for the common good? the effects of private …igov.berkeley.edu/sites/default/files/feng, xunan -...

TRANSCRIPT

Xunan Feng City University of Hong Kong

Anders C. Johansson*

Harvard University Stockholm School of Economics

Tianyu Zhang

City University of Hong Kong

November 2010

* Corresponding author, Stockholm School of Economics, P.O. Box 6501, SE-113 83 Stockholm,

Sweden. Phone: +46-8-736 9360. Fax: +46-8-31 30 17. Email: [email protected]. Johansson

acknowledges financial support from the Bank of Sweden Tercentenary Foundation (RJ), the Swedish

Foundation for International Cooperation in Research and Higher Education (STINT), and the Swedish

School of Advanced Asia-Pacific Studies (SSAAPS).

Preliminary draft, please do not quote

For the Common Good? The Effects of Private

Entrepreneurs’ Political Participation in China

1

For the Common Good? The Effects of Private

Entrepreneurs’ Political Participation in China

Abstract We study the benefits of private entrepreneurs entering into politics in China. Using original hand-collected data on political participation of entrepreneurs that control listed firms, we document evidence of rent seeking through their political networks and several potential channels through which rent seeking is realized. It is shown that political participation results in increased stock performance and operating performance, consistent with the rent-seeking argument. As rent-seeking channels, firms controlled by politically active private entrepreneurs are able to access debt financing better, lessen their tax burden, and engage in favorable M&A activities, at least partly explained by better access to regulated industries. This study thus sheds light on the benefits of political participation for private entrepreneurs in China and, more importantly, document several channels used to exploit political networks built up through active participation in politics. JEL Classification: G30; G32; G34; H20; P26 Keywords: Political participation; Entrepreneurial firms; Corporate governance; Rent seeking; Capital structure; Tax burden; Mergers and acquisitions; Regulated industry; China

2

1 Introduction

Do private entrepreneurs become politically active for the good of society? Or

do they enter into politics looking for preferential treatment and access to rent-seeking

opportunities? A small but growing literature has studied private entrepreneurs that

participate in politics in transition economies. The focus in most such studies is

mainly on the potential effects on firm value and operating performance. There are

only a few studies that identify and test the significance of different potential rent-

seeking channels that politically active private entrepreneurs may exploit through

their political connections.

This paper examines the valuation effect of political participation by private

entrepreneurs in China and analyzes several rent-seeking channels that lead to such an

effect. By identifying when a private entrepreneur enters into politics, we are able to

explore the potential benefits of doing so, and the channels through which the

entrepreneur may exploit his or her new political position. Such potential rent-seeking

channels include better access to capital, preferential tax treatment, and superior

access to regulated industries through corporate deals. China is perhaps especially

well suited for our study. Chinese private entrepreneurs have been politically active

for a long time, especially so after the then President Jiang Zemin welcomed them

into the Chinese Communist Party (CCP) in 2001. In a business environment marked

by poor legal protection, ambiguous property rights, and rent seeking, many Chinese

private entrepreneurs have tried to develop close ties to local and national politicians.

3

It is therefore valid to raise the question whether they enter into politics for the

common good or mainly to exploit rent-seeking opportunities otherwise not available

to them. To understand the workings and effects of entrepreneurs’ political

participation we thus (1) examine the effect of political participation on a firm’s long-

term stock performance and operating performance; and (2) study different potential

rent-seeking channels made available through political participation.

To analyze political participation, we identify when an entrepreneur (or one of

his or her family members) becomes a member of the Congress of the Chinese

Communist Party (CCCP), the National People’s Congress (NPC), the Chinese

People’s Political Consultative Conference (CPPCC), or any of their provincial

counterparts. Our hand-collected data set covers all listed entrepreneurial firms during

the period 1993-2009. For this period, we find 73 cases of private entrepreneurs

controlling listed firms that have entered into politics. We then perform an event study

based on the point in time when a private entrepreneurs becomes a member of any of

the political state entities mentioned above. We find that political participation has a

significant positive effect on long-run stock performance and that this effect increases

over time during an extended period after the event. We also document that political

participation has a significant positive effect on several accounting measures of

operating performance.

Having identified the positive effects of political participation on firm

performance and firm value, we then explore several potential channels through

which political participation enables such effects. Political participation facilitates

4

debt financing as indicated by higher leverage and longer maturity in debt for firms

controlled by politically active private entrepreneurs. Political participation also

improves the access to regulated industries through merger and acquisitions (M&As).

Finally, political participation reduce firms’ tax burden measured as the effective tax

rate.

Overall, our empirical findings provide a picture of the significant benefits that

stems from political participation by private entrepreneurs becoming in China. In

addition to documenting the effects on firm value and operating performance, we are

able to identify several channels through which politically active entrepreneurs are

able to exploit their rent-seeking opportunities. These results have important

implications for the literature on the relationship between entrepreneurs and the

political sphere and rent seeking in transition economies.

The remainder of this paper proceeds as follows. Section 2 provides a review

of the related literature on rent seeking and how entrepreneurs use political affiliations

to improve their business. Section 3 discusses the institutional background and the

relationship between private entrepreneurs and politicians in China. This section also

develops the hypotheses for the empirical analysis. Section 4 describes the data

sample and presents the initial empirical results of the effects on firm value and

operating performance. Building on these results, Section 5 then analyzes the different

rent-seeking channels. Finally, Section 6 concludes the paper.

5

2 Literature Review

This paper relates to research that focuses on rent seeking and how

entrepreneurs use their political ties to benefit their businesses. In her seminal article,

Krueger (1974) argues that it is natural for firms to devote economic resources toward

rent seeking in order to compete for favorable policy decisions. In general, politicians

are able to influence firms through a variety of policy decisions. Politicians may do

this for political as well as personal objectives (e.g., La Porta et al., 2002; Rajan and

Zingales, 2003). Government decisions can have a significant effect on firm

performance and firm value through various channels, such as preferential access to

finance, better access to different forms of government subsidies, tax benefits, and

reduced regulatory constraints.

Numerous studies have analyzed how political connections play an important

role for U.S. firms, including Roberts (1990), Kroszner and Stratmann (1998),

Jayachandran (2006), Knight (2006), Benmelech and Moskowitz (2007), Goldman et

al. (2009), and Cooper et al. (2010). Besides research on the U.S., there is a small but

growing literature on the importance of political relationships in other countries.

Faccio (2006) performs a cross-country analysis on firms with political connections.

She finds that such firms are more likely to be listed in countries with higher levels of

corruption and weaker legal systems. Fisman (2001) documents the effects of

announcements about the health condition of the former President of Indonesia,

Suharto. He shows that companies with close ties to the Suharto family experienced

abnormal losses in market value after news of Suharto’s deteriorating health was

6

published. Johnson and Mitton (2003) study the decision by Malaysia’s Prime

Minister Mahathir to fire the Deputy Prime Minister Anwar Ibrahim and impose

capital controls after the outbreak of the Asian financial crisis. They find that firms

with close ties to Mahathir benefitted greatly as a result of the capital controls. Faccio

et al. (2006) show that politically connected firms are more likely to be bailed out by

the government during times of distress. Fan et al. (2007) analyze how political

connections affect firm performance after partial privatizations and public offerings of

Chinese state-controlled firms. They find that political connections affect firm

performance and market value negatively, indicating that politicians continue to

extract resources from state-controlled companies after they have been partially

privatized. Finally, Claessens et al. (2008) analyze the Brazilian 1998 and 2002

elections. They document that higher campaign contributions result in higher stock

returns around announcements of election results.

Even though most research on political relationships and rent seeking has

focused on finding evidence for firm effects, a limited number of recent studies have

tried to identify potential rent-seeking channels. The channel that has been analyzed

most thoroughly is that of preferential access to financing. Faccio et al. (2006),

analyzing firms in 35 different countries, find that politically connected firms tend to

have higher leverage ratios. Johnson and Mitton (2003) show that politically

connected firms in Malaysia had significantly higher debt-asset ratios before the

Asian financial crisis and that they had less short-term debt, indicating that politically

connected firms have better access to long-term debt financing. Dinc (2005) looks at

7

the behavior of banks in developing countries. By focusing on political elections, he

finds that political motivations are a part of government-owned banks’ decision-

making process. Khwaja and Mian (2005) analyze politically connected firms in

Pakistan. They find that such firms have preferential access to loans and that they

borrow twice as much as other firms. As a result, politically connected firms in their

sample exhibit much higher default rates. Charumilind et al. (2006) analyze firms

with strong connections to politicians and banks in Thailand. They find that such

firms had significantly better access to long-term debt before the financial crisis

erupted in 1997. While these initial studies on rent-seeking channels made available

through political connections are important, our study provides a more comprehensive

picture. In addition to analyzing capital structure changes due to political

participation, we are able to identify other channels that politically active

entrepreneurs in China are able to exploit, such as increased tax benefits and access to

beneficial corporate deals.

3 Institutional Background and Hypotheses

3.1 Private Entrepreneurs and Politics in China

Private entrepreneurs did not constitute a major part of early economic

reforms in China. From 1978 up to 1988, the first form of private enterprises that was

allowed, so-called getihu, was restricted to have no more than eight employees.

During this period, private entrepreneurs basically played a somewhat limited role in

8

an experiment in which the Chinese government tried to come to grips with how

private businesses could function besides state-owned enterprises (SOEs). As a result,

early private entrepreneurs were only allowed to do business in sectors previously

ignored by larger SOEs. As they became increasingly important, private firms with

more than eight employees (siying qiye) were allowed in 1988. During the second half

of the 1980s, things seemed to progress fast. However, after the Tiananmen

demonstrations in 1989, private entrepreneurs experienced a negative setback in the

treatment they received from the government, after an event that most of them did not

take part in. The CCP imposed a formal ban stating that private entrepreneurs were

not allowed to be members in the party. Private entrepreneurs had been discriminated

against by the state and its different entities before, but after Tiananmen Incident, they

had to function in a more difficult business environment.

Albeit discriminatory practices were more or less the norm when dealing with

private enterprises, the private sector boomed during the 1990s. Deng Xiaoping’s

southern tour (nanxun) in 1992 also marked a change in the treatment of private

entrepreneurs. A wave of new economic reforms came to change the role

entrepreneurs played in the domestic economy. For example, the Chinese Company

Law was established in 1994, a first serious attempt to clarify the functions of both

state-owned and private enterprises. In the mid-1990s, the restructuring (gaizhi) of the

previously so important township and village enterprises (TVEs) had begun, a process

that soon increased in speed. Also, a major change in how the Chinese regime sees the

private sector was introduced in 1999, when it was stated that “individual, private and

9

other non-public economies that exist within the limits prescribed by law are major

components of the socialist market economy” (Tsai, 2006). In 2001, the former

Chinese leader Jiang Zemin declared that private entrepreneurs should be allowed to

join the CCP. This was reiterated formally during the 16th Party Congress the

following year, showing how important the private sector had become for the country.

In 2005, there were approximately 30 million registered private companies in China.

The same year, they accounted for approximately half of China’s total GDP (Tsai,

2007). Dougherty et al. (2007) find that the private sector increased in importance at

the turn of the century. In their study based on a data sample comprised by

approximately 250,000 companies, it is shown that private firms share of total

industrial product increased from 25% in 1998 to over 50% in 2003. It was this

change that Jiang Zemin acknowledged: private firms with their much higher average

productivity compared to SOEs continued to fuel the Chinese economy.

Regardless of the increasing acceptance of private entrepreneurs, they have

been significantly discriminated against for a long period of time. Entrepreneurs that

tried to build up their business during the early period of the economic reforms had to

rely on creative solutions to overcome such discrimination. For example, a large

number of private enterprises called “red-hat” (dai hongmaozi) firms registered as

publicly-owned firms as a way to disguise their true ownership (Tsai, 2007). It comes

as no surprise then that many private entrepreneurs have chosen to become politically

active at least partly to ensure better treatment by local and state officials.

Entrepreneurs that become members of the CCP are often called “red capitalists”

10

(Dickson, 2003). In this study, however, we focus on entrepreneurs that not only

become passive members of the CCP, but also choose to participate in politics at the

local or national level. It should be noted that while the number of politically active

private entrepreneurs is growing fast, it does not necessarily mean that all of them

constitute private entrepreneurs that decide to become members of the CCP or

become more politically active. For example, if we were to define a politically active

private entrepreneur as a person that is also a member of the CCP, then most such

individuals were members of the party before they became entrepreneurs (Dickson,

2008). After the decision to formally accept private entrepreneurs to become party

members in 2002, people inside the CCP quickly became active in a plethora of

private business ventures. This move, often called to “jump into the sea” (xia hai), has

spurred the private sector to grow even faster. While members of this group of private

entrepreneurs are interesting in their own right, this study focuses exclusively on the

private entrepreneurs that choose to become politically active after having gained

control of a company.

3.2 Defining Political Participation

As mentioned earlier, this study focuses on entrepreneurs that enter into

politics while already controlling a publically traded company. Political participation

is identified for either the private entrepreneur or one of his or her family members.

Following the related literature (e.g. La Porta et al., 1999), we identify shareholders

who control more than 10% of the outstanding shares. Thus, for a company to be

11

defined as a firm controlled by a private entrepreneur, the entrepreneur or his or her

family control at least 10% of the its outstanding shares. We then use representation at

one of three key state entities as a proxy for political participation. The three entities

are: the Congress of the Chinese Communist Party (CCCP), the National People’s

Congress (NPC), and the Chinese People’s Political Consultative Conference

(CPPCC). We also include participation at the provincial level of any of the three

entities. Wright (2010) states that private entrepreneurs have shown considerable

interest in joining these state entities and we therefore believe that a position in one of

them constitutes a strong indication of political participation.1

The CCCP functions as the highest body within the Communist Party of China

(CCP). The congress is held only once every five years. The NPC functions as the

country’s legislative body and is formally the highest organ of the state. Finally, the

CPPCC functions as a political advisory body and it consists of members from

different parties and organizations as well as individuals.

While the CCCP is the only entity that is directly organized by the CCP, both

the NPC and the CPPCC are close to the party. The CPPCC has been used as a way

for the CCP to attract non-CCP members and increase the support of the party.

Shambaugh (2009) also argues that the CPPCC is becoming more systematically

involved in the party’s policymaking process. Members of both the NPC and the

1 See also Chen and Dickson (2010) for a detailed discussion on entrepreneurs’ participation in these

state entities.

12

CPPCC on different levels are approved by the CCP, which indicates the party’s

influence on these entities. It is widely recognized that the inclusion of private

entrepreneurs into the NPC and CPPCC is a way for the CCP to co-opt this

increasingly important class. At the same time, an entrepreneur’s decision to join one

of the state entities in question is more than likely at least partially based on the fact

that he or she gets access to a powerful political network. It is thus logical to assume

that political participation could be used for the benefit of privately controlled firms.

3.3 Hypotheses

The literature on political connections shows that connected firms often are

able to exploit their rent-seeking opportunities. The final outcome of such behavior

depends on whether the effects of political ties are dominated by rent-seeking or the

grabbing hand phenomenon. For example, Fan et al. (2007) show that listed SOEs in

China tend to be negatively affected by political connections, indicating that the

presence of politically connected people in management and on the board can be

detrimental to firm value. However, we are focusing on private entrepreneurs whom

have not been rewarded the position in their firm as a result of political connections.

We thus expect that the controlling entrepreneur’s decision to enter into politics has a

positive effect on firm value as well as operating performance. The following

hypotheses focus on the effects of political participation:

Hypothesis 1a: A privately controlled firm experiences a positive effect on operating performance when the controlling entrepreneur becomes politically active

13

Hypothesis 1b: A privately controlled firm experiences a positive effect on firm value when the controlling entrepreneur becomes politically active

While the effects of political ties is analyzed in the research literature, less effort has

gone into identifying and analyzing channels through which entrepreneurs are able to

exploit rent-seeking opportunities. We identify and test several such channels. First,

previous studies have shown that political networks can improve firms’ access to

capital. In China, most capital is channeled through the banking system, controlled by

the state. For example, Fan et al. (2008) find a significant decline in leverage and debt

maturity ratios for firms connected to corrupted bureaucrats after corruption scandals

involving the bureaucrats become published. Political participation can thus result in

preferential access to debt financing.

Hypothesis 2a: A privately controlled firm experiences a positive effect on debt financing when the controlling entrepreneur becomes politically active Hypothesis 2b: A privately controlled firm experiences a positive effect on debt maturity when the controlling entrepreneur becomes politically active

Second, close ties to politicians may facilitate preferential tax treatments. If this is the

case, we can expect the tax level to be negatively affected when the entrepreneur that

controls the company participates in politics.

Hypothesis 3: A privately controlled firm experiences a decrease in its tax burden when the controlling entrepreneur becomes politically active

14

Third, political participation may result in political ties that provide better access to

corporate deals in the form of M&As. One potential effect of political participation is

thus that politically active entrepreneurs may obtain better access to certain regulated

industries. There are a number of industries that are heavily regulated in China,

including the energy, natural resources, and finance sectors. We can thus raise the

following hypothesis:

Hypothesis 4: Political participation by a the controlling entrepreneur has a positive effect on a firm’s ability to enter regulated industries through M&A deals

4 Data and Initial Empirical Analysis

4.1 Data and Sample Description

Our data set is comprised of all privately controlled listed firms on the

Shanghai and Shenzhen stock exchanges from 1993 to 2009. Firms with a private

citizen controlling at least 10% of the company are defined as privately controlled

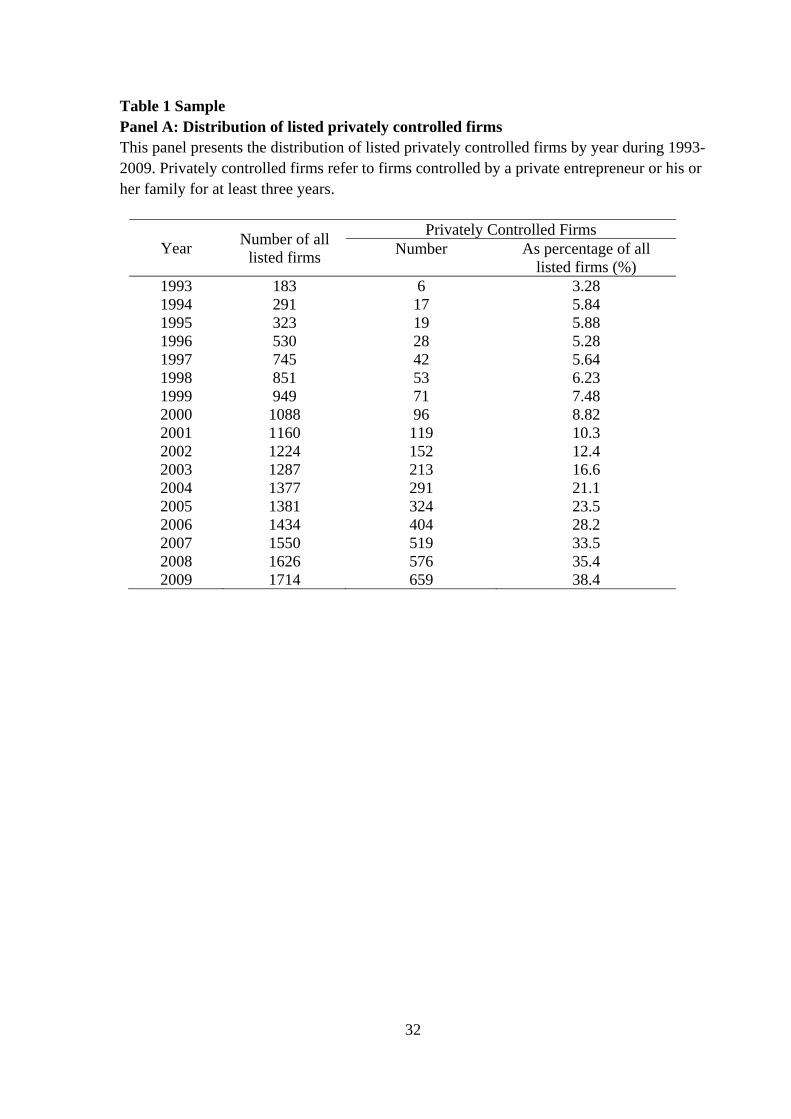

firms. Panel A in Table 1 shows the total number of listed firms and the number of

privately controlled firms for each year during the sample period. The number of

firms controlled by private entrepreneurs is very modest during the 1990s, never

reaching above 10% of the total number of listed firms. During the following decade,

however, the ratio of privately controlled firms to the total number of listed firms

increases fast. In 1993, the total number of listed firms was 183, of which only six

15

were controlled by private entrepreneurs. In 2009, the total of listed firms had

increased to 1714, with no less than 659 firms that can be defined as firms controlled

by private entrepreneurs. This means that the ratio of firms controlled by private

entrepreneurs to the total number of listed firms increased from a mere 3.28% to an

impressive 38.4% over the sample period. This change mirrors the overall

development in the Chinese economy, in which privately controlled firms constitute

an increasingly important part, especially during the last decade.

Next, we look at political participation by identifying when the controlling

private entrepreneur or one of his or her family members becomes politically active

(i.e. a member of the CCCP, the CPPCC, or the NPC). Panel B in Table 1 presents the

distribution of private entrepreneurs that become active in any of the main political

entities listed above. As expected, none of the private entrepreneurs participated in

politics during the most of the 1990s. Four of them became politically active during

the last years of that decade comprising no more than approximately 2% of the total

number of listed privately controlled firms in China. After the official recognition of

the importance of the private sector and the formal acceptance of private

entrepreneurs into the CCP in 2001 and 2002, the number of private entrepreneurs

that controlled a listed firm increased quickly. In 2009, a total of 73 privately

controlled firms had access to a political network through the political participation of

the controlling entrepreneur or one of his or her family members. This constituted

11.1% of the total number of privately controlled firms, indicating that not only were

private entrepreneurs allowed to enter into politics, they themselves clearly found it

16

attractive to do so. While approximately 11% of the number of privately controlled

firms is substantial, it is clear that the Chinese government has a process of its own to

select which private entrepreneurs that are allowed to take higher-level political

positions. This selection procedure can be seen as contributing to the rent-seeking

process.

4.2 Political Participation and Firm Value

To analyze the effects of political participation, we analyze stock performance

around the time when the political participation of private entrepreneurs that control

listed firms begins. In order to be compare stock performance of our sample firms

with regular firms controlled by private entrepreneurs, we first identify matching

firms. Matching firms are selected based on size (in terms of sales) and industry in the

year of political participation. Table 2 reports univariate tests for stock performance in

both the sample with companies controlled by private entrepreneurs that entered into

politics (the research sample) and the matching sample. We use cumulative abnormal

market-adjusted stock returns (CARs) to analyze the effects of political participation.

The CARs are based on monthly returns and are calculated using returns from three

months prior to the controlling private entrepreneur enters into politics up to 12 and

24 months after the event, respectively. Market returns used to calculate the CARs are

the equally-weighted monthly returns including dividends of all stocks on the

Shanghai and Shenzhen stock exchanges. Panel A in Table 2 presents the mean and

median CARs for the two groups. The average 12- and 24-month CARs for the

17

matching sample are 6.1% and 8.4%, while the CARs for the sample composed of

firms controlled by private entrepreneurs that enter into politics have a much higher

average mean of 13.6% and 27.3%, respectively. The difference is significant for both

time lengths. These results show that firms controlled by private entrepreneurs that

decide to become politically active outperform their peers with an average of 7.5%

over a 12-month period and 18.9% over 24 months. The results also indicate that the

difference between the two samples seem to increase over time, which means that the

advantages of developing an extensive political network through political

participation is not a one-time effect, but rather something that benefits the firm over

a long period of time. To shed more light on the long-term effects of political

participation, we calculate CARs for every month up to two years after the event.

Figure 1 shows how CARs for the two sample groups develop over time. It is evident

that the benefits of political participation by the controlling private entrepreneur are

highly beneficial for the firm and that the positive effects are persistent.

To control for other variables that may influence our results, we again estimate

OLS regressions, this time using the 12- and 24-month CARs as dependent variables.

We include the same variables as when analyzing operating performance, i.e. Tobin’s

Q, leverage, size, and industry and year dummies. Panel B in Table 2 reports the

regression results. Even when taking additional influential factors into account,

political participation still has a significant and positive effect on long-run stock

performance, especially over longer periods, as indicated by size and significance of

political participation when the 24-month CAR is the dependent variable. We can

18

therefore conclude that political participation by controlling private entrepreneur has a

significant positive effect not only on operating performance, but also firm value.

These initial results support those of earlier studies on how firms may benefit from

strong connections with leading politicians (e.g. Fisman, 2001; Faccio, 2006; and

Ferguson and Voth, 2008). Having established that political participation is closely

related to increases in firm performance, next we focus on potential channels firms

controlled by entrepreneurs that enter into politics may exploit for additional rent

seeking.

4.3 Political Participation and Operating Performance

To further analyze the effects of political participation, we compare changes in

operating performance based on when the political participation of private

entrepreneurs that control listed firms begins. We focus on six different measures of

accounting-based operating performance. First, we define growth in assets, sales, and

earnings as the growth of average of each measure during three years before the

entrepreneur becomes politically active to the average of the year of the entrepreneur

entering into politics and the year after. Second, we define change in return on sales

(ROS), return on assets (ROA), and return on earnings (ROE) as the difference

between the average of each measure during three years before the entrepreneur

becomes politically active and the average of the year that the entrepreneur enters into

politics and the year after. Before moving on to the regression analysis, we perform

tests for differences in the mean and median of the two groups for all six operating

19

performance measures. Panel A in Table 3 presents the descriptive statistics and the

results of univariate tests for the different operating performance measures. All

variables are winsorized at top and bottom 5%. Both the mean and median of all six

measures are significantly higher for firms with controlling private entrepreneurs that

enter into politics. These initial results show that firms controlled by private

entrepreneurs that enter into politics experience a significant positive effect of their

new political network.

To control for a number of factors that have been shown to influence operating

performance in later regressions, we also include three additional variables that are

commonly used in the literature on operating performance: Tobin’s Q, measured as

the sum of total market value of equity and total net liabilities divided by total assets;

leverage, measured as the ratio of total liabilities over total assets; and size, measured

as the natural logarithm of total assets. We again test for differences in mean and

median between the group of politically entrepreneurs and the matching group. Both

the mean and median of Tobin’s Q is significantly larger for firms with politically

active entrepreneurs, indicating their greater growth potential. Similarly, politically

active entrepreneurs have significantly higher leverage, even though the difference in

the mean is only significant at the 10% level. While we revisit this topic in a later

section, it is worth noting that firms controlled by politically private entrepreneurs

have higher debt levels than other entrepreneurial firms. Finally, the mean and median

of firm size in the two groups are indistinguishable. This shows that the matching

20

sample mirrors that of our sample of firms controlled by private entrepreneurs that

enter into politics during the sample period.

To control for other variables that may influence our results, we estimate

ordinary least squares (OLS) regressions using each of the six measures of operating

performance as dependent variables. Panel B in Table 3 presents the results of the six

OLS regressions with political participation, Tobin’s Q, leverage, size, and industry

and year dummies as independent variables. The regression results show that firms

controlled by private entrepreneurs that enter into politics experience an improved

operating performance, regardless of whether or not the change in performance is

measured by growth in assets, sales or earnings, or the change in ROS, ROA, or ROE.

These results are consistent with the initial univariate results in Panel A and show that

political participation by the controlling entrepreneur results in a positive effect on a

firm’s operating performance.

5 Identifying Rent-Seeking Channels

5.1 Access to Debt Financing and Debt Maturity

We begin our analysis of potential rent-seeking channels by looking at debt

structure and debt maturity. Our hypothesis is that political participation results in

better access to debt financing with resulting changes in debt structure and debt

maturity. To do this, we look at two separate variables. For debt financing, we analyze

the change in total debt over total assets and the total debt plus accounts payable over

21

total assets. To examine how firms use their newly found political networks to change

their debt composition, we focus on the change in long-term debt over total debt and

the long-term debt over total debt plus accounts payable.

Panel A in Table 4 provides a description of the sample based on the debt-

related variables. The changes in debt financing indicate that firms controlled by

private entrepreneurs that become politically active experience a significant positive

change in the debt ratio. Total debt over total assets as well as total debt plus accounts

payable over total assets are larger in both the mean and median for the group of firms

with politically active entrepreneurs. This means that after the controlling

entrepreneurs enter into politics, their firms are able to increase their leverage more

than normal firms controlled by private entrepreneurs. Focusing on the changes in

debt maturity, it is evident that political participation increases long-term debt as

share of total debt plus accounts payable. These results support earlier studies that

find evidence of higher leverage ratios and better access to long-term debt for

politically connected firms (e.g. Johnson and Mitton, 2003, and Faccio et al., 2006).

Next, we perform regressions to examine whether the financing policies of the

firms in the research sample change after the controlling entrepreneur engages in

political participation. We control for a number of additional factors that are known to

affect financial leverage and debt maturity. In addition to the three controls we used

previously, we also include profitability, measured as earnings over total assets, and

collateral, measured as the ratio of net fixed assets over total assets. Finally, we again

include industry and year dummies. Panel B in Table 4 reports the regression results

22

with each of the four debt measures as dependent variable. Column 1 presents the

regression results with the leverage variable as the dependent variable. Both total debt

over total assets and total debt plus accounts payable over total assets are affected by

political participation and the effect is positive and significant, indicating that firms

with access to comprehensive political networks as a result of their controlling

entrepreneur becoming politically active experience a significant increase in leverage.

Looking instead at the changes in debt maturity, political participation has a

somewhat weaker effect. However, the effect is still positive and significant at the

10% level for change in long-term debt over total debt plus accounts payable. Long-

term debt is thus positively related to political participation, indicating that firms

controlled by private entrepreneurs that enter into politics are able to shift to longer-

term debt. The results show that the changes in leverage and debt maturity cannot be

explained away by changes in other corporate fundamentals or industry and year

effects. Overall, the findings in Table 4 demonstrate how debt financing behavior

changes as private entrepreneurs that controls listed firms in China decide to enter

into politics.

5.2 Tax Burden

To analyze the changes in taxes after an entrepreneur engages in political

participation, we focus on the effective tax rates (ETR). ETR is defined as the tax

expense minus deferred tax expense divided by earnings before interest and tax

(EBIT). For completeness, we also use two alternative ETR measures. For the first

23

alternative measure (ETR1), we divide tax expenses only with EBIT. For the second

alternative measure (ETR2), we divide the difference between tax expenses and

deferred tax expenses with total profit. Then, to analyze the effect of political

participation, we calculate the change in tax burden as the difference between the

average annual ETR during the year of the event and the year after event and the

average annual ETR for the three years before the event. We also include several

control variables commonly seen in the literature on tax rates: capital intensity,

defined as the net fixed assets over total assets, and inventory intensity, defined as

inventory over total assets. We also use profitability, defined the same as before.

Panel A in Table 5 reports the mean and median values of change in the three

different tax burden measures. Initial tests for difference in mean and median show

that firms with entrepreneurs that enter into politics exhibit a significant reduction in

tax burden. While the mean of ERT is slightly positive for firms controlled by

politically active entrepreneurs, its median is negative. The mean and median is

negative for both ERT1 and ERT2 for firms controlled by entrepreneurs that become

politically active. For the matching sample, only the change in ERT1 is negative.

When testing for differences in mean and median, the negative effect is significantly

stronger for the research sample, indicating that political participation enables firms to

lower their tax burden relative to similar firms in the matching sample.

Panel B in Table 5 reports the results of the different regressions with each of

the three tax burden measures as dependent variables. The independent variable of

interest is again political participation. The coefficient for political participation is

24

negative and significant for each of the three tax burden measures. To conclude, even

when controlling for various alternative factors that may influence the dependent

variables, our results show that political participation by the controlling private

entrepreneur eases tax burden.

5.3 Access to Regulated Industries through M&A Deals

We have established that political participation has a positive impact on

operating performance and firm value and that some of this effect goes through debt

and tax burden channels. Next, we study how political participation affects privately

controlled firms’ access to beneficial corporate deals, either through mergers or

acquisitions. To analyze the effects of such deals, we identify M&A deals by firms

controlled by politically active private entrepreneurs. As before, we match these firms

with corresponding firms controlled by private entrepreneurs who have not entered

into politics through any of the three state entities we use as proxies for political

participation. We then carry out a regression analysis that focuses on access to

regulated industries in China.

The first two panels in Table 6 present descriptive statistics focusing on M&A

deals for both sample groups. Panel A reports the firm characteristics. Approximately

39% of the total number of deals was carried out by firms controlled by entrepreneurs

that are politically active. The standard control variables are also included: Tobin’s Q,

leverage, and size. The characteristics of the M&A transactions are reported in Panel

B. We measure type of M&A with a dummy variable that is equal to 1 when the

25

transaction is based on equity purchase and 0 otherwise. The variable M&A size is

measured as the ratio of the transaction value to the size of the buyer. We also include

the dummy variable regulated industry which is equal to 1 if the target firm is active

in one of China’s regulated industries and 0 otherwise. A majority of the M&A

transactions are based on stock purchases. The average size of the target company

relative to the buyer is relatively modest at 7.7%. Finally, only a minority of the total

number of transactions involves deals in regulated industries, mirroring the fact that it

is difficult for privately controlled firms to enter certain sectors of the Chinese

economy.

To analyze the influence that political participation may have on gaining

access to regulated industries, we perform a logistic regression with the dummy

variable regulated industry as dependent variable. Besides political participation, we

include our standard control variables as well as industry and year dummies. Panel C

in Table 6 reports the results of the logistic regression. The coefficient for regulated

industry is highly significant and positive. We can therefore conclude that a firm that

is controlled by a private entrepreneur that has entered into politics is more likely to

carry out an M&A transaction in a regulated industry. This means that political

participation by private entrepreneurs in China can be used to gain access into

industries that are heavily regulated and often closed to the private sector.

26

6 Conclusion

This paper examines the effects when Chinese private entrepreneurs enter into

politics. We firsts identify all listed firms that are controlled by entrepreneurs and then

analyze the effects of the event of initial political participation. The event is thus

defined as the controlling private entrepreneur entering into politics through one of

three important Chinese state entities. Consistent with the literature on rent seeking

and political connections, we find that political participation has a positive effect on

operating performance and firm value. This indicates that private entrepreneurs are

able to exploit their newly developed political networks for rent seeking.

We then examine several potentially important channels for rent seeking. First,

we find that firms controlled by private entrepreneurs that enter into politics are able

to increase their leverage after the event. We also find that political participation has a

positive effect on long-term debt relative to total debt. These results indicate that

political participation results in advantages when it comes to access to debt financing

and thus affect capital structure choices. Our findings on the effect of political

participation on debt financing thus support recent research findings suggesting that

financing patterns are affected not only by factors at the firm or industry level, but

also on the country level (e.g. Rajan and Zingales, 1995; Demigurc-Kunt and

Maksimovic, 1996, 1998, 1999; Booth et al., 2001).

Second, we look at several alternative measures of tax burden. Our findings

show that political participation results in a negative effect on efficient tax rates

(ETRs). This indicates that private entrepreneurs in China are able to exploit the

27

networks they build up through political participation to lower the tax burden of their

companies. Third, we analyze how firms’ corporate deals are affected by political

participation. We find that political participation significantly increases the likelihood

of corporate deals in China’s regulated industries. This means that private

entrepreneurs are able to access certain industries by entering into politics.

Our paper makes important contributions to the literature on political

connections and rent seeking. First, we document how China’s private entrepreneurs

can choose to become a member of any of the major political entities and thereby

improve their firms’ value and performance through rent seeking. Second, and more

importantly, we identify several important rent-seeking channels that private

entrepreneurs are able to exploit through their political participation, including better

access to debt financing, reductions in tax burden, and better access to heavily

regulated industries in China. Our results should be useful when trying to understand

problems in other emerging markets with similar institutional features.

28

References

Benmelech, E., Moskowitz, T., 2010. The political economy of financial regulation:

Evidence from U.S. state usury laws in the 19th Century. Journal of Finance,

forthcoming.

Booth, L., Aivazian, V., Demirguc-Kunt, A., Maksimovic, V., 2001. Capital

structures in developing countries. Journal of Finance 56, 87–130.

Charumilind, C., Kali, R., Wiwattanakantang, Y., 2006. Connected lending: Thailand

before the financial crisis. Journal of Business 79, 181-218.

Chen, J., Dickson, B.J., 2010. Allies of the state: China’s private entrepreneurs and

democratic change. Cambridge, MA: Harvard University Press.

Claessens, S., Feijen, E., Laeven, L., 2008. Political connections and preferential

access to finance: The role of campaign contributions. Journal of Financial

Economics 88, 554-580.

Cooper, M.J., Gulen, H., Ovtchinnikov, A.V., 2010. Corporate political contributions

and stock returns. Journal of Finance 65, 687-724.

Demirguc-Kunt, A., Maksimovic, V., 1996. Stock market development and firm

financing choices. World Bank Economic Review 10, 341–369.

Demirguc-Kunt, A., Maksimovic, V., 1998. Law, finance and firm growth. Journal of

Finance 53, 2107–2137.

29

Demirguc-Kunt, A., Maksimovic, V., 1999. Institutions, financial markets, and firm

debt maturity. Journal of Financial Economics 54, 295–336.

Dickson, B.J., 2003. Red capitalists in China: The party, private entrepreneurs, and

prospects for political change. New York: Cambridge University Press.

Dickson, B.J., 2008. Wealth into power: The communist party’s embrace of China’s

private sector. New York: Cambridge University Press

Dinc, I.S., 2005. Politicians and banks: Political influence on government-owned

banks in emerging markets. Journal of Financial Economics 77, 453-479.

Dougherty, S., Herd, R., He, P., 2007. Has a private sector emerged in China’s

industry? Evidence from a quarter of a million Chinese firms. China Economic

Review 18, 309-334.

Faccio, M., 2006. Politically connected firms. American Economic Review 96, 369-

386.

Faccio, M., Masulis, R.W., McConnell, J.J., 2006. Political connections and corporate

bailouts. Journal of Finance 61, 2597-2635.

Fan, J.P.H., Rui, O.M., Zhao, M., 2008. Public governance and corporate finance:

Evidence from corruption evidence. Journal of Comparative Economics 36, 343-364.

Fan, J.P.H., Wong, T.J., Zhang, T., 2007. Politically connected CEOs, corporate

governance, and post-IPO performance of China’s newly partially privatized firms.

Journal of Financial Economics 84, 330-357.

30

Ferguson, T., Voth, H.-J., 2008. Betting on Hitler – The value of political connections

in Nazi Germany. Quarterly Journal of Economics 123, 101-137.

Fisman, R., 2001. Estimating the value of political connections. American Economic

Review 91, 1095-1102.

Goldman, E., Rocholl, J., So, J., 2009. Do politically connected boards affect firm

value? Review of Financial Studies 22, 2331-2360.

Jayachandran, S., 2006. The Jeffords effect. Journal of Law and Economics 49, 397-

425.

Johnson, S., Mitton, T., 2003. Cronyism and Capital Controls: Evidence from

Malaysia. Journal of Financial Economics 67, 351-382.

Khwaja, A., Mian, A., 2005. Do lenders favor politically connected firms? Rent

provision in an emerging financial market. Quarterly Journal of Economics 120,

1371-1411.

Knight, B., 2006. Are policy platforms capitalized into equity prices? Evidence from

the Bush/Gore 2000 presidential election. Journal of Public Economics 90, 751-773.

Kroszner, R. S., Stratmann, T.E., 1998. Interest-group competition and the

organization of Congress: Theory and evidence from financial services’ political

action committees. American Economic Review 88, 1163-1187.

Krueger, A., 1974. The political economy of the rent-seeking society. American

Economic Review 64, 291-303.

31

La Porta, R., Lopez-de-Silanes, F., Shleifer, A., 1999. Corporate ownership around

the world. Journal of Finance 54, 471-518.

La Porta, R., Lopez-de-Silanes, F., Shleifer, A., Vishny, R., 2002. Investor protection

and corporate valuation. Journal of Finance 57, 1147-1170.

Rajan, R., Zingales, L., 1995. What do we know about capital structure? Some

evidence from international data. Journal of Finance 50, 1421–1460.

Rajan, R., Zingales, L., 2003. The Great Reversals: The politics of financial

development in the 20th century. Journal of Financial Economics 69, 5-50.

Roberts, B., 1990. A dead senator tells no lies: Seniority and the distribution of

Federal benefits. American Journal of Political Science 34, 31-58.

Shambaugh, D., 2009. China’s Communist Party: Atrophy and adaptation. Berkeley,

CA: The University of California Press.

Tsai, K.S., 2006. Adaptive informal institutions and endogenous change in China.

World Politics 59, 116-141.

Tsai, K.S., 2007. Capitalism without democracy: The private sector in contemporary

China. Ithaca, NY: Cornell University Press.

Wright, T., 2010. Accepting authoritarianism: State-society relations in China’s

reform era. Stanford, CA: Stanford University Press.

32

Table 1 Sample Panel A: Distribution of listed privately controlled firms This panel presents the distribution of listed privately controlled firms by year during 1993-2009. Privately controlled firms refer to firms controlled by a private entrepreneur or his or her family for at least three years.

Year Number of all

listed firms

Privately Controlled Firms Number As percentage of all

listed firms (%) 1993 183 6 3.28 1994 291 17 5.84 1995 323 19 5.88 1996 530 28 5.28 1997 745 42 5.64 1998 851 53 6.23 1999 949 71 7.48 2000 1088 96 8.82 2001 1160 119 10.3 2002 1224 152 12.4 2003 1287 213 16.6 2004 1377 291 21.1 2005 1381 324 23.5 2006 1434 404 28.2 2007 1550 519 33.5 2008 1626 576 35.4 2009 1714 659 38.4

33

Table 1 Sample (Continued) Panel B: Distribution of firms controlled by entrepreneurs that participate in politics This panel presents the distribution of firms that are controlled by politically active private entrepreneurs, which means that the entrepreneur (or one of his or her family members) is a member of the National People’s Congress (NPC), the Chinese People’s Political Consultative Conference (CPPCC), or the Congress of Chinese Communist Party (CCCP).

Year Number of entrepreneurial

firms

Firms controlled by politically active entrepreneurs

Numbers As percentage of all entrepreneurial firms (%)

1993 6 0 0.00 1994 17 0 0.00 1995 19 0 0.00 1996 28 0 0.00 1997 42 0 0.00 1998 53 2 3.77 1999 71 0 0.00 2000 96 0 0.00 2001 119 0 0.00 2002 152 1 0.66 2003 213 27 12.68 2004 291 0 0.00 2005 324 0 0.00 2006 404 0 0.00 2007 519 1 0.19 2008 576 42 7.29 2009 659 0 0.00 Total 3589 73 2.03

34

Table 2 Political Participation and Stock Performance Panel A: Univariate Tests This table presents univariate tests for stock performance in a window of [-3,12] and [-3,24] around the month of the beginning of political participation. The stock performance measures are calculated as the monthly cumulative abnormal returns (CARs), where the abnormal return is the market adjusted return. ***, **, and * denote significance at 1%, 5%, and 10%, respectively.

(1) CAR [-3 ,12]

Mean (Median)

(2) CAR [-3 ,24]

Mean (Median)

Research Sample 0.136 (0.157)

0.273 (0.335)

Matching Sample 0.061 (-0.033)

0.084 (0.058)

Difference 0.075* (0.156)*

0.189*** (0.335)***

T-test (Wilcoxon-Mann-Whitney Test)

1.65 (1.92)

2.67 (2.85)

N 73 73

35

Table 2 Political Participation and Stock Performance (Continued) Panel B: Multivariate analysis This table presents the OLS regression results of the effect of political participation on stock performance. The dependent variables are the cumulative abnormal returns (CARs), measured as cumulated monthly market-adjusted return in a window of [-3, 12] and [-3,24], respectively, where the month when the controlling entrepreneur becomes politically active is treated as 0. The independent variables include Political Network, which equals one for the year of and one year after the entrepreneur enters into politics and zero otherwise; Tobin’s Q, measured as the sum of total market value and total net liabilities divided by total assets; Leverage, measured as the ratio of total liabilities over total assets; Size, measured as the natural logarithm of total assets. Industry dummy and year dummy are also included but not reported. All variables are winsorized at top and bottom 5%. Robust t-statistics are given in parentheses. ***, **, and * denote significance at the 1%, 5% and 10% level, respectively.

(1) (2) CAR[-3, 12] CAR[-3, 24] Political Participation 0.050*

(1.76) 0.161** (2.25)

Tobin’s Q 0.027* (1.75)

0.055** (2.51)

Leverage 0.118 (0.65)

0.129 (0.59)

Size 0.051 (1.23)

0.103* (1.70)

Intercept -1.142 (-1.05)

-2.172* (-1.76)

Industry Yes Yes Year Yes Yes Observations 146 146 Adjusted R2 0.063 0.078

36

Table 3 Political Participation and Operating Performance Panel A: Descriptive Statistics and Univariate Tests This table presents the descriptive statistics for both the research and matching sample and univariate tests for differences in means and medians. The research sample is composed of private firms controlled by politically active private entrepreneurs. A matching firm is a firm of similar size, measured with total sales, in the same industry as the firm in the research sample. The growth in assets (sales, earnings, or operating earnings) are the growth rates of assets (sales, earnings, or operating earnings) from the average annual assets (sales, earnings or operating earnings) from the period of three years before to the average during the period of the year of the vent and the year after the controlling entrepreneur becomes politically active. ROS (ROA or ROE) is the difference between the average annual ROS (ROA or ROE) during the period of the year of the event and one year after it and the period of three years before the controlling entrepreneur enters into politics. Tobin’s Q is measured by the sum of total market value and total net liabilities divided by total assets. Leverage is the ratio of total liabilities over total assets. Size is the natural logarithm of total assets. All variables are winsorized at top and bottom 5%. *** ,** and * denote significance for the difference between the research sample and matching sample at 1%, 5%, and 10% respectively.

Research Sample Matching Sample N Mean Median Std. Dev. Mean Median Std. Dev. Growth in assets 73 0.362*** 0.325*** 0.30 0.158 -0.181 0.41 Growth in sales 73 0.413*** 0.378*** 0.40 0.233 -0.22 0.57 Growth in earnings 73 0.352** 0.287*** 10.92 -4.892 (-0.278) 22.15 Change in ROS 73 -0.006*** -0.007* 0.10 -0.074 (-0.028) 0.21 Change in ROA 73 -0.003* -0.001* 0.04 -0.019 (-0.014) 0.07 Change ROE 73 0.050*** -0.006** 0.25 -0.019 (-0.014) 0.35 Tobin’s Q 73 1.855*** 1.617** 0.873 1.550 1.373 0.489 Leverage 73 0.461* 0.455** 0.167 0.508 0.516 0.168 Size 73 20.965 20.993 0.735 21.027 21.023 0.661

37

Table 3 Political Participation and Operating Performance (Continued) Panel B: Regression Analysis This table presents the OLS regression results of the effect of political participation on operating performance. The dependent variables are the change in different debt financing structures and debt maturities. The independent variables include Political Participation, which equals one if the firm is controlled by an entrepreneur that enters into politics and zero otherwise; Tobin’s Q, measured as the sum of total market value and total net liabilities divided by total assets; Leverage, measured as the ratio of total liabilities over total assets; Size, measured as natural logarithm of total assets. Industry dummy and year dummy are also included but not reported. All variables are winsorized at top and bottom 5%. Robust t-statistics are given in parentheses. ***, **, and * denote significance at the 1%, 5% and 10% level, respectively.

(1) (2) (3) (4) (5) (6) Growth in

assets Growth in

sales Growth in Earnings

Change in ROS

Change in ROA

Change in ROE

Political Participation

0.171*** (3.73)

0.164** (2.53)

5.235** (2.08)

0.067***

(2.68)

0.015* (1.83)

0.128*** (3.08)

Tobin’s Q 0.125*** (3.36)

0.126** (2.33)

3.538* (1.69)

0.018 (0.89)

0.012* (1.71)

0.027 (0.78)

Leverage -0.169 (-1.23)

0.248 (1.25)

22.628*** (2.94)

0.077 (1.02)

0.053** (2.14)

0.212* (1.67)

Size 0.200*** (5.44)

0.172*** (3.22)

-0.113 (-0.05)

0.013 (0.64)

0.010 (1.43)

-0.026 (-0.77)

Intercept -4.159*** (-5.18)

-3.705*** (-3.18)

-19.524 (-0.43)

-0.419 (-0.94)

-0.268* (-1.82)

0.327 (0.44)

Industry Yes Yes Yes Yes Yes Yes Year Yes Yes Yes Yes Yes Yes Observations 146 146 146 146 146 146 Adjusted R2 0.254 0.129 0.068 0.037 0.047 0.065

38

Table 4 Political Participation and Changes in Debt Financing Structure and Debt Maturity Panel A: Descriptive Statistics This table presents the descriptive statistics of debt financing structure change and debt maturity change for both research and matching sample. The research sample is composed of private firms controlled by politically active private entrepreneurs. The matching firm is the one with similar size, measured as sales, in the same industry as that for firms obtaining political network. The Change in debt financing structure(or debt maturity) are the difference between the average annual debt financing structure(or debt maturity) variables in the period of year and one year after obtaining political network and the period of three years before obtaining political network. Debt financing structure is measured as total debt divided by total assets, or total debt plus accounts payable divided by total assets, Debt Maturity is measured as long-term debt divided by total debt, or long-term debt divided by total debt plus accounts payable. All variables are winsorized at top and bottom 5%. *** ,** and * denote significance for the difference between the research sample and matching sample at 1%,5% and 10% respectively.

Research Sample Matching Sample N Mean Median Std. Dev. Mean Median Std. Dev.

Change in Total Debt/ Total Assets

69 0.037*** 0.029*** 0.077

-0.005 -0.014 0.078

Change in (Total Debt + Accounts Payable) /

Total Assets

69 0.038** 0.045*** 0.095

0.002 -0.002 0.075

Change in Long-Term Debt/ Total Debt

69 0.021 0.000 0.203

-0.010 0.000 0.186

Change in Long-Term Debt/

(Total Debt + Accounts Payable)

69 0.022** 0.000 0.127

-0.022 0.000 0.113

39

Table 4 Political Participation and Changes in Debt Financing Structure and Debt Maturity (Continued) Panel B: Regression Analysis This table presents the OLS regression results of the effect of political participation on changes in debt financing structure and debt maturity. The dependent variables are change in debt financing structure and debt maturity. The independent variables are: Political Participation, which equals one for the firms controlled by entrepreneurs that enter into politics and zero otherwise; Tobin’s Q, measured as the sum of total market value and total net liabilities divided by total assets; Leverage, measured as the ratio of total liabilities to total assets; Size, measured as the natural logarithm of total assets; Profitably, measured as the ratio of earnings to total assets; and Collateral, measured as the ratio of total net fixed assets to total assets. Industry and year dummies are included but not reported. All variables are winsorized at top and bottom 5%. Robust t-statistics are given in parentheses. ***, **, and * denote significance at the 1%, 5% and 10% level, respectively.

(1) (2) (3) (4) Change in

Total Debt/ Total Assets

Change in (Total Debt +

Accounts Payable) / Total Assets

Change in Long Term-Debt / Total

Assets

Change in Long Term-Debt/

(Total Debt + Accounts Payable)

Political Participation

0.0410*** (3.14)

0.032*** (2.71)

0.038 (0.93)

0.043* (1.71)

Tobin’s Q 0.020 (1.41)

0.028* (1.87)

0.012 (0.31)

0.011 (0.46)

Leverage -0.051 (-1.02)

-0.012 (-0.24)

0.081 (0.59)

-0.024 (-0.29)

Size 0.033* (2.57)

0.035** (2.59)

0.013 (0.40)

0.003 (0.13)

Profitability 0.051 (0.23)

0.048 (0.21)

0.242 (0.40)

0.088 (0.23)

Collateral 0.005 (0.08)

0.060 (0.94)

0.027 (0.17)

0.036 (0.35)

Intercept 0.759*** (2.69)

0.839*** (2.80)

-0.304 ( -0.39)

0.062 (0.13)

Industry Yes Yes Yes Yes Year Yes Yes Yes Yes Observations 138 138 138 138 Adjusted R2 0.210 0.232 0.091 0.109

40

Table 5 Political Participation and Tax Burden Change Panel A: Descriptive Statistics This table reports the descriptive statistics of tax burden change for both the research and matching sample. The research sample is composed of private firms controlled by politically active private entrepreneurs. A matching firm is one of similar size, measured as total sales, and in the same industry as the corresponding firm controlled by an entrepreneur that enters into politics. The change in tax burden is the difference between the average annual ETR (or ETR1/ETR2) in the period of year and one year after obtaining political network and the period of three years before obtaining political network. ETR is defined as (tax expense-deferred tax expense)/EBIT, ETR1 is defined as tax expense/EBIT, and ETR2 is defined as tax expense/total profit. Capital intensity is defined as fixed net assets/total assets. Inventory intensity is defined as inventory/total assets. Profitability is defined as earnings/total assets. All variables are winsorized at top and bottom 5%. *** ,**, and * denote significance for the difference between the research sample and matching sample at 1%, 5%, and 10%, respectively.

Research Sample Matching Sample N Mean Median Std. Dev. Mean Median Std. Dev. Change in ERT 73 0.001* -0.003** 0.104 0.014 0.028 0.121 Change in ERT1 73 -0.028* -0.023* 0.080 -0.013 -0.001 0.088 Change ERT2 73 -0.033** -0.028* 0.104 0.007 0.006 0.142 Capital intensity 73 0.263 0.232 0.141 0.256 0.227 0.151 Inventory intensity 73 0.153 0.120 0.119 0.174 0.130 0.129 Profitability 73 0.048 0.049 0.041 0.017 0.014 0.049

41

Table 5 Political Participation and Tax Burden Change (Continued) Panel B: Regression Analysis This table reports the OLS regression results of the effect of political participation on tax burden change. The dependent variables are tax burden change, proxied by the change in ETR, ETR1, and ETR2, respectively. The independent variables include Political Participation, which equals one for the firms controlled by entrepreneurs that enter into politics and zero otherwise; Tobin’s Q, measured as the sum of total market valuation of equities and total net liabilities divided by total assets; Leverage, measured as the ratio of total liabilities over total assets; Size, measured as natural logarithm of total assets; Capital intensity, defined as fixed net assets/total assets; Inventory intensity, defined as inventory/total assets; Profitability, defined as earnings/total assets. Industry and year dummies are included but not reported. All variables are winsorized at top and bottom 5%. *** ,**, and * denote significance at the 1%, 5%, and 10%, respectively.

(1) Change in ERT

(2) Change in ERT1

(3) Change in ERT2

Political Participation -0.008* (1.68)

-0.011* (1.91)

-0.035* (-1.94)

Tobin’s Q -0.021 (-0.65)

0.000 (0.78)

0.042 (1.13)

Leverage 0.151 (1.31)

0.069 (1.00)

0.416*** (3.10)

Size -0.038 (-1.38)

-0.010 (-0.59)

-0.002 (-1.32)

Capital intensity -0.032 (-0.24)

0.020 (0.25)

0.235 (1.52)

Inventory intensity -0.114 (-0.70)

0.153 (1.58)

0.248 (1.30)

Profitability -0.610 (-1.44)

0.229 (0.93)

-0.210 (-0.44)

Intercept 1.028 (0.95)

0.326 (0.90)

-0.073 (-0.10)

Industry Yes Yes Yes Year Yes Yes Yes Observations 146 146 146 Adjusted R2 0.084 0.014 0.087

42

Table 6 Political Participation and M&A Transactions This table presents descriptive statistics when entrepreneurial firms make M&As, including data from both the research and matching sample. A matching firm is a firm of similar size, measured as total sales, in the same industry as that of the corresponding firm controlled by an entrepreneur that becomes politically active. Panel A reports the characteristics of the entrepreneurial firms with the following variables: Political Participation, a dummy variable that equals one if the M&A transaction takes place during the year that the controlling entrepreneur enters into politics or the year after, and 0 otherwise; Tobin’s Q, measured as the sum of total market value and total net liabilities divided by total assets; Leverage, measured as the ratio of total liabilities to total assets; and Size, measured as the natural logarithm of total assets. Panel B reports the characteristics of the transactions. Type of M&A is a dummy variable that is equal to 1 when entrepreneurial firms purchase equities and 0 otherwise. M&A Size is the ratio of the transaction value to the size of the buyer. Regulated Industry is equal to 1 if the target is in a regulated industry and 0 otherwise. Panel C reports the effects of political participation on regulated industry entry during M&As transactions by entrepreneurial firms. The dependent variable is a regulated industry entry dummy that is equal to 1 if the acquired target functions in a regulated industry and 0 otherwise. Industry and year dummies are included but not reported. All variables are winsorized at top and bottom 5%. Robust t-statistics are given in parentheses. A logistic regression is applied and Wald Chi-Square statistics are given in parentheses. *** ,** ,and * denote significance at the 1%, 5%, and 10% level, respectively.

Mean Median Std. Dev. Min Max

Panel A: Characteristics of Entrepreneurial Firms Political Participation 0.386 0 0.488 0 1 Tobin’s Q 2.509 1.681 2.777 0.869 32.869 Leverage 0.526 0.514 0.178 0.008 1.608 Size 21.253 21.209 0.826 18.687 23.811 Panel B: Characteristics of M&A Transactions Type of M&A 0.795 1 0.405 0 1 M&A Size 0.077 0.023 0.172 0 1.455 Regulated Industry 0.216 0 0.413 0 1

43

Table 6 Political Participation and M&A Transactions (Continued) Panel C: Regression Results - Dependent Variable: Regulated Industry Entry

Political Participation 0.1873***

(9.806) Tobin’s Q 0.066

(1.360) Leverage 1.611*

(3.214) Size 0.551***

(6.852) Intercept -1.3787***

(9.806) Industry Yes Year Yes Observations 268 Likelihood Ratio 12.440

44

Figure 1 Average Monthly Cumulative Abnormal Returns (CARs) This figure presents the cumulative abnormal returns (CARs) for the research sample and the matching sample, respectively. The research sample is composed of firms controlled by entrepreneurs that enter into politics and date 0 is equal to the month when the entrepreneur becomes politically active. The matching sample is comprised by firms that match the research sample firms based on size, measured as total sales, and industry.