flying on demand - airbus · global market forecast 2014- 2033 . bob lange . head of market and...

TRANSCRIPT

© AIRBUS all rights reserved. Confidential and proprietary document. © AIRBUS all rights reserved. Confidential and proprietary document.

Flying on Demand Deutsche Bank Toulouse, 22nd January 2015

Global Market Forecast 2014-2033

Bob Lange Head of Market and Product Strategy

© AIRBUS all rights reserved. Confidential and proprietary document.

Aviation’s benefit -

23 minutes

2 hours

4 – 12 hours

20 hours

The first commercial flight was 100 years ago

© AIRBUS all rights reserved. Confidential and proprietary document.

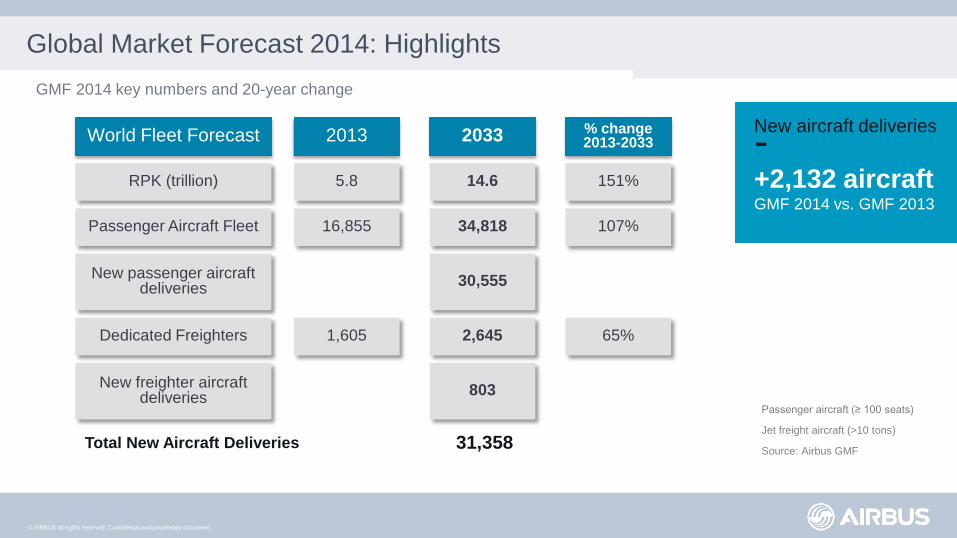

Global Market Forecast 2014: Highlights GMF 2014 key numbers and 20-year change

World Fleet Forecast 2013 2033 % change 2013-2033

RPK (trillion) 5.8 14.6 151%

Passenger Aircraft Fleet 16,855 34,818 107%

New passenger aircraft deliveries 30,555

Dedicated Freighters 1,605 2,645 65%

New freighter aircraft deliveries 803

Passenger aircraft (≥ 100 seats)

Jet freight aircraft (>10 tons)

Source: Airbus GMF

New aircraft deliveries - +2,132 aircraft GMF 2014 vs. GMF 2013

Total New Aircraft Deliveries 31,358

© AIRBUS all rights reserved. Confidential and proprietary document.

20-year demand for 31,358 new passenger and freight aircraft

Passenger aircraft (≥ 100 seats)

Jet freight aircraft (>10 tons)

Source: Airbus GMF

20-year new deliveries of passenger and freight aircraft

Market Value of - $4.6 trillion

22,071 single-aisle aircraft

7,786 twin-aisle aircraft

1,501 very large aircraft

31,358 new aircraft

© AIRBUS all rights reserved. Confidential and proprietary document.

Single-aisle: 70% of units; Wide-bodies: 55% of value

Passenger aircraft (≥ 100 seats) and jet freight aircraft (>10 tons)

Source: Airbus

31,400 New Deliveries GMF 2014 -2033

0

4,000

8,000

12,000

16,000

20,000

24,000

Single-aisle Twin-aisle Very Large Aircraft

1,500

7,800

22,100

70% 25% 5% % units

45% 44% 11% % value

20-year new deliveries of passenger and freighter aircraft

© AIRBUS all rights reserved. Confidential and proprietary document.

0

5

10

15

20

25

1980 1985 1990 1995 2000 2005 2010

Inflation-adjusted average yields have stabilised

Cents per RPK in 2013 US$

Source: ICAO, IATA, Airbus

Fairly stable

© AIRBUS all rights reserved. Confidential and proprietary document.

More movements, more connectivity….

Source: OAG, Airbus

Airport movements Airport connectivity

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010 2013

Avg. number of movements per airport Avg. number of destinations per airport

0

2

4

6

8

10

12

14

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010 2013

x2.4 x1.8

© AIRBUS all rights reserved. Confidential and proprietary document.

More seats per aircraft, and more of them filled

Source: OAG, Ascend, Airbus

Offered seats per aircraft

0

50

100

150

200

250

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010 2013

Avg. number of offered seats per aircraft (000)

50%

55%

60%

65%

70%

75%

80%

85%

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010 2013

World passenger load factors (%)

Source: ICAO, OAG, Airbus

Load factors

+17.4 percentage

points

© AIRBUS all rights reserved. Confidential and proprietary document.

Less fuel burn, therefore less emissions…

Source: ICAO, IATA, Airbus

Fuel consumption CO2 emissions

0

20

40

60

80

100

120

2000 2002 2004 2006 2008 2010 2012

Kilograms per passenger per trip (avg.) Kilograms per passenger per trip (avg.)

0

50

100

150

200

250

300

350

2000 2002 2004 2006 2008 2010 2012

-31% -31%

© AIRBUS all rights reserved. Confidential and proprietary document.

0

20

40

60

80

100

120

140

160

180

200

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

Jan 2015 forecast

Jan 2014 forecast

Short term oil forecast revised down; high oil price consensus over long term

Source: IHS Energy, Airbus

Forecast History

Brent oil price (US$ per bbl.)

© AIRBUS all rights reserved. Confidential and proprietary document.

Aircraft orders are correlated to airlines profitability

Source: Airbus, ICAO

Airlines results & net orders

0

500

1,000

1,500

2,000

2,500

3,000

3,500

-6%

-4%

-2%

0%

2%

4%

6%

8%

1990 1995 2000 2005 2010

Operating marginNet Orders

Operating margin (%) Units

© AIRBUS all rights reserved. Confidential and proprietary document.

Deliveries are much less volatile

Source: Airbus, ICAO

Airlines results & net orders

0

500

1,000

1,500

2,000

2,500

3,000

3,500

-6%

-4%

-2%

0%

2%

4%

6%

8%

1990 1995 2000 2005 2010

Operating marginDeliveriesNet Orders

Operating margin (%) Units

© AIRBUS all rights reserved. Confidential and proprietary document.

Oil Crisis Oil Crisis Gulf Crisis AsianCrisis 9/11 SARS Financial

Crisis

Air travel has proven to be resilient to external shocks

Source: ICAO, Airbus

World traffic - 73% growth through multiple crises over the last ten years

World annual traffic (RPKs - trillions)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1968 1973 1978 1983 1988 1993 1998 2003 2008 2013

© AIRBUS all rights reserved. Confidential and proprietary document.

-4%

-2%

0%

2%

4%

6%

8%

J M M J S N J M M J S N J M M J S N J M M J S N J M M J S N J M M J S N J M M J S N-4%

-2%

0%

2%

4%

6%

8%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

World real GDPWorld passenger traffic (ASKs)

Passenger traffic is outperforming GDP growth

% (year-over-year)

2008 2009 2010 2011 2012 2013 2014

World real GDP and passenger traffic

Source: IHS Global Insight, Airbus

+5.3%

December 2014 Passenger Traffic

© AIRBUS all rights reserved. Confidential and proprietary document.

A two-speed economic world

* 54 emerging economies

** 32 advanced economies

Source: IHS Global Insight, Airbus

Comparison of year-over-year GDP growth

-4%

-2%

0%

2%

4%

6%

8%

10%

1982 1986 1990 1994 1998 2002 2006 2010 2014 2018

Emerging economies*

Real GDP growth (%) History Forecast Emerging economies will continue to lead the pack

Advanced economies**

© AIRBUS all rights reserved. Confidential and proprietary document.

The World of 2033 will be very different from today

1- US 2- China 3- Japan 4- Germany 5- France 6- UK 7- Brazil 8- Russia 9- Italy 10- India

Source: IHS Global Insight, Airbus

1- China 2- US 3- India 4- Japan 5- Germany 6- UK 7- France 8- Brazil 9- Russia 10- Italy

1- China 2- US 3- India 4- Japan 5- Brazil 6- Germany 7- UK 8- Russia 9- France 10- Indonesia

GDP ranking based on nominal GDP expressed in US$

2013 2023 2033

© AIRBUS all rights reserved. Confidential and proprietary document.

+2.5% US Traffic

Asia-Pacific and other emerging markets are leading traffic growth

+6.5% Asia - Pacific Traffic

+2.6% Western Europe Traffic

% (year-over-year)

+9.4% Emerging Markets Traffic

ASKs year-over-year monthly evolution

2009 2010 2011 2012 2013 2014 Source: OAG, Airbus

-12%

-8%

-4%

0%

4%

8%

12%

16%

J M M J S N J M M J S N J M M J S N J M M J S N J M M J S N J M M J S N

© AIRBUS all rights reserved. Confidential and proprietary document.

In-service fleet

Emerging economies are driving future growth

Source: IHS Global Insight, Airbus

* Nominal GDP in US$

Emerging economies (54 countries) All other countries (150 countries)

38%

50% 54%

36%

GDP

59%

42%

Passengers trips

2033

Today

Population

69%

67%

© AIRBUS all rights reserved. Confidential and proprietary document.

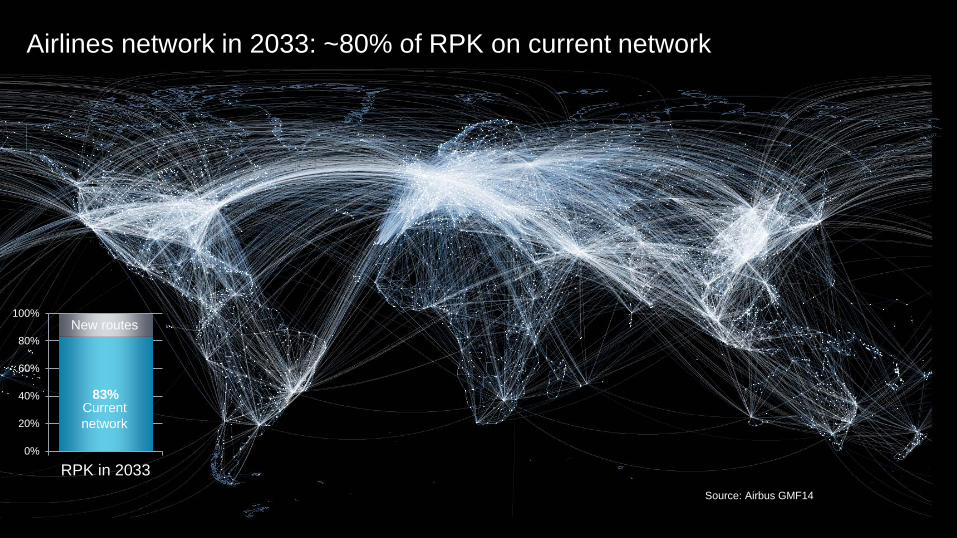

Airlines network in 2033: ~80% of RPK on current network

83%

0%

20%

40%

60%

80%

100%

RPK in 2033

Current network

New routes

Source: Airbus GMF14

© AIRBUS all rights reserved. Confidential and proprietary document. September 14

Emerging regions will account for the largest share of origin and destination traffic worldwide

Source: ICAO, Sabre GDD, Airbus GMF

0

2

4

6

8

10

12

14

16

2003 2005 2007 2009 2011 2013 2015 2017 2019 2021 2023 2025 2027 2029 2031 2033

World annual RPK (trillion)

2.6% p.a. Advanced – Advanced

5.0% p.a. Emerging – Advanced

6.8% p.a. Emerging – Emerging

Airbus GMF 2014

ICAO total traffic

© AIRBUS all rights reserved. Confidential and proprietary document.

Air transport growth is highest in expanding regions

Billions of people will increasingly want to travel by air

China India Middle East Asia Africa CIS Latin America Eastern Europe

Western Europe North America Japan

Yearly RPK growth 2014 - 2033

1 billion

people 2014

6.2 billion

people 2014

Em

ergi

ng/D

evel

opin

g A

dvan

ced

+6.0 %

+4.2 %

© AIRBUS all rights reserved. Confidential and proprietary document.

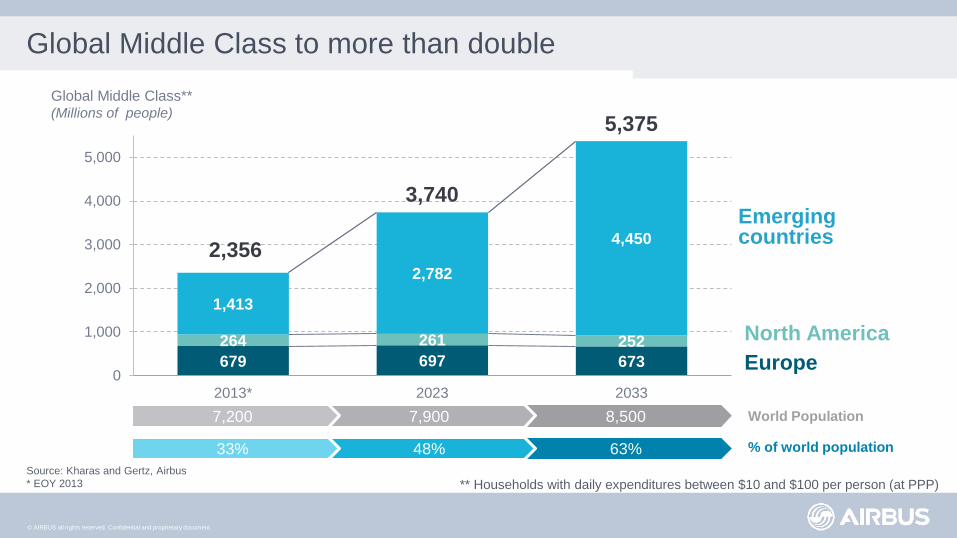

Global Middle Class to more than double

679 697 673 264 261 252

1,413

2,782

4,450

0

1,000

2,000

3,000

4,000

5,000

2013* 2023 2033

Global Middle Class** (Millions of people)

Emerging countries

World Population

% of world population

8,500

63%

7,900

48%

7,200

33% Source: Kharas and Gertz, Airbus * EOY 2013 ** Households with daily expenditures between $10 and $100 per person (at PPP)

3,740

2,356

5,375

North America Europe

© AIRBUS all rights reserved. Confidential and proprietary document.

0.01

0.10

1.00

10.00

0 20 40 60 80

Page 23

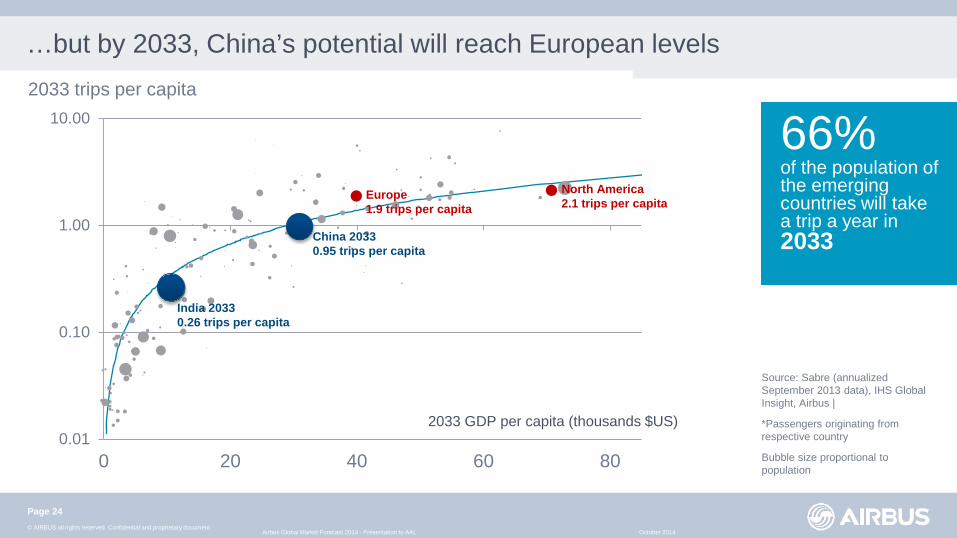

North Americans and Europeans are the most willing to fly

2/3 of the population of the emerging countries will take a trip a year in 2033

2013 trips per capita

2013 GDP per capita (thousands $US)

Europe ~1 trip per capita

India 2013 0.06 trips per capita

China 2013 0.25 trips per capita

October 2014 Airbus Global Market Forecast 2014 - Presentation to AAL

Source: Sabre (annualized September 2013 data), IHS Global Insight, Airbus |

*Passengers originating from respective country

Bubble size proportional to population

North America 1.6 trips per capita

© AIRBUS all rights reserved. Confidential and proprietary document.

0.01

0.10

1.00

10.00

0 20 40 60 80

…but by 2033, China’s potential will reach European levels

Source: Sabre (annualized September 2013 data), IHS Global Insight, Airbus |

*Passengers originating from respective country

Bubble size proportional to population

66% of the population of the emerging countries will take a trip a year in 2033

2033 trips per capita

2033 GDP per capita (thousands $US)

India 2033 0.26 trips per capita

China 2033 0.95 trips per capita

Page 24

October 2014 Airbus Global Market Forecast 2014 - Presentation to AAL

North America 2.1 trips per capita

Europe 1.9 trips per capita

© AIRBUS all rights reserved. Confidential and proprietary document.

Long-haul traffic grows stronger than short haul traffic

Source: OAG

* Long haul traffic: flight distance >2,000nm

Evolution of long-haul vs short-haul traffic (ASKs), 1973-2013, (Base 100 in 1973)

0

100

200

300

400

500

600

700

800

900

1000

1973 1978 1983 1988 1993 1998 2003 2008 2013

Long-haul traffic has grown 1% p.a. faster than short-haul

x6.2

Short-haul traffic

x9.1

Long-haul traffic

© AIRBUS all rights reserved. Confidential and proprietary document.

Long-haul traffic consolidation

Source: OAG, Airbus

* Long haul traffic: flight distance >2,000nm

Evolution of traffic per long-haul airline (ASKs), 1973-2013, (Base 100 in 1973)

ASK per airline have nearly quadrupled since 1973

0

50

100

150

200

250

300

350

400

1973 1978 1983 1988 1993 1998 2003 2008 2013

ASKs per Airline

Number of Airlines

© AIRBUS all rights reserved. Confidential and proprietary document.

Urbanisation to increase

49%

60%

67%

0%

10%

20%

30%

40%

50%

60%

70%

80%

-

1

2

3

4

5

6

7

8

9

10

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

RuralUrbanUrban share

billion History Forecast

Urban population: 1.3bn 2.3bn 3.5bn 5.0bn 6.4bn

World population and share of urban agglomeration evolution

Source: UN population division, Airbus

© AIRBUS all rights reserved. Confidential and proprietary document.

42 Aviation Mega-Cities in 2013

• >50 000 daily long-haul passengers

• >20 000 daily long-haul passengers

• >10 000 daily long-haul passengers

2013 Aviation Mega-Cities

42 Aviation

Mega-cities

Source: McKinsey, UNPD, Airbus GMF

0.8M Daily Passengers: Long Haul traffic to/ from/via Mega

Cities

90%+ of long-haul

traffic on routes to/from/via 42 cities

22% of World

GDP in 2013

© AIRBUS all rights reserved. Confidential and proprietary document.

… and 91 Mega-Cities by 2033

• >50 000 daily long-haul passengers

• >20 000 daily long-haul passengers

• >10 000 daily long-haul passengers

2033 Aviation Mega-Cities

Source: McKinsey, UNPD, Airbus GMF

91 Aviation

Mega-cities

2.2M Daily Passengers: Long Haul traffic to/ from/via Mega

Cities

95%+ of long-haul

traffic on routes to/from/via 91 cities

35% of World

GDP in 2013

© AIRBUS all rights reserved. Confidential and proprietary document.

The bigger the city, the wealthier the population 2013 Aviation Mega-Cities and 2013 GDP per capita (real 2010 $US, thousands)

0

20

40

60

AMC Otherlargecities

Region

North America (12 AMC)

05

10152025

AMC Otherlargecities

Region 0

5

10

15

AMC Otherlargecities

Region

0

20

40

60

AMC Otherlargecities

Region 010203040

AMC Otherlargecities

Region

0

10

20

30

AMC Otherlargecities

Region

010203040

AMC Otherlargecities

Region

Latin America (2 AMC)

Europe (9 AMC)

Africa (1 AMC)

Middle East (4 AMC)

CIS (1 AMC)

Asia-Pacific (13 AMC)

GDP per capita in Aviation Mega-Cities

4x World average

Source: McKinsey, UNPD, IHS Global Insight, Airbus GMF

Other large cities: urban agglomerations with a population above 300,000 people

© AIRBUS all rights reserved. Confidential and proprietary document.

0%

2%

4%

6%

8%

10%

12%

14%

Aviation Mega-City to AviationMega-City

Aviation Mega-City <>Secondary City

Secondary City to SecondaryCity

Routes between Aviation Mega-Cities carry a greater share of premium passengers

Percentage of premium passengers on route types Based on 2012 Aviation Mega-Cities

Source: SABRE, Airbus Market Research and Forecasts| Cities with more than 10,000 daily passengers, Long-haul traffic: flight distance >2,000nm, excl. domestic traffic

13% of passengers betwwen AMCs are Premium customers

© AIRBUS all rights reserved. Confidential and proprietary document.

Airbus Global Market Forecast

A 20 year aircraft demand and passenger traffic forecast

Airlines • Business Models • Operations • Competition • Geopolitics

Trends Analysis • Consumer & Travel

Surveys • Tourism • Migration • Traffic flows • Passenger demands

Governments & Regulators

• Liberalization/ deregulation • Investments and

constraints • Geopolitics

Market Research

Network Development • Route planning • Origin and destination

demand • Population centers

Traffic • Economics and

Econometrics • Fuel costs • Yields • Load Factors • Trade and Value of Goods

Fleet trends • Aircraft economics • Utilization • Fleet age and retirements

Forecast

© AIRBUS all rights reserved. Confidential and proprietary document.

Around 800 airlines and their subsidiaries are analysed…

80

44 40 36

92

119

23

43 34

46

18

68

98

58

0

20

40

60

80

100

120

140

Airlines distribution per region

Number of airlines

48%

19%

5%

17%

3% 8%

4% 9%

20%

6% 16%

45%

Global Network Major Network

Small Network LCC

Regional & Affiliate Charter

Installed seats in service (outside circle) Number of airlines (inside circle)

Airlines distribution per type

© AIRBUS all rights reserved. Confidential and proprietary document.

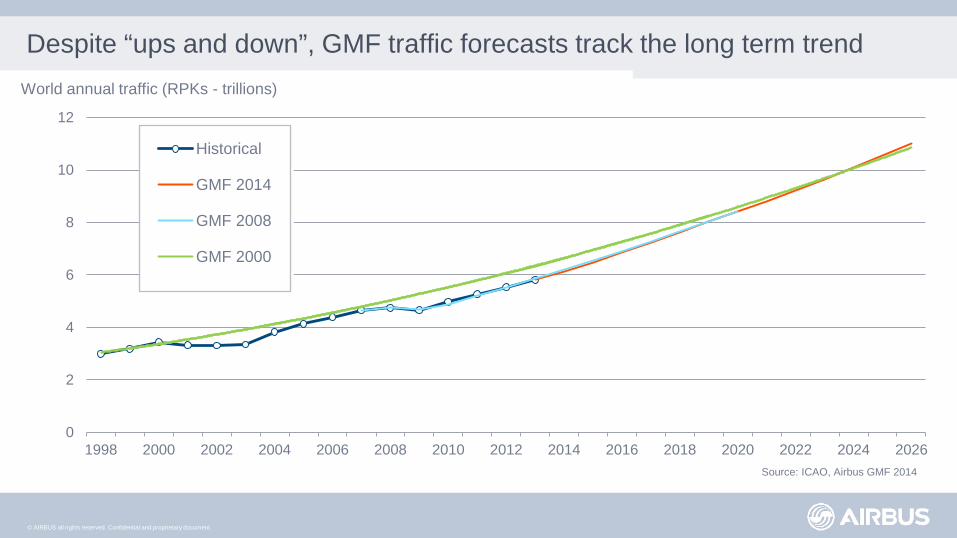

Despite “ups and down”, GMF traffic forecasts track the long term trend

0

2

4

6

8

10

12

1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024 2026

Historical

GMF 2014

GMF 2008

GMF 2000

World annual traffic (RPKs - trillions)

Source: ICAO, Airbus GMF 2014

© AIRBUS all rights reserved. Confidential and proprietary document.

Air traffic will double in the next 15 years

Source: ICAO, Airbus GMF 2014

0

2

4

6

8

10

12

14

16

1973 1978 1983 1988 1993 1998 2003 2008 2013 2018 2023 2028 2033

World annual RPK* (trillion) Airbus GMF 2014

ICAO total traffic

4.7%

2013-2033

© AIRBUS all rights reserved. Confidential and proprietary document.

Domestic PRC to become number one within 10 years

* 20-year annual growth rate (CAGR) Source: Airbus GMF

- 500 1,000 1,500 2,000

Sub Sahara Africa - Western EuropeAsia Advanced - Asia Emerging

Asia Emerging - Middle EastIndian Sub-Continent - USA

Central Europe - Western EuropeAsia Emerging - PRCSouth America - USA

Western Europe - South AmericaPRC - USA

Western Europe - PRCDomestic Brazil

Western Europe - Middle EastIndian Sub-Continent - Middle East

Domestic IndiaAsia Emerging - Western Europe

Domestic Asia EmergingWestern Europe - USA

Intra Western EuropeDomestic USADomestic PRC

Billion RPKs 20-year annual growth* 7.1% 1.9% 2.9% 2.9% 6.9% 4.0% 9.5% 6.8% 4.6% 6.0% 5.6% 6.6% 4.3% 5.3% 7.5% 5.4% 6.4% 6.8% 5.6% 4.3%

© AIRBUS all rights reserved. Confidential and proprietary document.

Asia-Pacific to lead in world traffic by 2033

Source: Airbus GMF 2014

RPK traffic by airline domicile (billions)

0 1,000 2,000 3,000 4,000 5,000

Asia-Pacific

Europe

North America

Middle East

Latin America

CIS

Africa

30%

25%

24%

8%

5%

4%

3%

5.7%

3.6%

2.9%

7.1%

5.4%

5.4%

4.7%

% of 2013 world RPK

20-year growth

36%

20%

17%

13%

6%

5%

3%

% of 2033 world RPK

2013 traffic 2014-2033 traffic

20-year world annual traffic growth

4.7%

© AIRBUS all rights reserved. Confidential and proprietary document.

31,400 New

aircraft

6,100

12,400

19,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Beginning 2014 2033

Demand for around 31,400 new aircraft

Stay in service

Replacement

Growth

Source: Airbus

Note: Passenger aircraft ≥100 seats, Freighter aircraft ≥10 tonnes

Fleet in service evolution; 2014-2033

18,500

37,500

© AIRBUS all rights reserved. Confidential and proprietary document.

Airbus order backlog by region vs. 20 year market forecast

At end December 2014. Values are rounded.

Does not include orders from undisclosed customers

North America 12%

Latin America

5%

Europe & CIS 17% Middle

East 7%

Africa

1% Asia

Pacific 27%

Lessors

20%

Backlog - 6,386 aircraft worth over $850 billion

© AIRBUS all rights reserved. Confidential and proprietary document.

Backlog today extends 3 to 4 years further in time than before

Share of backlog delivered/scheduled to be delivered

0%

20%

40%

60%

80%

100%

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

1993

2003

2013

Delivery lead time

Backlog today - 40% of the backlog is for delivery beyond 5 years In 2003, this value was 5%

Aircraft above 100 seats

Source: Airbus analysis from ASCEND database

© AIRBUS all rights reserved. Confidential and proprietary document.

Each year, deliveries represent on average 7% of the in service fleet

Source: Airbus analysis from ASCEND database

Aircraft >= 100 seats

Yearly deliveries of aircraft above 100 seats

0%

2%

4%

6%

8%

10%

12%

0

200

400

600

800

1,000

1,200

1,400

1981 1984 1987 1990 1993 1996 1999 2002 2005 2008 2011 2014

Deliveries as % of fleet Deliveries - Estimated ratio for 2015-2018 deliveries is 7.6% of the in-service fleet

© AIRBUS all rights reserved. Confidential and proprietary document.

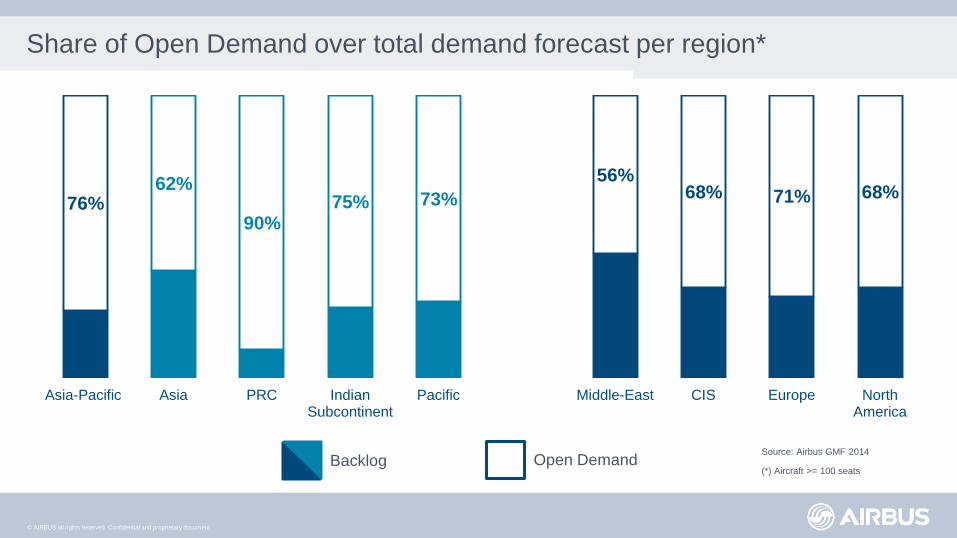

Share of Open Demand over total demand forecast per region*

Source: Airbus GMF 2014

(*) Aircraft >= 100 seats Open Demand Backlog

76% 62%

90% 75% 73%

56% 68% 71% 68%

Asia-Pacific Asia PRC IndianSubcontinent

Pacific Middle-East CIS Europe NorthAmerica

© AIRBUS all rights reserved. Confidential and proprietary document.

Summary

• Strong growth in passenger traffic – resilient growth through a difficult, but improving economic period

• Demand for 31,400 new aircraft by 2033 – ~30,600 passenger aircraft and nearly 800

freighter aircraft

• Replacement of ageing fleets – 20 year demand for 12,400 passenger aircraft for replacement, largely in the single-aisle segment

• Single-aisle aircraft represent 70% of demand in units, but wide-body aircraft represent 55% of value

• VLA demand driven by aviation mega-cities – more than 95%+ of all long-haul passengers will fly to, from or through 91 aviation mega-cities by 2033

© AIRBUS all rights reserved. Confidential and proprietary document.