for producer or broker/dealer use only. not for public distribution. life insurance review a sales...

TRANSCRIPT

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

Life Insurance ReviewA Sales Tool for Business Owners

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

• Special life insurance needs of business owners.

• Why a Life Insurance Review.

• 6 Questions to ask business owners.

• Hypothetical classic client situations.

• MetLife support.

Overview

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

Small Business Firms1:

• 5.5 million U.S. family businesses

• 57% of the U.S. GDP ($8.3 trillion)

• 78% of all new job creation

1 Family Enterprise USA 2011

The Significance of Business Owners

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

• 40% of U.S. businesses face a transfer of ownership issue at any given time.2

• 47% of middle market business owners 55 years and older are interested in selling their business within 3 years, yet over 90%of owners have not initiated the planning process. 2

• 24% of owners said they have not planned their business exit. 2

• Only 47% have business life insurance for some purpose.3

2 The Exit Advisor, Exit Strategy and Compensation Planning, April 2012.3 LIMRA’s Marketfacts Quarterly-Spring 2009.

The Reality

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

• Key Person Protection

• Business Succession/Continuation

– Partnership issues

– Sale at fair market value

– “Fair” inheritance to children with differing levels of business involvement

• Executive Benefits and Compensation

– Recruit, Retain, Reward, Retire

– Help address reverse discrimination issues

Role of Life Insurance: Business Owners

Why a Life Insurance Review?

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

• Portfolio review – Life Insurance Review

• What a review does

– Reviews a client’s needs

• Examines original vs. current goals

– Reviews existing life insurance to current goals

• Who needs to do a life insurance review?

– Financial advisors

– Trustees

– Business Owners

Why a Life Insurance Review?

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

• Family changes

– Marriage, birth, divorce

– Term to permanent

– Term at a better price

• Policy insufficient for current needs

• Changing job and benefits

• Owning a business

• Education funding

• Changes in retirement income needs or savings options

• Buying a home

Personal Changes

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

• Ownership

– New partners

– Retired partners

• Valuation

• Profitability

• Liquidity

• Estate tax potential

• Older children entering business

• Need for executive benefits

• Key person coverage needs

Business Changes

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

• Underperforming policies

• Changing insurer ratings

• Some policies scheduled for a jump in premiums

• Newer products

– More cost efficient

– Better guarantees.5

• New riders may offer improved options

• Improved underwriting

5 Guarantees refer to certain features or optional riders available on some insurance policies and are subject to product terms, exclusions and limitations and the insurer's claims-paying ability and financial strength.

Life Insurance Changes

6 Questions to Ask Business Owners

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

Do you have adequate funds to maintainyour lifestyle at retirement?

Distributions are generally treated first as tax free recovery of basis and then as taxable income, assuming the policy is not a Modified Endowment Contract (MEC). However, different rules apply in the first fifteen policy years, when distributions accompanied by benefit reductions may be taxable prior to basis recovery. Non-MEC loans are generally not subject to tax but may be taxable when the policy lapses, is surrendered, exchanged or otherwise terminated. In the case of a MEC, loans and withdrawals are taxable to the extent of policy gain and an additional 10%tax may apply if taken prior to age 591/2. Always confirm the status of a particular loan or withdrawal with a qualified tax advisor. Cash value accumulation may not be guaranteed depending on the type of product selected. Investments in variable life insurance are subject to market risk, including loss of principal

#1 Retirement Planning

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

If you were to suffer a disability, would yoube able to meet your financial obligations and/or

continue to run your business?

#2 Disability

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

If a key employee dies or resigns, would your business continue to be as successful?

#3 Key Person

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

What steps have you taken to prepare forthe future transfer your business to others at

a fair price?

#4 Exit Planning

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

Do you have benefit plans in place to recruit, reward and retain key employees?

#5 Executive Benefits

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

Can you successfully transfer the business assets you have worked a lifetime to accumulate?

#6 Estate Planning

HypotheticalClassic Client Situations

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

Bill & Ted Set up a cross-purchase when manufacturing

business was worth $4,000,000 7 years ago

Case Study

Were 50:50 Owners

Each bought a $2,000,000

Term Policyon the other

Bill paid more for Ted’s Policy

•Smoker

•Balanced costs with salary increase

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

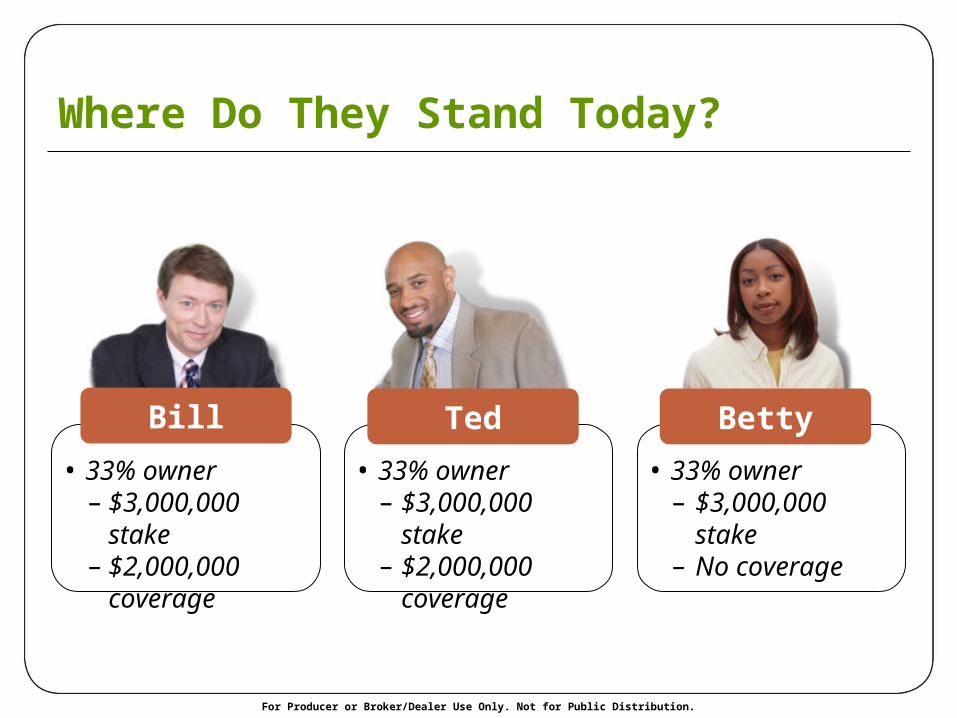

• 33% owner– $3,000,000 stake– No coverage

Betty

• 33% owner– $3,000,000 stake– $2,000,000

coverage

Ted

• 33% owner– $3,000,000 stake– $2,000,000

coverage

Bill

Where Do They Stand Today?

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

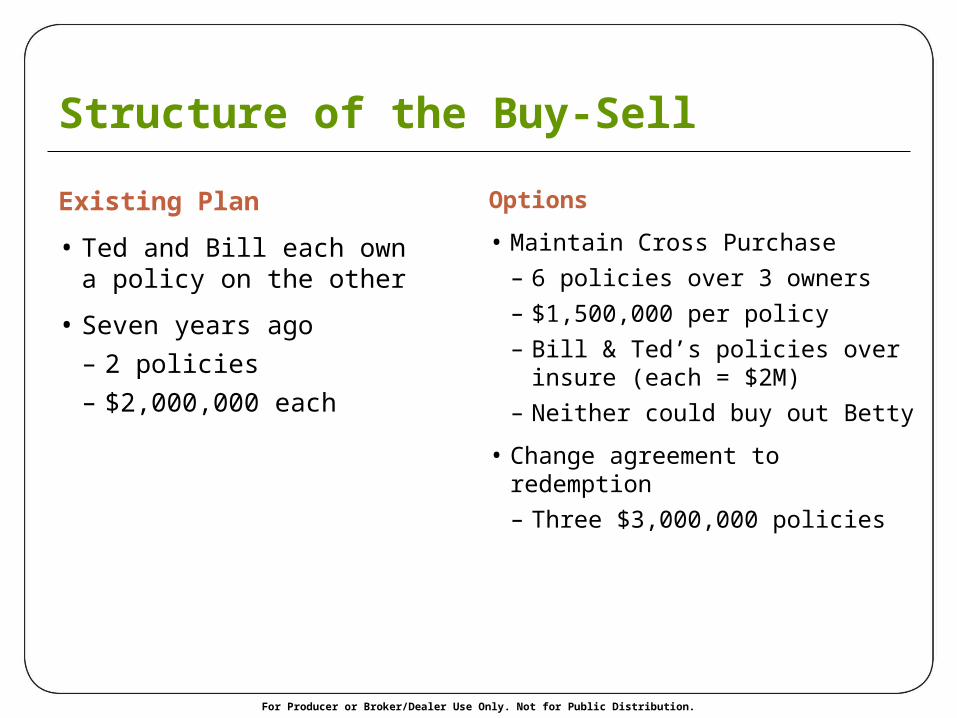

Existing Plan

• Ted and Bill each own a policy on the other

• Seven years ago

– 2 policies

– $2,000,000 each

Options

• Maintain Cross Purchase

– 6 policies over 3 owners

– $1,500,000 per policy

– Bill & Ted’s policies over insure (each = $2M)

– Neither could buy out Betty

• Change agreement to redemption

– Three $3,000,000 policies

Structure of the Buy-Sell

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

• Changing to permanent coverage

– Policy cash values can build business assets

– Can offer lifetime benefits

– Can fund post-retirement benefit programs

• Underwriting changes

– Ted no longer smokes

• Product changes

– May want to weigh new policy designs

Potential Benefits of changing coverage from term to permanent

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

• Lower Bill & Ted’s coverage to $1,500,000 each

• Obtain coverage on Betty

• Betty purchases coverage on Bill and Ted

• Evaluate cost of new coverage

Or

• Drop term in favor of properly structured and funded cash value life insurance

– Look to the cash value as a potential means of buy-out

Option 1 – Continue Cross Purchase

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

• Fewer policies, paid for by the business

• Now 3 @ $3,000,000 vs. 6 @ $1,500,000

• Use existing policies to help fund

Or

• Replace existing term with permanent cash value

• Uses for cash value

– Fund lifetime buyouts

– Fund nonqualified benefit programs

Certain transfers of policies may trigger adverse income tax consequences.Loans and withdrawals will decrease the cash value and the death benefit. If the policy has not performed as expected and to avoid a policy lapse, distributions may need to be reduced, stopped and/or premium payments may need to be resumed. Should the policy lapse or be surrendered prior to the death of the insured, there may be tax consequences.

Option 2 – Establish Redemption Agreement

MetLife Support

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

• Dedicated life insurance sales desk

• Marketing materials

• ePresentations

• Advanced Sales Center assistance for complex situations

Please note: This document is designed to provide introductory information on the subject matter. MetLife does not provide tax and legal advice. Clients should consult their attorney and/or tax advisor before making financial investment or planning decisions.

MetLife Support

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

• Permanent insurance

– Inforce ledger

– Copy of policy

• Term policy

– Copy of policy

• Employer benefit

– Benefit information

What Information Will I Need?

For Producer or Broker/Dealer Use Only. Not for Public Distribution.

Pursuant to IRS Circular 230, MetLife is providing you with the following notification: The information contained in this document is not intended to (and cannot) be used by anyone to avoid IRS penalties. This document supports the promotion and marketing of insurance products. Your clients should seek advice based on their particular circumstances from an independent tax advisor.

MetLife, its agents and representatives may not give legal or tax advice. Any discussion of taxes herein or related to this document is for general information purposes only and does not purport to be complete or cover every situation. Tax law is subject to interpretation and legislative change. Tax results and the appropriateness of any product for any specific taxpayer may vary depending on the facts and circumstances. You clients should consult with and rely on their own independent legal and tax advisers regarding their particular set of facts and circumstances.

Prospectuses for Equity Advantage Variable Universal Life, and for the investment portfolios offered thereunder, are available from MetLife. The policy prospectus contains information about the policies features, risks, charges and expenses. Investors should consider the investment objectives, contract features, risks, charges and expenses of the investment company carefully before investing. The investment objectives, risks and policies of the investment options, as well as other information about the investment options, are described in their respective prospectuses. Clients should read the prospectuses and consider this information carefully before investing. Product availability and features may vary by state.

MetLife life insurance policies have limitations, exclusions, charges, termination provisions and terms for keeping them in force. There is no guarantee that any of the variable investment options in this product will meet their stated goals or objectives. The account value is subject to market fluctuations so that, when withdrawn, it may be worth more or less than its original value. Guarantees are based on the claims-paying ability and financial strength of the issuing insurance company.

Life insurance is medically underwritten. Clients should not cancel their current coverage until their new coverage is in force. Surrender charges may be due on an exchange of one contract for another. A change in policy may require a medical examination. Surrenders may be taxable. Clients should consult their own tax advisors regarding tax liability on surrenders.

Life insurance products are issued by MetLife Investors USA Insurance Company, Irvine, CA 92614, in all jurisdictions except New York, where permanent life insurance products are issued by Metropolitan Life Insurance Company. New York, NY 10166 and term life insurance products are issued First MetLife Investors Insurance Company, New York, NY 10166. All guarantees are subject to the claims-paying ability and financial strength of the issuing insurance company. Variable products are distributed by MetLife Investors Distribution Company, Irvine, CA 92614. All are MetLife companies. June 2012

Insurance Products are:• Not A Deposit • Not FDIC-Insured • Not Insured By Any Federal Government Agency

• Not Guaranteed By Any Bank Or Credit Union • May Go Down In Value

BDVL22614 L00612265603[0614]© 2012 METLIFE, INC. PEANUTS © 2012 Peanuts Worldwide

Legal Disclaimer