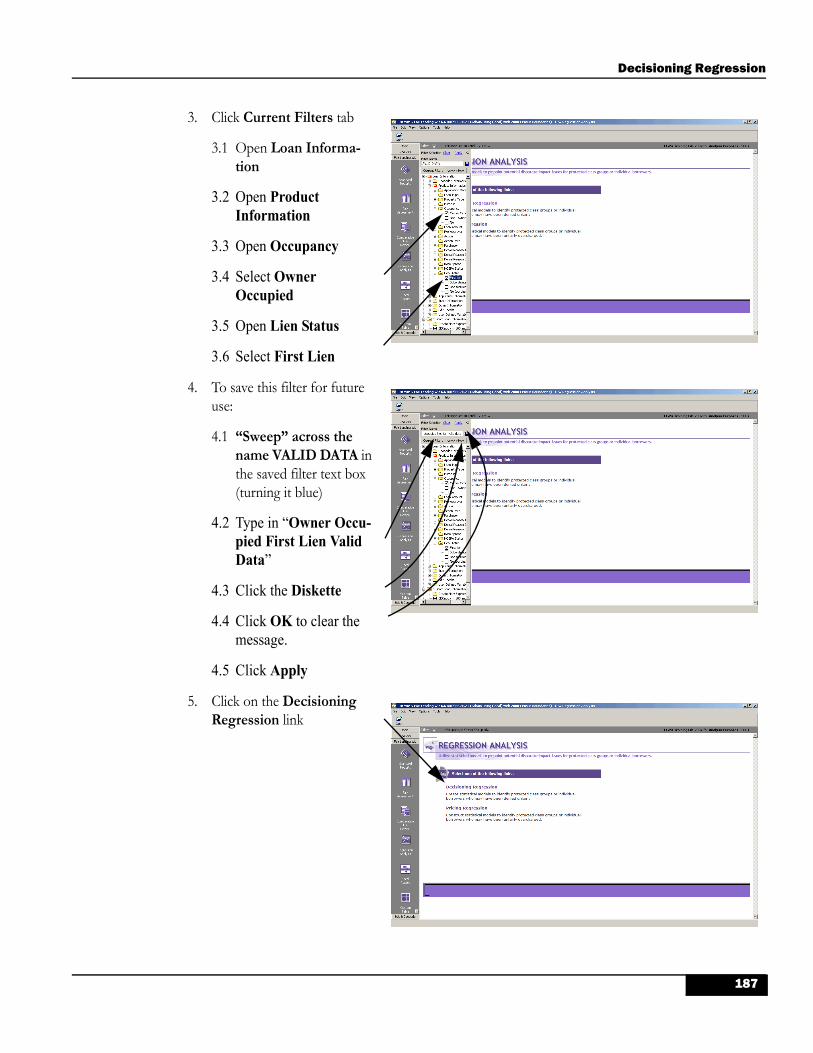

fl wiz training manual 9-08… · cra/fl wiz file but allows a user to change and/or add new...

TRANSCRIPT

Fair Lending Wiz®

Training Guide

Date: 9/2008

© Wolters Kluwer Financial ServicesWiz is registered in the U.S. Patent and Trademark Office.

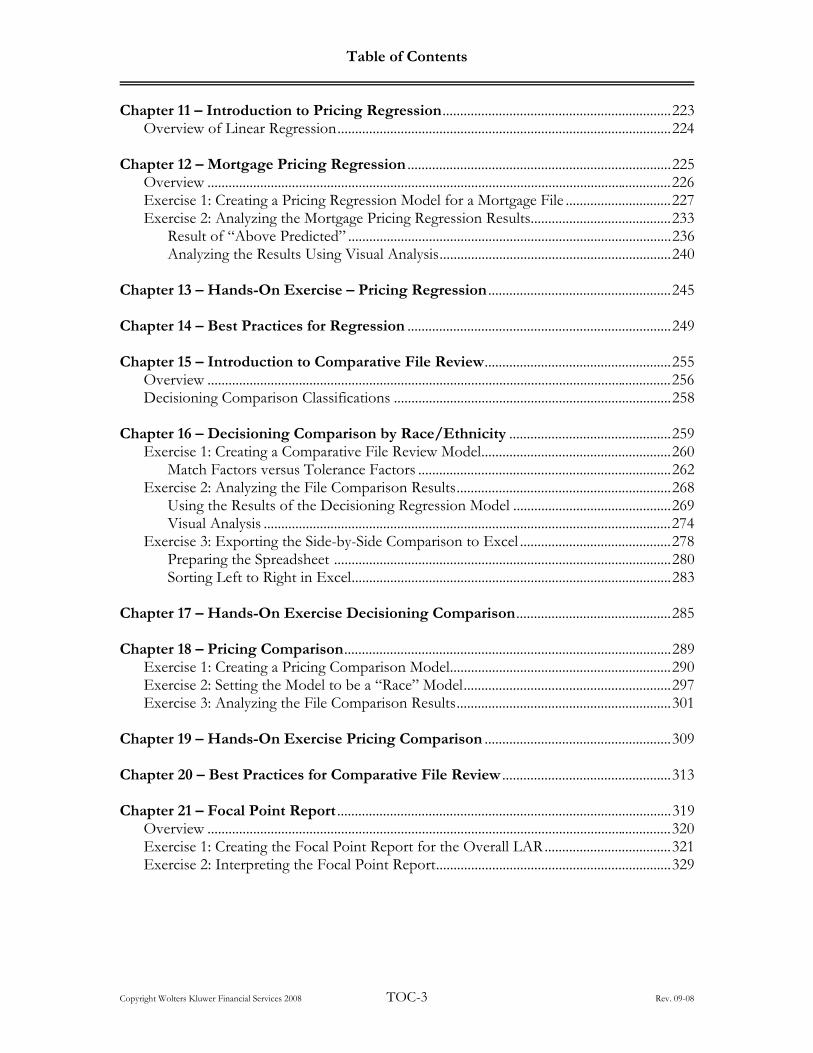

Fair Lending Wiz Training Guide Table of Contents

Chapter 1 – Importing ...................................................................................................................... 7 Overview ........................................................................................................................................ 8 Exercise 1: Importing a File Into FL Wiz ................................................................................. 9 Exercise 2: Updating an Existing File ......................................................................................21 Chapter 2 – Editing Data for Fair Lending .............................................................................29 Overview .....................................................................................................................................30 Exercise 1: Reviewing Data .......................................................................................................31 Exercise 2: Replacing Zeroes with “Nulls” .............................................................................41 Exercise 3: Using Modify Codes to Allow User Defined Fields to be Used......................45 Chapter 3 – Custom Tables ..........................................................................................................51 Overview ......................................................................................................................................52 Exercise 1: Obtaining a Distribution by Loan Product.........................................................53 Exercise 2: Calculating the Average APR by Loan Product .................................................61 Chapter 4 – File Management ....................................................................................................69 Overview ......................................................................................................................................70 Exercise 1: Copying a File..........................................................................................................71 Exercise 2: Copy with Filter ......................................................................................................73 Exercise 3: Modifying a File’s Structure...................................................................................78 Exercise 4: Adding Values to a New Field ..............................................................................81 Exercise 5: Adding/Modifying New Codes ............................................................................86 Exercise 6: Transferring/Installing a File ................................................................................89 Chapter 5 – Introduction to Statistics........................................................................................93 Overview ......................................................................................................................................94 Chapter 6 – Fair Lending Examination Procedures .............................................................99 Examination Scope Guidelines ...............................................................................................101 Understanding Credit Operations....................................................................................102 Evaluating the Potential for Discriminatory Conduct ..................................................104 Compliance Program Discrimination Risk Factors.......................................................106 Identify Residential Lending Risk Factors.............................................................................107 Overt Risk Factors .............................................................................................................109 Underwriting Risk Factors ................................................................................................109 Pricing Risk Factors ...........................................................................................................109 Steering Risk Factors..........................................................................................................110 Redlining Risk Factors .......................................................................................................110 Marketing Risk Factors......................................................................................................112

Table of Contents

Copyright Wolters Kluwer Financial Services 2008 TOC-2 Rev. 09-08

Identify Consumer Lending Risk Factors..............................................................................113 Identify Commercial Lending Risk Factors...........................................................................114 Chapter 7 – Data Integrity and Scoping .................................................................................117 Overview ....................................................................................................................................118 Exercise 1: Generating Reports with Filters..........................................................................119 Summary Report – Action Taken and Standard Summary Report without Filters..120 Summary Reports with Filters ..........................................................................................125 Exercise 2: Generating Data Quality Reports.......................................................................127 Understanding Data Quality Reports ..............................................................................130 Applying a Filter to Data Quality Reports......................................................................132 Exercise 3: Generating and Understanding Difference of Means Reports ......................138 Analyzing the APR.............................................................................................................143 Analyzing the Credit Score................................................................................................146 Analyzing Denied Credits using the Difference of Means Reports............................147 Exercise 4: Generating Risk Factor Reports .........................................................................149 Disparities in Denial Rates (Underwriting).....................................................................153 Disparities in Processing Times (Underwriting) ............................................................156 Credit Score Overrides (Underwriting) ...........................................................................159 Proportion of FHA versus Conventional Mortgages (Steering) .................................164 Redlining Reports ...............................................................................................................166 Exercise 5: HMDA Scoping Reports .....................................................................................168 Differences in Average Rate Spread ................................................................................171 Pricing Disparity Summary ...............................................................................................173 Risk Score by Geography ..................................................................................................175 Chapter 8 – Introduction to Decisioning Regression .........................................................179 Overview of Logistic Regression ...........................................................................................180 Specific Examples of Logistic Regression .............................................................................181 Chapter 9 – Decisioning Regression .......................................................................................183 Overview – Factors to Use in Regression Models ...............................................................184 Exercise 1: Creating a Decisioning Regression Model ........................................................185 Exercise 2: Analyzing Decisioning Regression Results .......................................................191 Advanced Statistics.............................................................................................................195 Race ......................................................................................................................................196 Denied and Review – Details ...........................................................................................197 Reviewing the Applicant Detail Record..........................................................................199 Visual Analysis ....................................................................................................................201 Exercise 3: Changing the % Cutoff ........................................................................................208 Exercise 4: Exporting and Printing Lists of Applicants ......................................................211 Chapter 10 – Hands-On Exercise Decisioning Regression ..............................................219

Table of Contents

Copyright Wolters Kluwer Financial Services 2008 TOC-3 Rev. 09-08

Chapter 11 – Introduction to Pricing Regression.................................................................223 Overview of Linear Regression...............................................................................................224 Chapter 12 – Mortgage Pricing Regression ...........................................................................225 Overview ....................................................................................................................................226 Exercise 1: Creating a Pricing Regression Model for a Mortgage File ..............................227 Exercise 2: Analyzing the Mortgage Pricing Regression Results........................................233 Result of “Above Predicted” ............................................................................................236 Analyzing the Results Using Visual Analysis..................................................................240 Chapter 13 – Hands-On Exercise – Pricing Regression ....................................................245 Chapter 14 – Best Practices for Regression ...........................................................................249 Chapter 15 – Introduction to Comparative File Review.....................................................255 Overview ....................................................................................................................................256 Decisioning Comparison Classifications ...............................................................................258 Chapter 16 – Decisioning Comparison by Race/Ethnicity ..............................................259 Exercise 1: Creating a Comparative File Review Model......................................................260 Match Factors versus Tolerance Factors ........................................................................262 Exercise 2: Analyzing the File Comparison Results.............................................................268 Using the Results of the Decisioning Regression Model .............................................269 Visual Analysis ....................................................................................................................274 Exercise 3: Exporting the Side-by-Side Comparison to Excel ...........................................278 Preparing the Spreadsheet ................................................................................................280 Sorting Left to Right in Excel...........................................................................................283 Chapter 17 – Hands-On Exercise Decisioning Comparison............................................285 Chapter 18 – Pricing Comparison.............................................................................................289 Exercise 1: Creating a Pricing Comparison Model...............................................................290 Exercise 2: Setting the Model to be a “Race” Model...........................................................297 Exercise 3: Analyzing the File Comparison Results.............................................................301 Chapter 19 – Hands-On Exercise Pricing Comparison .....................................................309 Chapter 20 – Best Practices for Comparative File Review ................................................313 Chapter 21 – Focal Point Report ...............................................................................................319 Overview ....................................................................................................................................320 Exercise 1: Creating the Focal Point Report for the Overall LAR....................................321 Exercise 2: Interpreting the Focal Point Report...................................................................329

Table of Contents

Copyright Wolters Kluwer Financial Services 2008 TOC-4 Rev. 09-08

Blank Page

Importing

Chapter 1

Importing

Upon completion of this lesson you will be able to:

Import a loan file.

Add records from one file into an existing file using the Update feature.

7

Fair Lending Wiz Training Guide

Overview

In order to have the most robust Fair Lending analysis, having access to relevant fields contained in your LOS (loan origination system) will enable you to perform a comprehensive analysis. But some-times those fields are not captured in your LOS. How can you include them in your file once you’ve received an extract containing the basic fields?

The following exercise will take you through the steps which will enable you to add, or update, data into an existing CRA/FL Wiz file. But before we can add information to an existing file, we must first import a file that has been generated from your LOS. When reviewing the extract, you notice that you will need to include fair lending fields to perform an in-depth fair lending analysis, fields such as Credit Score, LTV, and Back End Ratio, to name a few.

Your MIS group has provided you with an extract containing the standard HMDA fields, and has also provided you with another file that includes various fair lending fields. You need to import the extract file, then add the additional fields to your extract file.

8

Importing

Exercise 1: Importing a File Into FL Wiz

There are three ways to import a file: (1) Importing a New File, (2) Updating an Existing File, and (3) Appending to an Existing File. Importing a New File brings new information into CRA/FL Wiz. Importing using the Update a File feature makes use of an existing CRA/FL Wiz file but allows a user to change and/or add new informa-tion into that file. Importing data using the Append a File feature allows the user to only add new information into an existing CRA/FL Wiz file.

Before you can add data into an existing file, you must first import a new file. When you bring in this file you will need to create ‘place holders’, or empty fields that will accept the information that needs to be added to your extract. To import a file, follow these steps:

1. Select the Main tab and click the Import Wizard button.

9

Fair Lending Wiz Training Guide

2. Select New Format. Hit the Next button found at the bottom of the screen.

3. Select Text as the Source Data Type.

4. To locate the file to import, click the ellipsis button to navigate to the folder and then the source file (FL Mortgage File.csv). Click Next.

5. The Source File Format Selection screen allows you to set how your file is struc-tured.

10

Importing

6. Click the Row Delimiter drop-down button and select Carriage Return.

7. Click the Text Qualifier drop-down button. Select None.

8. Check the box next to First Row Has Column Names. By using this feature, the software will automatically match or “map” the fields found in your LOS to the fields found in CRA/FL Wiz. Click Next.

9. The software displays the Text File Column Delim-iter Selection screen when the source file is a delim-ited text file. You use this screen to select the type of delimiter used to separate fields in the source file. Select Comma. Click Next.

11

Fair Lending Wiz Training Guide

10. The Target File Selection screen provides you with the different file types, along with the ability to name your file. From the drop-down box, select Mortgage 2004.

Note: Use Mortgage 2004 for files created in 2004 and beyond. This file type incorporates changes made to the Regulations starting with 2004 submission files.

11. Under the New File option, type Mortgage YTD. Click Next.

Note:Which of these 3 options to use depends on your source file. “New file” would be used for the first month, or quarter, or an entire year. “Update” would be used to update an existing file. “Append” would be used to ADD a new quarter onto the pre-vious quarter’s data. KNOW your file’s contents.

12. You use the Census Year Selection screen to indi-cate whether you want to import a file with 1990 or 2000 census boundaries. Import a loan file using 2000 census tract bound-aries for action dates >=2003. Click Next.

12

Importing

13. Select the File Will be Geocoded in Wiz Sys-tem check box if you want to geocode the file in CRA/FL Wiz. Click Next.

Note: File must contain values in the files MSA, State, County, and Censustrac if you are NOT using the Wiz geocoder.

To be geocoded within the Wiz, the file must contain Address, City, State_abrv, and Zip.

14. Click the Auto-Map Remaining Source Columns link. This link automatically maps the fields in your Source col-umn and lists the fields in the Target column only if the source field matches the CRA/FL Wiz field name. If the software could not match a field, the corresponding source field displays <none>. You would then have to manually map the source field.

Look at the Data Preview for the Loan Amount field. The Loan Amount is displayed in whole dollars. However, the format for submission (and the software) requires the loan amount to be displayed in thousands.

You can add a replace command -- a command that will change the value in a specific field in the source file -- while you are importing records into CRA/FL Wiz. This is helpful to manip-

13

Fair Lending Wiz Training Guide

ulate data into a format required for submission and analysis purposes.

Example:

You will add a replace command to the import format so Loan Amount will be automatically divided by 1,000 while the records are being imported.

To add a replace command to divide the values in the Loan Amount field by 1,000, follow these steps:15. Under Source, click the

LoanAmount cell. Then click the ellipsis button.

16. From the Functions win-dow double-click Numeric and double-click the RoundTo1000( ) expression.

Source File (Source ÷ 1000)

Loan Amount 130000 130

14

Importing

17. Single click INSIDE the parentheses ( ) in the Expression Creating win-dow. In the column win-dow use the scroll bar to locate and double-click on LoanAmount. Click the Validate button.

Note:If the expression does not validate, make sure the field name was placed inside the parentheses correctly.

18. Click OK, then Apply.

15

Fair Lending Wiz Training Guide

19. Verify that Loan Amount is now displayed in thou-sands.

Now that you have rounded the loan amount to the nearest thousand during the import process, you also want to set placeholders (empty fields) to accept fair lending values when you import another file using update into the file just imported.

To set empty fields in your import format, follow these steps:

20. You want to make use of fields that are included in CRA/FL Wiz whenever possible. For example to include the Beacon Score, select the cell under the Source column called Bea-con. Click under the Source column to activate the drop-down menu. Select <Empty>.

16

Importing

21. A valid Beacon Score should always come in as a 3-character number. Therefore, there is no need to accept the default values of Numeric, with 9 positions to the left of the decimal, and 3 posi-tions to the right. Open the drop-down list under data type, and select INTEGER.

22. Follow the same process as above making LTV and BERatio active. Set both fields to be Numeric 9,15,2.

By performing this task during the import process, your file will be ready to accept these fields when you combine, or Update, another file with additional data. Once this step is completed, you will not have to per-form this step during another import as long as you continue to use this format. Hit Next.

There is one more thing that must be done to this file prior to perform-ing the actual import. There was one field (BRANCH_ID) where the field name provided in the .CSV (comma separated value) file did not match the FL Wiz field name (BRANCHNUMB).

17

Fair Lending Wiz Training Guide

23. Scroll up slightly (about mid-way between Beacon and Zip) until you find Branchnumb, which is cur-rently grayed out. In the source column for Branch-numb, click on <None>. Open the drop-down list, and click on Branch_ID as the field you wish to “map” to.

24. The Branchnumb field is only a single digit indica-tor. Set the Data type to CHAR, and the Size to 1.

25. Because you will be importing all records in the source file, you do not need to create a filter. Move to the next screen by clicking the Next but-ton.

18

Importing

26. You are now brought to the Thank You screen. To save the import format, check the box next to Save the Defined Import Format and name your format in the open box. Call your for-mat Mortgage with FL Fields.

27. Select Import Now. You also want to make sure you have the appropriate year selected. The year should represent the Action Year of your file (in this case - 2006). If it is not correct, select the drop-down menu and choose the correct year. Click Finish.

28. The software will now import the records from the source file into the tar-get file you have created.

19

Fair Lending Wiz Training Guide

29. Select Yes to view the summary. Print a copy of the summary to have as documentation of the pro-cess. Once you have printed the summary, select File>Exit.

20

Importing

Exercise 2: Updating an Existing File

Now that you have imported the file, you can add fair lending data from an additional file. This file must contain some type of unique identifier so the fields can be associated with the appropriate record. Application Number, or Applnumb, is a good field to use because it is a unique field, meaning each record should have a distinct application number.

Your system might not use the Application Number, however. Use what-ever field, or combination of fields, that will provide the ability to “match up” records between two files received from different systems.

To import a file using the Update feature, follow these steps:

1. Select Import Wizard.

2. Leave the default, New For-mat, selected. Hit Next.

21

Fair Lending Wiz Training Guide

3. On the Source File Selection screen, click the Source Data Type drop-down menu. Select Text.

4. Navigate outside of CRA/FL Wiz to select your source file. Click the Source Access File ellipsis button.

5. Select the file to be imported (Additional Fair Lending Fields.csv). Click Next.

6. In the File Format Selection screen, leave Delimited selected.

22

Importing

7. You need to set the Row Delimiter. Click the drop-down menu and select Car-riage Return.

8. Leave Text Qualifier set as None.

9. Click the box next to First Row Has Column Names. Click Next.

10. The Text File Column Delimiter Selection screen provides various types of delimiters. Leave the default, Comma, selected. Click Next.

23

Fair Lending Wiz Training Guide

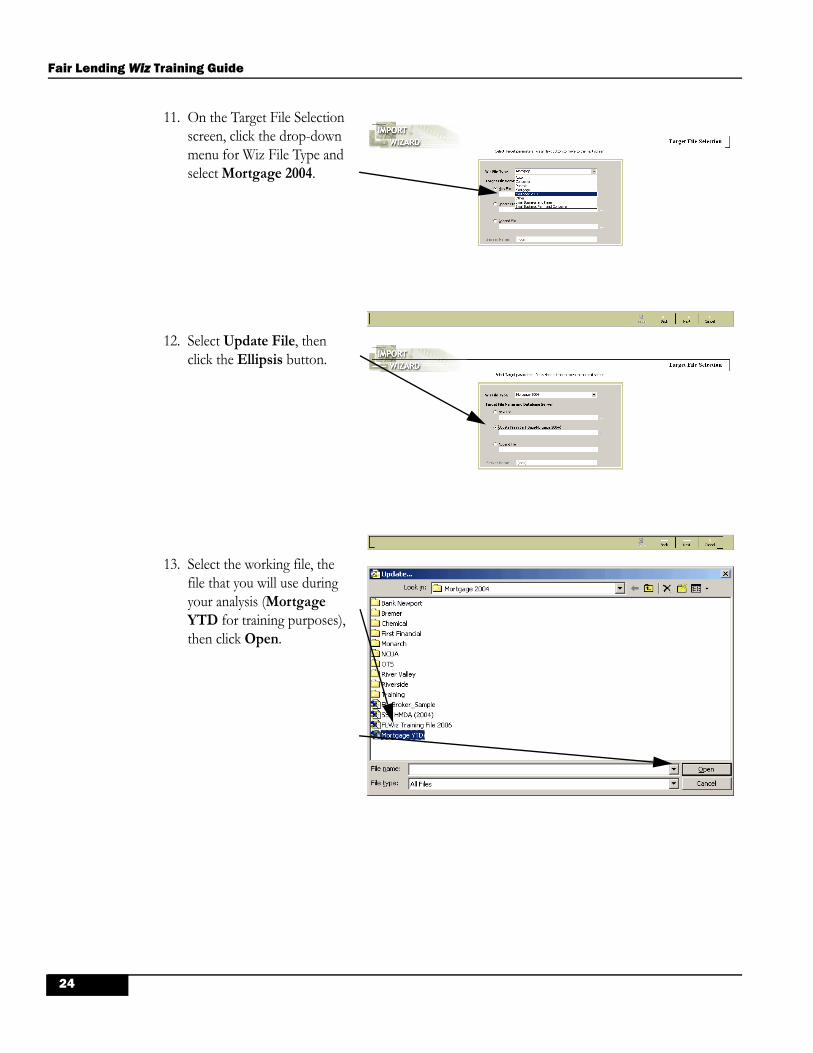

11. On the Target File Selection screen, click the drop-down menu for Wiz File Type and select Mortgage 2004.

12. Select Update File, then click the Ellipsis button.

13. Select the working file, the file that you will use during your analysis (Mortgage YTD for training purposes), then click Open.

24

Importing

14. Your file should be listed under Update File in Bank Data. Click Next.

15. Click Auto-Map Remain-ing Source Columns. This function will match, or “map”, columns found in your source file to your target file, IF they matched the FL Wiz field name. Scroll down, and you will see only Applnumb, Beacon, and LTV. What happened to the BERatio field?

16. Locate the “grayed out” field called BERatio. In that row, click on the word <None> under Source. Open the drop-down list, and select BER. Set the Scale to 2, then click the Next button.

25

Fair Lending Wiz Training Guide

17. The Matching Column Selec-tion screen allows you to select the field to base the matches on. Application Number, or Applnumb, makes the most sense to use because it is unique. Click Next.

18. On the Update Options screen, deselect all options. You do not want the system to Append Unmatched Records to the Updated File, because each “Unmatched Record” would only have 4 fields (applnumb, beacon, beratio, and LTV). Quality errors COULD be checked, but you are not replacing any values that would affect quality edits, so it best not to. Click Next.

19. Because you are importing all records, you do not need to create a filter. Click Next.

26

Importing

20. The system has now brought you to the Thank You screen. Save the import format as Fair Lending Fields. Click the Import Now box, mak-ing sure the Select Action Year is set to 2006. Click Fin-ish. The software processes the file through the import function and provides you with a summary screen. Click No when asked to view the summary.

27

Fair Lending Wiz Training Guide

28

Editing Data for Fair Lending

Chapter 2

Editing Data for Fair Lending

Upon completion of this lesson you will be able to:

Edit data for Fair Lending Analysis purposes

Use Replace commands to correct erroneous information in the Fair Lending Data

Use Modify Codes to make user-defined fields available in the Fair Lending models

29

Fair Lending Wiz Training Guide

Overview

A Fair Lending Analysis is no better than the data that you have available in your electronic file. For example, an excessively high (incorrect) value in the LTV field for an originated loan could very well set the threshold for acceptable values. For example, assume that you have an originated loan for a 49-year old male, white non-Hispanic borrower showing a loan-to-value ratio of 192%. Assume fur-ther that this is a middle-income individual who lives in a non-minority tract (< 10% minorities), and the tract is also a middle-income tract. The value of 192% becomes the threshold for acceptance for every fair lending comparison that can be done!

Before you start any kind of fair lending analysis, you must review the data at your disposal, and determine if there are individual or systemic problems that could interfere with the analysis. Keep notes as you do these reviews, as you will use the data for two purposes:

To know what filters need to be applied before some fair lending analyses are run

To help your institution determine where the errors are coming from, and whether they are part of a larger issue that needs to be corrected

30

Editing Data for Fair Lending

Exercise 1: Reviewing Data

From this point on, you will be using a file called FL Wiz Training File 2006 Revised. It contains over 19,000 records, and has fields in it for the applicants’ credit scores, back-end ratios (total debt-to-income ratios), LTVs, CLTVs, Length of Employment, and Length of Residence. The file also contains a field called “Loanprog”, which is a 10-character description of the specific loan program that the applicant was applying for.

To review the Fair Lending fields, follow these steps:

1. Click on the Main button in the View Bar, then click on File Management.

2. Click on the Mortgage 2004 folder. Right-click in the white area to the right of the file list in the right panel, then select Install/Restore from the contextual menu.

31

Fair Lending Wiz Training Guide

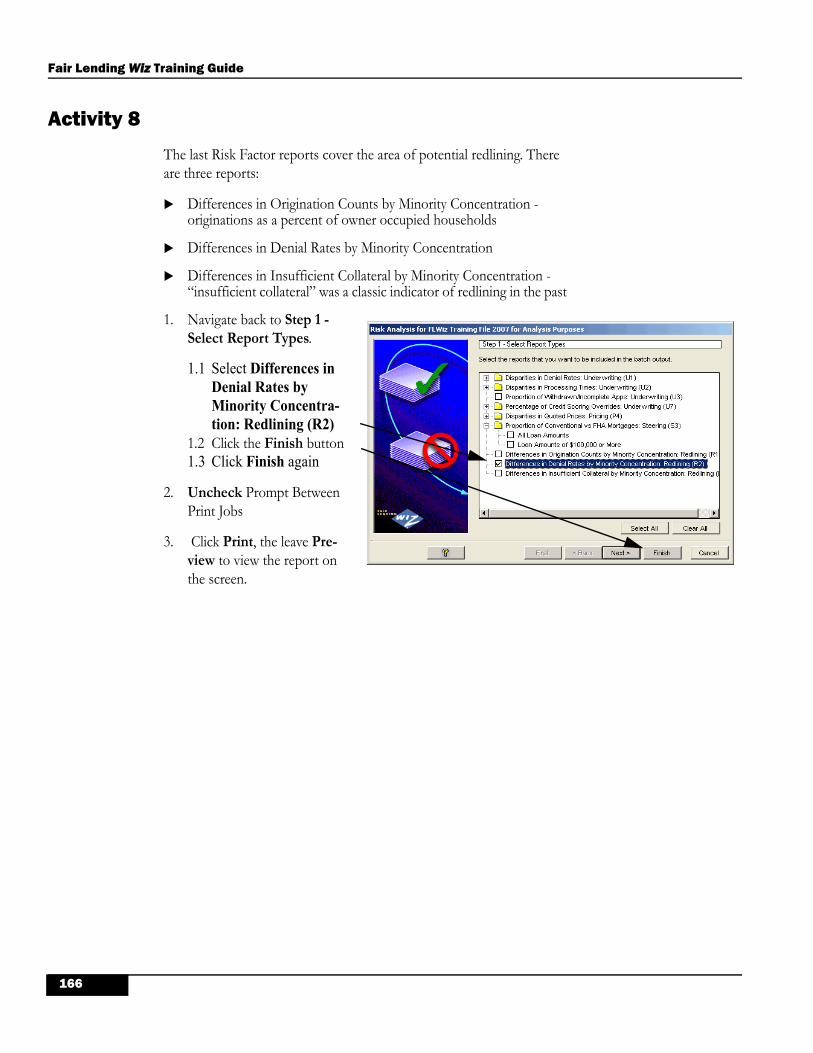

3. Navigate to the location of the FLW Files, then double-click on FLW Training File 2007.dat.

4. The software will Install the file, adding it to the list of Mortgage 2004 files, and pro-vide a message explaining that you should “Run Update Calculated Fields”. Click OK.

5. Right-click on the newly-installed file, and select Update Calculated Fields from the contextual menu. Click Yes when the mes-sage regarding Locked Records appears, and OK when the completion message appears.

32

Editing Data for Fair Lending

6. Right-click on the file again, and select Edit from the contextual menu.

7. When the file opens, it will most likely open to the Cur-rent Record screen. Click on the Browse tab.

8. It is always a good idea to check the overall quality of the file before starting your analysis. Click on the word EDIT in the menu, then select Govt Exception Summary Report (All).

9. The exception report shows all errors - Validity, Syntacti-cal, and Quality. This report shows ONLY Quality errors. This means that the file is properly geocoded, and that all required fields are filled in properly. Close the report when finished reviewing it.

33

Fair Lending Wiz Training Guide

10. .Right-click anywhere in the data, and click on Select Columns to View from the contextual menu.

11. Click on the blue link at the top that says Unselect All.

34

Editing Data for Fair Lending

12. Starting at the top of the window, select the following fields (use the scroll bar as neces-sary):

12.1 Action 12.2 Lien Status12.3 Loan Term12.4 Rate_Lock_Date12.5 APR12.6 Age12.7 Cust_Credt12.8 LTV12.9 BERatio12.10 Noterate12.11 LenEmploy12.12 LenResid12.13 LoanProg12.14 CLTV12.15 Raw_Rate_Spread12.16 Click the X to close the Manage Columns to

Browse dialog.

TipIf after clicking “Unselect All” you either click outside the dialog box, or close it with the “X”, click the Options dropdown menu, and select “Select Columns to View” to restore the window.

13. Since the APR is the first major field, start the analy-sis by reviewing the values contained within that field. How many are missing? How many zeroes are included for originated loans? What is the highest value for an originated loan? Click the Sort button to get started.

35

Fair Lending Wiz Training Guide

14. Double-click on the Other Information folder (or click on the + sign) to open the folder.

15. Double-click on APR, moving it to the right-hand side of the Sort Col-umns dialog screen, then click Apply.

16. How many zeroes are contained in the APR field? Scroll down until the see the last “0”, and click in that row. To see how many there are, look at the bottom left of the screen.

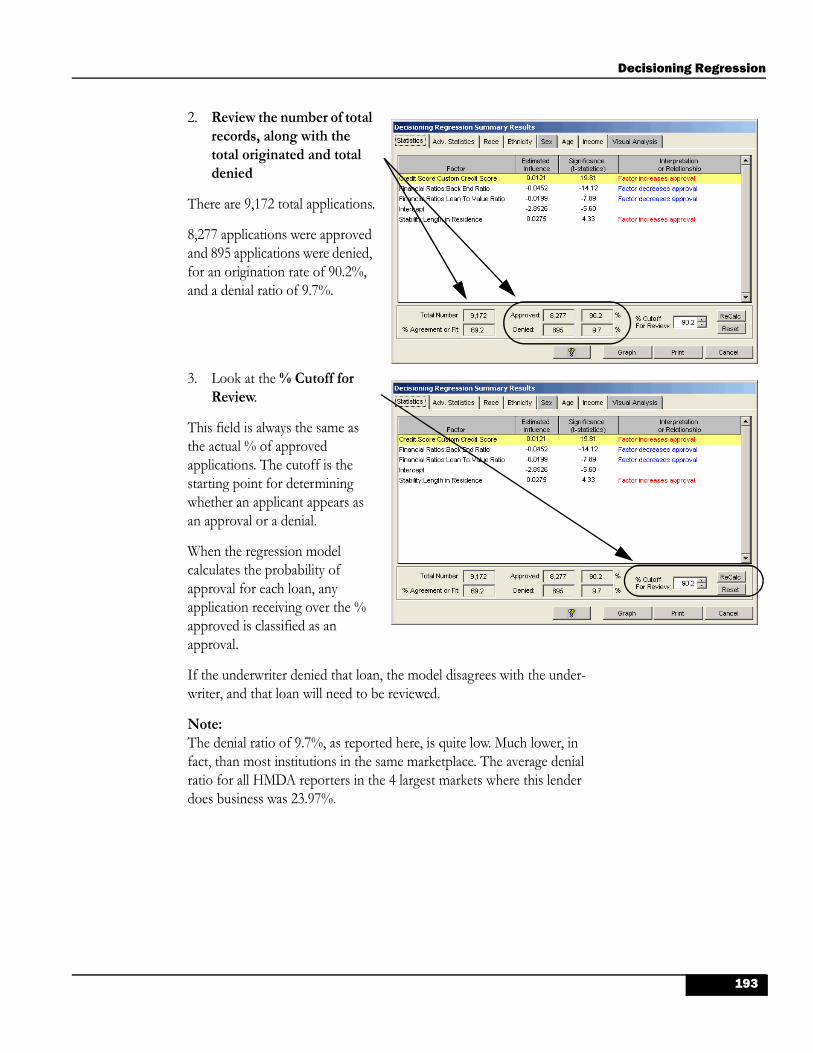

Note: Zeroes should not be included in any of the fair lending fields. A “0” is a real value, and will affect averages and other calculations. In these fields, it is best to change any zero to a “null” value, which will automatically be “thrown out” by the program.

36

Editing Data for Fair Lending

17. You should also take note of the fact that there are other “suspicious” values in the APR field. Is there a chance that an originated loan (see Action = “1”) had an APR of .25? Or 1.86%? This would be an issue that you would want to check on if this was your institution’s data.

18. To sort the APR in descending order, click on the Sort button in the Tool Bar again, and dou-ble-click on APR (or you can right-click on the APR, and select Descending from the contextual menu). Click Apply.

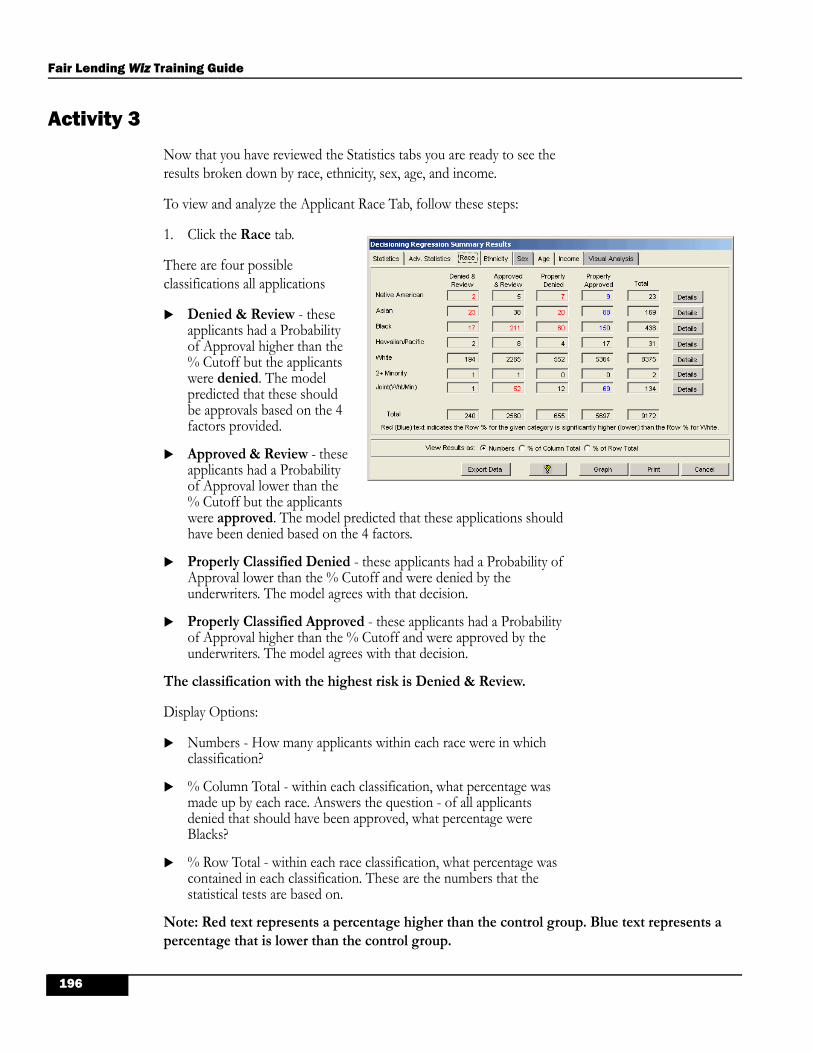

19. You will often see this message (...Would you like to save changes?). The answer depends upon what you have done. So far, no changes have been made in this file, so click on No.

20. The top of the list shows that the maximum APR was 16%. Was it an originated loan? The action code was “3”, so it was denied. The highest APR for an originated loan was 14.5%. Note that the lien status was a “3”. To find out what that means, click on the 3, and use the drop down list to review the codes.

37

Fair Lending Wiz Training Guide

21. Click on the Sort button. Right-click on APR, and select Remove from the contextual menu.

22. Double-click on the User Defined Variables folder.

23. Whenever you want to search an open list of variables, start typing the name you are looking for. In this case, you want to search the list of User Defined Variables for Noterate. Start typing Noterate until it is found.

38

Editing Data for Fair Lending

24. Double-click on Noter-ate, placing it on the right side as an ascending sort. Click Apply. Click No on the message “Would you like to save changes...”.

25. How many records have missing Entries? How many are zeroes? Any other “suspicious” val-ues at the low end of the scale?

26. Click on the Sort button again. Right-click on Noterate, and select Descending order. Click Apply.

39

Fair Lending Wiz Training Guide

27. What is your maximum value? Does it appear rea-sonable? Was it for an originated loan?

Test Your Knowledge

The primary variables that you will be using in the Fair Lending analysis are Cust_Credt (credit score), BERatio (back-end ratio, or total debt ratio), LTV (loan-to-value), and possibly CLTV (combined LTV with first and second liens).

Take each of these variables individually, and sort them in both ascend-ing and descending orders. Look for values that are outside the “normal” range. Be sure to check to see if the “erroneous” values are for origi-nated loans.

Notes on data quality:

Extra Credit:

How many originated loans were there with a Back-End Ratio greater than 100? ______________

How many originated loans were there with a loan-to-value greater than 100? __________________

Missing (Null) Zeroes? Lowest Value Highest Value?

Was the high-est for an originated loan? If not, what was the highest value for an origi-nated loan?

For BE Ratio and LTV, how many were over 100?

For BE Ratio, how many over 200?

Cust_CredtBE RatioLTVCLTV

40

Editing Data for Fair Lending

Exercise 2: Replacing Zeroes with “Nulls”

The presence of zeroes in your fair lending data fields can cause prob-lems. There are certain reports that calculate averages, and zero values bring down those averages. In addition, there are several places where the program will ignore records with “null” values in certain fields, but zeroes are allowed in.

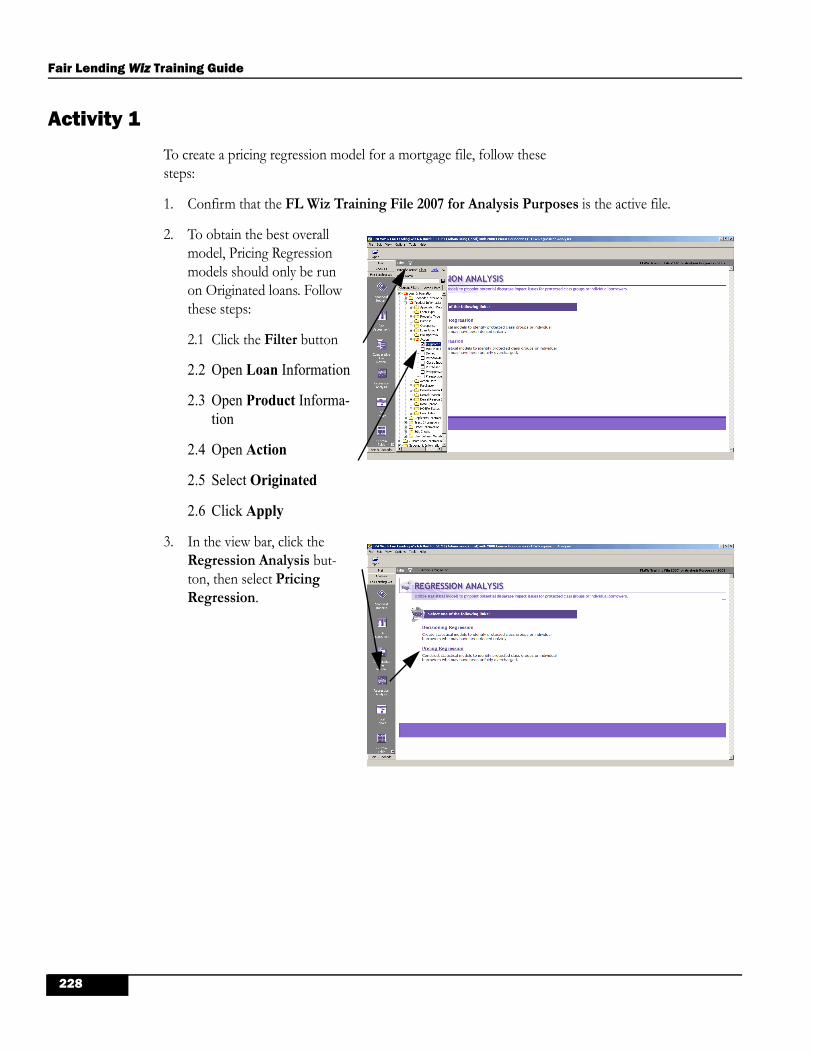

Bottom line? You should always replace the zeroes with “null” values in your non-HMDA (or non-required) fair lending fields.

Note: You can also replace zeroes with NULL values during the import process. To do this, you would click the ellipsis for the source field you wanted to modify. For example, if the APR had zeroes, you would click the ellipsis for the APR source field, and in the expression window, enter ‘ IIF(APR=0,””,APR) ‘. Call Technical Support for assistance setting this up the first time.

Based on what you have found in this file, you know there are zero val-ues in the APR and NoteRate fields. To correct these, follow these steps:

1. In the Tool Bar, click the Replace button. If asked to Save Changes, click No.

41

Fair Lending Wiz Training Guide

2. Step 1: For the Scope, click on All Records. Step 2: Click in the checkbox on the left side of the first column.

3. Step 3: Click on the drop-down list button, and select APR from the list.

4. Step 4: Under the Replace With column, click on <None>, then click the Ellipsis button.

42

Editing Data for Fair Lending

5. Step 5: IMPORTANT! For the NULL replacement to work, you MUST click on T-Sql on the top of the screen.

Note:The NULL statement does not work in VBScript. If you forget to choose TSql, you will receive an error message.

6. In the Expression Creating Window (the lower part), type the word “NULL”. No quotes are necessary, and caps are optional as well. Click Apply when done.

43

Fair Lending Wiz Training Guide

7. Click the word <None> under the Replace For col-umn, then click the Ellipsis. In the Expression Window, type “APR=0”. Again, no quotes are necessary. Click Apply. THIS STEP IS NEC-ESSARY, OR YOU WOULD REPLACE ALL APR VALUES WITH NULLS!

8. Following the same steps as above, do the same thing for Noterate. The finished expression should look like this. Click Execute.

Note: If you wanted to save these replace commands for future use, you would have typed in a name into the Replace Command text box, and clicked on the diskette.

9. Verify the message showing how many replaces were done.

44

Editing Data for Fair Lending

Exercise 3: Using Modify Codes to Allow User-Defined Fields to be Used

Both CRA Wiz and Fair Lending Wiz depend on “codes” to simplify the process. For example, the field called “Action” is coded with a “1” for Originated, a “2” for Approved Not Accepted”, “3” for Denied, etc.

User-Defined Fields (UDFs) do not automatically have codes defined for them. Without codes, the program does not know that a particular field exists, or how you want to use it in your fair lending analysis. Therefore, any field that is truly “user-defined”, and that you want to use in any of the regression or comparative models, must have codes defined.

For this file, there are three fields that are UDFs that you might want to use in the Fair Lending Models: (1) CLTV, (2) Fix_ARM (F=Fixed Rate, A=ARM), and (3) AU (for Automated Underwriting System; DO=Desk-top Originator, DU=Desktop Underwriter, LP = Loan Prospector, etc.)

To perform the Modify Codes procedure, follow these steps:

1. First, you need to be able to see these UDF fields in your “view”. Right-click any-where in the data, and click on Select Columns to View from the menu.

45

Fair Lending Wiz Training Guide

2. Scroll down about 80% of the way down the list (you should see a majority of the fields that you already have selected). Search for Fix_Arm, and AU, then click their respective checkboxes. Since CLTV is already selected, click on the “X” in the upper-right corner to close the dialog box.

3. Right-click in the data, and click on Locate Field.

4. Open the drop-down list, and start typing the field name “Fix-Arm”. In this case, just the “F” is sufficient to find the field you want. Click on Fix_Arm. When finished, close the Find Field dialog box by clicking on the “X” in the upper right corner.

46

Editing Data for Fair Lending

5. Right-click in the Fix_Arm field, and select Modify Codes from the menu.

6. You are now in the Modify Codes dialog box. This field contains two values -(1) F, and (2) A. In a text field, the easiest way to obtain these values is to click on the Retrieve Unique Values button.

7. For text fields, the Modify Codes Table only has two columns. The first is the description (used in Custom Tables), and the second is the code associated with that description. This step essentially told the software that a user-defined field called Fix_Arm exists, and that is has two pri-mary values - F, and A. Click Apply, and then click OK to the message telling you the code was modi-fied successfully.

47

Fair Lending Wiz Training Guide

8. Right-click in the AU field, and select Modify Codes from the menu. Because this is another text field, click on Retrieve Unique Values. Review the codes, then click Apply.

The final field is CLTV, and it is not a text field, but holds numeric val-ues instead. You have to decide ahead of time what distribution you want. In other words, if you wanted to calculate the average APR based on differing values of CLTV, what would you like to see? Typically, for pricing and for decisioning, it doesn’t make any difference when the CLTV is 80% or below. There MIGHT be a price increase at 85%, and another at 90%, 95%, and again at 97%.

9. Right-click in the CLTV field, and select Modify Codes. Click on Add New Code.

10. When New Code 1 is blue, type in “Missing or 0”, and press the Tab key. In the From column, type 0, <Tab>, To 0. <Tab>, Description = “1 to 80.00”, <Tab>, From 1, <Tab> To 80.00, <Tab>, Description = “80.01 to 85.00”, <Tab> From 80.01, <Tab> To 85.00, <Tab> Description = “85.01 to 90.00”, <Tab> From 85.01, <Tab> To 90.00. Continue until all rows as shown are completed, then Apply.

Warning: Once you have completed these lines, DO NOT tab again (leaving a blank line with no values in the “From” and “To” columns. If you acciden-tally do this, click the DELETE button, then APPLY.

48

Editing Data for Fair Lending

Review:

Data Quality:

Each field that you will use for Fair Lending analysis should contain val-ues that are valid. Zeroes can interfere with some of the calculations, and should be replaced with “null” values.

From the review, you know that this institution had some “bad” values in the fields you will need to use in the Fair Lending Analysis.

The back-end ratio had a high value for an originated loan of 50,060.

There were 213 records where the back-end ratio was over 100, with 69 of those originated.

The LTV had a high value for an originated loan of 188.

There were 79 records with an LTV over 100, and 4 of those were originated.

Leaving these erroneous values in some of the analysis models would impact your analysis in a negative manner. Therefore, you will see this fil-ter being placed in some of the models:

BERatio <= 100 and LTV <= 100

In addition, if this was your institution, you would want to find out how and why these values are getting into the database, and what could be done to remove them in the future.

Null Values:

You replaced the zeroes contained in the APR and Noterate fields with “null” values, which do not affect averages.

Modify Codes:

You performed the step called “Modify Codes” for three fields - CLTV, Fix_Arm, and AU.

49

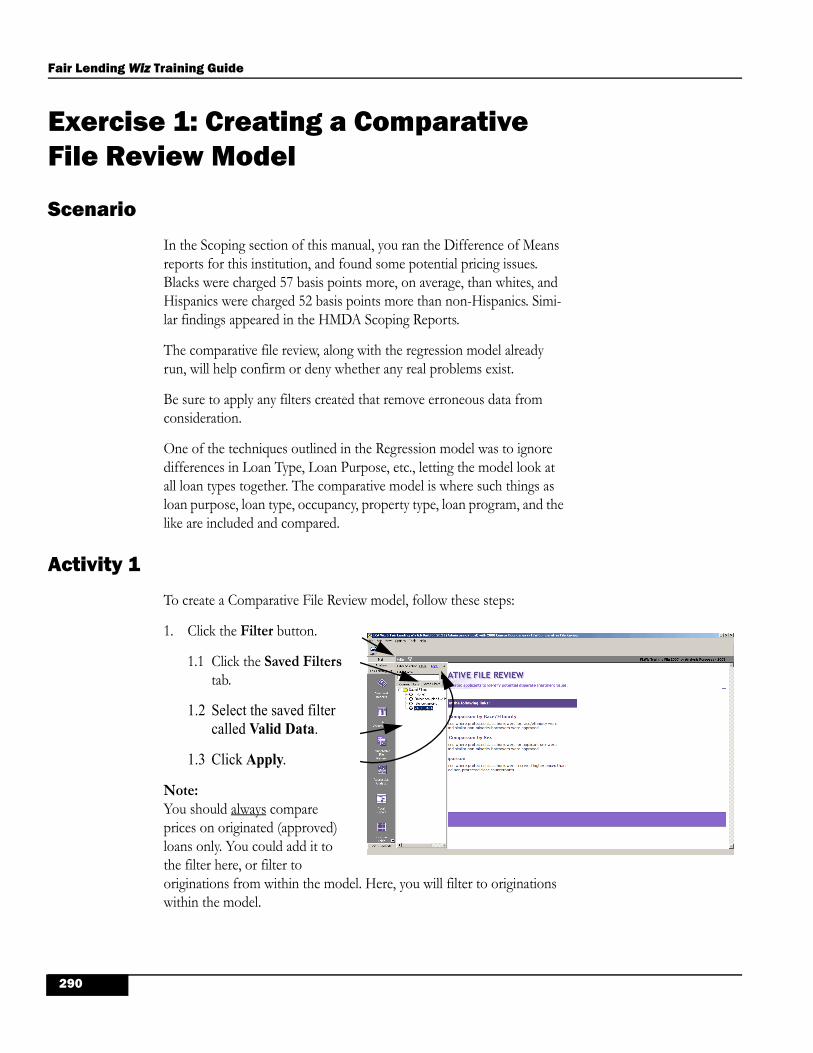

Fair Lending Wiz Training Guide

50

Custom Tables

Chapter 3

Custom Tables

Upon completion of this lesson you will be able to:

Create Custom Tables Using User-Defined Fields

Use Excel Pivot Tables to further Manipulate and Understand Data

Use a Custom Table to Calculate Average APRs by Race and Product

Create a Save Custom Table for Later Use

51

Fair Lending Wiz Training Guide

Overview

Fair Lending Wiz provides you with numerous standard reports. However, there will be times when you will want to analyze data contained within User Defined Fields, or to provide Management with a report that is not otherwise available within the Wiz.

Custom Tables can be used to produce a printed report, or an Excel Spreadsheet, that will allow you to manipulate and understand your data in ways you can’t even begin to imagine.

This chapter will take you through three examples of custom tables.

52

Custom Tables

Exercise 1: Obtaining a Distribution by Loan Product

Management has asked you for a detailed report showing the volume, and actions taken, for every mortgage loan product offered by your insti-tution.

To create this table in Excel, follow these steps:

1. From this point forward, you will be using the file called FL Wiz Training 2007 for Analysis Pur-poses

2. Click on the Main button in the View Bar, then click on File Management.

3. Click on the Mortgage 2004 folder. Right-click in the white area to the right of the file list in the right panel, then select Install/Restore from the contextual menu.

53

Fair Lending Wiz Training Guide

4. Navigate to the location of the FLW Files, then double-click on FLW Training File 2007 for Analysis Purposes.dat.

5. The software will Install the file, adding it to the list of Mortgage 2004 files, and pro-vide a message explaining that you should “Run Update Calculated Fields”. Click OK.

6. Right-click on the newly-installed file, and select Update Calculated Fields from the contextual menu. Click Yes when the mes-sage regarding Locked Records appears, and OK when the completion message appears.

54

Custom Tables

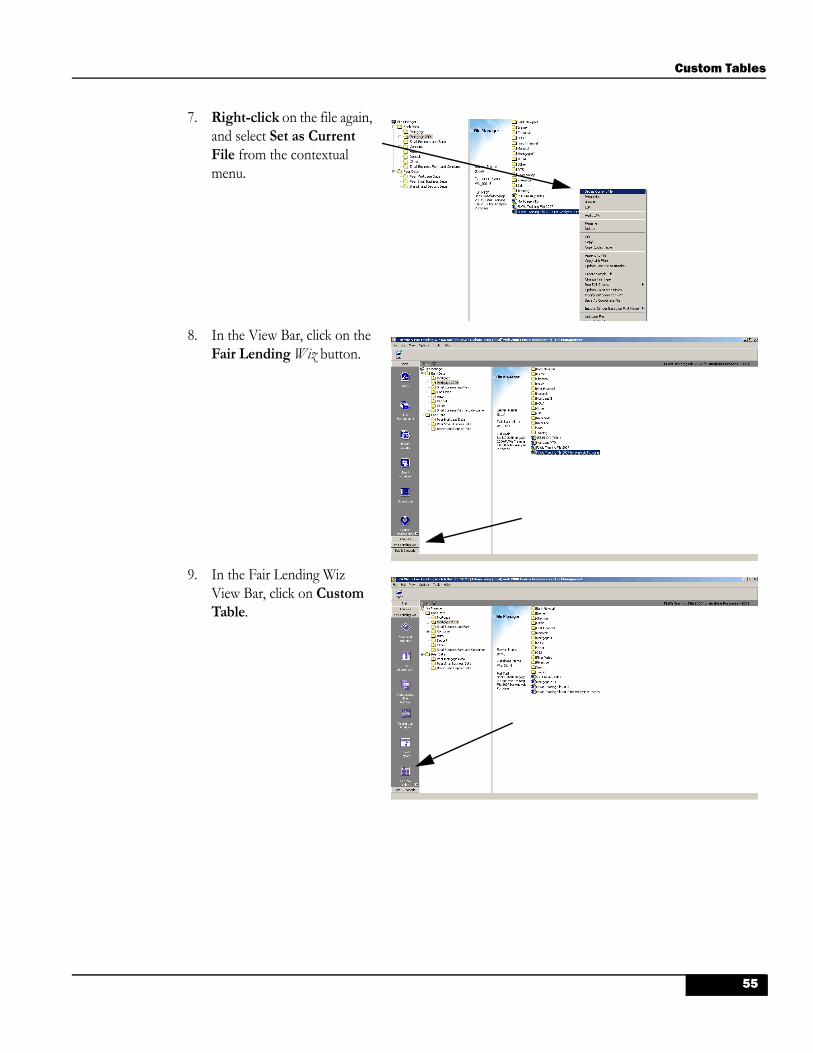

7. Right-click on the file again, and select Set as Current File from the contextual menu.

8. In the View Bar, click on the Fair Lending Wiz button.

9. In the Fair Lending Wiz View Bar, click on Custom Table.

55

Fair Lending Wiz Training Guide

10. For Custom Tables, the field folders are on the right. For this table, you are going to make the Column based on Action, and the Row based on the User Defined Field called Loanprog. Double-click on the Product Infor-mation folder.

11. .Right-click on Action, and select Send to Column.

12. Double-click on the User Defined folder, then right-click on Loanprog, and select Send to Row.

56

Custom Tables

13. You want to know the per-centage of each product by Action taken, so you need to add the % of Row Total cal-culation. Click on the Dis-play Subtotals checkbox, open the drop-down list, and select %Row Total.

14. In the Tool Bar, click on To Excel.

15. When Excel opens, you are in a Pivot Table. The Pivot Table field list needs to be closed, and Excel maximized to fill the whole screen. Click on the X to close the dialog box, and click on the Maxi-mize button to open the table in the full window.

57

Fair Lending Wiz Training Guide

16. To make the table easier to analyze, click on the Select All button, then select Format > Column > Autofit Selection.

17. Look through the data, looking at the number of originated, denied, and the the totals. You now want to sort the table in descending order by total applications received, but the percentages will inter-fere with that action. Right-click in the data, and select Pivot Table Wizard from the contextual menu.

18. There are two things to watch for here: (1) be sure the top bar shows “Step 3 of 3”. If not, click Cancel and right-click INSIDE the data. (2) The checkbox for Existing Spreadsheet should be checked. Click on the Layout button.

58

Custom Tables

19. In order to remove the percentages from the table, click on %Row of Count, and drag it off to the right. Click OK when done.

20. Click Finish to complete the action. Re-close the Pivot table field list.

21. To sort this table in descending order by product, click into the first cell in the Grand Total column (Cell I8). Click on the menu Data > Sort > Descending.

59

Fair Lending Wiz Training Guide

22. Regression analysis is discussed at length in an upcoming chapter. For now, you need to know that a regression model needs at least 250 records to be successful. For an Approval/Denial model, that would mean 250 Originated and Denied mixed. For a pricing model, that would mean 250 Originated. You can see that only a few prod-ucts meet that criteria.

23. Close and don’t save the spreadsheet (at your institution, you would most probably save your work).

24. Upon returning to your Cus-tom Table, double-click on the Custom Table name. Name the table Loanprog by Action, and click the Save button (the diskette).

60

Custom Tables

Exercise 2: Calculating the Average APR by Loan Product

When performing a Fair Lending Analysis, it is necessary to know where your risks are. For example, if there is an indication of pricing issues, what products are your highest priced products? What products produce the largest differences between white applicants and minority applicants? These questions can be answered by creating another Custom Table.

1. Right-click on Action (in the column heading), and select Delete from the con-textual menu.

2. Double-click to open the Applicants Informa-tion folder. Right-click on Race1, and select Send to Column.

61

Fair Lending Wiz Training Guide

3. Double-click on Race1 (in the column heading), and uncheck Not Pro-vided and Not Applica-ble. Click Apply.

4. Click to open the Select Data Content drop-down list, and select APR.

5. Uncheck the Display Subtotals checkbox.

62

Custom Tables

6. Under Select Data Con-tent, uncheck Sum, and check Count, Average, and Greatest Value. In the Tool Bar, click on the To Excel button.

7. When the table opens in Excel, close the Pivot Table field list, and Maximize Excel.

8. The “Custom Report 1” spreadsheet becomes your “Master” table, which can be renamed as such if desired. You will copy this table before you start massaging your data, creating formulas, etc.

9. Right-click on the Work-sheet called Custom Report 1, and select Move or Copy from the contextual menu.

10. In the Move or Copy dialog box, click on Sheet1, then click on Create a Copy, then click OK.

63

Fair Lending Wiz Training Guide

11. Right-click in the data, and select PivotTable Wizard.

11.1 In the Pivot Table Wizard dialog, click on Layout.

12. Drag Count off to the right.

12.1,Drag Max of Apr off to the right.

12.2 Click OK.

12.3 Click Finish.

13. Close the Pivot Table Field List dialog box again, then click into Cell D8.

64

Custom Tables

14. Click on the menu item Data, and select Sort. Change the Sort By ($D$8) to Descending, then click OK.

15. Your table now shows all products applied for by Blacks/African Americans, in descending order by the highest average APR for those applicants. This table is useful, but is not the end of the analy-sis by any means. Were Blacks and Whites charged the same average APR on these products? To calculate the DIFFERENCE between the minority and the control group (white), you would need to enter a formula. This can be done within a Pivot Table, but it is more dif-ficult. Follow the next steps to create a column showing the differ-ence between the two groups.

16. Press CTRL-A, then CTRL-A to select ALL of the table, then CTRL-C to Copy the table (you should see “Marching Ants” around the data).

65

Fair Lending Wiz Training Guide

17. Click on Edit, then Paste Special.

17.1 Select Values from the Paste Special dialog box, then click OK.

17.2 Press the Esc(ape) key to remove the “march-ing ants”.

18. In Cell H7, type “Differ-ence”

18.1 In Cell H8, type “=IF(F8>0,D8-F8,0)” (this formula calculates the difference IF there is an average for the White).

18.2 Copy this formula down to cover all Blacks by moving the cursor to the lower right corner of Cell H8 (the cursor should turn to a + sign), and dragging it down through Cell H66

19. Your table now shows the difference between the aver-age APR for blacks versus whites. To finish this task, you will use an Auto-Filter to sort the table.

66

Custom Tables

20. Place your cursor in Cell H7.Click on the menu item called Data.

20.1 Select Filter

20.2 Select Autofilter

21. Open the Autofilter drop-down list, and scroll up until you see Sort Descending, then select that option.

22. Here is your table, sorted in descending order by the products with the largest dif-ference between blacks and whites.

23. Close the Excel spreadsheet. Save it if you wish.

23.1 Save the Custom Table in the Wiz as “Distribution by Prod-uct and Race - Avg APR”.

Note: Ideally, you would have multiple worksheets, one for American Indian (sorted in descending order by product average), one for the difference between American Indians and Whites, two similar worksheets for Asians, two for Blacks, and two for Native Hawaiians.

67

Fair Lending Wiz Training Guide

Test Your Knowledge

Create a Custom Table that calculates the Average Note Rate for each Loan Product by Ethnicity (or Sex). Be sure to de-select Not Provided and Not Applicable from the column in the custom table.

Once you have the Master Table (Custom Report 1), create three copies:

Copy 1 - take out all but the average Note Rate

Copy 2 - sort by descending Note Rate for Hispanic applicants

Copy 3 - create and sort by descending Difference between Hispanics and non-Hispanics.

IF TIME PERMITS - Experiment! Add Application Number as a Row under Loanprog. Try different options.

Remember, you are limited to the number of Rows and Columns that Excel can hold (65,536 Rows by 256 Columns).

Review:

You created, and saved, two custom tables. The first table provided a list of the Loan Products by Action taken. You sorted the table in descend-ing order by product volume.

The second table replaced Action with Race1, and produced a Custom Report1 containing the Count, Average APR, and Maximum APR. You then copied the Worksheet and removed Count and Maximum APR. You sorted the table in descending order by average APR for Blacks, then calculated the difference between blacks and whites.

68

File Management

Chapter 4

File Management

Upon completion of this lesson, you will obtain the skills necessary to:

Copying an Entire File

Copying a File with a Filter Applied

Modifying a File’s Structure

Adding Values to a New Field Using Replace

Add Fields to a Codes Table (Modify Codes)

Transferring/Installing a File

69

Fair Lending Wiz Training Guide

Overview

File Management screen offers numerous options that allow you to work with your files.

Set as Current File - makes this file the one all work will be performed onProperties - Six tabs. Statistics shows how many recordsBrowse - opens table for browsing, but does not allow changesEdit - shortcut method for opening the file in the EditorAudit LAR - call Tech Support for proper use of this toolRename - allows the changing of the database nameDelete - deletes the file. You can not delete the current fileCut - select Cut, then Paste into a different folderCopy - copy entire file. COVERED IN THIS CHAPTER.Copy Codes Table - if your file has User Defined Fields with Codes, you can then paste the codes onto another file (if that file has the same fields)Append to File - appends the selected file onto another fileCopy with Filter - copies the file, but applies a filter in the process. COVERED IN THIS CHAPTER.Update One File to Another - if you have matching records in both files, this option allows you to specify which fields from the current file you want to update in another, existing fileCreate Sample File - specify number of records you wish in a random sample, and the program will create a separate file with that number of recordsChange File Type - call Tech Support for proper use of this toolRun Edit Checks - reruns all government and user-defined edit checksUpdate Calculated Fields - updates fields such as Rate Spread, Raw_Rate_Spread, Income as Percent of MSA Median, etc.Modify Zip Codes for RPO - compares the zip codes in your file against a database supplied by the post office. Removes Zip codes that do not exist for mail delivery purposes. Save as Coordinate File - used with Mapping in CRA-Wiz to map exact locations of your branches, loans, deposits, etc. The file MUST be geocoded in the WizImpute Gender Based on First Name - for Consumer or other files without codes for Sex. If you have FirstName, and CFirstName in your file, copy your original file, add SEX and COASEX, both of Data Type Char 1. After these fields are added, only those records with a code 1 (Male) or code 2 (Female) would be included in your analysisUnlocate File - call Tech Support for proper use of this toolTransfer/Backup - the best way to backup your file. This option will compress your file in .dat format and copy to a location of your choice. Excellent method for sharing files with others.Modify Structure - add or remove non-required fields from your file. COVERED IN THIS CHAPTER.Export File - export fields of your choice in 5 different formats

70

File Management

Exercise 1: Copying a File

In this exercise you will learn how to create a working copy of a file -- a feature that will become very useful as you start to manipulate your data.

1. Click the File Management button located in the main screen.

2. In the File Manager tree view, right-click on FL Wiz Training File 2007.

2.1 Select Copy from the contextual menu

3. Right-click in the “white area” to the right of the file list. From the new contextual menu, select Paste.

71

Fair Lending Wiz Training Guide

4. Your file copy is called by the same name as the original file, with an added (001).

72

File Management

Exercise 2: Copy with Filter

Copy with Filter is an excellent method for “permanently” removing unwanted records, or for making the file smaller for analysis purposes. For example, in an institution with hundreds of thousands of records, the software would perform each analysis much faster if a smaller group of “like” loans was in a copied file.

For this example, you will copy the FL Wiz Training File 2007 and create a file with just Conventional Home Purchase loans contained in it.

1. In the File Management tree view, right-click on FL Wiz Training File 2007.

1.1 Select Copy with Filter from the contextual menu

2. To enter the Target File’s name and path information, click on the Ellipsis (the three dots).

73

Fair Lending Wiz Training Guide

3. In the File Name text area, enter FL Wiz Training 2007 Conv HP Loans. Click Save.

4. Click the Next button to continue.

5. In the Select Columns to be Copied window, click on the blue link at the bottom of the screen that says Auto Map Remaining Columns.

Note: To copy only specific columns, individually select each column by clicking on the word “None” under the source column and select the appropriate field from the drop-down list.

74

File Management

6. When all columns are selected, click on the Next button at the bottom of the screen.

7. In the Filter File to be Cop-ied window.

7.1 Double-click Loan Information folder

7.2 Double-click Product Information folder

8. Double-click the Loan Type folder, and select Conventional.

75

Fair Lending Wiz Training Guide

9. Double-click the Purpose folder, and select Home Purchase.

10. IMPORTANT - Click Apply or the filter will not work. Click the Next button at the bottom of the screen.

11. Check all settings at the fin-ish window, then click on Finish.

76

File Management

12. The software displays a mes-sage telling you that the copy with filter was successful. In this case, the number of records copied was 7,622.

77

Fair Lending Wiz Training Guide

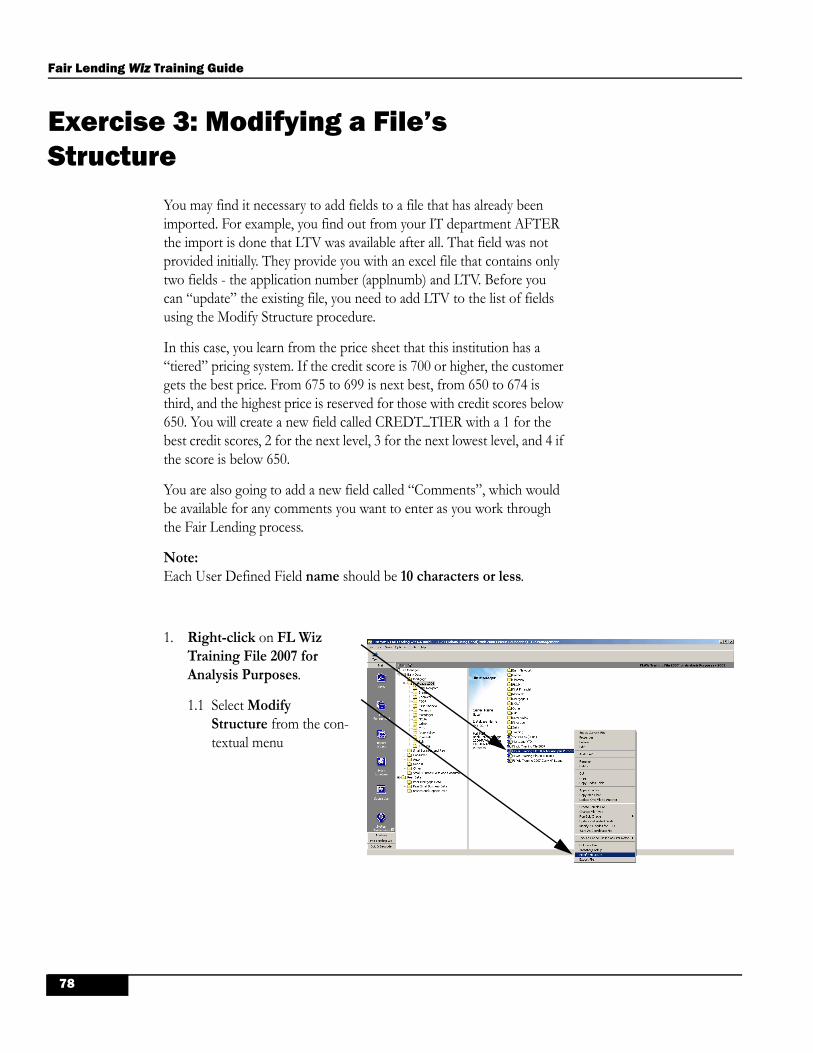

Exercise 3: Modifying a File’s Structure

You may find it necessary to add fields to a file that has already been imported. For example, you find out from your IT department AFTER the import is done that LTV was available after all. That field was not provided initially. They provide you with an excel file that contains only two fields - the application number (applnumb) and LTV. Before you can “update” the existing file, you need to add LTV to the list of fields using the Modify Structure procedure.

In this case, you learn from the price sheet that this institution has a “tiered” pricing system. If the credit score is 700 or higher, the customer gets the best price. From 675 to 699 is next best, from 650 to 674 is third, and the highest price is reserved for those with credit scores below 650. You will create a new field called CREDT_TIER with a 1 for the best credit scores, 2 for the next level, 3 for the next lowest level, and 4 if the score is below 650.

You are also going to add a new field called “Comments”, which would be available for any comments you want to enter as you work through the Fair Lending process.

Note: Each User Defined Field name should be 10 characters or less.

1. Right-click on FL Wiz Training File 2007 for Analysis Purposes.

1.1 Select Modify Structure from the con-textual menu

78

File Management

2. Click on the Optional Col-umns tab (you can not mod-ify the Required Columns).

3. Scroll down to the bottom of the list.

3.1 Click on Add New Column

4. When COLUMN00 is high-lighted in blue, type CREDT_TIER.

4.1 Click in the Data Type column

4.2 Open the drop-down list

4.3 Select Int (Integer).

5. Click on Add New Column once again.

79

Fair Lending Wiz Training Guide

6. Replace COLUMN00 with COMMENTS,

6.1 Set the Data Type to VarChar

6.2 Set the length to 50.

7. Click on the Apply button. Scroll down to the bottom of the field list to see the changes.

7.1 Click OK to finish the process.

80

File Management

Exercise 4: Adding Values to a New Field

You created a new field called “CREDT_TIER” in the last exercise. You need to populate this field with values based on the credit scores stored in the CUST_CREDT field.

You will use the Replace Wizard to fill the new field. There are at least two ways of doing this:

Create a separate Replace line for each “tier”

Replace CREDT_TIER with 1 FOR CUST_CREDT >= 700

Replace CREDT_TIER with 2 FOR CUST_CREDT >= 675 and CUST_CREDT < 700

Replace CREDT_TIER with 3 FOR CUST_CREDT >= 650 and CUST_CREDT < 675

Replace CREDT_TIER with 4 FOR CUST_CREDT <650

Create ONE replace statement that will take care of all four possibilities, using an Intelligent IF statement to perform the logic necessary. As in Excel, the IF statement considers the logic statement, and if true, applies the first option. If false, it goes to the second option.

Replace CREDT_TIER with

IIF(cust_credt >= 700,1,

IIF(cust_credt >= 675 and cust_credt < 700,2,

IIF(cust_credt >= 650 and cust_credt < 675,3,

IIF(cust_credt < 650,4,5))))

FOR cust_credt > 0

You will be using the first method shown above.

81

Fair Lending Wiz Training Guide

1. Right-click on FL Wiz Training File 2007 for Analysis Purposes.

1.1 Select Edit from the contextual menu.

2. In the Tool Bar, click on the Replace button.

3. To start, follow these direc-tions:

3.1 Click All Records3.2 Click the Checkbox for

the first row of replace commands

3.3 Open the drop-down list, and type CREDT, then select CREDT_TIER from the list.

82

File Management

4. Click into the Replace With box.

4.1 Click on the Ellipsis on the right side

5. In the lower part of the screen (the Expression Win-dow), type “1” without quotes, the click on Apply.

6. Click into the Replace For box, then click the Ellipsis.

7. Once in the Expression Builder, single-click on any field to activate that portion of the Expression Builder.

7.1 Start typing CUST_CREDT until that field is found.

7.2 Double-click on CUST_CREDT.

83

Fair Lending Wiz Training Guide

8. In the Expression Window, click after CUST_CREDT, and type in >= 700. Click Apply.

Note: Spaces are OPTIONAL between the field name and the >= symbols. However, if you were to stack two com-mands together (this AND that), the word AND must be separated by spaces.

9. For the second line in the replace set:

9.1 Click the Checkbox for a second line

9.2 Open the Target drop-down list and select Credt_Tier

9.3 Click the Ellipsis in the Replace With area

9.4 Type 2.9.5 Click Apply.9.6 Click the Ellipsis in the

Replace For area9.7 Type in the Expres-

sion “cust_credt >= 675 and cust_credt < 700”

9.8 Click Apply.

84

File Management

10. Complete the remainder of Lines 3 and 4:

10.1 Line 3, replace with “3”

Note: Click the drop-down list and select an expression to copy, then click the Ellipsis to modify it.

10.2 Line 3, replace for cust_credt >= 650 and cust_credt < 675

10.3 Line 4, replace with “4”10.4 Line 4, replace for

cust_credt < 650

11. Get in the habit of saving expressions that you may use again. Click into the Replace Command text box until the cursor flashes within the box.

11.1 Type Replace Credt_Tier from Cust_Credt.

11.2 Click the Save button.

11.3 Click OK.

12. Click on Execute. The mes-sage should reflect success and show the changes reflected to the right.

85

Fair Lending Wiz Training Guide

Exercise 5: Adding / Modifying New Code(s)

Adding a new field to your file is only effective for your analyses if you also add the field to the FL Wiz codes table -- essentially registering the field with FL Wiz. THIS STEP ALLOWS THESE FIELDS TO BE USED IN YOUR FAIR LENDING MODELS.

1. On the File Management screen, right-click on FL Wiz Training File 2007 for Analysis Purposes.

1.1 Select Edit from the contextual menu.

2. Right-click anywhere in the data, and select Locate Field from the contextual menu.

86

File Management

3. Open the drop-down list of fields, and start typing CREDT_TIER until it is located. Select Credt_Tier.

3.1 Close the Find Field dialog box

4. Right-click in the Credt_Tier column.

4.1 Select Modify Codes from the contextual menu.

5. Click the Add New Code button.

6. Follow these steps to input the codes:

6.1 Description: 700+ Press <TAB> key after each entry.

6.1 Code 1 From: 1 To 16.2 Press the <TAB> key to move to the next line6.3 Description: 675 to 6996.4 Code 2 From 2 To 2 6.5 Press the <TAB> key for another line6.6 Description: 650 to 674 6.7 Code 3 From 3 To 3 6.8 Press <TAB> once more6.9 Description: <6506.10Code 4 From 4 To 4 DO NOT PRESS <TAB> AGAIN!

Warning:If you do press Tab too many times, leaving a line with blanks in it, DO NOT click Apply. Instead, click the Delete button, and remove the line with the blanks.

87

Fair Lending Wiz Training Guide

7. Before clicking the Apply button, check your Codes against those on the right. When you are sure all codes are Ok, and that you do NOT have an extra line, click Apply.

Note: When you perform the MODIFY CODES on a text field (the one you just did was numeric), you simply click on the Retrieve Unique Values button to obtain the list of codes.

88

File Management

Exercise 6: Transferring / Installing a File

Fair Lending Wiz clients using a stand-alone work station from a CRA Wiz client within the same institution can install a data file (having a .dat extension) that has been imported, geocoded and edited in CRA Wiz. By using this feature, the Fair Lending Wiz client can immediately use a file for analysis as soon as it’s transferred into their system.

The following exercise will bring you through the steps to install a file.

1. In the View Bar, click on Main, then on File Management to return to the primary file manage-ment screen.

2. Right-click on FL Wiz Training File 2007 for Analysis Purposes.

2.1 Select Transfer/Backup from the contextual menu

89

Fair Lending Wiz Training Guide

3. The Transfer process takes you to a Windows dialog box. Click on the Desktop button in the View Bar, and allow the transferred file to be placed on the desktop. Click Save.

4. To Install the file (in the same folder), right-click within the open area to the right of the folder list.

4.1 Select Install/Restore

5. CRA/FL Wiz will bring you into your Windows Explorer. Navigate to the Desktop, and select the file that you recently backed up.

5.1 When warned about the fact that the same file already exists, click Yes to give the file a new name.

5.2 Name it Install Trial File

5.3 Click OK.

90

File Management

6. Once the process is finished, hit OK. The data file is now in File Manage-ment and can be accessed immediately for analysis.

91

Fair Lending Wiz Training Guide

92

Introduction to Statistics

Chapter 5

Introduction to Statistics

Upon completion of this chapter you will:

Understand basic statistical terms and definitions.

Understand what a T-Statistic is, and how it is used.

Understand the Normal Distribution.

Understand Standard Deviation.

Understand the concept of statistical significance.

93

Fair Lending Wiz Training Guide

Overview

We use Statistics to investigate data. We can use it to generalize, to identify trends or summarize large amounts of information with a few key metrics. Additionally, we use it to identify particular points of interest amongst all the noise, “outliers”, or data that is inconsistent with its peers - an operation that would take a tremendous amount of time and effort to do manually, and perhaps impossible to accom-plish by hand. We created Fair Lending Wiz to be an expert guide to aid you in your search for even a hint of discriminatory practice. But to use Fair Lending Wiz effectively, you will need an understanding of some basic statistical principals, which will be laid out here.

Consider this list of average monthly temperatures for the city of Boston over 13 months:

The mean (or average) temperature is calculated by adding up all the temperatures and then dividing by the total number (13, in this case):

(29 + 34 + 39 + 48 + 58 + 68 + 74 + 72 + 65 + 55 + 45 + 34 + 31) / 13 = 50.2

So the mean temperature for Boston between January ‘06 and January ‘07 was 50.2 degrees.

The median is the middle number when the list is sorted from lowest to highest, like so:

29, 31, 34, 34, 39, 45, 48, 55, 58, 65, 68, 72, 74

The median for this list is 48. (For an even number of data points where there is no single middle value, the median is the average of the middle TWO values.)

The mode is the single value that appears more than any other. In our example there is only one number, 34, that appears more than once therefore, 34 is the mode.

Month Avg Temp

January ‘06 29February ‘06 34March ‘06 39April ‘06 48May ‘06 58June ‘06 68July ‘06 74August ‘06 72September ‘06 65October ‘06 55November ‘06 45December ‘06 34January ‘06 31

94

Introduction to Statistics

Next, we can calculate the standard deviation. Standard deviation is a measure of the average distance between all the data points and the mean. You can tell by looking at the range of values in the table (from a low of 29 to a high of 74) that the standard deviation is going to be relatively high. Our mean, as stated above, is 50.2, so to find the standard deviation we calculate (or, even better, have the computer calculate) the difference between each point and 50.2. The equation to calculate standard deviation is as follows:

Where n is the number of data points in the sample (13 in our case), y is the mean (50.2), and yi is the ith value in the dataset (so 29, 34, 39, etc.).

Carrying out the calculation gives 15.9 as the standard deviation. At this point we should define normal distribution, which will give us some insight into understanding standard deviation.

You’ve probably seen graphs of a normal distribution before. It is more commonly known as a bell curve.

The curve describes the spread of observed values in a hypothetical, “perfectly distributed’ sample set. It describes some phenomenon- such as the spread of interest rates granted to borrowers- where we expect most of the values to be close to the center “hump” of the curve, and fewer and fewer values as you move away from the center. The middle value - the top of the curve - is the mean.

The models in Fair Lending Wiz assume that your loan data should roughly follow this kind of distribution. To understand why this makes intuitive sense, imagine that the curve above is a graph of all the interest rates attached to the a particular type of loan sold by your company in a year (on the x-axis) versus the number of people who took out loans at each rate (on the y-axis). Say the top of the curve represents the number of people who received loans at 7% - the most common rate. Many of the values around 7%, such as 6.8% or 7.3%, are also quite com-mon, as evidenced by the height of the curve at those values. However, we’d also expect that a few loans will fall away from the mean. One of the purposes of Fair Lending Wiz is to help you explain loans in the “tails” of the graph, to the far left (the very low rates) and, more importantly, the values to the far right (the high rates).

1

)(1

2

−

−∑=

n

yyn

ii

95

Fair Lending Wiz Training Guide

The standard deviation tells us how spread out the values are - the higher the standard deviation, the longer and more rounded the curve. Likewise, a small standard deviation means the curve will be tall and skinny - meaning a greater percentage of values are close to the mean.

In a perfect normal distribution, all the values that lie within one standard deviation in each direction from the mean comprise 68% of the data set:

Two standard deviations (actually, a standard deviation of 1.96, to be precise) in each direction includes 95% of the data set:

.

96

Introduction to Statistics

In our Fair Lending analysis, we look at loans that fall outside 95% of the graph contained inside two standard deviations. Of course, we expect to find 5% of all our loans in this outside region. However, there is the possibility that the exceptionally high (or low) rates weren’t determined by “chance” but more deliberate factors. And it is these loans that get lenders into trouble. In fact, by the way the normal distribution is defined, if we find a value that is more than two standard deviations from the mean, we call it statistically significant, since the likelihood that the discrepancy is due to “chance” is only 5%.

One final bit of terminology: A t-stat is simply the number of standard deviations a value lies from the mean. If the t-stat is greater than 1.96, that value is marked as statistically significant (and it can be posi-tive or negative - a negative t-stat means it lies to the left, and a positive t-stat means that value lies to the right).

97

Fair Lending Wiz Training Guide

98

Fair Lending Examination Procedures

Chapter 6

Fair Lending Examination Procedures

Upon completion of this lesson you will:

Understand, at least to some degree, the Interagency Fair Lending Examination Procedures

Know the primary sections of the exam procedures

Know what “Focal Points” and Risk Factors are

99

Fair Lending Wiz Training Guide

Overview

Prior to conducting any type of analysis, it is important to discern where the potential fair lending risks are in your file. With this information you can focus your analysis on a specific product or market. This process not only saves time but also helps you to determine if the data that you are working with is of high quality. This process is also recommended by the Fair Lending Examination Procedures.

To help you determine the scope, focal points, and intensity of your analysis, PCi recommends becoming thoroughly familiar with the “Inter-agency Fair Lending Examination Procedures”. By understanding what process your regulator will use to determine your potential fair lending risks, you can perform the same steps ahead of time and resolve any issues that you may find.

100

Fair Lending Examination Procedures

Interagency Fair Lending Examination Procedures

Part I - Examination Scope Guidelines

The scope of an examination encompasses the loan product(s), mar-ket(s), decision center(s), timeframe, and prohibited basis and control group(s) to be analyzed during the examination. These procedures refer to each potential combination of those elements as a “Focal Point”. Setting the scope of an examination involves first, identifying all of the potential focal points that appear worthwhile to examine. Then from among those, examiners select the focal point(s) that will form the scope of the examination based on risk factors, priorities established in these procedures or by their respective agencies, the record from past exami-nations, and other relevant guidance. This phase includes obtaining an overview of an institutions compliance management system as it relates to fair lending.

Scoping may disclose the existence of circumstances, such as the use of credit scoring or the amount of residential lending which, under an agency’s policy, call for the use of regression analysis or other statistical methods of identifying potential discrimination with respect to one or more loan products. Where that is the case, the agency’s specialized pro-cedures should be employed for such loan products rather than the pro-cedures set forth below.

Setting the intensity of an examination means determining the breadth and depth of the analysis that will be conducted on the selected loan product(s). This process entails a more involved consideration of com-pliance management quality, particularly as it relates to selected products, to reach an informed decision regarding how large a sample of files to review in any transactional analyses performed and whether certain aspects of the credit process deserve heightened scrutiny.

The scoping process can be performed either off-site, onsite, or both, depending on whatever is determined most feasible. In the interest of minimizing burdens on both the examination team and the lender, requests for information from the institution should be carefully thought out so as to include only the information that will clearly be useful in the examination process. Finally, any off-site information requests should be made sufficiently in advance of the on-site schedule to permit institu-tions adequate time to assemble necessary information and provide it to the examination team in a timely fashion.

101

Fair Lending Wiz Training Guide

Examiners should focus the examination based on: