for personal use only - asx2014/02/18 · price (12 months) 2.5 - 15.0 ¢ cash (31 dec) $0.8 m for...

TRANSCRIPT

Celamin Holdings NL | February 2014

Tunisian Phosphate

February 2014

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

IMPORTANT INFORMATION AND DISCLAIMER

Disclaimer

This presentation is not a prospectus nor an offer of securities in any jurisdiction nor a securities recommendation. The information in this

presentation is an overview and does not contain all information necessary for investment decisions. In making investment decisions in

connection with any acquisition of securities, investors should rely on their own examination of Celamin Holdings NL and consult their

own legal, business and/or financial advisers.

The information contained in this presentation has been prepared in good faith by Celamin Holdings NL, however no representation or

warranty expressed or implied is made as to the accuracy, correctness, completeness or adequacy of any statements, estimates,

options, or other information contained in this presentation. To the maximum extent permitted by law, Celamin Holdings NL, its Directors,

officers, employees and agents disclaim liability for any loss or damage which may be suffered by any person through the use of reliance

on anything contained in or omitted from this presentation.

Certain information in this presentation refers to the intentions of Celamin Holdings NL, but these are not intended to be forecasts,

forward looking statements or statements about the future matters for the purposes of the Corporations Act or any other applicable law.

The occurrence of the events in the future are subject to risk, uncertainties and other actions that may cause Celamin Holding NL’s

actual results, performance or achievements to differ from those referred to in this presentation. Accordingly Celamin Holdings NL, its

Directors, officers, employees and agents do not vie any assurance or guarantee that the occurrence of these events referred to in the

presentation will actually occur as contemplated.

.

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

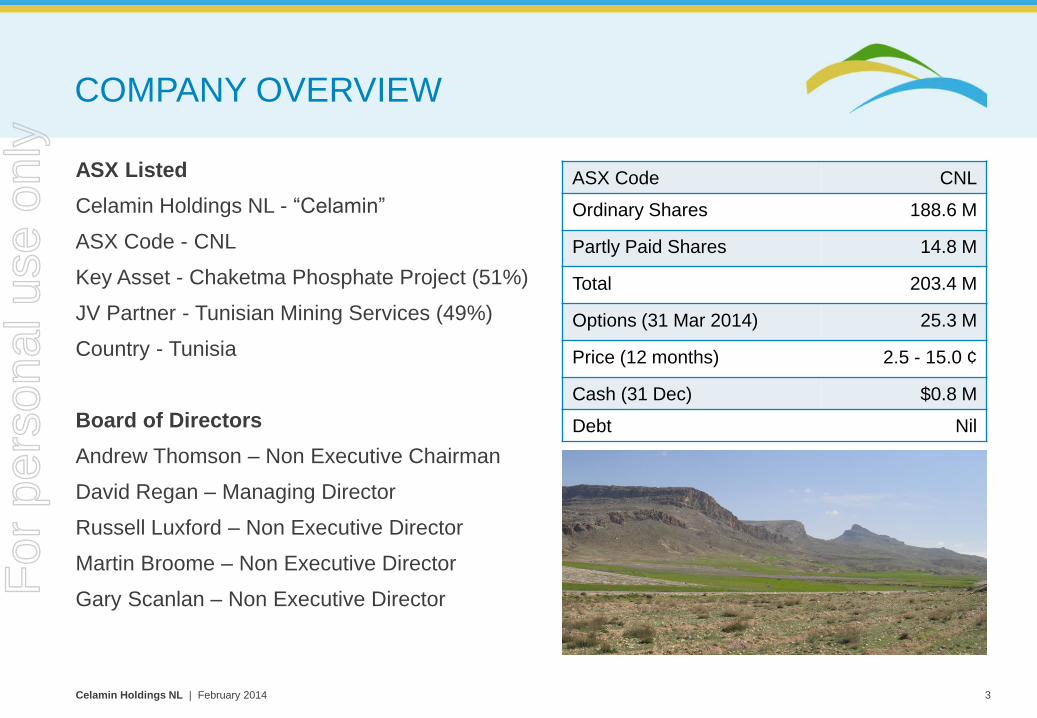

COMPANY OVERVIEW

3

ASX Listed

Celamin Holdings NL - “Celamin”

ASX Code - CNL

Key Asset - Chaketma Phosphate Project (51%)

JV Partner - Tunisian Mining Services (49%)

Country - Tunisia

Board of Directors

Andrew Thomson – Non Executive Chairman

David Regan – Managing Director

Russell Luxford – Non Executive Director

Martin Broome – Non Executive Director

Gary Scanlan – Non Executive Director

the Northwest

ASX Code CNL

Ordinary Shares 188.6 M

Partly Paid Shares 14.8 M

Total 203.4 M

Options (31 Mar 2014) 25.3 M

Price (12 months) 2.5 - 15.0 ¢

Cash (31 Dec) $0.8 M

Debt Nil

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

BOARD OF DIRECTORS

Andrew Thomson, Non-Executive Chairman

Former Federal MP and Citadel Resources Group Chairman

David Regan, Managing Director

Former Citadel Resources Group Director; more than 20 years’ North African / Middle East

experience in resources sector.

Russell Luxford, Non-Executive Director

Non Executive Director of Discovery Metals; former Project Director Maaden Al Jalamid

Phosphate Project; former Operations Manager WMC Phosphate Hill; engineer specialised in

large scale minerals project development and operations.

Martin Broome, Non-Executive Director

Director of Barclays Bank of Zambia.

Gary Scanlan, Non-Executive Director

Former Director of Citadel Resources Group; Non Executive Director of Lion Gold (Singapore

listed); 28 years experience in mining, including 18 years with Newmont/Newcrest Executive

General Manager Finance.

4

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

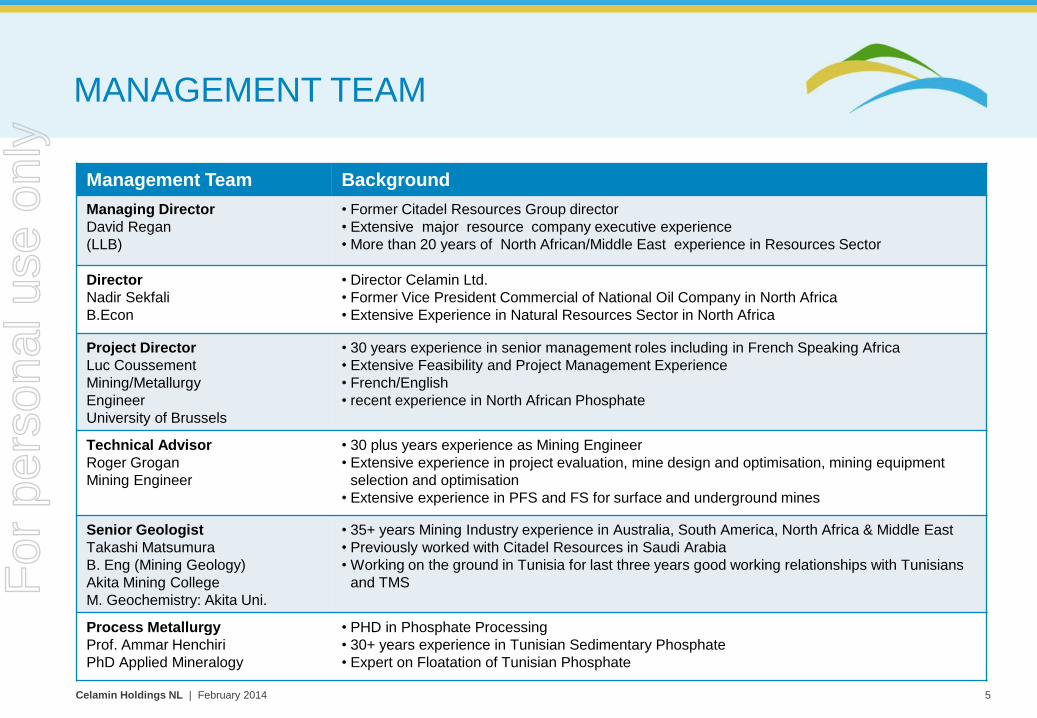

MANAGEMENT TEAM

5

Management Team Background

Managing Director

David Regan

(LLB)

• Former Citadel Resources Group director

• Extensive major resource company executive experience

• More than 20 years of North African/Middle East experience in Resources Sector

Director

Nadir Sekfali

B.Econ

• Director Celamin Ltd.

• Former Vice President Commercial of National Oil Company in North Africa

• Extensive Experience in Natural Resources Sector in North Africa

Project Director

Luc Coussement

Mining/Metallurgy

Engineer

University of Brussels

• 30 years experience in senior management roles including in French Speaking Africa

• Extensive Feasibility and Project Management Experience

• French/English

• recent experience in North African Phosphate

Technical Advisor

Roger Grogan

Mining Engineer

• 30 plus years experience as Mining Engineer

• Extensive experience in project evaluation, mine design and optimisation, mining equipment

selection and optimisation

• Extensive experience in PFS and FS for surface and underground mines

Senior Geologist

Takashi Matsumura

B. Eng (Mining Geology)

Akita Mining College

M. Geochemistry: Akita Uni.

• 35+ years Mining Industry experience in Australia, South America, North Africa & Middle East

• Previously worked with Citadel Resources in Saudi Arabia

• Working on the ground in Tunisia for last three years good working relationships with Tunisians

and TMS

Process Metallurgy

Prof. Ammar Henchiri

PhD Applied Mineralogy

• PHD in Phosphate Processing

• 30+ years experience in Tunisian Sedimentary Phosphate

• Expert on Floatation of Tunisian Phosphate

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

LOCATION

6

TUNISIA

Country

› Location – 140km south of Italy

› Phosphate Infrast. – extensive

› History – 128 years of Phosphate

Mining (since 1886)

Project

› Chaketma – core project (51%)

› Location – 200km SW of Tunis

› Rail – 35km away

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

INFRASTRUCTURE

Extensive Infrastructure

› Road – adjacent to sealed road

› Rail – 35km to rail (1.5Mtpa capacity)

› Ports – numerous options available

› Power – electricity and gas available

› Water – options identified

› Pilot plants & storage facilities – present

› People infrastructure – extensive skill base

Rail & Port

› Rail – line upgrades, rolling stock, sidings

› Ports – equipped (storage, sidings, loading)

7

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

ACHIEVEMENTS

Continued Progress

› License – renewed May 2013 (3 years)

› Resource –130Mt @ 20.5% P2O5 (JORC Inferred)

› Ownership – 51% (formerly 50%). TMS (49%)

› Drilling – upgrading resource

› Project Team – assembled in Tunis

› Metallurgy – positive test work

› Offtakers – advanced discussions underway

› DFS Engineering – proposals being finalised

› Environmental & Social – studies underway

› Global Financial Organisation – potential investor

› Bir El Afou – disposed

8

Six Prospects: (i) Gassaa El Kebira (ii) Douar Ouled Hamouda (iii) Kef El Aguab (iv) Sidi Ali Ben Oum Ezzine (v) Kef El Louz (vi) Gassat Ezerbat

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

FINANCING & OFFTAKE

Financing

› Offtakers – indicative interest

› Strategic Banking Investors – interest from multilateral Finance Organisation(s)

› Regional Equity Investors – African/European investors

Marketing

› Samples – issued, tested and approved for key premium markets

› Offtake – long term supply interest

› Demand – up to 3mtpa

› Supply – not volume constrained

9

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

SCOPING STUDY

› Study – completed July 2012

› Life – +50 years

› Production – 0.75Mtpa (Year 1) & 1.5Mtpa (Year 2) of P2O5

› Metallurgy – 30-32% P2O5 confirmed as possible

› Conceptual target – 229Mt @ 20% P2O5

› Infrastructure – capable of supporting 1.5Mtpa (rail, port, electricity, gas)

› Preliminary Environmental and Social Studies: no ‘fatal flaws’

› Robust project economics:

- Capex - US$364M (opportunity to reduce during DFS)

- Opex – US$62/t (0.75Mtpa) & US$55/t (1.5Mtpa)

- Payback – 3.5 years

- NPV - US$605M (10% discount)

- IRR - 28%

10

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

CAPITAL COSTS

› Capital costs – based on estimates from Bir El Afou PFS

› Production – 1.5Mtpa concentrate

11

Exclusions include:

- land acquisition;

- mine development costs beyond

the first 2 months;

- closure and reclamation costs;

- working capital;

- capitalised interest; and

- financing charges.

- connection to rail head option:

slurry, truck or rail

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

SCOPING STUDY – UPDATED DCF PROFILE

12

Updated from Scoping Study: Higher Grade, Lower Strip Ratio in Kef El Louz and Gassa Kebira,

Assumptions: 2016: $130/Mt, 2017 $133/Mt Long Term Phosphate Rock Price $143/Mt (2018 onwards) based on Offtaker/Trader discussions.

Discount Rate: 10%.

CAPEX: $ 364m (+/-35%) Scoping Study Estimate, excluding Land acquisition mine development beyond first 2 months, closure and reclamation

costs, working capital, capitalised interest and financing charges, connection to rail head option, slurry, ruck or rail

($350)

($300)

($250)

($200)

($150)

($100)

($50)

$0

$50

$100

$150

$200

2008 2012 2016 2020 2024 2028 2032 2036 2040 2044 2048 2052 2056 2060 2064 2068 2072

Mil

lio

n U

.S.

Do

lla

rs

Year

Chaketma – DCF Profile (US$M)

Net Unlevered Cash Flow Net Income Cumulative Unlevered Cash Flow

Forward Economics

Value at 01 January 2014 = US$505.5 million

Internal Rate of Return = 25.2 percent

Exposure = US$284.6 million

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

CHAKETMA PROJECT – TIMELINE

Timetable - indicative

13

2014

Appoint DFS Engineer

2014

DFS

Completion

2015

Financing &

Construction

2016

Production

Item Date

Appoint of DFS Engineering group 2014

DFS Completion – $10M 2014

Mining License 2015

Financing & Construction 2015

Production 2016

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

RESOURCES

› 130 Mt @ 20.5% P2O5 (JORC inferred)

- Gassa Kebira - 93Mt @ 20.3% P₂O₅ (6:1 strip)

- Kef El Louz North - 37Mt @ 21% P₂O₅ (4:1 strip)

› Upside - only 2 of 6 prospects drilled

› Life - 35+ years based on 2 prospects only

14

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

DRILLING

15

› Drilling – typically demonstrating wide, mineralised, zones

› Depth – mineralisation at times occurs from surface

› Grades – generally +20%

Drill Hole From (m) To (m) Intercept (m) P2O5% CaO%

CHDD-2012-047 52.3 94.3 42.0 21.5 40.8

CHDD-2012-068 20.5 42.1 41.7 20.8 40.7

CHDD-2012-033 26.1 65.7 39.7 21.4 40.6

CHDD-2012-070 31.5 71.1 39.6 21.4 41.5

CHDD-2012-027 32.0 68.0 36.0 20.9 40.1

CHDD-2012-025 43.3 77.0 34.4 21.2 40.7

CHDD-2012-040 21.7 51.5 29.8 20.9 41.1

Drilling Intersections – Kef El Louz

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

METALLURGY

› Results to date - marketable concentrate verified with good recoveries

› Composite sample* - covering full intersected width of Kef El Louz resource:

- Concentrate grade - 31.0% P2O5

- Recovery - 68% P2O5

- MgO - less than 1.0%

› Major European reagent supplier – independently confirms test work

- Test work on a full composite sample at ambient temperature. Comparable results:

- Concentrate grade - 30.5% P2O5

- Recovery - 68.6%

- MgO - 0.7%

- Minor elements - acceptable industry standard ranges

› Engineering Contractors (Independent) - similar results achieved

16

* Bench scale test work focused on available reagent suite with number of stages of flotation – conventional phosphate reverse flotation, open circuit, elevated temp.

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

PROCESSING FLOW CHART

17

› Processing - crush, grind & flotation

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

MINING

18

› Mining – staged approach

› Waste – disposed near base of mining

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

THE MARKET

19

Source: Indexmundi, World Bank

Annual Consumption (Mt nutrients) Global Fertilizer Consumption (Mt nutrients)

N P2O5 K20 Total

2007/08 100.8 38.5 29.1 168.4

2008/09 98.3 33.9 23.1 155.3

2009/10 102.2 37.6 23.6 163.4

2010/11 104.2 40.6 27.5 172.3

2011/12 107.8 40.6 27.7 176.1

2102/13(e) 107.6 40.4 28.0 176.0

Change -0.2% -0.5% 1.2% 0.0%

2013/14(f) 109.6 41.1 28.7 179.5

Change 1.8% 1.8% 2.6% 2.0%

2014/15(f) 111.9 42.3 30.1 184.3

Change 2.1% 2.7% 4.9% 2.7%

Source: IFA Agriculture, Dec 2013

0

200

400

600

800

1000

1200

1400

Jan-0

4

Jul-0

4

Jan-0

5

Jul-0

5

Jan-0

6

Jul-0

6

Jan-0

7

Jul-0

7

Jan-0

8

Jul-0

8

Jan-0

9

Jul-0

9

Jan-1

0

Jul-1

0

Jan-1

1

Jul-1

1

Jan-1

2

Jul-1

2

Jan-1

3

Jul-1

3

Phos Rock DAP TSP UREA KCl

Fertiliser Prices USD per Tonne – FOB various Ports – Rock Phos Morocco

Source: IndexMundi, World Bank

Phos Rock – DAP Price – DAP Nola Swap Contracts Feb-April 2014

0

200

400

600

800

1000

1200

1400

Jan-0

4

Jul-0

4

Jan-0

5

Jul-0

5

Jan-0

6

Jul-0

6

Jan-0

7

Jul-0

7

Jan-0

8

Jul-0

8

Jan-0

9

Jul-0

9

Jan-1

0

Jul-1

0

Jan-1

1

Jul-1

1

Jan-1

2

Jul-1

2

Jan-1

3

Jul-1

3

Jan-1

4

DAP Price Phos Rock Price

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

DEMAND & TUNISIAN SUPPLY

Demand

› Fertiliser demand – rising following a pause in 2012/13 *

› Fertiliser forecast demand – 2.0% rise in 2013/14 & 2.7% 2014/15 *

› Phosphate forecast demand – 1.5% rise in 2013/14 & 2.7% 2014/15 *

Tunisia – global player

› Top 5 – rock producer in the world (exporting globally)

› Top 5 – Diammonium Phosphate (DAP) exporter

› Top 2 – Trisodium Phosphate (TSP) exporter

› Discovered – 1885 (1886 mining begins)

Source: 39th International Fertiliser Assoc. Enlarged Council Meeting, Paris Dec 2013: Short Term Fertiliser Outlook 2013-2014, PHeffer & M.Prud’homme

20

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

TUNISIA

Mining

› Mining Tax: 25% (tax exemption first 5 years)

› Royalty: 1% of gross revenue

› Repatriation allowed: no tax on shareholder dividends

› Downstream processing attracts 10-year tax holiday

Country

› Political – caretaker Govt with elected Constitutional Assembly

› New projects – strong support; employment key; educated population

› GDP Growth – 3.6% (2012) & 4.0% (2013F). Source: IMF

Chaketma

› Unemployment – 21% (National 13%) and regionally, poorest in Tunisia

› Youth population – more than 67% of local population under 20 years old

› Jobs – priority; revitalise old mining province; flow-on opportunities; utilise existing infrastructure

21

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

SUMMARY – WHY INVEST?

› Location – proximity to Europe

› Country – in-country phosphate expertise & infrastructure

› Quality – Northern Africa is a key global phosphate supplier

› Product – large, good grade, low impurities

› Resource – JORC compliant (two of six prospects drilled)

› Life – +35 years (+50 years achievable)

› Costs – low

› Infrastructure – roads, rail, ports, gas, electricity & water

› Demand – industry player interest

› Financiers – discussions underway

› Board/Management – credible & experienced

22

For

per

sona

l use

onl

y

Celamin Holdings NL | February 2014

Celamin Holdings NL

www.celaminnl.com.au

CONTACT US

For

per

sona

l use

onl

y