focused assessment audits & role of broker in enforcement proceedings michael e. roll pisani...

TRANSCRIPT

Focused Assessment Audits Focused Assessment Audits & Role of Broker in & Role of Broker in

Enforcement ProceedingsEnforcement Proceedings

Michael E. RollPisani & Roll PLLC1875 Century Park East, Suite 600Los Angeles, CA 90067Tel 1.310.826.4410Fax 1.877.674.5789mroll@worldtradelawyers.comwww.worldtradelawyers.com

Texas Brokers &Forwarders AnnualConference El Paso, Texas September 25, 2008

FOCUSED ASSESSMENT AUDITS

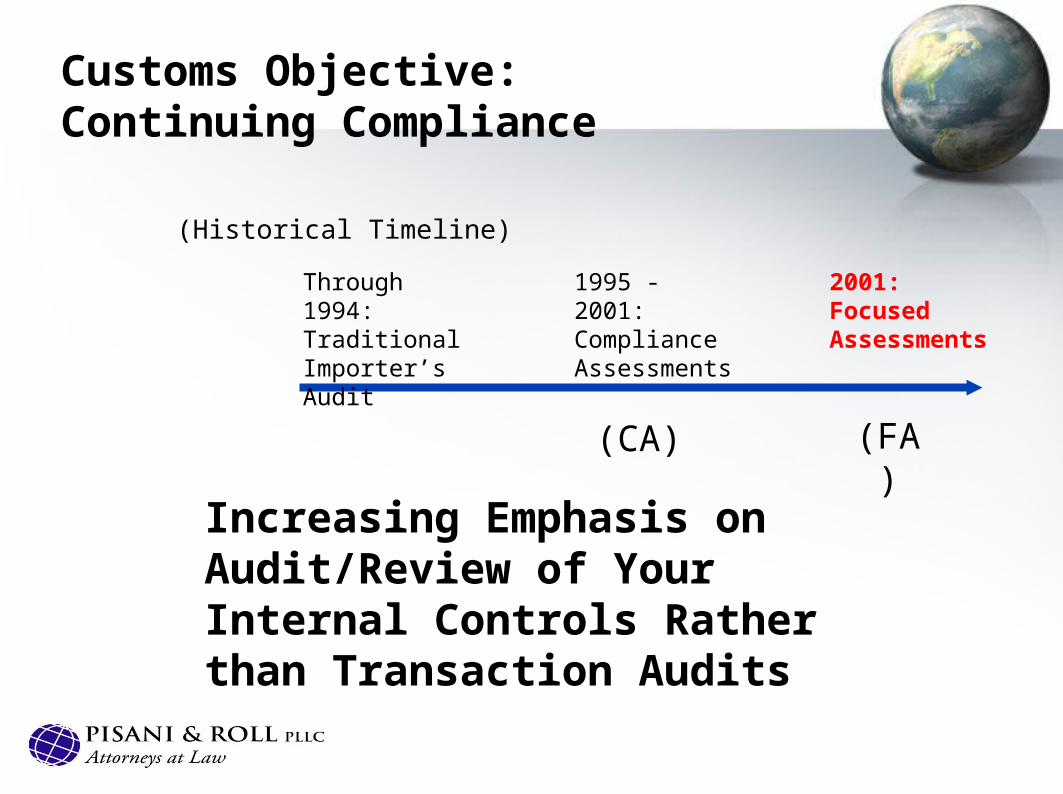

2001: Focused Assessments

Customs Objective:Continuing Compliance

1995 - 2001: Compliance Assessments

Increasing Emphasis on Audit/Review of Your Internal Controls Rather than Transaction Audits

Through 1994: Traditional Importer’s Audit

(CA) (FA)

(Historical Timeline)

Why the Heightened Emphasis on Internal Controls?

• Study of 426 Compliance Assessments (October 1995 – March 2001)

What is an Internal Control?

• A continuous built-in process

• That provides reasonable assurance

• And is affected by people

Why have Internal Controls?

• Internal controls achieve:– Effectiveness and efficiency of

operations

– Compliance with laws and regulations

– Reliability of data

What is an Internal Control System?

• Control environment

• Risk assessment

• Control activities

• Information and communication

• Monitoring

Customs’ Conclusions from Study

• Internal controls are a good predictor of actual compliance

• Importers with adequate internal controls had minimal non-compliance and loss of revenue (Average Revenue Recovery: $45,402)

• Importers without adequate internal controls had significant non-compliance and revenue losses (Average Revenue Recovery: $428,227!)

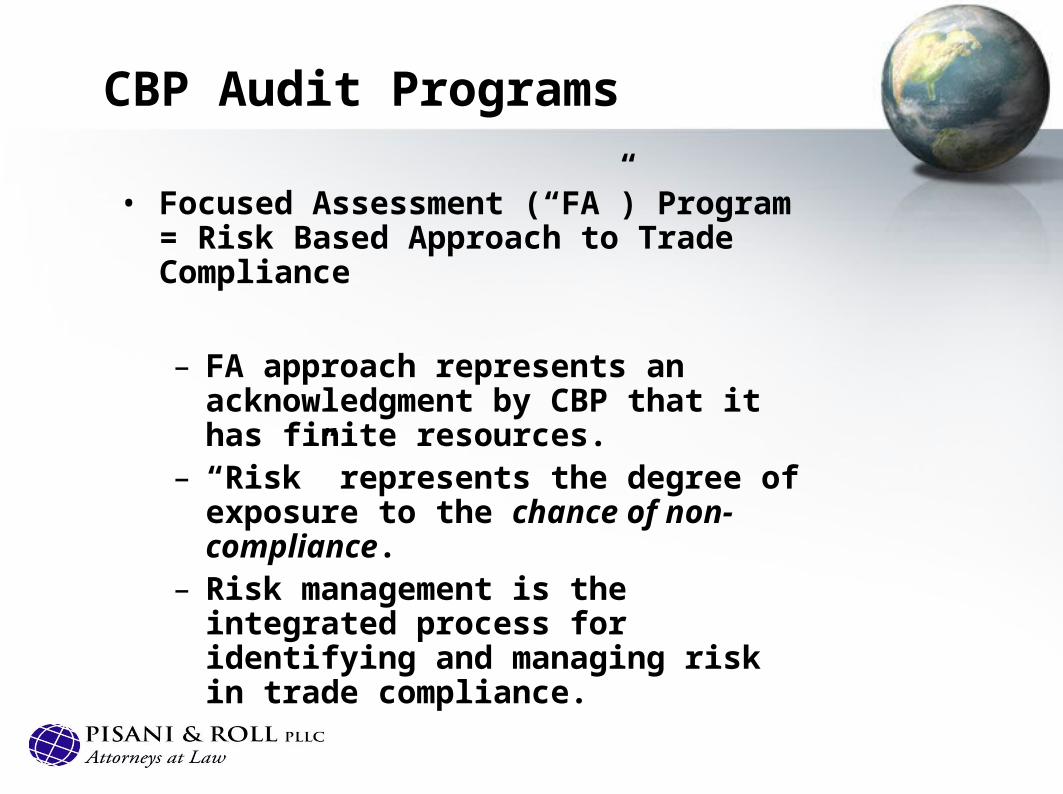

CBP Audit Programs

• Focused Assessment (“FA”) Program = Risk Based Approach to Trade Compliance

– FA approach represents an acknowledgment by CBP that it has finite resources.

– “Risk” represents the degree of exposure to the chance of non-compliance.

– Risk management is the integrated process for identifying and managing risk in trade compliance.

Focused Assessment Key Elements

• Starts with Internal Controls (System & Processes)– Good Internal Controls = Less Risk for

Customs– Internal controls should be documented

• Evaluates Controls to:– Identify System Strengths & Weaknesses– Help Predict Future Compliance

• COMPANY OFFICIALS ARE INTERVIEWED• Results in Risk Assessment• Company Gets Blueprint for Future Compliance

FA Auditee Selection Process

• Based on Risk Factors– Duty liability/Special Duty Provisions– Annual Entered Value– Significance/sensitivity of import issues– Compliance Measurement rate for

HTSUS/Industry/Company– Prior History with Regulatory Audit Division

(OST Data)• Primary Focus Industry (PFI) – no longer relevant

as selection criteria• Top 9,000 Importers• Some Random Selection

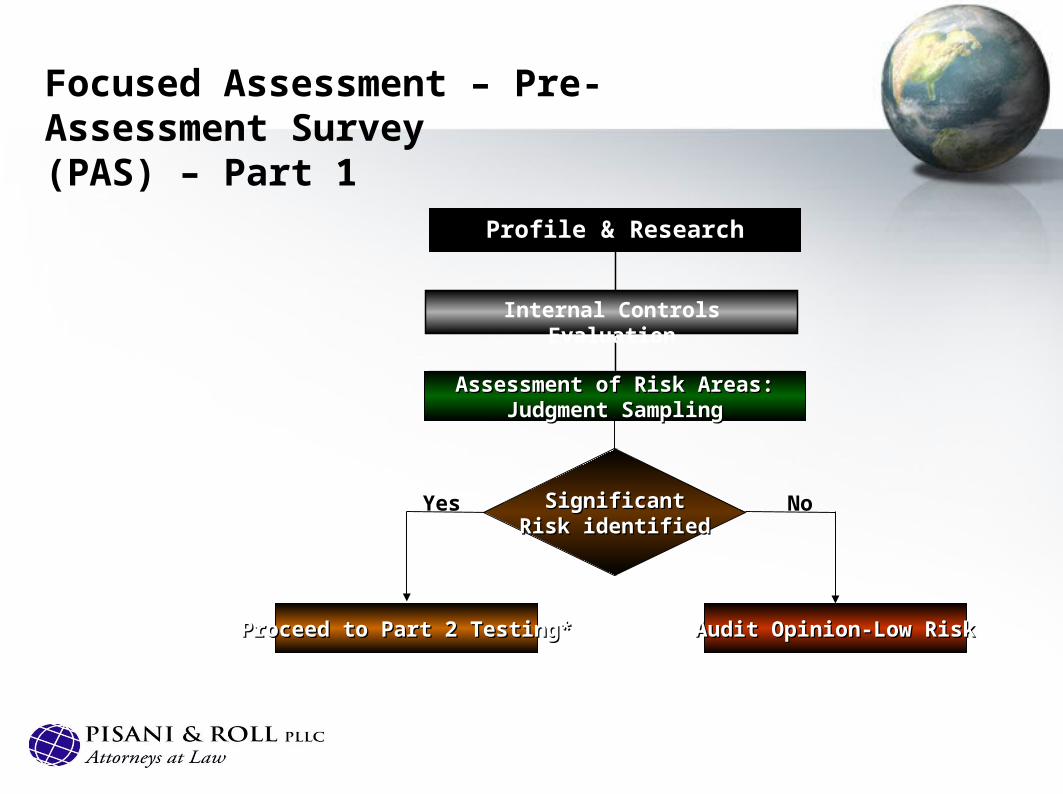

Proceed to Part 2 Testing*Proceed to Part 2 Testing* Audit Opinion-Low RiskAudit Opinion-Low Risk

NoYes SignificantSignificantRisk identifiedRisk identified

Internal Controls Evaluation

Profile & ResearchProfile & Research

Assessment of Risk Areas:Assessment of Risk Areas:Judgment SamplingJudgment Sampling

Focused Assessment – Pre-Assessment Survey(PAS) – Part 1

ClassificationClassification

AppraisementAppraisement

98029802ADD/CVDADD/CVDValueValue

GSPGSP

TransshipmentTransshipment

Identified Area(s)Identified Area(s)of Riskof Risk

Internal ControlInternal ControlAssessmentAssessment

FA - Pre-assessment Survey (PAS)

Internal Control Review & Testing of Controls

Evaluating Results• The results of the judgment sample testing are put in

perspective and weakness are evaluated as a whole. A decision at this point is made whether or not to proceed to Part II, the Assessment Compliance Testing (ACT) phase.

• Proceed to ACT– Inadequate internal controls– Material systemic error– No Agreement on Compliance Improvement Plan

(CIP)• Do not proceed to ACT

– Adequate internal controls– Non-systemic errors– Agreement on CIP

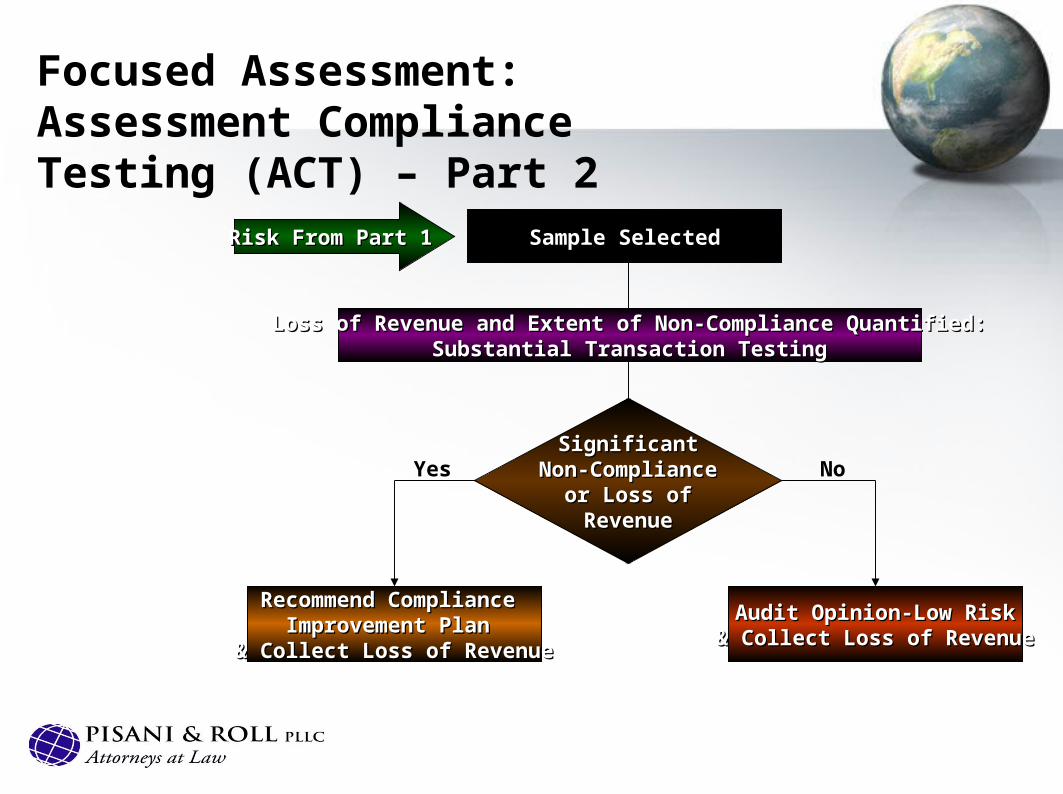

Recommend Compliance Recommend Compliance Improvement Plan Improvement Plan

& Collect Loss of Revenue& Collect Loss of Revenue

Audit Opinion-Low RiskAudit Opinion-Low Risk& Collect Loss of Revenue& Collect Loss of Revenue

Yes NoSignificantSignificant

Non-ComplianceNon-Complianceor Loss ofor Loss ofRevenueRevenue

Risk From Part 1Risk From Part 1

Loss of Revenue and Extent of Non-Compliance Quantified:Loss of Revenue and Extent of Non-Compliance Quantified:Substantial Transaction TestingSubstantial Transaction Testing

Sample SelectedSample Selected

Focused Assessment: Assessment Compliance Testing (ACT) – Part 2

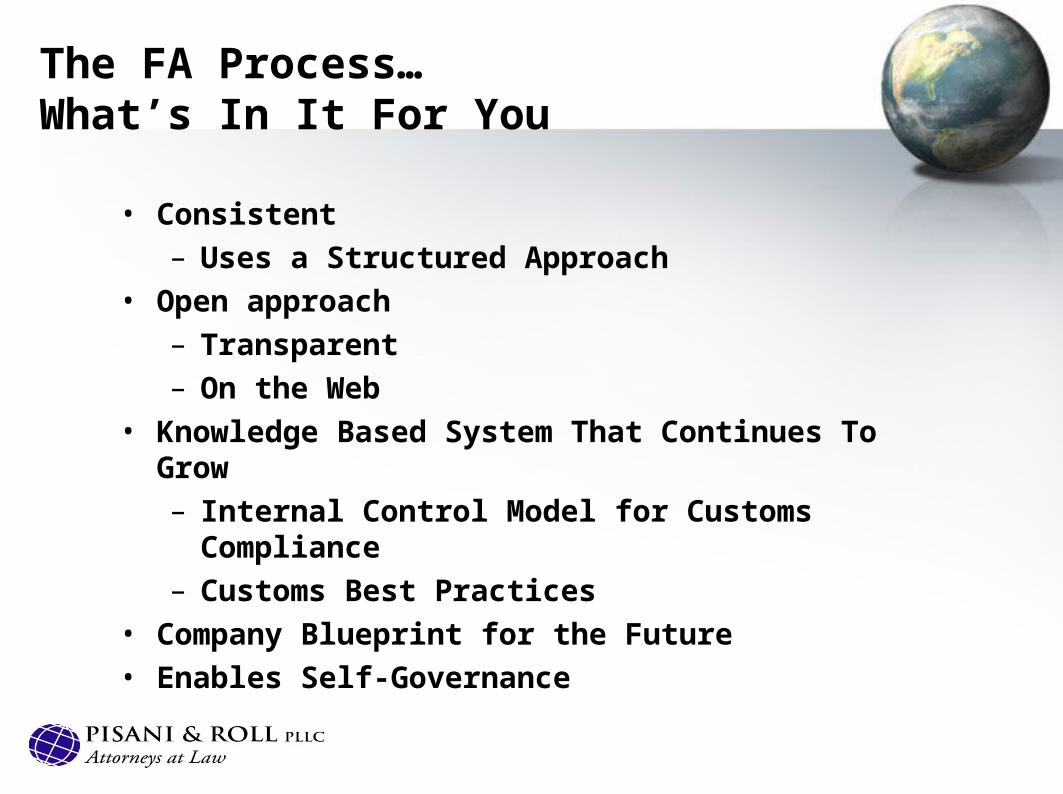

The FA Process…What’s In It For You

• Consistent– Uses a Structured Approach

• Open approach– Transparent– On the Web

• Knowledge Based System That Continues To Grow– Internal Control Model for Customs Compliance– Customs Best Practices

• Company Blueprint for the Future• Enables Self-Governance

What You Can Do

• Assess your risk of non-compliance

• Look for strengths and weaknesses in internal controls

• Document your internal controls

• Test transactions regularly and when weaknesses are identified

Key Internal Control Components

1. Corporate Compliance Statement – shows upper management’s buy in

2. Customs Compliance Manual – shows awareness of rules and regulations

3. Process Map of Customs Operations – shows thoughtful consideration of the totality of an import transaction

4. Written Procedures – shows systemic, institutional approach to compliance

5. Periodic Internal Reviews (Self-Assessments) – shows commitment to ongoing improvement

6. Training – shows willingness to learn

1. Corporate Compliance Statement Should:

• State company’s commitment to compliance• Affirm company-wide responsibility for

compliance (team approach)• Identify resources available to employees

(intranet, internet, and/or compliance manual)• Identify person or group responsible for

compliance• Provide instruction on reporting instances of non-

compliance and give assurance that no retribution will follow

• Describe punitive consequences for failure to follow

2. Customs Compliance ManualShould Be:

• Tailored to the specific needs and operations of the company

• User-friendly and void of too many “legalese”• Instructive for the customs department and non-

customs departments• Updated routinely based on factual or legal changes

and developments• Readily available to employees (intranet)• Used as a training tool

3. Process Map Of CustomsOperations Should:

• Depict all departments involved in importing

– Purchasing– Engineering– Research &

Development– Manufacturing– Tax

– Accounting– Legal– Transportation– Receiving/Inventory

Describe relevant import–related information resident within each department

Depict the flow of information between each department and the import department

A Process Map Of CustomsOperations Should: (cont.)

• Identify systems within each department that validate declarations made to Customs such as:

– Tariff classification– Parts database– Contracts database

– Department-specific databases– Accounts payable – Receiving reports

(overages/shortages)

• Identify source documents maintained by each department and their location

4. Written Procedures Should Be:

• Developed for all departments maintaining information relevant to the import process

• Developed in cooperation with the import department and based on feedback from other departments

• User-friendly, easy to follow, and readily available

• Incorporated into normal training regiment• Tested and updated periodically

5. Self-Testing Of Import Operations Should Confirm:

• What you declared to Custom was accurate– Tariff classification– Duty–preference program– Value (method and seller/buyer

relationship)– Origin– Quantity– Non-dutiable charges

Self-Testing Of Import Operations Should Confirm: (cont.)

• What you declared to Customs was complete– Invoice requirements– Statutory additions to transaction value

– Additional payments outside commercial invoice

– Documentary requirements

Additionally, Self-Testing Should Be:

• Conducted by qualified “independent” internal or external expert

• Comprised of representative sample of imports– Random and statistically valid sample

(number may vary)– Judgment sample (number may vary)

Additionally, Self-Testing Should Be: (cont.)

• Structured to capture “cradle to grave” information

– Purchasing– Contracts– Manufacturing– Product specs– Bill of materials

– Engineering/R&D– Accounting records– Transportation– Receiving/Inventory

• Performed at least annually (sometimes more frequently)

6. Training

• Identify:

– Areas for training

– Potential audiences

• Provide training using internal and external resources

• Document training (e.g., training logs)

What can a broker do?

• Develop and implement standard work instructions/procedures for handling importer’s account– Process for reporting classifications, claiming special

duty programs, handling additions to price paid or payable, etc.

– Process for handling prior disclosures, corrections to entries, PEA/SIL, CBP Form 28/29 responses, etc.

• Recordkeeping support during audit

ROLE OF THE BROKER IN ENFORCEMENT PROCEEDINGS

Review of some key broker regulations …..

§ 111.26 Interference with examination of records

• Except in accordance with the provisions of part 163 of this chapter, a broker must not refuse access to, conceal, remove, or destroy the whole or any part of any record relating to his transactions as a broker which is being sought, or which the broker has reasonable grounds to believe may be sought, by the Department of Homeland Security or any representative of the Department of Homeland Security, nor may he otherwise interfere, or attempt to interfere, with any proper and lawful efforts to procure or reproduce information contained in those records.

§ 111.29 Diligence in correspondence and paying monies

• (a) Due diligence by broker. Each broker must exercise due diligence in making financial settlements, in answering correspondence, and in preparing or assisting in the preparation and filing of records relating to any customs business matter handled by him as a broker …..

§ 111.32 False information

• A broker must not file or procure or assist in the filing of any claim, or of any document, affidavit, or other papers, known by such broker to be false. In addition, a broker must not knowingly give, or solicit or procure the giving of, any false or misleading information or testimony in any matter pending before the Department of Homeland Security or any representative of the Department of Homeland Security.

§ 111.53 Grounds for suspension or revocation of license or permit

• (a) The broker has made or caused to be made in any application for any license or permit under this part, or report filed with Customs, any statement which was, at the time and in light of the circumstances under which it was made, false or misleading with respect to any material fact, or has omitted to state in any application or report any material fact which was required;

§ 111.53 Grounds for suspension or revocation of license or permit

• (b) The broker has been convicted, at any time after the filing of an application for a license under §111.12, of any felony or misdemeanor which:– (1) Involved the importation or exportation of

merchandise;– (2) Arose out of the conduct of customs business; or– (3) Involved larceny, theft, robbery, extortion, forgery,

counterfeiting, fraudulent concealment, embezzlement, fraudulent conversion, or misappropriation of funds;

§ 111.53 Grounds for suspension or revocation of license or permit

• (c) The broker has violated any provision of any law enforced by Customs or the rules or regulations issued under any provision of any law enforced by Customs;

• (d) The broker has counseled, commanded, induced, procured, or knowingly aided or abetted the violations by any other person of any provision of any law enforced by Customs or the rules or regulations issued under any provision of any law enforced by Customs;

§ 111.53 Grounds for suspension or revocation of license or permit

• (e) The broker has knowingly employed, or continues to employ, any person who has been convicted of a felony, without written approval of that employment from the Assistant Commissioner;

• (f) The broker has, in the course of customs business, with intent to defraud, in any manner willfully and knowingly deceived, misled or threatened any client or prospective client; or

§ 111.53 Grounds for suspension or revocation of license or permit

• (g) The broker no longer meets the applicable requirements of §§111.11 and 111.19.

Enforcement proceedings

• But … remember that the broker is the agent of importer and that it owes a fiduciary duty to importer to act in importer’s best interest– Replies to Customs

• Should be in writing if possible and be done with importer’s consent

– Do NOT provide Customs with evidence re potential violations by importer unless you first, contact attorneys for broker and importer

• Again, if told by Customs not to alert importer, contact broker’s attorneys

Enforcement proceedings

• Do NOT file prior disclosure for clients without their consent• May file prior disclosure to protect broker, but leave client

out of it …– Yet, is that possible?