flexible budgets and standard costs

DESCRIPTION

Flexible Budgets and Standard Costs. Chapter 23. HORNGREN ♦ HARRISON ♦ BAMBER ♦ BEST ♦ FRASER ♦ WILLETT. Objectives. 1.Prepare a flexible budget for the statement of financial performance 2.Prepare a financial performance report - PowerPoint PPT PresentationTRANSCRIPT

Flexible Budgets and

Standard CostsChapter 23

HORNGREN ♦ HARRISON ♦ BAMBER ♦ BEST ♦ FRASER ♦ WILLETT

23 - 2Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Objectives

1. Prepare a flexible budget for the statement of financial performance

2. Prepare a financial performance report3. Identify the benefits of standard costing4. Calculate standard cost variances for direct

material and direct labour5. Analyse manufacturing overhead in a standard

cost system6. Record transactions at standard cost7. Prepare a standard cost statement of financial

performance for management

23 - 3Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Objective 1

Prepare a flexible budgetfor the statement of financial

performance.

23 - 4Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Kool-Time PoolsComparison of Actual Results with Static Budget

For the Month Ended June 30, 2004

Actual Static Results Budget Variance

Pools 10 8 2 FRevenues $120,000 $ 96,000 $24,000 FExpenses 105,000 84,000 $21,000 UNet Profit $ 15,000 $ 12,000 $ 3,000 F

Static versus Flexible Budgets

23 - 5Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Static versus Flexible Budgets

Expected Output Volume Only

Static Budget

(8 Pools)

23 - 6Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Static versus Flexible Budgets

Range of Output Volumes

Flexible Budget

(5 Pools) (8 Pools) (11 Pools)

23 - 7Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Flexible Budgets

What are the flexible budgets for Kool-Time Poolswhen expected volume is 5, 8, and 11 pools?

Budgeted sales price per pool is $12,000.Budgeted variable expenses per pool are $8,000.

Total budgeted fixed cost is $20,000.

23 - 8Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Flexible Budgets

Kool-Time Pools Flexible BudgetsUnits 5 8 11Sales revenue $60,000 $ 96,000 $132,000Variable expenses 40,000 64,000 88,000Fixed expenses 20,000 20,000 20,000Net Profit $ 0 $ 12,000 $ 24,000

23 - 9Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Graphing the FlexibleBudget Formula

$0

$108,000

0 5 8 11

Number of Swimming Pools Installed

Tot

al E

xpen

ses

$84,000

$60,000

$20,000

Variable cost

$8,000per poolinstalled

Fixed cost$20,000

per month

Total cost line

23 - 10Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

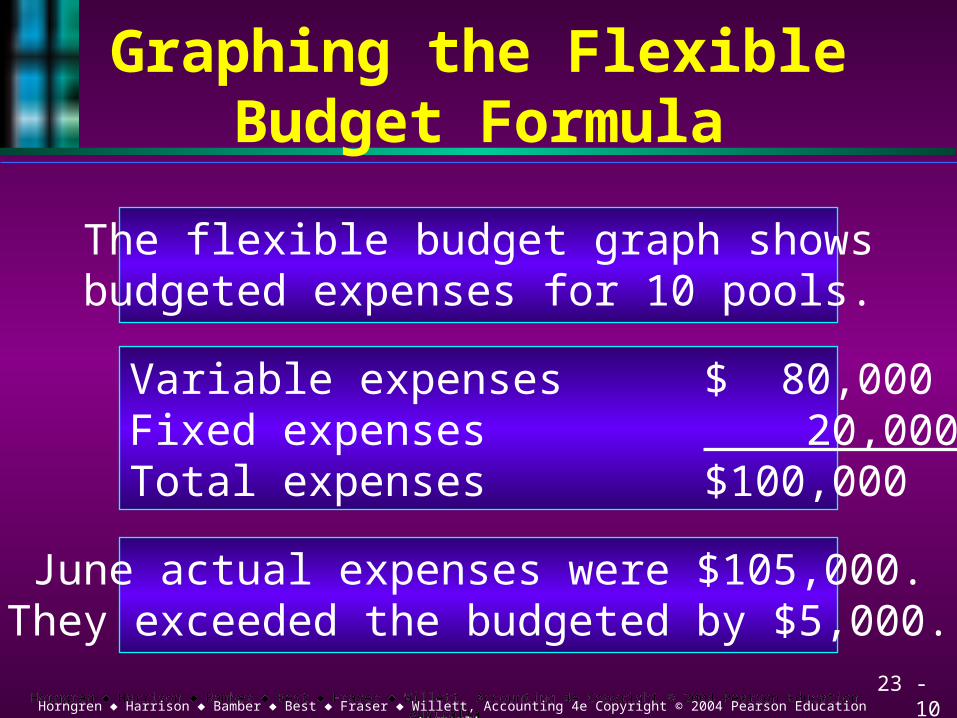

Graphing the FlexibleBudget Formula

The flexible budget graph showsbudgeted expenses for 10 pools.

Variable expenses $ 80,000Fixed expenses 20,000Total expenses $100,000

June actual expenses were $105,000.They exceeded the budgeted by $5,000.

23 - 11Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Objective 2

Prepare a financialperformance

report.

23 - 12Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Kool-Time Pools Performance Report

Actual Flexible Static Results Budget Budget

Pools 10 10 8Revenues $120,000 $120,000 $ 96,000Variable expenses 83,000 80,000 64,000Fixed expenses 22,000 20,000 20,000Total expenses 105,000 100,000 84,000Net Profit $ 15,000 $ 20,000 $ 12,000

23 - 13Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Kool-Time Pools Performance Report

Flexible Budget Variance Sales Volume Variance

ActualResults$15,000

StaticBudget$12,000

FlexibleBudget$20,000

$5,000 U $8,000 F

23 - 14Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Kool-Time Pools Performance Report

Static Budget Variance

ActualResults$15,000

StaticBudget$12,000

$3,000 F

23 - 15Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

The Flexible Budgetand Variance Analysis

The flexible budget variance is the difference between what the company spent at the actual level of output and what it should have spent to obtain the actual level of output.

It highlights the difference between actual costs and flexible budget costs.

23 - 16Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

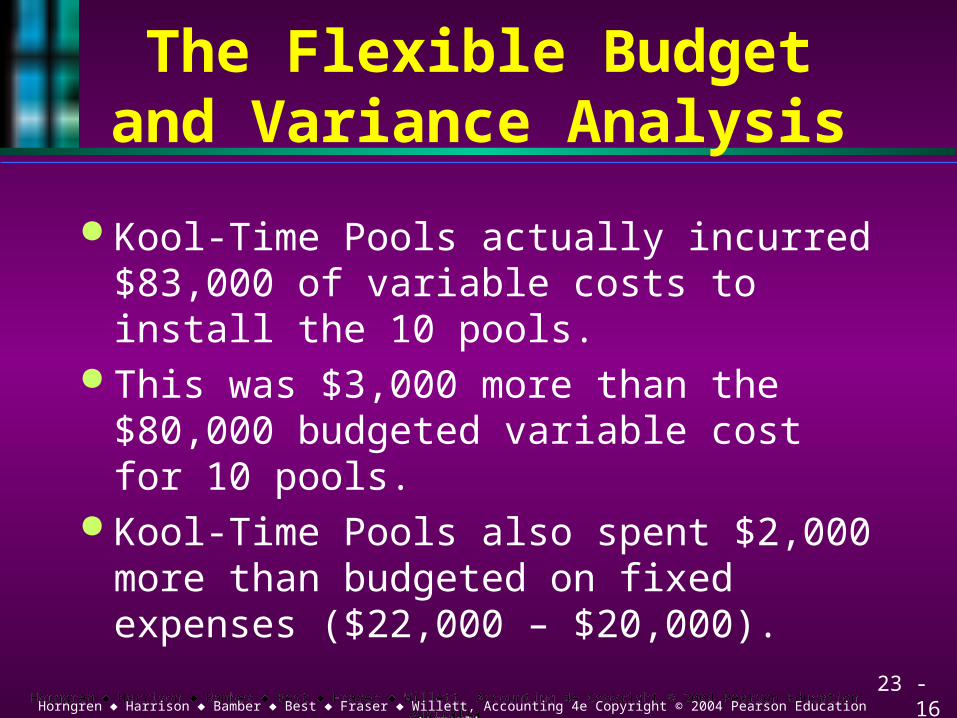

The Flexible Budgetand Variance Analysis

Kool-Time Pools actually incurred $83,000 of variable costs to install the 10 pools.

This was $3,000 more than the $80,000 budgeted variable cost for 10 pools.

Kool-Time Pools also spent $2,000 more than budgeted on fixed expenses ($22,000 – $20,000).

23 - 17Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Objective 3

Identify the benefits

of standard costs.

23 - 18Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Benefits of Standard Costs

Standard costs are carefully predetermined costs.

They help managers plan by providing the unit amounts, which are the building blocks of budgeting.

They help simplify record keeping. Standard quantity often is referred to as

the quantity that should have been used.

23 - 19Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Benefits of Standard Costs

Standards costs are different to flexible budgets because;Flexible budgets keep fixed costs

constant, within the relevant range.Standard costs are on a per unit basis and

allocate an amount of fixed costs to each unit.

23 - 20Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Objective 4

Calculate standard cost variances for

direct materials and direct labour.

23 - 21Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Direct Material andDirect Labour Variances

1 Price, or rate, which measures how well the business keeps unit prices of materials and labour within standards.

2 Efficiency, or quantity, which measures whether the quantity of materials or labour used to make the actual number of outputs is within the budget.

23 - 22Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Price Variance...

– is the difference between the actual price and standard price of inputs used multiplied by the actual quantity of inputs.

Price variance = (Actual quantity × Actual price) – (Actual quantity × Standard price) or...

Actual quantity × (AP – SP)

23 - 23Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

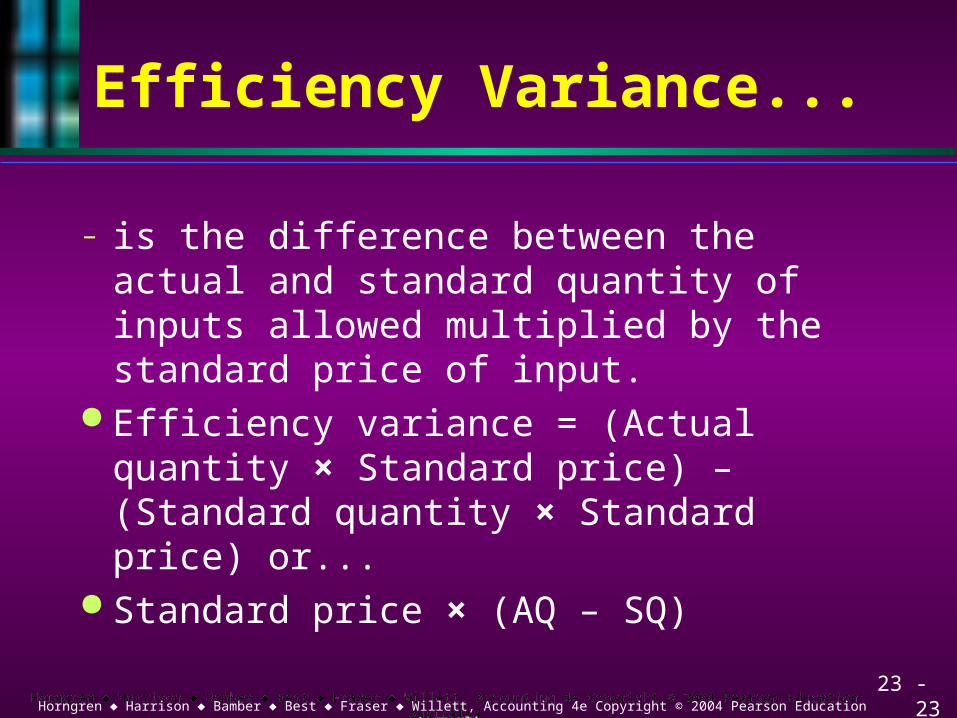

Efficiency Variance...

– is the difference between the actual and standard quantity of inputs allowed multiplied by the standard price of input.

Efficiency variance = (Actual quantity × Standard price) – (Standard quantity × Standard price) or...

Standard price × (AQ – SQ)

23 - 24Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Variance analysis begins with a total variance to be explained – in this example, $5,000.

Actual variable expenses $ 83,000Flexible budget – 80,000 Difference 3,000

Actual fixed expenses were $2,000more than budgeted.

Example of Standard Costing

23 - 25Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

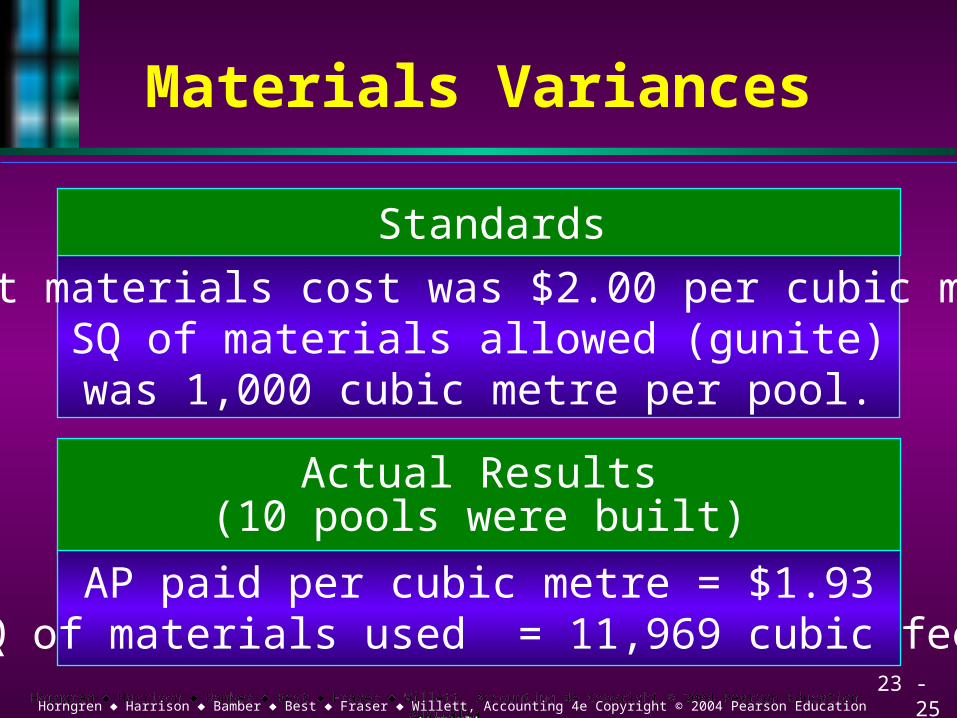

Materials Variances

Direct materials cost was $2.00 per cubic metre.SQ of materials allowed (gunite)was 1,000 cubic metre per pool.

Standards

Actual Results (10 pools were built)

AP paid per cubic metre = $1.93AQ of materials used = 11,969 cubic feet

23 - 26Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

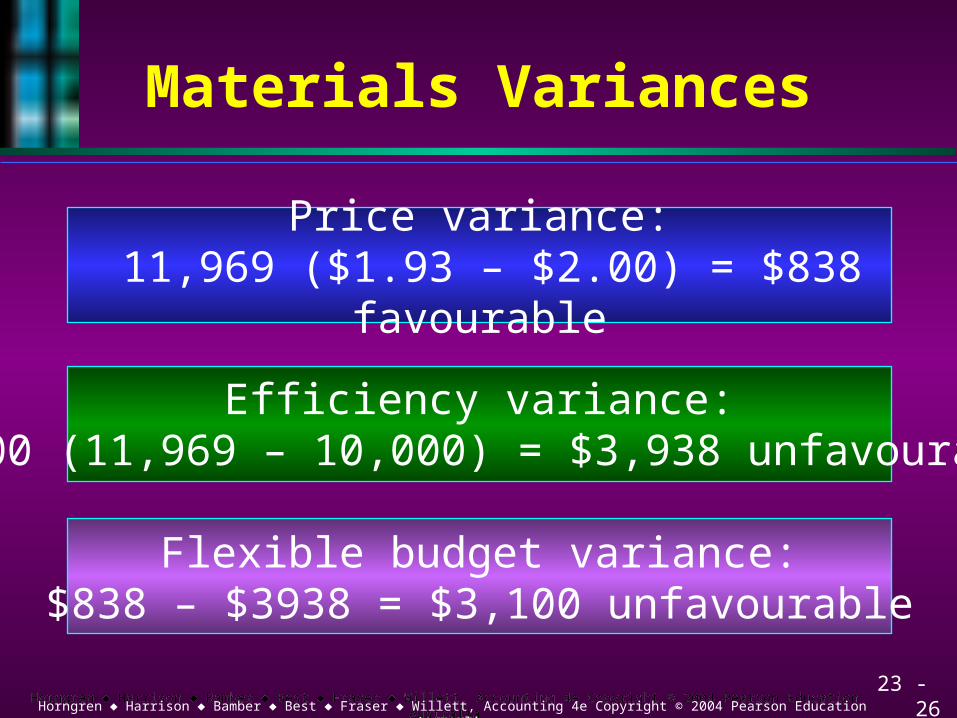

Price variance: 11,969 ($1.93 – $2.00) = $838 favourable

Efficiency variance:$2.00 (11,969 – 10,000) = $3,938 unfavourable

Flexible budget variance:$838 – $3938 = $3,100 unfavourable

Materials Variances

23 - 27Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Materials Variances

Actual cost incurred: (Actual inputs × Actual price) = 11,969 × $1.93 = $22,100

Standard cost of actual inputs: (Actual inputs × Standard price) = 11,969 × $2 = $23,938

Flexible budget: (Standard inputs × Standard price) = 10,000 × $2 = $20,000

23 - 28Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Labour Variances

Standards

Actual Results (10 pools were built)

Direct labour cost was $4,200 per pool.SP (rate) was $10.50 per hour.

Standard hours per pool was 400.

AP (actual rate) was $11.00 per hour.AQ (actual hours) was 3,800.

23 - 29Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Labour Variances

Price (or rate) variance:3,800($11.00 – $10.50) = $1,900 unfavourable

Efficiency variance:$10.50(3,800 – 4,000) = $2,100 favourable

Flexible budget variance:$2,100 – $1,900 = $200 favourable

23 - 30Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

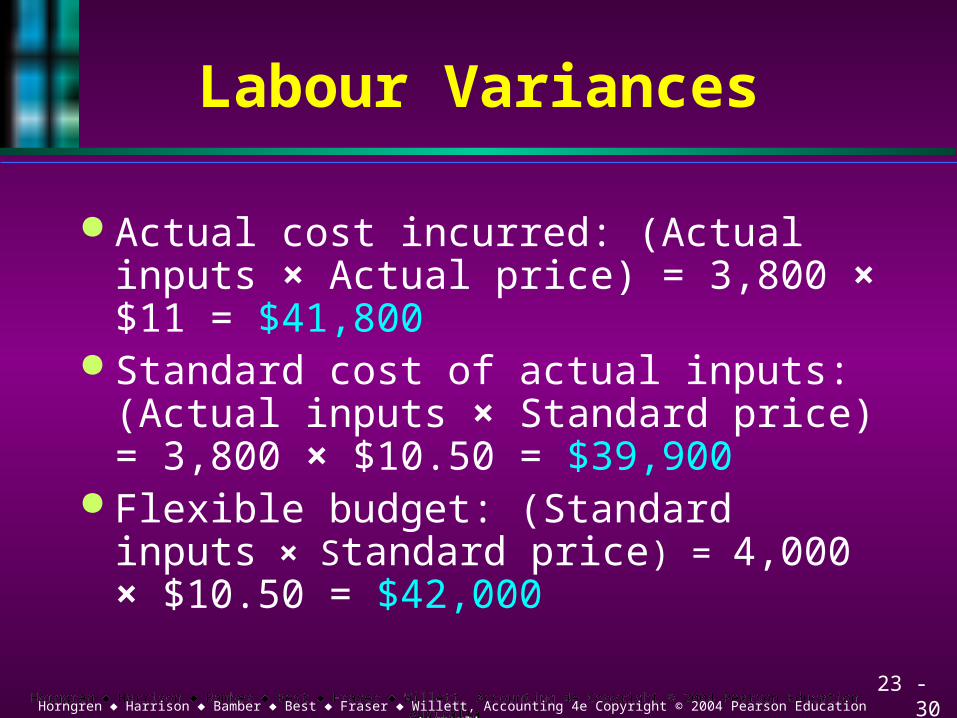

Labour Variances

Actual cost incurred: (Actual inputs × Actual price) = 3,800 × $11 = $41,800

Standard cost of actual inputs: (Actual inputs × Standard price) = 3,800 × $10.50 = $39,900

Flexible budget: (Standard inputs × Standard price) = 4,000 × $10.50 = $42,000

23 - 31Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Flexible Budget Variancesfor Materials and Labour

Flexible budget variance for materials $3,100 UFlexible budget variance for labour 200 FTotal variances $2,900 U

Total flexible budget variance $5,000 UMaterials and labour variances 2,900 UFlexible budget overhead variances $2,100*U

*Flexible budget man. O/H variance $1,300 U*Marketing and admin. O/H variance $ 800 U

(see Exhibit 23-9 page 1005 textbook)

23 - 32Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Objective 5

Analyse manufacturing overheadin a standard cost system.

23 - 33Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Manufacturing Overhead Variances

The flexible budget variance for manufacturing overhead shows whether managers are keeping total overhead costs within the budgeted amount for the actual production of the period (actual – flexible).

The production volume variance (this is a new concept and not part of the total flexible budget variance ) arises when actual production differs from the level in the static budget (allocated – flexible).

23 - 34Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Allocating Overhead to Production

Kool-Time Pools allocates manufacturing overhead to production based on standard direct labour hours for the actual number of outputs.

The static budget, which is based on expected output of 8 pools, is known at the beginning of the period.

23 - 35Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Allocating Overhead to Production

Standards

Actual Results (10 pools were built)

Variable overhead cost was $800 per pool.Standard hours per pool were 400.Fixed overhead cost was $12,000.

Actual variable overhead was $9,000.Actual hours were 3,800 fixed overhead was

$12,300 and total overhead was $21,300.

23 - 36Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Allocating Overhead to Production

In a standard cost system, manufacturing overhead is allocated to production based on a predetermined overhead rate.

Most companies base their predetermined overhead rates on amounts from the static (master) budget which is known at the beginning of the year (month).

23 - 37Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Allocating Overhead to Production

Kool-Time PoolsBudget Data for the Month Ended June 30, 2004

Budget type Static FlexiblePools 8 10Standard direct labour hours 3,200 4,000Overhead cost:

Variable $ 6,400 $ 8,000Fixed 12,000 12,000

Total $18,400 $20,000

23 - 38Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

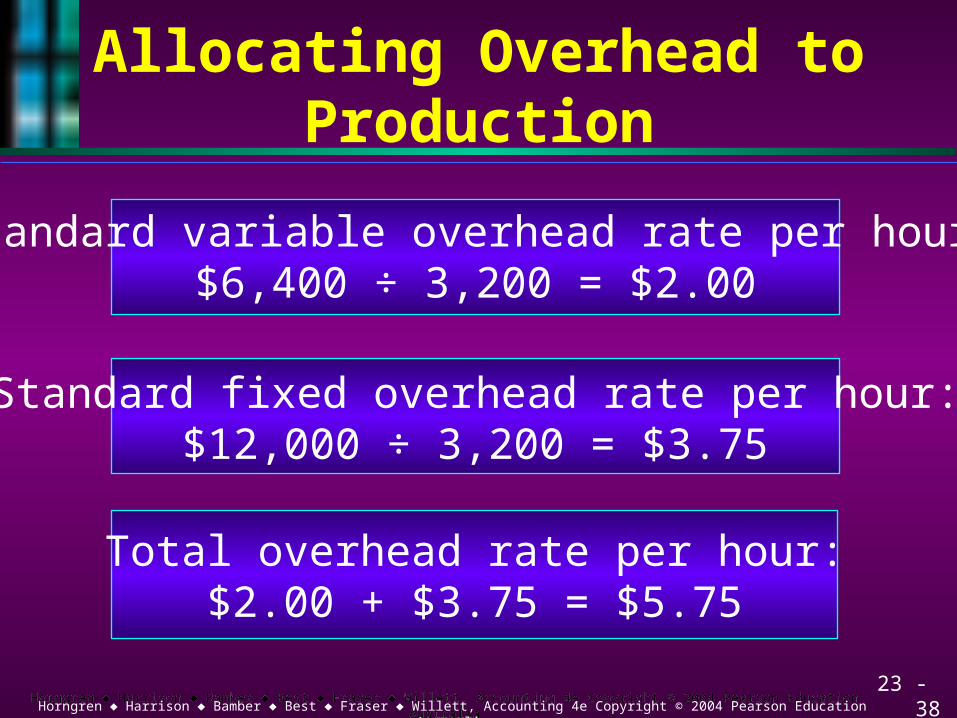

Allocating Overhead to Production

Standard variable overhead rate per hour:$6,400 ÷ 3,200 = $2.00

Standard fixed overhead rate per hour:$12,000 ÷ 3,200 = $3.75

Total overhead rate per hour:$2.00 + $3.75 = $5.75

23 - 39Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

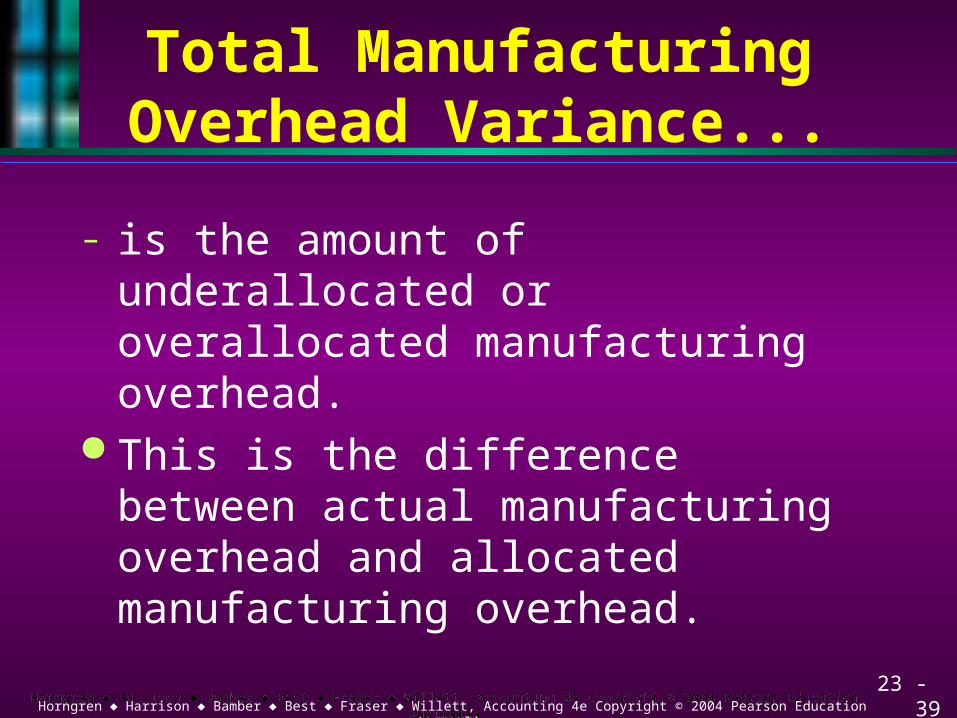

Total ManufacturingOverhead Variance...

– is the amount of underallocated or overallocated manufacturing overhead.

This is the difference between actual manufacturing overhead and allocated manufacturing overhead.

23 - 40Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Total ManufacturingOverhead Variance

How much standard overhead is allocated to production?

4,000 × $2.00 $ 8,000 variable4,000 × $3.75 15,000 fixedTotal $23,000

Total manufacturing overhead cost varianceis allocated minus actual:

$23,000 – $21,300 = $1,700 favourable

23 - 41Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Total ManufacturingOverhead Variance

The total manufacturing overhead variance is split into the manufacturing flexible budget variance and the production volume variance:

Flexible budget overhead for actual production = $12,000 + (4,000 × $2) = $20,000.

23 - 42Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Overhead Flexible Budget Variance

Kool-Time Pools – a comparison of actual results withthe flexible budget overhead for actual production:

Actual Results Flexible Budget Variance

Pools 10 10Overhead cost:Variable $ 9,000 $ 8,000 $1,000 UFixed 12,300 12,000 $ 300 UTotal $21,300 $20,000 $1,300 U

Overhead flexible variance is $1,300 unfavourable.

23 - 43Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

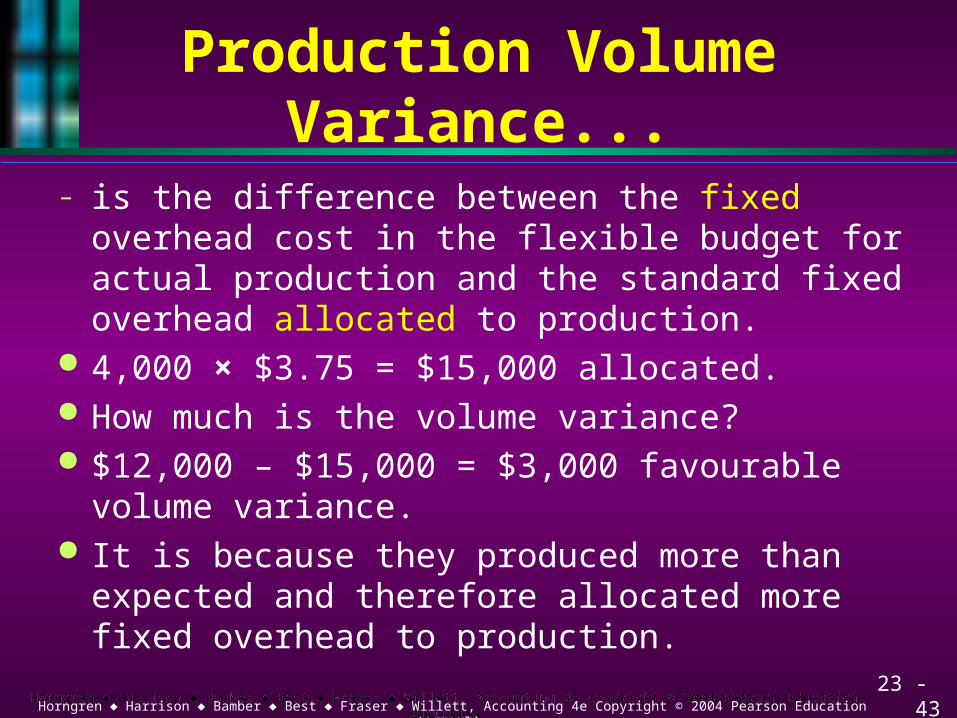

Production Volume Variance...

– is the difference between the fixed overhead cost in the flexible budget for actual production and the standard fixed overhead allocated to production.

4,000 × $3.75 = $15,000 allocated. How much is the volume variance? $12,000 – $15,000 = $3,000 favourable volume

variance. It is because they produced more than expected

and therefore allocated more fixed overhead to production.

23 - 44Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Flexible Budget Variance

Flexible budget variance: $5,000 U

Materials $3,100 ULabour 200 FMarketing and admin. variance 800 UFlexible budget man. overhead variance 1,300 UTotal $5,000 U

23 - 45Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Total Variances

Why was actual profit $5,000 less than the flexible budget for 10 pools?

Variable costs exceeded the flexible budget by $3,000 and actual fixed costs exceeded the static budget by $2,000.

See exhibit 23-9 page 1005 textbook

23 - 46Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Record transactions

at standard cost.

Objective 6

23 - 47Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

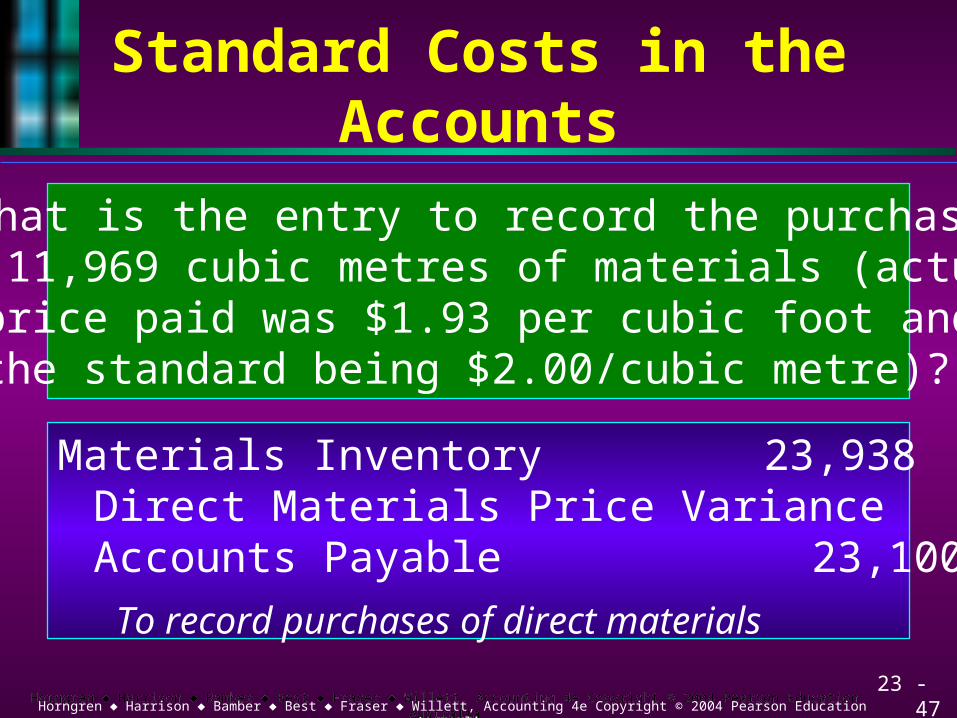

What is the entry to record the purchaseof 11,969 cubic metres of materials (actual

price paid was $1.93 per cubic foot andthe standard being $2.00/cubic metre)?

Standard Costs in the Accounts

Materials Inventory 23,938Direct Materials Price Variance 838Accounts Payable 23,100

To record purchases of direct materials

23 - 48Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

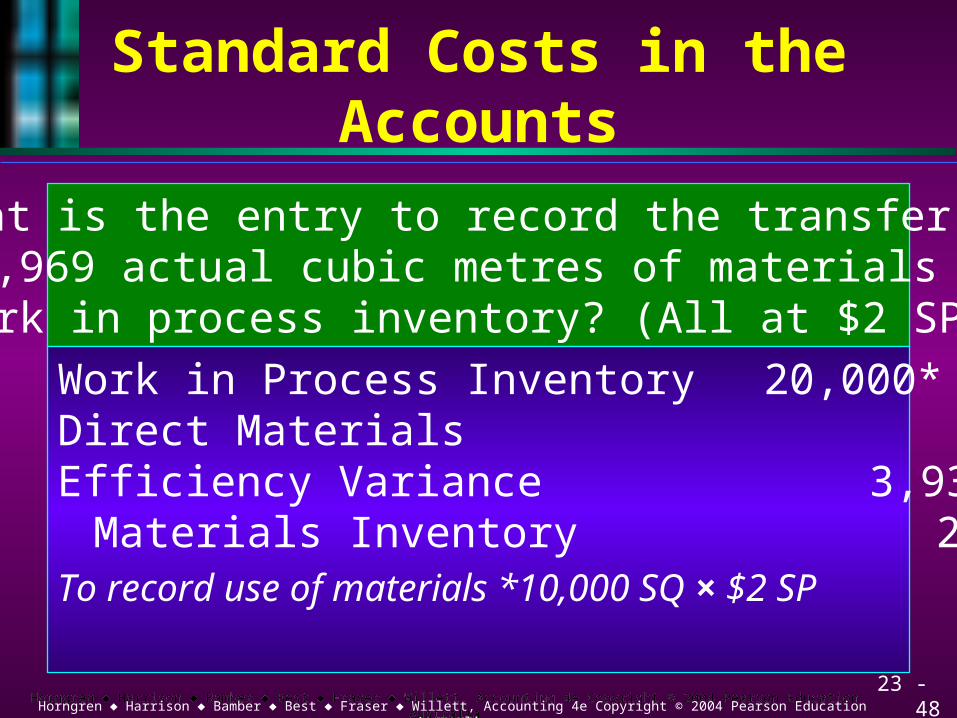

What is the entry to record the transfer of11,969 actual cubic metres of materials towork in process inventory? (All at $2 SP)

Standard Costs in the Accounts

Work in Process Inventory 20,000*Direct MaterialsEfficiency Variance 3,938

Materials Inventory 23,938To record use of materials *10,000 SQ × $2 SP

23 - 49Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

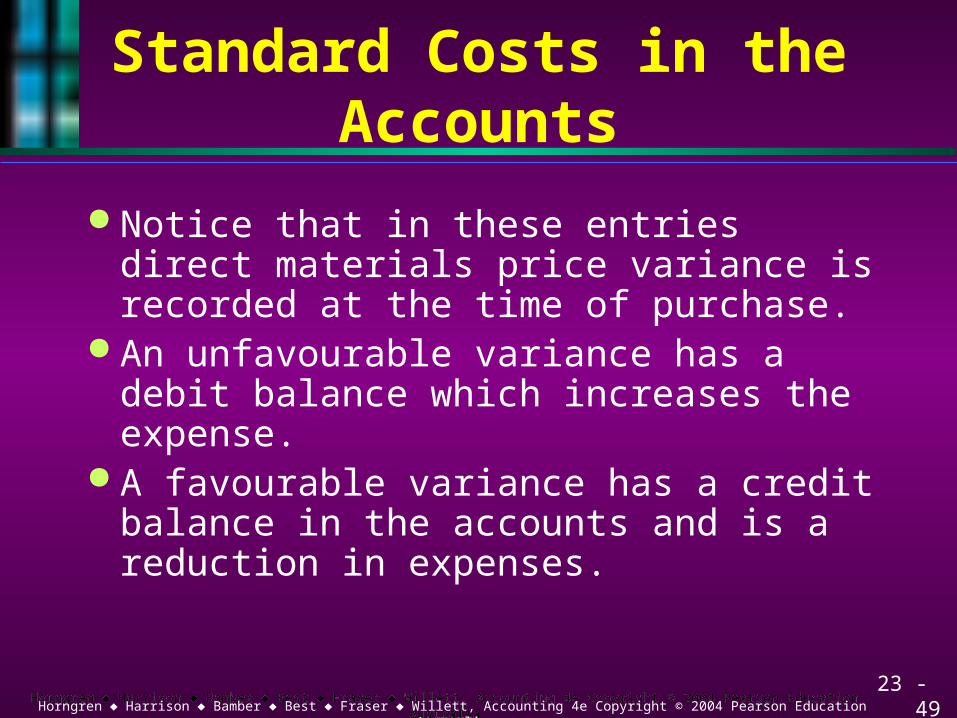

Standard Costs in the Accounts

Notice that in these entries direct materials price variance is recorded at the time of purchase.

An unfavourable variance has a debit balance which increases the expense.

A favourable variance has a credit balance in the accounts and is a reduction in expenses.

23 - 50Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Standard Costs in the Accounts

Manufacturing Overhead 21,300 Accounts Payable, Accumulated Depreciation, and Other accounts

21,300 To record actual overhead costs incurred

See Exhibit 23-14 page 1013 textbook See Exhibit 23-14 page 1013 textbook

23 - 51Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

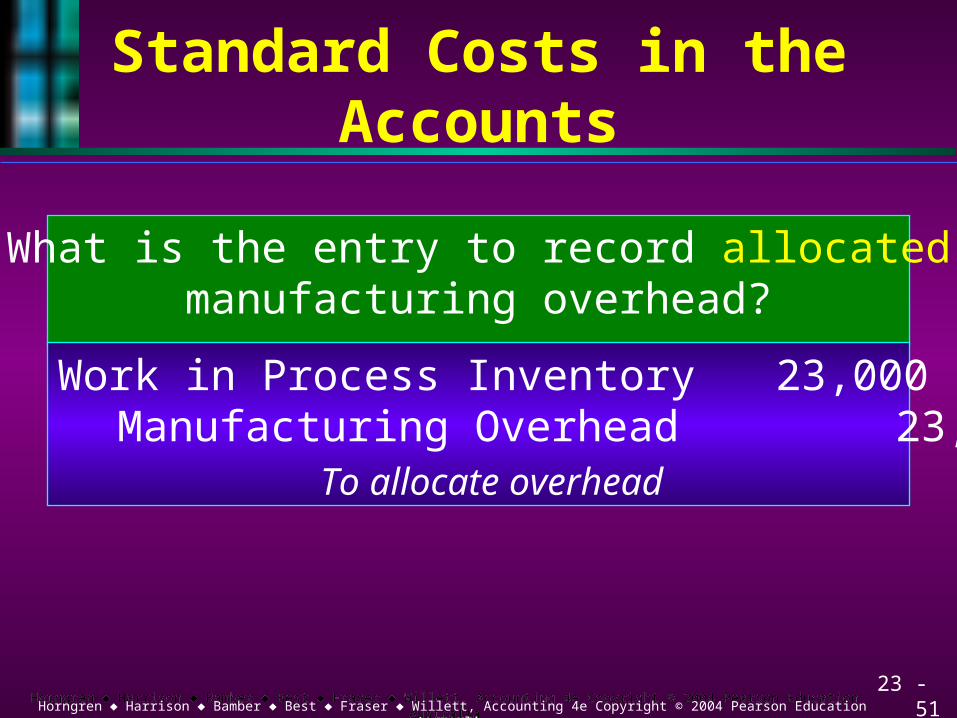

Standard Costs in the Accounts

What is the entry to record allocatedmanufacturing overhead?

Work in Process Inventory 23,000Manufacturing Overhead 23,000

To allocate overhead

23 - 52Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Other Entries

Finished Goods Inventory 85,000Work in Process Inventory 85,000

To record completion of 10 pools

Cost of Goods Sold 85,000Finished Goods Inventory 85,000

To record sale of 10 pools

23 - 53Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Closing Variances

Unfavourable Variances

Favourable VariancesMaterials price $ 838Labour efficiency 2,100Production volume 3,000Total $ 5,938

Materials efficiency $ 3,938Labour price 1,900Flexible budget 1,300Total $ 7,138

23 - 54Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Closing Variances

$7,138 unfavourable – $5,938 favourable= $1,200 unfavourable

Profit and Loss Summary 1,200Net Variance 1,200

To close various variances

This entry decreases profits.

23 - 55Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Prepare a standard coststatement of financial

performancefor management.

Objective 7

23 - 56Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Standard Cost Statement of Financial

Performance for Management Standard Costing

Revenues $120,000COGS 85,000Unadjusted gross profit $ 35,000

Actual CostingRevenues $120,000Cost of goods sold 86,200Unadjusted income $ 33,800

23 - 57Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Standard Cost Statement of Financial

Performance for Management Closing the $1,200 net unfavourable

variance to profit and loss summary reduces the gross profits by $1,200.

This produces the $33,800 gross profit figure.

Remember standard costs are different to flexible budgets.

23 - 58Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

End of Chapter 23