for personal use only · 1.refer marketable reserves note (p21), jorc probable reserve (rom) of...

TRANSCRIPT

For

per

sona

l use

onl

y

Quarterly Report for the period ended 31 December 2011

ASX Code: SMR 1

Quarterly Overview The December quarter saw Stanmore Coal make significant progress as results were received and collated from the extensive exploration drilling and project development activities undertaken during 2011.

The results of a Pre‐Feasibility Study (PFS) at The Range were released during the quarter which demonstrated improved project economics and operating parameters. Capital costs have remained within expectations while operating costs have fallen relative to the previous Conceptual Mining Study (CMS). An initial 94Mt Marketable Reserve1 statement was delivered for the deposit which underpins the company’s application for 5Mtpa of capacity at the Wiggins Island Coal Export Terminal (WICET) for this project.

The Range PFS concluded that the mine life would extend to 26 years (up from 18 in the CMS) with a Net Present Value of $846m for the owner mining case. Production of a high quality export thermal coal is planned to commence in 2015 with a ramp up to the full production rate of 5Mtpa shortly thereafter.

During the quarter the company also defined an initial 95Mt JORC Inferred Resource at its Belview underground coking coal project. Early coal quality tests indicate that this coal will be a high quality coking coal with a CSN of 7‐8 and ash of 6‐7%. Further drilling is planned to test the additional 205 – 345Mt Exploration Target2.

An initial 25.7Mt of JORC Indicated Resource was defined at Mackenzie along with a 45% increase in the Total JORC Indicated + Inferred Resource to 143.2Mt. The latest results of an ongoing coal quality program indicate considerable variability in yield across the deposit and optimisation work is underway to address beneficiation and metallurgical issues that have been identified. Drilling and test work will continue to investigate the most likely economic targets within the 27km long project area.

Stanmore Coal continues to work closely with the key infrastructure providers in relation to our application for port and rail capacity. WICET Expansion Phase 1 (WEXP1) is at the short listing phase and the company continues to interact positively with the WICET team about our potential allocation. We understand formal allocation decisions for WEXP1 are scheduled to be made by WICET by the end of the first quarter of 2012. Meanwhile the Surat Basin Rail (SBR) project linking The Range project to Gladstone ports including WICET took a big step forward with the Queensland Government approval of the development scheme for the Surat Basin Infrastructure Corridor State Development Area.

At the end of the quarter Stanmore Coal completed a Placement to institutional and sophisticated investors at $0.74 per share to raise $14.1 million. Subsequent to the end of the quarter a further $10 million equity raising was confirmed from via a placement and Share Purchase Plan offered to existing shareholders at $0.74 per share.

1.Refer Marketable Reserves Note (p21), JORC Probable Reserve (ROM) of 117.5Mt 2. Refer Exploration Target Note (p21)

For

per

sona

l use

onl

y

Quarterly Report for the period ended 31 December 2011

ASX Code: SMR 2

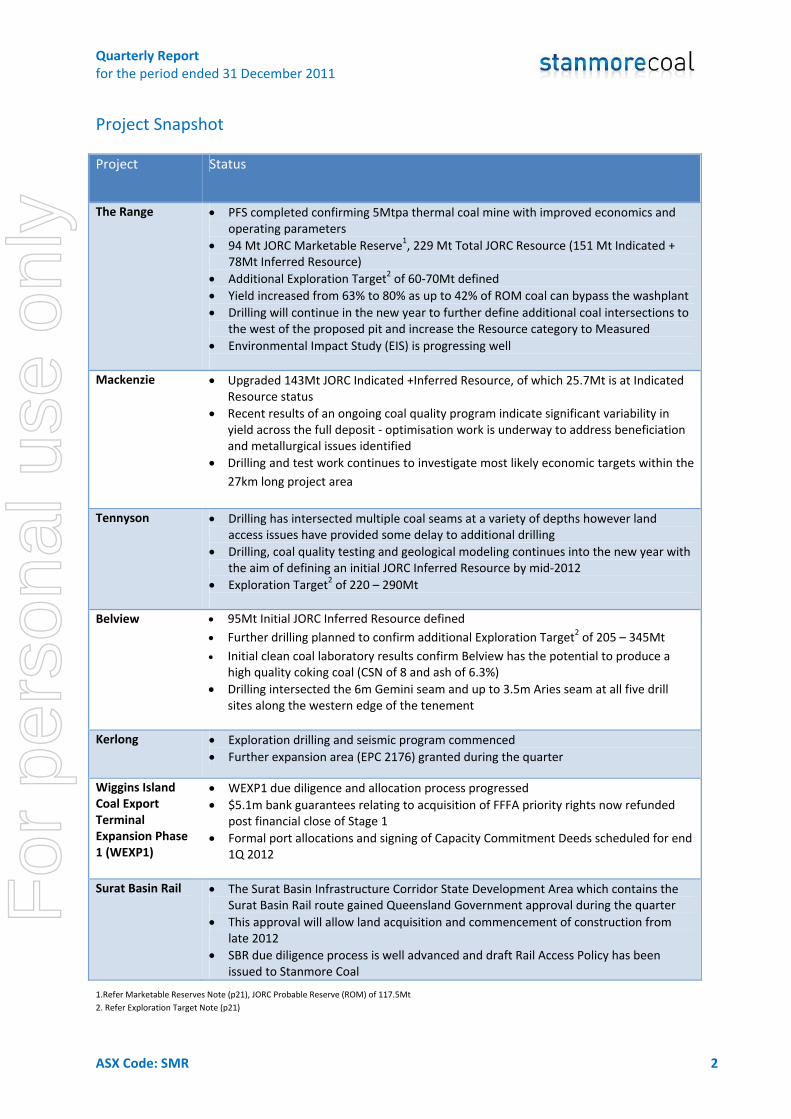

Project Snapshot Project Status

The Range • PFS completed confirming 5Mtpa thermal coal mine with improved economics and operating parameters

• 94 Mt JORC Marketable Reserve1, 229 Mt Total JORC Resource (151 Mt Indicated + 78Mt Inferred Resource)

• Additional Exploration Target2 of 60‐70Mt defined • Yield increased from 63% to 80% as up to 42% of ROM coal can bypass the washplant • Drilling will continue in the new year to further define additional coal intersections to

the west of the proposed pit and increase the Resource category to Measured • Environmental Impact Study (EIS) is progressing well

Mackenzie • Upgraded 143Mt JORC Indicated +Inferred Resource, of which 25.7Mt is at Indicated

Resource status • Recent results of an ongoing coal quality program indicate significant variability in

yield across the full deposit ‐ optimisation work is underway to address beneficiation and metallurgical issues identified

• Drilling and test work continues to investigate most likely economic targets within the 27km long project area

Tennyson • Drilling has intersected multiple coal seams at a variety of depths however land access issues have provided some delay to additional drilling

• Drilling, coal quality testing and geological modeling continues into the new year with the aim of defining an initial JORC Inferred Resource by mid‐2012

• Exploration Target2 of 220 – 290Mt

Belview • 95Mt Initial JORC Inferred Resource defined • Further drilling planned to confirm additional Exploration Target2 of 205 – 345Mt • Initial clean coal laboratory results confirm Belview has the potential to produce a

high quality coking coal (CSN of 8 and ash of 6.3%) • Drilling intersected the 6m Gemini seam and up to 3.5m Aries seam at all five drill

sites along the western edge of the tenement

Kerlong • Exploration drilling and seismic program commenced • Further expansion area (EPC 2176) granted during the quarter

Wiggins Island Coal Export Terminal Expansion Phase 1 (WEXP1)

• WEXP1 due diligence and allocation process progressed • $5.1m bank guarantees relating to acquisition of FFFA priority rights now refunded

post financial close of Stage 1 • Formal port allocations and signing of Capacity Commitment Deeds scheduled for end

1Q 2012

Surat Basin Rail • The Surat Basin Infrastructure Corridor State Development Area which contains the Surat Basin Rail route gained Queensland Government approval during the quarter

• This approval will allow land acquisition and commencement of construction from late 2012

• SBR due diligence process is well advanced and draft Rail Access Policy has been issued to Stanmore Coal

1.Refer Marketable Reserves Note (p21), JORC Probable Reserve (ROM) of 117.5Mt 2. Refer Exploration Target Note (p21)

For

per

sona

l use

onl

y

Quarterly Report for the period ended 31 December 2011

ASX Code: SMR 3

Project Review The Range Project EPC 1112, 2030 / MLA 55001 Stanmore Coal 100% ownership Location: Surat Basin – 24km south‐east of Wandoan Area: 96km2

JORC Resource: Total of 229 Mt high quality open pit thermal coal (151Mt Indicated + 78 Inferred Resource) JORC Marketable Reserves: 94 Mt (Note:1) During the quarter Stanmore Coal announced positive results from the Pre‐feasibility Study (PFS) for The Range with improved project economics relative those in the Conceptual Mining Study carried completed in late 2010.

The Range Project is located 25 kilometres south east of the Wandoan township, within the Surat Basin. It is well located relative to existing key infrastructure and the planned Surat Basin Rail line, which will provide a rail link to the coal ports at Gladstone.

The project remains on track for first coal in 2015 subject to statutory approvals being attained and completion of third party infrastructure.

The PFS considered both owner mining and contractor mining options to produce 5 Mtpa of export coal over a mine life of 26 years, the results of which are summarised below.

Capital and Operating Costs The development capital cost estimates are shown below for both owner and contract mining cases. The introduction of a conveyor system for transport of coal from the mine site to the Surat Basin Rail has increased capital expenditure by some $50m above the cost of the haul road proposed in the Conceptual Mining Study. However, the conveyor system will reduce operating costs and lower the risk of disruption due to potential seasonal flooding of the haul road.

Development Capital ($Am) Owner Mining Contract Mining

Coal Handling & Prep Plant 134 134

Surface Infrastructure 120 123

Conveyer & Rail Loop 113 113

Mining Fleet to first coal (2015)

101

Contingency 37 37

Total 505 407

Figure 1: Capital Expenditure

In the owner operator case a further $85m of mining equipment will be purchased during 2016 / 17 from operating cash flow to enable ramp up to full production.

For

per

sona

l use

onl

y

Quarterly Report for the period ended 31 December 2011

ASX Code: SMR 4

The estimated operating costs are outlined below. Operating cost savings relative to the previous Conceptual Mining Study relate mainly to:

the introduction of a conveyor transport system to the rail head

the identification of extensive seams of clean coal which do not need washing which has led to the introduction of a bypass circuit. The effective yield for the project has increased from 63% to 80% with the ability to pass 42% of the ROM coal through the bypass circuit creating an improvement in the operating costs per tonne of product coal

Operating Costs (First 17 years of production)

Owner Mining Contract Mining

Mining & processing cost (FOR) $A/t 39.4 49.8

With Rail & port costs (FOB)3 $A/t 71.9 81.7

3. Plus State Government Royalty estimated at $6.80. Including overheads.

Figure 2: Operating Costs

Project Economics The financial modelling conducted as part of the study indicates strongly positive net present values for both the owner mining case and the contractor case under a range of long term coal price assumptions.

Owner Mining Contract Mining

NPV ($Am)4 846 703

4. Based on Credit Suisse long term forecasts (US$120/t FOB Newcastle thermal coal price and exchange rate of 0.85 AUD/USD) and a nominal discount rate of 10.0% (WACC)

Figure 3: Net Present Value of The Range Project

A number of additional shallow coal seams have been intersected in holes during sterilisation drilling to the west of the main deposit which appear to be in the lower Juandah sequence. Further drilling and laboratory testing is ongoing to confirm the extent and quality of these seams, and an additional Exploration Target2 of 60 – 70 million tonnes has been established in relation to this area.

Site Layout and Services The original two pit design from the Conceptual Mining Study has consolidated to a single larger pit due to the definition of additional shallow coal from drilling conducted during the year. The siting of the Coal Handling and Preparation Plant (CHPP) and associated infrastructure has been chosen to minimise haul distances for ROM coal and avoid sterilising any potential future coal deposits.

The main power requirements are from the CHPP and two 800 tonne class electric hydraulic shovels. Demand is estimated to be between 12MW to 14MW and power is likely to come from the mains grid through Powerlink and Ergon. Alternatives such as site based, gas fired electricity generators are also being investigated and will be considered if they provide a better economic outcome.

For

per

sona

l use

onl

y

Quarterly Report for the period ended 31 December 2011

ASX Code: SMR 5

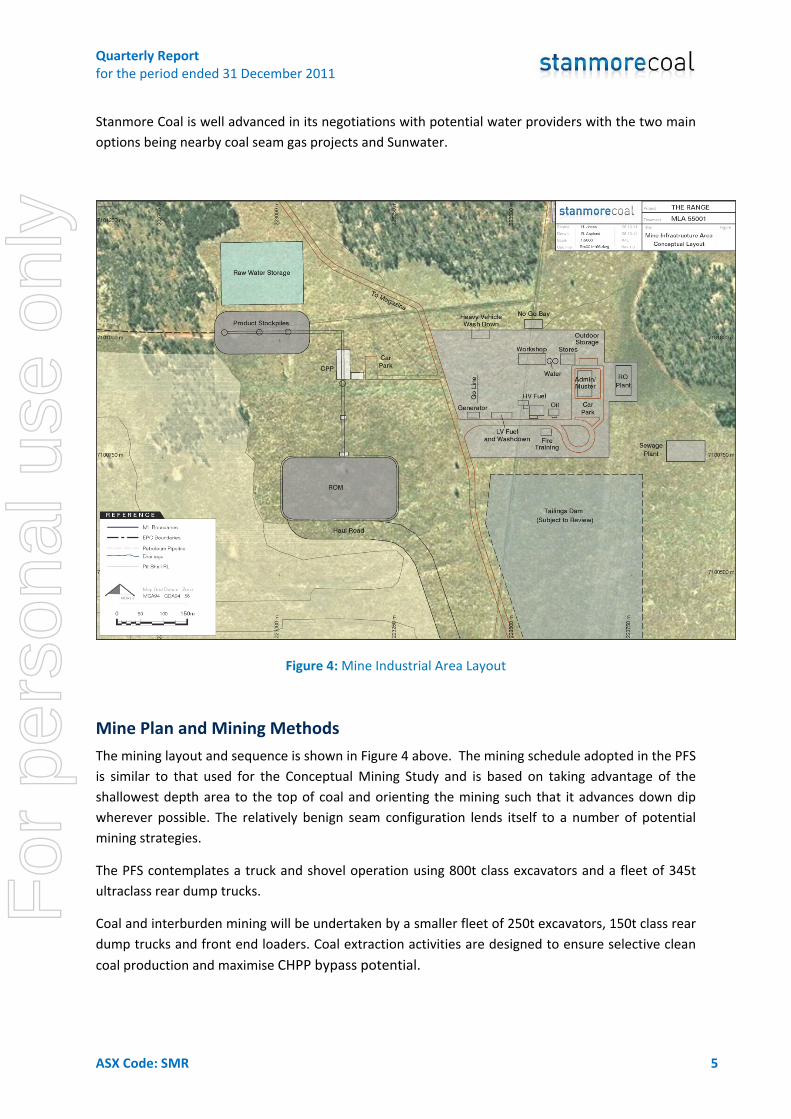

Stanmore Coal is well advanced in its negotiations with potential water providers with the two main options being nearby coal seam gas projects and Sunwater.

Figure 4: Mine Industrial Area Layout

Mine Plan and Mining Methods The mining layout and sequence is shown in Figure 4 above. The mining schedule adopted in the PFS is similar to that used for the Conceptual Mining Study and is based on taking advantage of the shallowest depth area to the top of coal and orienting the mining such that it advances down dip wherever possible. The relatively benign seam configuration lends itself to a number of potential mining strategies.

The PFS contemplates a truck and shovel operation using 800t class excavators and a fleet of 345t ultraclass rear dump trucks.

Coal and interburden mining will be undertaken by a smaller fleet of 250t excavators, 150t class rear dump trucks and front end loaders. Coal extraction activities are designed to ensure selective clean coal production and maximise CHPP bypass potential.

For

per

sona

l use

onl

y

Quarterly Report for the period ended 31 December 2011

ASX Code: SMR 6

The initial production workforce of approximately 400 people will be accommodated at a combination of local housing and village accommodation in Wandoan.

The mine life has increased from 18 years in the Conceptual Mining Study to 26 years largely on the basis of the enhanced yield which leads to a more optimal use of the deposit. The ROM strip ratio averages 6.7 bcm/t over the first 17 years of the mine life.

Figure 5: Mining Sequence Snapshot – 2027

Coal Handling and Preparation Plant The proposed Coal Handling and Preparation Plant (CHPP) has been designed at a feed rate of 750tph to allow for campaign washing operations alternated with bypass operations. The front end crushing and screening system has been designed to accommodate both the washed and bypass coal streams. The CHPP will incorporate proven technologies – dense medium cyclones and spirals for product beneficiation.

The raw ash content of individual coal plies is as low as 3.7% (with an average of 20.5% air dried). Favourable raw ash levels over much of the resource allows 42% of ROM coal to bypass the wash plant and be direct shipped. This leads to 53% of product coal being direct shipped without wash plant losses. As a result of this the overall effective yield is 80% while the coal that is washed has a yield of 64%.

For

per

sona

l use

onl

y

Quarterly Report for the period ended 31 December 2011

ASX Code: SMR 7

Coal Product Transport A 25 kilometre overland conveyor is proposed to a train load‐out facility and rail loop at the planned Surat Basin Rail (SBR) link, due for completion in 2015. The preferred tie‐in point to the SBR is north of the town of Wandoan which eliminates any reliance on rail construction beyond the Wandoan mine tie in point.

Coal will be stockpiled at the rail head and then loaded to trains for railing to the Wiggins Island Coal Export Terminal (WICET) at Gladstone. Stanmore Coal is a participant in the WICET Stage 2 expansion process and has acquired 7Mtpa of priority capacity rights in the terminal expansion.

Coal Quality Surat Basin coals are currently being exported in significant tonnages to the Asian utility market. The Range coal features good energy content, ability to produce low ash, low levels of trace element impurities by international standards, low sulphur and nitrogen contents and excellent burnout characteristics.

Favourable washability characteristics allow flexibility in choice of product ash with a likely product range of 10% ‐ 14.4% ash.

The Range Coal Quality Summary Product 1 Product 2 Product 3

Ash % ad 10.0 12.0 14.4

Volatile Matter % ad 41.6 40.7 39.8

Fixed Carbon % ad 40.4 39.3 37.7

Total Sulphur % ad 0.4 0.4 0.4

Nitrogen (ult) % daf 1.1% 1.1% 1.1%

Total Moisture % 14% 13.5% 13%

Gross Calorific Value kcal/kg ad 6,375 6,217 6,026

Gross Calorific Value kcal/kg daf 7,774 7,771 7,777

Figure 6: Coal Quality

The PFS case is based on maximising energy recovery from the resource by bypassing as much coal as possible and washing the remainder to an ash content of 13.0% (air dried). This leads to a product ash of 14.4% (air dried) as shown in Product 3 above. The optimal ash and energy content for the deposit will be determined in the Definitive Feasibility Study in conjunction with further marketing analysis.

The introduction of bypass coal which avoids the wash plant also provides a beneficial lowering of lower total moisture content in the product coal.

For

per

sona

l use

onl

y

Quarterly Report for the period ended 31 December 2011

ASX Code: SMR 8

Further Optimisation Potential A number of areas were identified for further investigation with the potential to further improve the project economics. These include:

Further refinement of the mining method and fleet to maximise the use of cheaper overburden dozer push

Revisiting the optimal product ash and bypass coal configuration. The Range coal has the potential to be washed to an ash level of between 10% and 17% at varying yields. Additional market analysis is planned to identify the optimal product ash specifications

Potential for in pit crushing and conveying systems for waste transport and Wirtgen surface miner to remove coal and thin interburden materials

Potential for shared infrastructure costs on the overland conveyor and at the rail loadout area

Possible cost savings and washplant efficiency improvements from new technologies such as the use of reflux classifiers

Successful drilling to the west of the current proposed pit has the potential to extend the resource base and mine life

These will be investigated during the Definitive Feasibility Study which will commence in early 2012.

For

per

sona

l use

onl

y

Quarterly Report for the period ended 31 December 2011

ASX Code: SMR 9

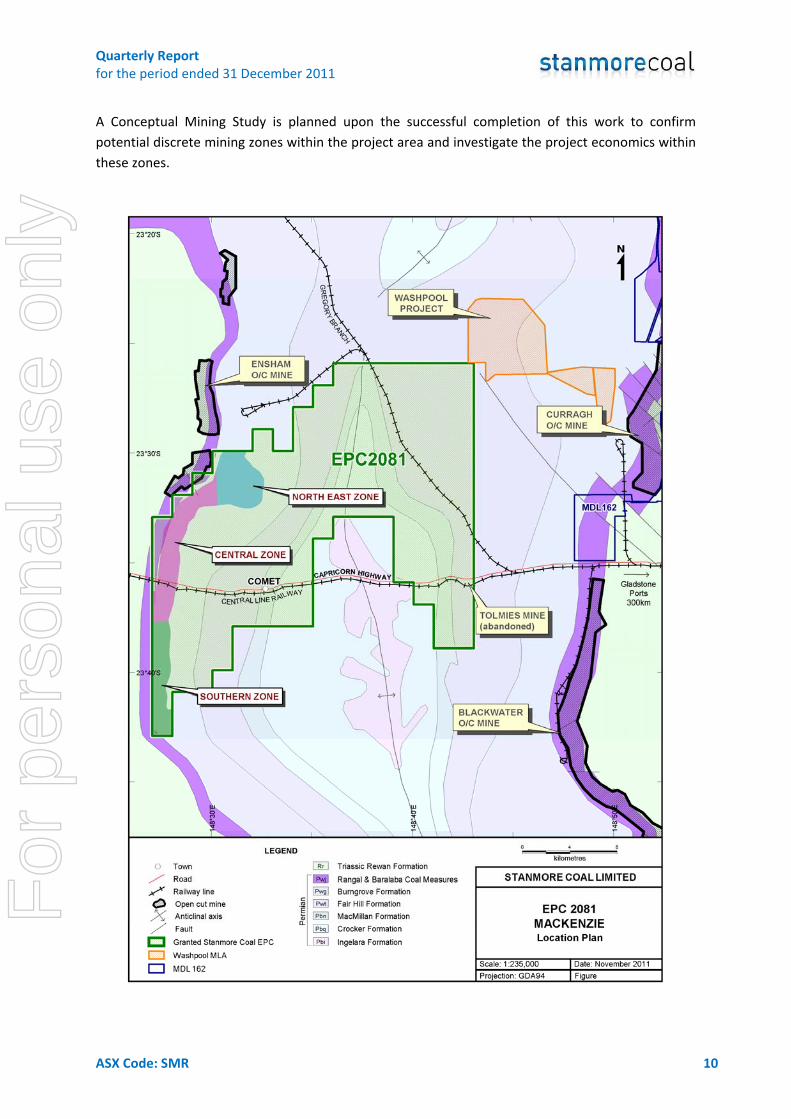

Mackenzie Coking Coal Project EPC 2081 Stanmore Coal 100% ownership Location : 30km west of Blackwater Area: 512km2

JORC Inferred Resource: 143Mt coal (25.7Mt Indicated + 117.5Mt Inferred)

Stanmore Coal completed an interim review of the Mackenzie deposit during the quarter which has resulted in the definition of the first 25.7 million tonnes (Mt) of JORC Indicated Resource and a 45% increase of the Total JORC Resource to 143.2 Mt (25.7Mt Indicated + 117.5Mt Inferred).

November 2011 August 2010

Indicated Resource 25.7 Mt ‐

Inferred Resource 117.5 Mt 99.0 Mt

Total 143.2 Mt 99.0 Mt

Figure 7: Coal Quality

Since the August 2010 review a further 53 holes have been drilled and the current model now includes a total of 80 holes. The coal sequence comprises two main coal seams being the Leo and Aquarius seams within the Burngrove Formation. The seams strike in a general North South direction over an approximate 27km strike length, and dip towards the west at approximately 2 degrees. The main coal seams occur at depths of between 10 and 110 metres.

This year’s laboratory analysis program has incorporated pre‐treatment procedures that simulate the mine handling and coal preparation techniques. Results from this year’s program, when compared with data from 2010 obtained from the south of the deposit, indicate a lowering of average yield5 to 26% over all seams and over the entire 27km length of the deposit for the target 15‐17% ash coking product. Variability occurs across the deposit and between the various seams with yields ranging from 11% to 71%. Work is continuing to complete the laboratory program and determine which combination of seams is likely to produce an economic coking coal product. The higher ash seams are also being investigated to determine whether they could form a secondary thermal coal product. Further work is under way to address beneficiation and metallurgical issues identified with the aim of improving the yield.

Yield Optimisation Investigations

Work is continuing on alternative processing methods that may improve product ash and recovery. This additional analysis includes optimising pre‐treatment methods and extended analysis of the fines fraction with the aim of increasing fines recovery and maximising potential coal yields. Further investigation of fine material via supplementary processing techniques is currently being undertaken with the aim of improving product yield.

5. Note all yields and ash results reported include fines and exclude mining losses and dilution

For

per

sona

l use

onl

y

Quarterly Report for the period ended 31 December 2011

ASX Code: SMR 10

A Conceptual Mining Study is planned upon the successful completion of this work to confirm potential discrete mining zones within the project area and investigate the project economics within these zones.

For

per

sona

l use

onl

y

Quarterly Report for the period ended 31 December 2011

ASX Code: SMR 11

Tennyson Thermal / Coking Coal Project EPC 1168 Stanmore Coal 100% ownership Location: adjacent to Emerald Area: 131km2

Exploration Target2: 220‐290 Mt underground thermal and potential metallurgical coal The proposed drilling program at Tennyson was reviewed during the quarter and will now consist of eight holes that will allow the calculation of an initial JORC Resource. This program was originally planned for the December quarter but was impacted by delays in complying with the new State regulations regarding land access for exploration. Holes completed to date have intersected multiple coal seams at a variety of depths with the Aries seam thickness averaging 2.5 metres, the Corvus seam 2.6 metres and the Liskeard seam 2.1 metres.

Modelling of results indicates that the Aries seam subcrops at around 150 metres and dips to the east, south and southwest to a maximum depth of around 490 metres. Historic quality testing of the Aries seam in the project area points to a raw ash of between 10 to 15 percent and indicates that this seam could support a low ash, low sulphur export quality thermal coal with specific energies of up to 6680 kcal/kg.

For

per

sona

l use

onl

y

Quarterly Report for the period ended 31 December 2011

ASX Code: SMR 12

Belview Coking Coal Project EPC 1114 Stanmore Coal 100% ownership Location: 10km south‐east of Blackwater Area: 131km2

JORC Inferred Resource: 95Mt Additional Exploration Target2: 205 – 345Mt underground prime coking coal During the December quarter Stanmore Coal defined an initial JORC Inferred Resource of 95 Mt in the Gemini seam of the Rangal Coal Measures. The Gemini coal seam was previously mined as a hard coking coal at BHP’s historical Leichhardt mine 4km to the west of Belview. The key seams that have been intersected by Stanmore Coal in the Belview lease are the Aries, Gemini, Orion and Pisces seams.

A further exploration program is planned for 2012 to extend the Inferred Resource and address core recovery issues encountered in a number of the drill holes. To date the Inferred Resource has been calculated from the Gemini seam only, based on testing of the central three holes of the initial six hole program completed in the western margin of the tenement. An increase to the initial JORC Inferred Resource is anticipated on completion of further drilling.

Seam Mean Thickness

(m)

Maximium Thickness

(m)

Minimum Thickness

(m)

Number of Intersections

JORC Inferred (Mt)

Additional

Exploration Target2 (Mt)

Aries 2.2 3.1 1.1 6 80‐120

Gemini 5.5 6.8 1.9 6 95 25‐65

Orion 5.6 8.2 3.1 5 40‐60

Pisces Upper

3.0 3.2 2.8 5 40‐60

Pisces Lower

2.5 3.4 1.2 5 20‐40

Total 95 205‐345

Figure 8: Coal Seam Details (Borehole Intersections)

Gemini Seam Coal Quality

Coal quality test work from the three holes tested to date has determined that the Gemini Seam is capable of producing a dual product comprising a high quality hard coking and a low ash, high energy thermal coal.

Raw crucible swell numbers typically range from 1.5 to 9 and average 3.8. Average raw ash of 13.4% and raw energy of 7,260 kcal / kg (air dried) was achieved. Coal rank and average coal quality appears at this stage to remain fairly consistent with increases in depth.

For

per

sona

l use

onl

y

Quarterly Report for the period ended 31 December 2011

ASX Code: SMR 13

Initial clean coal laboratory test results for the central three holes demonstrate a substantial improvement in coking properties from washing with a combined coking and thermal product yield5 of 90%.

Figure 9. Gemini Seam Clean Coal Results (average across full 6m seam)

(ad – air dried), (daf – dry ash free)

Coking properties increase towards the base of the coal seam. Should the deposit be selectively mined for the lower 2.5m of the seam an enhanced coking coal is achieved as shown below.

Figure 10. Coking Coal Comparison

6. Source: GSQ 2003

Washed Results

Primary Hard Coking Product

Secondary Thermal / Weak Coking Product

Yield2 45% 45%

Ash ad 7.0% 10%

Volatile Matter

ad 21.1% 20.7%

Fixed Carbon

ad 70.5% 67.9%

CSN ad 7 2

Total Sulphur

ad 0.40% 0.35%

Specific Energy

kcal/kg ad

7,880 7,570

Specific Energy

Kcal/kg daf

8,603 8,544

Belview Gemini Seam Other Bowen Basin Hard Coking Coals6

Entire 6m seam

Lower 2.5m of seam only

Blackwater Mine

Curragh Mine

Cook Mine

Ash ad 7.0% 6.3% 8.0% 7.0% 6.0%

Volatile Matter

ad 21.1% 21.2% 27% 21‐23% 27.5%

CSN ad 7 8 6 7‐8 7.5

Total Sulphur

ad 0.4% 0.4% 0.5% 0.5‐0.6% 0.35%

Specific Energy

kcal/kg ad

7,880 7,965 7,643 7,834

For

per

sona

l use

onl

y

Quarterly Report for the period ended 31 December 2011

ASX Code: SMR 14

The clean coal composites above from the first three holes tested demonstrate that the Belview coal has attractive coking coal characteristics and compares well to other nearby hard coking coal mines in the Bowen Basin.

Further coking tests are being conducted including petrographic analysis to confirm the coal rank and other coking properties.

Aries Seam Coal Quality

Initial clean coal composite results from the first of the Aries seam samples similarly demonstrate very attractive coking coal qualities and the potential to optimise yield by the production of a secondary high energy thermal product.

Figure 11. Aries Seam Washability Results

(ad – air dried)

The company is planning to commission a scoping study to identify the potential project economics at Belview using modern underground mining methods.

Aries Seam Primary Hard Coking Product

Secondary Thermal Product

Yield 36.8% 31.2%

Ash ad 9% 15.3%

Volatile Matter

ad 21.4% 21.3%

Fixed Carbon

ad 68.4% 62.1%

CSN ad 8 1.5

Total Sulphur

ad 0.5% 0.4%

Specific Energy

kcal/kg ad

7,656 6,856

For

per

sona

l use

onl

y

Quarterly Report for the period ended 31 December 2011

ASX Code: SMR 15

For

per

sona

l use

onl

y

Quarterly Report for the period ended 31 December 2011

ASX Code: SMR 16

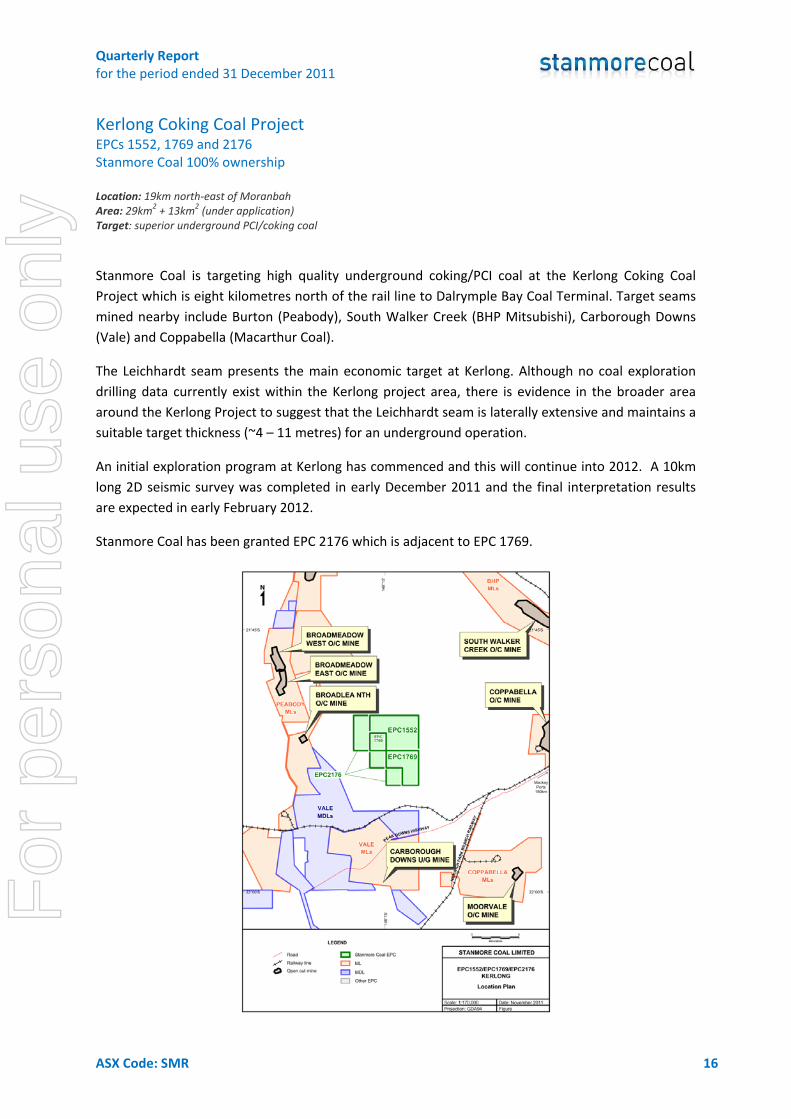

Kerlong Coking Coal Project EPCs 1552, 1769 and 2176 Stanmore Coal 100% ownership Location: 19km north‐east of Moranbah Area: 29km2 + 13km2 (under application)

Target: superior underground PCI/coking coal

Stanmore Coal is targeting high quality underground coking/PCI coal at the Kerlong Coking Coal Project which is eight kilometres north of the rail line to Dalrymple Bay Coal Terminal. Target seams mined nearby include Burton (Peabody), South Walker Creek (BHP Mitsubishi), Carborough Downs (Vale) and Coppabella (Macarthur Coal).

The Leichhardt seam presents the main economic target at Kerlong. Although no coal exploration drilling data currently exist within the Kerlong project area, there is evidence in the broader area around the Kerlong Project to suggest that the Leichhardt seam is laterally extensive and maintains a suitable target thickness (~4 – 11 metres) for an underground operation.

An initial exploration program at Kerlong has commenced and this will continue into 2012. A 10km long 2D seismic survey was completed in early December 2011 and the final interpretation results are expected in early February 2012.

Stanmore Coal has been granted EPC 2176 which is adjacent to EPC 1769.

For

per

sona

l use

onl

y

Quarterly Report for the period ended 31 December 2011

ASX Code: SMR 17

New Cambria Project EPCs 1113, 2039, 2371 Stanmore Coal 100% ownership Location: 20km east of Blackwater Area: 117km2

Target: open pit Yarrabee style low‐volatiles PCI coal

The New Cambria Project is targeting the up‐thrust Rangal Coal Measures which contain low‐volatile, low to medium ash PCI coal with open cut mining potential. High energy coal has been mined historically at the adjoining Excel Colliery and the project is located adjacent to the rail line to Gladstone. Coal Seam Gas (CSG) co‐development discussions have commenced. A seismic program is planned for the first half of 2012 which will identify potential drilling targets.

For

per

sona

l use

onl

y

Quarterly Report for the period ended 31 December 2011

ASX Code: SMR 18

Port and Rail Wiggins Island Coal Export Terminal Expansion Phase 1 Stanmore Coal is a participant in the WICET Expansion Phase 1 (WEXP1) process which is scheduled to provide a 30Mtpa capacity expansion at WICET by 2015. WICET is now moving to shortlist qualifying parties for WEXP1 in advance of successful participants signing Capacity Commitment Deeds (CCD’s), which is currently scheduled for the end of the first quarter of 2012. The company continues to interact positively with the WICET team about our potential allocation in the port.

Stanmore Coal previously acquired seven million tonnes per annum (Mtpa) of priority capacity rights at the WICET. The acquisition of these priority rights increases the likelihood of the Company securing its requested port allocation in WEXP1.

The cost of the 7Mtpa of FFFA priority rights to Stanmore Coal was $1.05m. In addition, the Company agreed to take over the bank guarantees and interest payments of the vendors (totalling $5.77m) that relate to the FFFA priority rights. With financial close of WICET Stage 1 achieved on 30th September 2011 the bank guarantees securing Stanmore’s priority rights were released on 4th November 2011. WICET Stage 1 construction is now underway.

Other Ports Stanmore Coal has previously entered into conditional agreements to ship up to 12 million tonnes per annum (Mtpa) of coal through the proposed Dudgeon Point Coal Terminal (DPCT) from 2016.

In addition, Stanmore Coal continues to review all infrastructure options including a number of other proposed ports in the Gladstone region.

Rail During the quarter the Surat Basin Rail (SBR) project reached an important milestone with the granting of Queensland Government approval for the development scheme for the State Development Area which contains the route for the planned line which will link The Range project to the Ports of Gladstone including the WICET terminal.

Stanmore Coal has applied for five million tonnes of capacity on the SBR to deliver high quality export thermal coal from the proposed The Range project.

Granting of this approval will now allow the SBR joint venture to move to compulsory acquisition of key land along the proposed route and will allow commencement and ultimate completion of construction in time for delivery of first coal in 2015.

The SBR due diligence process is well advanced and draft Rail Access Policy was issued to Stanmore Coal in December 2011 to commence the formal negotiations for access to the rail line.

For

per

sona

l use

onl

y

Quarterly Report for the period ended 31 December 2011

ASX Code: SMR 19

Corporate Completion of Capital Raising

During the December quarter Stanmore Coal successfully raised $14.1 million via a placement of approximately 19.1 million ordinary shares to institutional and sophisticated investors at $0.74 per share (“Placement”).

The Placement was oversubscribed and received strong support from existing institutional shareholders as well as a number of new investors.

Net proceeds of the Placement will be predominantly applied to fund a definitive feasibility study at the Range, continuing exploration at other key projects, initial stage funding of port and rail infrastructure commitments and general working capital requirements.

Stanmore Coal also offered eligible shareholders the opportunity to participate in a partially underwritten Share Purchase Plan (“SPP”) to raise up to a further $10 million at the same issue price. The SPP was well subscribed for and subsequent to the end of the quarter, the company announced that the full $10 million had been successfully raised.

Permit Applications –

Project Tenement Number Tenement Name Date of

Application Type

Brown River EPCA 1546 Brown River 7/08/2008 Primary EPCA 2062 May Creek 17/02/2010 Primary EPCA 2113 Brown River North 6/05/2010 Secondary EPCA 2520 Brown River East 3/5/2011 Priority Carnarvon EPCA 1630 Carnarvon 28/10/2008 Secondary Altamondt EPCA 2177 Altamondt 2/08/2010 Priority

Mining Lease Applications

Project Tenement Number Tenement Name Date of

Application Status

The Range MLA 55001 The Range 3/11/2010 EIS advised Other granted Stanmore Coal EPCs:

• EPC 1545 & 1567 ‐ Ironpot Creek • EPC 1687 – Theresa Creek – Granted 28/07/2011 • EPC 1627 – Ten Mile Creek – Granted 12/08/2011 • EPC 1804 ‐ Yamala North

Desktop studies on these EPC’s are underway in advance of site exploration programs.

For

per

sona

l use

onl

y

Quarterly Report for the period ended 31 December 2011

ASX Code: SMR 20

Contacts For further information, please contact: Mr Nick Jorss Managing Director 07 3238 1000

Mr Andrew Barber Investor Relations Manager 07 3212 9216 0418 783 701

Competent Persons Statement

The information in this report relating to exploration results and coal resources is based on information compiled by Mr Wes Nichols who is a member of the Australasian Institute of Mining and Metallurgy and is a full time employee of Stanmore Coal. Mr Nichols is a qualified geologist and has sufficient experience that is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking, to qualify as Competent Person as defined in the 2004 Edition of the JORC Code. Mr Nichols consents to the inclusion in this document of the matters based on the information, in the form and context in which it appears.

The information in this report relating to coal reserves is based on information compiled by Mr Richard Hoskings who is a full time employee of Minserve Pty Ltd. Mr Hoskings is a mining engineer, a member of the Australian Institute of Mining and Metallurgy (AusIMM) and has the relevant experience (30+ years) in relation to the mineralisation being reported to qualify as a Competent Person as defined in the “Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves (The JORC Code 2004 Edition)”. Mr Hoskings consents to the inclusion in the report of the matters based on the information, in the form and context in which it appears

Note 1: Marketable Reserves Note

The Marketable Coal Reserves of 94Mt is derived from a JORC compliant run of mine (ROM) Coal Reserve of 117.5Mt based on a 14.8% ash product and predicted yield of 80%.

Note 2: Exploration Target Note

All statements as to exploration targets of Stanmore Coal and statements as to potential quality and grade are conceptual in nature. There has been insufficient exploration undertaken to date to define a coal resource and identification of a resource will be totally dependent on the outcome of further exploration. Any statement contained in this report as to exploration results or exploration targets has been made consistent with the requirements of the Australasian code for reporting of exploration results, mineral resources and ore reserves (JORC Code).

About Stanmore Coal Limited (ASX code: SMR)

Stanmore Coal is a growth focused, pure play coal exploration and development company with a number of prospective coal projects and exploration areas within Queensland’s Bowen and Surat Basins. Stanmore Coal is focused on the creation of shareholder value via the identification and development of coal deposits, with a focus on the prime coal bearing regions of the east coast of Australia.

Stanmore Coal holds 100% interests in its seven coal project areas, covering over 1,080 km2 in total. These projects include significant deposits of open pit coking and thermal coal and are typically well located for export infrastructure.

Stanmore Coal Limited ACN 131 920 968 Phone: +61 (7) 3238 1000 | Fax: +61 (7) 3212 6250 Email: [email protected]| Web: www.stanmorecoal.com.au Street address: Level 11, 10 Market Street, Brisbane QLD 4000 Postal address: GPO Box 2602, Brisbane QLD 4001

For

per

sona

l use

onl

y