M

TN

TFS1

47 T

FSA

DV

F20D

DB

SA

EPF0

12

Emir

a

TFS1

51 T

FSA

CG

R3

8 C

algr

o

NTC

22

Net

care

MB

P03

9 M

BSA

RD

FB13

Red

efin

e

AAA A AAA AA+ AA AAA AA+ AA- AAA AA+ AA- A+ AAA A A AA+ AA+ AA- N/R A+ AA- AAA AA+ AA+ A+ N/R A+ AA- AAA AA+ A AAA N/R A+ AAA AA+

13-Mar-

17

17-Mar-

17

20-Mar-

17

22-Mar-

17

27-Mar-17 28-Mar-

17

05-Apr-17

11-Apr-17

08-May-

17

09-May-

17

24-May-

17

26-May-

17

12-Jun-17

14-Jun-17

30-Jun-17

10-Jul-17

13-Jul-17

21-Jul-17

27-Jul-17

24-Aug-17

28-Aug-17

29-Aug-17

04-Sep-17 15-Sep-17

22-Sep-17

10-Oct-17

11-Oct-17

12-Oct-17

23-Oct-17

06-Nov-

17

30-Nov-

17

13-Feb-18

15-Feb-18

23-Feb-18

12-Mar-

18

Spre

ad

Vo

lum

e

Amount Issued ('Rbn) Spread at issue (bps)

Secured

Secured

NOTE:# Notes are Senior Unsecured unless stated otherwise## Spreads are floating (above 3-month JIBAR), Fixed rates are represented comparably as swap spreads

NOTE:# Notes are Senior Unsecured unless stated otherwise## Spreads are floating (above 3-month JIBAR), Fixed rates are represented comparably as swap spreads

DCM TRENDS | 23 MARCH 18 | PAGE 14

0

100

200

300

400

500

600

0

0.5

1

1.5

2

2.5

3

3.5

FRJ22FirstRand

NGL02Nedbank

Group

FBJ22ZFNB

NamibiaLtd

SBT101Standard

BankGroup

IBL101Investec

IBL102Investec

BGL16Barclays

AfricaGroup

ABFN21Absa

SBS55SBSA

SBS56SBSA

NGLT1ANedbank

Group

BGT01Barclays

AfricaGroup

SBT102Standard

BankGroup

FRS171FirstRand

DSY01Discovery

SBS60SBSA

FRJ23FirstRand

SBT201Standard

BankGroup

NBK45BNedbank

INLV05Investec

NGL04Nedbank

Group

AA A- AA- BBB AA- BBB AA- AA- B+ BBB- BB- AA+ AA- AA+ AA+ BBB AA+ BB+ BBB+

07-Mar-17

14-Mar-17

20-Mar-17

30-Mar-17

24-May-17 30-May-17

12-Jun-17 30-Jun-1711-Sep-1721-Sep-1716-Oct-17 21-Nov-17

18-Jan-18 31-Jan-18 12-Feb-1815-Feb-18 15-Mar-18

19-Mar-18

Spre

ad

Vo

lum

e

Amount Issued ('Rbn) Spread at issue (bps)

SPREAD DEVELOPMENT

5-Year New Issuances – Financials

Source: JSE, Bloomberg, Nedbank CIB

5-Year New Issuances – Corporates and State-Owned Enterprises

Source: JSE, Bloomberg, Nedbank CIB

Jr. Subordinated

Subordinated

Jr. Subordinated

0

50

100

150

200

250

300

350

0

0.5

1

1.5

2

2.5

GR

T19

Gro

wth

po

int

IPF2

1 In

vest

ec P

rop

erty

Fu

nd

TFS1

45 T

FSA

LBK

18

Lan

d B

ank

RD

FB11

Red

efin

e

DV

F22

DB

SA

VK

E10

Vu

kile

Pro

per

ty F

un

d

BA

W2

8 B

arlo

wo

rld

LBK

20

Lan

d B

ank

IPF2

2 In

vest

ec P

rop

erty

Fu

nd

BID

08 B

idve

stco

SHS3

3 St

ein

ho

ff

MTN

07 M

TN

NTC

21

Net

care

EQS1

0 en

X

APF

06 A

ccel

erat

e P

rop

erty

Fu

nd

DV

F22B

DB

SA

LBK

23

Lan

d B

ank

TL23

Tel

kom

TL24

Tel

kom

MTN

09 M

TN

TFS1

48 T

FSA

RES

40

Res

ilien

t

GR

T22

Gro

wth

po

int

DV

F22C

DB

SA

KA

P11

KA

P

MB

P03

8 M

BSA

SHS3

4 St

ein

ho

ff

FIFB

14 F

ort

ress

FIFB

15 F

ort

ress

RD

FB12

Red

efin

e

KA

P01

2 K

AP

RES

41

Res

ilien

t

IDC

P07

IDC

IPF2

4 In

vest

ec P

rop

erty

Fu

nd

NTC

23

Net

care

HPF

11

HPF

BA

W2

9 B

arlo

wo

rld

MB

P04

0 M

BSA

GR

T24

G G

row

thp

oin

t

RD

FB14

Red

efin

e

AAA A AAA AA+ AA AA+ AA+ AA- AA+ A AA+ AA+ AA- A+ BBB AA- AA+ AA+ AA- AAA AA- AAA AA+ A+ AAA B- AA AA AA+ A+ AA- AA+ A A+ A+ AA+ AAA AAA AA+

13-Mar-

17

17-Mar-

17

20-Mar-

17

22-Mar-

17

27-Mar-

17

28-Mar-

17

08-May-

17

06-Jun-17

08-Jun-17

14-Jun-17

30-Jun-17

10-Jul-17

13-Jul-17

27-Jul-17

28-Jul-17

24-Aug-17

29-Aug-17

04-Sep-17 11-Oct-17

12-Oct-17

13-Oct-17

16-Oct-17

23-Oct-17

24-Oct-17

02-Nov-

17

03-Nov-

17

07-Nov-

17

20-Nov-

17

27-Nov-

17

30-Nov-17 15-Dec-17

05-Feb-18

15-Feb-18

19-Feb-18

22-Feb-18

23-Feb-18

09-Mar-

18

12-Mar-

18

Spre

ad

Vo

lum

e

Amount Issued ('Rbn) Spread at issue (bps)

Secured

Secured

Secured

NOTE:# Notes are Senior Unsecured unless stated otherwise## Spreads are floating (above 3-month JIBAR), Fixed rates are represented comparably as swap spreads

Jr. Subordinated

Subordinated

Jr. Subordinated

NOTE:# Notes are Senior Unsecured unless stated otherwise## Spreads are floating (above 3-month JIBAR), Fixed rates are represented comparably as swap spreads

DCM TRENDS | 23 MARCH 18 | PAGE 15

SPREAD DEVELOPMENT

≥7-Year New Issuances – Financials

Source: JSE, Bloomberg, Nedbank CIB

≥7-Year New Issuances – Corporates and State-Owned Enterprises

Source: JSE, Bloomberg, Nedbank CIB

0

50

100

150

200

250

300

350

400

450

0

0.5

1

1.5

2

2.5

3

AB

FN2

2 A

bsa

SBS5

7 S

BSA

BG

L17

Bar

clay

s A

fric

a G

rou

p

LGL0

9 L

iber

ty G

rou

p

BG

L19

Bar

clay

s A

fric

a G

rou

p

FRS1

72

Firs

tRan

d

AB

FN2

4 A

bsa

AB

FN2

5 A

bsa

DSY

02 D

isco

very

DSY

03 D

isco

very

NB

K46B

Ned

ban

k

FRX

27 F

irst

Ran

d

FRX

32 F

irst

Ran

d

BG

L15

Bar

clay

s A

fric

a G

rou

p

SBS5

2 S

BSA

SBS5

3 S

BSA

AB

FN2

3 A

bsa

NG

L03

Ned

ban

k G

rou

p

SBS5

8 S

BSA

IV04

6 In

vest

ec

SNT0

4 Sa

nta

m

FRB

I29

Fir

stR

and

FRB

23

Firs

tRan

d

BG

L18

Bar

clay

s A

fric

a G

rou

p

AB

FN2

6 A

bsa

MM

IG06

MM

I Gro

up

OM

I01

Old

Mu

tual

Insu

re

MM

IG06

MM

I Gro

up

NB

K47B

Ned

ban

k

AA- AA- BBB AA BBB AA+ AA AA- AA+ AA A- A A AA- BBB AA- AA- AA- AA- AA BBB AA AA A+ AA AA+

30-May-

17

12-Jun-17

14-Aug-17

28-Aug-17

29-Sep-17

16-Oct-17

17-Oct-17 21-Nov-17 15-Feb-18

07-Mar-17 16-Mar-

17

25-Apr-17

02-May-

17

25-May-17 12-Jun-17

21-Jun-17

27-Jun-17

27-Jul-17

20-Sep-17

29-Sep-17

17-Oct-17

19-Oct-17

20-Nov-

17

04-Dec-17

15-Feb-18

7-10 Years 10-20 Years

Spre

ad

Vo

lum

e

Amount Issued ('Rbn) Spread at issue (bps)

Subordinated Unsecured

Subordinated Unsecured

Subordinated Unsecured

Subordinated Unsecured

NOTE:# Notes are Senior Unsecured unless stated otherwise## Spreads are floating (above 3-month JIBAR), Fixed rates are represented comparably as swap spreads

0

50

100

150

200

250

0

0.2

0.4

0.6

0.8

1

1.2

GRT20Growthpoint

GRT21Growthpoint

TL25 Telkom LBK24 LandBank

MTN10 MTN GRT23Growthpoint

DVF24 DBSA TL26 Telkom GRT25GGrowthpoint

EMM07 EMM CCT04 City ofCape Town

EMM07PEMM

GRT26GGrowthpoint

AAA AA+ AA+ AA- AAA AA+ AA+ AAA AAA AAA AAA

23-Mar-17 04-Sep-17 10-Oct-17 11-Oct-17 16-Oct-17 23-Oct-17 24-Nov-17 09-Mar-18 10-Jul-17 17-Jul-17 09-Mar-18

7-10 Years 10-20 Years

Spre

ad

Vo

lum

e

Amount Issued ('Rbn) Spread at issue (bps)

DCM TRENDS | 23 MARCH 18 | PAGE 16

BOND CURVES

Corporate Relative Value Yield Curve

Source: Bloomberg

Financials Relative Value Yield Curve

Source: Bloomberg

USD Billions

USD Billions

DCM TRENDS | 23 MARCH 18 | PAGE 17

BOND CURVES

State-Owned Enterprises Relative Value Yield Curve

Source: Bloomberg

Consolidated Relative Value Yield Curve (All Bonds Issued)

Source: Bloomberg

USD Billions

USD Billions

DCM TRENDS | 23 MARCH 18 | PAGE 18

RATINGS DISTRIBUTION

Issuances LTM – Clustering of issuances in the “AA” band

Source: JSE, Bloomberg, Nedbank CIB

Issuers/Notes Standardised Rating Distribution

Source: JSE, Bloomberg, Nedbank CIB

0

5

10

15

20

25

30

AAA

AA+

AA

AA-

A+

A

A-

BBB+

BBB

BBB-

BB-

B+

B-

N/R

Bonds (Vanilla)

Amount Issued ('Rbn)

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

AAA AA+ AA AA- A+ A A- BBB+ BBB BBB- BB- B+ B B- NR

Nu

mb

er o

f Is

suer

s

Standardised Rating

Calgro is the only issuer in the market that is not rated

DCM TRENDS | 23 MARCH 18 | PAGE 19

RATINGS DISTRIBUTION

S&P Ratings Distribution

Source: JSE, Bloomberg, Nedbank CIB

Moody’s Ratings Distribution

Source: JSE, Bloomberg, Nedbank CIB

0

1

2

3

4

5

6

Ban

k

Insu

ran

ce

Man

ufa

ctu

rin

g &

Ind

ust

rial

Mu

nic

ipal

ity

NB

FI

Pro

pe

rty

Ban

k

Bu

sin

ess

Serv

ices DFI

Min

ing

Mu

nic

ipal

ity

Pro

pe

rty

Tele

com

s, M

edia

& IC

T

Tran

spo

rt &

Lo

gist

ics

Ban

k

Insu

ran

ce

Ban

k

Insu

ran

ce

Tele

com

s, M

edia

& IC

T

Tran

spo

rt &

Lo

gist

ics

Tran

spo

rt &

Lo

gist

ics

Ban

k

Mu

nic

ipal

ity

Ban

k

Po

wer

Po

wer

Po

wer

NB

FI

AAA AA+ AA AA- A+ BBB+ BBB CC

Nu

mb

er

of

Issu

ers

/No

tes

rate

d

Guaranteed Senior Unsecured Guaranteed Subordinated Hybrid/Junior Subordinated/Prefs. Lower Tier II Subordinated Senior Unsecured

Senior Unsecured (IFS) Senior Unsecured/RCF Subordinated Tier II Subordinated Upper Tier II Subordinated

0

1

2

3

4

5

6

7

Ban

k

Min

ing

Insu

ran

ce

Sove

reig

n

Tran

spo

rt &

Lo

gist

ics

Wat

er

Wat

er

Min

ing

Tele

com

s, M

edia

& IC

T

Tran

spo

rt &

Lo

gist

ics

Ban

k

Insu

ran

ce

Min

ing

NB

FI

Ret

ail

Ban

k

Insu

ran

ce

Ban

k

Min

ing

Ban

k

Man

ufa

ctu

rin

g &

Ind

ust

rial

Min

ing

Po

wer

AAA AA+ AA AA- A+ A BBB+ BBB B

Nu

mb

er o

f Is

suer

s/N

ote

s ra

ted

Guaranteed Senior Unsecured Hybrid/Junior Subordinated/Prefs. Lower Tier II Subordinated Senior Secured

Senior Unsecured Senior Unsecured (IFS) Senior Unsecured/RCF Subordinated

Tier II Subordinated Tier II Subordinated (deferrable) Tier II Subordinated (non-deferrable) Upper Tier II Subordinated

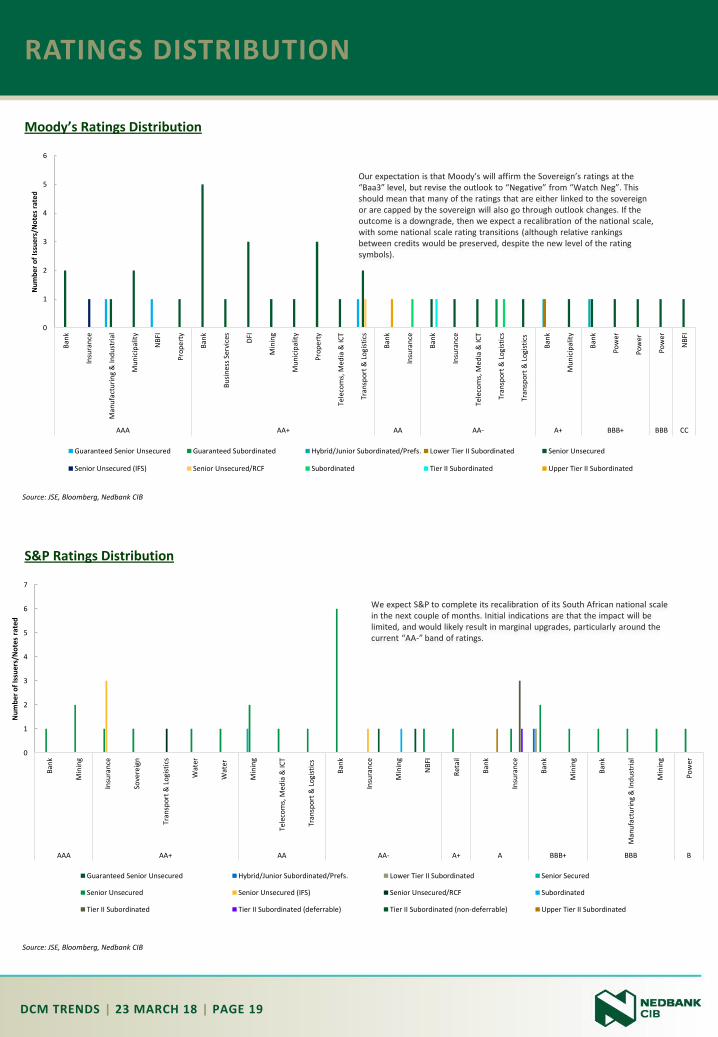

We expect S&P to complete its recalibration of its South African national scale in the next couple of months. Initial indications are that the impact will be limited, and would likely result in marginal upgrades, particularly around the current “AA-” band of ratings.

Our expectation is that Moody’s will affirm the Sovereign’s ratings at the “Baa3” level, but revise the outlook to “Negative” from “Watch Neg”. This should mean that many of the ratings that are either linked to the sovereign or are capped by the sovereign will also go through outlook changes. If the outcome is a downgrade, then we expect a recalibration of the national scale, with some national scale rating transitions (although relative rankings between credits would be preserved, despite the new level of the rating symbols).

DCM TRENDS | 23 MARCH 18 | PAGE 20

RATINGS DISTRIBUTION

GCR Ratings Distribution

Source: JSE, Bloomberg, Nedbank CIB

Fitch Ratings Distribution

Source: JSE, Bloomberg, Nedbank CIB

0

1

2

3

4

5

6

7

8

9

Insu

ran

ce

Man

ufa

ctu

rin

g &

Ind

ust

rial

Tran

spo

rt &

Lo

gist

ics

DFI

Insu

ran

ce

Po

wer

Wat

er

Wat

er

Ban

k

Insu

ran

ce

Tele

com

s, M

edia

& IC

T

Tran

spo

rt &

Lo

gist

ics

Ban

k

Ban

k

Po

wer

AAA AA+ AA AA- A

Nu

mb

er o

f Is

suer

s/N

ote

s ra

ted

Guaranteed Senior Unsecured Hybrid/Junior Subordinated/Prefs. Senior Unsecured Senior Unsecured (IFS) Senior Unsecured/RCF

Term Loan Term Loan/Bond Tier II Subordinated Upper Tier II Subordinated

0

1

2

3

4

5

Insu

ran

ce

Ban

k

DFI

Pro

pe

rty

Ban

k

Mu

nic

ipal

ity

Pro

pe

rty

Ban

k

Insu

ran

ce

Pro

pe

rty

Ban

k

DFI

Hea

lth

care

Insu

ran

ce

Man

ufa

ctu

rin

g &

Ind

ust

rial

NB

FI

Pro

pe

rty

Bu

sin

ess

Serv

ices

Edu

cati

on

Man

ufa

ctu

rin

g &

Ind

ust

rial

Pro

pe

rty

Ret

ail

Tele

com

s, M

edia

& IC

T

Ban

k

Co

nst

ruct

ion

Man

ufa

ctu

rin

g &

Ind

ust

rial

Min

ing

NB

FI

Pro

pe

rty

Ban

k

Insu

ran

ce

NB

FI

Pro

pe

rty

Ret

ail

Co

nst

ruct

ion

Edu

cati

on

Insu

ran

ce

NB

FI

Pro

pe

rty

Tran

spo

rt &

Lo

gist

ics

Bu

sin

ess

Serv

ices

Edu

cati

on

Tele

com

s, M

edia

& IC

T

NB

FI

AAA AA+ AA AA- A+ A A- BBB+ BBB BBB- BB- B

Nu

mb

er o

f Is

suer

s/N

ote

s ra

ted

Senior Secured Senior Unsecured Senior Unsecured (CPA) Senior Unsecured (IFS) Tier II Subordinated Tier II Subordinated

DCM TRENDS | 23 MARCH 18 | PAGE 21

CONTACTS

Analysts

Nthulleng MphahleleAnalystTel : +27 11 294 7032 [email protected]

Jones GondoSenior Credit Research Analyst Tel : +27 11 294 [email protected]

Links To Recent Publications

• Fixed Income Credit Insights: SA Sovereign Credit Rating Preview – Moody’s, Published 20 March 2018• Fixed Income Credit Insights: Pre-Budget Credit Insight, Published 21 February 2018• Fixed Income Credit Insights: Market Update – Eskom Holdings SOC Ltd, Published 18 January 2018• Fixed Income Credit Insights: Market Update – Steinhoff, Published 16 January 2018