for personal use only - asxalexium supplies to 12 mattress brands, several of which are the top 10...

TRANSCRIPT

1

September 2017

For

per

sona

l use

onl

y

1 Company Overview

2 Who We Are

3 Business Model & Strategy

4 Key Markets

5 Market Opportunities

6 Financial Analysis

7 2018 Outlook

8 Management Bios and Company History

2

September 2017 Investor PresentationF

or p

erso

nal u

se o

nly

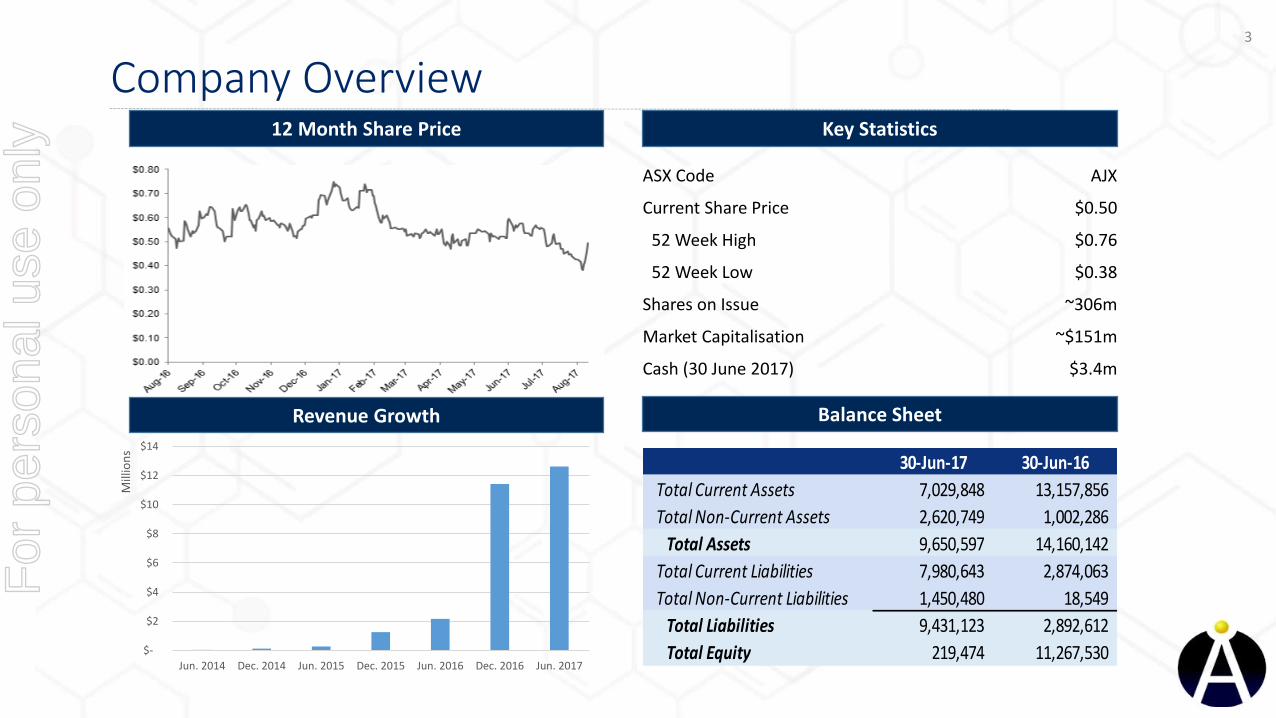

Key Statistics

ASX Code AJX

Current Share Price $0.50

52 Week High $0.76

52 Week Low $0.38

Shares on Issue ~306m

Market Capitalisation ~$151m

Cash (30 June 2017) $3.4m

$-

$2

$4

$6

$8

$10

$12

$14

Jun. 2014 Dec. 2014 Jun. 2015 Dec. 2015 Jun. 2016 Dec. 2016 Jun. 2017

Mill

ion

s

Company Overview3

30-Jun-17 30-Jun-16

Total Current Assets 7,029,848 13,157,856

Total Non-Current Assets 2,620,749 1,002,286

Total Assets 9,650,597 14,160,142

Total Current Liabilities 7,980,643 2,874,063

Total Non-Current Liabilities 1,450,480 18,549

Total Liabilities 9,431,123 2,892,612

Total Equity 219,474 11,267,530

12 Month Share Price

Revenue Growth Balance Sheet

For

per

sona

l use

onl

y

1 Company Overview

2 Who We Are

3 Business Model & Strategy

4 Key Markets

5 Market Opportunities

6 Financial Analysis

7 2018 Outlook

8 Management Bios and Company History

4

September 2017 Investor PresentationF

or p

erso

nal u

se o

nly

Who are We?

➢ Alexium International is a speciality chemicals developer based in Greer, South Carolina, USA, with its headquarters in Perth, WA.

➢ Focus on environmentally friendly, non-hazardous Flame Retardants (FR) and Phase Change Materials (PCM) that offer superior performance

➢ Cost effective, patented Solutions for both textile and non-textile markets

➢ Formulations made as a single step, drop-in solution that can be added at any finishing facility around the globe with no changes to equipment

➢ Rapid growth in sales from A$0.4m in 2015 to A$24m in 2017

➢ Identified addressable market opportunity in excess of US$3.0bn

Environmentally-Friendly FR Solutions

Knowledgeable Formulation Experts

Extensive Customer Support

Exceptional FR Performance

Innovation Driven

5F

or p

erso

nal u

se o

nly

➢ Capable of producing extremely wide range of cost–effective chemical solutions at full commercial volumes using a network of toll manufacturers

➢ Develop highly innovative and robust chemical solutions ready-to-use at our customers facility from day one

➢ IP portfolio of 20+ global patent applications covering chemical structures and applications

What do we produce?6

For

per

sona

l use

onl

y

1 Company Overview

2 Who We Are

3 Business Model & Strategy

4 Key Markets

5 Market Opportunities

6 Financial Analysis

7 2018 Outlook

8 Management Bios and Company History

7

September 2017 Investor PresentationF

or p

erso

nal u

se o

nly

➢ Alexium team has over 150 years of collective experience in chemical synthesis, manufacturing, product development and sales➢ CEO and Chief Scientist PHDs in chemistry, 8

R&D staff all PHDs

➢ Identify key markets in significant transition that are underserved by current market players and/or structure

Attack those markets through combination of novel

How our strategy will achieve results

➢ Leverage low-capital manufacturing strategyand key relationship with major industryplayers to price competitively and impacttarget markets quickly

➢ Lower cost and Longevity; Keys to Success➢ Two most important products are up to

50% cheaper than incumbents➢ Remaining products are more durable

and regulation compliant

8F

or p

erso

nal u

se o

nly

Meets textile industry’s and regulators’ urgent demand for

“green” FR chemistry that passes new strict environmental

regulations

Award Winning Technology (WBT 2009, Frost & Sullivan Award,

TechConnect Innovation Award)

Cost and performance advantage over existing

textile solutions

Lightweight, durable and can be laundered

Major focus on sales - expanding sales on Alexiflam™, Alexiflam-

NF™, Alexiflam-SYN ™ and Custom FR

blends for fabrics

Alexium is shifting emphasis on sales/product/customer/logistics support, but is also quickly maturing new products

from a healthy product pipeline

Validation by strong and growing DoD relationship + commercial pipeline

Alexium has routinely shown itself to be unequalled in the

marketplace

Alexium's Compelling Advantage

9F

or p

erso

nal u

se o

nly

Global Reach with a Simple Model

Global Business model

➢ R&D all undertaken at head office in Greer, South Carolina (major hub of industry and excellent transport links)➢Doesn’t manufacture, this is all outsourced to 12 producers around the world; no constraints to ramping up production➢Most important relationship with ICL – currently largest producer of FR chemistry globally➢ Sales channels into each continent, but largely US centric at this stage – 48 sales reps globally➢Not a catalogue provider like competitors – can tailor chemistry specifically to clients needs

Alexium Operations

➢ New facility in Greer South Carolina has 25,000 square feet of office and lab space

➢ Ensures capability for continuing product and team expansion to meet demand growth

➢ Highly sophisticated purpose built state of the art laboratory

➢ Corporate and Sales teams now co-located with product support and R&D teams

➢ Nearby to Greenville Spartanburg International Airport

Where is our reach?10

For

per

sona

l use

onl

y

Why are We Different?

Novel Eco-

Friendly Chemistry

Alexium

Exceptional Value

Proposition

Clear Market Demand (Military/

Commercial)

Expanding Patent

Portfolio

Commercial & Military

Partnerships

Unique Proprietary Technology

11

The Alexium Strategy➢ Identify key markets in significant transition that are

underserved by current market players and/orstructure

➢ Provide unparalleled integration support with end usercustomers to assist early adoption and productinnovation

➢ Attack markets via value add reseller model to allowrapid global expansion

➢ Leverage low-capital toll manufacturing strategy andwith major industry players to allow rapid scale up andglobally established supply chainFor

per

sona

l use

onl

y

Product manufacturer

Commission finisher

Product testing

Commercial production order

Commercial production order

Chemical supplier Supply of product

Raw material order

Toll manufacturer

Raw material delivery

Supply of chemistry

Chemistry order

12

Business Development CycleF

or p

erso

nal u

se o

nly

Scale through asset-light operating model

➢ Strategic partnerships established to rapidly scale go-to-market capabilities.

➢ Manpak is in Australia, Brocolor in Germany; VLS in Belgium, Euroflam in the UK with the other partners being located in the US.

13

Toll Manufacturing/Supply ChainF

or p

erso

nal u

se o

nly

Alexium has established strategic partnerships in order to rapidly scale its go-to-market capabilities➢ Partnerships were carefully selected according to geography and sector expertise➢ 48 sales agents representing various Alexium target markets started in 2016

Global Distribution & Sales Agent Network

• Europe, Asia Transport and military & workwear segments

• Brazil Workwear, carpet, and transportation industries

• Australia & New Zealand Transportation, workwear, carpet, upholstery

• Southeast Asia: Myanmar, Vietnam, Indonesia, Thailand, Malaysia, Singapore

Polymers & formulated compounds sales groups

• Israel & Mediterranean Textiles (workwear, military, bedding, transportation) , polymers, plastics

Schmits Chemical Solutions

• Northern & Southern Europe Workwear, transportation, bedding, and military

Southern Solutions LLC

• South eastern US Polymers and textiles

14

PartnershipsF

or p

erso

nal u

se o

nly

1 Company Overview

2 Who We Are

3 Business Model & Strategy

4 Key Markets

5 Market Opportunities

6 Financial Analysis

7 2018 Outlook

8 Management Bios and Company History

15

September 2017 Investor PresentationF

or p

erso

nal u

se o

nly

Legislative changes to incumbent FR technology; Existing technology is progressively banned globally.

➢ EPA/EU moving to ban 65% of current FR chemistryThe FR market is a US$7bn p.a. industry, with now roughly 65% of the incumbent technology/chemistry under regulatory pressure globally. EPA => top 10 hit list => Outside of Asbestos, most of the remaining chemicals are halocarbons, meaning they contain chlorine, bromine and related halogen elements. These have been identified as hazardous to human health, with some causing cancers, fertility problems and other diseases. 41% of the world’s current bromine production going towards FR => worlds largest supplier is ICL (key Alexium strategic partner)

➢ EU already banned, 12 US states have already moved

The EU is already ahead of the US, banning bromine in 2015 after a report into the toxicity of the chemical was commissioned and delivered to the European Commission in 2014. Twelve states have enacted legislation banning or limiting the use of toxic FR, including California, New York, New Jersey, Massachusetts, Maryland and Washington

➢ Alexium product range is specifically non-toxic and environmentally friendly

Alexium chemistry has been independently verified as free from toxic chemicals, including bromine, halogens and formaldehyde

Regulatory demands for environmentally and biologically friendly solutions

16F

or p

erso

nal u

se o

nly

Fire Retardant Market

*Source: MarketsandMarkets’ Report on the Flame Retardant Market:

Market Drivers

➢ Increasing amounts of goods beingmanufactured require FR treatments

➢ Stringent fire safety regulations causingcompanies to look for more effective performance in FR

➢ Increased focus on environmentally friendlysolutions

➢ Evidence of toxicity and bio accumulation inhalogenated compounds and carcinogens

➢ New legislation in Europe & USArestricting/eliminating the use of severalbrominated/halogenated compounds

➢ Asia represents an equally large opportunityas import bans are placed on incumbentproducts

➢ Operating in a US$7BN market which has a forecastedcompound annual growth rate of ~5.7% until 2019

➢ 40 million tonnes of FR chemicals sold annually with anestimated market value of $7 billion in 2014

➢ Expected compound annual growth rate (CAGR) of 5.7%,rising to $10 billion by 2019

➢ Organophosphorus flame retardants have the highest rateof annual growth of 7.5%

➢ Europe and North America account for 46.7% of theworld’s FR chemical consumption

➢ FR used in textiles, flooring and furnishings, automotive,transportation, building and construction, electronics,wires and cables industries

➢ Flooring and furnishings and textiles currently serviced byAlexium are worth $2.5 billion growing to $3.4 billion in2019 worldwide

Key Stats

17F

or p

erso

nal u

se o

nly

Alexicool, the break-through PCM chemistry that underpins the next wave of heat resistant and cooling fabrics/textiles for theapparel, mattress and bed linen industries.

What is a PCM?

➢ Alexicool is the chemistry that can improve the efficiency of apparel and other textiles to absorb heat and moisture, andkeep the body cool, in a manner superior to that which is already available, while also lasting for a longer wash-cycle.

➢ The microscopic molecule attaches to a fibre and can retain heat and cool the textile it is applied to, and then re-chargeitself when the heat source is removed (i.e. a human).

➢ It has quickly become Alexium’s fastest growing product line, and in our view, can continue to be so over the medium term.

➢ Major brands in this industry (majority apparel) include Nike Dri-FIT, Underarmour HeatGear or Coolswitch, Reebok ONESeries to name but a selection of the products available.

Opportunities

➢ Apparel: Key national supplier has commenced trials for use in their range of sweat-wicking/cooling fashion and sports products.

➢ Mattresses: Alexium supplies to 12 mattress brands, several of which are the top 10 largest in the US, through a network of commissioned finishers.

➢ Bed linen: Alexium recently began working with Pegasus and is seeing initial solid success with cool touch pillow shells and mattress pads.

PCM- A new standard in Textiles18

For

per

sona

l use

onl

y

1 Company Overview

2 Who We Are

3 Business Model & Strategy

4 Key Markets

5 Market Opportunities

6 Financial Analysis

7 2018 Outlook

8 Management Bios and Company History

19

September 2017 Investor PresentationF

or p

erso

nal u

se o

nly

Alexium’s Current Opportunities

Military

Transportation

Home Furnishings

Work Wear

Outdoor

2017 Snapshot

Defense Sector➢ Successfully downselected for the Natick Green Initiative, additional grant funding expected 2Q 2015➢ Working directly with major prime contractor to the U.S. Army to develop and launch next-

generation FR Army Combat Uniform (FRACU)

Transportation Sector➢ Produced samples for a total of 6 clients which pass all FR specifications➢ Proceeded to full-scale commercial trials for 5 of those clients➢ Revenue generation already commenced for 1 of the clients

Home Furnishings Sector➢ Produced samples for 8 clients➢ Proceeded to full-scale commercial trials for 6 of those clients➢ Revenue generation commenced for 1 of client

Work Wear Sector➢ Exclusive Partnership with iTextiles (Producer of 60% of all Denim Work Wear in the World)➢ Co-Branding Initiative

Outdoor Fabrics Sector➢ Produced samples for two of the largest suppliers to this market➢ Developed sales and marketing agreement with one of those customers➢ Substantial progress made in establishing manufacturing and supply-chain presence in Asia

20F

or p

erso

nal u

se o

nly

1 Company Overview

2 Who We Are

3 Business Model & Strategy

4 Key Markets

5 Market Opportunities

6 Financial Analysis

7 2018 Outlook

8 Management Bios and Company History

21

September 2017 Investor PresentationF

or p

erso

nal u

se o

nly

Financial Overview

➢ Total revenue grew 604% over the prior fiscal year to $24.02M

➢ Margin on chemical sales grew by 13.3 percentage points

$0.36M $0.24M $0.39M

$3.41M

$24.02M

-

5

10

15

20

25

2013 2014 2015 2016 2017

MIL

LIO

NS

Five Year Revenue Trend

22F

or p

erso

nal u

se o

nly

Financial Overview

$3.0M $23.8M

(12.08%)

1.24%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

-

5

10

15

20

25

2016 2017

MIL

LIO

NS

2016 vs 2017

Sales Revenue Gross Margin

➢ Revenue from chemistry sales up 693%from $3M to $24M

➢ Margin on chemical sales grew by 13.3percentage points

➢ Sales revenue grew 12% in the second half ofthe year as a result of continued gains in themattress industry

➢ Gross margin gain of 4.2 percentage from H1 to H2 was due to supply chain improvements and production scale pricing with raw material supplier. This trend has continued to improve margins.

$11.2M $12.6M

(0.97%)

3.21%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

-

2

4

6

8

10

12

14

H1 H2

MIL

LIO

NS

FY 2017 First Half vs Second Half

Sales Revenue Gross Margin

23F

or p

erso

nal u

se o

nly

Financial Overview

➢ Revenue increased by 15% in Q4 due to beddingsales ramping to record highs

➢ Gross margins increased by 32.3 percentage points asramp up in bedding sales allowed for better rawmaterial pricing in Q4 from economies of scale

➢ Revenue in Q4 showed continued growth over priorperiods

➢ June revenues slightly lower than previous months dueto US Independence Day holiday slowing production forend customers

➢ Margins showed steady progression towards ourcalendar end year target of 40%

➢ 31% margins on June sales directly contributed toAlexium reaching a cash neutral position on pace tomeet its mid-year goal

$5.87M $6.75M

(14.08%)

18.23%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

-

1

2

3

4

5

6

7

Q3 Q4

MIL

LIO

NS

Q3 vs. Q4

Sales Revenue Gross Margin

$2.2M $2.45M $2.1M

6.47%

18.17%

30.63%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

-

0.5

1.0

1.5

2.0

2.5

3.0

April May June

MIL

LIO

NS

Q4 by Month

Sales Revenue Gross Margin

24F

or p

erso

nal u

se o

nly

2017 Financial Results

Revenue from ordinary activities

up 595% to 24,034,416

Loss from ordinary activities for the period after

tax attributable to members

down 21% to (12,155,268)

Net loss for the period attributable to members down 21% to (12,155,268)

2017 2016 Improvement

EBITDA (11,010,566) (15,240,398) 27.75%

Basic loss per share (cents per share) (4.02) (6.97) 42.32%

➢ Revenue from chemistry sales up 693% from $3M to $24M

➢ Margin on chemical sales grew by 13.3 percentage points

➢ EBITDA up 27.75%

➢ First ever cash neutral month in June

➢ Final approval for new debt facility obtained on 9/1/17➢ Refinancing current debt at lower

rate➢ Drawing down additional $5M to

fund working capital

25F

or p

erso

nal u

se o

nly

Selling, General and Administrative CostsCurrent Period Previous Period % of Revenue % of Revenue

2017 2016 2017 2016

Administrative expenses (1,512,740) (1,361,276) 6.29% 39.37%

Depreciation and amortisation expenses (359,241) (204,473) 1.49% 5.91%

Employee benefits expense (5,104,877) (3,672,088) 21.24% 106.19%

Share based payments - (4,175,190) 120.74%

Research and development (1,878,367) (1,984,423) 7.82% 57.39%

Professional fees (1,525,349) (2,130,604) 6.35% 61.61%

Other expenses (1,507,547) (2,010,910) 6.27% 58.15%

Change in fair value of derivative liability (189,276) - 0.79% -

Finance costs (596,184) - 2.48% -

Total Expense (12,673,581) (15,538,964) 52.73% 449.37%

➢ ADMINISTRATIVE COSTS-Administrative costs increased this year by $0.15M, but dropped from 40% to 6% of total revenue. Continued reductions in administrative costs in relation torevenue are planned for FY2018. Alexium was able to realize several operational benefits from the new facility including a reduction in administrative costs byUS$0.15M to be realized over the first 5 years of the lease.

➢ DEPRECIATION AND AMORTIZATION-In October, 2016, Alexium finalized the build of its new, state of the art facility. Related depreciation and amortization expenses increased $155K for the period, butwas down as a percent of revenue.

➢ EMPLOYEE BENEFITS EXPENSE-Employee costs increased by $1.4M but decreased as a percent of total revenue to 21% from 108% in FY2016. This trend is expected to continue and the Company isexpecting a reduction in staffing costs in FY2018 as post year-end reductions have occurred. Board costs and Executive Director costs have been substantiallyreduced following a combination of the Board voting to lower Board and Committee Fees for FY18, the retirement of the Executive Director of Strategy and the moveof the Executive Chairman to Non-Executive Chairman.

26F

or p

erso

nal u

se o

nly

Cash Flow Statement 30-Jun-17 30-Jun-16

Cash flows from operating activities

Receipts from customers 22,433,226 3,318,758

Payments to suppliers and employees -34,774,370 -13,515,181

Interest received 12,018 44,018

Interest and other costs of finance paid -512,582 -

Goods & services tax (paid) / received from ATO 114,186 76,044

Net cash used in operating activities -12,727,522 -10,076,361

Cash flows from investing activities

Purchase of property, plant and equipment -1,597,678 -181,484

Investments in and maintenance of intangible assets - -28,276

Other non-current assets -21,529 -

Proceeds from disposal of property, plant and equipment 547 -

Net cash flows from investing activities -1,618,660 -209,760

Cash flows from financing activities

Proceeds from issue of ordinary shares - 6,000,000

Proceeds from exercise of options 663,033 3,906,113

Proceeds from borrowings 6,674,676 -

Payment of share issue costs - -396,000

Transaction costs related to loans and borrowings -126,085 -

Payment of financing lease principal -167,862 -

Net cash flows from financing activities 7,043,762 9,510,113

Net increase / (decrease) in cash held -7,302,420 -776,008

Cash and cash equivalents at the beginning of the period 11,218,556 11,621,603

Effects of exchange rate changes on cash -506,353 372,961

Cash and cash equivalents at the end of the period 3,409,783 11,218,556

CASH NEUTRALITY

➢Average monthly sales over $2.25M for the final quarter of FY17

➢Margins exceeding 30% in June a major contributor to cash neutral milestone

➢Margins continue through Q1 2018

CASH POSITION

➢$3.4M in cash and $1.4M in receivables at end of period

➢US$10M debt facility received final approval on 9/1/17

➢Alexium in strong position to fund organic growth going forward

27F

or p

erso

nal u

se o

nly

1 Company Overview

2 Who We Are

3 Business Model & Strategy

4 Key Markets

5 Market Opportunities

6 Financial Analysis

7 2018 Outlook

8 Management Bios and Company History

28

September 2017 Investor PresentationF

or p

erso

nal u

se o

nly

2018 Outlook

➢MILITARY

The Company will continue to work with strategic fabric and garment partners to advance its progress towardsachieving major military contracts in FY2018. Work will focus on breathability and weight of the base fabric asdurability of the flame retardant treatments continue to meet performance requirements. In addition, the Company will begin to identifypotential licensees of its proprietary Reactive Surface Treatment technology as global chemical and biological threats are increasing.

➢FORM STRATEGIC PARTNERSHIPS FOR GLOBAL ALEXIFLAM™ NF LAUNCH

Due to significant industry interest in the value proposition of Alexiflam™ NF, Alexium will be forming strategicpartnerships to maximize the value of Alexiflam™ NF for its shareholders. Those partnerships will likely includeexclusive licensees for various markets and manufacturing agreements.

➢IMPROVEMENT IN FINANCIALS AND PROFITABLE GROWTH

Through a combination of price increases and supply chain management, Alexium will continue to convert itsearlier market penetration revenue streams to profitability. In addition, increasing market share in current markets and expansion intonew markets will result in profitable growth.

➢EXPANSION OUTSIDE OF TEXTILES

Efforts began in FY2017 to diversify Alexium’s revenue streams outside of textiles. Several of these opportunities are expected tomaterialize in FY2018. While a continued push into epoxy/polymeric markets is ongoing, the Company also has market adoptions plannedin protective coatings and wood treatments.

➢CONTINUED GROWTH IN BEDDING AND PILLOWS

Planned expansion into the pillow market with Pegasus Home Fashions will continue to drive revenues upward and the number of beddingbrands using Alexium chemistry will increase. Through the reporting date Alexium has already added two new bedding customers.

➢COMMERCIALIZATION OF TENTING TREATMENT

Alexium’s all-in-one Oeko-tex Certified tent fabric treatment (including FR, water repellency, coatings and binders) to realize penetrationinto highly eco-conscious tenting market space.

29F

or p

erso

nal u

se o

nly

1 Company Overview

2 Who We Are

3 Business Model & Strategy

4 Key Markets

5 Market Opportunities

6 Financial Analysis

7 2018 Outlook

8 Management Bios and Company History

30

September 2017 Investor PresentationF

or p

erso

nal u

se o

nly

Board of DirectorsGavin Rezos – Non-Executive Chairman

▪ Extensive international investment banking experience

▪ Held CEO & Board positions in successful technology companies in Australia, the UK, US & Singapore

▪ Former Non-Executive Director of Iluka Resources, Department 13, Metalysis plc and former Investment Banking Director atHSBC

Craig Metz – Non Executive Director

▪ Partner at Nelson, Mullins, Riley and Scarborough LLP with over 20 years experience in legislative and regulatory affairs

▪ Served as Chief of Staff to the late Congressman Floyd Spence (R-SC)

▪ Held staff positions in the United States Senate and House of Representatives

▪ Appointed to senior positions in the Executive Branch of the Federal Government

Brigadier General Stephen Cheney, USMC – Non-Executive Director

▪ Former Inspector General of the Marine Corps and Commanding General of Parris Island Marine Base

▪ Former Deputy Executive Secretary to U.S. Defense Secretary Dick Cheney under President George H.W. Bush

▪ Sits on Secretary of State John Kerry’s Foreign Affairs Policy Board

31

Congresswoman Karen Thurman, (D-FL) – Non-Executive Director

▪ Congresswoman Karen Thurman served in the United States House of Representatives from 1993 to 2003

▪ Prior to being elected to Congress in 1992, Thurman served in the Florida State Senate for 10 years

▪ She obtained her bachelor's degree in Education from the University of Florida

For

per

sona

l use

onl

y

Executive Management32

Dirk Van Hyning– Chief Executive Officer

Dr. Van Hyning received his BS in Chemical Engineering from North Carolina State University before receiving his MS and Ph.D. in Chemical Engineering from The University of Illinois at Urban-Champaign. Dr. Van Hyning has extensive experience in product development and scale-up, and previously worked at Milliken & Company.

Aaron Krech- Chief Financial Officer

Mr. Krech serves as the Chief Financial Officer at Alexium International Group Limited. Mr. Krech has previous experience in corporate treasury analysis and risk management at Blue Cross and Blue Shield. He has earned a business degree from the Darla Moore School of Business at the University of South Carolina.

Robert Brookins- Vice President of Research and Product Development

Dr. Robert (Bob) Brookins- Ph.D., M.A.E. B.A. B.Sc is Vice President of Research and Product Development. Dr. Brookins has experience in organic synthesis, materials chemistry, and chem/bio decontamination. He received his Ph.D. from the University of Florida in the areas of synthesis and characterization of conjugated poly-electrolytes and polymers with an emphasis on developing new polymerization methods. Upon completion of his Ph.D., he worked at the US Air Force Research Laboratory at Tyndall AFB, where he developed decontamination methods for chemical and biological threats, and developed novel synthetic routes for reactive and functional surfaces.

For

per

sona

l use

onl

y

Executive Management, Continued

33

Mark Wise– Vice President of Investor Relations

Mr. Wise possesses over 30 years of experience in investment markets and previously was a Portfolio Manager in New York, where he managed portfolios of Asian and Australian equities. Mr. Wise earned a Bachelor of Commerce degree with a focus in Accounting and Finance from the University of New South Wales in Sydney Australia.

Brian Enlow– Vice President of Finance

Previously Alexium’s Financial Reporting Manager, his professional background includes public accounting, both audit and taxation, as well as corporate accounting roles focusing on financial reporting and cost accounting. Mr. Enlow is a graduate of The University of Arkansas at Fayetteville where he received a BS in Financial Management and Investment, and The University of Texas where he studied Accounting.

Jessica Hutchison- Vice President of Human Resources

Jessica holds a Bachelor of arts in English from Georgia Southern University and a Masters of Science in Human Resources from Western Carolina University. She possesses several years of experience in the Human Resources Industry.

Scott Hunter- Vice President of Sales and Marketing

Scott holds a Bachelor of Science in Chemistry from the University of Dayton in Dayton, Ohio. He possesses over 20 years’ experience in solution sales and leadership within the specialty chemical field with a successful track record within both Fortune 500 and mid-cap privately held organizations. Scott is a versatile leader who is passionate about identifying root-barriers impeding success while establishing strategic processes, partnerships, and innovative approaches to unlock growth within companies.

For

per

sona

l use

onl

y

34

Company HistoryF

or p

erso

nal u

se o

nly