flowers industries, inc

TRANSCRIPT

Xufei Xu

Yi Li

Sin Tung Chan

Xiaoqiao Wang

Minyi Xu

Flowers Industries, IncBMGT440 Financial Case Analysis

Introduction

A largest U.S. wholesale baking company

Based in Thomasville, Georgia

Founded in 1919

Produced baked food, snack foods, & convenience

food

Goal : most profitable Least-Cost Producer

1970s – 1980s: Grown through Acquisition strategy

which has served the company for many years

Flowers Industry, Inc.’s History

1984 — Sales of $603 mil

1985 — Became a Fortune 500 company

Significant Sales Growth came from Acquisition

50-60% Sale Growth – from acquisition

100% Earnings Growth – from internal development

1974-1984 Industry S&500 Flowers

Compound

Revenue Growth

3% 8% 17%

EPS Decrease 6% 6% 17%

Anticipate Opportunities

Marty Wood tried to find an opportunity to raise 50

million dollars to finance the company.

Three alternatives:

1. Common stock issue

2. Straight debt issue

3. Convertible Subordinated debentures

- Not immediately require capital

Company’s Financial Status

Financially profitable during 1974- 1984.

Sales growth=17%

S&P 500 average=8%

High EPS growth

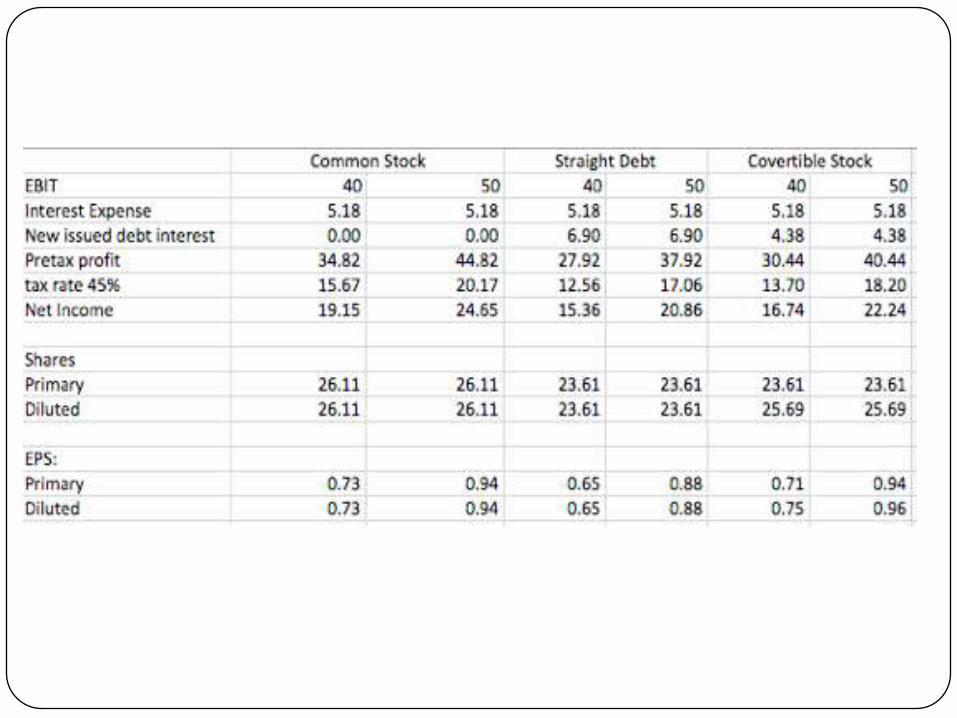

EPS Analysis

Fact: Raise approximately 50 million dollars to

continue their acquisition opportunities

Three ways need to be consider: Straight debt financing

Common Stock

Convertible bond

Step 1: Calculate Net Income

Step2: Calculate Number of Shares

Step3: Calculate EPS

However, the fully diluted EPS in the case of convertible debt adjusts for

the assumed conversion of the debt by adding back the after-tax cost of

debt which equals:

(Net income +new interest expense*(1-45%))/number of diluted shares outstanding

Choose Convertible Stock!

• Financial Risks

• Flexibility

• Voting Control

• Timing of Financing

Other Factors

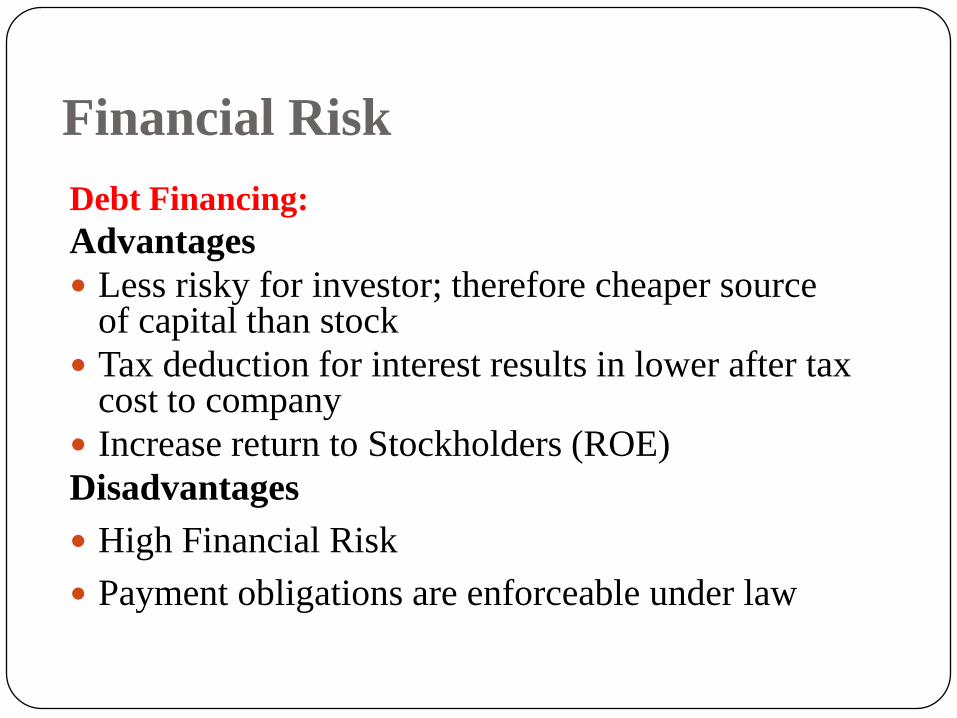

Financial Risk

Debt Financing:

Advantages

Less risky for investor; therefore cheaper source of capital than stock

Tax deduction for interest results in lower after tax cost to company

Increase return to Stockholders (ROE)

Disadvantages

High Financial Risk

Payment obligations are enforceable under law

Financial Risk

Equity financing:

Advantage:

No legal obligation to pay dividends if not making any

profit

Low financial risk

Disadvantage:

More risky for investors makes it more expensive form of

capital

Require higher return for investing in stock

Flexibility

Debt Financing:

Have specific monthly payment

Potential to go bankrupt

Equity financing:

Preferred; because lower regular cash payment

requirements

Voting Control

Debt financing have more percentage of voting control

Straight debt has no dilution on ownership at all

Best option from Voting control perspective

Timing

When interest rate is high, the company will choose to

use equity financing method rather than debt financing.

However, if the stock price of the company is high, the

company is willing to issue stock rather than debt

because the stock price is somewhat overvalued.

Market interest rate is relatively low and the stock

market is not well, choose convertible stock!

3-step Analysis:1. Price without calling the option

2. Term to call

3. Confirm that the term is fair to call

When should the company call the

option?

1. Price without calling

2.Term to call

Dividend

3. Is it a fair estimate?

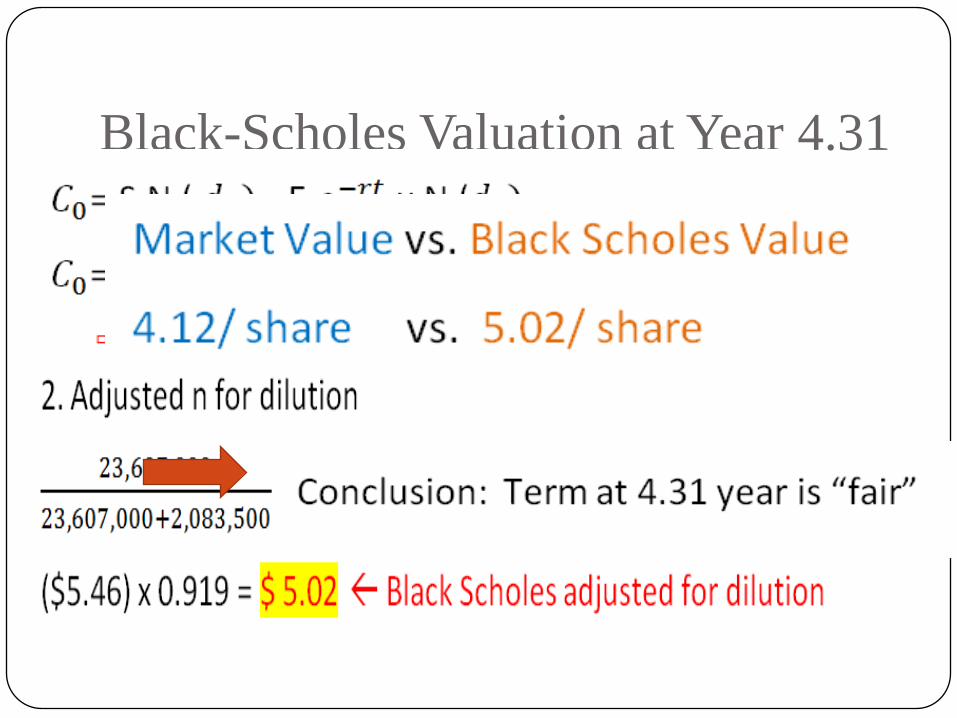

To confirm, we use two approaches:

1. Market value

2. Black-Scholes Value

evaluating whether option contracts are fairly priced

comparing the price of this instrument, the exercise

price of the option, the volatility of the instrument,

the time remaining until the expiration of the option

contract, and current interest rates

Market Price Valuation at year 4.31

Black-Scholes Valuation at Year 4.31

Recommendation and Decision

Best choice: Convertible bonds

Yields the highest EPS

Better control over the leveraging process

EPS growth was maintained at 15%

Stock price went above conversion price in late 1987

and early 1988.

Convertible bonds were called only in August 1992.

Questions?