flowserve corporate...

TRANSCRIPT

Flowserve Corporate OverviewLehman Brothers Industrial Select ConferenceFebruary 11 – 13, 2008

Lew Kling, President and Chief Executive OfficerMark Blinn, SVP, CFO and Latin America OperationsZac Nagle, VP Investor Relations

Flowserve Corporation Proprietary & Confidential Page 2

Special NoteSAFE HARBOR STATEMENT: This presentation includes forward-looking statements. Forward-looking statements are all statements that are not statements of historical facts and include, without limitation, statements relating to our business strategy and statements of expectations, beliefs, future plans and strategies and anticipated developments concerning our industry, business, operations and financial performance and condition. The words “believe”, “seek”, “anticipate”, “plan”, “estimate”, “expect”, “intend”, “project”, “forecast”, “predict”, “potential”, “continue”, “will”, “may”, “could”, “should”, and other words of similar meaning are intended to identify forward-looking statements. The forward-looking statements made in this news release are made pursuant to safe harbor provisions of the Private Securities Litigation Reform Act of 1995. These forward-looking statements involve known and unknown risks, uncertainties and other factors that, in some cases, are beyond our control. These risks, uncertainties and factors may cause our actual results, performance and achievements, or industry results and market trends, to be materially different from any future results, performance, achievements or trends expressed or implied by such forward-looking statements. Important risks, uncertainties and other factors that could cause actual results to differ from these forward-looking statements include, but are not limited to, the following: inherent limitations of the effectiveness of our internal control over financial reporting; potential adverse consequences resulting from securities class action litigation and other litigation, including asbestos-containing product claims; the possibility of adverse consequences related to the domestic and foreign government actions regarding our participation in the United Nations Oil-for-Food Program; the possibility of adverse consequences of governmental tax audits of our tax returns, including the ongoing IRS audit of our U.S. tax returns for the years 2002 through 2004; our ability to convert bookings, which are not subject to nor computed in accordance with generally accepted accounting principles, into revenues at acceptable, if any, profit margins, since such profit margins cannot be assured or assumed to follow historical trends; changes in the financial markets and the availability of capital; changes in the already competitive environment for our products or competitors' responses to our strategies; our inability to continue to expand our market presence through acquisitions, and unforeseen integration difficulties or costs resulting from acquisitions; economic, political and other risks associated with our international operations, including military actions, trade embargoes or any terrorist attacks that could affect customer markets, including the continuing conflict in Iraq, uncertainties in certain Middle Eastern countries such as Iran, and their potential impact on Middle Eastern markets and global petroleum producers; our ability to comply with the laws and regulations affecting our international operations, including the U.S. export laws, and the effect of any noncompliance; the potential adverse impact of a significant downturn in petroleum, chemical, power and water industries; changes in economic conditions and the extent of economic growth in the U.S. and other countries and regions; unanticipated difficulties or costs associated with the implementation of systems, including software; unanticipated higher costs associated with environmental compliance and liabilities; our relative geographical profitability and its impact on our utilization of foreign tax credits; the potential impact of our indebtedness on cash flows and our ability to meet the financial covenants and other requirements in our debt agreements; adverse changes in the regulatory climate and other legal obligations imposed on us; and other factors described from time to time in our filings with the SEC. It is not possible to foresee or identify all the factors that may affect our future performance or any forward-looking information, and new risk factors can emerge from time to time. Given these risks and uncertainties, you should not place undue reliance on forward-looking statements as a prediction of actual results. All forward-looking statements included in this news release are based on information available to us on the date of this news release. We undertake no obligation to revise or update any forward-looking statement or disclose any facts, events or circumstances that occur after the date hereof that may affect the accuracy of any forward-looking statement.

Mining Pulp & PaperOil / Gas Power Chemical Water

Page 3Flowserve Proprietary & Confidential

INFRASTRUCTURE INDUSTRIES

North America Latin America Europe Middle East Africa China India Rest of Asia

GLOBAL PRESENCE

GENERAL INDUSTRIESFood & Bev

A Leading Portfolio of Products, Solutions & Services

Flowserve Applies It’s Product Expertise to Provide Value-Add for Our Customers

A Broad Set of Product Capabilities Critical IndustryApplication SolutionsPumps - Valves - Seals

AftermarketSupport Services

Global Quick Response Center (QRC) Footprint

Product Management

Skills Management

Operations Management

Oil / Gas

Chemical Water

General Industry

Power

Mining Pulp & PaperOil / Gas Power Chemical Water

Page 4Flowserve Proprietary & Confidential

INFRASTRUCTURE INDUSTRIES

North America Latin America Europe Middle East Africa China India Rest of Asia

GLOBAL PRESENCE

GENERAL INDUSTRIESFood & Bev

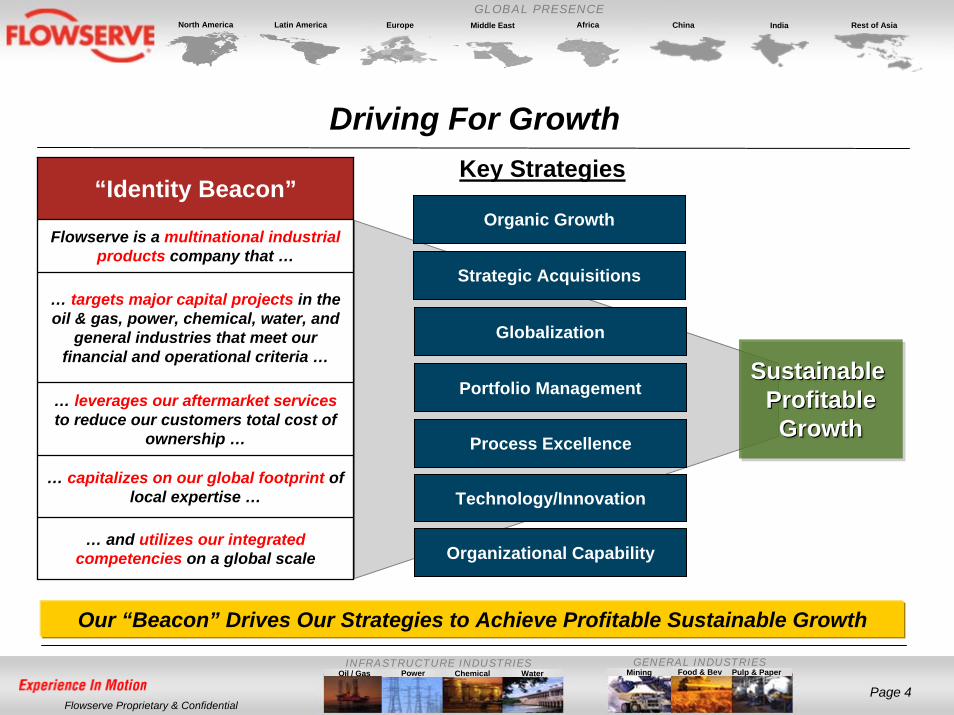

Driving For Growth

Organic Growth

Globalization

Strategic Acquisitions

Organizational Capability

Process Excellence

Technology/Innovation

Key Strategies

Sustainable ProfitableGrowth

Sustainable Sustainable ProfitableProfitableGrowthGrowth

“Identity Beacon”

Flowserve is a multinational industrial products company that …

… targets major capital projects in the oil & gas, power, chemical, water, and

general industries that meet our financial and operational criteria …

… leverages our aftermarket servicesto reduce our customers total cost of

ownership …

… capitalizes on our global footprint of local expertise …

… and utilizes our integrated competencies on a global scale

Our “Beacon” Drives Our Strategies to Achieve Profitable Sustainable Growth

Portfolio Management

Mining Pulp & PaperOil / Gas Power Chemical Water

Page 5Flowserve Proprietary & Confidential

INFRASTRUCTURE INDUSTRIES

North America Latin America Europe Middle East Africa China India Rest of Asia

GLOBAL PRESENCE

GENERAL INDUSTRIESFood & Bev

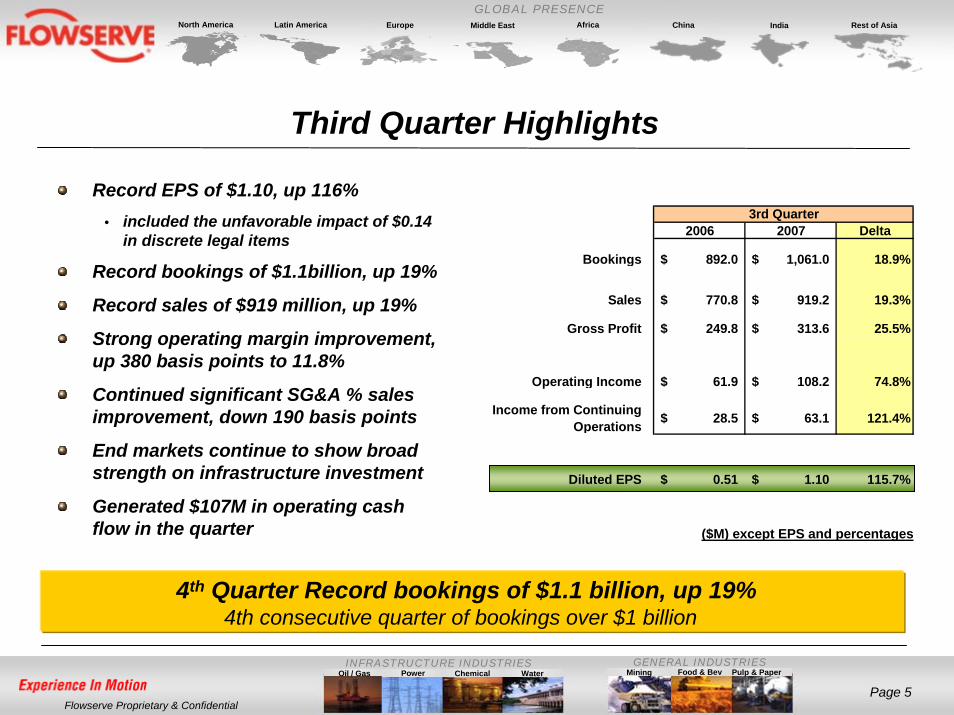

Third Quarter Highlights

* Please refer to the Company’s Q3 Press Release and 10-Q for more detailed information regarding the discrete legal items.

Record EPS of $1.10, up 116%• included the unfavorable impact of $0.14

in discrete legal items

Record bookings of $1.1billion, up 19%

Record sales of $919 million, up 19%

Strong operating margin improvement, up 380 basis points to 11.8%

Continued significant SG&A % sales improvement, down 190 basis points

End markets continue to show broad strength on infrastructure investment

Generated $107M in operating cash flow in the quarter

4th Quarter Record bookings of $1.1 billion, up 19%4th consecutive quarter of bookings over $1 billion

($M) except EPS and percentages

2006 2007 Delta

Bookings 892.0$ 1,061.0$ 18.9%

Sales 770.8$ 919.2$ 19.3%

Gross Profit 249.8$ 313.6$ 25.5%

Operating Income 61.9$ 108.2$ 74.8%

Income from Continuing Operations 28.5$ 63.1$ 121.4%

Diluted EPS 0.51$ 1.10$ 115.7%

3rd Quarter

Mining Pulp & PaperOil / Gas Power Chemical Water

Page 6Flowserve Proprietary & Confidential

INFRASTRUCTURE INDUSTRIES

North America Latin America Europe Middle East Africa China India Rest of Asia

GLOBAL PRESENCE

GENERAL INDUSTRIESFood & Bev

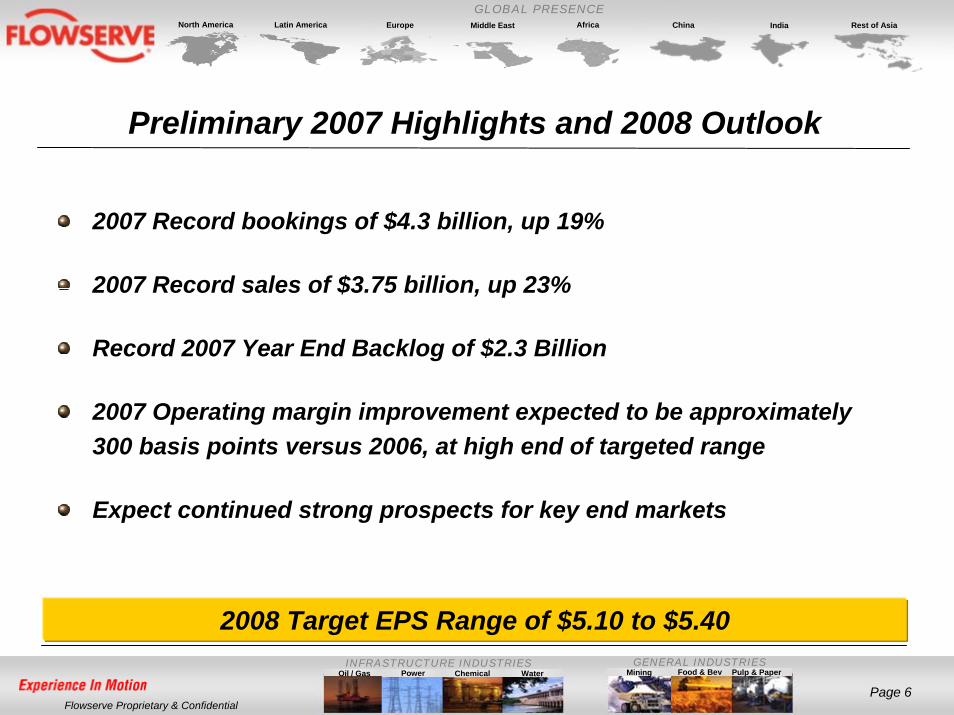

Preliminary 2007 Highlights and 2008 Outlook

2007 Record bookings of $4.3 billion, up 19%

2007 Record sales of $3.75 billion, up 23%

Record 2007 Year End Backlog of $2.3 Billion

2007 Operating margin improvement expected to be approximately 300 basis points versus 2006, at high end of targeted range

Expect continued strong prospects for key end markets

2008 Target EPS Range of $5.10 to $5.40

Mining Pulp & PaperOil / Gas Power Chemical Water

Page 7Flowserve Proprietary & Confidential

INFRASTRUCTURE INDUSTRIES

North America Latin America Europe Middle East Africa China India Rest of Asia

GLOBAL PRESENCE

GENERAL INDUSTRIESFood & Bev

$2,184$2,424 $2,520

$2,927

$3,617

$4,319

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,000

Strong Bookings Growth

19% Bookings Growth Supported by All Industries in 2007

2002 2003 2004 2005 2006 2007

*

* Excludes Discontinued Operations

($ millions)

*

Mining Pulp & PaperOil / Gas Power Chemical Water

Page 8Flowserve Proprietary & Confidential

INFRASTRUCTURE INDUSTRIES

North America Latin America Europe Middle East Africa China India Rest of Asia

GLOBAL PRESENCE

GENERAL INDUSTRIESFood & Bev

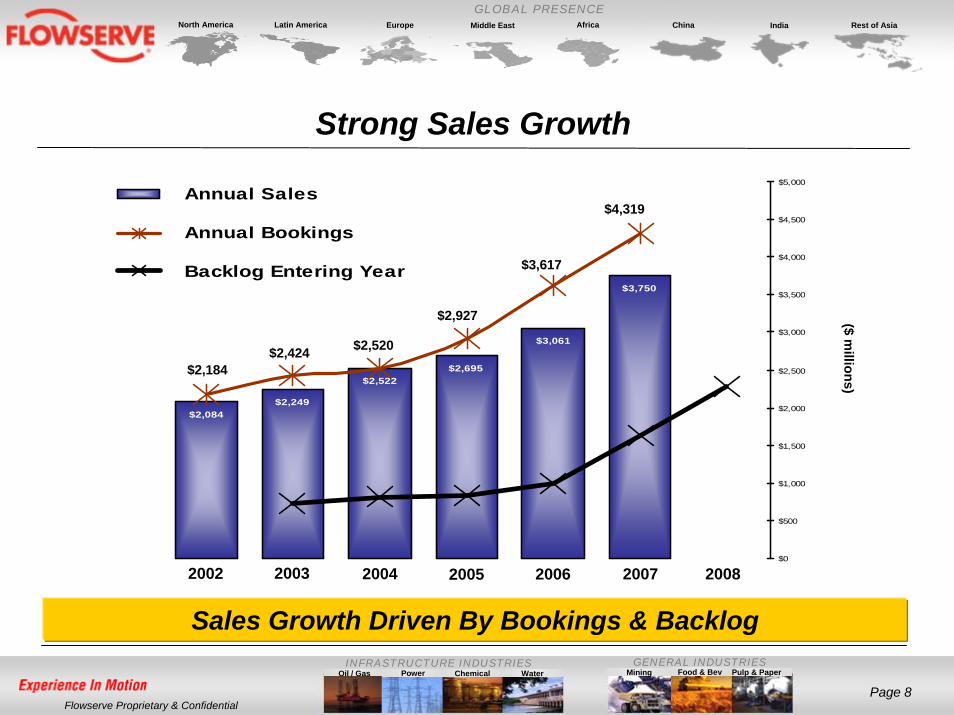

Strong Sales Growth

Sales Growth Driven By Bookings & Backlog

$2,084$2,249

$2,522$2,695

$3,061

$3,750

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,000

Annual Sales

Annual Bookings

Backlog Entering Year

($ millions)

2002 2003 2004 2005 2006 2007 2008

$2,184$2,424 $2,520

$2,927

$3,617

$4,319

Mining Pulp & PaperOil / Gas Power Chemical Water

Page 9Flowserve Proprietary & Confidential

INFRASTRUCTURE INDUSTRIES

North America Latin America Europe Middle East Africa China India Rest of Asia

GLOBAL PRESENCE

GENERAL INDUSTRIESFood & Bev

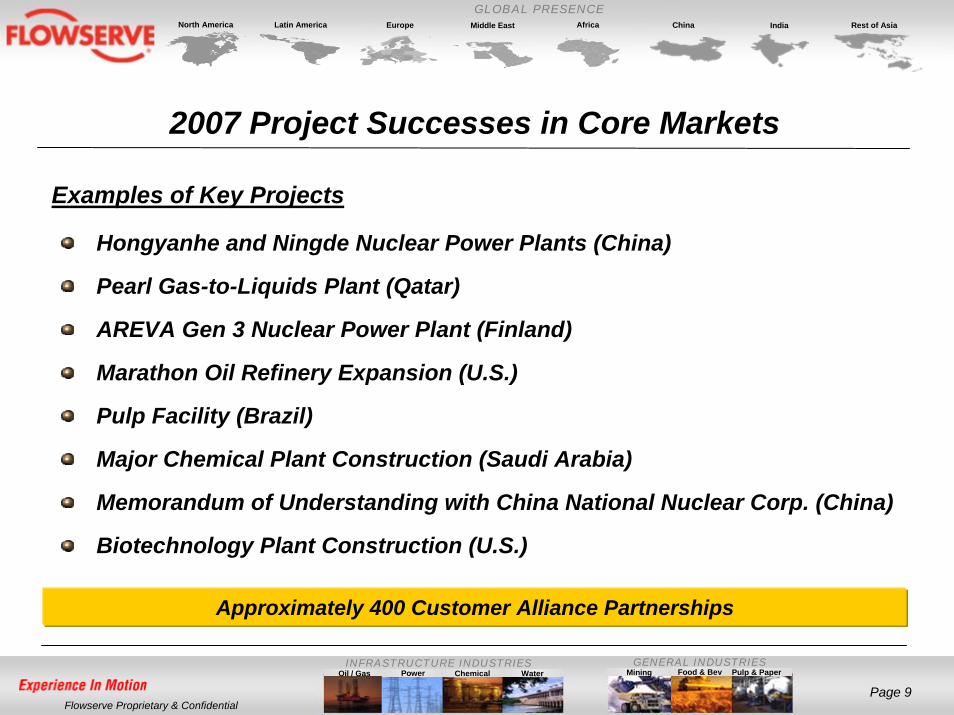

2007 Project Successes in Core Markets

Hongyanhe and Ningde Nuclear Power Plants (China)

Pearl Gas-to-Liquids Plant (Qatar)

AREVA Gen 3 Nuclear Power Plant (Finland)

Marathon Oil Refinery Expansion (U.S.)

Pulp Facility (Brazil)

Major Chemical Plant Construction (Saudi Arabia)

Memorandum of Understanding with China National Nuclear Corp. (China)

Biotechnology Plant Construction (U.S.)

Examples of Key Projects

Approximately 400 Customer Alliance Partnerships

Mining Pulp & PaperOil / Gas Power Chemical Water

Page 10Flowserve Proprietary & Confidential

INFRASTRUCTURE INDUSTRIES

North America Latin America Europe Middle East Africa China India Rest of Asia

GLOBAL PRESENCE

GENERAL INDUSTRIESFood & Bev

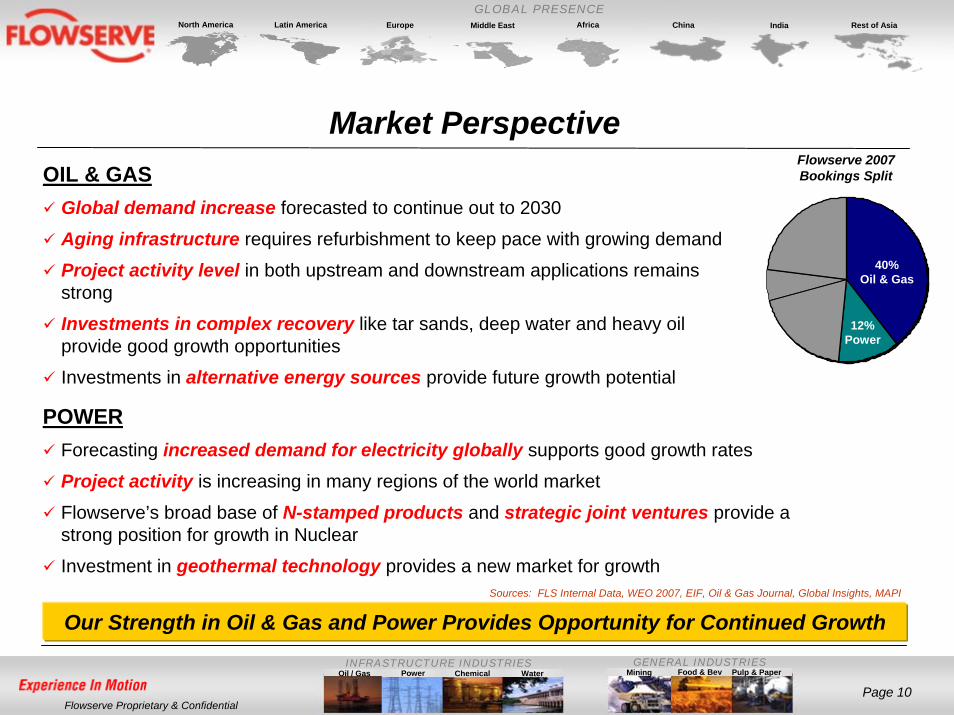

Market Perspective

Our Strength in Oil & Gas and Power Provides Opportunity for Continued Growth

POWERForecasting increased demand for electricity globally supports good growth rates

Project activity is increasing in many regions of the world market

Flowserve’s broad base of N-stamped products and strategic joint ventures provide a strong position for growth in Nuclear

Investment in geothermal technology provides a new market for growth

OIL & GASGlobal demand increase forecasted to continue out to 2030

Aging infrastructure requires refurbishment to keep pace with growing demand

Project activity level in both upstream and downstream applications remains strong

Investments in complex recovery like tar sands, deep water and heavy oil provide good growth opportunities

Investments in alternative energy sources provide future growth potential

Flowserve 2007 Bookings Split

Sources: FLS Internal Data, WEO 2007, EIF, Oil & Gas Journal, Global Insights, MAPI

40%Oil & Gas

12%Power

Mining Pulp & PaperOil / Gas Power Chemical Water

Page 11Flowserve Proprietary & Confidential

INFRASTRUCTURE INDUSTRIES

North America Latin America Europe Middle East Africa China India Rest of Asia

GLOBAL PRESENCE

GENERAL INDUSTRIESFood & Bev

Market Perspective

Project Win Rates Drive Strong Growth in These Important Markets

CHEMICAL & PHARMACEUTICALSForecasting capital investments in chemical remains positive

Many of our specialty products specifically designed for chemical helped fuel significant growth this year

Project activity is still strong - particularly in Asia

WATER Global demand for water is forecasted to provide consistent yearly investment growth

Flowserve investments in desalination continue to provide opportunities in this growing segment

The infrastructure demands in the developing parts of the world are increasing the need for large volume water transportation which Flowserve products serve well

40%

23%

6%

19%12%

Sources: FLS Internal Data, WEO 2007, EIF, Oil & Gas Journal, Global Insights, MAPI

Flowserve 2007 Bookings Split

19%Chemical

Water 6%

Mining Pulp & PaperOil / Gas Power Chemical Water

Page 12Flowserve Proprietary & Confidential

INFRASTRUCTURE INDUSTRIES

North America Latin America Europe Middle East Africa China India Rest of Asia

GLOBAL PRESENCE

GENERAL INDUSTRIESFood & Bev

Market Perspective

Flowserve Investments for Growth are Paying Dividends

GENERAL INDUSTRIES

The expansion of Flowserve’s capabilities in managing slurry materials is supporting good growth in the mining & ore processing industry

Flowserve’s line of specialty valves for the pulp & paper industry have strongly contributed to growth in this segment

Investment in district heating & cooling particularly in central Europe and Russia maintains a positive outlook

Investments in biotechnology programs (fuels and plastics), driven by government programs, provide good growth opportunities

Sources: FLS Internal Data, WEO 2007, EIF, Oil & Gas Journal, Global Insights, MAPI

Flowserve 2007 Bookings Split

23%General

Industries

Mining Pulp & PaperOil / Gas Power Chemical Water

Page 13Flowserve Proprietary & Confidential

INFRASTRUCTURE INDUSTRIES

North America Latin America Europe Middle East Africa China India Rest of Asia

GLOBAL PRESENCE

GENERAL INDUSTRIESFood & Bev

Continuing to Execute on Our StrategiesGrowth Objectives

Flowserve continues strong growth performance in Bookings, Revenue and Operating Profit

Earnings per Share performance demonstrates the effectiveness of our global footprint and strong employee commitment

Market OutlookThe future continues to look promising due to the investment growth in Chemical, Power and Water combined with the strength of the Oil & Gas sector

With our investments in globalizing our assets, Flowserve is well positioned to participate in and support the growth of developing markets around the world

Future FocusFlowserve will continue to strengthen its relationships with key customers to build and support long term business alliancesWe will continue investing to drive growth throughout our businesses and maintain our focus on on-time delivery and quality performanceWe will keep up our focus on driving improved financial performance by linking our leadership’s compensation to our results

Mining Pulp & PaperOil / Gas Power Chemical Water

Page 14Flowserve Proprietary & Confidential

INFRASTRUCTURE INDUSTRIES

North America Latin America Europe Middle East Africa China India Rest of Asia

GLOBAL PRESENCE

GENERAL INDUSTRIESFood & Bev

Corporate Social Responsibility (CSR)Flowserve supports our employees, our customersemployees, our customers and their communitiescommunities while playing a critical role playing a critical role in protecting the environmentin protecting the environment by providing products which meet the highest levels of emissions highest levels of emissions control.control.

• Environmental Protection• Energy Management• Chemical Usage and Controls

• Products Designed to Meet Industry Standards for Emissions Control

• Sustainable Product Lifecycle

• Process Optimization

• World Trade Organization Labor Standards

• Ethics and Compliance Focus

• Award Winning Safety Programs

• Supporting the Communities Where our Employees and Customers Live and Work

Flowserve is Positioned Well to Adhere to the Global Standards of the Future

Global TrendsIndexes

ISO StandardsIndustry Trends

Mining Pulp & PaperOil / Gas Power Chemical Water

Page 15Flowserve Proprietary & Confidential

INFRASTRUCTURE INDUSTRIES

North America Latin America Europe Middle East Africa China India Rest of Asia

GLOBAL PRESENCE

GENERAL INDUSTRIESFood & Bev

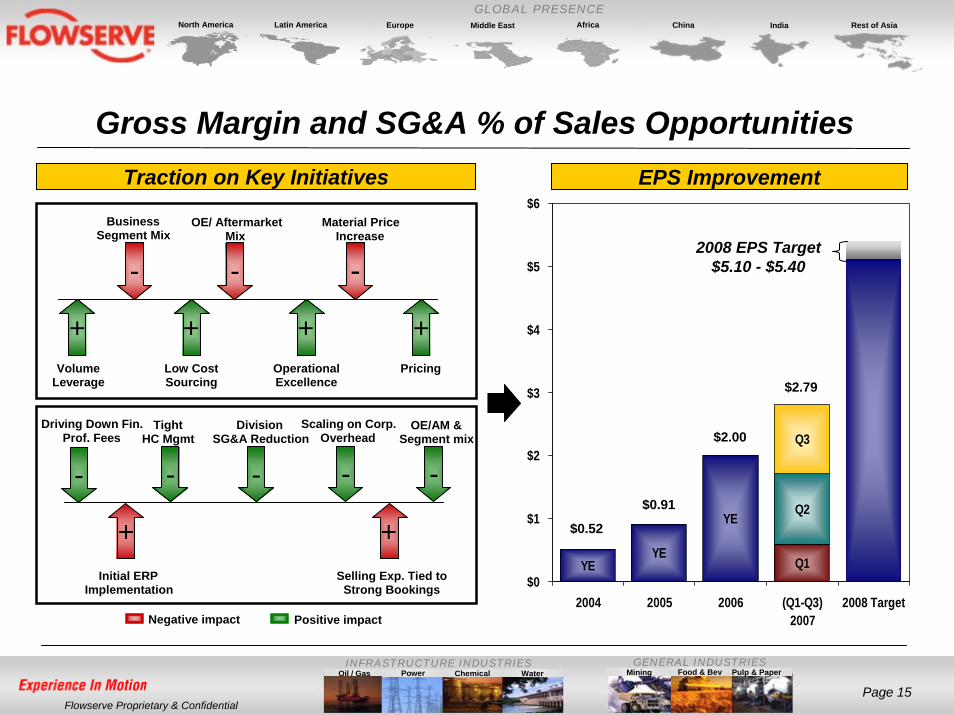

Gross Margin and SG&A % of Sales OpportunitiesTraction on Key Initiatives

-

+ + ++

Business Segment Mix

OE/ AftermarketMix

Material Price Increase

Volume Leverage

Low Cost Sourcing

Operational Excellence

Pricing

- -

Negative impact Positive impact

- -

++

Initial ERP Implementation

Selling Exp. Tied to Strong Bookings

Driving Down Fin. Prof. Fees

Tight HC Mgmt

-

OE/AM &Segment mix

Division SG&A Reduction

- -

Scaling on Corp. Overhead

YEYE

YE

Q1

Q2

Q3

$0

$1

$2

$3

$4

$5

$6

2004 2005 2006 (Q1-Q3)2007

2008 Target

2008 EPS Target$5.10 - $5.40

$0.52

$0.91

$2.00

$2.79

EPS Improvement

Mining Pulp & PaperOil / Gas Power Chemical Water

Page 16Flowserve Proprietary & Confidential

INFRASTRUCTURE INDUSTRIES

North America Latin America Europe Middle East Africa China India Rest of Asia

GLOBAL PRESENCE

GENERAL INDUSTRIESFood & Bev

Questions and Answers