food demand in australia: trends and food security...

TRANSCRIPT

Food demand in Australia: Trends and food security issues Lindsay Hogan

Research by the Australian Bureau of Agricultural and Resource Economics and Sciences

Research Report 17.7 June 2017

Food demand in Australia: Trends and food security issues ABARES

i

© Commonwealth of Australia 2017

Ownership of intellectual property rights Unless otherwise noted, copyright (and any other intellectual property rights, if any) in this publication is owned by the Commonwealth of Australia (referred to as the Commonwealth).

Creative Commons licence All material in this publication is licensed under a Creative Commons Attribution 4.0 International Licence except content supplied by third parties, logos and the Commonwealth Coat of Arms.

Inquiries about the licence and any use of this document should be emailed to [email protected].

Cataloguing data Hogan, L 2017, Food demand in Australia: Trends and food security issues, ABARES Research Report 17.7, Canberra, June. CC BY 4.0.

ISSN 1447-8358 ISBN 978-1-74323-346-7 ABARES project 43574

Internet This publication is available at agriculture.gov.au/abares/publications.

Australian Bureau of Agricultural and Resource Economics and Sciences (ABARES) Postal address GPO Box 858 Canberra ACT 2601 Switchboard +61 2 6272 2010 Email [email protected] Web agriculture.gov.au/abares

Disclaimer The Australian Government acting through the Department of Agriculture and Water Resources, represented by the Australian Bureau of Agricultural and Resource Economics and Sciences, has exercised due care and skill in preparing and compiling the information and data in this publication. Notwithstanding, the Department of Agriculture and Water Resources, ABARES, its employees and advisers disclaim all liability, including for negligence and for any loss, damage, injury, expense or cost incurred by any person as a result of accessing, using or relying on information or data in this publication to the maximum extent permitted by law.

Acknowledgements The author very much appreciates information and helpful comments from Nick Blong, Usha Sriram-Prasad and Lynda Hayden from the Agricultural Policy Division in the Department of Agriculture and Water Resources, and Peter Gooday, David Galeano, Sally Thorpe, Trish Gleeson, Diane Stefaniac and Peter Berry from ABARES. Thanks also to Mihir Gupta for preparing the data visualisation tool that accompanies this report.

Food demand in Australia: Trends and food security issues ABARES

ii

Contents Summary .................................................................................................................................................................................................... 1

1 Introduction ............................................................................................................................................................................... 7

2 Long-term trends in Australia’s household food consumption ................................................................... 9

Recent trends ............................................................................................................................................................................... 9

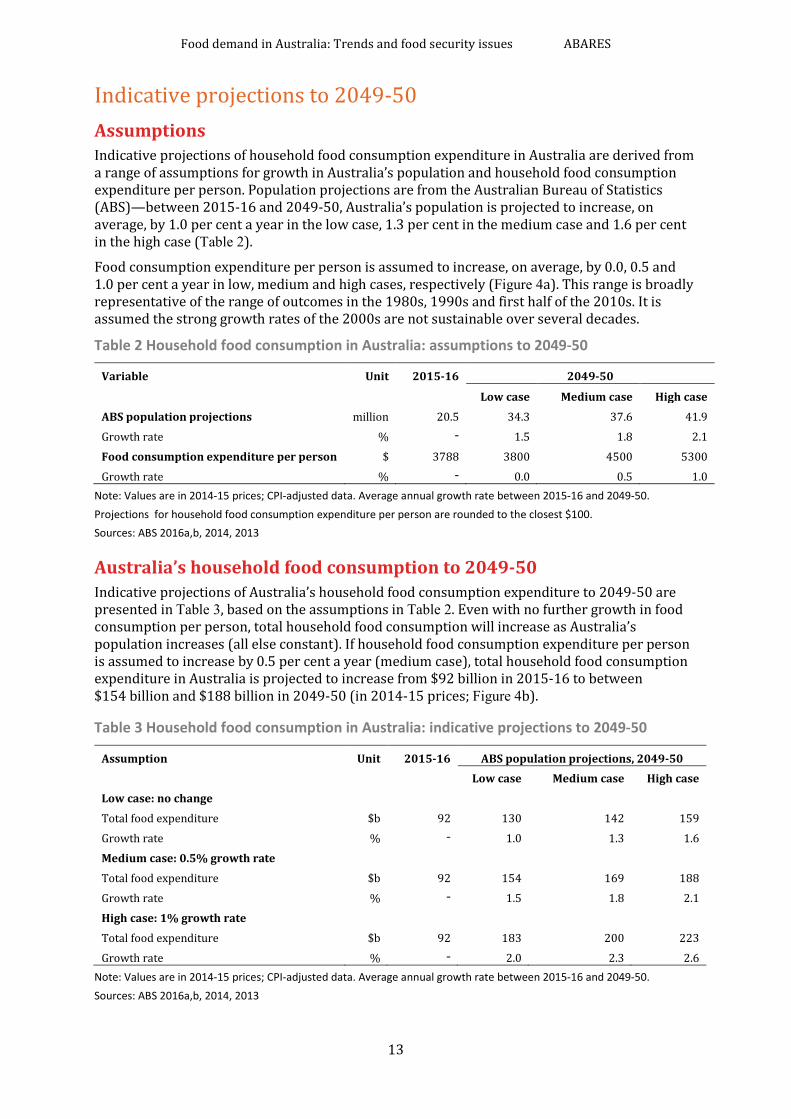

Indicative projections to 2049-50 ................................................................................................................................... 13

3 Household characteristics and food expenditure in Australia ................................................................. 15

Recent trends ............................................................................................................................................................................ 15

Household food expenditure by income quintile: 2009-10 ................................................................................. 17

Household food expenditure by net worth quintile: 2009-10 ............................................................................ 21

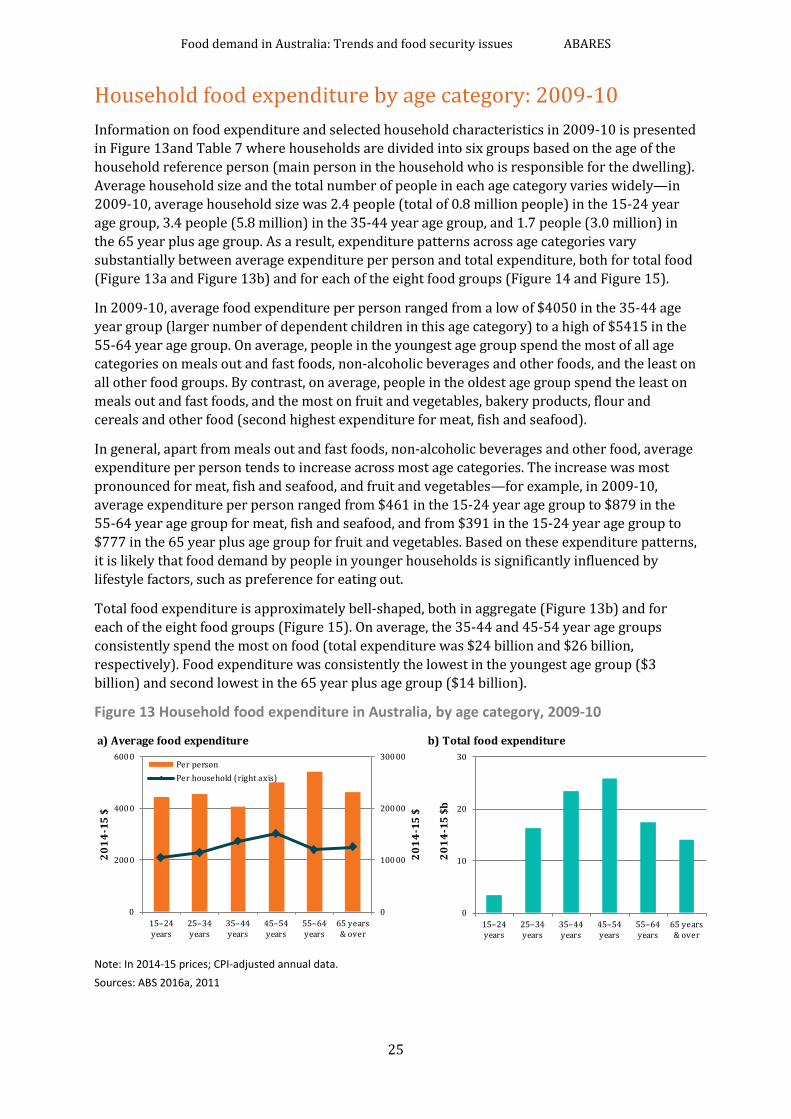

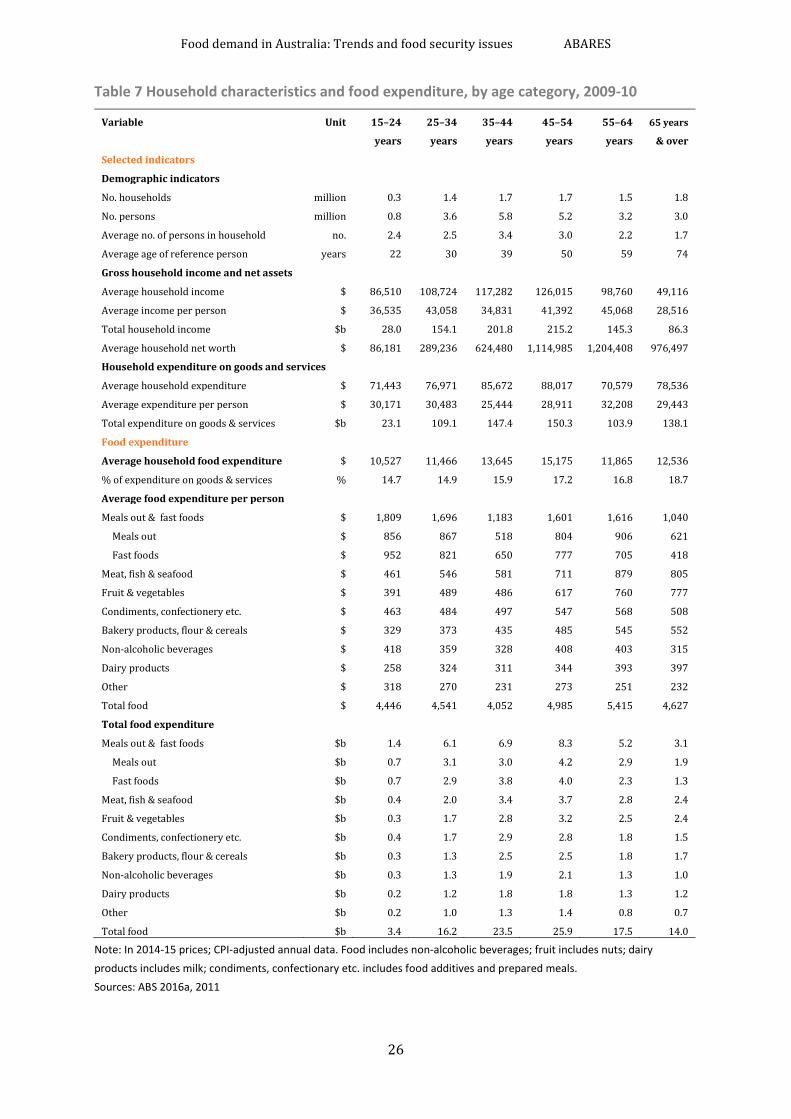

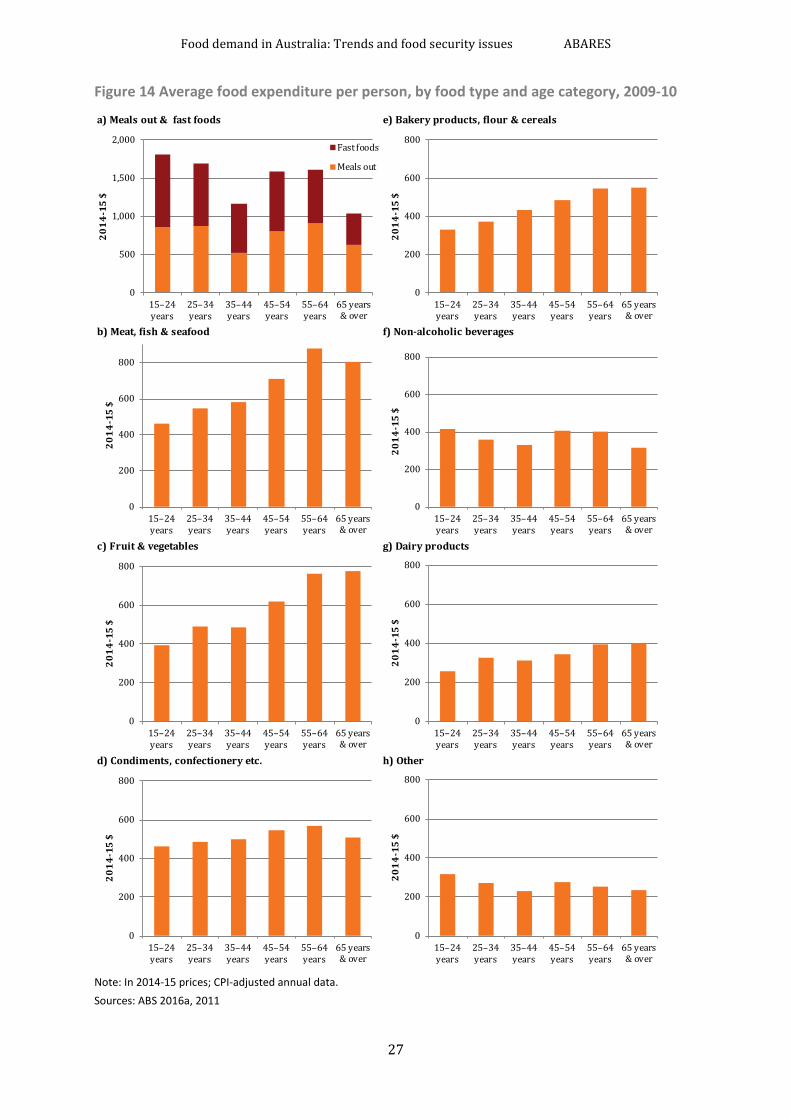

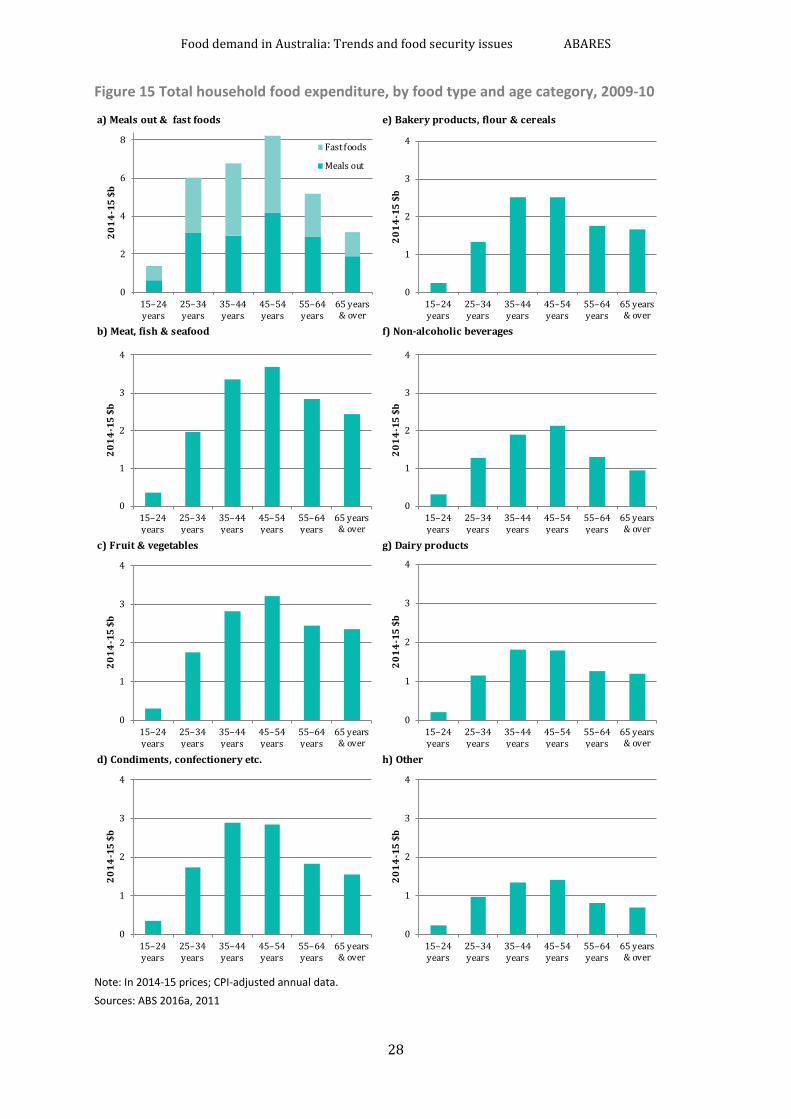

Household food expenditure by age category: 2009-10 ....................................................................................... 25

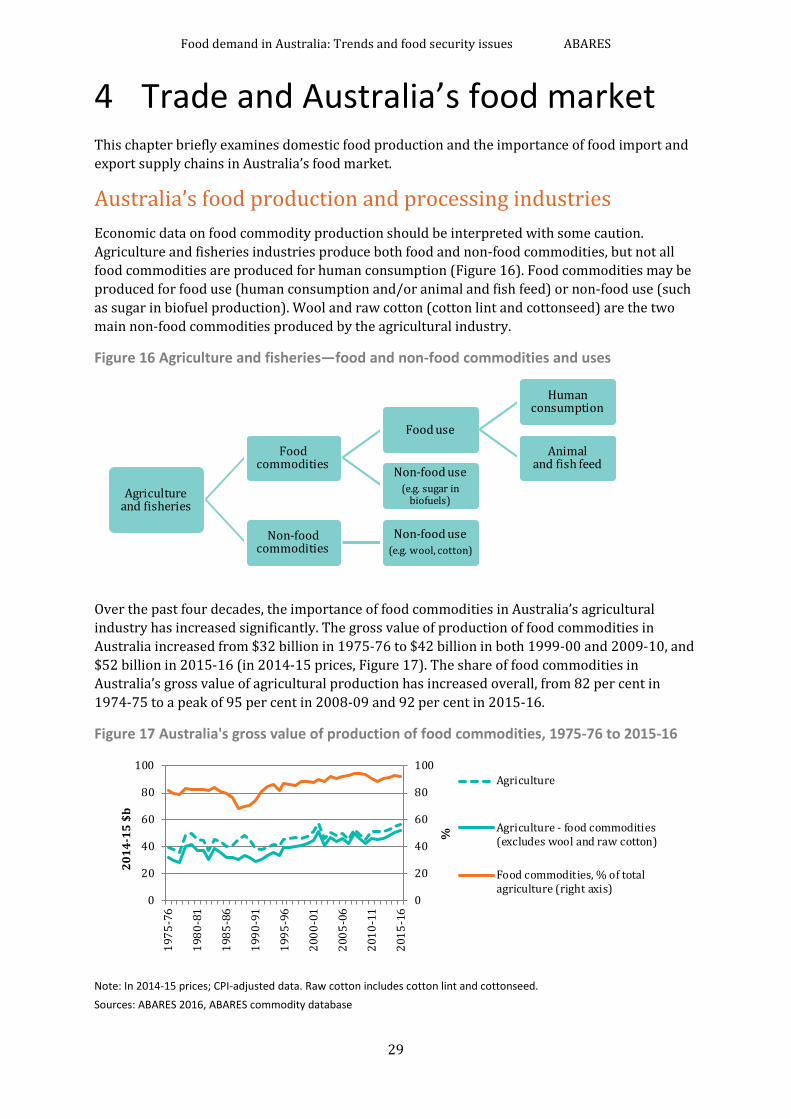

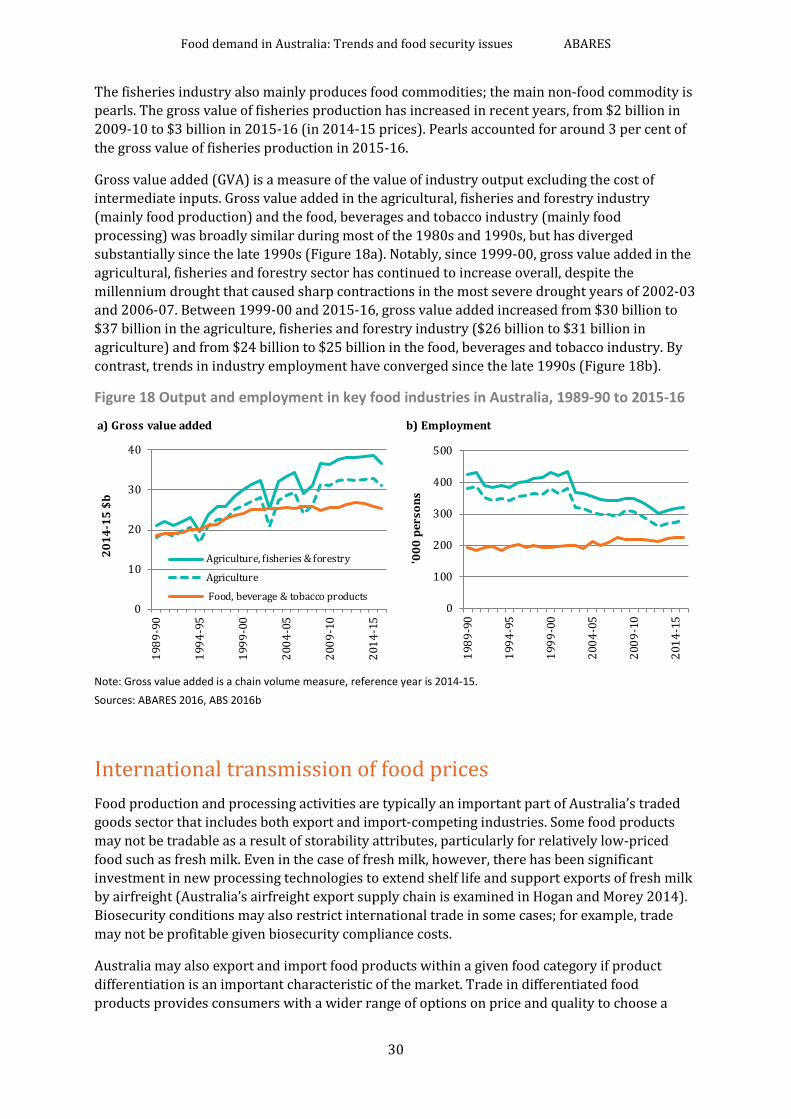

4 Trade and Australia’s food market ............................................................................................................................ 29

Australia’s food production and processing industries ......................................................................................... 29

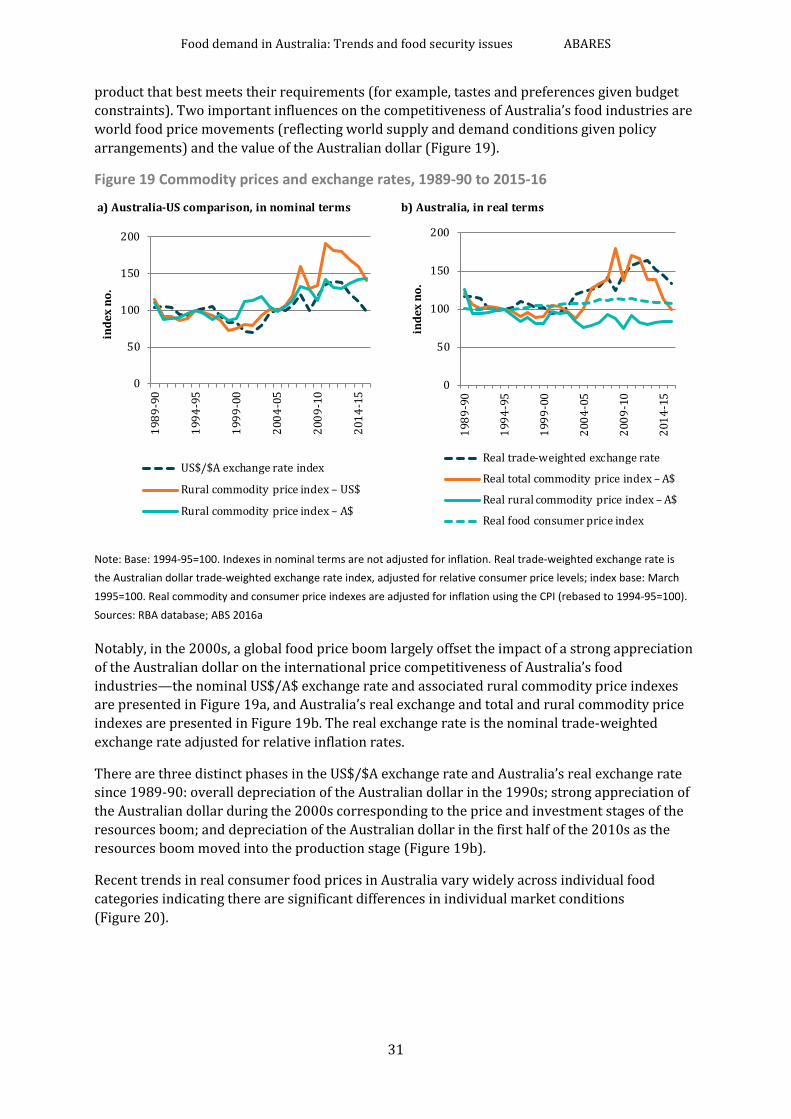

International transmission of food prices ................................................................................................................... 30

Importance of food trade ..................................................................................................................................................... 33

5 Food security issues ........................................................................................................................................................... 38

Definitions of food security and the role of government ...................................................................................... 38

Australia’s tax-transfer system ......................................................................................................................................... 39

Information policies: food prices and quality attributes....................................................................................... 44

6 Conclusion ................................................................................................................................................................................ 48

Appendix A: Food consumption and related measures ....................................................................................................... 49

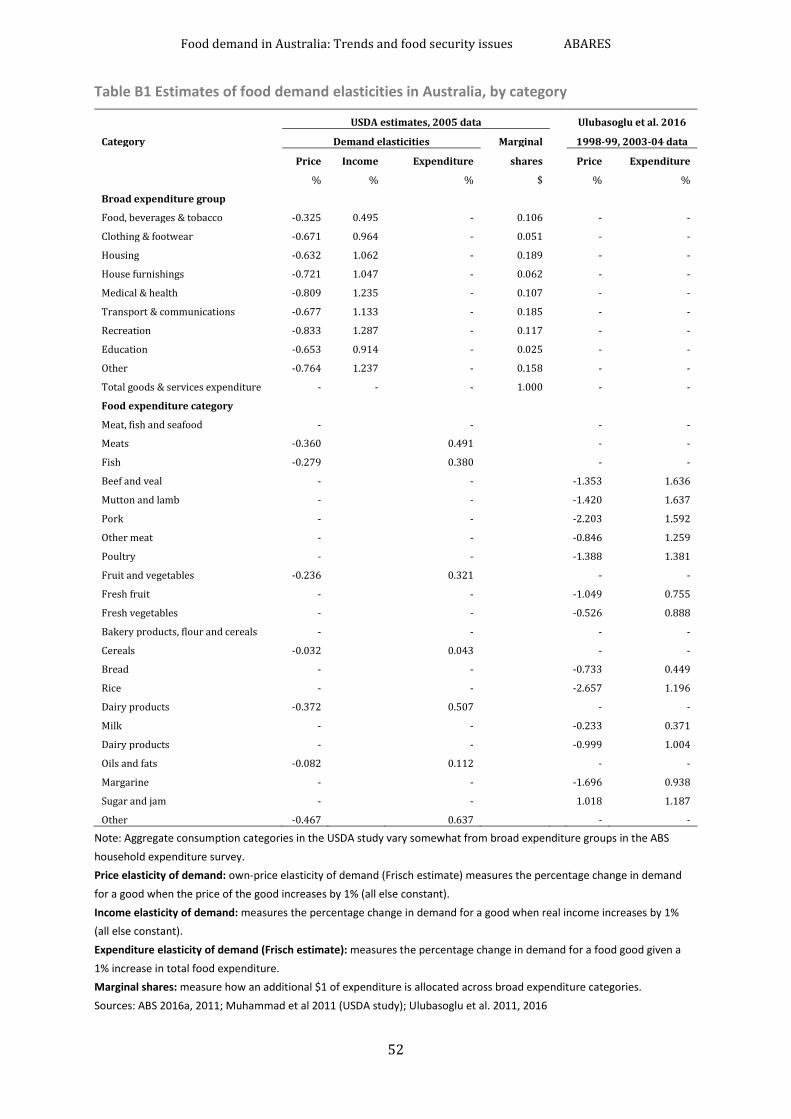

Appendix B: Food types and demand elasticities ................................................................................................................... 51

Appendix C: Private risk management strategies in food markets ................................................................................ 53

Appendix D: Australia’s consumer policy framework and food safety ......................................................................... 54

Appendix E: OECD classification of taxes ................................................................................................................................... 55

References ................................................................................................................................................................................................ 58

Food demand in Australia: Trends and food security issues ABARES

iii

Tables Table 1 Household food consumption and related indicators, Australia, selected years ..................................... 10

Table 2 Household food consumption in Australia: assumptions to 2049-50 .......................................................... 13

Table 3 Household food consumption in Australia: indicative projections to 2049-50 ....................................... 13

Table 4 Household food expenditure in Australia, by food category, selected years ............................................. 15

Table 5 Household characteristics and food expenditure, by income quintile, 2009-10 ..................................... 18

Table 6 Household characteristics and food expenditure, by net worth quintile, 2009-10 ................................ 22

Table 7 Household characteristics and food expenditure, by age category, 2009-10 ........................................... 26

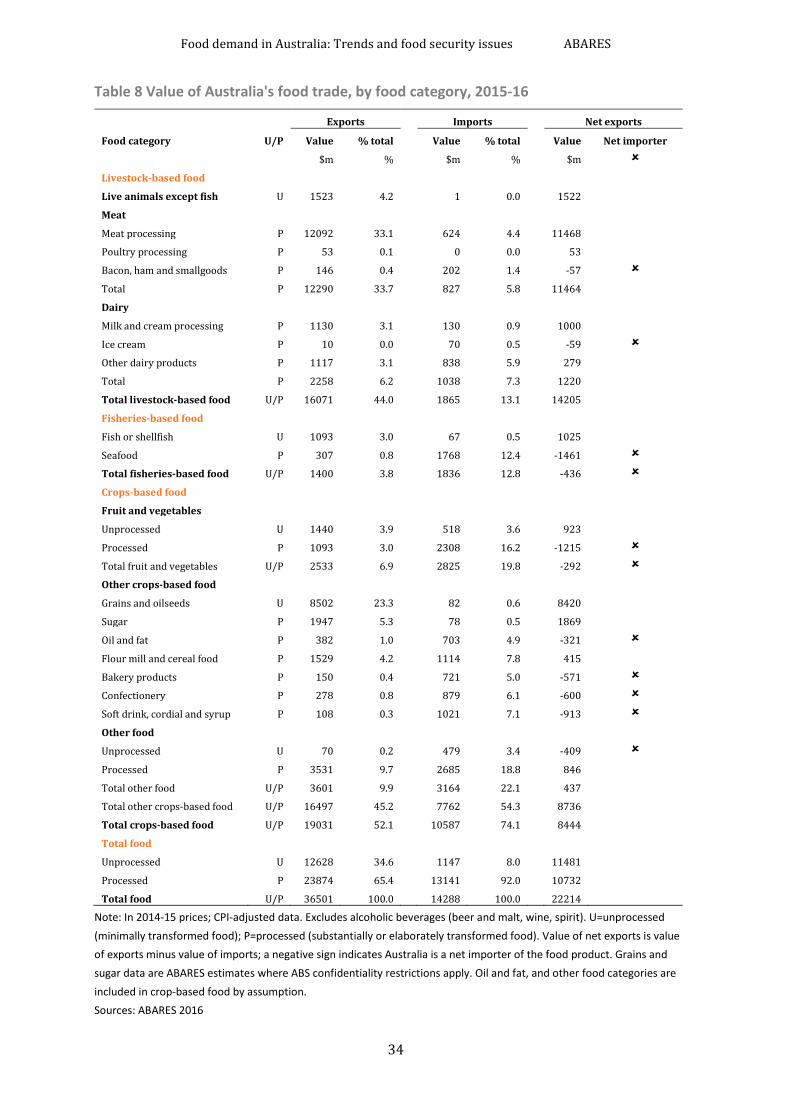

Table 8 Value of Australia's food trade, by food category, 2015-16 .............................................................................. 34

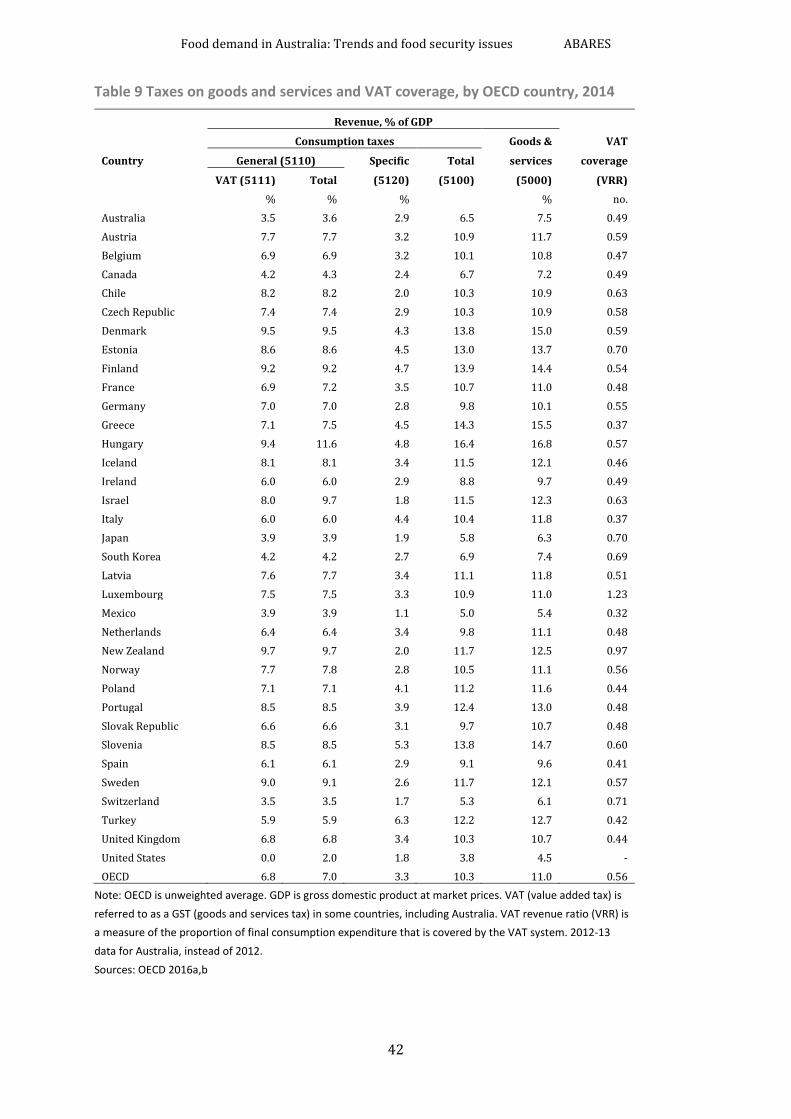

Table 9 Taxes on goods and services and VAT coverage, by OECD country, 2014 ................................................. 42

Table 10 VAT treatment of food, by OECD country, 2016 .................................................................................................. 43

Table B1 Estimates of food demand elasticities in Australia, by category .................................................................. 52

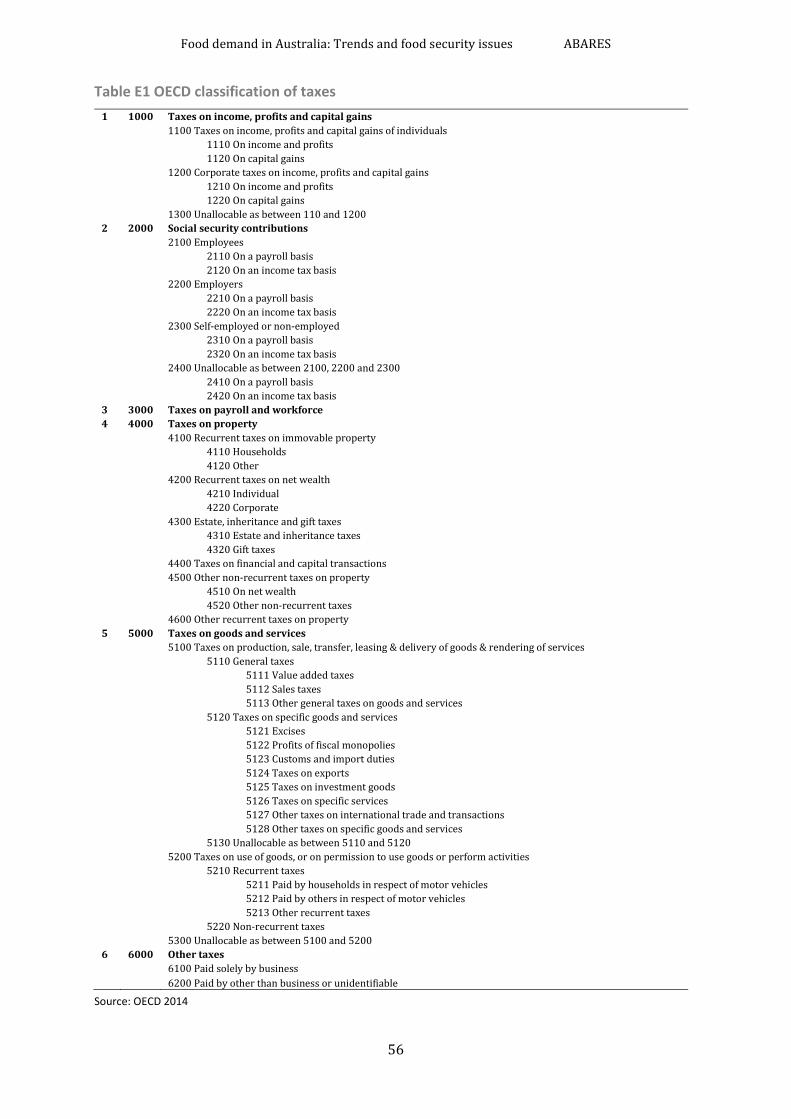

Table E1 OECD classification of taxes .......................................................................................................................................... 56

Figures Figure S1 Australia's household food consumption: indicative projections to 2049-50......................................... 1

Figure S2 Distribution of Australia's average household food expenditure, selected years .................................. 2

Figure S3 Household food expenditure per person in Australia, by category, 2009-10 .......................................... 3

Figure S4 Total household food expenditure in Australia, by category, 2009-10 ...................................................... 4

Figure S5 Importance of trade in Australia's food consumption and production, 1989-90 to 2015-16 .......... 5

Figure 1 Key components in Australia's household income account, 1964-65 to 2015-16 ................................... 9

Figure 2 Household food consumption expenditure per person in Australia, 1964-65 to 2015-16 ............... 12

Figure 3 Australia's household income per person and food prices, 1964-65 to 2015-16 ................................. 12

Figure 4 Australia's household food consumption: indicative projections to 2049-50 ........................................ 14

Figure 5 Household food expenditure in Australia, selected years ................................................................................ 16

Figure 6 Household food expenditure per person in Australia, by food type, selected years ............................ 16

Figure 7 Household food expenditure in Australia, by income quintile, 2009-10................................................... 17

Figure 8 Average food expenditure per person, by food type and income quintile, 2009-10............................ 19

Figure 9 Total household food expenditure, by food type and income quintile, 2009-10 ................................... 20

Figure 10 Household food expenditure in Australia, by net worth quintile, 2009-10 .......................................... 21

Figure 11 Average food expenditure per person, by food type and net worth quintile, 2009-10 .................. 23

Figure 12 Total household food expenditure in Australia, by food type and net worth quintile, 2009-10 . 24

Figure 13 Household food expenditure in Australia, by age category, 2009-10 ...................................................... 25

Figure 14 Average food expenditure per person, by food type and age category, 2009-10 ............................... 27

Figure 15 Total household food expenditure, by food type and age category, 2009-10 ...................................... 28

Figure 16 Agriculture and fisheries—food and non-food commodities and uses ................................................... 29

Figure 17 Australia's gross value of production of food commodities, 1975-76 to 2015-16 ............................. 29

Figure 18 Output and employment in key food industries in Australia, 1989-90 to 2015-16 .......................... 30

Figure 19 Commodity prices and exchange rates, 1989-90 to 2015-16 ...................................................................... 31

Food demand in Australia: Trends and food security issues ABARES

iv

Figure 20 Real food prices and consumption in Australia, by main food type, 1988-89 to 2015-16 ............. 32

Figure 21 Importance of trade in Australia's food consumption and production, 1989-90 to 2015-16 ....... 33

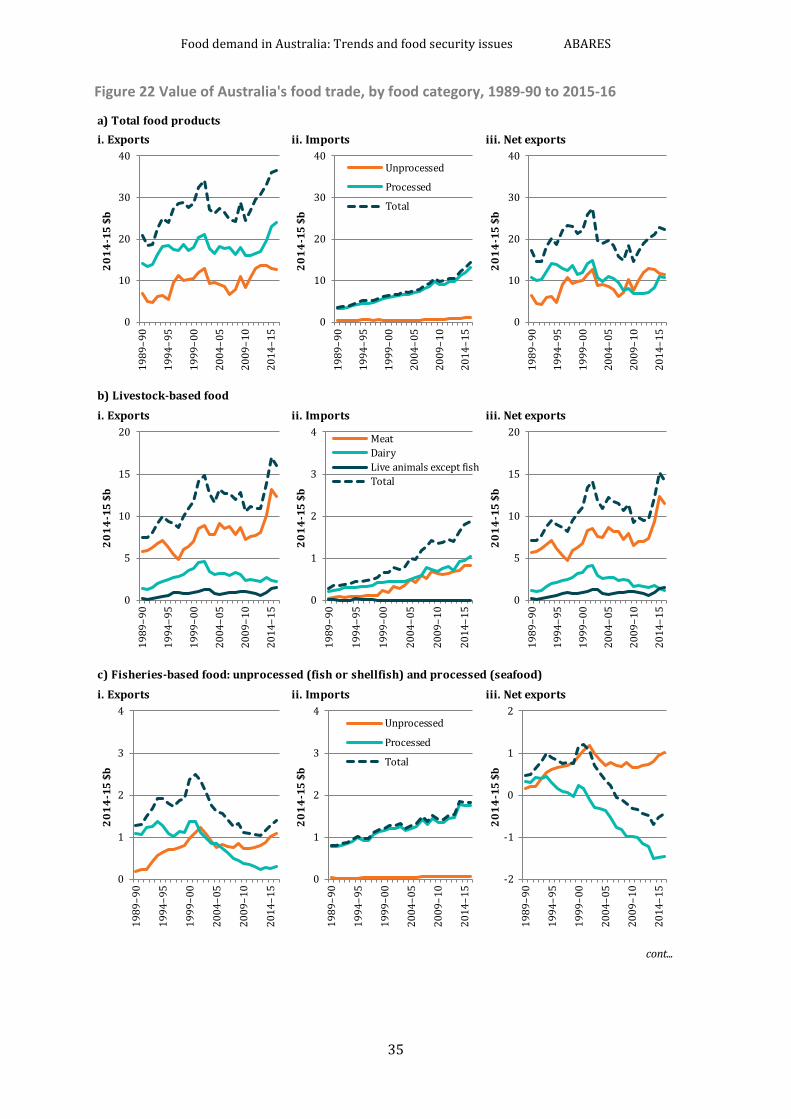

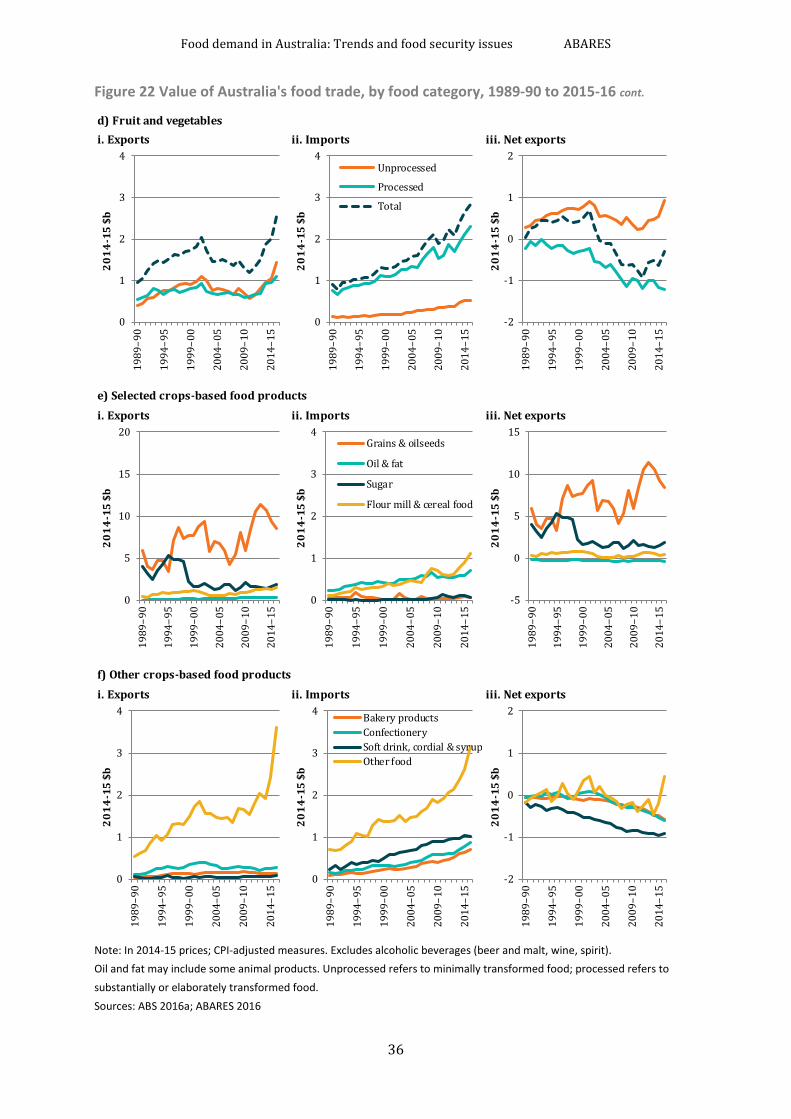

Figure 22 Value of Australia's food trade, by food category, 1989-90 to 2015-16 ................................................. 35

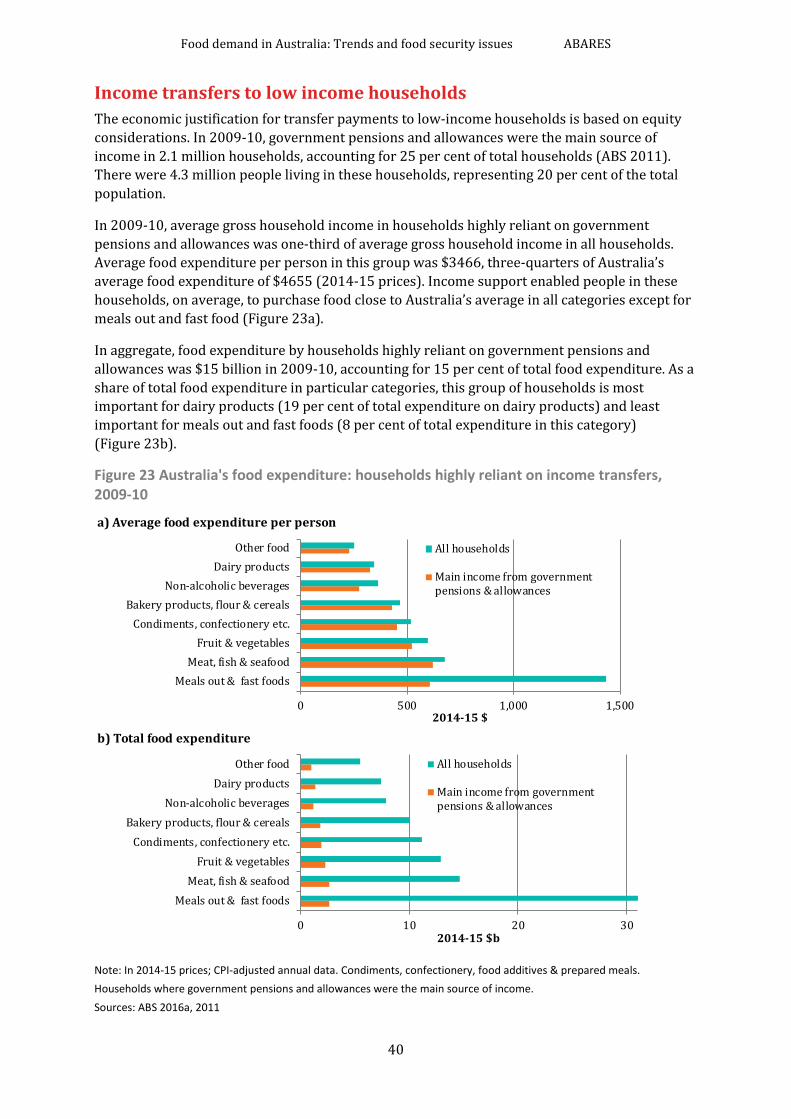

Figure 23 Australia's food expenditure: households highly reliant on income transfers, 2009-10 ................ 40

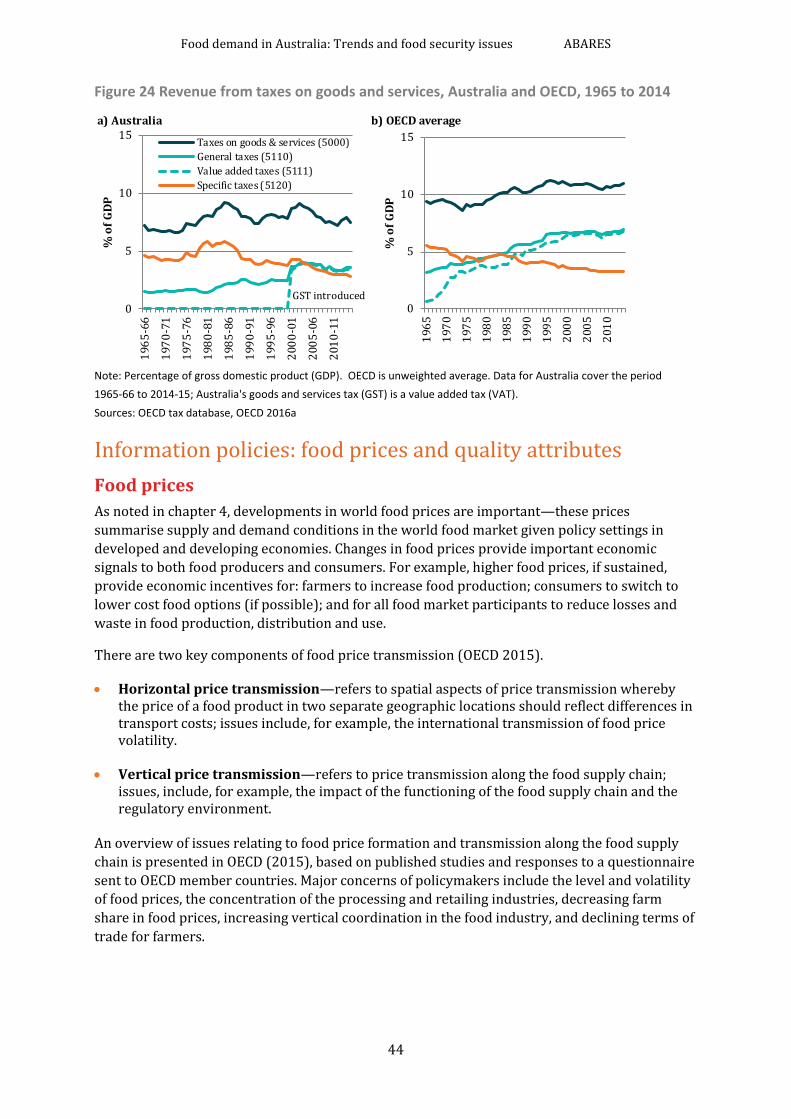

Figure 24 Revenue from taxes on goods and services, Australia and OECD, 1965 to 2014 ................................ 44

Figure B1 Growth rates in food consumption, prices and income in Australia, 1999-00 to 2015-16 ............ 51

Boxes Box 1 Definitions of food security ................................................................................................................................................. 38

Box 2 Information market failures................................................................................................................................................ 45

Box 3 Australian Government guidelines for healthy lifestyle choices ........................................................................ 47

Food demand in Australia: Trends and food security issues ABARES

1

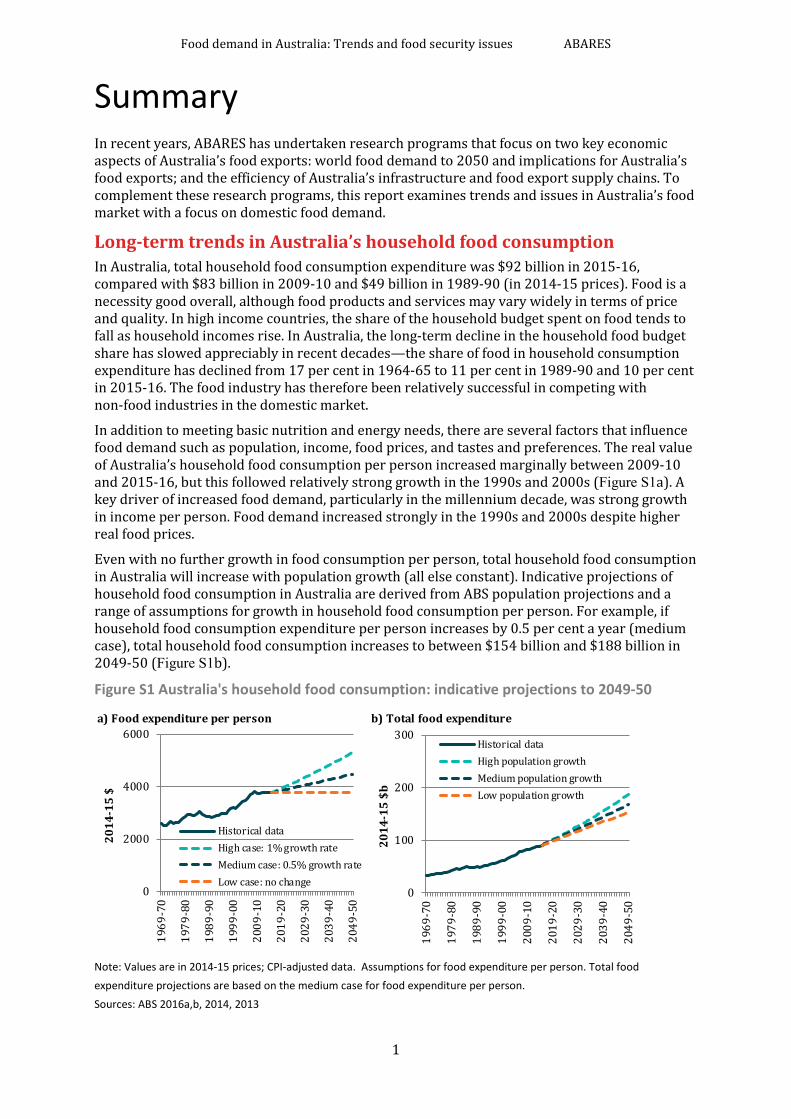

Summary In recent years, ABARES has undertaken research programs that focus on two key economic aspects of Australia’s food exports: world food demand to 2050 and implications for Australia’s food exports; and the efficiency of Australia’s infrastructure and food export supply chains. To complement these research programs, this report examines trends and issues in Australia’s food market with a focus on domestic food demand.

Long-term trends in Australia’s household food consumption In Australia, total household food consumption expenditure was $92 billion in 2015-16, compared with $83 billion in 2009-10 and $49 billion in 1989-90 (in 2014-15 prices). Food is a necessity good overall, although food products and services may vary widely in terms of price and quality. In high income countries, the share of the household budget spent on food tends to fall as household incomes rise. In Australia, the long-term decline in the household food budget share has slowed appreciably in recent decades—the share of food in household consumption expenditure has declined from 17 per cent in 1964-65 to 11 per cent in 1989-90 and 10 per cent in 2015-16. The food industry has therefore been relatively successful in competing with non-food industries in the domestic market.

In addition to meeting basic nutrition and energy needs, there are several factors that influence food demand such as population, income, food prices, and tastes and preferences. The real value of Australia’s household food consumption per person increased marginally between 2009-10 and 2015-16, but this followed relatively strong growth in the 1990s and 2000s (Figure S1a). A key driver of increased food demand, particularly in the millennium decade, was strong growth in income per person. Food demand increased strongly in the 1990s and 2000s despite higher real food prices.

Even with no further growth in food consumption per person, total household food consumption in Australia will increase with population growth (all else constant). Indicative projections of household food consumption in Australia are derived from ABS population projections and a range of assumptions for growth in household food consumption per person. For example, if household food consumption expenditure per person increases by 0.5 per cent a year (medium case), total household food consumption increases to between $154 billion and $188 billion in 2049-50 (Figure S1b).

Figure S1 Australia's household food consumption: indicative projections to 2049-50

Note: Values are in 2014-15 prices; CPI-adjusted data. Assumptions for food expenditure per person. Total food expenditure projections are based on the medium case for food expenditure per person. Sources: ABS 2016a,b, 2014, 2013

a) Food expenditure per person b) Total food expenditure

0

100

200

300

1969

-70

1979

-80

1989

-90

1999

-00

2009

-10

2019

-20

2029

-30

2039

-40

2049

-50

2014

-15

$b

Historical dataHigh population growthMedium population growthLow population growth

0

2000

4000

6000

1969

-70

1979

-80

1989

-90

1999

-00

2009

-10

2019

-20

2029

-30

2039

-40

2049

-50

2014

-15

$

Historical dataHigh case: 1% growth rateMedium case: 0.5% growth rateLow case: no change

Food demand in Australia: Trends and food security issues ABARES

2

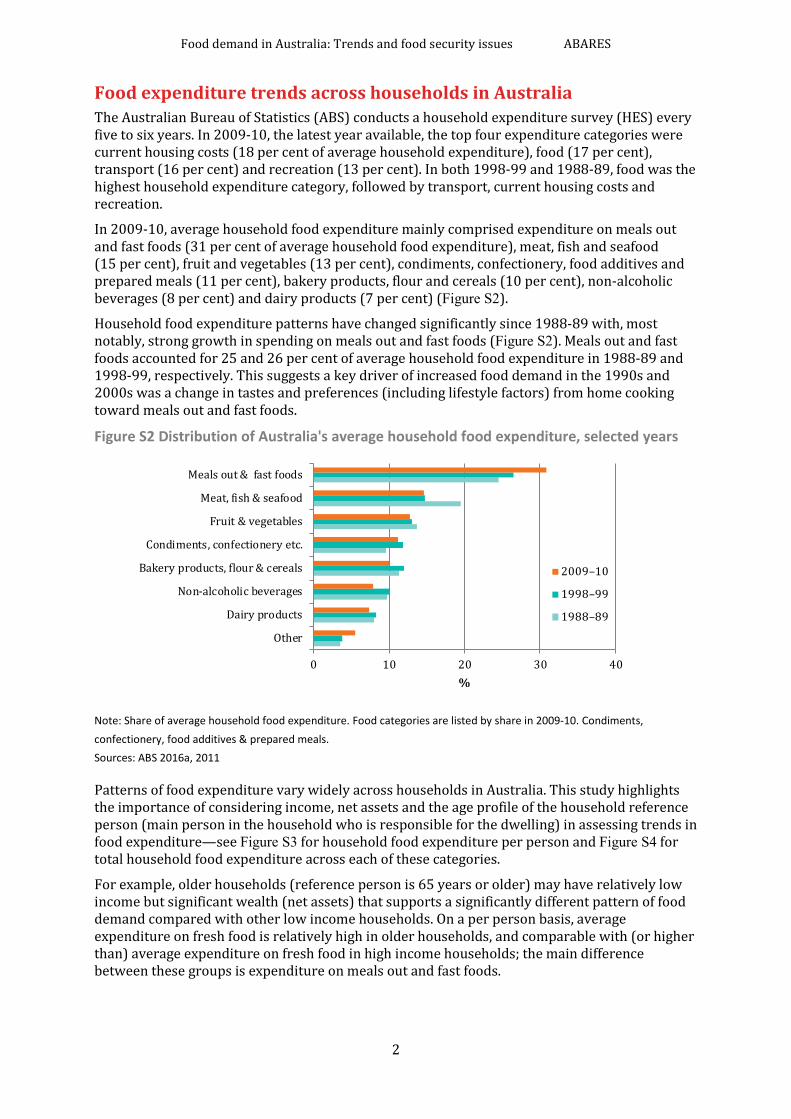

Food expenditure trends across households in Australia The Australian Bureau of Statistics (ABS) conducts a household expenditure survey (HES) every five to six years. In 2009-10, the latest year available, the top four expenditure categories were current housing costs (18 per cent of average household expenditure), food (17 per cent), transport (16 per cent) and recreation (13 per cent). In both 1998-99 and 1988-89, food was the highest household expenditure category, followed by transport, current housing costs and recreation.

In 2009-10, average household food expenditure mainly comprised expenditure on meals out and fast foods (31 per cent of average household food expenditure), meat, fish and seafood (15 per cent), fruit and vegetables (13 per cent), condiments, confectionery, food additives and prepared meals (11 per cent), bakery products, flour and cereals (10 per cent), non-alcoholic beverages (8 per cent) and dairy products (7 per cent) (Figure S2).

Household food expenditure patterns have changed significantly since 1988-89 with, most notably, strong growth in spending on meals out and fast foods (Figure S2). Meals out and fast foods accounted for 25 and 26 per cent of average household food expenditure in 1988-89 and 1998-99, respectively. This suggests a key driver of increased food demand in the 1990s and 2000s was a change in tastes and preferences (including lifestyle factors) from home cooking toward meals out and fast foods.

Figure S2 Distribution of Australia's average household food expenditure, selected years

Note: Share of average household food expenditure. Food categories are listed by share in 2009-10. Condiments, confectionery, food additives & prepared meals. Sources: ABS 2016a, 2011

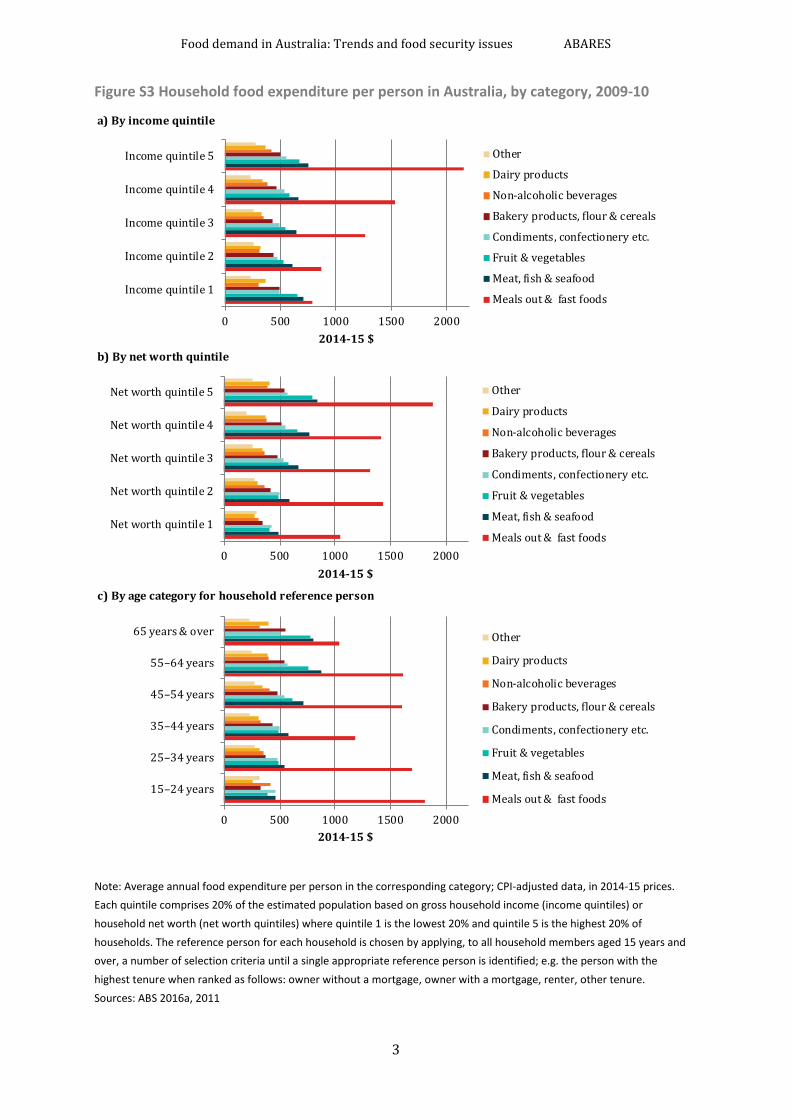

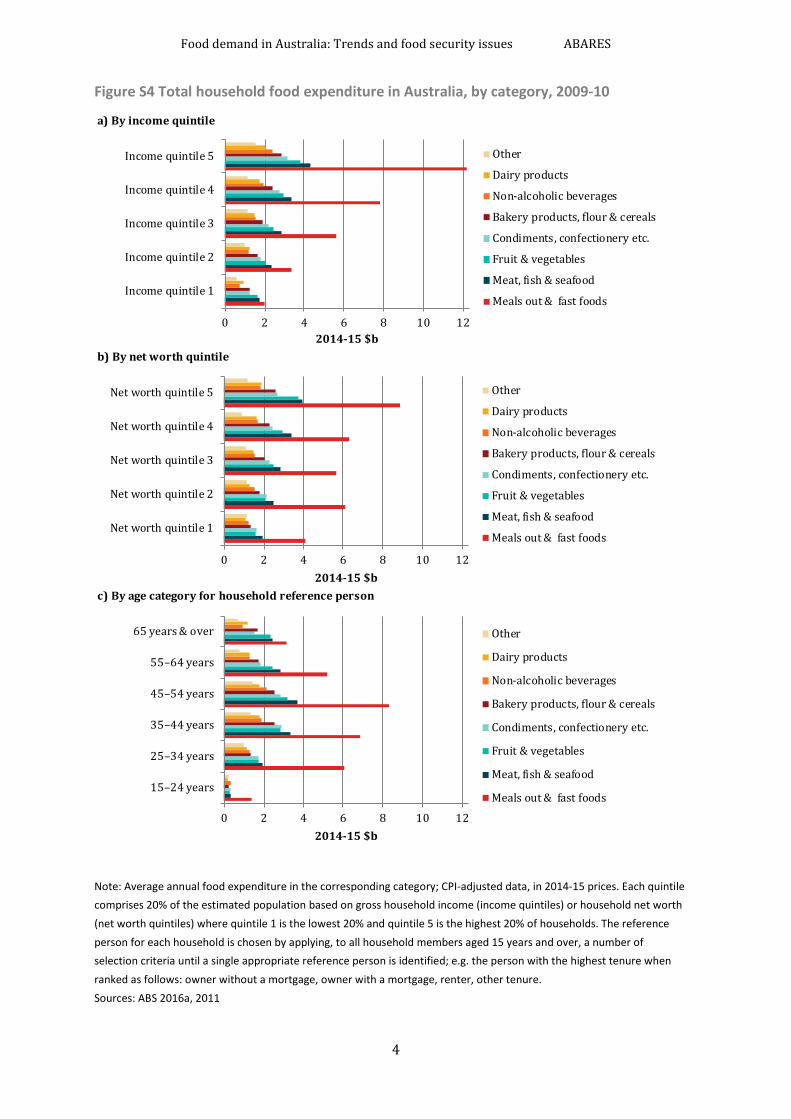

Patterns of food expenditure vary widely across households in Australia. This study highlights the importance of considering income, net assets and the age profile of the household reference person (main person in the household who is responsible for the dwelling) in assessing trends in food expenditure—see Figure S3 for household food expenditure per person and Figure S4 for total household food expenditure across each of these categories.

For example, older households (reference person is 65 years or older) may have relatively low income but significant wealth (net assets) that supports a significantly different pattern of food demand compared with other low income households. On a per person basis, average expenditure on fresh food is relatively high in older households, and comparable with (or higher than) average expenditure on fresh food in high income households; the main difference between these groups is expenditure on meals out and fast foods.

0 10 20 30 40

Other

Dairy products

Non-alcoholic beverages

Bakery products, flour & cereals

Condiments, confectionery etc.

Fruit & vegetables

Meat, fish & seafood

Meals out & fast foods

%

2009–10

1998–99

1988–89

Food demand in Australia: Trends and food security issues ABARES

3

Figure S3 Household food expenditure per person in Australia, by category, 2009-10

Note: Average annual food expenditure per person in the corresponding category; CPI-adjusted data, in 2014-15 prices. Each quintile comprises 20% of the estimated population based on gross household income (income quintiles) or household net worth (net worth quintiles) where quintile 1 is the lowest 20% and quintile 5 is the highest 20% of households. The reference person for each household is chosen by applying, to all household members aged 15 years and over, a number of selection criteria until a single appropriate reference person is identified; e.g. the person with the highest tenure when ranked as follows: owner without a mortgage, owner with a mortgage, renter, other tenure. Sources: ABS 2016a, 2011

a) By income quintile

b) By net worth quintile

c) By age category for household reference person

0 500 1000 1500 2000

Income quintile 1

Income quintile 2

Income quintile 3

Income quintile 4

Income quintile 5

2014-15 $

Other

Dairy products

Non-alcoholic beverages

Bakery products, flour & cereals

Condiments, confectionery etc.

Fruit & vegetables

Meat, fish & seafood

Meals out & fast foods

0 500 1000 1500 2000

Net worth quintile 1

Net worth quintile 2

Net worth quintile 3

Net worth quintile 4

Net worth quintile 5

2014-15 $

Other

Dairy products

Non-alcoholic beverages

Bakery products, flour & cereals

Condiments, confectionery etc.

Fruit & vegetables

Meat, fish & seafood

Meals out & fast foods

0 500 1000 1500 2000

15–24 years

25–34 years

35–44 years

45–54 years

55–64 years

65 years & over

2014-15 $

Other

Dairy products

Non-alcoholic beverages

Bakery products, flour & cereals

Condiments, confectionery etc.

Fruit & vegetables

Meat, fish & seafood

Meals out & fast foods

Food demand in Australia: Trends and food security issues ABARES

4

Figure S4 Total household food expenditure in Australia, by category, 2009-10

Note: Average annual food expenditure in the corresponding category; CPI-adjusted data, in 2014-15 prices. Each quintile comprises 20% of the estimated population based on gross household income (income quintiles) or household net worth (net worth quintiles) where quintile 1 is the lowest 20% and quintile 5 is the highest 20% of households. The reference person for each household is chosen by applying, to all household members aged 15 years and over, a number of selection criteria until a single appropriate reference person is identified; e.g. the person with the highest tenure when ranked as follows: owner without a mortgage, owner with a mortgage, renter, other tenure. Sources: ABS 2016a, 2011

a) By income quintile

b) By net worth quintile

c) By age category for household reference person

0 2 4 6 8 10 12

Income quintile 1

Income quintile 2

Income quintile 3

Income quintile 4

Income quintile 5

2014-15 $b

Other

Dairy products

Non-alcoholic beverages

Bakery products, flour & cereals

Condiments, confectionery etc.

Fruit & vegetables

Meat, fish & seafood

Meals out & fast foods

0 2 4 6 8 10 12

Net worth quintile 1

Net worth quintile 2

Net worth quintile 3

Net worth quintile 4

Net worth quintile 5

2014-15 $b

Other

Dairy products

Non-alcoholic beverages

Bakery products, flour & cereals

Condiments, confectionery etc.

Fruit & vegetables

Meat, fish & seafood

Meals out & fast foods

0 2 4 6 8 10 12

15–24 years

25–34 years

35–44 years

45–54 years

55–64 years

65 years & over

2014-15 $b

Other

Dairy products

Non-alcoholic beverages

Bakery products, flour & cereals

Condiments, confectionery etc.

Fruit & vegetables

Meat, fish & seafood

Meals out & fast foods

Food demand in Australia: Trends and food security issues ABARES

5

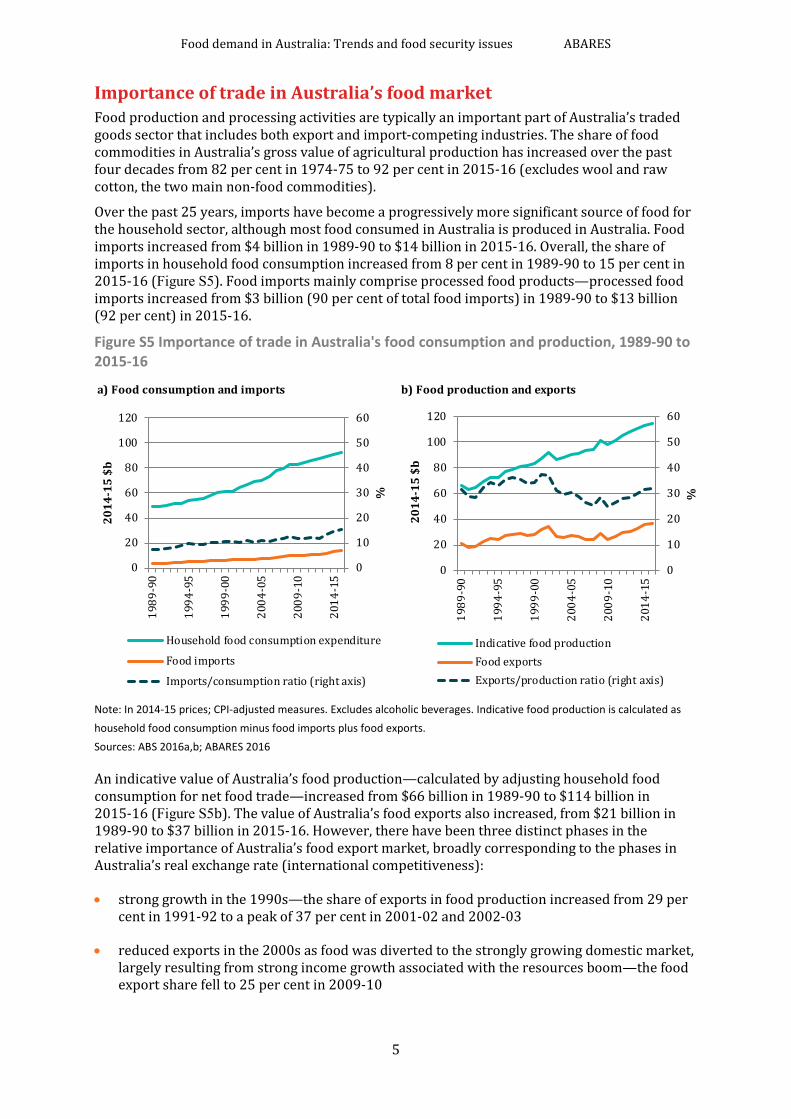

Importance of trade in Australia’s food market Food production and processing activities are typically an important part of Australia’s traded goods sector that includes both export and import-competing industries. The share of food commodities in Australia’s gross value of agricultural production has increased over the past four decades from 82 per cent in 1974-75 to 92 per cent in 2015-16 (excludes wool and raw cotton, the two main non-food commodities).

Over the past 25 years, imports have become a progressively more significant source of food for the household sector, although most food consumed in Australia is produced in Australia. Food imports increased from $4 billion in 1989-90 to $14 billion in 2015-16. Overall, the share of imports in household food consumption increased from 8 per cent in 1989-90 to 15 per cent in 2015-16 (Figure S5). Food imports mainly comprise processed food products—processed food imports increased from $3 billion (90 per cent of total food imports) in 1989-90 to $13 billion (92 per cent) in 2015-16.

Figure S5 Importance of trade in Australia's food consumption and production, 1989-90 to 2015-16

Note: In 2014-15 prices; CPI-adjusted measures. Excludes alcoholic beverages. Indicative food production is calculated as household food consumption minus food imports plus food exports. Sources: ABS 2016a,b; ABARES 2016

An indicative value of Australia’s food production—calculated by adjusting household food consumption for net food trade—increased from $66 billion in 1989-90 to $114 billion in 2015-16 (Figure S5b). The value of Australia’s food exports also increased, from $21 billion in 1989-90 to $37 billion in 2015-16. However, there have been three distinct phases in the relative importance of Australia’s food export market, broadly corresponding to the phases in Australia’s real exchange rate (international competitiveness):

• strong growth in the 1990s—the share of exports in food production increased from 29 per cent in 1991-92 to a peak of 37 per cent in 2001-02 and 2002-03

• reduced exports in the 2000s as food was diverted to the strongly growing domestic market, largely resulting from strong income growth associated with the resources boom—the food export share fell to 25 per cent in 2009-10

a) Food consumption and imports b) Food production and exports

0

10

20

30

40

50

60

0

20

40

60

80

100

120

1989

-90

1994

-95

1999

-00

2004

-05

2009

-10

2014

-15

%

2014

-15

$b

Household food consumption expenditure

Food imports

Imports/consumption ratio (right axis)

0

10

20

30

40

50

60

0

20

40

60

80

100

120

1989

-90

1994

-95

1999

-00

2004

-05

2009

-10

2014

-15

%

2014

-15

$b

Indicative food productionFood exportsExports/production ratio (right axis)

Food demand in Australia: Trends and food security issues ABARES

6

• a resumption of strong export growth in the first half of the 2010s associated with the fall in the real exchange rate and slower growth in domestic food demand—the food export share increased to 32 per cent in 2015-16.

Overall, net food exports were $22 billion in 2015-16, indicating Australia continues to have an important international competitive advantage in food trade. In 2015-16, Australia was a significant net importer in six categories: seafood; processed fruit and vegetables; soft drink, cordials and syrups; confectionary; bakery products; and oils and fats.

Issues This report briefly examines key factors in Australia’s policy approach that underpin Australia’s high level of food security. One of the most important roles of government is to ensure the food security of the population. In general terms, food security refers to the adequate and reliable provision of food that is safe, nutritious and affordable. In aggregate, as a net food exporter, Australia produces food in excess of domestic requirements. Key domestic food security concerns relate to food access and use for low income people, particularly in regional and remote areas. Governments also have an important role in ensuring people have access to adequate food in emergency situations following natural disasters such as floods and bushfires.

From an economic perspective, governments aim to address market failures and achieve distributional goals. The tax-transfer system is a key component of the overarching policy framework that contributes to Australia’s high level of food security. Two mechanisms that are significant contributors to food security are:

• income support to low-income households through transfer payments, and

• exemption of fresh food in the goods and services tax (GST).

The economic justification for transfer payments to low-income households is based on equity considerations. In 2009-10, government pensions and allowances were the main source of income in 25 per cent of total households covering 20 per cent of the total population. Income support enabled people in these households, on average, to purchase food close to Australia’s average in all categories except for meals out and fast food. In aggregate, food expenditure by these households was $15 billion, accounting for 15 per cent of total food expenditure in 2009-10. This group of households is most important for dairy products (19 per cent of total expenditure on dairy products) and least important for meals out and fast foods (8 per cent of total expenditure in this category).

Fresh food is exempt in Australia’s goods and services tax (GST), reducing the consumer price of fresh food (all else constant). There are two economic implications of exempting fresh food in the GST relating to key food security concerns across households.

• Equity implications—complementing the transfer system by reducing the tax burden in low-income households; meat, fish and seafood, and fruit and vegetables are major food expenditure categories, on average, for people in households that are highly reliant on income transfers.

• Encouraging the consumption of fresh food—consumption of nutritious fresh food has important positive health benefits for people (positive externalities), reducing future health costs to the individual and society overall (all else constant).

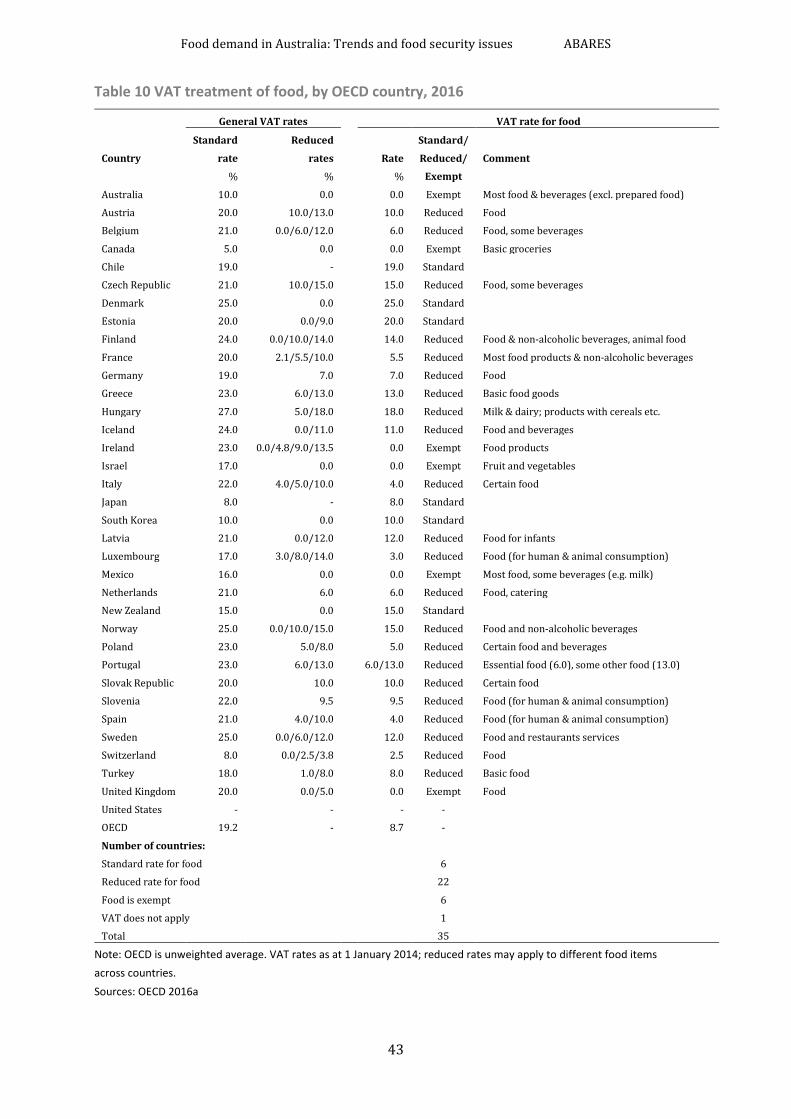

Broad-based consumption taxes—referred to as a value added tax (VAT) or a goods and services tax (GST)—apply in 34 of 35 OECD countries. A wide range of VAT rates and coverage apply across OECD countries, but exemptions or reduced rates for food apply in 28 OECD countries. For example, VAT exemptions for food apply in the United Kingdom where the standard VAT

Food demand in Australia: Trends and food security issues ABARES

7

rate is 20 per cent, and in Canada (for basic groceries) where the standard VAT rate is 5 per cent. By contrast, New Zealand applies a broad-based consumption tax to nearly all goods and services, including food, at a rate of 15 per cent.

In addition to income and food prices, the tastes and preferences of individuals are important economic influences on consumer food choices. An important aspect of information market failure occurs when consumers are not fully informed about the quality attributes of a product or the health implications of food choices. Australian governments have had a major role in developing two important food labels that provide consumers with information about food nutrition.

• Nutrition label—a relatively detailed guide to the nutrition content of a food product; a nutrition information panel is included on most food products.

• Health star rating label—a summary guide to the nutrition content of a food product, implemented since June 2014 on a voluntary basis by the food industry; the health star rating is a front-of-pack labelling system that rates the overall nutritional profile of packaged food and assigns it a rating from ½ a star to 5 stars where a higher star rating indicates a healthier food option.

The education system also contributes to consumer understanding of healthy food choices over the longer term in two ways—by teaching nutrition as part of the school curriculum, and by providing a range of healthy food options in school canteens. For example, in February 2017, the NSW Government released a new healthy schools canteen strategy whereby 75 per cent of canteen menus must comprise healthy food options (such as fruits, vegetables, sandwiches, pastas and stir fries), while the remaining food options require a health star rating of 3.5 stars or higher.

Conclusion The domestic market is important for Australia’s food producers including farmers, food processors and food service providers. Food expenditure per person tends to be higher, on average, in households with higher incomes—notably, the share of total food expenditure spent on meals out and fast foods is significantly higher for households with higher incomes. By contrast, the distribution of food expenditure is broadly similar across household groups based on net worth—that is, households with high net worth spend relatively more on food in aggregate, but the shares spent on the main food categories are broadly similar.

The food industry supplies a broad range of food products and services in response to food demand in different segments of the domestic market. There is ongoing innovation by the food industry to increase the efficiency and effectiveness of the food supply chain, including to enhance further Australia’s high level of food security. For example, major food retailers have developed product lines to sell imperfect fruit and vegetables at lower prices. Patterns of food expenditure indicate there are also likely to be ongoing economic opportunities to obtain a price premium for reliable food quality attributes.

Food demand in Australia: Trends and food security issues ABARES

8

1 Introduction In recent years, ABARES has undertaken research programs that focus on two key economic aspects of Australia’s food exports.

• World food demand to 2050 and implications for Australia’s food exports—the world’s long-term food requirements are likely to be substantial, particularly as the world population is projected to increase from around 7 billion in 2011 to 9.3 billion in 2050 and 10.1 billion in 2100 (UN 2011; medium variant; HLPE 2011). ABARES projections indicate that world agrifood consumption and imports are likely to increase markedly to 2050, with relatively strong growth in food demand in the Asian region (see, for example, Gunning-Trant et al. 2015; Hamshere et al. 2014 a,b; ABARES 2013; Linehan et al. 2013, 2012 a,b).

• Efficiency of Australia’s infrastructure and food export supply chains—ensuring Australia’s infrastructure and biosecurity systems allow food producers, processors and exporters to move food cost-effectively and efficiently to destination markets is a key to realising potential new and expanded export market opportunities. A preliminary economic assessment was released in November 2013 (Nguyen et al. 2013), followed by studies on Australia’s airfreight food exports (Hogan and Morey 2014), Australia’s wheat industry (Nguyen et al. 2015) and Australia’s beef industry (Goesch et al. 2015). Some background information on the farm-to-retail price spread and farm share in food supply chains in Australia is provided in Nguyen et al. (2016).

To complement these research programs, this report examines trends and issues in Australia’s food demand. Food is a necessity good overall, although food products may vary widely in terms of price and quality. In 2015-16, household food consumption expenditure in Australia was $92 billion, accounting for 10 per cent of total household consumption expenditure (in 2014-15 prices; ABS 2016a,b). In this report, unless otherwise specified, food excludes alcoholic beverages and, for consistency with ABS national accounts data, all real values are given in 2014-15 prices. Definitions of household food consumption expenditure and related measures are given in appendix A.

The structure of the report is as follows.

• Trends (chapters 2-4)—chapter 2 briefly examines long-term trends in household food consumption expenditure, including indicative projections to 2049-50; chapter 3 examines household food consumption in more detail using household expenditure survey data; and chapter 4 examines the importance of trade in Australia’s food market.

• Issues (chapter 5)—chapter 5 briefly examines economic issues relevant to food demand in Australia with a focus on key factors in the policy approach that underpin Australia’s high level of food security.

Some concluding comments are provided in chapter 6.

Food demand in Australia: Trends and food security issues ABARES

9

2 Long-term trends in Australia’s household food consumption

This chapter briefly examines historical trends in Australia’s household food consumption and three important influences on food demand: population, food prices and household incomes. Indicative projections to 2049-50 are also provided.

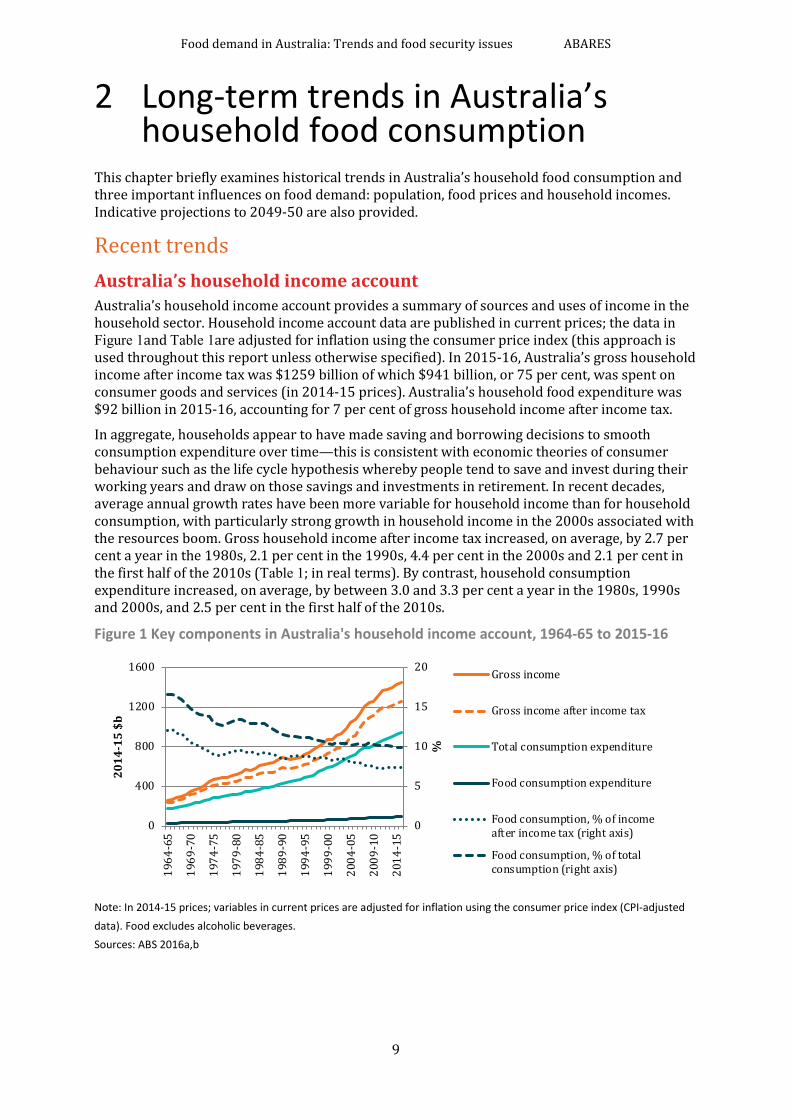

Recent trends Australia’s household income account Australia’s household income account provides a summary of sources and uses of income in the household sector. Household income account data are published in current prices; the data in Figure 1and Table 1are adjusted for inflation using the consumer price index (this approach is used throughout this report unless otherwise specified). In 2015-16, Australia’s gross household income after income tax was $1259 billion of which $941 billion, or 75 per cent, was spent on consumer goods and services (in 2014-15 prices). Australia’s household food expenditure was $92 billion in 2015-16, accounting for 7 per cent of gross household income after income tax.

In aggregate, households appear to have made saving and borrowing decisions to smooth consumption expenditure over time—this is consistent with economic theories of consumer behaviour such as the life cycle hypothesis whereby people tend to save and invest during their working years and draw on those savings and investments in retirement. In recent decades, average annual growth rates have been more variable for household income than for household consumption, with particularly strong growth in household income in the 2000s associated with the resources boom. Gross household income after income tax increased, on average, by 2.7 per cent a year in the 1980s, 2.1 per cent in the 1990s, 4.4 per cent in the 2000s and 2.1 per cent in the first half of the 2010s (Table 1; in real terms). By contrast, household consumption expenditure increased, on average, by between 3.0 and 3.3 per cent a year in the 1980s, 1990s and 2000s, and 2.5 per cent in the first half of the 2010s.

Figure 1 Key components in Australia's household income account, 1964-65 to 2015-16

Note: In 2014-15 prices; variables in current prices are adjusted for inflation using the consumer price index (CPI-adjusted data). Food excludes alcoholic beverages. Sources: ABS 2016a,b

0

5

10

15

20

0

400

800

1200

1600

1964

-65

1969

-70

1974

-75

1979

-80

1984

-85

1989

-90

1994

-95

1999

-00

2004

-05

2009

-10

2014

-15

%

2014

-15

$b

Gross income

Gross income after income tax

Total consumption expenditure

Food consumption expenditure

Food consumption, % of incomeafter income tax (right axis)

Food consumption, % of totalconsumption (right axis)

Food demand in Australia: Trends and food security issues ABARES

10

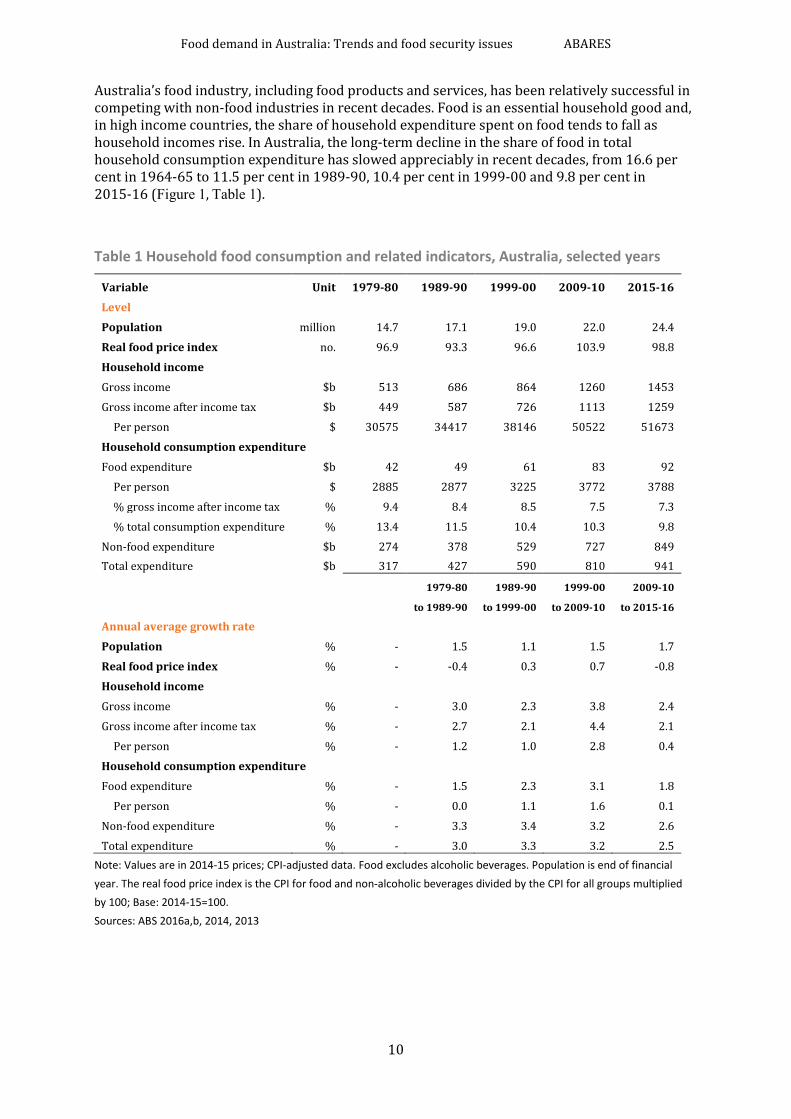

Australia’s food industry, including food products and services, has been relatively successful in competing with non-food industries in recent decades. Food is an essential household good and, in high income countries, the share of household expenditure spent on food tends to fall as household incomes rise. In Australia, the long-term decline in the share of food in total household consumption expenditure has slowed appreciably in recent decades, from 16.6 per cent in 1964-65 to 11.5 per cent in 1989-90, 10.4 per cent in 1999-00 and 9.8 per cent in 2015-16 (Figure 1, Table 1).

Table 1 Household food consumption and related indicators, Australia, selected years

Variable Unit 1979-80 1989-90 1999-00 2009-10 2015-16 Level Population million 14.7 17.1 19.0 22.0 24.4 Real food price index no. 96.9 93.3 96.6 103.9 98.8 Household income Gross income $b 513 686 864 1260 1453 Gross income after income tax $b 449 587 726 1113 1259

Per person $ 30575 34417 38146 50522 51673 Household consumption expenditure Food expenditure $b 42 49 61 83 92

Per person $ 2885 2877 3225 3772 3788 % gross income after income tax % 9.4 8.4 8.5 7.5 7.3 % total consumption expenditure % 13.4 11.5 10.4 10.3 9.8

Non-food expenditure $b 274 378 529 727 849 Total expenditure $b 317 427 590 810 941

1979-80 1989-90 1999-00 2009-10

to 1989-90 to 1999-00 to 2009-10 to 2015-16

Annual average growth rate Population % - 1.5 1.1 1.5 1.7 Real food price index % - -0.4 0.3 0.7 -0.8 Household income Gross income % - 3.0 2.3 3.8 2.4 Gross income after income tax % - 2.7 2.1 4.4 2.1

Per person % - 1.2 1.0 2.8 0.4 Household consumption expenditure Food expenditure % - 1.5 2.3 3.1 1.8

Per person % - 0.0 1.1 1.6 0.1 Non-food expenditure % - 3.3 3.4 3.2 2.6 Total expenditure % - 3.0 3.3 3.2 2.5

Note: Values are in 2014-15 prices; CPI-adjusted data. Food excludes alcoholic beverages. Population is end of financial year. The real food price index is the CPI for food and non-alcoholic beverages divided by the CPI for all groups multiplied by 100; Base: 2014-15=100. Sources: ABS 2016a,b, 2014, 2013

Food demand in Australia: Trends and food security issues ABARES

11

Food demand and consumption The terms food demand and food consumption are often used interchangeably but, from an economic perspective, it can be useful to distinguish between these terms. Food consumption is the market outcome based on demand and supply conditions, including international trade. The food demand curve, also referred to as the marginal benefit curve, indicates the willingness of consumers to pay for an additional quantity of food. Consumers are assumed to demand food provided the price does not exceed the marginal benefit of purchasing the food.

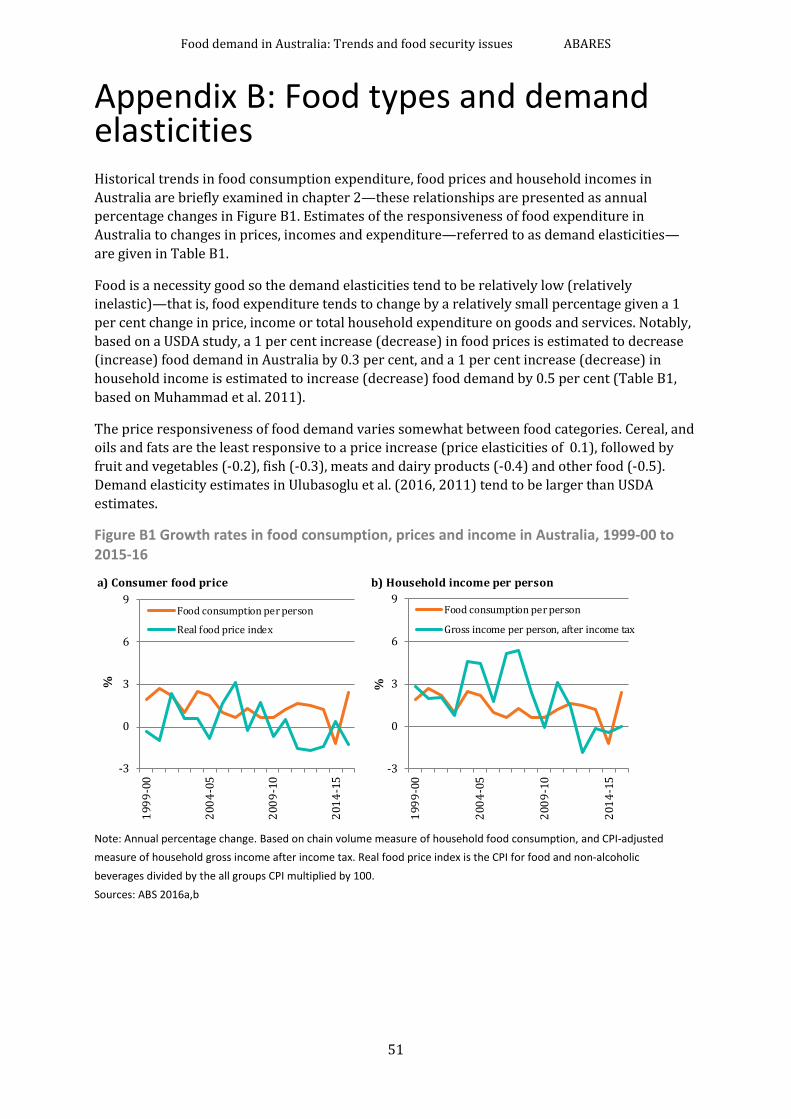

At a minimum, food is required to meet the basic nutrition and energy needs of people. Food demand is influenced by factors such as the population, household income, food prices, food quality, and consumer tastes and preferences (including lifestyle choices). Estimates of the responsiveness of food demand in Australia to changes in price, income and expenditure—referred to as food demand elasticities—are presented in appendix B. For example, a USDA study provides food demand elasticity estimates for Australia (Muhammad et al. 2011).

• Price elasticity of demand—measures the percentage change in demand for a good when the real price of the good increases by 1 per cent (all else constant); for example, demand for food, beverages and tobacco in Australia is estimated to fall (rise) by 0.3 per cent if the real price increases (decreases) by 1 per cent.

• Income elasticity of demand—measures the percentage change in demand for a good when real consumer income increases by 1 per cent (all else constant); for example, demand for food, beverages and tobacco in Australia is estimated to increase by 0.5 per cent if real income increases by 1 per cent.

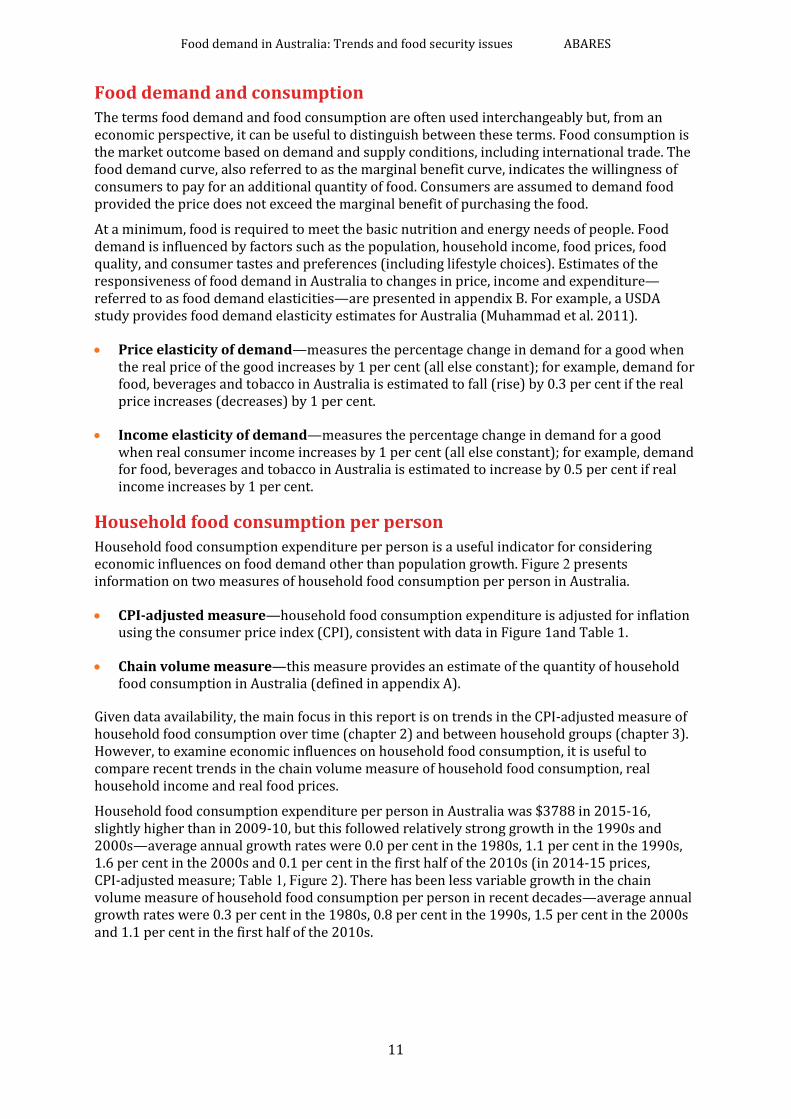

Household food consumption per person Household food consumption expenditure per person is a useful indicator for considering economic influences on food demand other than population growth. Figure 2 presents information on two measures of household food consumption per person in Australia.

• CPI-adjusted measure—household food consumption expenditure is adjusted for inflation using the consumer price index (CPI), consistent with data in Figure 1and Table 1.

• Chain volume measure—this measure provides an estimate of the quantity of household food consumption in Australia (defined in appendix A).

Given data availability, the main focus in this report is on trends in the CPI-adjusted measure of household food consumption over time (chapter 2) and between household groups (chapter 3). However, to examine economic influences on household food consumption, it is useful to compare recent trends in the chain volume measure of household food consumption, real household income and real food prices.

Household food consumption expenditure per person in Australia was $3788 in 2015-16, slightly higher than in 2009-10, but this followed relatively strong growth in the 1990s and 2000s—average annual growth rates were 0.0 per cent in the 1980s, 1.1 per cent in the 1990s, 1.6 per cent in the 2000s and 0.1 per cent in the first half of the 2010s (in 2014-15 prices, CPI-adjusted measure; Table 1, Figure 2). There has been less variable growth in the chain volume measure of household food consumption per person in recent decades—average annual growth rates were 0.3 per cent in the 1980s, 0.8 per cent in the 1990s, 1.5 per cent in the 2000s and 1.1 per cent in the first half of the 2010s.

Food demand in Australia: Trends and food security issues ABARES

12

Figure 2 Household food consumption expenditure per person in Australia, 1964-65 to 2015-16

Note: In 2014-15 prices. Chain volume measure reference year is 2014-15, Sources: ABS 2016a,b

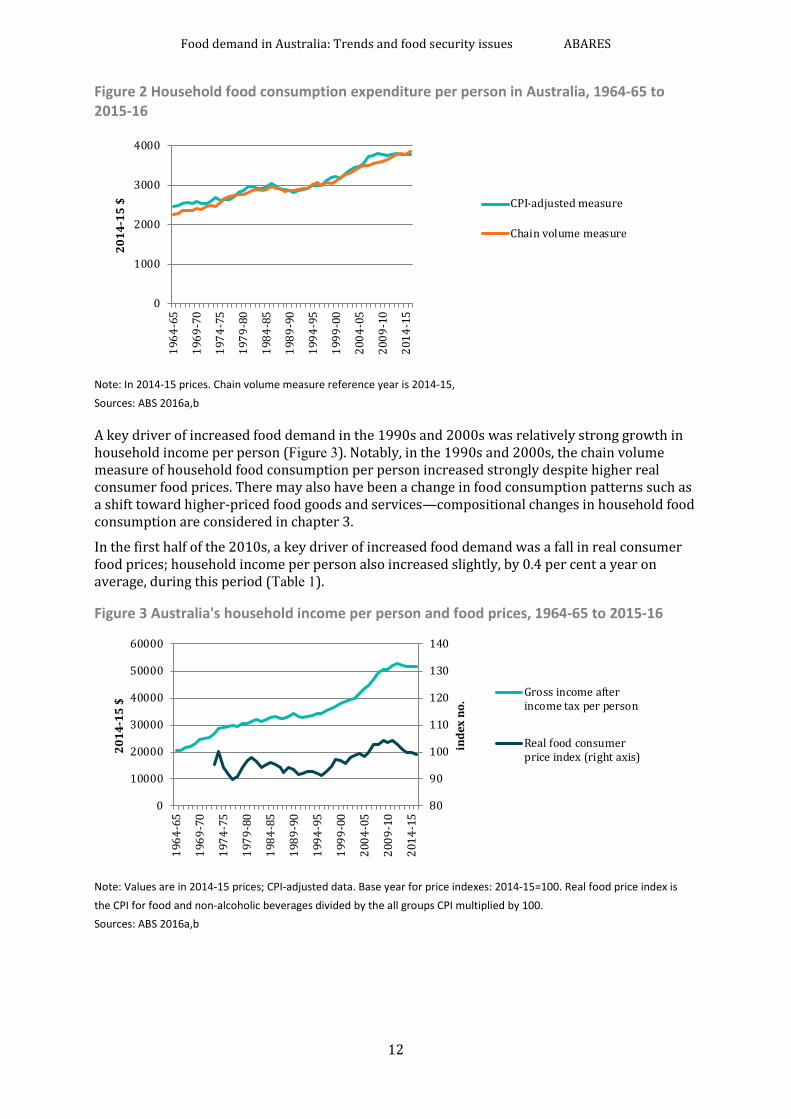

A key driver of increased food demand in the 1990s and 2000s was relatively strong growth in household income per person (Figure 3). Notably, in the 1990s and 2000s, the chain volume measure of household food consumption per person increased strongly despite higher real consumer food prices. There may also have been a change in food consumption patterns such as a shift toward higher-priced food goods and services—compositional changes in household food consumption are considered in chapter 3.

In the first half of the 2010s, a key driver of increased food demand was a fall in real consumer food prices; household income per person also increased slightly, by 0.4 per cent a year on average, during this period (Table 1).

Figure 3 Australia's household income per person and food prices, 1964-65 to 2015-16

Note: Values are in 2014-15 prices; CPI-adjusted data. Base year for price indexes: 2014-15=100. Real food price index is the CPI for food and non-alcoholic beverages divided by the all groups CPI multiplied by 100. Sources: ABS 2016a,b

0

1000

2000

3000

4000

1964

-65

1969

-70

1974

-75

1979

-80

1984

-85

1989

-90

1994

-95

1999

-00

2004

-05

2009

-10

2014

-15

2014

-15

$ CPI-adjusted measure

Chain volume measure

80

90

100

110

120

130

140

0

10000

20000

30000

40000

50000

60000

1964

-65

1969

-70

1974

-75

1979

-80

1984

-85

1989

-90

1994

-95

1999

-00

2004

-05

2009

-10

2014

-15

inde

x no

.

2014

-15

$

Gross income afterincome tax per person

Real food consumerprice index (right axis)

Food demand in Australia: Trends and food security issues ABARES

13

Indicative projections to 2049-50 Assumptions Indicative projections of household food consumption expenditure in Australia are derived from a range of assumptions for growth in Australia’s population and household food consumption expenditure per person. Population projections are from the Australian Bureau of Statistics (ABS)—between 2015-16 and 2049-50, Australia’s population is projected to increase, on average, by 1.0 per cent a year in the low case, 1.3 per cent in the medium case and 1.6 per cent in the high case (Table 2).

Food consumption expenditure per person is assumed to increase, on average, by 0.0, 0.5 and 1.0 per cent a year in low, medium and high cases, respectively (Figure 4a). This range is broadly representative of the range of outcomes in the 1980s, 1990s and first half of the 2010s. It is assumed the strong growth rates of the 2000s are not sustainable over several decades.

Table 2 Household food consumption in Australia: assumptions to 2049-50

Variable Unit 2015-16 2049-50

Low case Medium case High case ABS population projections million 20.5 34.3 37.6 41.9 Growth rate % - 1.5 1.8 2.1 Food consumption expenditure per person $ 3788 3800 4500 5300 Growth rate % - 0.0 0.5 1.0

Note: Values are in 2014-15 prices; CPI-adjusted data. Average annual growth rate between 2015-16 and 2049-50. Projections for household food consumption expenditure per person are rounded to the closest $100. Sources: ABS 2016a,b, 2014, 2013

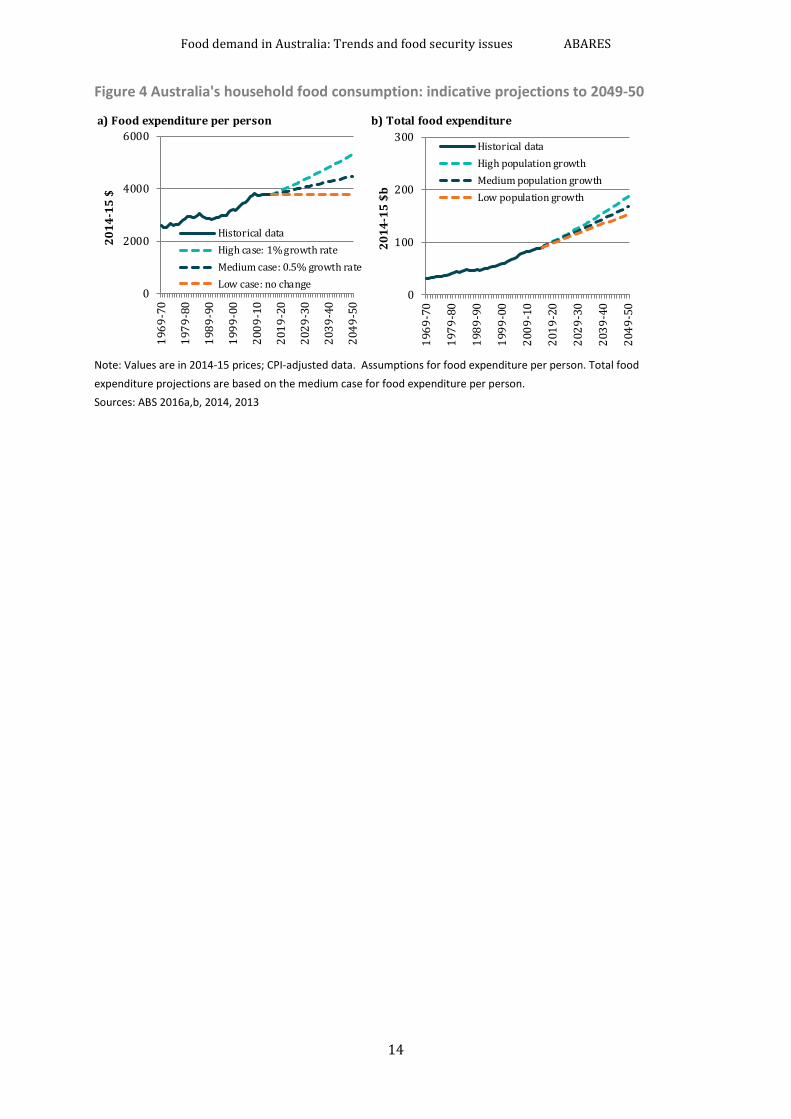

Australia’s household food consumption to 2049-50 Indicative projections of Australia’s household food consumption expenditure to 2049-50 are presented in Table 3, based on the assumptions in Table 2. Even with no further growth in food consumption per person, total household food consumption will increase as Australia’s population increases (all else constant). If household food consumption expenditure per person is assumed to increase by 0.5 per cent a year (medium case), total household food consumption expenditure in Australia is projected to increase from $92 billion in 2015-16 to between $154 billion and $188 billion in 2049-50 (in 2014-15 prices; Figure 4b).

Table 3 Household food consumption in Australia: indicative projections to 2049-50

Assumption Unit 2015-16 ABS population projections, 2049-50

Low case Medium case High case Low case: no change Total food expenditure $b 92 130 142 159 Growth rate % - 1.0 1.3 1.6 Medium case: 0.5% growth rate Total food expenditure $b 92 154 169 188 Growth rate % - 1.5 1.8 2.1 High case: 1% growth rate Total food expenditure $b 92 183 200 223 Growth rate % - 2.0 2.3 2.6

Note: Values are in 2014-15 prices; CPI-adjusted data. Average annual growth rate between 2015-16 and 2049-50. Sources: ABS 2016a,b, 2014, 2013

Food demand in Australia: Trends and food security issues ABARES

14

Figure 4 Australia's household food consumption: indicative projections to 2049-50

Note: Values are in 2014-15 prices; CPI-adjusted data. Assumptions for food expenditure per person. Total food expenditure projections are based on the medium case for food expenditure per person. Sources: ABS 2016a,b, 2014, 2013

a) Food expenditure per person b) Total food expenditure

0

100

200

300

1969

-70

1979

-80

1989

-90

1999

-00

2009

-10

2019

-20

2029

-30

2039

-40

2049

-50

2014

-15

$b

Historical dataHigh population growthMedium population growthLow population growth

0

2000

4000

6000

1969

-70

1979

-80

1989

-90

1999

-00

2009

-10

2019

-20

2029

-30

2039

-40

2049

-50

2014

-15

$

Historical dataHigh case: 1% growth rateMedium case: 0.5% growth rateLow case: no change

Food demand in Australia: Trends and food security issues ABARES

15

3 Household characteristics and food expenditure in Australia

This chapter uses ABS household expenditure survey (HES) data to briefly examine trends in Australia’s household food expenditure both over time and in more detail in 2009-10. Three influences on food demand in 2009-10 are considered: household income, household net worth and age of household reference person.

Recent trends The ABS regularly conducts a survey of individual households in Australia to ‘collect detailed information about the expenditure, income, assets, liabilities and household characteristics of households resident in private dwellings throughout Australia’ (ABS 2011, p.60). HES data may be used to compare expenditure patterns and household characteristics between population subgroups such as low and high income earners.

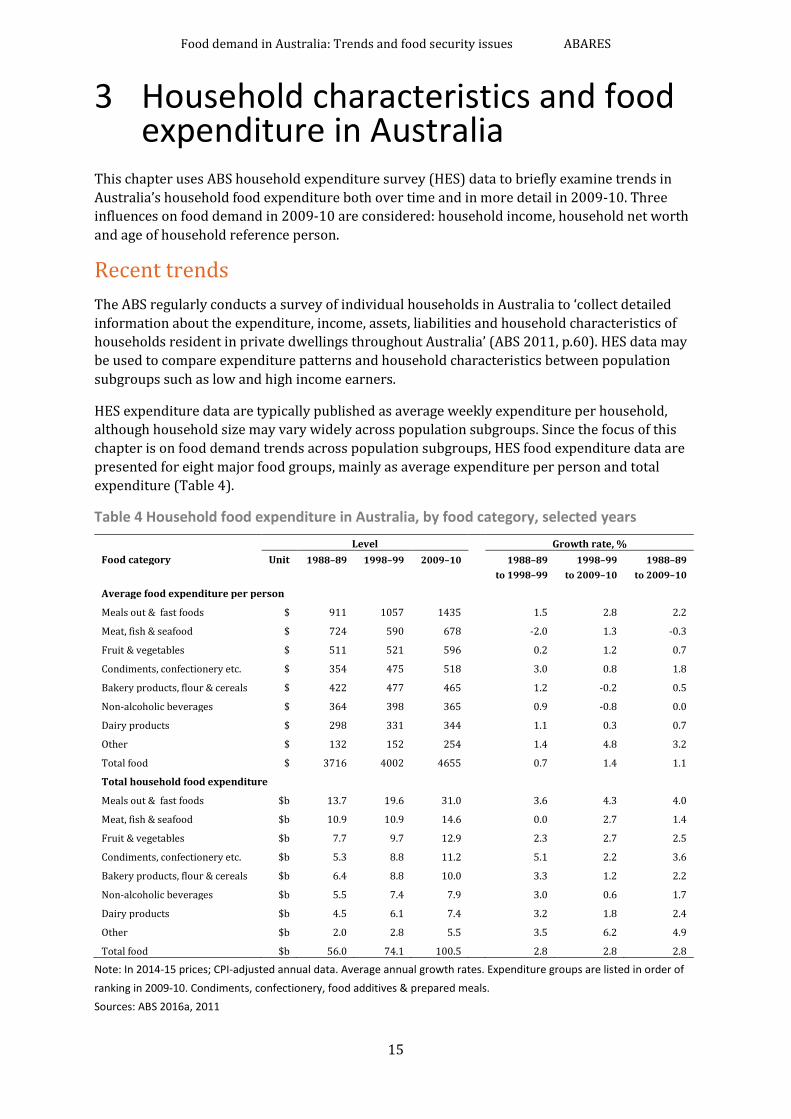

HES expenditure data are typically published as average weekly expenditure per household, although household size may vary widely across population subgroups. Since the focus of this chapter is on food demand trends across population subgroups, HES food expenditure data are presented for eight major food groups, mainly as average expenditure per person and total expenditure (Table 4).

Table 4 Household food expenditure in Australia, by food category, selected years

Level Growth rate, % Food category Unit 1988–89 1998–99 2009–10 1988–89 1998–99 1988–89

to 1998–99 to 2009–10 to 2009–10

Average food expenditure per person

Meals out & fast foods $ 911 1057 1435 1.5 2.8 2.2

Meat, fish & seafood $ 724 590 678 -2.0 1.3 -0.3

Fruit & vegetables $ 511 521 596 0.2 1.2 0.7

Condiments, confectionery etc. $ 354 475 518 3.0 0.8 1.8

Bakery products, flour & cereals $ 422 477 465 1.2 -0.2 0.5

Non-alcoholic beverages $ 364 398 365 0.9 -0.8 0.0

Dairy products $ 298 331 344 1.1 0.3 0.7

Other $ 132 152 254 1.4 4.8 3.2

Total food $ 3716 4002 4655 0.7 1.4 1.1

Total household food expenditure

Meals out & fast foods $b 13.7 19.6 31.0 3.6 4.3 4.0

Meat, fish & seafood $b 10.9 10.9 14.6 0.0 2.7 1.4

Fruit & vegetables $b 7.7 9.7 12.9 2.3 2.7 2.5

Condiments, confectionery etc. $b 5.3 8.8 11.2 5.1 2.2 3.6

Bakery products, flour & cereals $b 6.4 8.8 10.0 3.3 1.2 2.2

Non-alcoholic beverages $b 5.5 7.4 7.9 3.0 0.6 1.7

Dairy products $b 4.5 6.1 7.4 3.2 1.8 2.4

Other $b 2.0 2.8 5.5 3.5 6.2 4.9

Total food $b 56.0 74.1 100.5 2.8 2.8 2.8

Note: In 2014-15 prices; CPI-adjusted annual data. Average annual growth rates. Expenditure groups are listed in order of ranking in 2009-10. Condiments, confectionery, food additives & prepared meals. Sources: ABS 2016a, 2011

Food demand in Australia: Trends and food security issues ABARES

16

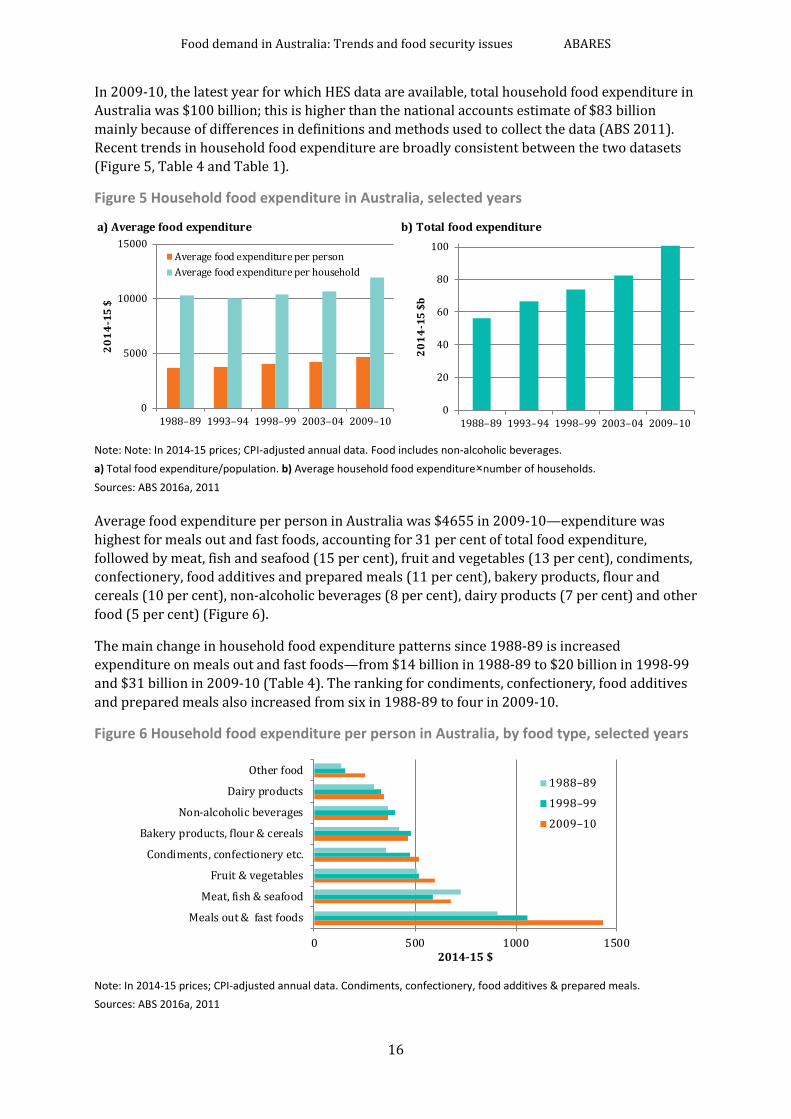

In 2009-10, the latest year for which HES data are available, total household food expenditure in Australia was $100 billion; this is higher than the national accounts estimate of $83 billion mainly because of differences in definitions and methods used to collect the data (ABS 2011). Recent trends in household food expenditure are broadly consistent between the two datasets (Figure 5, Table 4 and Table 1).

Figure 5 Household food expenditure in Australia, selected years

Note: Note: In 2014-15 prices; CPI-adjusted annual data. Food includes non-alcoholic beverages. a) Total food expenditure/population. b) Average household food expenditurenumber of households. Sources: ABS 2016a, 2011

Average food expenditure per person in Australia was $4655 in 2009-10—expenditure was highest for meals out and fast foods, accounting for 31 per cent of total food expenditure, followed by meat, fish and seafood (15 per cent), fruit and vegetables (13 per cent), condiments, confectionery, food additives and prepared meals (11 per cent), bakery products, flour and cereals (10 per cent), non-alcoholic beverages (8 per cent), dairy products (7 per cent) and other food (5 per cent) (Figure 6).

The main change in household food expenditure patterns since 1988-89 is increased expenditure on meals out and fast foods—from $14 billion in 1988-89 to $20 billion in 1998-99 and $31 billion in 2009-10 (Table 4). The ranking for condiments, confectionery, food additives and prepared meals also increased from six in 1988-89 to four in 2009-10.

Figure 6 Household food expenditure per person in Australia, by food type, selected years

Note: In 2014-15 prices; CPI-adjusted annual data. Condiments, confectionery, food additives & prepared meals. Sources: ABS 2016a, 2011

a) Average food expenditure b) Total food expenditure

0

20

40

60

80

100

1988–89 1993–94 1998–99 2003–04 2009–1020

14-1

5 $b

0

5000

10000

15000

1988–89 1993–94 1998–99 2003–04 2009–10

2014

-15

$

Average food expenditure per personAverage food expenditure per household

0 500 1000 1500

Meals out & fast foods

Meat, fish & seafood

Fruit & vegetables

Condiments, confectionery etc.

Bakery products, flour & cereals

Non-alcoholic beverages

Dairy products

Other food

2014-15 $

1988–89

1998–99

2009–10

Food demand in Australia: Trends and food security issues ABARES

17

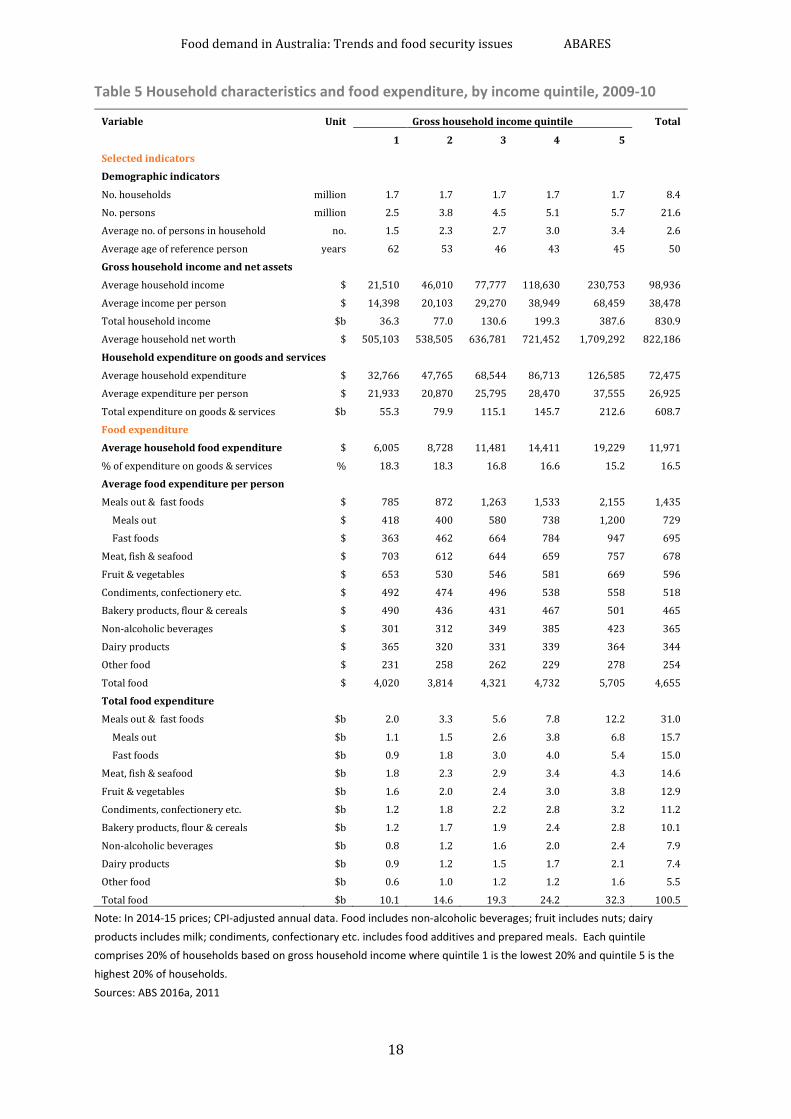

Household food expenditure by income quintile: 2009-10 Information on food expenditure and selected household characteristics in 2009-10 is presented in Figure 7 and Table 5 where households are divided into five groups based on gross household income. These groups are referred to as quintiles where, for example, quintile 1 includes the 20 per cent of households with the lowest gross household income.

In 2009-10, average food expenditure per household ranged from $6005 in the lowest income group (quintile 1) to $19220 in the highest income group (quintile 5; in 2014-15 prices). The average household size increases with income quintile, from 1.5 people in the lowest income group to 3.4 people in the highest income group. Adjusting for household size reduces the expenditure difference between the lowest and highest income groups—in 2009-10, average food expenditure per person ranged from $4020 in quintile 1 and $3814 in quintile 2 to $5705 in quintile 5 (Figure 7a).

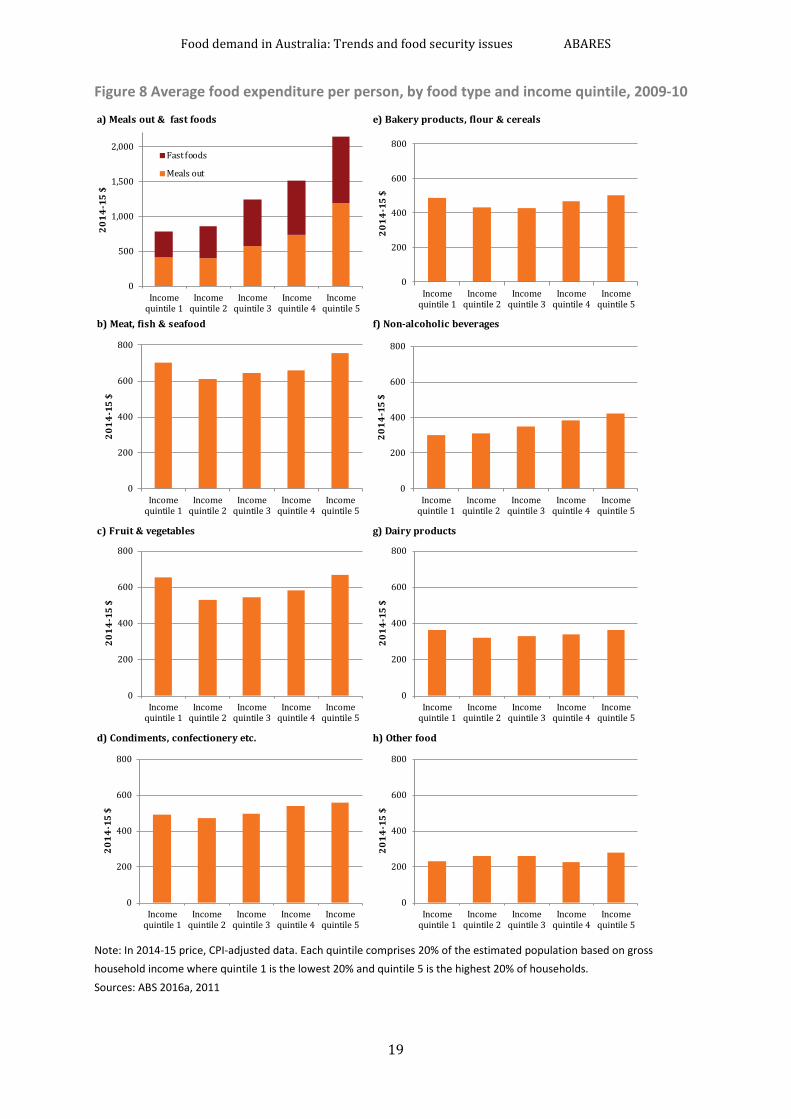

Of the eight food groups, the main difference between income groups is expenditure on meals out and fast foods—average expenditure per person ranged from $785 in the lowest income group to $2155 in the highest income group (Table 5, Figure 8).

Based on food expenditure patterns and other information for the lowest income group, there is likely to be a significant number of people in this group who are older, more likely to purchase food for cooking at home, and who are drawing on net assets accumulated through their working lives to maintain living standards. For five of the eight food groups, average expenditure per person was higher in the lowest income group than in the second lowest income group. Average expenditure per person in the lowest income group was the highest of all income groups for dairy products, and the second highest for meat, fish and seafood, fruit and vegetables, and bakery products, flour and cereals. Food expenditure patterns across household net wealth groups are considered in the next section.

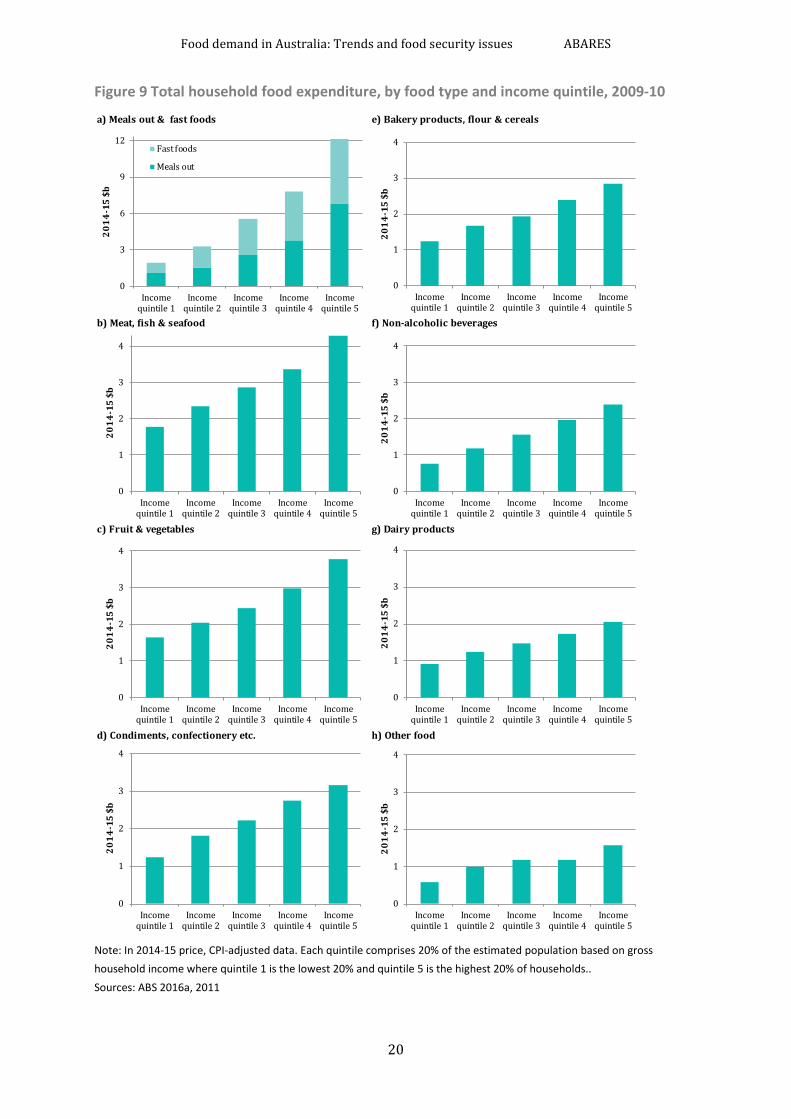

As a result of higher food expenditure per person and/or larger household size, total food expenditure increased consistently across income groups in aggregate (Figure 7b) and for each of the eight food groups (Figure 9). Total food expenditure ranged from $10 billion in the lowest income group to $32 billion in the highest income group (Table 4).

Figure 7 Household food expenditure in Australia, by income quintile, 2009-10

Note: In 2014-15 prices; CPI-adjusted annual data. Each quintile comprises 20% of households based on gross household income where quintile 1 is the lowest 20% and quintile 5 is the highest 20% of households. Sources: ABS 2016a, 2011

a) Average food expenditure b) Total food expenditure

0

10

20

30

Incomequintile 1

Incomequintile 2

Incomequintile 3

Incomequintile 4

Incomequintile 5

2014

-15

$b

0

100 00

200 00

300 00

0

200 0

400 0

600 0

Incomequintile 1

Incomequintile 2

Incomequintile 3

Incomequintile 4

Incomequintile 5

2014

-15

$

2014

-15

$

Per person

Per household (right axis)

Food demand in Australia: Trends and food security issues ABARES

18

Table 5 Household characteristics and food expenditure, by income quintile, 2009-10

Variable Unit Gross household income quintile Total

1 2 3 4 5 Selected indicators

Demographic indicators

No. households million 1.7 1.7 1.7 1.7 1.7 8.4

No. persons million 2.5 3.8 4.5 5.1 5.7 21.6

Average no. of persons in household no. 1.5 2.3 2.7 3.0 3.4 2.6

Average age of reference person years 62 53 46 43 45 50

Gross household income and net assets

Average household income $ 21,510 46,010 77,777 118,630 230,753 98,936

Average income per person $ 14,398 20,103 29,270 38,949 68,459 38,478

Total household income $b 36.3 77.0 130.6 199.3 387.6 830.9

Average household net worth $ 505,103 538,505 636,781 721,452 1,709,292 822,186

Household expenditure on goods and services

Average household expenditure $ 32,766 47,765 68,544 86,713 126,585 72,475

Average expenditure per person $ 21,933 20,870 25,795 28,470 37,555 26,925

Total expenditure on goods & services $b 55.3 79.9 115.1 145.7 212.6 608.7

Food expenditure

Average household food expenditure $ 6,005 8,728 11,481 14,411 19,229 11,971

% of expenditure on goods & services % 18.3 18.3 16.8 16.6 15.2 16.5

Average food expenditure per person

Meals out & fast foods $ 785 872 1,263 1,533 2,155 1,435

Meals out $ 418 400 580 738 1,200 729

Fast foods $ 363 462 664 784 947 695

Meat, fish & seafood $ 703 612 644 659 757 678

Fruit & vegetables $ 653 530 546 581 669 596

Condiments, confectionery etc. $ 492 474 496 538 558 518

Bakery products, flour & cereals $ 490 436 431 467 501 465

Non-alcoholic beverages $ 301 312 349 385 423 365

Dairy products $ 365 320 331 339 364 344

Other food $ 231 258 262 229 278 254

Total food $ 4,020 3,814 4,321 4,732 5,705 4,655

Total food expenditure

Meals out & fast foods $b 2.0 3.3 5.6 7.8 12.2 31.0

Meals out $b 1.1 1.5 2.6 3.8 6.8 15.7

Fast foods $b 0.9 1.8 3.0 4.0 5.4 15.0

Meat, fish & seafood $b 1.8 2.3 2.9 3.4 4.3 14.6

Fruit & vegetables $b 1.6 2.0 2.4 3.0 3.8 12.9

Condiments, confectionery etc. $b 1.2 1.8 2.2 2.8 3.2 11.2

Bakery products, flour & cereals $b 1.2 1.7 1.9 2.4 2.8 10.1

Non-alcoholic beverages $b 0.8 1.2 1.6 2.0 2.4 7.9

Dairy products $b 0.9 1.2 1.5 1.7 2.1 7.4

Other food $b 0.6 1.0 1.2 1.2 1.6 5.5

Total food $b 10.1 14.6 19.3 24.2 32.3 100.5

Note: In 2014-15 prices; CPI-adjusted annual data. Food includes non-alcoholic beverages; fruit includes nuts; dairy products includes milk; condiments, confectionary etc. includes food additives and prepared meals. Each quintile comprises 20% of households based on gross household income where quintile 1 is the lowest 20% and quintile 5 is the highest 20% of households. Sources: ABS 2016a, 2011

Food demand in Australia: Trends and food security issues ABARES

19

Figure 8 Average food expenditure per person, by food type and income quintile, 2009-10

Note: In 2014-15 price, CPI-adjusted data. Each quintile comprises 20% of the estimated population based on gross household income where quintile 1 is the lowest 20% and quintile 5 is the highest 20% of households. Sources: ABS 2016a, 2011

a) Meals out & fast foods e) Bakery products, flour & cereals

b) Meat, fish & seafood f) Non-alcoholic beverages

c) Fruit & vegetables g) Dairy products

d) Condiments, confectionery etc. h) Other food

0

500

1,000

1,500

2,000

Incomequintile 1

Incomequintile 2

Incomequintile 3

Incomequintile 4

Incomequintile 5

2014

-15

$

Fast foods

Meals out

0

200

400

600

800

Incomequintile 1

Incomequintile 2

Incomequintile 3

Incomequintile 4

Incomequintile 5

2014

-15

$

0

200

400

600

800

Incomequintile 1

Incomequintile 2

Incomequintile 3

Incomequintile 4

Incomequintile 5

2014

-15

$

0

200

400

600

800

Incomequintile 1

Incomequintile 2

Incomequintile 3

Incomequintile 4

Incomequintile 5

2014

-15

$

0

200

400

600

800

Incomequintile 1

Incomequintile 2

Incomequintile 3

Incomequintile 4

Incomequintile 5

2014

-15

$

0

200

400

600

800

Incomequintile 1

Incomequintile 2

Incomequintile 3

Incomequintile 4

Incomequintile 5

2014

-15

$

0

200

400

600

800

Incomequintile 1

Incomequintile 2

Incomequintile 3

Incomequintile 4

Incomequintile 5

2014

-15

$

0

200

400

600

800

Incomequintile 1

Incomequintile 2

Incomequintile 3

Incomequintile 4

Incomequintile 5

2014

-15

$

Food demand in Australia: Trends and food security issues ABARES

20

Figure 9 Total household food expenditure, by food type and income quintile, 2009-10

Note: In 2014-15 price, CPI-adjusted data. Each quintile comprises 20% of the estimated population based on gross household income where quintile 1 is the lowest 20% and quintile 5 is the highest 20% of households.. Sources: ABS 2016a, 2011

a) Meals out & fast foods e) Bakery products, flour & cereals

b) Meat, fish & seafood f) Non-alcoholic beverages

c) Fruit & vegetables g) Dairy products

d) Condiments, confectionery etc. h) Other food

0

1

2

3

4

Incomequintile 1

Incomequintile 2

Incomequintile 3

Incomequintile 4

Incomequintile 5

2014

-15

$b

0

1

2

3

4

Incomequintile 1

Incomequintile 2

Incomequintile 3

Incomequintile 4

Incomequintile 5

2014

-15

$b

0

1

2

3

4

Incomequintile 1

Incomequintile 2

Incomequintile 3

Incomequintile 4

Incomequintile 5

2014

-15

$b

0

1

2

3

4

Incomequintile 1

Incomequintile 2

Incomequintile 3

Incomequintile 4

Incomequintile 5

2014

-15

$b

0

1

2

3

4

Incomequintile 1

Incomequintile 2

Incomequintile 3

Incomequintile 4

Incomequintile 5

2014

-15

$b

0

1

2

3

4

Incomequintile 1

Incomequintile 2

Incomequintile 3

Incomequintile 4

Incomequintile 5

2014

-15

$b

0

1

2

3

4

Incomequintile 1

Incomequintile 2

Incomequintile 3

Incomequintile 4

Incomequintile 5

2014

-15

$b

0

3

6

9

12

Incomequintile 1

Incomequintile 2

Incomequintile 3

Incomequintile 4

Incomequintile 5

2014

-15

$b

Fast foods

Meals out

Food demand in Australia: Trends and food security issues ABARES

21

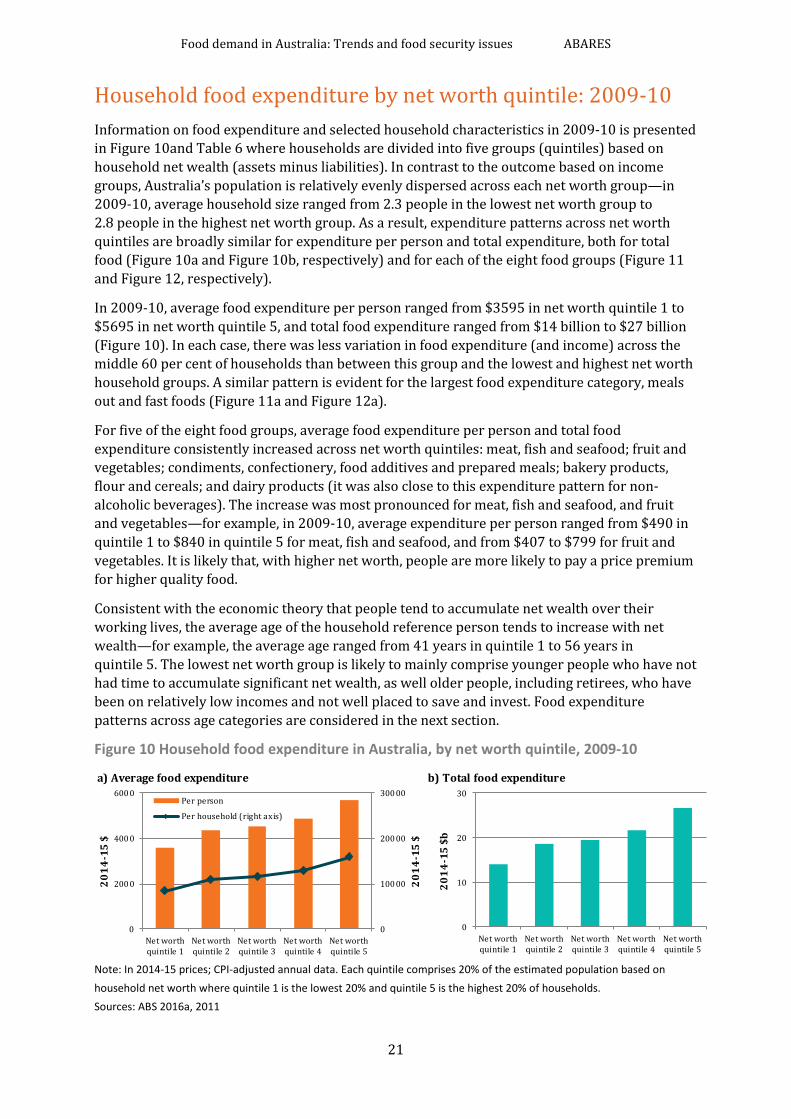

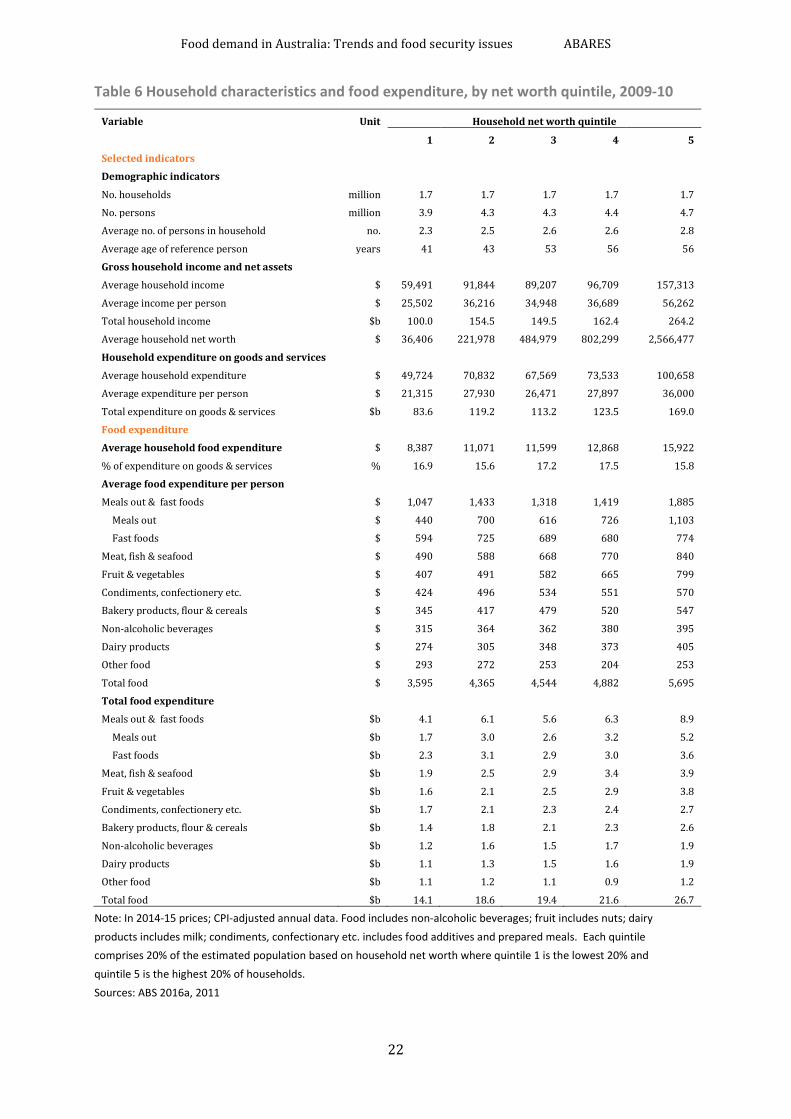

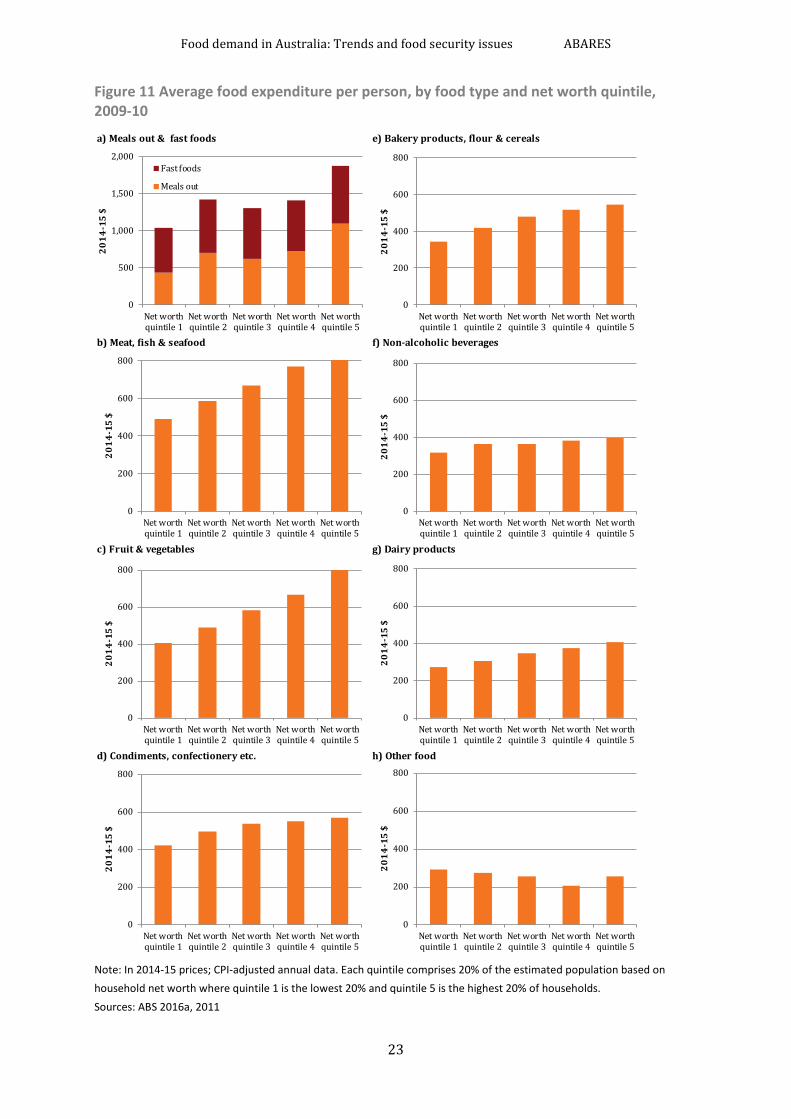

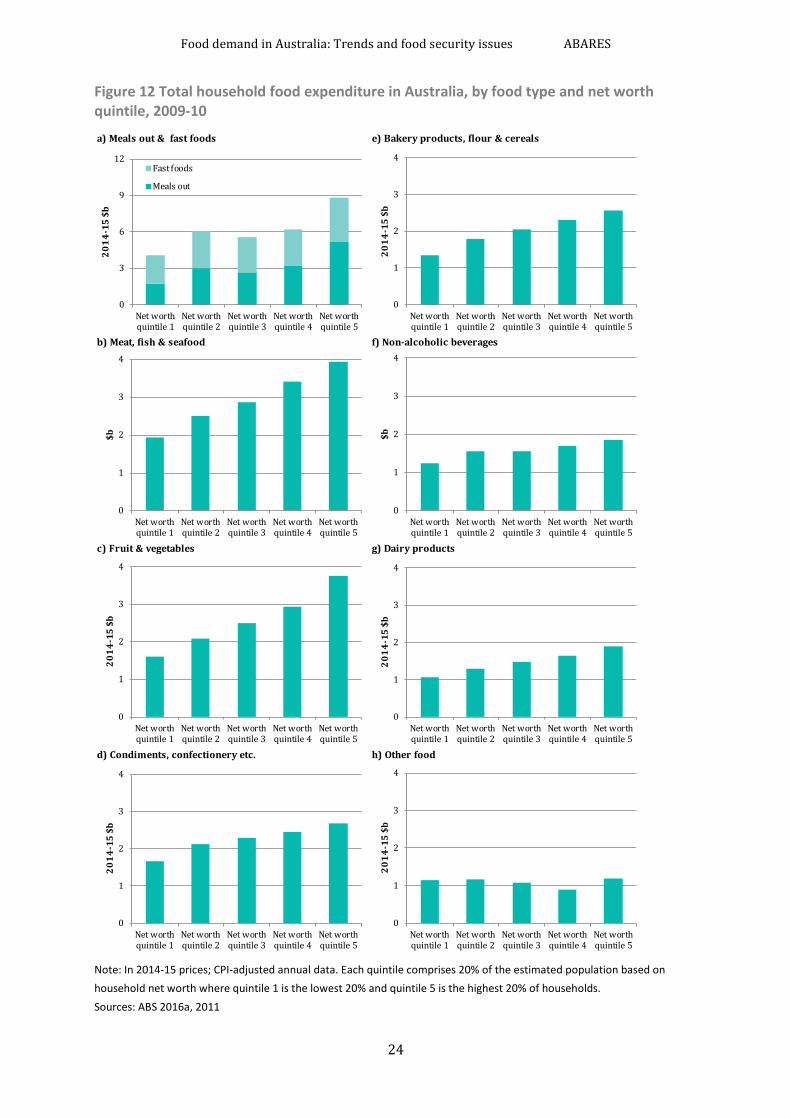

Household food expenditure by net worth quintile: 2009-10 Information on food expenditure and selected household characteristics in 2009-10 is presented in Figure 10and Table 6 where households are divided into five groups (quintiles) based on household net wealth (assets minus liabilities). In contrast to the outcome based on income groups, Australia’s population is relatively evenly dispersed across each net worth group—in 2009-10, average household size ranged from 2.3 people in the lowest net worth group to 2.8 people in the highest net worth group. As a result, expenditure patterns across net worth quintiles are broadly similar for expenditure per person and total expenditure, both for total food (Figure 10a and Figure 10b, respectively) and for each of the eight food groups (Figure 11 and Figure 12, respectively).

In 2009-10, average food expenditure per person ranged from $3595 in net worth quintile 1 to $5695 in net worth quintile 5, and total food expenditure ranged from $14 billion to $27 billion (Figure 10). In each case, there was less variation in food expenditure (and income) across the middle 60 per cent of households than between this group and the lowest and highest net worth household groups. A similar pattern is evident for the largest food expenditure category, meals out and fast foods (Figure 11a and Figure 12a).

For five of the eight food groups, average food expenditure per person and total food expenditure consistently increased across net worth quintiles: meat, fish and seafood; fruit and vegetables; condiments, confectionery, food additives and prepared meals; bakery products, flour and cereals; and dairy products (it was also close to this expenditure pattern for non-alcoholic beverages). The increase was most pronounced for meat, fish and seafood, and fruit and vegetables—for example, in 2009-10, average expenditure per person ranged from $490 in quintile 1 to $840 in quintile 5 for meat, fish and seafood, and from $407 to $799 for fruit and vegetables. It is likely that, with higher net worth, people are more likely to pay a price premium for higher quality food.

Consistent with the economic theory that people tend to accumulate net wealth over their working lives, the average age of the household reference person tends to increase with net wealth—for example, the average age ranged from 41 years in quintile 1 to 56 years in quintile 5. The lowest net worth group is likely to mainly comprise younger people who have not had time to accumulate significant net wealth, as well older people, including retirees, who have been on relatively low incomes and not well placed to save and invest. Food expenditure patterns across age categories are considered in the next section.

Figure 10 Household food expenditure in Australia, by net worth quintile, 2009-10

Note: In 2014-15 prices; CPI-adjusted annual data. Each quintile comprises 20% of the estimated population based on household net worth where quintile 1 is the lowest 20% and quintile 5 is the highest 20% of households. Sources: ABS 2016a, 2011

a) Average food expenditure b) Total food expenditure

0

10

20

30

Net worthquintile 1

Net worthquintile 2

Net worthquintile 3

Net worthquintile 4

Net worthquintile 5

2014

-15

$b

0

100 00

200 00

300 00

0

200 0

400 0

600 0

Net worthquintile 1

Net worthquintile 2

Net worthquintile 3

Net worthquintile 4

Net worthquintile 5

2014

-15

$

2014

-15

$

Per person

Per household (right axis)

Food demand in Australia: Trends and food security issues ABARES

22

Table 6 Household characteristics and food expenditure, by net worth quintile, 2009-10

Variable Unit Household net worth quintile

1 2 3 4 5

Selected indicators

Demographic indicators

No. households million 1.7 1.7 1.7 1.7 1.7

No. persons million 3.9 4.3 4.3 4.4 4.7

Average no. of persons in household no. 2.3 2.5 2.6 2.6 2.8

Average age of reference person years 41 43 53 56 56

Gross household income and net assets

Average household income $ 59,491 91,844 89,207 96,709 157,313

Average income per person $ 25,502 36,216 34,948 36,689 56,262

Total household income $b 100.0 154.5 149.5 162.4 264.2

Average household net worth $ 36,406 221,978 484,979 802,299 2,566,477

Household expenditure on goods and services

Average household expenditure $ 49,724 70,832 67,569 73,533 100,658

Average expenditure per person $ 21,315 27,930 26,471 27,897 36,000

Total expenditure on goods & services $b 83.6 119.2 113.2 123.5 169.0

Food expenditure

Average household food expenditure $ 8,387 11,071 11,599 12,868 15,922

% of expenditure on goods & services % 16.9 15.6 17.2 17.5 15.8

Average food expenditure per person

Meals out & fast foods $ 1,047 1,433 1,318 1,419 1,885

Meals out $ 440 700 616 726 1,103

Fast foods $ 594 725 689 680 774

Meat, fish & seafood $ 490 588 668 770 840

Fruit & vegetables $ 407 491 582 665 799

Condiments, confectionery etc. $ 424 496 534 551 570

Bakery products, flour & cereals $ 345 417 479 520 547

Non-alcoholic beverages $ 315 364 362 380 395

Dairy products $ 274 305 348 373 405

Other food $ 293 272 253 204 253

Total food $ 3,595 4,365 4,544 4,882 5,695

Total food expenditure

Meals out & fast foods $b 4.1 6.1 5.6 6.3 8.9

Meals out $b 1.7 3.0 2.6 3.2 5.2

Fast foods $b 2.3 3.1 2.9 3.0 3.6

Meat, fish & seafood $b 1.9 2.5 2.9 3.4 3.9

Fruit & vegetables $b 1.6 2.1 2.5 2.9 3.8

Condiments, confectionery etc. $b 1.7 2.1 2.3 2.4 2.7

Bakery products, flour & cereals $b 1.4 1.8 2.1 2.3 2.6

Non-alcoholic beverages $b 1.2 1.6 1.5 1.7 1.9

Dairy products $b 1.1 1.3 1.5 1.6 1.9

Other food $b 1.1 1.2 1.1 0.9 1.2

Total food $b 14.1 18.6 19.4 21.6 26.7

Note: In 2014-15 prices; CPI-adjusted annual data. Food includes non-alcoholic beverages; fruit includes nuts; dairy products includes milk; condiments, confectionary etc. includes food additives and prepared meals. Each quintile comprises 20% of the estimated population based on household net worth where quintile 1 is the lowest 20% and quintile 5 is the highest 20% of households. Sources: ABS 2016a, 2011

Food demand in Australia: Trends and food security issues ABARES

23

Figure 11 Average food expenditure per person, by food type and net worth quintile, 2009-10

Note: In 2014-15 prices; CPI-adjusted annual data. Each quintile comprises 20% of the estimated population based on household net worth where quintile 1 is the lowest 20% and quintile 5 is the highest 20% of households. Sources: ABS 2016a, 2011

a) Meals out & fast foods e) Bakery products, flour & cereals

b) Meat, fish & seafood f) Non-alcoholic beverages

c) Fruit & vegetables g) Dairy products

d) Condiments, confectionery etc. h) Other food

0

500

1,000

1,500

2,000

Net worthquintile 1

Net worthquintile 2

Net worthquintile 3

Net worthquintile 4

Net worthquintile 5

2014

-15

$

Fast foods

Meals out

0

200

400

600

800

Net worthquintile 1

Net worthquintile 2

Net worthquintile 3

Net worthquintile 4

Net worthquintile 5

2014

-15

$

0

200

400

600

800

Net worthquintile 1

Net worthquintile 2

Net worthquintile 3

Net worthquintile 4

Net worthquintile 5

2014

-15

$

0

200

400

600

800

Net worthquintile 1

Net worthquintile 2

Net worthquintile 3

Net worthquintile 4

Net worthquintile 5

2014

-15

$

0

200

400

600

800

Net worthquintile 1

Net worthquintile 2

Net worthquintile 3

Net worthquintile 4

Net worthquintile 5

2014

-15

$

0

200

400

600

800

Net worthquintile 1

Net worthquintile 2

Net worthquintile 3

Net worthquintile 4

Net worthquintile 5

2014

-15

$

0

200

400

600

800

Net worthquintile 1

Net worthquintile 2

Net worthquintile 3

Net worthquintile 4

Net worthquintile 5

2014

-15

$

0

200

400

600

800

Net worthquintile 1

Net worthquintile 2

Net worthquintile 3

Net worthquintile 4

Net worthquintile 5

2014

-15

$

Food demand in Australia: Trends and food security issues ABARES

24

Figure 12 Total household food expenditure in Australia, by food type and net worth quintile, 2009-10

Note: In 2014-15 prices; CPI-adjusted annual data. Each quintile comprises 20% of the estimated population based on household net worth where quintile 1 is the lowest 20% and quintile 5 is the highest 20% of households. Sources: ABS 2016a, 2011

a) Meals out & fast foods e) Bakery products, flour & cereals

b) Meat, fish & seafood f) Non-alcoholic beverages

c) Fruit & vegetables g) Dairy products

d) Condiments, confectionery etc. h) Other food

0

3

6

9

12

Net worthquintile 1

Net worthquintile 2

Net worthquintile 3

Net worthquintile 4

Net worthquintile 5

2014

-15

$b

Fast foods

Meals out

0

1

2

3

4

Net worthquintile 1

Net worthquintile 2

Net worthquintile 3

Net worthquintile 4

Net worthquintile 5

2014

-15

$b

0

1

2

3

4

Net worthquintile 1

Net worthquintile 2

Net worthquintile 3

Net worthquintile 4

Net worthquintile 5

2014

-15

$b

0

1

2

3

4

Net worthquintile 1

Net worthquintile 2

Net worthquintile 3

Net worthquintile 4

Net worthquintile 5

$b

0

1

2

3

4

Net worthquintile 1

Net worthquintile 2

Net worthquintile 3

Net worthquintile 4

Net worthquintile 5

2014

-15

$b

0

1

2

3

4

Net worthquintile 1

Net worthquintile 2

Net worthquintile 3

Net worthquintile 4

Net worthquintile 5

$b

0

1

2

3

4

Net worthquintile 1

Net worthquintile 2

Net worthquintile 3

Net worthquintile 4

Net worthquintile 5

2014

-15

$b

0

1

2

3

4

Net worthquintile 1

Net worthquintile 2